Under this Act, foreign companies traded on any U.S. exchanges are required to have their auditors submit to inspection by the Public Company Accounting Oversight Board (PCAOB) in an effort to establish that they’re neither owned nor controlled by a foreign government. With a wealth of Chinese companies trading in the U.S., the legislation is likely to have a significant impact on Chinese companies and their accounting firms, as well as U.S. investors and the capital market, for years to come.

How the HFCAA works

The Act will amend Section 104 the Sarbanes-Oxley Act of 2002, the comprehensive legislation passed by Congress aimed at overseeing the conduct of public companies. Pursuant to the HFCAA, there will be a number of sizable changes.

• First, the Securities and Exchange Commission (SEC) will now be required to identify companies that are utilizing registered public accounting firms located outside the United States that are preventing audits from the PCAOB.

• Additionally, the SEC must prohibit securities trading of these public companies within U.S. markets following three consecutive years of non-inspection. Under the language of the bill, these companies will be prohibited from trading on either a national securities exchange or “through any other method that is within the jurisdiction of the Commission to regulate, including through the method of trading that is commonly referred to as the ‘over-the-counter’ trading of securities.” It should be noted that in the event an issuer receives a trading prohibition, then the issuer is allowed to have the prohibition overturned as long as it is able to retain an accounting firm that can be fully inspected by the PCAOB.

• Also, as part of the Act, there are disclosure requirements for non-inspection years for foreign issuers of securities that utilize firms to prepare audit reports. For instance, they will need to disclose the percentage of shares owned by foreign government entities. They will also need to disclose whether or not foreign government entities have “controlling financial interest with respect to the issue.”

• Finally, there are also disclosure requirements that specifically involve China. According to the Act, the names of each official of the Chinese Communist Party of the board of directors of either the issuer or “the operating entity with respect to the issuer” must be disclosed in their Form 10-K, Form 20-F, and shell company reports. Additionally, it must be disclosed if the issuer’s articles of incorporation (or “equivalent organizing document”) has “any charter of the Chinese Communist Party, including the text of any such charter.”

Potential impact of the HFCAA

While the HFCAA applies to any U.S.-listed company incorporated outside the United States, including Mainland China, Hong Kong, France, and Belgium, it is generally understood as explicitly targeting Chinese companies under the restrictions imposed by the Chinese government.

This Act could lead to an increase in the number Chinese and Hong Kong-based issuers being delisted from U.S. exchanges in the coming years. In fact, according to the list of public companies affected by obstacles to PCAOB inspections, there are more than 200 Chinese companies currently audited by CPA firms in mainland China and Hong Kong that would be negatively impacted. These companies, including popular stocks such as Alibaba Group Holding Ltd – ADR, Baidu Inc, JD.com Inc, and Nio Inc – ADR, could feel the brunt of this new legislation.

Note that the Big Four accounting firms in China are independent from the Big Four in the U.S. and do not meet the audit requirements of the PCAOB since they are under the China’s national security laws and the Chinese Securities Law, which prohibit Chinese companies from providing records “relating to securities business activities” overseas without approval by the Chinese securities regulator. Besides, the imminent enactment would certainly discourage new listing of Chinese companies in the U.S. as it could result in a discount on the trading prices as investors may factor in the potential de-listing risk.

However, it remains to be seen how the SEC implementation will roll out within 90 days of the HFCAA’s enactment, which could be greatly influenced by the new leadership of the SEC. According to Bloomberg, President-elect Joe Biden is expected to pick Gary Gensler to head the SEC.

Additionally, because of the three-year compliance timeline in the Act, Chinese companies may consider several options to mitigate the impending risks. The most likely one is to engage a reputable U.S.-based CPA firm, preferably one that has an established China Group, who understands both the Chinese business climate and the U.S. accounting rules, and most importantly obtain a clean compliance record with PCAOB. Yet, it’s also critical that companies consider other factors such as the investor and make sustainable long-term plan to maintain a legitimate and confident position in US capital markets.

If you have any questions

MGO’s SEC practice has a dedicated China Group experienced with Chinese IPOs, RTOs, M&A deals and the unique characteristics of SPAC acquisitions. To understand your options, and the path ahead, please feel free to reach out to us for a consultation.

In the cannabis and hemp industries, capturing the true value of real estate holdings in an M&A deal can be both elusive and central to the overall success of the transaction. Difficult-to-acquire licenses and permits are essential for operating, which often drives up the “ticket price” of property, ignoring operational and market realities that suppress value in the long run. On the flip side, real estate holdings are sometimes considered “throw-ins” during a large M&A deal. These properties can hold risks and exposures, or, in many cases, are under-utilized and present an opportunity to uncover hidden value.

Both Acquirers and Target companies must take specific steps toward understanding the varied layers of risk and opportunity presented by real estate holdings. In the following, we will address some common scenarios and provide guidance on the best way to ensure fair value throughout an M&A deal.

Real estate as a starting point for enterprise value

Leaders of cannabis and hemp enterprises must understand that real estate should be a focus of the M&A process from the very beginning. All too often, c-suite executives are well-acquainted with detailed financial analyses for other parts of the business, but have a limited or out-of-date idea of their enterprise’s square footage, details of lease agreements, or comparable values in shifting real estate markets. Oftentimes it takes a major business event, like an M&A deal, to spur leadership to reexamine and understand real estate holdings and strategy. Regrettably, and all too often, principals come to that realization post-closing and realize they may have left money on the table.

In an M&A deal, the party that takes a proactive approach to real estate considerations gains an upper-hand in negotiations and calculating value. Real estate holdings can provide immediate opportunities for liquidity, cost-reduction, or revenue generation. At the same time, detailed due diligence can reveal redundant properties, costly debt obligations, unbreakable leases, and other red flags that would undermine value post-closing.

For both sides of the M&A transaction, real estate strategy and valuation should be a core consideration of the overall goals and value drivers of the deal. A direct path to this mindset is to place real estate holdings on the same level of importance as other assets that drive value – human capital, technology, intellectual property, etc. Ensuring that real estate strategy aligns with business goals and objectives will save considerable headaches and potential liabilities in the later stages of negotiating and closing the deal.

Qualify and confirm all real estate data

One of the harmful side-effects of a laissez-faire attitude toward real estate in M&A is that the entire deal can be structured around data that is simply inaccurate or incomplete. This inconsistency is not necessarily the result of an overt deception, but too often it is simply an oversight. Valuations can also be based upon pride and ego, without supporting market data.

Let’s visit a very common M&A scenario: The Target company has real estate data on file from when they purchased or leased the property (which may have been years ago), and that data says headquarters is 20,000 sq. ft. of office space. Perhaps they invested heavily into improvements like custom interiors that did nothing to add value to the real estate. The Target includes that number in the valuation process and the Acquirer assumes it is accurate. Following the deal, the Acquirer moves in and, in the worst case, realizes there is actually only 15,000 sq. ft. of useable space. Or it is equally common that the Acquirer learns the space is actually 25,000 sq. ft. Either way, value has been misrepresented or underreported. M&A deals involve a multitude of figures and calculations, and sometimes things are simply missed. But those small things can have a major impact on value and performance in the long run.

