What is the policy now? Well, the Tax Cuts and Jobs Act (TCJA) of 2017 changed the treatment of R&E costs so that taxpayers must capitalize all R&E costs incurred after December 31, 2021, and amortize them over either a five-year period (domestic costs) or a 15-year period (foreign costs). Previously, taxpayers could either (1) immediately deduct R&E expenditures, or (2) elect to amortize those costs over a period of five or more years, which gave the taxpayer the ability to choose the option that would be the most beneficial for them.

While it is still possible for the legislative process to postpone or repeal mandatory capitalization of Section 174 costs (including retroactively applying any changes to the 2022 tax year), such legislation would need to have bipartisan support due to the currently divided Congress.

In this article, we review what it would mean for your business if the much-anticipated revisions to Section 174 do not occur, and what kind of planning you should do to prepare on the front end. A number of these recommendations will be further refined once additional IRS guidance is provided.

Background on 174 R&E expenditures

R&E expenses for income tax purposes are defined under Section 174 and its regulations. In Treasury Regulation Section 1.174-2(a), R&E expenditures are described as expenditures incurred by the taxpayer in connection with the taxpayer’s trade or business in the experimental or laboratory sense. Section 174(c)(3) – added by the TCJA – also notes that any amount paid or incurred in connection with the development of any software shall also be an R&E expenditure subject to capitalization. Generally, when determining R&E expenses, not only are direct costs of R&E factored in, but also the indirect costs incident to the development or improvement of a product.

Common expenses included in R&E costs under Section 174 are the following. Many of these expenses are considered for Section 174 specifically and are not qualified research expenses for purposes of the R&D credit.

- Attorneys’ fees in connection with filing and completing patent applications.

- Allowance for depreciation or depletion of property to the extent used in connection with R&E.

- Employee wages and employee benefits and costs in connection with R&E.

- Supplies, computer leasing, and contract research costs in connection with R&E.

- Pilot model expenditures.

- Facility expenditures in connection with R&E.

- Ordinary and extraordinary utilities in connection with R&E.

- Travel expenditures incident to R&E.

- Foreign research expenditures.

- Additional overhead expenditures incident to R&E.

*In addition to the above, there are other criteria used for determining what expenses qualify for the R&D credit that do not apply towards determining Section 174 costs.

In contrast, the following are common expenses that are excluded from the expansive definition of R&E costs under Section 174:

- the ordinary testing or inspection of materials or products for quality control;

- efficiency surveys;

- management studies;

- consumer surveys;

- advertising or promotions;

- acquisition of another’s patent, model, production or process;

- research in connection with literary, historical, or similar projects; and

- expenditures for the acquisition or improvement of land.

The current R&E amortization rule explained

The ability to deduct R&E costs changed for all tax years beginning after December 31, 2021. As previously mentioned, these costs can no longer be deducted in full and must be capitalized and then amortized over five years for domestic costs and over 15 years for foreign costs. This amortization starts at the midpoint of the first year that the expenses were incurred, which results in only 10% of domestic costs (1/2 of 20%) being able to be deducted in their first year.

Per IRS guidance, this mandatory change can be implemented as an automatic accounting method change through attaching a statement to a taxpayer’s first income tax return with a year beginning after 2021, in lieu of filing the much more intricate Form 3115. This change should not have an effect on prior tax years, since the automatic method change is implemented on a “cut-off basis.”

Macro effect of mandatory capitalization

As mentioned above, before the prior rule was changed, every R&E expense could be deducted in full in the year they were incurred. While it is expected that the Section 174 expensing rules will revert to this — to some extent — through pressure from persistent lobbyists, this change has not been incorporated into a bill yet.

Some believe the mandatory R&E capitalization and amortization will adversely affect U.S. innovation, potentially resulting in a detrimental impact on our global competitiveness and jobs. For more than 60 years, businesses were able to immediately deduct their R&D expenses in the year those expenses were incurred (or choose to defer based on what worked for them). Now, the amortization of new R&E costs could cost businesses billions in cash taxes.

Significant considerations

Estimated Tax Payments: For taxpayers making estimated tax payments utilizing current year taxable income, consideration should be given to R&E expenditures and how the capitalization of those expenditures may impact taxable income and timing of cash tax payments. A closer look at refining the various accounts in a taxpayer’s books may be needed for this.

Tax Accounting / ASC 740: Taxpayers should be mindful of whether a new deferred tax asset is created, if any adjustment of existing deferred taxes may be necessary, or if a full or partial valuation allowance may be needed.

Other Areas Affected: The amortization requirement also affects other areas of taxable income, including the following:

- increases the deductibility of business interest under Section 163(j),

- increases the deductibility of the QBI (Qualified Business Income) deduction,

- increases the amount of GILTI (global intangible low-taxed income) for controlled foreign corporations,

- potentially adjusts the amount of FDII (foreign derived intangible income) deduction that can be taken,

- changes the amount of R&E expenses allocable for purposes of the foreign tax credit, and

- impacts state taxable income for the few states that do not conform to the capitalization requirement (e.g., California).

R&D credit considerations

The Section 174 capitalization requirements should not directly impact the amount of expenses that can be used for the R&D Tax Credit under Section 41, since the research credit is calculated using a much smaller subset of R&E expenditures than Section 174 and is not limited by the capitalization requirement. As Section 174 is much broader in scope, it applies to expenditures both eligible and ineligible for the research credit.

Another consideration for tax planning is that the research credit will be even more important to assist with reducing the additional tax liability that will be generated by the R&E treatment change, since the credit can help offset some of the tax liability increase. Moreover, the analysis & processes used to determine the R&D credit can be leveraged to identify Section 174 R&E expenses, which helps create some efficiencies in quantifying the overall effect of the mandatory capitalization and amortization requirement.

Extend impacted returns where possible

Tax return extensions are highly recommended for tax returns that have their due dates coming up. Not only is there the pending IRS guidance that may significantly change R&E expense calculations, but also the act of extending tax returns should allow more time for tax returns to be superseded (rather than amended) and should allow for R&D credit claims to be made on originally filed returns.

This is echoed by a September 2021 Chief Counsel Memorandum issued by the IRS, which made the process for claiming a refund under the R&D credit far more stringent. The memorandum relayed that taxpayers must provide more information on business components, identify the research activities performed, and name the individuals who performed each research activity. Given the additional amount of detail needed, taxpayers making R&D credit claims on amended returns — especially small businesses — have a heavier burden than those who make the claim on an originally filed returns.

How will it affect you?

If the mandatory R&E capitalization requirement is not changed, you should consider how the 174 capitalization rules will affect your business and how claiming the R&D credit will help offset the increase in tax liability. If you currently have an R&D credit analysis and/or an ASC 730 financial statement analysis, those studies can be used as starting points to determine the overall effect of Section 174 — keeping in mind that neither analysis includes all the costs included in Section 174.

If the requirement is changed, there are several ways that the R&E expense landscape could turn out for taxpayers. Ideally, Congress will revert to the prior rule regarding R&D expenses. In that situation, you should be able to choose what is best for you — immediately deducting or deferring.

Our perspective

As experienced advisors, MGO can help model the best R&E position for you, through the 2022 tax year and beyond — potentially saving you significant amounts of money. Our holistic tax advisor and business advisor-first philosophy factors not only the direct effects of the R&E capitalization requirement, but also the impact on other areas of your tax returns (e.g., international, transfer pricing, state, and local tax) and what potential savings you can obtain by claiming the R&D credit. Please feel free to reach out to any of our R&E costing profesionals below to get the experienced insight that you deserve.

About the author

Danielle Bradley is a senior manager in MGO’s National Tax Credits and Incentives practice. She focuses on helping businesses identify, substantiate, and defend federal and state tax credits and incentives. She has helped hundreds of companies monetize and defend over $100 million in various tax credits and incentives, such as the Research and Development (R&D) Tax Credit, Orphan Drug Credit, Employee Retention Credit, meals and entertainment deduction, and the current Research and Experimental (R&E) amortization calculations. Danielle has extensive experience in various industries, including software and technology, life sciences, manufacturing, aerospace and defense, and food, beverage and agriculture businesses.

Contact Danielle to further discuss the R&E amortization or other credits and incentives at Danielle Bradley (Tax Credits and Incentives Director), Matthew Sapowith (Tax Partner), or Michael Silvio (Tax Partner).

