Executive Summary:

- Implementing basic accounting practices and understanding tax implications can help individuals working independently in creative fields gain clarity, meet obligations, and maximize income.

- Separating business and personal finances, tracking income and expenses, and budgeting for estimated taxes can help creators be proactive in their financial planning.

- Creators earning income across state lines or internationally need to be aware of varying taxation requirements in different jurisdictions.

~

Today’s artists need to view themselves as both businesses and creatives. Whether you are a painter, digital artist, photographer, website designer, YouTuber, Instagrammer, or any type of artist, creator, or influencer, understanding and managing your financial obligations is a crucial aspect of sustaining a thriving career.

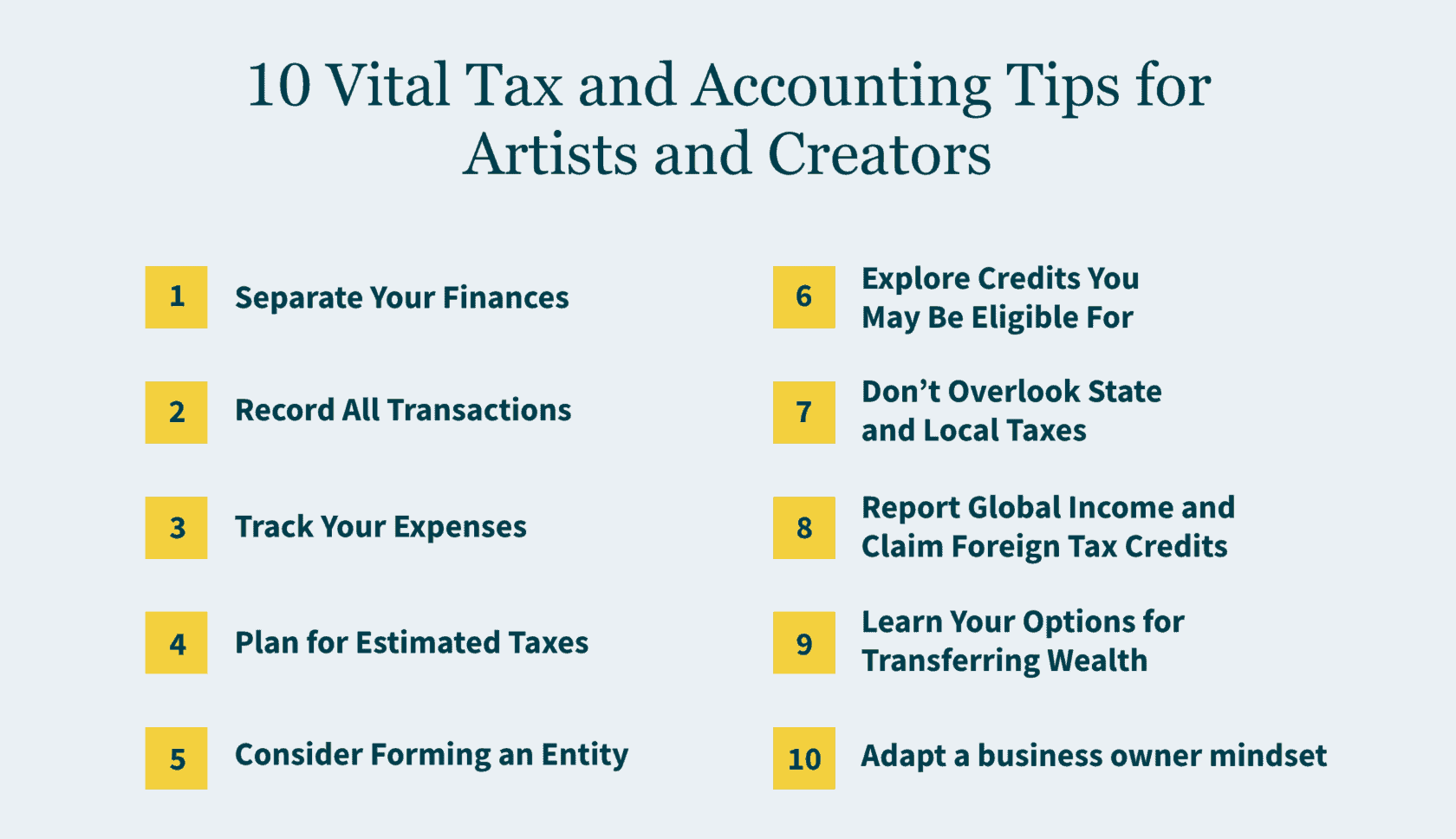

Here are 10 tips to help you meet your tax reporting responsibilities and get the most from your hard-earned income:

1. Separate Your Finances

To make your accounting more efficient and streamline the tax-filing process, it is a smart idea to separate your business and personal finances. Designate a dedicated business account to track income and expenses related to your artistic endeavors. This separation not only simplifies tax reporting but also enhances financial clarity, making it easier to assess the overall health of your creative enterprise.

Tip: Establish a separate account for business transactions, or multiple business accounts to allocate money for categories such as expenses, taxes, and savings.

2. Record All Transactions

Sometimes it can be challenging to determine what constitutes income. That’s why it’s important to track everything. Gifts received by sponsors are often taxable, especially if they are products in exchange for services (e.g., promotion of product). “Donations” from various fundraising activities like Kickstarter are also considered revenue. On the other hand, crypto and non-fungible tokens (NFTs) are considered property. Selling them usually generates a capital gain or loss.

Tip: Log all payments and gifts received, even if you are unsure, so your tax preparer can report appropriately.