The only solution to this problem is to dedicate resources to qualifying and quantifying data related to real estate holdings. When preparing to sell, Target companies should review all assumptions – square footage, usage percentage, useful life, etc. – and conduct field measurements and physical condition assessments (“PCA’s”). This will help your team understand the value of your holdings and set realistic expectations, and perhaps just as importantly, it saves you from the embarrassment of providing inaccurate numbers exposed during Acquirer’s due diligence—and getting re-traded on price and terms. That reputation will ripple through the marketplace.

From the Acquirer’s side, the details of real estate holdings should come under the same level of scrutiny as financials, control environment, etc. Your due diligence team should commission its own field measurements and PCA, and also seek out market comparables to confirm appraisals. It is simply unsafe and unwise to assume the accuracy of any of these details. Performing your own assessments could reveal a solid basis to re-negotiate the M&A, and will help shape post-merger integration planning.

Tax analysis will reveal risks and opportunities

The maze of tax regimes and regulatory requirements cannabis and hemp operators navigate naturally creates opportunities to maximize efficiencies. This is particularly the case when it comes to enterprise restructuring to navigate the tax burden of 280E.

For example, it may be possible to establish a real estate holding company that is a distinct entity from any “plant-touching” operations. By restructuring the real estate holdings and contributing those assets to this new entity it may be possible to take advantage of additional tax benefits not afforded to the group if owned directly by the “plant-touching” entity. This all assumes a fair market rent is charged between the entities.

Recently, operators have looked to sale/leaseback transactions to help with cash flow needs and thus these types of transactions have gained prominence for cannabis and hemp operators. It is important that these transactions be carefully reviewed prior to execution to ensure they can maintain their tax status as a true sale and subsequent lease, instead of being considered a deferred financing transaction. If a Target company has a sale/leaseback deal established but under audit the facts and circumstances do not hold up, this could open up major tax liabilities for the Acquirer.

When entering into an M&A transaction, it is important that the Acquirer look at the historical and future aspects of the Target’s assets, including the real estate, to maximize efficiencies of these potentially separate operations. It is also equally important to review pre-established agreements/transactions to ensure the appropriate tax classification has been made and that the appropriate facts and circumstances that gave rise to the agreements/transactions have been documented and followed to limit any potential negative exposure in the future.

Contract small print could make or break a deal

An area of particular focus during due diligence should be a review, and close read, of the Target company’s existing property leases and other contracts. There are any number of clauses and agreements that seem harmless and inconsequential on the surface, but can have disastrous effects in difficult situations. In many cases the lease/contract of a property is more important than the details of the property itself. For example, if the non-negotiable rent on a retail location is too high (and scheduled to go higher), there may be no way to ever turn a profit.

The financial distress resulting from the COVID-19 pandemic has brought these issues to the forefront in the real estate industry. Rent payment and occupancy issues are shifting the fundamental economics of many property deals and contracts. If, for example, you are acquiring a commercial location that is under-utilized because of market demand or governmental mandate, you must confirm whether sub-leases or assignments are allowed at below the contract price. If not, you could be stuck with a costly, underperforming asset amid quickly shifting commercial real estate demand.

In many leases and contracts there are Tenant Improvement Allowance conditions that require the landlord to fund certain property improvement projects. If utilizing these terms is part of the Acquirer’s plans, you may need to have frank and open conversations with landlords about whether the funds for these projects are still available, and if those contract obligations will be met. Details like these are often penned during times of financial comfort without consequences to the non-performing party, but a landlord struggling with cash flow may not have the capability to meet contract standards.

These are just a few examples from a multitude of potential real estate contract issues that can emerge. It is recommended to not only examine these contracts very closely, but have dedicated real estate industry experts perform independent assessments that account for broader social, economic, and market realities. That independent analysis will help your executive team formulate a real estate strategy that better aligns with core business objectives.

Dig deep to uncover real value

There are countless scenarios where issues related to real estate make or break an otherwise solid M&A transaction, whether before or after closing the deal. The only path forward is to treat real estate holdings with the same care and attention paid to the other asset classes driving the deal. The cannabis and hemp industries have recently endured micro-boom-and-bust cycles that have left many assets under-performing. As Target companies offload these assets, and Acquirers seek out good deals, both parties must undertake focused efforts to establish the fair value of complex real estate assets and obligations.

Catch up on previous articles in this series and see what’s coming next…

]]>Mergers with SPACs have always been an alternative to traditional IPOs. With the IPO market effectively minimized for the time being, SPAC mergers are an increasingly desirable public market liquidity option for private companies.

What the numbers tell us

2020 is a record-shattering year for a revitalized SPAC market. According to data provided by ELLO Capital, there have been 95 SPAC IPOs so far in 2020, raising $37.8 billion (average size: $397 million). That compares with 59 in all of 2019, which raised $13.6 billion (average size: $230 million).

On July 22, 2020, Pershing Square founder Bill Ackman raised $4 billion in the IPO of Pershing Square Tontine Holdings Ltd., the largest SPAC IPO to date. With an initial target of $3 billion, the SPAC included a unique pricing approach: a fixed pool of warrants to be distributed to shareholders who accept a subsequent deal – increasing the take for approvers.

“COVID-19 is likely a direct cause of the acceleration in SPACs this year, as global lockdown policies have restricted travel and the ability to do roadshows. As a result, SPACs have largely replaced traditional IPOs,” said Mark Young, co-founding partner of Bridge Point Capital. “Plus, SPACS appeal to the high-growth technology sector, which has led the market recovery post-February correction, and continue to drive grwoth in the work-from-home economy.”

SPACs: rules of the road

- Speed is the name of the game – Leveraging the market expertise of leadership team, a SPAC can raise funds in a matter of days, without the time and resource demands of a roadshow.

- Minimum value is set – The acquired company/companies must have a minimum value, generally 80% of the fund the SPAC has in escrow following the IPO. Multiple closings, obviously, complicate the otherwise-simple SPAC process and inject completion risk into the transaction.

- The clock is ticking – There’s a deadline reality for both the SPAC and the target: If the SPAC doesn’t close the deal by the deadline, it must return the funds it raised in its offering. On the flip side, getting near the deadline can help give a target company some leverage.

- Valuation risk – Investors in SPACs are very much like IPO investors: there is an expectation that they are buying at a discount and there is significant growth potential around the corner. They are not looking for turnaround stories. In turn, SPACs are perceived as focused on growth verticals.

- Shareholder approval required – The SPAC is a public company that inherits all the baggage – reporting/regulatory demands, liabilities, etc. – of a public company. Approval by target company shareholders likely will be required. And the SPAC would need to file a proxy statement and secure approval from the Securities and Exchange Commission.

