- The IRS has intensified enforcement of transfer pricing regulations, significantly increasing potential penalties.

- Organizations can reduce exposure to transfer pricing penalties by ensuring adequate documentation and applying global transfer pricing policies consistently.

- In cases where penalties are imposed, businesses can seek penalty abatement by demonstrating reasonable cause and good faith, substantial compliance with transfer pricing rules, and leveraging effective representation from knowledgeable tax advisors.

~

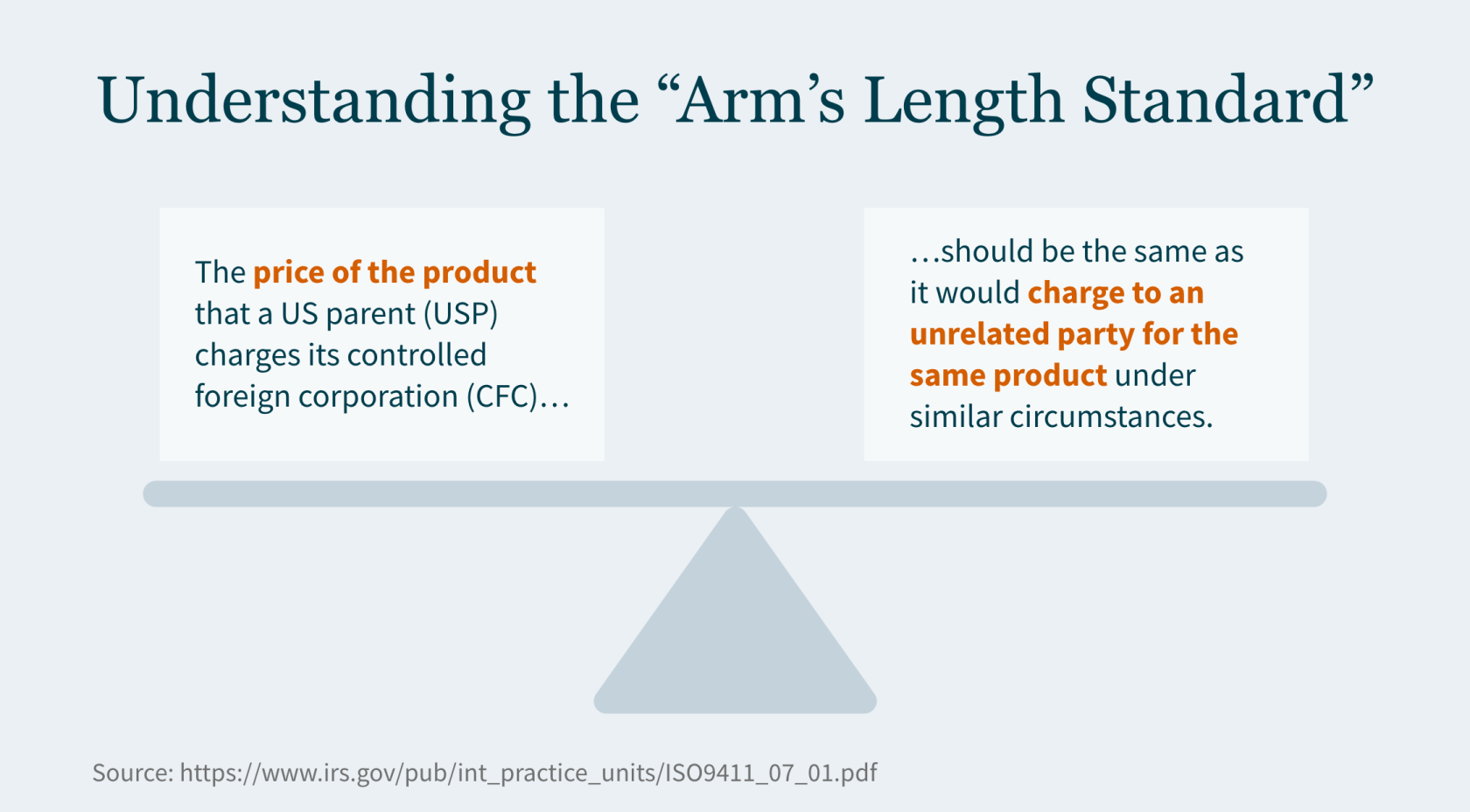

The Internal Revenue Service (IRS) implemented transfer pricing penalties to ensure the intercompany pricing reported on your income tax return is determined in a manner consistent with the arm’s length standard.

Until recently, penalty assessments were rare — not because improper transfer pricing between related parties was rare, but because IRS examiners tended to accept inadequate documentation. That leniency appears to be a thing of the past.

The IRS has indicated it will focus on applying Internal Revenue Code (IRC) Section 6662 penalties where proper documentation is lacking. This trend warrants serious attention if your company engages in cross-border transactions.

Imposing Transfer Pricing Penalties

The IRS can impose penalties when allocations under Section 482 result in substantial or gross increases in taxable income or where there are substantial or gross valuation misstatements concerning the transfer prices themselves.

These penalties can be severe, ranging from 20% to 40% of the tax underpayment, depending on the degree of non-compliance and the taxpayer’s disclosure of relevant information.

Historically, you could avoid these penalties by demonstrating you had reasonably used a transfer pricing method outlined in Section 482 or another method to more reliably determine transfer prices. Taxpayers must also provide contemporaneous documentation within 30 days of a request from the IRS.

The IRS’s Shift Toward Increased Penalty Assertion

The IRS Advisory Council’s 2018 Report noted that, although some transfer pricing documentation quality possibly fell short of the Section 6662 requirements, the IRS had not consistently asserted the penalty. Since then, the IRS has produced guidance addressing common flaws in transfer pricing documentation and best practices, and the agency is now expressing a renewed commitment to applying penalties more frequently and vigorously.

Holly Paz, commissioner of the IRS Large Business and International Division, spoke at several tax practitioner events in late 2022 — including the AICPA’s National Tax Conference, the American Bar Association Section of Taxation’s Philadelphia Tax Conference, and a Bloomberg Tax event. During these events, Paz noted the IRS has had success in litigating transfer pricing cases and is taking a closer look at economic substance and sham transactions — even in cases with transfer pricing documentation — to determine where it is appropriate to assert penalties.

Mitigating Exposure to Transfer Pricing Penalties

In 2020, the IRS published Transfer Pricing Documentation Best Practices Frequently Asked Questions (FAQs). These FAQs point to several features of proper documentation IRS agents look for when determining whether the agency should audit an organization’s transfer pricing methods.

Incorporating these features into your documentation may help reduce your risks:

- Sensitivity analysis – Assess the impact of removing a comparable company from the dataset and determine if such removal alters your position relative to the arm’s-length range. Evaluate how different profit-level indicators might change the results.

- Segmented financial data analysis – Examine if the segmented financial data accurately reflects the arm’s-length nature of the intercompany transaction. Detail the methodology used in constructing this data.

- Profit allocation in intercompany transactions – Analyze profit distribution among entities in the transaction. Ensure equitable economic outcomes for all parties, not just the tested party.

- Description of risks and related-party allocations – Describe associated risks in each intercompany transaction. Explain how profits and losses are allocated among related parties.