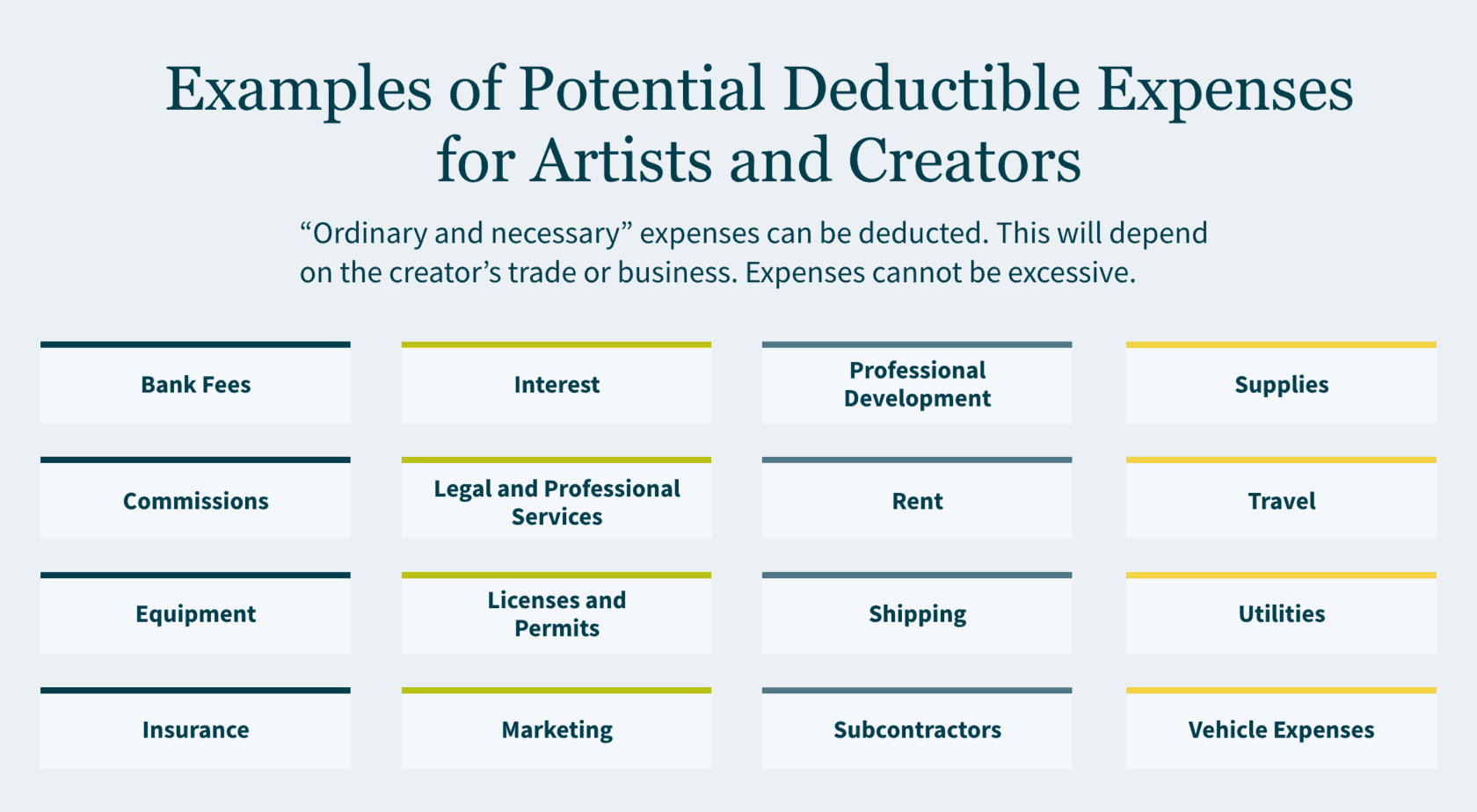

3. Track Your Expenses

Creators and artists can benefit from various tax deductions tailored to their industry. Deductible expenses may include art supplies, equipment, software subscriptions, professional development, and even a portion of your home used as a dedicated workspace. While expenses should not be excessive, any “ordinary and necessary” expenses of your craft can be deducted.

Tip: Save receipts and track expenses in real-time using a spreadsheet, app, or software for easy recording and reporting.

4. Consider Forming an Entity

Creators who run their own business are often independent contractors. Consider setting up an entity for the business — which can help protect your personal assets from your business assets and offer tax savings. S Corporations and LLCs are common for smaller businesses. For larger businesses where investors are coming in, C Corporation may make sense.

Tip: Do some research or talk to a tax professional to find out if setting up an entity makes business and financial sense for you.

5. Explore Credits You May Be Eligible For

Artists also may be eligible for various tax credits that can help offset their tax liability. Research and Development (R&D) credits can be applicable to certain creative processes, rewarding innovation in your artistic pursuits. For instance, software development is considered to be R&D for income tax purposes.

Tip: Consult a tax professional about ways to maximize credits and minimize your tax liability.

6. Don’t Overlook State and Local Taxes (SALT)

Beyond federal taxes, SALT significantly impact overall tax liability. When selling art online (whether physical or digital), be mindful of sales tax requirements, which are determined by local laws. Whether revenue is from “tangible” versus “intangible” products (physical objects versus services, ideas, software, etc.) can dictate where taxation occurs — affecting if your income is subject to sales tax or not.

Tip: Stay informed about varying tax rates, and be cautious of sales and use tax implications tied to transmitting creative art across state lines.