- Redemption risk – Here’s an interesting twist: At the time of the transaction, the SPAC’s public shareholders can redeem their stock. The risk: the SPAC’s cash availability – which might be needed to complete the transaction – could take a hit if the redemptions are significant.

- Warrants also in play – Sometimes the purchase price includes stock; the value of those shares are impacted by the associated rights. In most cases, the warrants can be exercised at a premium to the original offering price. What can happen: the valuation of stock included in purchase price may rise above, or fall below, the value of the stock issued to a target. The driving factor: can a deal actually get done.

- Navigate the de-SPAC phase – Definition: the time between the definitive agreement and closing. What needs to be done: communicate details of the transaction to the SPAC’s stakeholders. The goal: optimize the story, educate sales people, engage analysts – protect value.

The record so far

• DraftKings (NASDAQ: DKNG): Shares in the online fantasy and gambling company jumped to $18.69 per share when the merger agreement was announced in December, and then edged up to $19.35 per share on the first day of trading, Since then, the price has climbed to about $44.00 per share before settling back into the $37.00-$40.00 area. Its current market capitalization is over $13.5 billion.

• Virgin Galactic (NYSE: SPCE.N): The Richard Branson-backed competitor to Elon Musk’s SpaceX and Jeff Bezos’ Blue Origin, Virgin Galactic shares currently trade in around $17.00-$20.00, about double their late October day-one level, and more than three times their low of $6.90 per share. The stock has reached a high of $42.49 per share, and the company’s current market capitalization is $3.9 billion.

• Nikola (NASDAQ: NKLA): The green truck company has been on a roller-coaster ride since its late June debut. It has climbed as high as $93.99 at one point and currently trades at about $37.00 per share. Market capitalization is just under $14 billion.

Leading the way is a pending deal from Churchill Capital Corp. III, which has agreed to acquire health-cost management services provider MultiPlan for $11 billion. This would make it the largest ever SPAC deal.

“The healthcare and life sciences industries are two sectors likely to continue driving SPAC growth in the COVID-19 era,” said Nadia Tian, co-founding partner of Bridge Point Capital. “This is because healthcare traditionally outperforms the market in a recession, SPACs allow biotech companies to have more cash on hand than a traditional IPO, and the government and consumers are especially focused on these areas as we search for solutions to the COVID-19 outbreak.”

Final thoughts

Private companies that were planning an IPO or other significant M&A deal before the global economic downturn caused by the COVID-19 pandemic may want to seriously consider a SPAC deal. As with all transactions significant, intensive planning, vetting, due diligence and other considerations must be undertaken.

MGO’s dedicated SEC practice has experience with IPOs, RTOs, M&A deals and the unique characteristics of SPAC acquisitions. To understand your options, and the path ahead, please feel free to reach out to us for a consultation.

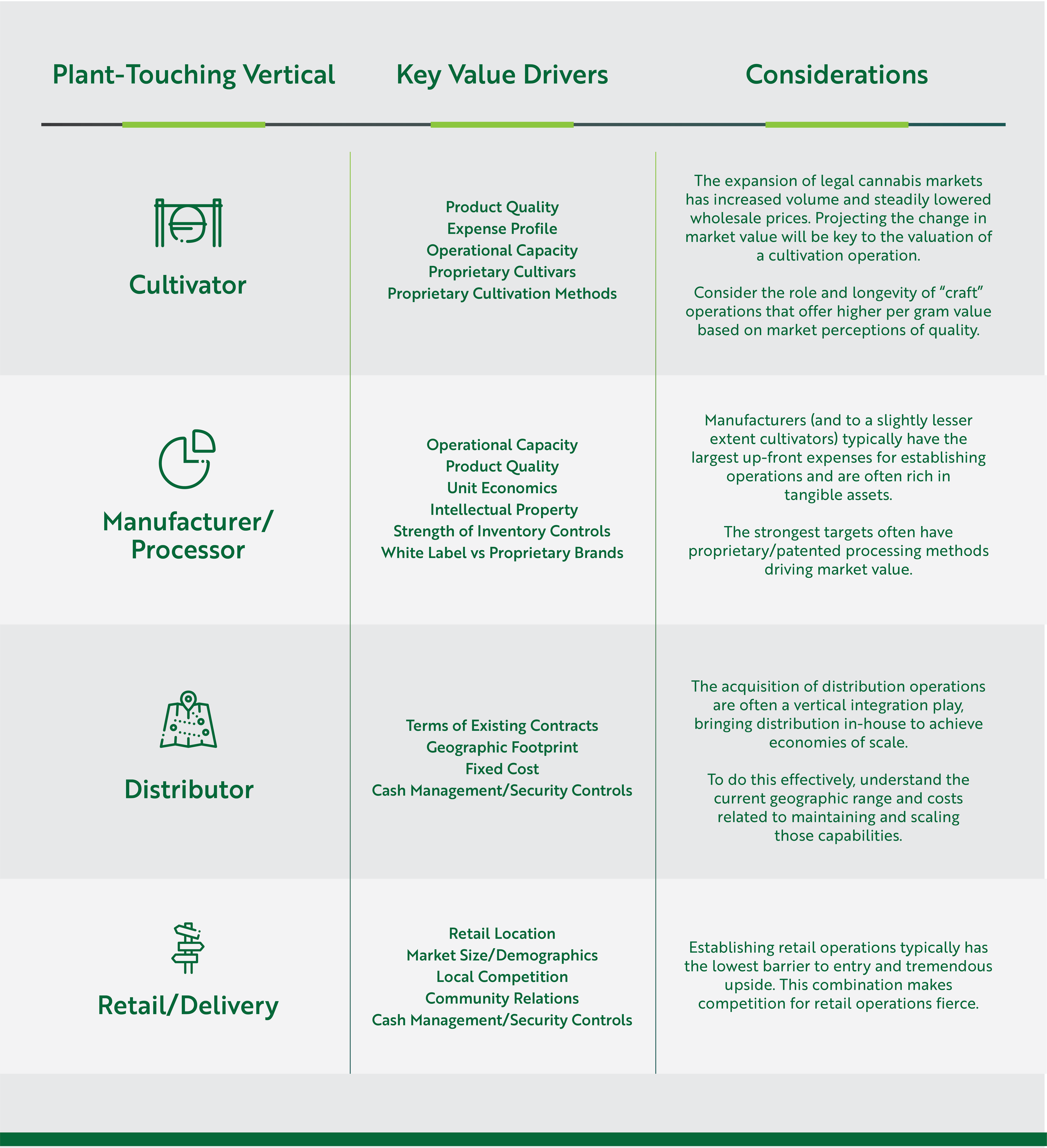

]]>Assessing the value of a cannabis/hemp operation will ultimately be the foundation of any M&A deal. The Acquirer will seek the lowest “fair” price for the Target company and its assets, whereas the Target company will value itself at the highest possible price. The truth will fall somewhere in between and it is of central importance that both parties feel that risks are acknowledged, and that the value brought to the table is recognized.