- Atypical business circumstances – Identify any unusual business conditions affecting the intercompany transaction. Discuss challenges in the economic analysis due to specific business results for the year.

To navigate this heightened scrutiny, taxpayers must take a proactive approach to document pricing transfer decisions. Steps you can take to avoid commonly seen inadequacies include:

- Providing a detailed description of your business and industry to help IRS agents understand operations and the larger marketplace in which you operate.

- Avoid using a checklist format. Instead, opt for a comprehensive analysis linking facts to the analysis. Base the analysis on well-supported facts, avoiding broad assumptions about the business.

- Ensure consistency in risk allocation with intercompany agreements. Align risk allocation with the comparable companies used in the economic analysis, and clearly explain any adjustments made to comparable companies for risk considerations.

- Prepare a best method selection analysis that justifies rejecting alternative methods for analyzing the intercompany transaction and provides a rationale for the chosen method.

- Clearly outline any adjustments to comparable data, such as working capital or location savings adjustments.

If you believe you have valuation misstatements or understated income tax in previously filed returns, it’s not too late to correct them. Filing a qualified amended return before the IRS contacts you about a transfer pricing audit is a defense against penalties. However, you must pay all taxes associated with the amended returns.

Seeking Penalty Abatement

In instances where penalties are assessed, it may be possible for taxpayers to seek abatement by demonstrating high-quality transfer pricing documentation. You may have a reasonable chance of having penalties abated if you:

- Demonstrate reasonable cause and good faith. Establish that the underpayment was due to reasonable cause, and you acted in good faith.

- Substantial compliance. Show that, despite any errors, you substantially followed the transfer pricing rules.

How We Can Help

The resurgence of transfer pricing penalties is an opportunity to reassess your transfer pricing strategies and compliance mechanisms.

For personalized guidance and assistance navigating these complexities, contact MGO today. Our team of professionals is equipped to help you mitigate risks, confirm compliance, and effectively manage any disputes with tax authorities. Act now to safeguard your business against the pitfalls of transfer pricing penalties.

]]>- State tax authorities are escalating audits of intercompany transactions, as transfer pricing crackdowns in several states are generating millions in tax revenue.

- These state initiatives indicate growing regulatory emphasis on transfer pricing, which may encourage more aggressive audits (especially if budgets tighten).

- Companies operating across state borders should take proactive steps, like conducting transfer pricing studies to validate policies and strengthen defenses before audits strike.

~

A recent Bloomberg article affirms state tax authorities are ramping up audits of intercompany transactions at multistate corporations. The report points to an increase in audits in three “separate-reporting” states following transfer pricing settlement initiatives as a beacon of audit activity to come across other states that take this approach.

While not ideal for multistate operators, this development may not come as a surprise to companies with international operations who have dealt with a myriad of cross-border tax issues in recent years. Close observers of state and local tax (SALT) developments have been predicting for many years the potential that states will be adopting similar positions with respect to transfer pricing. In a 2022 article focused on SALT transfer pricing enforcement, we highlighted several key indicators that more state transfer pricing audits could be on the horizon – including state budget deficits, a surge in auditor and consultant hirings, and renewed interest among states in collaborating on multistate audits.

With confirmation that state-driven transfer pricing audits are on the rise, it is imperative for corporations operating across state borders to assess your transfer pricing risks and fortify your documentation and audit defense strategies.

Surge of Transfer Pricing Audits in Separate-Reporting States

According to the Bloomberg Tax report, the recent spike in transfer pricing audit activity has predominantly affected Southeastern states categorized as separate-reporting states. Currently, there are 17 separate-reporting states in the United States. With the exception of a handful of states like Indiana, Pennsylvania, Iowa, and Delaware, most separate-reporting states are located in the Southeast region.

How separate-reporting states differ from other states in their taxation approach to corporations:

- In separate-reporting states, each corporation within an affiliated group is required to file its individual tax return. This treatment considers them as separate entities with independent income, recognizing intercompany transactions, and allowing for varying tax liabilities.

- In contrast, combined-reporting states require or allow affiliated corporations within a corporate group to file a single tax return, treating them as a unitary business with shared income, often eliminating intercompany transactions.

Notably, two Southeastern states, Louisiana and North Carolina, have recently concluded audit resolution programs that significantly boosted their state revenues. Louisiana’s program generated nearly $38 million, while North Carolina’s efforts resulted in more than $124 million. Meanwhile, New Jersey, a Mid-Atlantic state that abandoned separate reporting in favor of combined reporting in 2019, is in the midst of a transfer pricing resolution program that has already collected almost $30 million. The success of these programs in collecting tax revenue is likely to motivate other states to explore similar initiatives.

The success and subsequent expansion of these programs signify a growing emphasis on transfer pricing at the state tax authority level. State tax agencies are enhancing their knowledge and enforcement activities in this domain, giving auditors more confidence to adjust returns in transfer pricing disputes. This increasing competency may be viewed as a valuable tool by states – both those requiring separate and combined reporting – that are seeking ways to augment revenue streams.

Strengthen Your Transfer Pricing Defenses Before State Audits Strike

To preemptively safeguard your business from a state transfer pricing audit, a proactive approach to validating pricing policies is essential – and a comprehensive transfer pricing study is your primary defense.

Here are three key advantages of conducting a transfer pricing study:

- Document Your Transfer Pricing Policy: A transfer pricing study provides robust documentation that can counter inflated tax assessments by identifying key intercompany transactions, referencing benchmark data, and highlighting any deviations that necessitate policy adjustments. Even if your company has undertaken prior studies, annual updates are indispensable to align with evolving business landscapes and provide tax penalty protection.

- Mitigate Your Risk: Beyond reducing audit risks and potential liabilities, these studies also play a pivotal role in supporting major corporate events like mergers and acquisitions (M&A). By demonstrating pricing compliance, they ensure that domestic affiliates have robust documentation and effective cost allocation analysis, thus preventing over-taxation or under-taxation.

- Ensure Consistency: Minimize uncertainty by achieving uniform entity-specific compensation across state agencies and affiliated entities. Swift collaboration with advisors when audits arise enhances dispute resolution capabilities.

As states continue to gain confidence in challenging transfer pricing, multistate corporations must take proactive measures to ensure the resilience of their intercompany transactions under intensified scrutiny.

Get Ahead of the Game with a Transfer Pricing Study

If your company engages in substantial intercompany transactions across state lines, initiating a review of your current pricing policies, preparing your transfer pricing policies, and ensuring compliance with U.S. transfer pricing rules should be a top priority. Proactive measures can help you stay ahead of potential issues before state auditors come knocking. We have a robust transfer pricing team that works closely with our State and Local (SALT) Tax and Tax Controversy practices. Through a combined effort we can support you through every stage of managing a transfer pricing audit. Talk to our transfer pricing professionals today to find out how we can help you minimize your exposure to transfer pricing audits.

]]>- Recent global events have emphasized the need for reviewing and strengthening the supply chain for manufacturers from both an operational and cost savings perspective.