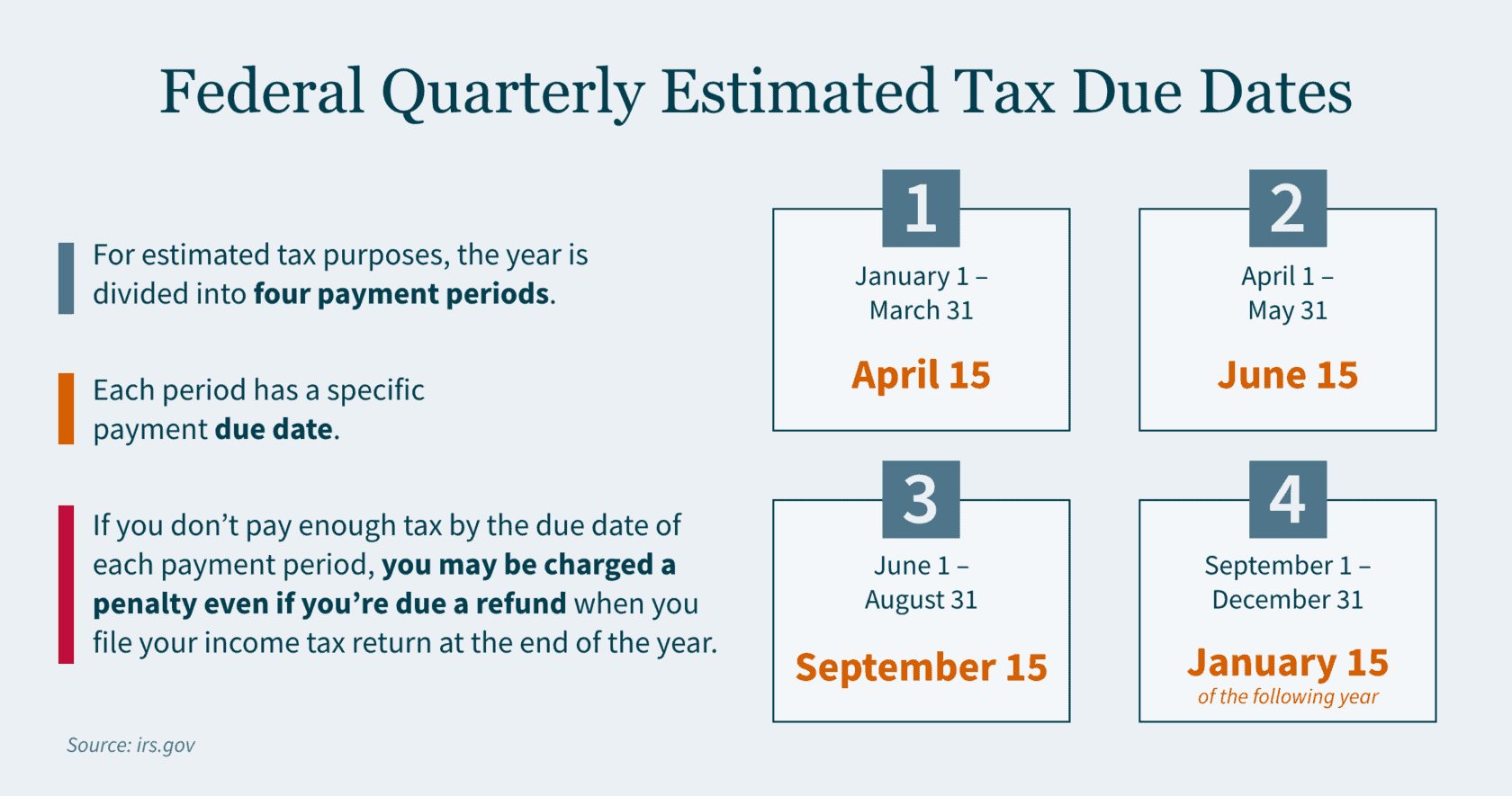

7. Plan for Estimated Taxes

As an independent contractor with variable income streams, you should plan for estimated taxes to avoid financial surprises. These quarterly payments encompass income taxes on your profits plus the self-employment tax (covering Social Security and Medicare). For those earning up to $160,200 in net income, the self-employment tax rate currently stands at 15.3%. The silver lining is that you can deduct half of this self-employment tax when filing your income taxes.

Tip: Set aside a portion of your income for estimated tax payments, ensuring proactive financial planning throughout the year.

8. Report Global Income and Claim Foreign Tax Credits

United States (U.S.) citizens or residents earning abroad must report all worldwide income to the Internal Revenue Service (IRS). If you’re earning income in or from foreign countries, it’s crucial to understand foreign tax credits, filing requirements, and deductibility in various jurisdictions. Every tax jurisdiction may have a different method to tax your creation; and different tax implications may arise based on where brands and intellectual property are created and protected.

Tip: Work with a tax professional to evaluate the potential benefits of foreign tax credits for non-U.S. income.

9. Learn Your Options for Transferring Wealth

Digital assets such as domain names, electronically stored photos, and videos to email and social media accounts all have value. When transferring these as gifts or bequests, there may be tax implications that can be circumvented if the transfer is appropriately structured or organized.

Tip: Consider trusts and estate planning for more tax-efficient wealth transfer.

10. Adapt a Business Owner Mindset

As an artist, embracing a business owner’s perspective is essential for long-term success. Understanding basic financial statements like balance sheets and profit and loss (P&L) statements allows you to gauge profitability, identify your most valuable revenue sources, and streamline your efforts. Elevating your financial literacy empowers you to make more informed decisions — which can lead to greater freedom and flexibility in your artistic career.

Quick Tip: Learn to read a balance sheet and create a basic P&L statement for a clearer financial picture.

Integrate Financial Management into Your Creative Journey

Effective financial planning is like a great work of art — every brushstroke matters. By taking these steps today you can better position yourself to continue pursuing your creative passion tomorrow.

Need a hand with taxes and accounting for your creative venture? Our Entertainment, Sports, and Media practice works with a diverse range of artists — from musicians to photographers to online creators — and our International Tax and State and Local Tax teams can provide guidance to help you address areas like sales tax or foreign tax credits. Reach out to MGO today.

- In April, the U.S. Tax Court made news when it ruled in favor of businessman Alon Farhy, who challenged the Internal Revenue Service (IRS)’s authority to assess penalties for the failure to file IRS Form 5471.

- IRS Form 5471 is the Information Return of U.S. Persons With Respect to Certain Foreign Corporations.

- Taxpayers may be interested in filing protective refunds, and they should start the process sooner rather than later—there is a statute of limitations of two years for claiming refunds.

- This case’s ruling could have reverberating effects when it comes to the IRS collecting additional penalties, but only time will tell.

On April 3, 2023, the U.S. Tax Court came to a decision in the case Farhy v. Commissioner, ruling that the Internal Revenue Service (IRS) does not have the statutory authority to assess penalties for the failure to file IRS Form 5471, or the Information Return of U.S. Persons With Respect to Certain Foreign Corporations, against taxpayers. It also ruled that the IRS cannot administratively collect such penalties via levy.

Now that the IRS doesn’t have the authority to assess certain foreign information return penalties according to the court, affected taxpayers may want to file protective refund claims, even if the case goes to appeals — especially given the short statute of limitations of two years for claiming refunds.

Our Tax Controversy team breaks down the Farhy case, as well as what it may mean for your international filings — and the future of the IRS’s penalty collections.

The case

Alon Farhy owned 100% of a Belize corporation from 2003 until 2010, as well as 100% of another Belize corporation from 2005 until 2010. He admitted he participated in an illegal scheme to reduce his income tax and gained immunity from prosecution. However, throughout the time of his ownership of these two companies, he was required to file IRS Forms 5471 for both — but he didn’t.

The IRS then mailed him a notice in February 2016, alerting him of his failure to file. He still didn’t file, and in November 2018, he assessed $10,000 per failure to file, per year — plus a continuation penalty of $50,000 for each year he failed to file. The IRS determined his failures to file were deliberate, and so the penalties were met with the appropriate approval within the IRS.

Farhy didn’t dispute that he didn’t file. He also didn’t deny he failed to pay. Instead, he challenged the IRS’s legal authority to assess IRC section 6038 penalties.

The court’s ruling

The U.S. Tax Court then held that Congress authorized the assessment for a variety of penalties — namely, those found in subchapter B of chapter 68 of subtitle F — but not for those penalties under IRC sections 6038(b)(1) and (2), which apply to Form 5471. Because these penalties were not assessable, the court decided the IRS was prohibited from proceeding with collection, and the only way the IRS can pursue collection of the taxpayer’s penalties was by 28 U.S.C. Sec. 2461(a) — which allows recovery of any penalty by civil court action.

How this court decision affects your international penalty assessments

This case holds that the IRS may not assess penalties under IRC section 6038(b), or failure to file IRS Form 5471. The case’s ruling doesn’t mean you don’t have an obligation to file IRS Form 5471 — or any other required form.

Ultimately, this decision is expected to have a broad reach and will affect most IRS Form 5471 filers, namely category 1, 4, and 5 filers (but not category 2 and 3 filers, who are subject to penalties under IRC section 6679).