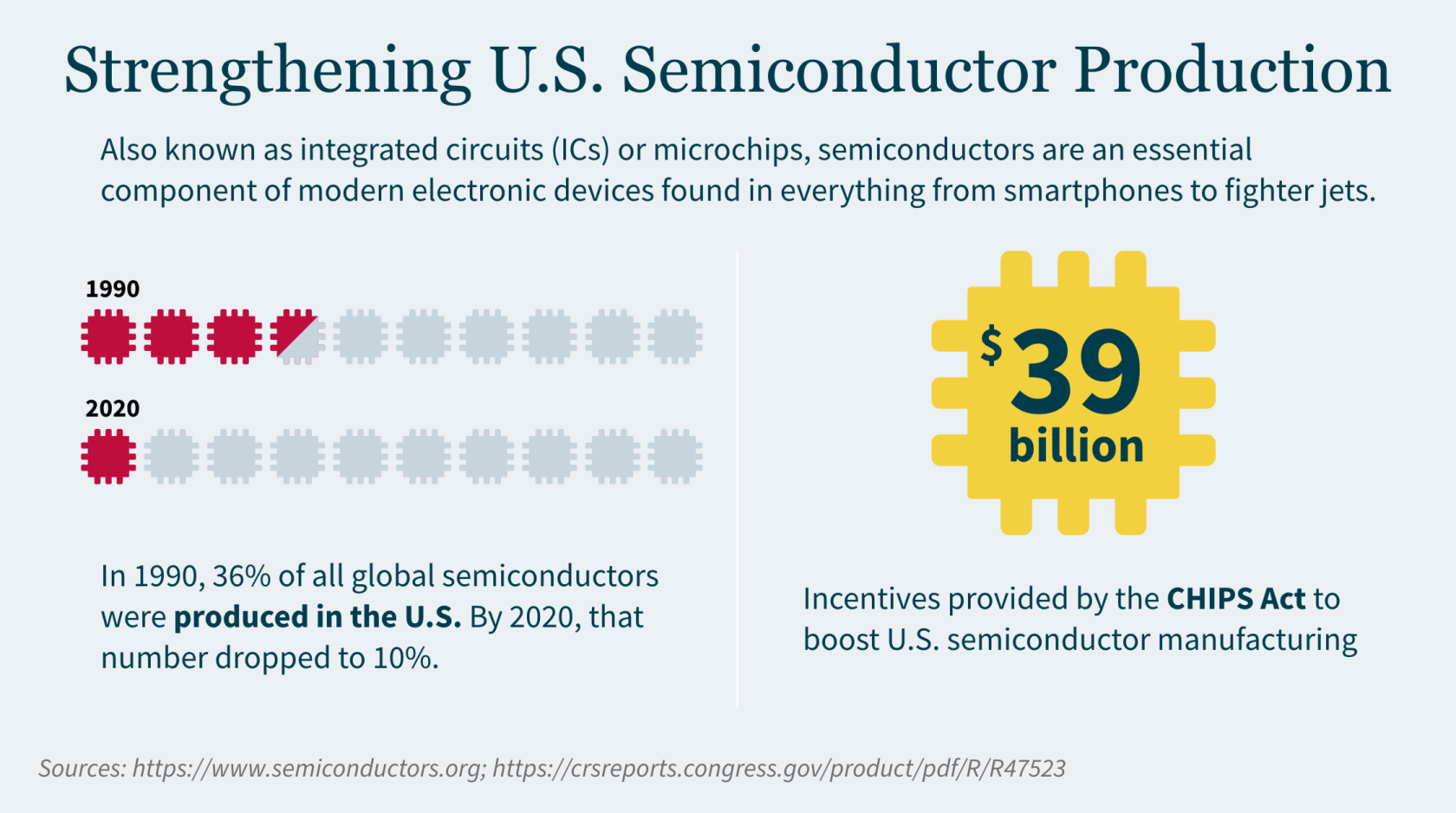

]]>- The CHIPS Act provides more than $50 billion to boost U.S. semiconductor manufacturing, including current funding opportunities for commercial fabrication facilities and advanced packaging research and development (R&D).

- The Advanced Manufacturing Tax Credit (Section 48D) offers a 25% credit for qualified investments into semiconductor manufacturing facilities placed in service from 2023-2026.

- Companies seeking CHIPS incentives or 48D credit should understand eligibility requirements, review application process details, and connect with specialized tax credits and incentives professionals to ensure maximum benefit.

~

On August 9, 2022, President Joe Biden signed into law the Creating Helpful Incentives to Produce Semiconductors Act of 2022 (commonly referred to as the CHIPS Act). The legislation provides $52.7 billion to increase semiconductor research and development in the United States. The CHIPS Act also established the Advanced Manufacturing Tax Credit (Section 48D), available to entities that manufacture semiconductors.

Recently, the government awarded its first major CHIPS Act grant – providing $1.5 billion to GlobalFoundries, one of the world’s leading semiconductor manufacturers, to expand its semiconductor production in New York and Vermont. That grant is expected to be the first of several announcements in the coming months as the government ramps up CHIPS Act funding.

What is the Purpose of the CHIPS Act?

The intent of CHIPS is simple: the U.S. wants to incentivize domestic companies to manufacture semiconductors. The president called the CHIPS Act a “once-in-a-generation investment in America itself,” as the legislation aims to lower costs and create jobs in the production of these advanced chips.

The COVID-19 pandemic forced the semiconductor industry to operate at a reduced capacity, while lockdowns increased demand for products using semiconductors (computers, tablets, gaming systems, cars, etc.). This created a perfect storm, fueling a shortage of semiconductors. As a result, the U.S. recognized the need to increase its semiconductor output.

However, manufacturing semiconductors is not cheap and requires substantial investments. CHIPS, along with the available tax credit, encourages these investments.

The CHIPS Act includes provisions for:

- $39 billion in incentives to build, expand, or modernize domestic facilities and equipment for semiconductor manufacturing, assembly, testing, advanced packaging, or research and development

- $13.2 billion in R&D and workforce development

- $500 million for international information communications technology security and semiconductor supply chain activities

Understanding the Advanced Manufacturing Tax Credit

With the addition of Section 48D to the Internal Revenue Code, CHIPS offers a new tax credit if your company invests in advanced manufacturing facilities or facilities whose primary purpose is manufacturing semiconductors or semiconductor manufacturing equipment.

Eligible businesses can receive a 25% tax credit of “qualified investments”. You can elect to treat the credit as payment against tax (i.e., direct pay) if you do not have sufficient tax liability to utilize the credit, making this essentially a refundable tax credit.

Eligibility criteria for 48D

To be eligible for 48D, you must have made a qualified investment for any taxable year integral to an “advanced manufacturing facility” for semiconductors placed in service during that year. Qualified properties must be:

- Buildings, structural components, or parts of a building (not including administrative services or other functions unrelated to manufacturing)

- Crucial to the operation of the advanced manufacturing facility

- Constructed or built by the taxpayer

- Qualified for amortization or depreciation

Taxpayers that use facilities and equipment outside the U.S. will not be eligible (similar to other investment credit requirements). Other taxpayers ineligible for the credit include:

- Foreign entities noted as “foreign entities of concern” (i.e., foreign terrorist organizations or organizations included on the Office of Foreign Assets Control list).

- Taxpayers that have engaged in significant transactions involving the material expansion of semiconductor manufacturing capacity in China or another foreign country of concern.

- If a taxpayer enters a transaction in a foreign country of concern within 10 years of claiming the credit, it will be recaptured.

48D timing

The tax credit applies to any property placed in service after December 31, 2022, for which construction begins before January 1, 2027. It does not apply after December 31, 2026, nor can you use the tax credit for constructing a property after this date. If construction on a facility began before January 1, 2023, the credit applies only to the portion of the construction started after August 9, 2022.

Application process

In March 2023, the IRS issued proposed regulations addressing direct payment of Section 48D credit. The proposed regulations also require taxpayers to register through an IRS electronic portal before treating Section 48D as a direct payment on a tax return.

The IRS will issue a registration number for each qualified investment for which your company is claiming a credit, and that number must be included on your tax return.

CHIPS Incentive Opportunities

To access CHIPS incentives, your company must first apply for open funding opportunities. To date, the U.S. Department of Commerce has issued three Notice of Funding Opportunities (NOFOs) through the CHIPS for America program:

- Commercial Fabrication Facilities – Currently accepting applicants

- Small-Scale Supplier Projects – No longer accepting applicants, in second phase of process

- National Advanced Packaging Manufacturing Program (NAPMP) Materials & Substrates – Just announced on February 28, 2024

How to apply for open NOFOs

Application forms and instructions are available on the CHIPS Incentives Program application portal. FAQs, guides, and templates can also be found in the “Resources” section of the portal.

The application process includes the following stages:

- Statement of interest

- Pre-application (optional, but recommended)

- Full application

- Due diligence

- Award preparation and issuance

Statement of interest – To submit a statement of interest, applicants need to register for an account on the CHIPS Incentives Portal. A statement of interest must be submitted at least 21 days prior to submitting a pre-application or full application.

Pre-application – The optional pre-application provides an opportunity to ensure your projects are consistent with program requirements. During this stage, you will receive feedback on strengths and weaknesses of your proposal and recommendations for improvement.

Full application – Both pre-applications and full applications are accepted on a rolling basis.

Due diligence – Your application will undergo review to ensure alignment with evaluation criteria specified in the Notice of Funding Opportunity (NOFO), with the possibility of requests for additional information.

Award preparation and issuance – Before receiving an award, you must have an active registration in the System for Award Management (SAM). It’s a good idea to begin the registration process for SAM.gov early as it may take anywhere from two weeks to six months (due to information verification requirements). Check out SAM.gov’s Entity Registration Checklist.

Maximizing Your Semiconductor Manufacturing Tax Credits and Incentives

Navigating CHIPS’s nuances can be challenging – especially when claiming the available tax credit and determining how it is refundable. Furthermore, companies seeking to increase their semiconductor manufacturing capacity in the U.S. should also assess application and opportunity for federal and state R&D tax credits and incentives.

With more than 30 years of experience, our dedicated Tax Credits and Incentives team can help you maximize your credit benefits, develop the appropriate documentation methodology, assist in calculating and claiming credits, and defend your claims. Our full-service firm, led by experienced CPAs and attorneys, provides a holistic approach to examining your organization and determining how to best reach your goals.

]]>We sat down with Tony to ask him some questions about his journey from pre-law student to a leader who excels at crafting relationships that last:

What inspired you to pursue a career in accounting?

My journey into accounting started off as pre-law. Business and entrepreneurship always had a place in my spirit! I remember sitting in my elective business course freshman year, debating with my classmates about which career path had the most available jobs. We looked at the classified ads and saw that the number of jobs for accountants was significantly higher than for attorneys, and that sparked my interest!