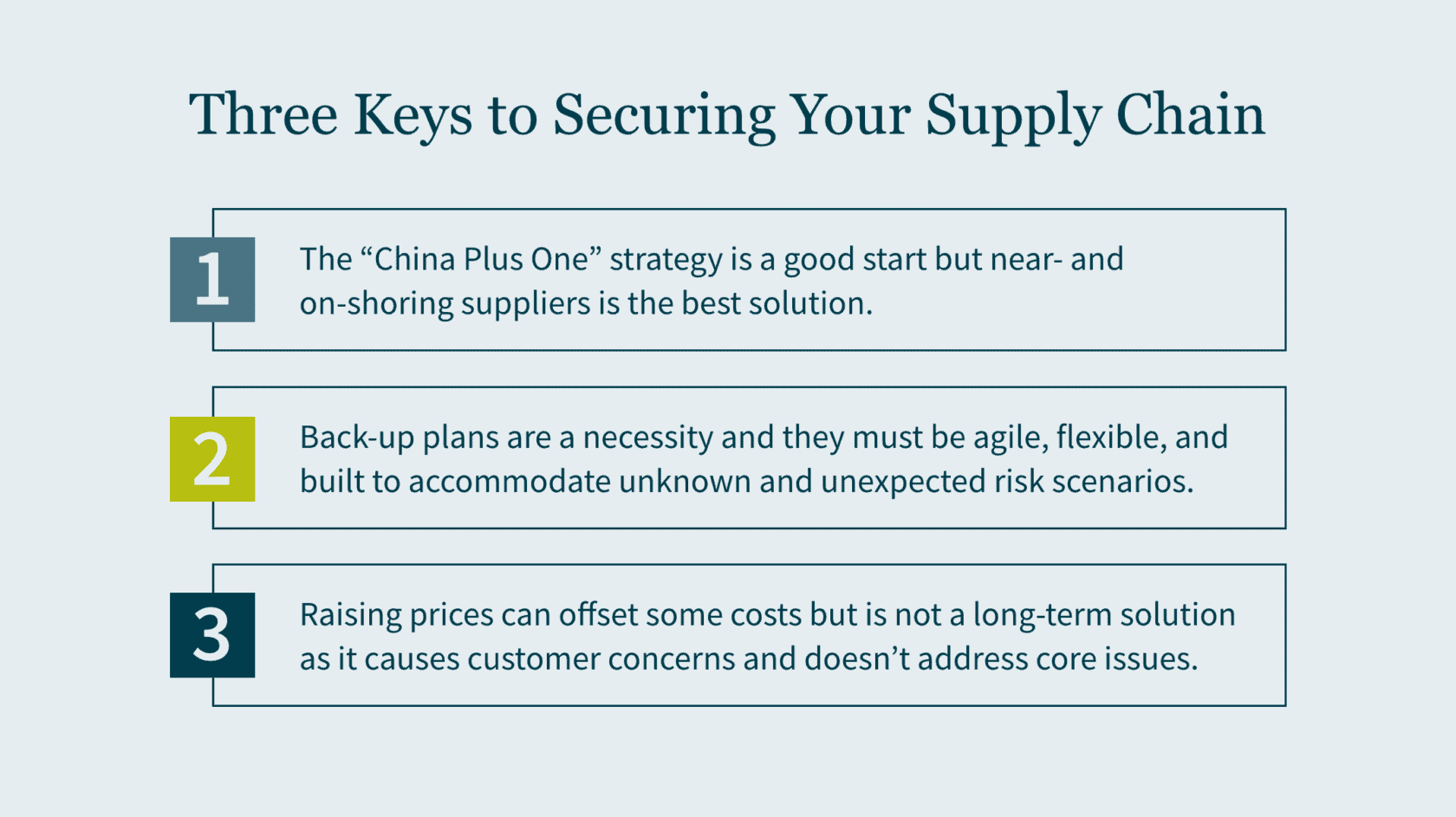

- A “China Plus One” strategy is a good start but may prove inadequate depending on the nature of a disruption.

- Supply chain backup plans need to be agile, flexible, and built with contingencies for undetermined issues.

- Raising prices may address some concerns but also causes customer issues and is not a long-term solution.

During the COVID-19 pandemic, organizations across different trades and industries faced a number of operational obstacles caused by supply chain disruptions. From economic uncertainty, to labor shortages, to rising costs, leaders had to find alternatives to create an agile and adaptable framework for this ever-changing market. With the global tax overhaul where juristidictions are racing for the middle and not the bottom, companies are faced with continuous change.

Our International Tax and Transfer Pricing leaders have developed methods and problem-solving techniques for local and global networks. These approaches help businesses address their supply chain challenges, as well as give guidance on how to continually evaluate and adjust their strategic initiatives while considering tax and transfer pricing risks in their supply chain decisions. The proverbial tax tail should not wag the dog but it should not be ignored either. Companies should consider performing transfer pricing analyses to determine how to allocate the financial impact of the changes to the supply chain among related entities and ensure appropriate remuneration to those entities involved in supply chain initiatives for their respective functions performed and risk incurred in the process.

In this article, we will answer three of our most-asked questions and provide the necessary steps to transform and optimize supply chains amid constant uncertainty — now and in the future.

#1: Can adopting the “China Plus One” strategy diversify my supply chain?

In recent years, most U.S.-based businesses and consumers have learned that global supply chains have become too dependent on China. Prior to 2020, business leaders had already begun shifting away from China in the wake of the previous administration’s tariff challenges, intangible property (IP) disputes, and the ensuing trade war. Factory and port shutdowns in China in the early days of the pandemic and the issues that have followed were wakeup calls for those that hadn’t implemented alternative sources of supply. An enduring lesson of the past few years is that sole sourcing from any vendor or vendors in one location comes with a high-risk level. In renewing the supply chain, companies must consider the economic climate, the political environment, the ease of doing business, and personnel availability. Tax and transfer pricing is generally not in the forefront nor should it be. But giving it some thought after consider the already mentioned items may pay significant dividends.

Building redundancy into the supply chain at different tiers and maintaining inventory levels have become necessary steps for international manufacturers.The China Plus One strategy has been on the radar of companies that operate in China for several years, but the need to diversify supply chains is now a priority, with many manufacturers actively pursuing supplementary sourcing from another country in Southeast Asia. However, the supply chain crisis of the past two years shows this strategy may also be failing. As long as the goods produced are an ocean away from the markets that consume them, uncertainty from various disruptive factors can lead to shortages, higher costs, lower revenues, and customer dissatisfaction.

Actions moving forward:

Along with decoupling from China, truly de-risking the supply chain comes down to three factors:

- Optionality

- Redundancy

- Market proximity

While fully onshoring production and supply sources may not be operationally, economically, or logistically feasible, the supply network is less risky when it is closer to the market where it is widely consumed.

Consider engaging or contracting new stateside suppliers and local manufacturers to better serve the U.S. market. You should also review your supply base for any overreliance on a single source or geography. After that, you can research the best options to decrease the distance between where your products are produced and purchased. Insourcing, onshoring, nearshoring and acquisitions are all viable options. The approach that makes sense for your business must consider cost, capacity, quality, control, and reputation. Regardless of your approach, the goal should be to improve supply chain resilience and flexibility so you can better manage disruptions.