In most cases, a third-party valuation expert will be brought in to conduct an impartial assessment. To recognize the true value of an operation, it is essential that this valuator is not only an expert in the cannabis and/or hemp industries, but also specializes in the appropriate verticals. For example, when assessing a cultivation facility, the valuator must have the skill to go beyond standard benchmarks, like yield/sq. ft. and grams/watt, and be able to interview the head of cultivation, understand the specialized skills they are bringing (or lacking) and also assess intangibles like the value of unique cultivars. Similarly for a retailer, revenue and expenses provide a baseline, but a valuator must also understand nuances, like the socio-economic details of operating markets and consumer attitudes to proprietary brands.

Valuation in any industry is a complex process, but like all things cannabis and hemp, shifting regulatory and market conditions present another layer of complexity that limit the use of traditional metrics and values. This makes cannabis and hemp valuations as much art as science. In the following, we will lay out the quantifiable fundamentals behind a valuation and provide some key considerations for intangible aspects that lift (or depress) the real value of an operation.

Key factors in valuing a cannabis business

Regulatory Compliance – Every legally-operating cannabis or hemp business in the U.S. is necessarily licensed and compliant with state and local regulations. Since every market is unique and presents different challenges and opportunities, it is essential to both understand those rules and confirm that a Target company has the proper operations and internal controls in place to maintain compliance. In the best case scenario, the failure to maintain compliance will result in fines, penalties and temporary cessation of operations. In the worst case scenario, the entire operation can be permanently shut down.

License Terms, Supply and Demand – The broader conditions driving regulatory compliance are the structure and supply of licenses. In many jurisdictions, including California, many operators are working under temporary licenses, as approval processes for permanent licenses have been delayed. Temporary licenses are tenuous and provide no guarantees that a permanent license will follow. The value of an operation is largely dependent upon the ability to operate legally – excepting some cases of asset sales – making it essential to understand the specifics of how each license was attained and all relevant terms and conditions.

In general, when access to licenses is limited, those licenses are worth more. Many markets, whether at the state or local level, have strict caps on issuing licenses. In states with well-established markets, licenses have been issued for years, leading to an oversupply that can lower both cannabis prices and business valuations. It is also important to consider that states and localities can change their licensing procedures, which could potentially upend the market with new licenses or drive up value by limiting new issuances.

Management Team – Depending on the structure of an M&A deal, and post-integration plans, the skills and experience of the management team of the Target company can help determine a business’s value. The Target company’s leadership will have played a key role in achieving current performance, and will provide projected revenue and long-term strategic plans. Ambitious strategic plans are rarely worth the paper they are written on if the leadership team does not have potential to achieve them. Taking stock of the collective history of the Target company’s leadership will help put projections into perspective.

Even an M&A deal is focused on acquiring assets or integrating Target company operations without keeping senior management, the experience of the team that built the Target company will provide another metric for the viability of existing operational and financial processes and controls.

Operator categories and considerations

In the many verticals of cannabis, businesses fall into one of two broad categories: plant-touching, which are directly involved in cultivating, processing, or selling cannabis, and ancillary, which provide products and services to support the cannabis industry. Going beyond standard financial and operational metrics, each vertical has unique circumstances and considerations that will play a role in valuing the business.

Vertical integration is a key value driver across all plant-touching operations. Having a stake in more than one vertical provides control over product quality and supply, increases margins, and multiplies company value when executed correctly.

Commonly used methods for performing valuations

The following are four commonly used methods to assess value in the cannabis and hemp industries. The appropriate valuation method(s) depends on the company being valued, and will likely include a combination of approaches.

Discounted Cash Flow Analysis (DCF) – DCF measures the value of a company as the present value of all future projected cash flows. The DCF method is dependent upon multi-year projections of future cash flows, adjusted by an appropriate discount rate.

Strengths: Theoretically, if all assumptions hold true, DCF is the most accurate method for valuing a company as it provides an intrinsic valuation. This method allows the appraiser to adjust the financial forecast for different operating outcomes and assumptions to analyze the impact of various scenarios.

Weaknesses: DCF requires making assumptions about future performance and risk profile – and the valuation is only as good as the accuracy of those assumptions. The complexity of the cannabis market makes identifying realistic assumptions difficult.

Precedent Transactions Analysis – Building on the business adage of “something is worth what someone will pay for it,” Precedent Transactions Analysis analyzes the valuation metrics of similar businesses or assets that have been sold or have raised capital. The most common valuation metrics utilized are Enterprise Value / Revenue and Enterprise Value / EBITDA. By examining comparable transactions, an approximate value can be determined by adjusting for company size, growth, and other factors giving a relative valuation range.

Strengths: Based on actual valuations achieved by companies in the market, the Precedent Transactions Analysis can be an accurate gauge of the market’s perspective on value.

Weaknesses: There are a multitude of intangible qualities that ultimately determine value, including changes in leadership and shifting market conditions, the latter of which is completely outside the control of a business. There is limited amounts of data for cannabis/hemp industry transactions, and broader economic and social changes have essentially thrown out the comparisons used in previous years.

Public Comparable Company Analysis – This method values a company by analyzing the valuation metrics of comparable publically-traded companies. Similar to the Precedent Transactions Analysis, adjustments must be made to account for differences between the subject company and the comparable companies.

Strengths: The price of publically-traded companies are based on up-to-date market data and easily accessible. Additionally, quarterly earnings reports and other investor reports can provide detailed financial and operational information.

Weaknesses: This method is more useful in well-established industries with a multitude of comparable companies. Additionally, public company valuations are volatile and can swing heavily due to market factors independent of the company’s fundamentals.

Adjusted Net Asset Approach – The is approach values a company based on the fair market value of its assets less its liabilities. Assets include tangible assets, such as equipment, licenses, and staff, as well as intangible assets such as brand name and a loyal customer base.

Strengths: This approach establishes a fundamental baseline of value based on the company’s owned assets. If the company goes bankrupt, investors can hopefully at least recover the fair market value of these assets.

Weaknesses: As this approach does not consider a company’s income-generating potential, which is significant for most cannabis companies. This approach is generally reserved for distressed and capital-intensive companies.

Everything begins with thorough due diligence

Valuing any business first requires performing in-depth due diligence to understand the inner workings of the company. This includes analyzing the company’s products and services, operations, management team, market, competition, corporate governance, and more. Underlying each of these analyses is the on-going assessment of the company’s risks.

Companies should provide financial projections detailing their projected Income Statement and Cash Flow Statement for the next several years. Projections should utilize assumptions, which management can justify, and should be supported through thorough due diligence efforts. Recent events have shown that financial projections must be analyzed carefully as many are based on assumptions that no longer hold true – making achieving those projections impossible.

We provide more detail about the due diligence process in our dedicated article (COMING SOON).