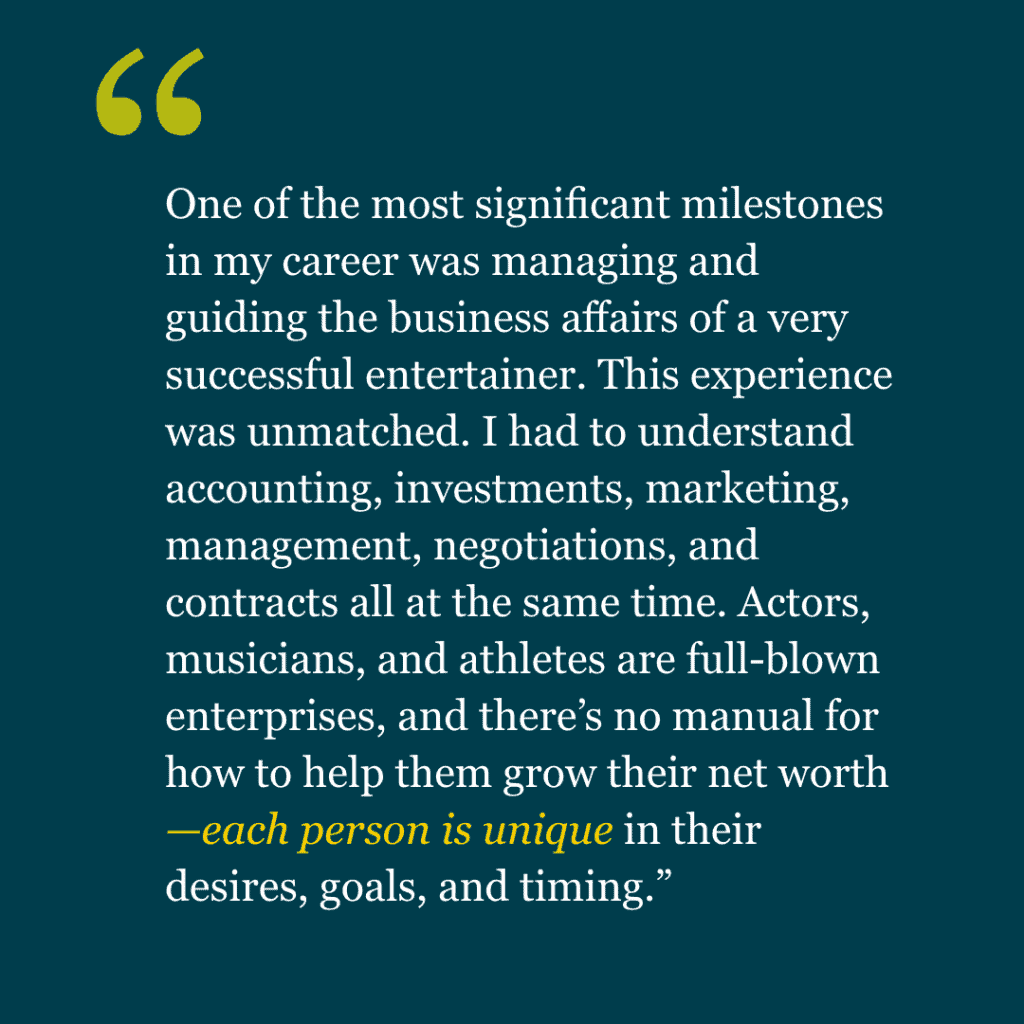

What is a key milestone in your career that you are particularly proud of?

One of the most significant milestones in my career was managing and guiding the business affairs of a very successful entertainer. This experience was unmatched. I had to understand accounting, investments, marketing, management, negotiations, and contracts all at the same time. Actors, musicians, and athletes are full-blown enterprises, and there’s no manual for how to help them grow their net worth — each person is unique in their desires, goals, and timing.

What resources that you have found helpful in your career would you recommend to others?

Networking is key. And I don’t just mean meeting people. I mean, taking the time to understand the person or people you’re engaging with. Really understand what they do, how they do it, their challenges, their successes. Our careers become a series of experiences, and you find that there’s common ground between your journey and others’ . Finding it can help deepen your relationships.

Who has been your greatest source of inspiration in your career?

One of my greatest sources of inspiration is still one of my closest friends and mentors today: Mr. Avery Munnings, who was one of the first African American partners at a Big 4 firm in the Atlanta area. When I was a first year, he told me that when I’m going through the audit programs and asking questions of seasoned executives at large and small companies alike, to seek the answers as if I’m going to use the information in my own company one day. That was a spark to my thinking and approach to problem-solving.

What advice would you give to those just starting out in the field?

Network closely with your colleagues in every department and level. We spend so much of our daily lives in the workplace, and building great internal relationships can improve our overall wellbeing and sense of where we fit in. Not only does it teach us about ourselves, but it also helps us understand each other’s strengths and opportunities, maximizing our work experiences.

Lonnie was kind enough to share his reflections on a variety of topics — from why he chose accounting to the need for diversity in recruitment to the importance of pursuing your passions:

Entering accounting

I became an Enrolled Agent because I wanted to be able to challenge IRS positions and represent the taxpayers. It’s taught me tax ethics, as well as given me the confidence to solve my clients’ greatest tax problems.

Seeing the big picture

My first job in engineering was in the cost estimating department for an architect engineering firm specializing in power plant construction, and I flirted with becoming a cost engineer, using my accounting knowledge to help develop budgets and monitor construction spending. This taught me to learn how to pay attention to detail — but also how to look at the big picture.

Embracing change

Be able to embrace change and be open to new beginnings. View the initial frustration with beginning again as an opportunity for growth. Sometimes, you’ve got to take a step back in order to go forward. Accounting — especially taxation — is a great field if you like to help people. There’s great joy in saving someone money or developing a strategy to reduce taxes.

Continually learning

In our profession, we have the endless opportunity to learn something new. The laws frequently change, and new laws are enacted, so you have to stay up to date with what you’ve learned.

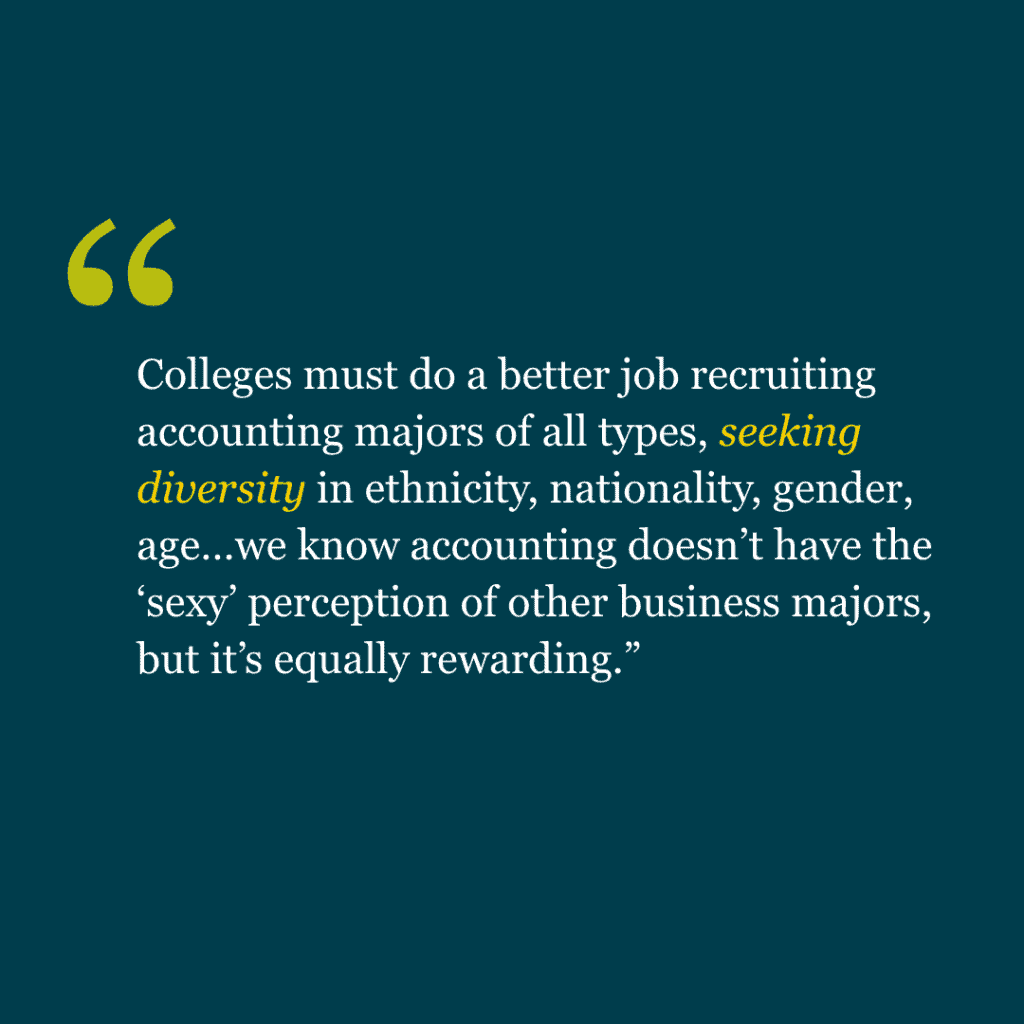

Diversity in accounting

Colleges must do a better job recruiting accounting majors of all types, seeking diversity in ethnicity, nationality, gender, age…we know accounting doesn’t have the ‘sexy’ perception of other business majors, but it’s equally rewarding.

Pursuing your passion

If I were able to give my younger self some advice, it would be to take the plunge sooner. Never be afraid to pursue your passion.

- The IRS has intensified enforcement of transfer pricing regulations, significantly increasing potential penalties.

- Organizations can reduce exposure to transfer pricing penalties by ensuring adequate documentation and applying global transfer pricing policies consistently.

- In cases where penalties are imposed, businesses can seek penalty abatement by demonstrating reasonable cause and good faith, substantial compliance with transfer pricing rules, and leveraging effective representation from knowledgeable tax advisors.