However, the case’s impact could permeate even deeper. For years, some practitioners have spoken out against the IRS’s systemic assessment of international information return (IIR) penalties after a return is filed late, making it impossible for taxpayers to avoid deficiency procedures. The court’s decision now reveals how a taxpayer can be protected by the judicial branch when something is deemed unfair. Farhy took a stand, challenged the system, and won — opening the door for potential challenges in the future.

It’s uncertain as to whether the IRS will appeal the court’s decision. But it seems as though the stakes are too high for the IRS not to appeal. While we don’t know what will happen, a former IRS official has stated he expects that, for cases currently pending review by IRS Appeals, Farhy will not be viewed as controlling law yet.

The impact of the ruling is clear and will most likely impact many taxpayers who are contesting — or who have already paid — IRC 6038 penalties. It may also affect other civil penalties where Congress has not prescribed the method of assessment in the future.

How you should respond to the court’s decision

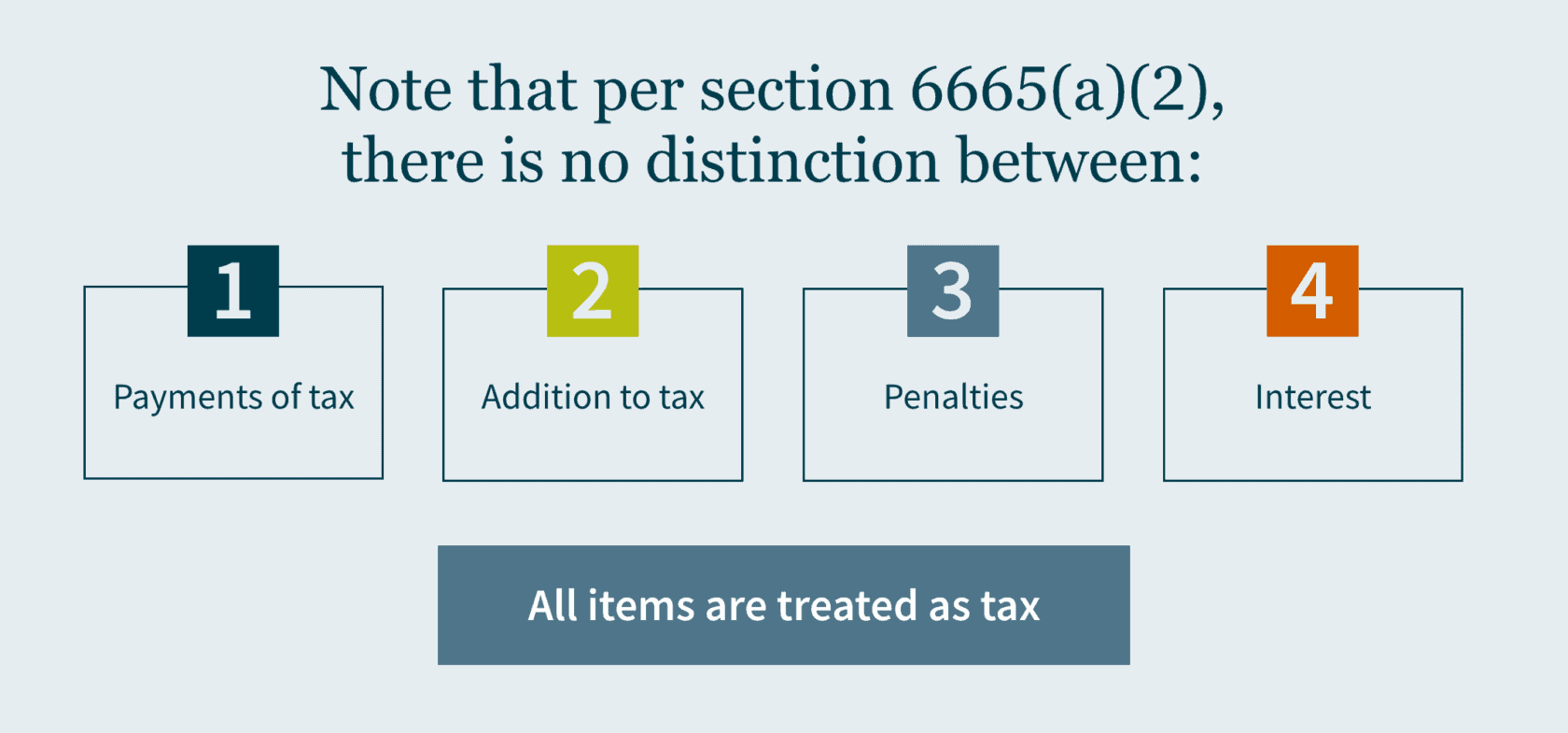

You should move quickly to take advantage of the court’s decision, as there is a two-year statute of limitations from the time a tax is paid to make a protective claim for a refund. It’s likely this legislation wouldn’t affect refund claims since that would be governed by the law that existed when the penalties were assessed. Note that per IRC section 6665(a)(2), there is no distinction between payments of tax, addition to tax, penalties, or interest — so all items are treated as tax.

If you’ve previously paid the $10,000 penalty, it’s important to file your protective claim now, unless you’ve entered into an agreement with the IRS to extend the statute of limitations, which can occur during an examination. Requesting a refund won’t ever hurt, but some practitioners believe the IRS may try to keep any penalty money it collected, even if the assessment is invalid— because, in its eyes, the claim may not be. Just know, you can file your protective claim for a refund but may not get it, at least not any time soon.

The Farhy decision could likewise be applied to other US IRS forms, such as 5472, 8865, 8938, 926, 8858, 8854, and some argue the Farhy decision may also be applied to IRS Form 3520.

How MGO can help

Only time will tell if the court’s decision will open the government up to additional criticisms for other penalty assessments. If you have paid your penalties and are wondering what your current options are, MGO’s experienced International Tax team can help you determine if you’re eligible to file a refund claim.

Contact us to learn more.