Every valuation represents a unique case

Valuing a cannabis business is a complex process that is generally done on a case-by-case basis. There is no one answer to the best way to value a business. Landing on an accurate valuation requires in-depth due diligence to analyze the quantitative and qualitative factors driving the company. Ultimately, meetings with the leadership team and visiting the company’s facilities to see the business in action will speak volumes about underlying operational strength and long-term potential.

Catch up on previous articles in this series and see what’s coming next…

]]>Deal structure can be viewed as the “Terms and Conditions” of an M&A deal. It lays out the rights and obligations of both parties, and provides a roadmap for completing the deal successfully. While deal structures are necessarily complex, they typically fall within three overall strategies, each with distinct advantages and disadvantages: Merger, Asset Acquisition and Stock Purchase.

In the following we will address these options, and common alternatives within each category, and provide guidance on their effectiveness in the cannabis and hemp markets.

Key considerations of an M&A structure

Before we get to the actual M&A structure options, it is worth addressing a couple essential factors that play a role in the value of an M&A deal for both sides. Each transaction structure has a unique relationship to these factors and may be advantageous or disadvantageous to both parties.

Transfer of Liabilities: Any company in the legally complex and highly-regulated cannabis and hemp industries bears a certain number of liabilities. When a company is acquired in a stock deal or is merged with, in most cases, the resulting entity takes on those liabilities. The one exception being asset deals, where a buyer purchases all or select assets instead of the equity of the target. In asset deals, liabilities are not required to be transferred.

Shareholder/Third-Party Consent: A layer of complexity for all transaction structures is presented by the need to get consent from related parties. Some degree of shareholder consent is a requirement for mergers and stock/share purchase agreements, and depending on the Target company, getting consent may be smooth, or so difficult it derails negotiations.

Beyond that initial line of consent, deals are likely to require “third party” consent from the Target company’s existing contract holders – which can include suppliers, landlords, employee unions, etc. This is a particularly important consideration in deals where a “change of control” occurs. When the Target company is dissolved as part of the transaction process, the Acquirer is typically required to re-negotiate or enter into new contracts with third parties. Non-tangible assets, including intellectual property, trademarks and patents, and operating licenses, present a further layer of complexity where the Acquirer is often required to have the ownership of those assets formally transferred to the new entity.

Tax Impact: The structure of a deal will ultimately determine which aspects are taxed and which are tax-free. For example, asset acquisitions and stock/share purchases have tax consequences for both the Acquirer and Target companies. However, some merger types can be structured so that at least a part of the sale proceeds can be tax-deferred.

As this can have a significant impact on the ROI of any deal, a deep dive into tax implications (and liabilities) is a must. In the following, we will address the tax implications of each structure in broad strokes, but for more detail please see our article on M&A Tax Implications (COMING SOON).

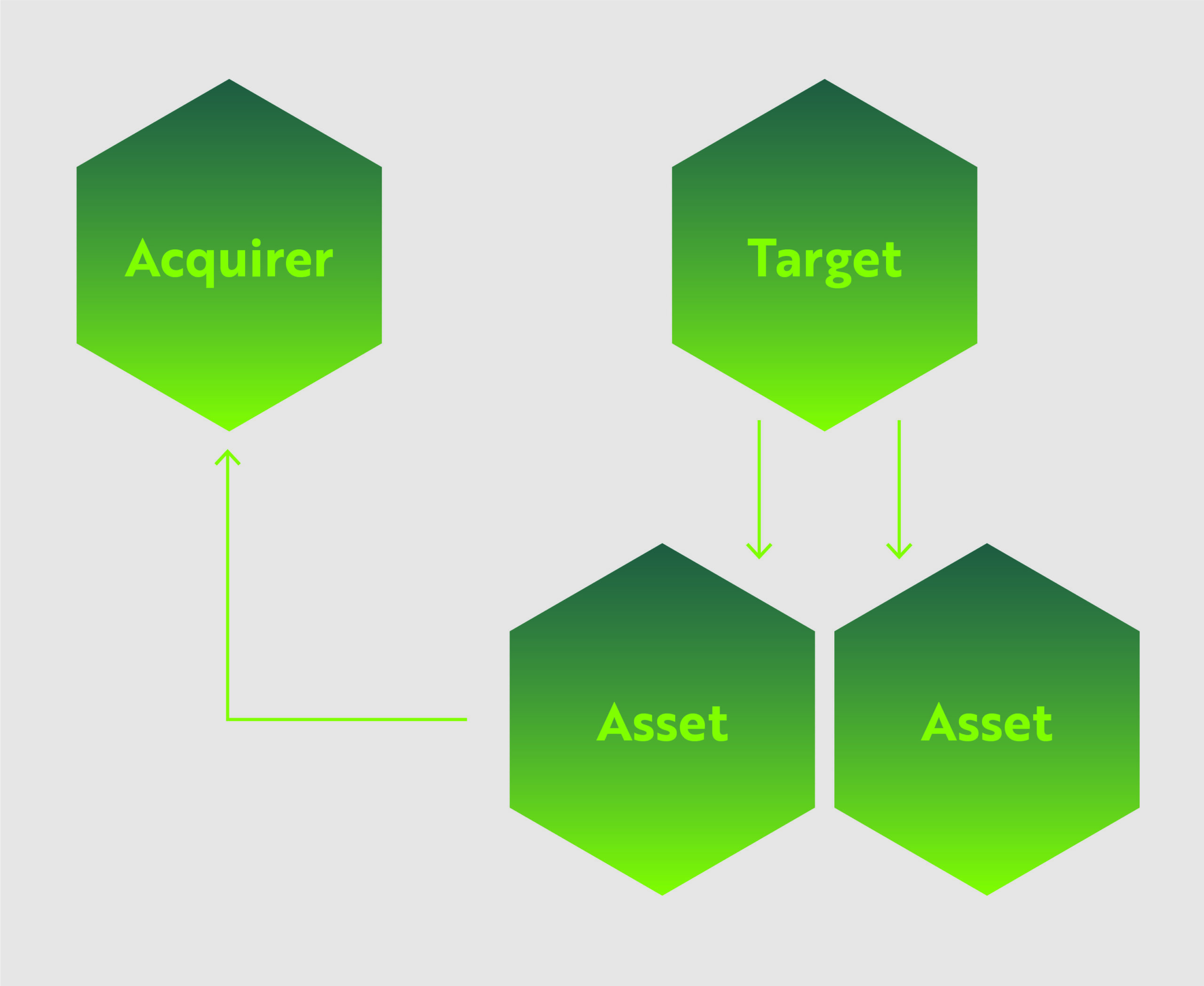

Asset acquisitions

In this structure, the Acquirer identifies specific or all assets held by the Target company, which can include equipment, real estate, leases, inventory, equipment and patents, and pays an agreed-upon value, in cash and/or stock, for those assets. The Target company may continue operation after the deal.

This is one of the most common transaction structures, as the Acquirer can identify the specific assets that match their business plan and avoid burdensome or undesirable aspects of the Target company. From the Target company’s perspective, they can offload under-performing/non-core assets or streamline operations, and either continue operating, pivot, or unwind their company.