~

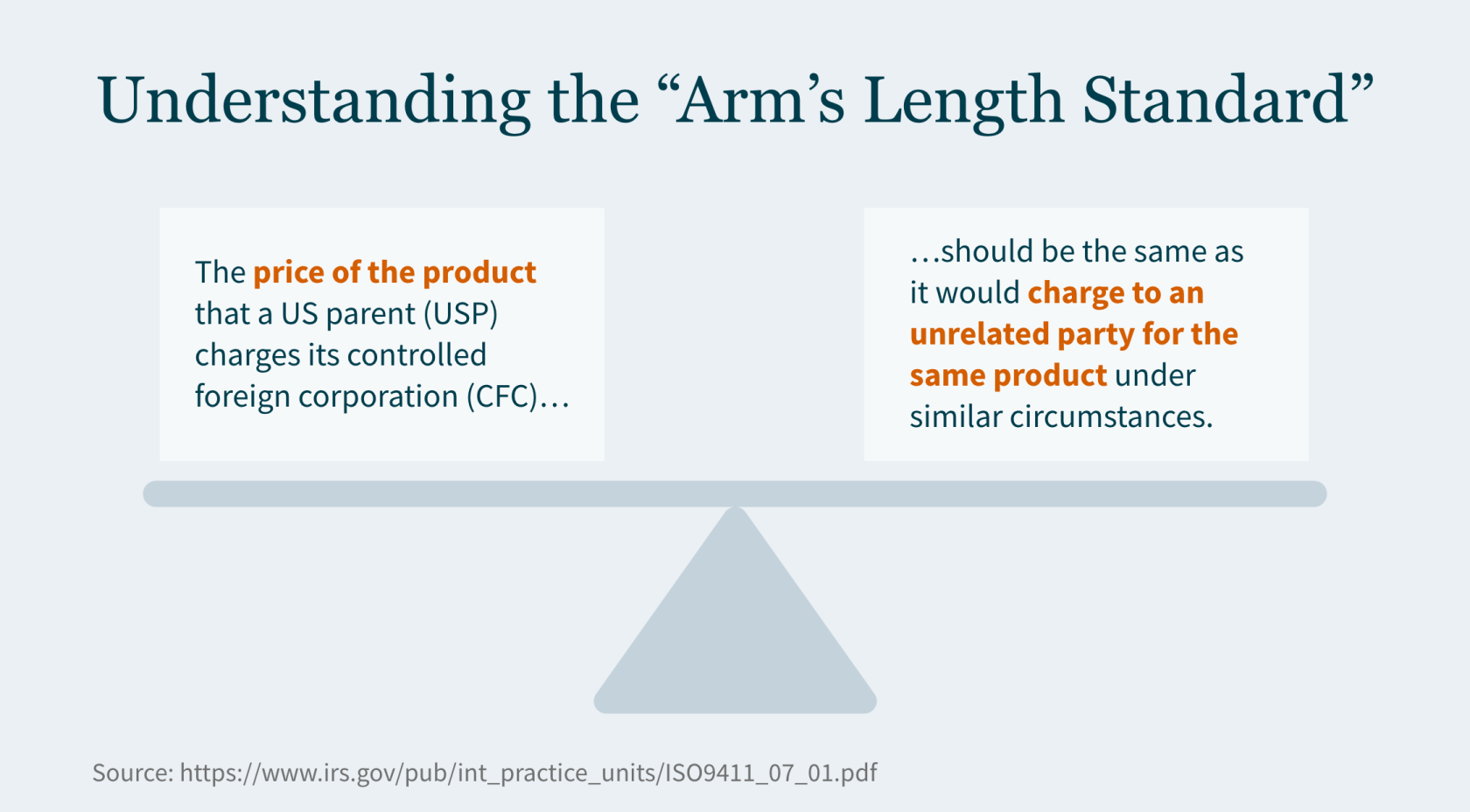

The Internal Revenue Service (IRS) implemented transfer pricing penalties to ensure the intercompany pricing reported on your income tax return is determined in a manner consistent with the arm’s length standard.

Until recently, penalty assessments were rare — not because improper transfer pricing between related parties was rare, but because IRS examiners tended to accept inadequate documentation. That leniency appears to be a thing of the past.

The IRS has indicated it will focus on applying Internal Revenue Code (IRC) Section 6662 penalties where proper documentation is lacking. This trend warrants serious attention if your company engages in cross-border transactions.

Imposing Transfer Pricing Penalties

The IRS can impose penalties when allocations under Section 482 result in substantial or gross increases in taxable income or where there are substantial or gross valuation misstatements concerning the transfer prices themselves.

These penalties can be severe, ranging from 20% to 40% of the tax underpayment, depending on the degree of non-compliance and the taxpayer’s disclosure of relevant information.

Historically, you could avoid these penalties by demonstrating you had reasonably used a transfer pricing method outlined in Section 482 or another method to more reliably determine transfer prices. Taxpayers must also provide contemporaneous documentation within 30 days of a request from the IRS.

The IRS’s Shift Toward Increased Penalty Assertion

The IRS Advisory Council’s 2018 Report noted that, although some transfer pricing documentation quality possibly fell short of the Section 6662 requirements, the IRS had not consistently asserted the penalty. Since then, the IRS has produced guidance addressing common flaws in transfer pricing documentation and best practices, and the agency is now expressing a renewed commitment to applying penalties more frequently and vigorously.

Holly Paz, commissioner of the IRS Large Business and International Division, spoke at several tax practitioner events in late 2022 — including the AICPA’s National Tax Conference, the American Bar Association Section of Taxation’s Philadelphia Tax Conference, and a Bloomberg Tax event. During these events, Paz noted the IRS has had success in litigating transfer pricing cases and is taking a closer look at economic substance and sham transactions — even in cases with transfer pricing documentation — to determine where it is appropriate to assert penalties.

Mitigating Exposure to Transfer Pricing Penalties

In 2020, the IRS published Transfer Pricing Documentation Best Practices Frequently Asked Questions (FAQs). These FAQs point to several features of proper documentation IRS agents look for when determining whether the agency should audit an organization’s transfer pricing methods.

Incorporating these features into your documentation may help reduce your risks:

- Sensitivity analysis – Assess the impact of removing a comparable company from the dataset and determine if such removal alters your position relative to the arm’s-length range. Evaluate how different profit-level indicators might change the results.

- Segmented financial data analysis – Examine if the segmented financial data accurately reflects the arm’s-length nature of the intercompany transaction. Detail the methodology used in constructing this data.

- Profit allocation in intercompany transactions – Analyze profit distribution among entities in the transaction. Ensure equitable economic outcomes for all parties, not just the tested party.

- Description of risks and related-party allocations – Describe associated risks in each intercompany transaction. Explain how profits and losses are allocated among related parties.

- Atypical business circumstances – Identify any unusual business conditions affecting the intercompany transaction. Discuss challenges in the economic analysis due to specific business results for the year.

To navigate this heightened scrutiny, taxpayers must take a proactive approach to document pricing transfer decisions. Steps you can take to avoid commonly seen inadequacies include:

- Providing a detailed description of your business and industry to help IRS agents understand operations and the larger marketplace in which you operate.

- Avoid using a checklist format. Instead, opt for a comprehensive analysis linking facts to the analysis. Base the analysis on well-supported facts, avoiding broad assumptions about the business.

- Ensure consistency in risk allocation with intercompany agreements. Align risk allocation with the comparable companies used in the economic analysis, and clearly explain any adjustments made to comparable companies for risk considerations.

- Prepare a best method selection analysis that justifies rejecting alternative methods for analyzing the intercompany transaction and provides a rationale for the chosen method.

- Clearly outline any adjustments to comparable data, such as working capital or location savings adjustments.

If you believe you have valuation misstatements or understated income tax in previously filed returns, it’s not too late to correct them. Filing a qualified amended return before the IRS contacts you about a transfer pricing audit is a defense against penalties. However, you must pay all taxes associated with the amended returns.

Seeking Penalty Abatement

In instances where penalties are assessed, it may be possible for taxpayers to seek abatement by demonstrating high-quality transfer pricing documentation. You may have a reasonable chance of having penalties abated if you:

- Demonstrate reasonable cause and good faith. Establish that the underpayment was due to reasonable cause, and you acted in good faith.

- Substantial compliance. Show that, despite any errors, you substantially followed the transfer pricing rules.

How We Can Help

The resurgence of transfer pricing penalties is an opportunity to reassess your transfer pricing strategies and compliance mechanisms.

For personalized guidance and assistance navigating these complexities, contact MGO today. Our team of professionals is equipped to help you mitigate risks, confirm compliance, and effectively manage any disputes with tax authorities. Act now to safeguard your business against the pitfalls of transfer pricing penalties.

]]>Here is a brief Q&A with Marlon about how he came to accounting, and what tips and advice he would share with others:

What inspired you to pursue a career in accounting?

I’ve always been interested and good with numbers. In the summer of 1979, my cousin and I decided to develop a mobile juice stand. I started calculating that our profits would be better if we used the orange drink from McDonalds instead of orange juice, as our cost of goods sold would be less.

What key milestones in your accounting career are you particularly proud of?

One of the proudest moments in my career is becoming the first Black Partner at Weaver. We used to joke I was the first Canadian Partner too.

What tips have you found particularly helpful in your career that you would recommend to others?

Find your niche — something that you enjoy doing. Early in my career, I realized I’m not the greatest writer. But I had a fascination with computers and how they could be used to make our lives better. So I leveraged this interest to utilize the tool throughout my career as technology has changed.

What career advice would you give to your younger self?

If I envisioned myself as a Manager at MGO today, I’d tell myself to learn how to say no, so you can be the best at the work in front of you. We all think we’re good at multitasking, but the truth is, it’s more important to focus on excelling at the task at hand and providing the very best service so nothing falls through the cracks.

Here are some insights from Renee on what drives her success:

“We’ve all heard stories about how, as Black professionals, we have to work harder than our nonminority colleagues and excel beyond our counterparts in order to be recognized. But my hard work, loyalty, and dedication to my profession is not driven by the color of my skin; rather, by the passion that I feel for what I do.

My dad was a NYC police officer and taught us discipline and strength. My mom, an entrepreneur, instilled in us a belief in spirituality and God. Both parents always taught me to give my best efforts to everything I do, from the smallest to the largest task—dedicating and giving my whole self to doing my best. I’ve carried that through my entire life.

Although I am thankful to my parents for instilling hard work and discipline in me, I wish that someone had taught me that no matter how hard you work, no matter how many times you say, ‘yes’ to take on additional work, no one is going to reward you unless you value yourself and ask for it.“

Executive Summary:

- A reverse sales and use tax audit is a proactive measure to help your organization identify and recover overpayments, and devise strategies to reduce future sales and use tax burdens.

- Sales and use tax requirements and exemptions vary from jurisdiction to jurisdiction, but your purchases may qualify for a full- or partial-tax exemption.

- Conducting a reverse audit can positively impact your organization’s bottom line, improve compliance processes, and lead to more informed decision-making.

Sales and use tax rates and regulations change often, and the rules vary widely from state to state. As a result, you may find yourself “over-complying” with sales tax rules and neglecting potential savings when it comes to purchase exemptions.