]]>

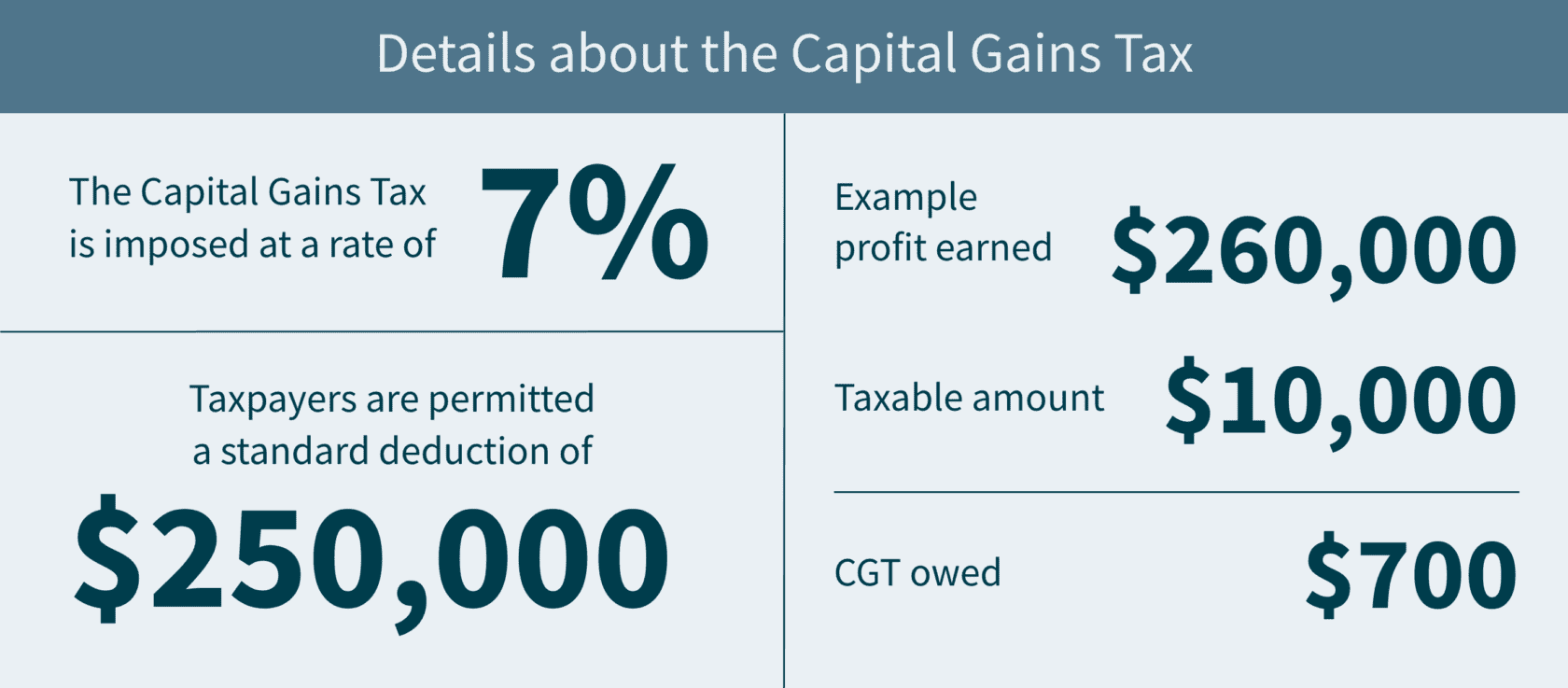

- The Supreme Court of Washington State issued a landmark ruling maintaining the constitutionality of the state’s capital gains tax (CGT) by determining that it’s an excise tax, or a tax on a good or service (and not a property tax).

- It’s imposed at a rate of 7% and taxpayers can claim a standard deduction of $250,000.

- There are other deductions, like long-term gains from the sales of qualified family-owned small businesses and charitable contributions of more than $250,000.

- You may be able to apply a tax credit.

On March 24, 2023, the Supreme Court of Washington State (SCOWA) ruled 7-2 to uphold the constitutionality of the state’s controversial capital gains tax. Thus, by the April 18, 2023, deadline, Washington residents recognizing capital gains income (and nonresidents engaged in transactions occurring within the state) in 2022 will have to calculate this new tax and pay accordingly.

Our State and Local Tax team breaks down what you need to know about this divisive tax with an impending deadline.

The details about CGT

The CGT was created when Washington enacted Senate Bill 5096 in April 2021 with the intention of having the excise tax proceeds — projected to be nearly $415 million — fund the state’s early education and childcare programs. Charged on long-term Washington-allocated capital gains, the CGT is imposed at a rate of 7% of an individual’s federal capital gain from a sale or exchange of long-term investments that exceed $250,000. This includes stocks, bonds, businesses, and other assets.

The controversy of CGT

This bill has generated controversy since its inception — mostly because it is categorized as an excise tax and not an income tax (Washington is one of nine states that doesn’t have income tax due to limitations in the state constitution on the state government assessing a tax on “property”). As a reminder, an excise tax is a legislated tax on the sale of specific services, activities, or goods.

In March 2022, the Douglas County Superior Court in Washington deemed the CGT unconstitutional as an impermissible income tax that is only masquerading as an excise tax. The Court defined gains as income, and therefore property under the Washington Constitution, that the state impermissibly taxed at a non-uniform rate (i.e., the tax doesn’t apply to every resident equally, but only those whose profits exceed the $250,000 threshold). In the past, Washington’s Supreme Court has considered income as property — and property must be taxed at a flat rate.

Since state revenue relies on sales and business taxes, taxpayers who earn the least will end up paying a higher share of their income in tax. This notion has split public opinion. Community groups and labor unions believe the tax is not just legal, it’s necessary because of its capability to create a more equitable tax system. But organizations with business interests in mind find it to be bad public policy in addition to violating the constitution.

However, the Washington Supreme Court ruled to uphold the tax, agreeing it is constitutional as an excise tax — “levied on the sale or exchange of capital assets, not on capital assets or gains themselves.” In other words, the Court reasoned that the tax is tied not to the person’s ownership interest in the property (which would be unconstitutional), but on the transaction itself.

Calculating your tax base

Adjusted capital gains

As mentioned, the new tax is imposed on your adjusted capital gains allocated to Washington, minus allowable deductions and exemptions. First, it starts with your federal net long-term capital gain for the tax year. It’s then adjusted by adding back long-term capital losses from sales or exchanges that are exempt or not allocated to the state. Finally, you subtract your long-term capital gains from sales or exchanges that are exempt or not allocated to the state.

Deductions

There are several deductions allowed against adjusted capital gains. Individual taxpayers are permitted a $250,000 standard deduction in calculating the CGT. But married or state-registered domestic partners that file a single federal tax return collectively have only a single $250,000 deduction. For example, if you earned $260,000 in profit from selling bonds in the past year, only $10,000 would be taxed, and the CGT owed would be $700. And if you and your husband together earned $260,000 from selling bonds, you wouldn’t get to “double” the standard deduction – you’d have the same tax bill.

Additional deductions include long-term gains from the sales of qualified family-owned small businesses, and charitable contributions. Associated regulations do treat the sale or transfer of an interest in a “qualified family-owned small business” as a separate deduction from the charitable deduction. (Note that the “qualified family-owned small business” is not the same as the federal Qualified Small Business Stock (QSBS) tax exclusion — there are separate requirements). To receive the charitable deduction, you would need to contribute over $250,000, not exceeding a deduction of $100,000 in total. Consequently, if you donate $350,000, you’ll receive the maximum deduction.