#2: Does having a back-up plan reduce supply chain disruptions?

Preparation and readiness may help with how your company fares during industry interruptions. A back-up plan should have built-in agility so it can be adapted and activated quickly based on a variety of external factors.

In recent years, manufacturers learned static backup plans were not adequate to address rapidly changing global conditions. These backup strategies were not agile enough to be effective amid complex disruption. Consequently, manufacturers were challenged to get the level of service they needed from existing suppliers or quickly identify new suppliers, resulting in processes that simply were not feasible from an implementation or sustainable cost standpoint.

Backup plans are a necessity, but they’re generally based on known risks. As global supply chains grow more intertwined and the universe of uncertainty expands, new risks and variables come into play. You can’t just plan for one contingency; you need to weigh the possible outcomes for multiple options across different scenarios. Changes in manufacturing locations and sourcing strategies aren’t the only scenarios worth evaluating, nor is resilience to disruption the only outcome worth measuring. For example, if you’re considering expanding into a new market or adding to your product mix, those strategic adjustments should be factored into your supply chain model and assessed for plausibility. Tax liabilities, trade compliance risks, and total cost to serve are no less critical considerations than deliverability or lead times.

The reality is you cannot prepare for every contingency, so scenario planning needs to evolve to detect signals of disruption earlier and enable greater agility in supply chain decision-making when the unexpected occurs. For example, if your company is planning on vertical integration thath will be the cause of significant in-country hiring, you must assess the benefits of employment credits and incentives that can help reduce overhead costs.

Actions moving forward:

Review your supply chain model to:

- reflect current constraints;

- incorporate points of vulnerability; and

- conduct a scenario planning exercise to address a specific problem or inform your next strategic move.

Ideally, you should simulate multiple scenarios to pressure test the supply chain, anticipate issues, and chart the best path forward when disruption hits. Scenario planning should become a regular business practice so you can quickly respond to unforeseen events.

#3: Will raising prices offset the increasing costs of materials and logistics?

Although raising prices is not the only way to successfully reduce costs, there are some tradeoffs that will have to be considered. Higher costs are an unfortunate reality for most manufacturers in the current supply chain environment. Because cost reductions are not easy to accomplish, many companies are shifting their focus to cost containment within areas of their supply chains that they can control. Higher costs are a sure way of reducing taxable income and where possible, selectively deciding where the spend will occur in the supply chain may not reduce the impact of inflation or costs being spent – however it may impact the amount of tax dollars being spent. Tax, like all other costs, is an expense that should be viewed and considered for cost reduction measures.

For example, intercompany movements are often rife with inefficiency or seldom get the level of scrutiny they deserve. If parts and finished goods are shipped intercompany, ask why: Is there a value add, is it because your business has always done it that way, or is it an enabling factor to hedge against process inefficiencies? If your global supply chain is failing to consistently meet the needs of local markets, does the original rationale for keeping production and sources of supply at a distance still stand? Or would it be beneficial to establish a near or local market capability? Using models like a contract manufacturer can be a quicker way to further evaluate whether it makes sense to establish an in-house capability.

It’s also a good time to revisit lean initiatives that you may have previously dismissed or deprioritized—though be cautious of prioritizing efficiency at the expense of resilience. And beyond your own four walls, there are a few foundational measures of good supply chain hygiene that may help with cost takeout:

- Shift from transportation spot rates to contract rates to stabilize pricing.

- Ensure you have contracts with alternate suppliers; don’t rely on a single source.

- Encourage your customers to optimize order volume for full truck or container loads through more rigorous enforcement of transactional service standards.

These measures may help manage costs to some degree but are unlikely to completely offset them. By raising prices, you will more than likely create frustration and confusion among your customers. However, if you find yourself absolutely needing to raise prices, it’s better to be upfront and honest rather than taking a below-the-radar approach.

Another way to address rising costs, rather than passing additional costs onto all your customers, is to consider segmenting them and developing pricing strategies based on level of priority.

Actions moving forward:

Perform an in-depth analysis of your customer base and product suite to understand the most and least profitable segments. Consider implementing a price segmentation strategy that shifts the heaviest burden of cost increases to your least profitable customers. Also, take a close look at your least profitable product segments and how they line up with cost distribution. Do you have slow-moving SKUs driving a disproportionate amount of costs? It may make sense to rationalize them.

We can help strengthen your supply chain

Now is the perfect time for manufacturers to gain competitive advantage by optimizing production and delivery processes and prioritizing long-term spending goals. Our International Tax and Transfer Pricing and Management Advisory practice leaders are ready to assess your current supply chain, identify potential points of weakness, adjusting transfer pricing policies, and assist you in implementing strengthening procedures. Reach out to our team to learn how we can reduce your risk and power production.

]]>- Many international companies are struggling with their supply chain management amid external factors playing out on the global stage.

- To mitigate the challenges, you should be aware of the current trends in supply management as well as strategies to improve your resilience and flexibility.

- Current trends include AI and automation, supply chain as a service, circular supply chains, risk management and stability, and sustainability.

- Diversifying your supply chain and creating a backup plan can help you remain agile.

- Know the tax implications of your supply chain.

The last two years have seen major disruption in supply chain management — and throughout 2023, that turbulence is expected to continue. The freight supply and demand equation was a common issue during the pandemic and recovery period. We’re now seeing how the Russian-Ukraine conflict is reshaping the global supply chain for many companies. And amid all the economic uncertainty, supply shortages, and rising costs, the U.S. and EU (European Union) have been heavily investing in infrastructure, putting even more pressure on China with the U.S.-imposed tariffs’ strenuous implications.

While managing your supply chain is currently a challenge, you’re not completely at the mercy of these external factors which are generally outside of your control. There are strategies to mitigate the impact to your supply chain: your goals should be to both improve your supply chain resilience and flexibility to allow you to better manage the disruptions — those foreseen and unforeseen.

Our International Tax team breaks down some of the current trends and strategies to be aware of.

Trends in supply chain management

Some of the main trends in supply chain management include artificial intelligence and automation, supply chain as a service, circular supply chains, risk management and stability, and an increased focus on sustainability. Now, more than ever, mid-market multinational companies must be strategic. These additional constraints cause strain on these companies that are being forced to pivot to address these issues among additional disruption.

Odds are, you’ve been rethinking the way you currently manage your supply chain — because the global situations aren’t changing. The China tariffs are unlikely to disband soon, and there seems to be no end in sight to the Russia-Ukraine conflict.

Diversifying your supply chain

Many agree that the global supply chain was too dependent on China, and now companies are considering breaking away from the Asia Pacific region to look at the Mexican maquiladora or IMMEX programs. Both these programs are, for all intents and purposes, synonymous, save for one detail: the IMMEX added shelter companies as a modality. Under this shelter program, companies may set up operations in Mexico without establishing a legal Mexican entity.