For the cannabis industry, asset sales are often preferred as many companies are still working out their operational specifics and the exchange of assets can be mutually beneficial.

Advantages/Disadvantages

Transfer of Liabilities: One of the strongest advantages of an asset deal structure is that the process of negotiating the assets for sale will include discussion of related liabilities. In many cases, the Acquirer can avoid taking on certain liabilities, depending on the types of assets discussed. This gives the Acquirer an added line of defense for protecting itself against inherited liabilities.

Shareholder/Third-Party Consent: Asset acquisitions are unique among the M&A transaction structures in that they do not necessarily require a stockholder majority agreement to conduct the deal.

However, because the entire Target company entity is not transferred in the deal, consent of third-parties can be a major roadblock. Unfortunately, as stated in our M&A Strategy article, many cannabis markets licenses are inextricably linked to the organization/ownership group that applied for and received the license. This means that acquiring an asset, for example a cultivation facility, does not necessarily mean the license to operate the facility can be included in the deal, and would likely require re-application or negotiation with regulatory authorities.

Tax Impact: A major consideration is the potential tax implications of an asset deal. Both the Acquirer and Target company will face immediate tax consequences following the deal. The Acquirer has a slight advantage in that a “step-up” in basis typically occurs, allowing the acquirer to depreciate the assets following the deal. Whereas the Target company is liable for the corporate tax of the sale and will also pay taxes on dividends from the sale.

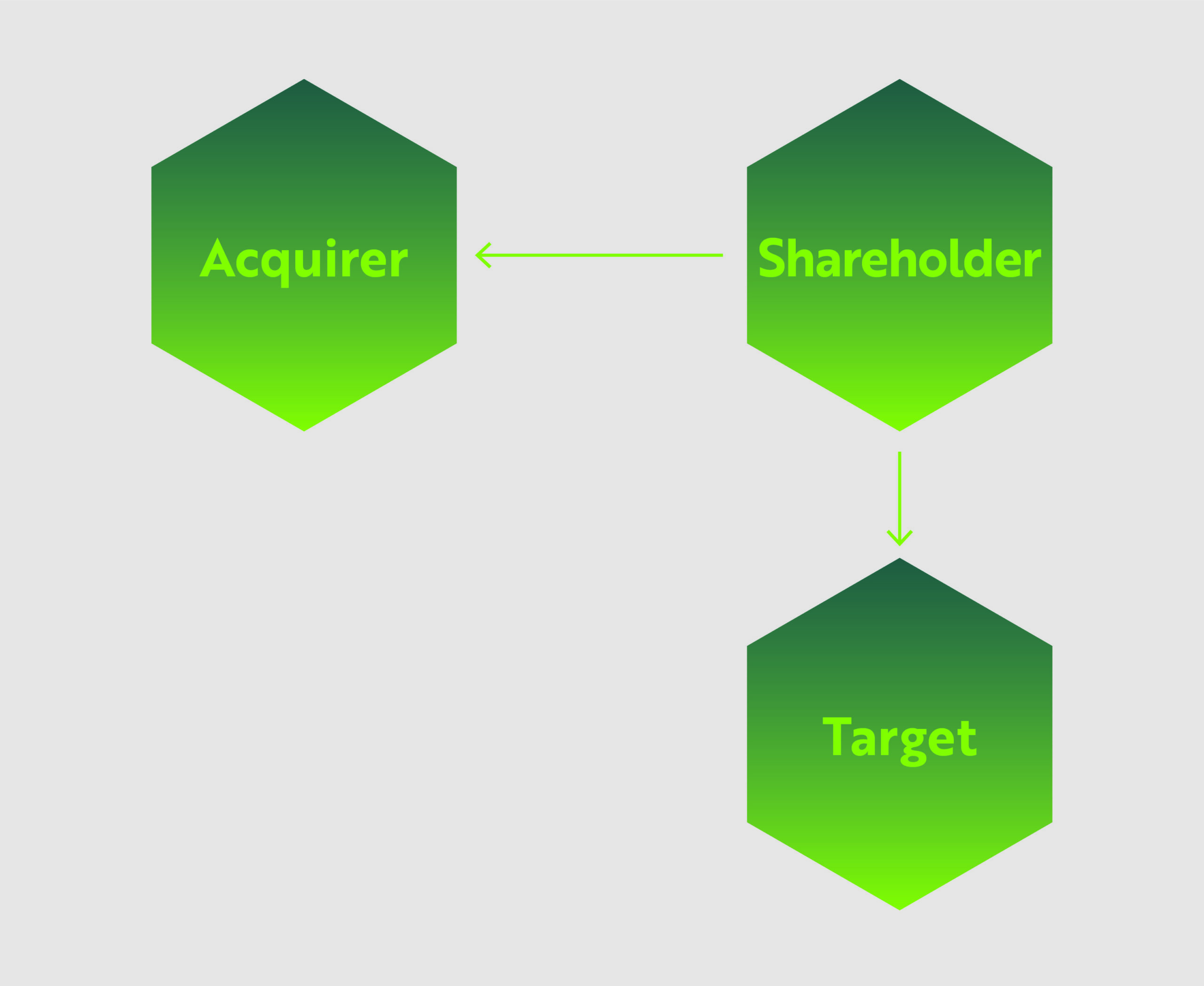

Stock/share purchase

In some ways, a stock/share purchase is a more efficient version of a merger. In this structure, the acquiring company simply purchases the ownership shares of the Target business. The companies do not necessarily merge and the Target company retains its name, structure, operations and business contracts. The Target business simply has a new ownership group.

Advantages/Disadvantages

Transfer of Liabilities: Since the entirety of the company comes under new ownership, all related liabilities are also transferred.

Shareholder/Third Party Consent: To complete a stock deal, the Acquirer needs shareholder approval, which is not problematic in many circumstances. But if the deal is for 100% of a company and/or the Target company has a plenitude of minority shareholders, getting shareholder approval can be difficult, and in some cases, make a deal impossible.

Because assets and contracts remain in the name of the Target company, third party consent is typically not required unless the relevant contracts contain specific prohibitions against assignment when there is a change of control.

Tax Impact: The primary concern for this deal is the unequal tax burdens for the Acquirer vs the Shareholders of the Target company. This structure is ideal for Target company shareholders because it avoids the double taxation that typically occurs with asset sales. Whereas Acquirers face several potentially unfavorable tax outcomes. Firstly, the Target company’s assets do not get adjusted to fair market value, and instead, continue with their historical tax basis. This denies the Acquirer any benefits from depreciation or amortization of the assets (although admittedly not as important in the cannabis industry due to 280E). Additionally, the Acquirer inherits any tax liabilities and uncertain tax positions from the Target company, raising the risk profile of the transaction.