Exemptions

Certain long-term capital gains and losses from sales of capital assets are not subject to the tax. These exempt items include sales or exchanges of the following types of assets:

- Livestock;

- Timber;

- Real estate, and land structures; and

- Capital assets held in IRAs, 401(k) plans, and other qualified retirement plans

Allocating your capital gains and losses

If you were living in Washington at the time of a sale or exchange of intangibles (e.g., stocks, bonds, etc.), related long-term capital gains and losses are allocated to Washington.

In addition, gains or losses from the sale or exchange of other (tangible) personal property is allocated to Washington if:

- The property was in Washington at any time during the tax year when the sale/exchange occurred,

- You were a Washington resident at the time of the sale/exchange, and

- You were “not subject to the payment of an income tax or excise tax legally imposed” by another jurisdiction* on that long-term capital gain or loss.

* Jurisdiction is defined to include not only U.S. states, political subdivisions, territories, and possessions, but also foreign countries and political subdivisions of foreign countries.

Good news: a tax credit is available

If you’re interested in applying a tax credit against this new tax, you might be able to. Any Washington capital gains tax can qualify as a credit against the Washington business and occupation (B&O) tax — given that the B&O tax includes the gain from a transaction subject to capital gains tax (because it applies to ALL gross receipts regardless of character).

In addition, a credit can be applied for an income or excise tax legally imposed by another jurisdiction on capital gains “derived from capital assets within the other taxing jurisdiction to the extent such capital gains are included in the taxpayer’s Washington capital gains.”

Filing your returns

Remember, a Washington capital gains tax return is required only if tax is owed — and it must be filed on or before the due date of your federal income tax return, including extensions. But the payment of the tax is required BY the original due date of your federal income tax return, NOT including extensions. Any filing and payments must be done online using the MyDOR portal by April 18, 2023, for most taxpayers.

How MGO can help

Keep in mind that while this tax will more than likely impact Washington residents the most, if you are a nonresident whose capital gains from the sales and exchanges of your tangible personal property is allocated to Washington, you could be affected too. Accordingly, anyone with a large gain event (other than the sale of real property) during 2022 or later years, should consider whether this tax may affect them.

MGO’s State and Local Tax team can help you prepare and file this return and manage any of the other surprises that can occur in state and local tax. Contact us if you have additional questions about how the capital gains tax impacts your finances, or if you’re interested in additional strategies to boost your tax efficiency.

]]>- California Governor Newsom strives to amend the personal income tax laws to prevent wealthy taxpayers from utilizing Incomplete Gift Non-Grantor trusts.

- California residents use this by transferring assets into trusts held by nonresident trustees in states without income tax.

- If this legislation passes, taxpayers will no longer be able to take advantage of the strategy.

If you reduce California income tax with an ING, Newsom is onto you

Californian legislators propose to amend the personal income tax laws to close a little-known-but-effective loophole for the wealthy by targeting Incomplete Gift Non-Grantor (ING) trusts set up in other states with more favorable income tax rules. To date, California residents have had the opportunity to transfer assets into these trusts held by nonresident trustees in states without income tax, utilizing the state’s sourcing rules to avoid the tax. If approved, this new legislation will put a stop to this tax planning strategy.

Taxing the rich in California

As it stands, the ING trust is not commonly used. There are about 1,500 California residents with this trust in states without income tax — and if implemented, California would see a minimal revenue increase (about $30 million in the first year and $15 million in the following years). However, this would put an end to a tax planning strategy the wealthy have been using to their benefit for about 20 years.

Because California is home to more billionaires than any other state at the same time as it also has the highest rate of poverty in the U.S., the concept of taxing the rich holds a certain appeal. In the past, Newsom has opposed proposals to raise taxes — but this proposal was included in the governor’s $223.6 billion budget plan for the next fiscal year, which begins in July. Whether the item survives the legislative process remains to be seen, but if New York’s passage of a similar law in 2014 is any indication, we are likely to see the end of this tax planning strategy for California’s ultra-rich.

Moreover, this proposal has a retroactive element, differentiating it from New York’s and opening it up to potential lawsuits (New York trust holders had a five-month period to move their accounts to a different type of trust without incurring the tax). Newsom is pushing for the measure to begin the calendar year after its implementation.

How the ING works (worked)

What is an ING, and why is Newsom trying to prevent its use? California taxpayers can transfer their assets into out-of-state, incomplete, non-grantor trusts (INGs), which constitute separate, taxable entities under state and federal tax law, and this move avoids California income tax on any appreciation or gains from those assets because it is “sourced” to another state based on the location of the trustee (i.e., the bank or whatever financial institution offers the trustee services in the other state). The non-grantor aspect comes into play when the taxpayer establishing the trust (the “grantor”) gives up control over managing investments or distributing assets to the trustee (contrast with a “grantor trust” in which the grantor continues to control how money is invested/distributed within the trust during their lifetime). For the trust to be deemed “incomplete,” the grantors specify how the money can be used.

Some of the states where these trusts are typically established include Florida, Wyoming, Delaware, Nevada, Tennessee, and South Dakota. For example, a California resident (TP) may decide to transfer stock in their business into an ING established in South Dakota. If TP held the stock directly, then as a resident, all the dividends (or if he sold it, the gain) would be taxable by California on their personal income tax return. But since TP doesn’t hold the asset – the ING does – the ING recognizes the income relating to the stock. California’s current rules provide that the income is sourced to (and thus taxable in) the state where the trustee is domiciled, and for this ING that location is South Dakota, which, incidentally, does not tax this sort of income.

Newsom is hoping that by eliminating this tax-free option, the state of California will be able to increase tax revenue in a way that will not alienate a large number of voters.

How MGO can help

If you are a California resident and currently use an ING as a tax strategy, there are steps to take now to avoid a negative impact. MGO’s experienced Private Client Services team can help you identify and implement an effective response.

]]>The tax relief postpones tax filing and payment deadlines occurring between January 8, 2023, and May 15, 2023, to a new due date of October 15, 2023.

Some of the filings and payments postponed include:

- Individual income tax returns due on April 18

- Business tax returns normally due on March 15 and April 18

- 2022 contributions to IRAs and health savings accounts

- Quarterly estimated tax payments normally due January 17 and April 18

- Quarterly payroll and excise tax returns normally due on January 31 and April 30

The current list of counties that qualify for this relief can be found here.

If you qualify for this postponement, you generally do not need to contact the IRS or FTB to obtain relief. Relief is automatically granted for affected taxpayers who have an address of record located in one of the designated counties. However, if you still receive a late filing or late payment notice and the notice shows the original or extended filing, payment, or deposit due date falling within the postponement period, you should call the number on the notice to have the penalty abated.