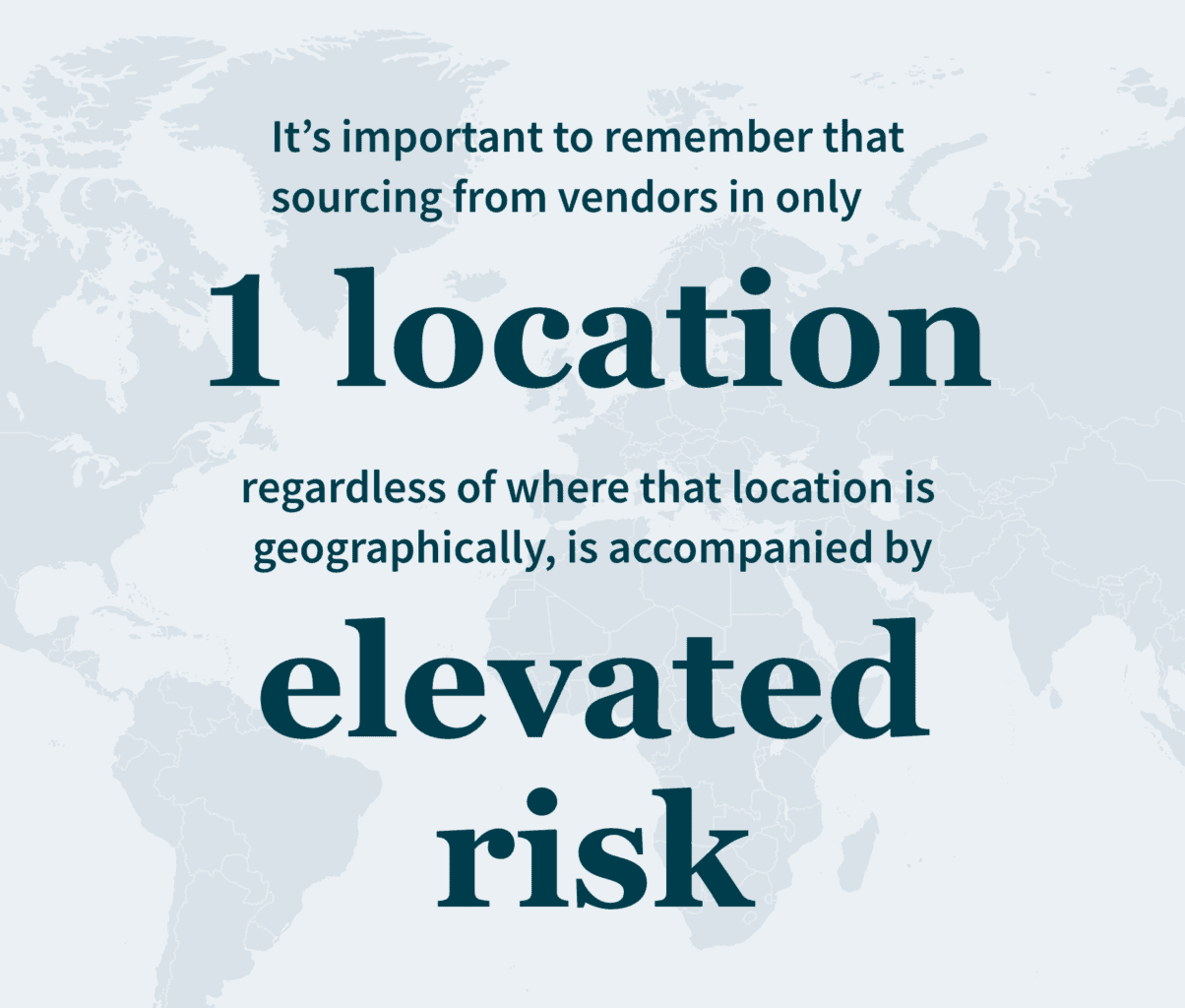

These programs have been in existence since the 1960s, so they’ve proven their worth — however, they don’t work for everyone, so it’s worth perusing other options. It’s important to remember that sourcing from vendors in only one location, regardless of where that location is geographically, is accompanied by elevated risk.

To mitigate this, you should not only diversify your supply chain but also create redundancies to avoid a single point of failure. In addition, bringing your sources of supply closer to where you operate also reduces the opportunity for risk. Engage with new suppliers and manufacturers in the Americas, for instance, and analyze your current suppliers to see if there is any one region you rely on more heavily already, then minimize the distance between your production and purchasing — without, of course, sacrificing quality, cost, control, and reputation. By optimizing your global footprint, you can maximize your production opportunities, minimize risk, and scout new vendors and locations for future efficiency.

Devising a backup plan for supply chain disruptions to address multiple contingencies

At the end of the day, we know that no matter how sophisticated or agile your supply chain backup plan is, external factors — which are never static — can affect things in unexpected ways. With rapidly and ceaselessly changing global conditions, there’s no way to account for everything you could encounter.

But there are ways to prepare. Plan for multiple contingencies, weighing their outcomes. Don’t forget to think broadly and for new opportunities — for example, if you’re looking at expanding into new markets or territories or want to add a new product line, you must assess their plausibleness under a variety of conditions (and not just logistical conditions, like lead times and delivery … but also tax liabilities and compliance, too).

Keep your supply chain planning agile and ready to evolve by reviewing its current model and updating it to ensure it reflects the restraints and vulnerabilities you’re presently dealing with. By making a step-by-step plan — for multiple scenarios — you can chart your path forward, regardless of what unfolds on the global stage in these uncertain times.

How MGO can help

Knowing the tax implications of your supply chain is crucial to your global success, and our experienced International Tax team can help you navigate the supply chain turmoil — no matter how turbulent. By reviewing your current supply chain model to determine where your processes can be strengthened and made more efficient, as well as pinpointing your vulnerabilities, we can help you hone your supply chain’s true potential while safeguarding it against whatever comes next.

About the authors

John Apuzzo is the leader of our International Tax Practice. He supports public and private companies, and high-net-worth individuals, as they conduct business on the global stage. His passion for developing optimal tax strategies helps his clients reinvest in their businesses and enjoy the wealth they have worked so hard to earn.

Mandy Li is a transfer pricing partner and provides strategic and tactical transfer pricing solutions to public and private multinational organizations. She supports highly complex global engagements, with an emphasis on transactions moving to and from the China region.

]]>- Companies face tax burden challenges related the classification of cannabis as a Schedule I controlled substance and IRC 280E.

- To navigate this, companies may be able to utilize vertical integration strategies and incorporate transfer pricing best practices to minimize tax exposure.

- A transfer pricing study will help identify and risks or opportunities for improvement.

As the cannabis market continues to grow, in the United States cannabis operators continue to face difficulties related to an excessive tax burden due to IRC 280E. One of the most effective strategies for mitigating tax exposure under 280E has been to leverage the benefits of vertical integration.

Since IRC 280E affects the various verticals differently, some cannabis companies are able to isolate activities within distinct business units and maximize Cost of Goods Sold (COGS) calculation to mitigate the impact of IRC 280E.

The potential downside is two-fold. First, IRS tax court cases have made it clear that isolating business units is not a universal solution. And secondly, if not optimally established and documented, transactions between the business units can be problematic and create issues with the IRS.

This article breaks down the impact of IRC 280E, demonstrates the potential benefits of vertical integration, and describes how a proactive transfer pricing strategy can help you maneuver the specific tax and regulatory considerations that affect the industry.