For example, many states provide agricultural and manufacturing exemptions from sales and use taxes, which you can take advantage of by presenting the appropriate sales tax exemption certificate form to your vendors. And for taxes that have already been paid (and that are still within the statute of limitations), you can submit a claim for refund — through a process that is often referred to as a “reverse audit.”

Good candidates for a sales and use tax audit include any business with multistate operations or large fixed asset investments — including cannabis cultivators, manufacturers, construction companies, or any entity in consumer products, healthcare, research and development, and agriculture.

Let’s explore how our State and Local Tax team can leverage exemptions and perform a reverse audit to improve your bottom line.

Understanding Reverse Sales Tax Audits

Sales tax rates and exemptions vary by state and are frequently impacted by evolving department of revenue interpretations and legislative changes at the state and local levels. This makes compliance challenging, and it’s not uncommon for companies to misapply regulations, remit tax at a higher rate, or miss out on potential full or partial tax exemptions.

During a reverse sales tax audit, members of our State and Local Tax team conduct an in-depth review to identify overpayments of sales and use taxes. This process involves examining your purchase records and tax returns to uncover instances where tax was overpaid or erroneously paid.

Once we determine how much tax was overpaid, we prepare the paperwork to request refunds from the appropriate jurisdictions. Most importantly, we train your team to better understand the sales tax and use laws, rates, and exemptions to prevent costly mistakes in the future.

Key Components of the Audit Process

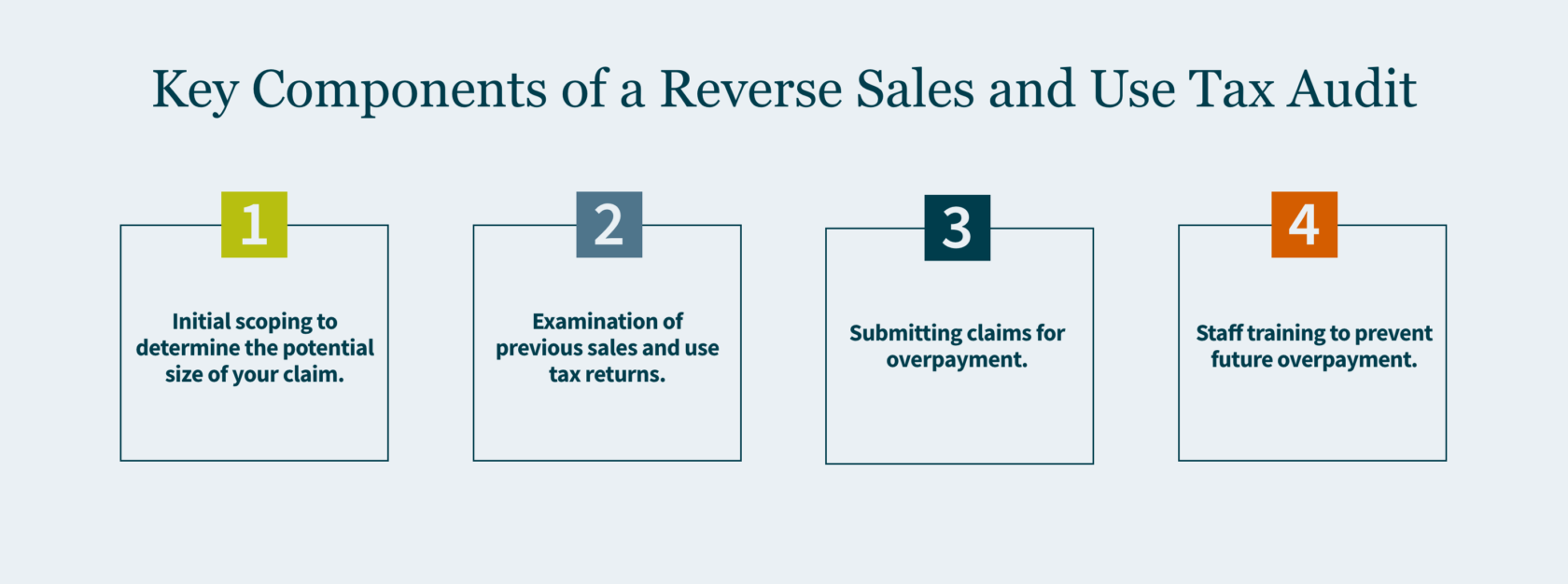

While the term “audit” might have a negative connotation for business owners, a reverse audit isn’t about uncovering wrongdoing but helping your organization locate and uncover potential savings. Although the specific steps for a reverse sales and use tax audit will depend on your business’s unique attributes, the process typically looks something like this:

- Initial scoping to determine the potential size of your claim. We gain an understanding of your business, the jurisdictions you operate in, and your purchasing processes to determine how you were charged tax by vendors and estimate the potential refund we might be able to claim as a result of the reverse audit.

- Examination of previous sales and use tax returns. We review your past returns, invoices, accruals, and other documentation to identify discrepancies and potential overpayments. This involves a line-by-line analysis to confirm tax calculations align with the prevailing tax laws and detect instances where sales tax was paid on non-taxable items or where full- or partial-tax exemptions were overlooked. We also confirm valid exemption certificates are in place and have been correctly applied to qualifying transactions.

- Submitting claims for overpayment. We prepare and submit refund claims to the relevant authorities (keeping in mind the statute of limitations periods, which can vary from state to state). Each state has its own forms and procedures for submitting refund claims. Refunds can also offset audit assessments from state and local governments. This reduces the liability imposed and lowers the amount on which penalties and interest are calculated.

- Train your staff. Finally, we train your team members to identify potential tax-exempt purchases and how to be sure vendors do not charge tax on exempt items. We also provide instruction on proper tax exemption certificate documentation and storage in the event of a future state tax audit. This helps make sure your organization won’t overpay sales and use taxes going forward.

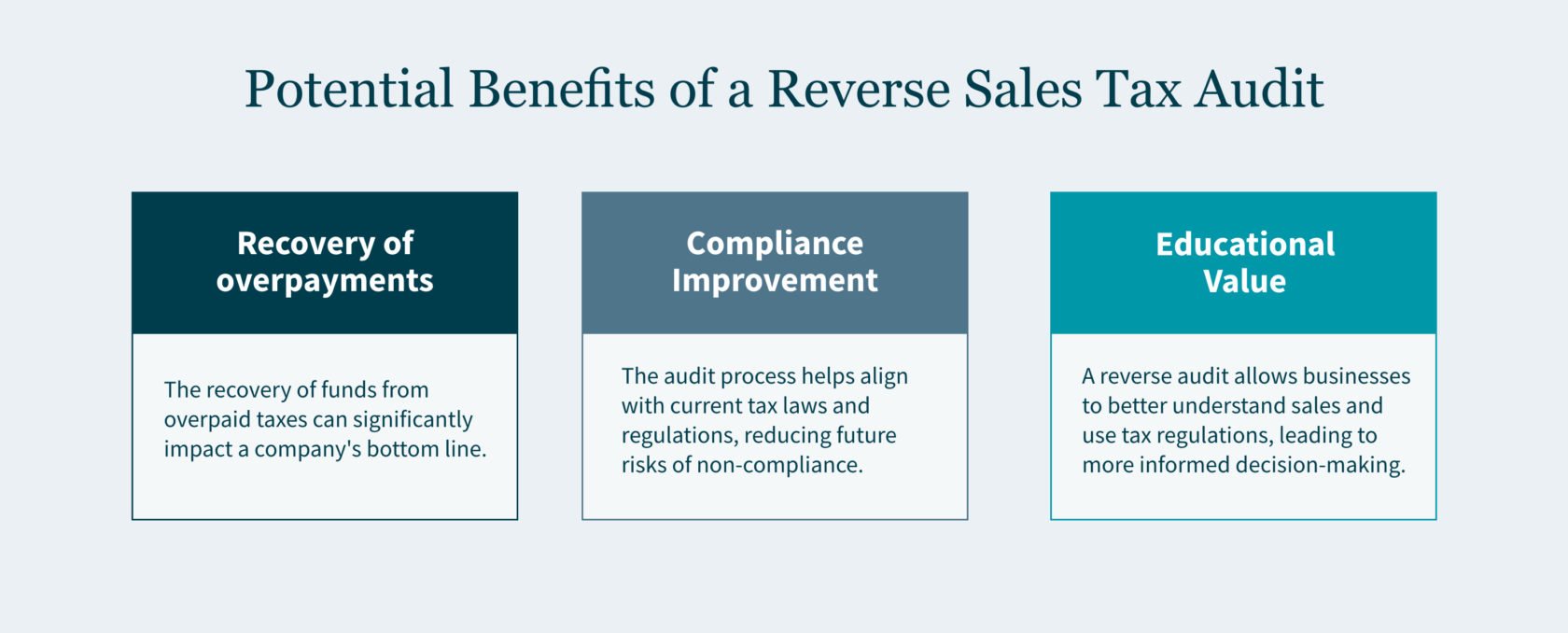

- Recovery of overpayments: The primary benefit is the recovery of funds from overpaid taxes, which can significantly impact your company’s bottom line.

- Compliance improvement: The audit process helps align with current tax laws and regulations, reducing future risks of non-compliance.

- Educational value: A reverse audit helps businesses better understand sales and use tax regulations, leading to more informed decision-making.

Potential Benefits of a Reverse Sales Tax Audit

Key benefits of a reverse audit include:

How MGO Can Help

A reverse sales tax audit is not merely a financial recovery tool but a strategic approach to confirm compliance and optimize tax positions.

To explore how a reverse sales tax audit can benefit your business, contact MGO today. Our team of professionals can discuss your company’s purchases, potential exemptions, and the reverse audit process to determine whether the potential financial opportunities outweigh the time and effort required for the audit.

]]>Executive Summary:

- Implementing basic accounting practices and understanding tax implications can help individuals working independently in creative fields gain clarity, meet obligations, and maximize income.

- Separating business and personal finances, tracking income and expenses, and budgeting for estimated taxes can help creators be proactive in their financial planning.

- Creators earning income across state lines or internationally need to be aware of varying taxation requirements in different jurisdictions.

~

Today’s artists need to view themselves as both businesses and creatives. Whether you are a painter, digital artist, photographer, website designer, YouTuber, Instagrammer, or any type of artist, creator, or influencer, understanding and managing your financial obligations is a crucial aspect of sustaining a thriving career.