If you have questions or need assistance, contact MGO’s experienced State and Local Tax team.

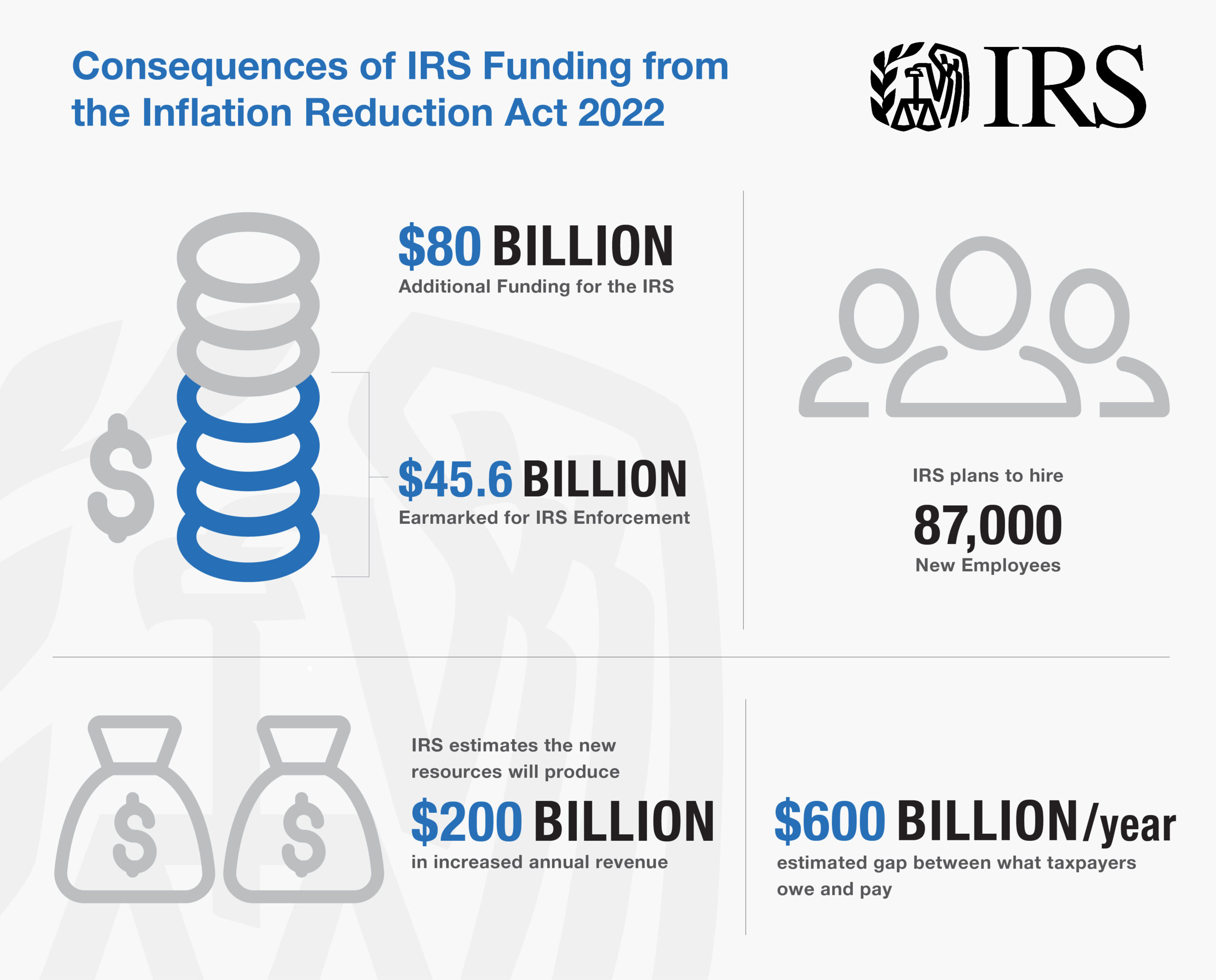

]]>- The Inflation Reduction Act of 2022 includes $80B in funding for the Internal Revenue Service.

- Over half of the funding will be set aside for IRS enforcement so the agency can hire more staff to conduct more audits, hoping to target those who do not pay their taxes.

- This will most likely subject those taxpayers with complex filings to additional scrutiny.

The Inflation Reduction Act of 2022 was recently signed into law with an eye-opening provision: the inclusion of nearly $80 billion in additional funding for the Internal Revenue Service (IRS). $45.6 billion of that is earmarked for IRS enforcement, which will be used to help the underfunded agency hire additional staff and conduct future audits in the hopes of collecting unpaid taxes.

Many publications cite the IRS plans to hire up to 87,000 new employees, though the actual number will be released in the coming months. These new hires will fill positions ranging from auditors to customer service representatives to IT specialists. The IRS has been plagued by more than a decade of budget cuts, which has limited its ability to modernize its old technology and staff appropriately. Since 2010, the agency’s enforcement staff has declined by 30%. The funding appropriate in the Inflation Reduction Act hopes to reverse this trend and bring in an estimated $203 billion in increased revenue.

The MGO Tax Controversy team breaks down what you need to know about this big change that could increase your risk of an audit.

How will the increase in IRS staff affect taxpayers?

Critics of the increase in IRS funding have claimed that the new resources will be used to target low to middle-income Americans and small businesses, burdening them with more audits and examinations. The Treasury Department refutes these claims reiterating they plan to focus primarily on large corporations and the wealthy — those more likely to evade paying their taxes — to close the tax gap, or the difference between what taxpayers pay in taxes and what they actually owe – an estimated to be $600 billion per year.

The IRS hopes the investment in funding will bring in around $203.7 billion in revenue because between 2015 and 2019, IRS audits declined significantly — 75% for Americans making $1 million or more and 33% for filers with low to moderate incomes. Lower-income Americans are mostly wage earners, so their audits are less complex and can be automated. However, more complex filers, notably large corporations and high-net-worth individuals and families – require the hands-on engagement of IRS agents and are most likely to experience increased levels of scrutiny from the new hires.

Ultimately, the average taxpayer should have an improved tax filing experience. New staff will be on hand to answer questions by phone, technology systems will be improved and modernized, and the backlog of unprocessed returns should diminish.

What is the timeline for implementing these changes?

While there is no set timeline, it is likely the way IRS audits work will change with the increase in funding. Currently, software is used to rank each tax return with a numeric score, and higher scores trigger an audit. Other mechanisms the IRS uses to determine candidates for audits include enforcement initiatives referred to as “campaigns” based on various criteria. The new funding will take time to phase in, and so will the hiring and training of new workers. It is expected new auditors will complete a six-month training program, starting small with cases involving a few hundred thousand dollars instead of tens of millions. Forbes performed some creative math to conclude while the funding will increase IRS audits, it is not likely to occur for the next few years.