What IRC 280E means for your tax liability

Section 280E penalizes traffickers of Schedule I or II drugs by prohibiting the deduction of “ordinary and necessary” business expenses after reducing gross receipts by COGS, essentially resulting in your federal income tax liability being calculated based on gross income, not net income. For a cannabis operator, COGS typically consist of the cost of acquiring inventory by purchase or production.

Not only are these cannabis companies facing high federal taxes, but there is now an intense level of scrutiny in both federal and state tax audits on intercompany arrangements.

Impact of vertical integration on IRC 280E calculations

Many cannabis companies have become vertically integrated, i.e., combining production function (i.e., cultivation and manufacturing) of cannabis with retail or resale (i.e., distribution) or sometimes all three. Since Section 280E is directly related to selling or the “trafficking” of cannabis-related products, it has the biggest potential impact on retail operations. This means that if a producer can support a higher selling price to its retailer, the retailer will have more COGS from the producer, and the producer will have more costs to deduct because of the allowance of indirect costs.

The business motivation for vertical integration is to better control the supply chain and the end user’s experience. From a tax perspective, cannabis taxpayers want to dis-integrate activities subject to 280E from those for which a position can be argued that they are non-280E activities, such as management services. The Internal Revenue Service (IRS) uses transfer pricing to challenge such segregation and to make allocations between or among the members of a controlled group.

How a transfer pricing study can help your cannabis business

Whether its receives the recent budget infusion or not, the IRS is likely to conduct more transfer pricing audits of the cannabis industry, compared to other industries. These audits frequently result in much higher tax adjustments and significant penalties. In addition, since several states have had budgetary shortfalls due to COVID-19 and other factors, multistate businesses are more frequently being audited by individual states’ tax authorities. If your business has international or domestic intercompany transactions, you’re facing a difficult and uphill battle amid current local, state, and federal tax regulations. The best defense against an IRS transfer pricing audit is a comprehensive transfer pricing study.

A robust transfer pricing study provides the basis with which a company can refute and push back against federal and state claims that their intercompany transactions have no economic or operational substance. As part of a transfer pricing study we will work with you to identify key classes of intercompany transactions, document the pricing of such transactions and reference comparable benchmark data sets to support qualifying transactions. Where transactions fall outside norms, we will work with you to identify differentiating characteristics and seek other data if available, or recommend policy and pricing changes, along with an assessment of the potential exposure.

Taxpayers with inadequate or out of date transfer pricing policies risk an increased likelihood of controversy and transfer pricing adjustments. Thus, even if you have had a transfer pricing study performed in the past, it is important to have it reviewed and updated.

While a transfer pricing study directly reduces a company’s risk of tax assessments and liabilities resulting from tax audits, they also indirectly reduce execution risk when a company is considering an M&A transaction, a capital raise, or go public transaction.

How MGO can help you integrate transfer pricing for the cannabis industry

MGO’s transfer pricing practice has significant experience with the various transfer pricing concerns of the cannabis industry. We also work closely with our federal and state tax practices to assist many cannabis companies with their specific tax and regulatory considerations, which include:

- Section 280E disallowance of ordinary business expense deductions;

- Common supply chain concerns for operators, like state restrictions on inventory and separation of cannabis and industrial hemp;

- Non-plant-touching structures that operate independently from the 280E-affected business lines; and

- Sales and excise taxes specific to the cannabis industry.

To learn more about how we can help support establishing, optimizing, and documenting transfer pricing policies so your business can grow in this dynamic industry, contact us.

]]>State and local enforcement is increasing and states are hiring

The number of state transfer pricing audits has significantly increased in the past few years, and state tax authorities are adding transfer pricing resources, including auditors and outside consultants, even throughout the COVID-19 pandemic.

As a result of the potential for increased revenue, there has been renewed interest in collaboration among state tax authorities on transfer pricing. The State Intercompany Transactions Advisory Service (SITAS) of Multistate Tax Commission (MTC) was established in 2014 to unite those states interested in transfer pricing, encourage information sharing among them, and train groups for transfer pricing audits. With little interest at the time, the group stopped convening in 2016, but in 2021, it has re-emerged with renewed state interest in information sharing when it comes to multi-state audits. MTC is working on multiple initiatives for transfer pricing collaboration among states. It promotes the exchange of taxpayer information, which permits the states to collaborate on audit, compliance, enforcement, and litigation activities. MTC is also drafting a proposed white paper on the taxation of digital products and processes.

Indiana, North Davidina, and Louisiana are among the states that are leading efforts in state transfer pricing dispute resolution. Indiana introduced an advance pricing agreement (APA) program in 2020 to offer taxpayers an avenue for resolving existing and potential transfer pricing disputes with the state directly. An Indiana APA covers two three-year audit cycles. The Indiana Department of Revenue (DOR) also goes to pre-audit years if net operating losses are involved — not to make assessments for those years but to adjust the NOL carryover deduction that comes into the audit years. In July 2021, Indiana DOR officially proposed bilateral APAs in separate-reporting states.

In 2020, North Davidina announced an amnesty program for taxpayers to voluntarily disclose state transfer pricing positions and reach agreements with the state on intercompany pricing without facing additional penalties. This effort resulted in roughly $100 million in tax revenue collected from more than 100 participating taxpayers through the program. Similarly, in October 2021, the Louisiana Department of Revenue invited eligible taxpayers to participate in a voluntary initiative, the Louisiana Transfer Pricing Managed Audit Program, which aims to resolve transfer pricing disputes. It is anticipated that other state tax authorities will also develop similar programs to those in Indiana, North Davidina, and Louisiana to boost their tax revenues.

Transfer pricing issues can arise when there are transactions between two or more members of a unitary group. While most states require or permit “combined” reporting, under which affiliated entities conducting a unitary business file a group return that includes entities with out-of-state activities (and eliminates many intercompany transactions), seventeen states use “separate” reporting, which finds each entity filing its own return regardless of corporate affiliation. In both “combined” and “separate” reporting jurisdictions, transfer pricing can become an issue, but particularly in separate reporting states, the taxpayer’s separate-company taxable income can be directly affected by the pricing of transactions between the taxpayer and any domestic or foreign affiliates with out-of-state activities. And even in “combined” jurisdictions, state tax authorities may review the transfer price of transactions between related companies – both domestic and sometimes even foreign entities, depending on the state’s “water’s-edge” rules for including non-U.S. affiliates – to identify potential abuse of intercompany pricing (e.g., by overvaluing expense deductions or under-reporting income).

What the state and local tax authorities are looking at

At the federal level, transfer pricing is governed by the regulations promulgated under Internal Revenue Code (IRC) section 482 based on the rules of the arm’s length standard, which requires that the results of intercompany transactions be consistent with the results of comparable transactions between unrelated entities. Most states have adopted some form of the federal transfer pricing rules under IRC section 482. For example, Utah and Indiana have codified the language of IRC section 482 in the state statute.

State and local tax authorities are not bound solely to the arm’s length standard and are free to assert their own transfer pricing requirements. Intercompany transactions are often scrutinized at the SALT level in accordance with concepts like economic substance and business purpose, and in key focus areas such as royalties, debt, management or franchise fees, insurance, expense deductions, and allocations. The concepts are either derived from base erosion and profit shifting (BEPS) or incorporated into the state regulations.