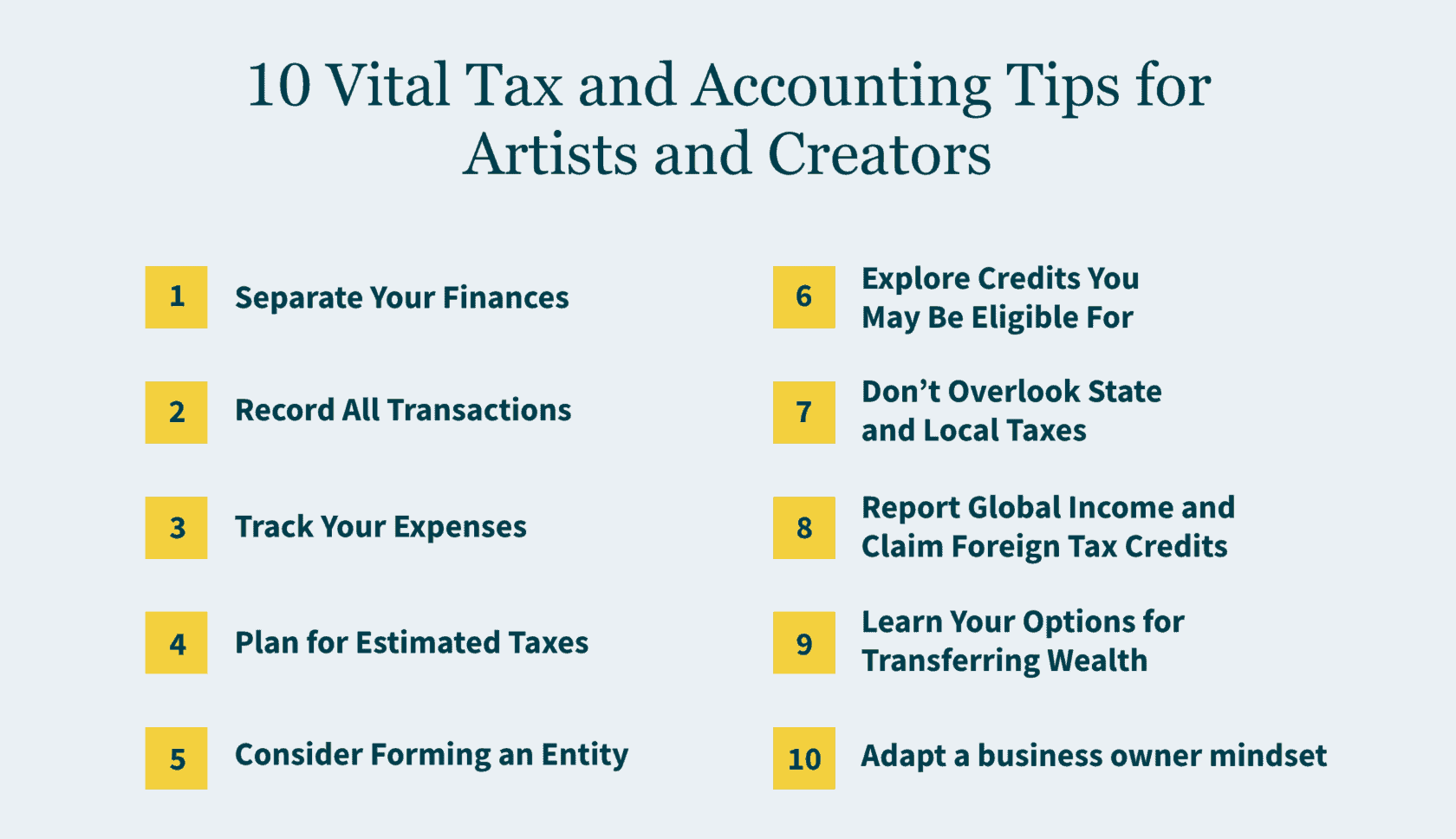

Here are 10 tips to help you meet your tax reporting responsibilities and get the most from your hard-earned income:

1. Separate Your Finances

To make your accounting more efficient and streamline the tax-filing process, it is a smart idea to separate your business and personal finances. Designate a dedicated business account to track income and expenses related to your artistic endeavors. This separation not only simplifies tax reporting but also enhances financial clarity, making it easier to assess the overall health of your creative enterprise.

Tip: Establish a separate account for business transactions, or multiple business accounts to allocate money for categories such as expenses, taxes, and savings.

2. Record All Transactions

Sometimes it can be challenging to determine what constitutes income. That’s why it’s important to track everything. Gifts received by sponsors are often taxable, especially if they are products in exchange for services (e.g., promotion of product). “Donations” from various fundraising activities like Kickstarter are also considered revenue. On the other hand, crypto and non-fungible tokens (NFTs) are considered property. Selling them usually generates a capital gain or loss.

Tip: Log all payments and gifts received, even if you are unsure, so your tax preparer can report appropriately.

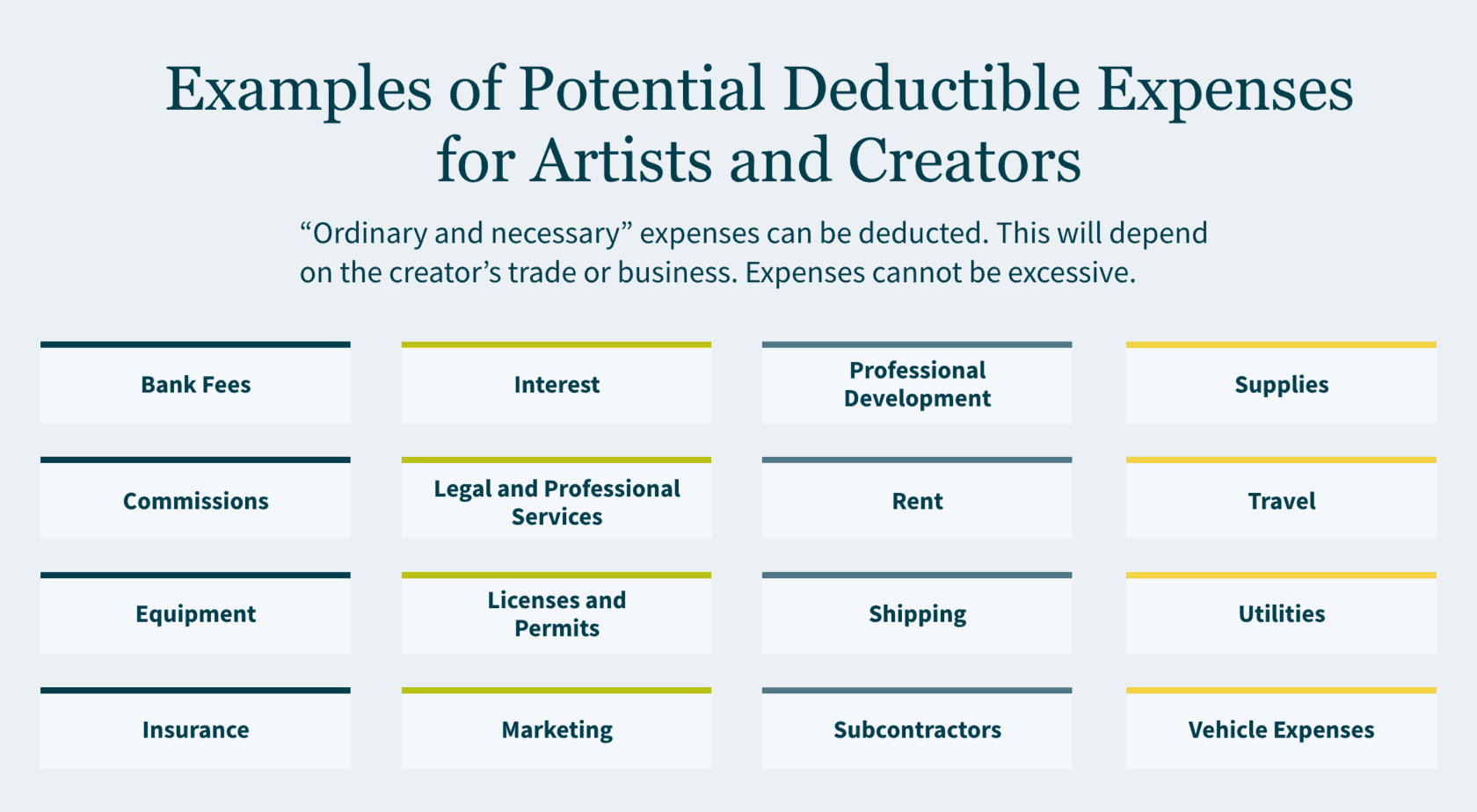

3. Track Your Expenses

Creators and artists can benefit from various tax deductions tailored to their industry. Deductible expenses may include art supplies, equipment, software subscriptions, professional development, and even a portion of your home used as a dedicated workspace. While expenses should not be excessive, any “ordinary and necessary” expenses of your craft can be deducted.

Tip: Save receipts and track expenses in real-time using a spreadsheet, app, or software for easy recording and reporting.

4. Consider Forming an Entity

Creators who run their own business are often independent contractors. Consider setting up an entity for the business — which can help protect your personal assets from your business assets and offer tax savings. S Corporations and LLCs are common for smaller businesses. For larger businesses where investors are coming in, C Corporation may make sense.

Tip: Do some research or talk to a tax professional to find out if setting up an entity makes business and financial sense for you.

5. Explore Credits You May Be Eligible For

Artists also may be eligible for various tax credits that can help offset their tax liability. Research and Development (R&D) credits can be applicable to certain creative processes, rewarding innovation in your artistic pursuits. For instance, software development is considered to be R&D for income tax purposes.

Tip: Consult a tax professional about ways to maximize credits and minimize your tax liability.

6. Don’t Overlook State and Local Taxes (SALT)

Beyond federal taxes, SALT significantly impact overall tax liability. When selling art online (whether physical or digital), be mindful of sales tax requirements, which are determined by local laws. Whether revenue is from “tangible” versus “intangible” products (physical objects versus services, ideas, software, etc.) can dictate where taxation occurs — affecting if your income is subject to sales tax or not.