Three types of mergers

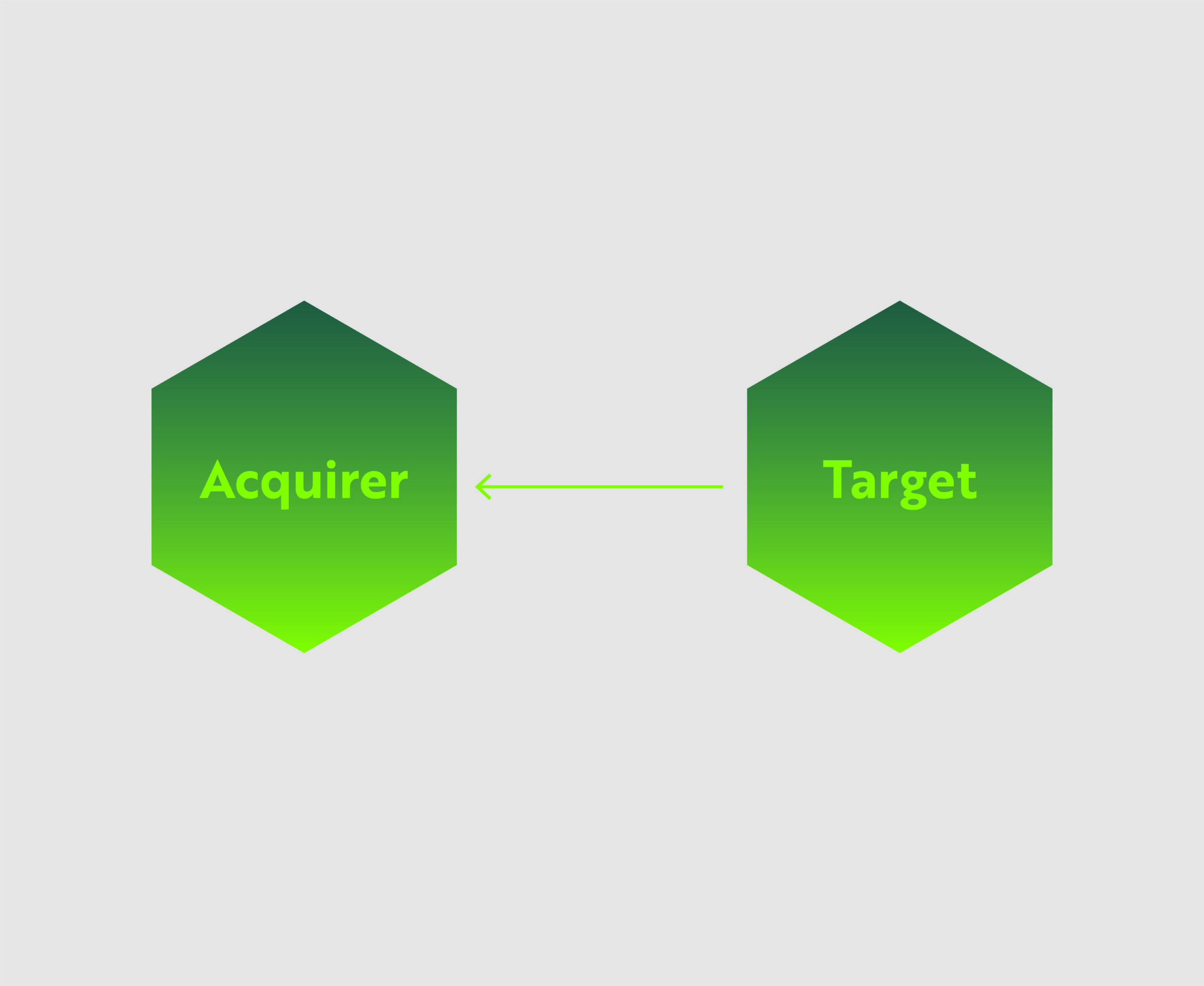

1: Direct merger

In the most straight-forward option, the Acquiring company simply acquires the entirety of the target company, including all assets and liabilities. Target company shareholders are either bought out of their shares with cash, promissory notes, or given compensatory shares of the Acquiring company. The Target company is then considered dissolved upon completion of the deal.