The tools available to the state tax authorities to tackle transfer pricing issues include adopting IRC section 482, forced combination, alternative apportionment, related party expense addback, and asserting nexus with the out-of-state entities.

Under audit, states generally have the authority to require taxpayers to file on a combined basis on audit, or to use an alternative apportionment methodology. In addition, some states disallow certain deductions for expenses between related parties and require businesses to add back the deductions to their income.

When state tax authorities have deviated from IRC section 482, they have faced resistance to their transfer pricing approaches. Some recent court cases have sided with taxpayers and determined that state lacked sufficient support to claim that separate returns do not accurately reflect taxpayer income or that transactions lack economic substance. State revenue authorities have also been required to adhere to more standardized transfer pricing rules and practice when applying the state versions of IRC section 482. As a response, state tax authorities are actively engaging transfer pricing economists and professionals to boost their efforts against tax losses from intercompany pricing.

How to defend your transactions: taxpayer best practices

For transfer pricing among domestic affiliates, transfer pricing documentation is the best defense to support intercompany transactions. Companies anticipating significant intercompany transactions should prepare a transfer pricing study to document those transactions. The transfer pricing study should be completed contemporaneously with the completion of the tax return to provide penalty protection in case of transfer pricing adjustments.

Companies should closely examine their operations and determine the amount and details of all current and anticipated intercompany transactions, as well as try to avoid any single entity over- or under-paying taxes in any given state by valuing and compensating each affiliated entity for its relative contribution to the success of the business. Appropriate cost allocation analysis helps to ensure that revenue and expenses are allocated to the correct entities based on the contribution of each entity to the business.

Consistency is key for companies preparing a transfer pricing study and should ensure consistency across state revenue agencies. It is also crucial for taxpayers to ensure consistency in intercompany agreements, transfer pricing policies, and documentation to minimize audit risks. Businesses should have intercompany agreements in place and keep them up to date. It is important to incorporate transfer pricing as an integral part of the company’s business and tax planning process. Appropriate transfer pricing policies and documentation must be reviewed/updated periodically to reflect the new economic and business environment.

When facing state audits related to intercompany transactions, companies should work closely with their tax advisors to actively respond to requests from tax authorities to avoid prolonged audit processes and mitigate adjustment and penalties. Companies should also explore dispute resolutions such as state APA and voluntary disclosures for existing and future intercompany transactions to reduce tax uncertainties and associated costs.

How we can help

This area is complicated and filled with potential pitfalls. We are here to guide you – whether it’s to review your intercompany transactions and determine arm’s length pricing, help establish your transfer pricing policy, or represent you in an IRS audit. MGO’s SALT and Transfer Pricing teams are highly experienced and can guide you through best practices in these various areas. Reach out to our team of professionals to help protect your business.

]]>OECD BEPS 2.0 overview

The OECD/G20 Inclusive Framework on BEPS released Blueprints on Pillar One and Pillar Two. The Blueprints address the tax challenges of the digitalization of the economy and propose fundamental changes to global tax rules. All multinational businesses will feel the impact of the changes.

BEPS 2.0 contains two parallel elements: Pillar One would revise profit allocation and nexus rules to allocate more taxing rights to market countries. Pillar Two would establish new global minimum tax rules to ensure that all business income is subject to at least a minimum level of tax.

The application of Pillar One rules is limited to MNEs that have a consolidated revenue above €750 million ($914 million) and also have in-scope revenues outside the domestic market above a threshold that is not yet defined. The three basic elements of Pillar One:

• A new taxing right for market jurisdictions based upon a share of a business’ residual profits (Amount A)

• A fixed return for certain distribution and marketing activities physically in a market jurisdiction (Amount B)

• Enhanced dispute prevention and resolution mechanisms to improve tax certainty

What is Amount A?

Amount A grants market jurisdictions new taxing rights using a formula that is not based on the arm’s length principle. Taxing rights are based on an active and sustained engagement in a market jurisdiction rather than a company’s physical presence. The two broad sets of businesses subject to Amount A are consumer-facing businesses (CFB), and automated digital services (ADS).

The Amount A formula is made up of three distinct components:

• A profitability threshold will isolate residual profits potentially subject to reallocation.

• A reallocation percentage will define the share of residual profits (actual profits minus the profitability threshold) or allocable tax base of the market jurisdictions.

• An allocation key will be used to allocate the tax base among the eligible jurisdictions.

The Blueprint does not yet define the profitability threshold or reallocation percentage threshold, but these will be determined through additional work by the Inclusive Framework.

What is Amount B?

Amount B has two goals. First, it is intended to simplify transfer pricing rules for tax administrations and reduce compliance costs for taxpayers. Second, it is intended to reduce disputes between tax administrations and taxpayers.

Amount B attempts to set a standard baseline return for routine marketing and distribution activities. The transactional net margin method will be used to determine Amount B and the remuneration for the baseline activities. Amount B would be implemented through domestic law, and the Blueprint indicates that existing treaties can resolve disputes, but where there is no treaty in place, a new treaty-based dispute resolution mechanism may be required.

New rules establish a framework of minimum taxation for multinationals

Pillar Two Blueprint introduced several new rules to establish a global framework of minimum taxation, which only apply to MNE groups with a total consolidated revenue above €750 million.

• The income inclusion rule (IIR) operates as a top-up tax when income of controlled foreign entities is taxed below an effective minimum tax rate.

• The switch-over rule (SoR) complements the IIR by removing treaty obstacles in situations where a jurisdiction uses an exemption method that could frustrate the application of a top-up tax to branch structures.

• The undertaxed payments rule (UTPR) serves as a backstop to the IIR through application to certain constituent entities; the top-up tax computation is the same as under the IIR.

• The subject-to-tax rule (STTR) would help countries protect their tax base by denying treaty benefits for deductible payments made to jurisdictions with low or no taxation from related parties of the same consolidated group of businesses.

Biden international tax proposals

The Biden administration has responded to the OECD BEPS 2.0 and has also proposed changes for U.S. tax policy. Biden’s proposals were aimed at helping fund his $2.25 trillion infrastructure plan with a big focus on clean energy. Clearly, they were also an attempt to stabilize the international tax architecture. The proposals call for raising the current tax rate on global intangible low-tax income (GILT), to 21% from 10.5% and ending a tax break for companies exporting U.S.-manufactured goods, known as foreign derived intangible income (FDII).

The United States has proposed to OECD a simple profitability threshold to determine which companies are subject to Pillar One rules. The U.S. proposal would replace the complicated definitions the current OECD proposals use to determine which industries and business models are affected. It would affect fewer companies than the OECD proposals, without reducing how much corporate profit is reallocated. According to the U.S. proposal, it would apply to no more than 100 multinationals. For Pillar Two, the United States recently proposed a 15% global minimum tax which would put pressure on negotiators in the OECD discussion to move higher than the 12.5% they were expected to agree on.