Tip: Stay informed about varying tax rates, and be cautious of sales and use tax implications tied to transmitting creative art across state lines.

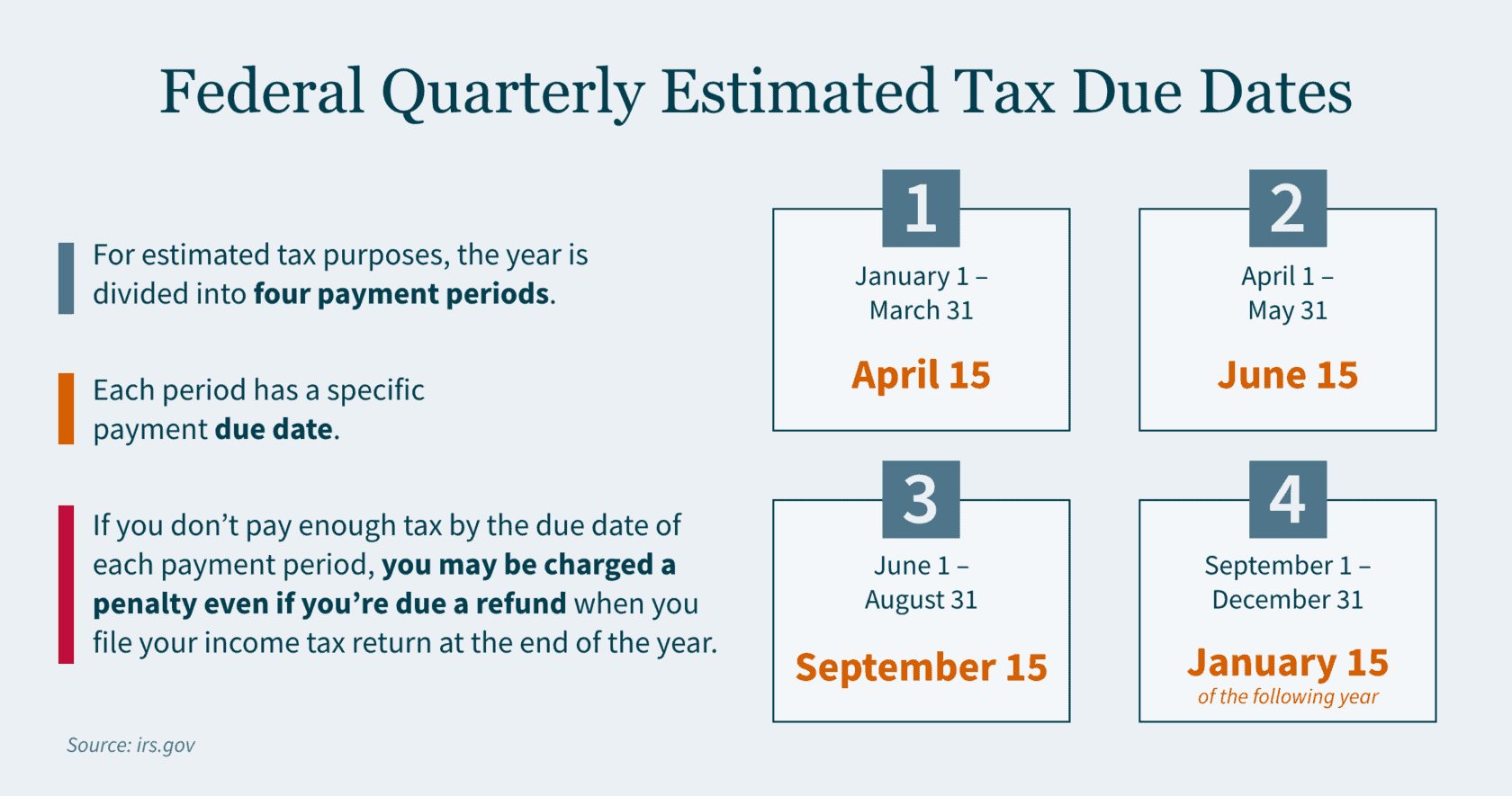

7. Plan for Estimated Taxes

As an independent contractor with variable income streams, you should plan for estimated taxes to avoid financial surprises. These quarterly payments encompass income taxes on your profits plus the self-employment tax (covering Social Security and Medicare). For those earning up to $160,200 in net income, the self-employment tax rate currently stands at 15.3%. The silver lining is that you can deduct half of this self-employment tax when filing your income taxes.

Tip: Set aside a portion of your income for estimated tax payments, ensuring proactive financial planning throughout the year.

8. Report Global Income and Claim Foreign Tax Credits

United States (U.S.) citizens or residents earning abroad must report all worldwide income to the Internal Revenue Service (IRS). If you’re earning income in or from foreign countries, it’s crucial to understand foreign tax credits, filing requirements, and deductibility in various jurisdictions. Every tax jurisdiction may have a different method to tax your creation; and different tax implications may arise based on where brands and intellectual property are created and protected.

Tip: Work with a tax professional to evaluate the potential benefits of foreign tax credits for non-U.S. income.

9. Learn Your Options for Transferring Wealth

Digital assets such as domain names, electronically stored photos, and videos to email and social media accounts all have value. When transferring these as gifts or bequests, there may be tax implications that can be circumvented if the transfer is appropriately structured or organized.

Tip: Consider trusts and estate planning for more tax-efficient wealth transfer.

10. Adapt a Business Owner Mindset

As an artist, embracing a business owner’s perspective is essential for long-term success. Understanding basic financial statements like balance sheets and profit and loss (P&L) statements allows you to gauge profitability, identify your most valuable revenue sources, and streamline your efforts. Elevating your financial literacy empowers you to make more informed decisions — which can lead to greater freedom and flexibility in your artistic career.

Quick Tip: Learn to read a balance sheet and create a basic P&L statement for a clearer financial picture.

Integrate Financial Management into Your Creative Journey

Effective financial planning is like a great work of art — every brushstroke matters. By taking these steps today you can better position yourself to continue pursuing your creative passion tomorrow.

Need a hand with taxes and accounting for your creative venture? Our Entertainment, Sports, and Media practice works with a diverse range of artists — from musicians to photographers to online creators — and our International Tax and State and Local Tax teams can provide guidance to help you address areas like sales tax or foreign tax credits. Reach out to MGO today.

- Internal controls, especially around fraud prevention, are essential for limiting losses, driving efficiency, improving accountability, and boosting company value during investments or M&A deals.

- The “tone at the top” from leadership in fostering an ethical environment, along with proper segregation of duties, are key elements for fraud prevention and strong internal controls.

- Well-established policies and procedures, like Delegation of Authority rules and restricted system access protocols, are also vital for maintaining adequate controls to enable company growth.

~

As the economy stands on shaky legs, private equity and venture capital firms are necessarily careful and strategic when assessing potential investment opportunities. Whether your long-term plan includes acquiring another company, selling your business, or seeking new capital, strengthening your internal control environment — with a focus on preventing fraud — is a powerful way to increase actual and perceived value.

In the following, we will lay out the reasons why fraud prevention is an essential element to proper corporate governance and illustrate key areas to examine whether your internal control environment is built to help your operation succeed.

The Importance of Internal Controls in Fraud Prevention

A robust internal control system is the first step toward managing, mitigating, and uncovering fraud. A strong internal control environment will:

Protect your company’s assets by reducing the risk of theft or misappropriation of cash, inventory, equipment, and intellectual property.

Detect fraudulent activities or irregularities early on and deter employees from attempting fraud in the first place.

Provide cost savings by limiting opportunities for financial losses, costly investigations, and legal expenses associated with fraud.

Drive operational efficiency by providing clear processes and guidelines that reduce the risk of errors or inefficiencies in day-to-day operations.

Improve employee accountability by implementing checks and balances that discourage unethical behavior.

When seeking an investment or undertaking a significant M&A deal, you should have a firm grasp of the strength and quality of your internal control environment. Not only will you reduce the risk of fraud in the near term, but you will also cultivate confidence with potential investors and M&A partners.

Fraud Prevention Starts with the “Tone at the Top”

The first key element to look for in measuring the strength of your internal controls is ensuring a clear and proactive “tone at the top”, meaning an ethical environment fostered by the board of directors, audit committee, and senior management. A good tone at the top encourages positive behavior and helps prevent fraud and other unethical practices.