2: Forward indirect merger

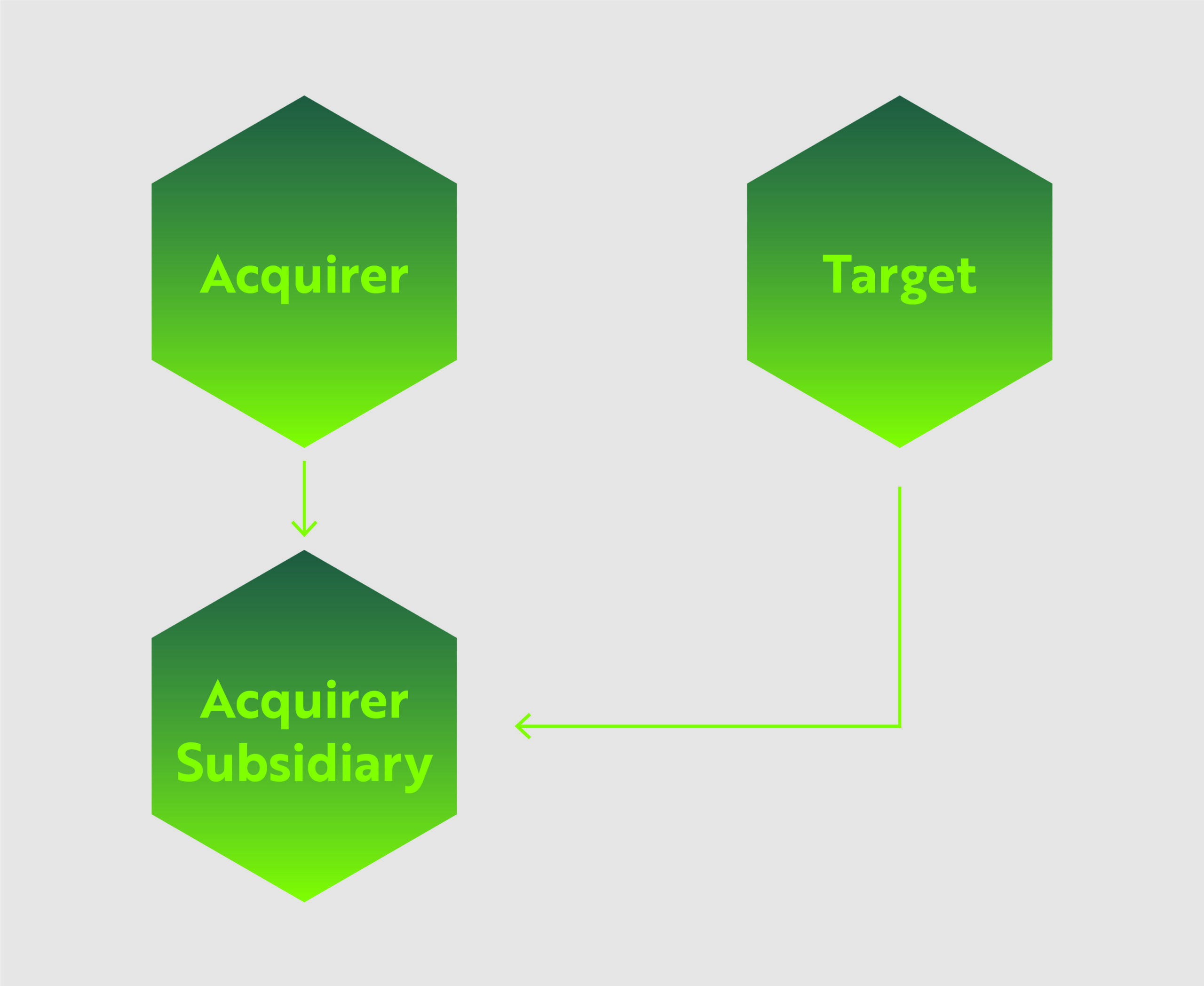

Also known as a forward triangular merger, the Acquiring company merges the Target company into a subsidiary of the Acquirer. The Target company is dissolved upon completion of the deal.

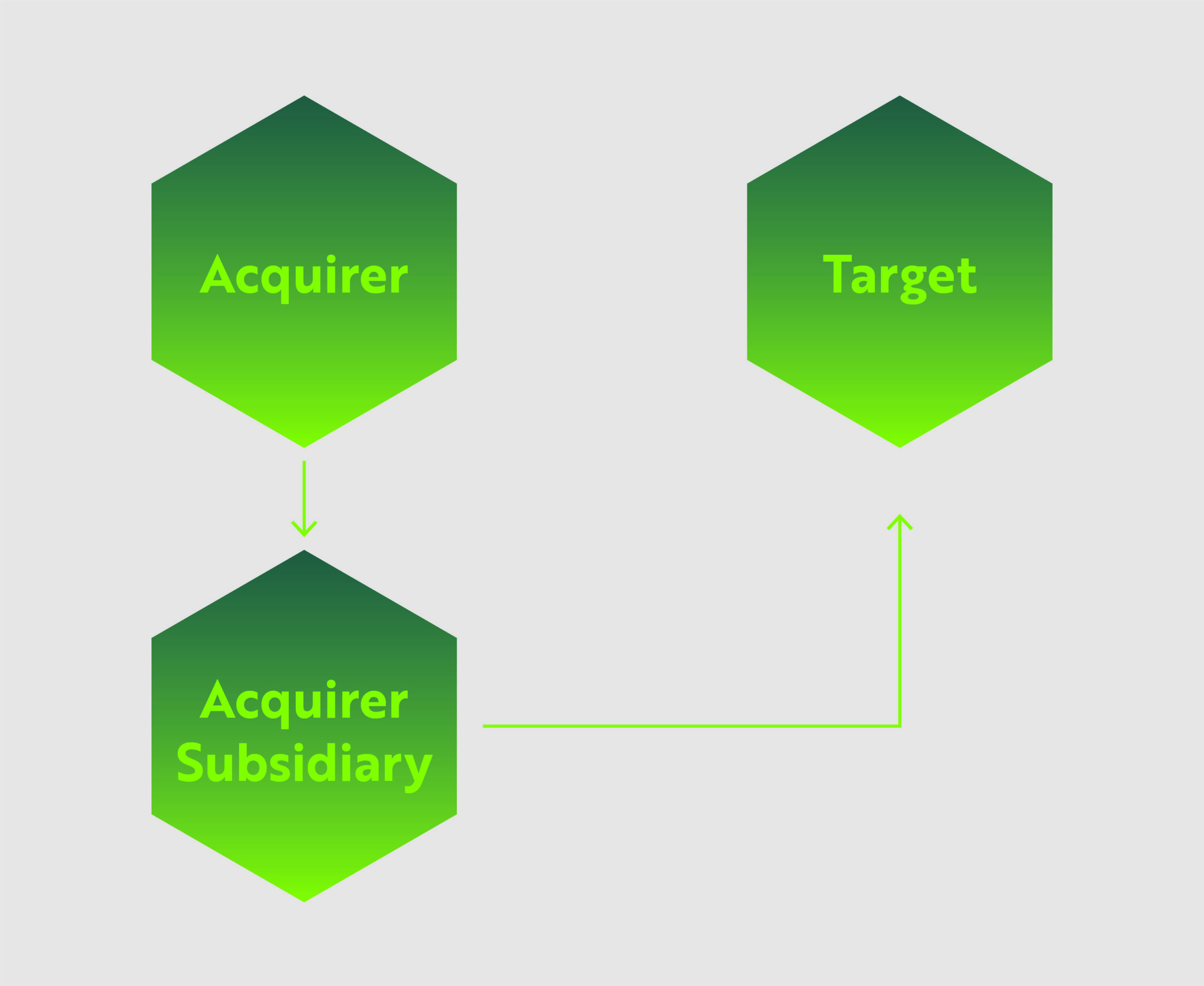

3: Reverse indirect merger

The third merger option is called the reverse triangular merger. In this deal the Acquirer uses a wholly-owned subsidiary to merge with the Target company. In this instance, the Target company is the surviving entity.

This is one of the most common merger types because not only is the Acquirer protected from certain liabilities due to the use of the subsidiary, but the Target company’s assets and contracts are preserved. In the cannabis industry, this is particularly advantageous because Acquirers can avoid a lot of red tape when entering a new market by simply taking up the licenses and business deals of the Target company.

Advantages/Disadvantages

Transfer of Liabilities: In option #1, the acquirer assumes all liabilities from the Target company. Options #2 and #3, provide some protection as the use of the subsidiary helps shield the Acquirer from certain liabilities.

Shareholder/Third Party Consent: Mergers can be performed without 100% shareholder approval. Typically, the Acquirer and Target company leadership will determine a mutually acceptable stockholder approval threshold.

Options #1 and #2, where the Target company is ultimately dissolved, will require re-negotiation of certain contracts and licenses. Whereas in option #3, as long as the Target company remains in operation, the contracts and licenses will likely remain intact, barring any “change of control” conditions.

Tax Impact: Ultimately, the tax implications of the merger options are complex and depend on whether cash or shares are used. Some mergers and reorganizations can be structured so that at least a part of the sale proceeds, in the form of acquirer’s stock, can receive tax-deferred treatment.

In conclusion

Each deal structure comes with its own tax advantages (or disadvantages), business continuity implications, and legal requirements. All of these factors must be considered and balanced during the negotiating process.

Catch up on previous articles in this series and see what’s coming next…

]]>The trade-off is greater public and regulatory scrutiny, and often, fundamental changes to the way a business operates. We’ve assembled this guide to layout the roadmap for a successful IPO. Utilizing experience gained from years of developing registration statements, auditing and preparing financial statements, and conducting due diligence, we present the core steps and concepts required. The IPO process is complex, resource-intensive, and pocked with pitfalls to the unprepared.

]]>