Transfer pricing implications for MNEs

A lot of uncertainties remain. COVID-19 has had fundamental impacts on how we live, work, and do business. COVID-related spending and other economic challenges may prompt increased scrutiny from tax authorities. But some businesses may be able to turn these challenges into opportunities. Here are some strategies and practices that can make a difference:

• Plan for uncertainty. The economic and regulatory environments remain fluid, so it is critical for companies to review their business operations and transfer pricing policies more regularly and adjust along with these changes. The proposed tax rules may affect incentives regarding the location of profits and investments. MNEs should plan ahead by modeling the potential tax impacts of these new rules to quantify the effects. Reviewing financial results and making adjustments only for the year-end may trigger customs and corporate tax audits.

• Supply or value chain restructuring. Businesses need to consider both temporary and permanent impacts of COVID-19 and the new tax rules. This is critical time to review how to adapt business structure to the changing consumer behavior, supply chain dynamics, and tax policy updates. It’s also time to evaluate the digitalization of business and its tax implications.

• Add more rigor to compliance. Meeting the requirements for documentation is more critical. To minimize audit risks, it is extremely important for taxpayers to ensure consistency in intercompany agreements, transfer pricing policies, and documentation. Businesses should have intercompany agreements in place and keep them up-to-date. Appropriate transfer pricing policies and documentation should reflect the new economic and business environment.

• Talk to your tax advisors. Transfer pricing analysis can begin a healthy discussion that identifies business challenges and opportunities. Exploring your business and tax structures can help you plan for economic and regulatory uncertainties and minimize your risks.

MGO’s specialized transfer pricing team offers you the resources you need to develop a solution that is designed to meet the specific needs of your business. Contact us for more information about transfer pricing.

]]>The economic impact of the COVID-19 pandemic is having serious implications for multinational groups’ transfer prices, analyses, and documentation. In this unprecedented environment, businesses must reexamine the fundamental principles underlying their transfer pricing policies and take proactive steps to develop and ensure defensible comparable companies and benchmarks are guiding transfer pricing now, in 2020, and as the global economy ultimately recovers from the COVID-19 outbreak.

Disruption hits transfer pricing methodologies

Transfer pricing benchmarking, valuation, compliance, planning studies and accepted methodologies, such as CUPs, CPM/TNMM and even the residual profit split, hinge on applying reasonable comparable companies and these companies’ financial results to determine defensible transfer prices among and between controlled legal affiliates located across international or US state borders. Currently, COVID19 is an unexpected global market supply and also a demand shock that is impacting the balance sheets and overall profitability of comparable companies applied in transfer pricing analyses.

Most multinational and US domestic multistate firms establish their current year FY2020 transfer pricing policies and profitability metrics (gross margins, cost plus mark ups, interest rates, etc.) based on best comparable company financial data available in the most recent prior year (2019) or prior three years (2017 – 2019). This approach is the basis for OECD and UN transfer pricing guidelines, as well as US Section 482 and local country transfer pricing regulations. The key assumption underpinning these comparability analyses, most relevant in establishing current FY2020 transfer pricing policies, is that the underlying macro economy will largely remain stable and unchanged year to year.

However, the first calendar quarter of 2020 is directly challenging this underlying assumption. In the first calendar quarter of 2020, especially since March 2020, nations around the world are being challenged with “stay at home” policies, severely limited or suspended business operations, and severe reductions in their workforce to prevent the spread of COVID-19 among their communities.

COVID-19 has few historical precedents

The major difference between this unexpected COVID-19 pandemic economic supply shock and the sharp downturn in 2008-2009, is that the COVID-19 pandemic shock is being felt widely across multiple industry sectors. In comparison, the 2008-2009 shock was largely limited to the financial services and banking industries. Lehman Brothers went bankrupt and US unemployment rose to a high of 10.2% in 2009, but for the most part, the US and global workforce still had jobs and continued to work.

This is not the case in the current COVID-19 environment, which has caused severe dislocation and disruption in global supply chains and workforce. US unemployment is expected to exceed 2009 levels by May 2020.

When economic assumptions fail

COVID-19 has triggered the validity of the underlying macro-economic stability assumption behind currently-active FY2020 transfer pricing policies and operations. As a result, the actual, current 2020 financial results of comparable companies that underpin FY2019 and FY2017-FY2019 transfer pricing benchmark analyses, which are actively being applied to drive and manage multinational companies’ FY2020 transfer pricing policies in Q1-Q2/2020 — and likely for the rest of this fiscal year and into fiscal 2021 — are sorely out of step with actual business operations and depressed financial returns that the multinational firms’ tested party affiliates may currently be facing.

The comparable companies’ actual 2020 financial results may be able to inform FY2021 transfer pricing policies, but they are currently not available contemporaneously to determine the arm’s length profitability or valuation required to determine firms’ FY2020 transfer pricing policies and support operations to settle accruals and book journal entries on a quarterly or monthly basis.

What businesses can do

There are a number of available options to address this disruption, depending on how your company is being impacted by COVID-19.

Option 1: For companies experiencing or expected to experience sharp contraction in their business operations during this supply shock and into 2021:

- MGO can provide a ‘look-back’ benchmark analysis to review comparability of a companies’ profitability margins during the 2008-2011 financial downturn and analyze how these comparable companies were impacted financially during that earlier period. Each industry will be impacted differently; however, one can assume that comparable companies’ profitability (or lack thereof) during the 2008-2009 recessionary period could at least provide a ceiling for an expected range of returns among comparable companies now facing an unexpected global economic supply shock in fiscal 2020.

- MGO can review the national COVID-19 guarantees and company support payments and assess whether affiliate financials need to be adjusted to account for these subsidy measures. Inter-company markups and profit margins may trend downward as a result.

- MGO can re-examine industry competitors and assess overall comparable company impacts in the specific industries due to COVID-19. For example, we can determine whether your firm’s global sales and marketing affiliates should continue earning positive or break even returns depending on peer and industry performance.

- MGO can review and make recommendations for revising inter-company agreements that ensure optimal tax and transfer pricing risk-taking positions for controlled affiliates.

Option 2: For companies facing increased or expanded business opportunities during this supply shock (like Amazon, Costco, Medical suppliers and Pharmaceutical companies among others):

- The Commensurate with Income (“CWI”) standard could provide additional audit defense support ex-post for active FY2020 transfer pricing policies currently being applied.

- Negative economic supply shocks can be optimal opportunities to implement tax restructuring and associated shifts in IP ownership. MGO can assess international restructuring opportunities and conduct IP and business enterprise valuations for private and publicly traded firms.

Option 3: For companies in a zero or negative interest rate environment:

- The cost of accruing Payables and Receives and other working capital becomes near zero. Some of these assets and liabilities may be written off entirely, materially written down or recharacterized as debt or equity.

- Adjustments and revisions to comparable company balance sheets in fiscal 2020 and 2021 are thereby worth reviewing to ensure similar tax treatment and COVID-19-related adjustments are obtained for transactions among and between related parties.

The MGO Transfer Pricing Practice is ready to assist and provide ‘look-back’ benchmarks, revised Valuations and new Commensurate with Income Analyses. We can help ensure you have an audit-defensible position for your company’s US and global transfer pricing policies and operations, at the close of fiscal 2020 and looking ahead into fiscal 2021, that consider the economic impact of COVID-19 on your industry and firm.

To schedule a consultation, contact us today.

]]>