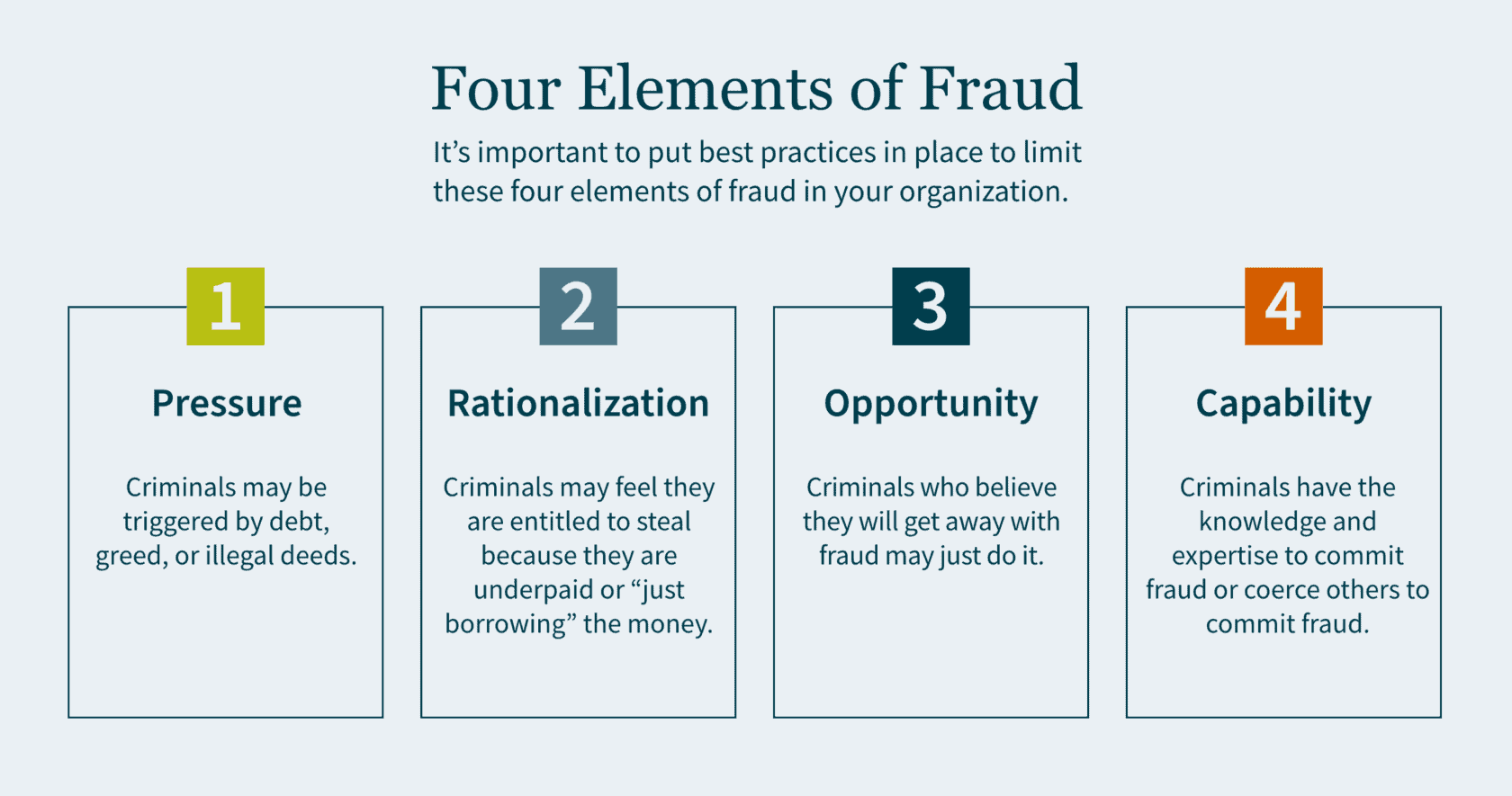

There are four elements to fraud: pressure, rationalization, opportunity and capability.

Pressure motivates crime. This could be triggered by debt, greed, or illegal deeds. Individuals who have financial problems and commit financial crimes tend to rationalize their actions. Criminals may feel that they are entitled to the money they are stealing, because they believe they are underpaid. In some cases, they simply rationalize to themselves that they are only “borrowing” the money and have every intention of paying it back.

Criminals who can commit fraud and believe they will get away with it may just do it. Capability means the criminal has the expertise as well as the intelligence to coerce others into committing fraud. The board of directors is responsible for selecting and monitoring executive management to ensure best practices are in place to limit the motivations of all four elements of fraud.

Proper Segregation of Duties for Internal Controls

The second key element to look for in your internal controls is a well-established segregation of duties. The idea is to establish controls so that no single person has the ability that would allow them the opportunity to commit fraud. Companies must make it extremely difficult for any single employee to have the opportunity to perpetrate a crime and subsequently cover it up.

Fraud Controls

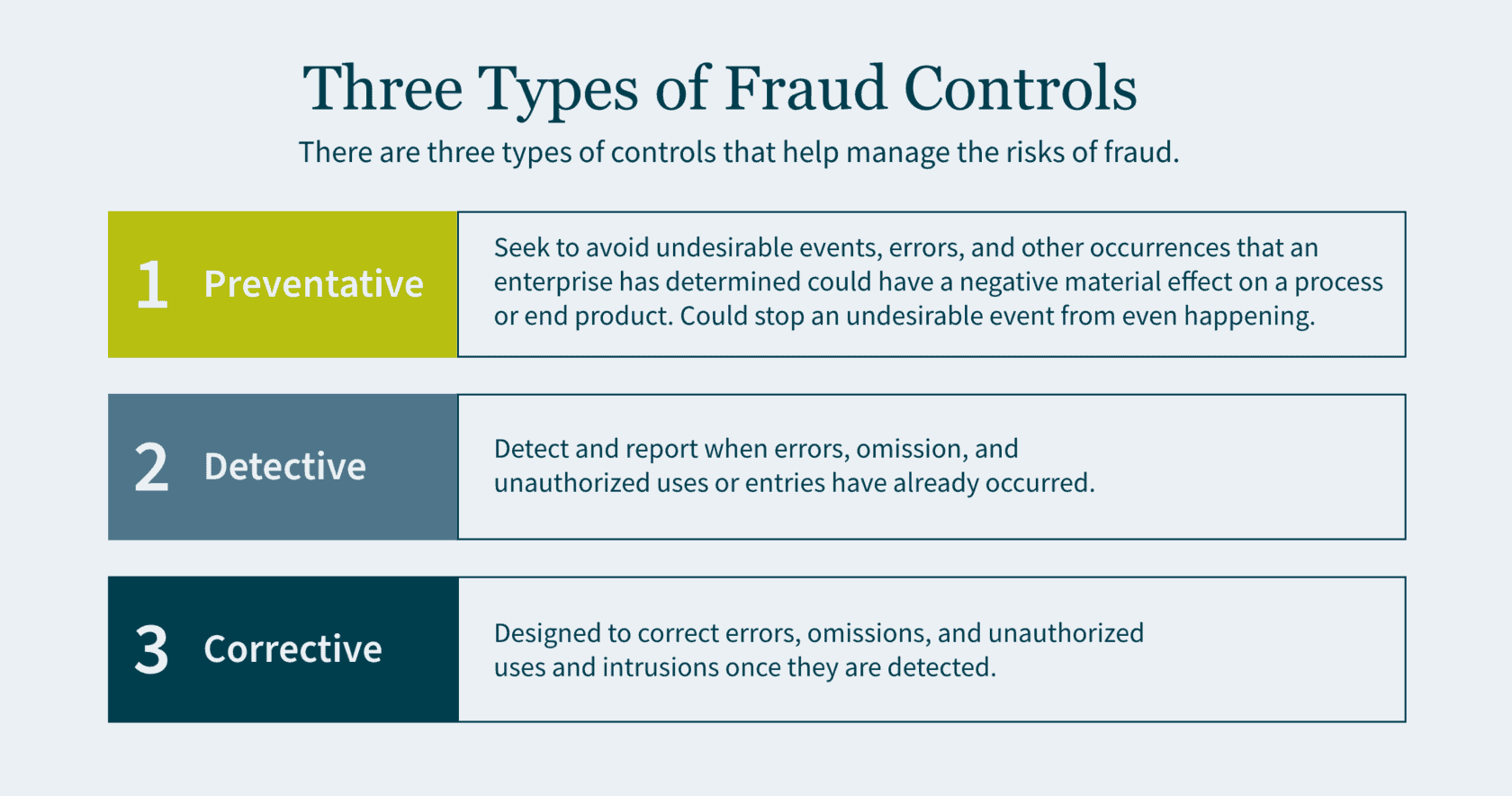

There are three types of controls that help manage the risks of fraud: preventative, detective, and corrective.

- Preventative controls seek to avoid undesirable events, errors, and other occurrences that an enterprise has determined could have a negative material effect on a process or end product. Preventative controls are the best of the three as they are the first line of defense and a backstop to fraud. If designed correctly, preventative controls stop an undesirable event from even happening.

- Detective controls exist to detect and report when errors, omission, and unauthorized uses or entries have already occurred. Although it is important to identify these adverse events, you are doing so after the fraud has already been committed.

- Corrective (also referred to as compensating) controls are designed to correct errors, omissions, and unauthorized uses and intrusions once they are detected.

Preventing Misappropriation of Assets

An important component of segregation of duties is to prevent the misappropriation of assets and reduce fraud risk. Below are some examples of best practices for various types of assets:

- Cash Receipt: segregate the receipt of cash/checks and the recording of the journal entry in the accounting system into two roles.

- Accounts Receivable: segregate the responsibilities of recording cash received from customers and providing credit memos to customers. (If one person performs both functions, it creates the opportunity to divert payments from the customer to the employee and then cover the theft with a matching credit to the customer’s account).

- Cash Reconciliation: the individuals who authorize, process, or record cash should not perform the bank reconciliation to the general ledger.

- Inventory: individuals who order goods from the suppliers should not have the ability to log the goods received in the accounting system.

- Payroll: segregate the responsibilities of compiling gross and net pay for payroll, with the responsibilities of verifying the calculation. (If a single individual performs both functions, it allows for the opportunity to increase personal compensation and the compensation of others without authorization. It also provides an opportunity to create a fictitious payee and make corresponding payroll checks).

The Importance of Policies and Procedures

The third key element to look for in your investees is well-established policies and procedures. Make sure that any company you consider acquiring has basic policies and procedures in place, such as Delegation of Authority (DOA).

The DOA is a policy where the executive team delegates authority to the management of the company. Individuals should be considered appropriate to fulfill delegated roles and responsibilities. The DOA should be reviewed at least annually. Subsequently, it is important to ensure that the DOA is being followed, and that approvals do not deviate from it. Any such anomalies should be rare and, when they do occur, they need to be reviewed and approved. Constant deviations from the DOA may be a sign that the DOA needs to be restructured.

A second essential policy and procedure is restricted computer and application access. This is to protect sensitive company financials and proprietary data. The company should have a robust control environment and maintain computer logins and password access on a need-to-know basis. Access should only be granted by the owner of the application or system and subsequently logged by the administrator. Now more than ever companies are hiring remote employees. This shift in the dynamic workspace further emphasizes the need for a quality IT controls environment.

How We Can Help

As you prepare your company for future growth, getting an impartial third-party opinion on your internal control environment can be a powerful tool for finding gaps and inefficiencies, and implementing value-added changes.

Our dedicated Public Company teams offer a deep level of industry experience and technical skills. We can help prepare your company for a major capital raise, including going public via an IPO or RTO. Or we can help optimize value for an M&A deal, whether you are buying or selling. Contact us today to access an external, holistic vision focused on helping you grow and succeed

]]>