How can I avoid future audits?

The best way to avoid an audit remains simple: pay your taxes on time and in compliance with tax laws. Simple accounting and documentation best practices are your best friend. If you feel you are at risk for a potential audit, you’ll want to get a head start now by ensuring your records are accurate and have been updated and maintained. Save your receipts and include every detail you can in your bookkeeping logs. If you do get audited in the coming wave, you’ll be glad you have all of this information organized and on-hand.

Our perspective on the increase in IRS staffing

The IRS has long been criticized because of their inability to provide taxpayers with the level and quality of service they deserve. The increase in funding as part of the Inflation Reduction Act should help. On the other hand, the number of tax audits is likely to increase, and you will want to be ready.

MGO’s dedicated Tax Controversy team can help by providing a holistic look at your tax filings as well as provide guidance for conflict resolution. From prevention to resolution, we guide you every step of the way.

If you’re an operator or investor in the cannabis industry, our Tax Practice recently published the Cannabis IRS Audit Survival Guide, which details everything you need to do to prepare for and navigate a tax audit. You can download the Guide for free here.

About the author

T. Renee Parker is a tax partner and the National Tax Controversy Practice Leader at MGO. With more than 15 years of tax controversy experience, she is a member of the IRS Tax Advocacy Panel and is well-versed in all areas of tax controversy. These include but are not limited to U.S. federal, state, and local tax audits; sales and use/payroll tax audits; international tax compliance related audits; negotiation and settlements with tax authorities; and corresponding and negotiation with tax authorities. Contact Renee at RParker@MGOCPA.com.

]]>In Notice 2021-39, the IRS released guidance providing penalty relief for filers who made “good faith efforts” to adopt the new schedules. More recently, in response to continued concern and feedback from taxpayers and practitioners, the IRS has indicated that under certain circumstances taxpayers will be entirely relieved of the need to file the new forms this year.

A tough tax season for the IRS

The announcement of additional relief comes as IRS Commissioner Charles Rettig has acknowledged that the agency faces “enormous challenges” this tax season. For example, millions of taxpayers are still waiting for prior years’ returns to be processed thanks to a monumental backlog.

To address such issues, he says, the IRS has taken “extraordinary measures,” including mandatory overtime for IRS employees, the creation and assignment of “surge teams,” and the temporary suspension of the mailing of certain automated compliance notices to taxpayers. In addition, the partial suspension of the filing requirements for Schedules K-2 and K-3 might ease the burden for both affected taxpayers and the IRS.

K-2 and K-3 filing requirements

Provisions of the Tax Cuts and Jobs Act, which was enacted in 2017, require taxpayers to provide significantly more information to calculate their U.S. tax liability for items of international tax relevance. The Schedule K-2 reports such items, and the Schedule K-3 reports a partner’s distributive share of those items.

Schedules K-2 and K-3 must be filed with a partnership’s Form 1065, “U.S. Return of Partnership Income,” or an S corporation’s Form 1120-S, “U.S. Income Tax Return for an S Corporation.” These new schedules require more detailed and complete reporting than the entities may have provided in the past.

Schedules K-2 and K-3 replace portions of Schedule K and numerous unformatted statements attached to earlier versions of Schedule K-1. Previously, partners and S corporation shareholders could obtain the information included on the schedules through various statements or schedules the respective entity opted to provide, if any.

In January of 2022, the IRS surprised many in the tax community when it posted changes to the instructions for the schedules. Under the revised instructions, an entity may need to report information on the schedules even if it had no foreign partners, foreign source income, assets generating such income, or foreign taxes paid or accrued.

For example, if a partner claims a credit for foreign taxes paid, the partner might need certain information from the partnership to file his or her own tax return. Although some narrow exceptions apply, this change expanded the pool of taxpayers required to file the schedules.

Latest exception

Under the latest guidance, announced February 16th through an IRS FAQ, partnerships and S corporations do not need to file the schedules if they satisfy all the following requirements for the 2021 tax year:

- The direct partners in the domestic partnership are not foreign partnerships, corporations, individuals, estates or trusts, and

- The domestic partnership or S corporation has no foreign activity, including 1) foreign taxes paid or accrued, or 2) ownership of assets that generate, have generated or may be expected to generate foreign-source income.

- For the 2020 tax year, the domestic partnership or S corporation did not provide its partners or shareholders — nor did they request — information regarding any foreign transactions.

- The domestic partnership or S corporation has no knowledge that partners or shareholders are requesting such information for the 2021 tax year.

Entities that meet these criteria are not required to file Schedules K-2 and K-3. But there is an important caveat; if such a partnership or S corporation is notified by a partner or shareholder that it needs all or part of the information included on Schedule K-3 to complete its tax return, the entity must provide that information.

Moreover, if the partner or shareholder notifies the entity of this need before the entity files its own return, the entity no longer satisfies the criteria for the exception. As a result, it must provide Schedule K-3 to the partner or shareholder and file the schedules with the IRS.

“Good faith exception”

In addition to the FAQ exemption, Notice 2021-39, released in June 2021, exempts affected taxpayers from penalties for the 2021 tax year if they make a good faith effort to comply with the filing requirements for Schedules K-2 and K-3. While some are calling this a “good faith” exception, there’s some irony in this, given that the IRS is not exactly acting in good faith itself.

When determining whether a filer has established such an effort, the IRS considers, among other things:

- The extent to which the filer has made changes to its systems, processes, and procedures for collecting and processing the information required to file the schedules;

- The extent to which the filer has obtained information from partners, shareholders, or a controlled foreign partnership or, if not obtained, applied reasonable assumptions; and

- The steps taken by the filer to modify the partnership or S corporation agreement or governing instrument to facilitate the sharing of information with partners and shareholders that is relevant to determining whether and how to file the schedules.

The IRS will not impose the relevant penalties for any incorrect or incomplete reporting on the schedules if it determines the taxpayer exercised the requisite good faith efforts.

Temporary reprieves

Both the IRS FAQ exception and the “good faith exception” explicitly refer to 2021 tax year filings. In the absence of additional or updated guidance, partnerships and S corporations should expect and prepare to file the schedules for 2022 and later tax years.

MGO tax advisors are available

If you have questions, MGO can help. Please reach out to our partnership and international tax professionals for assistance. We can help keep you in compliance with these new requirements.

]]>Eligibility for the casualty loss deduction

Casualty losses can result from the damage, destruction or loss of property due to any sudden, unexpected or unusual event. Examples include floods, hurricanes, tornadoes, fires, earthquakes and volcanic eruptions. Normal wear and tear or progressive deterioration of property doesn’t constitute a deductible casualty loss. For example, drought generally doesn’t qualify.

The availability of the tax deduction for casualty losses varies depending on whether the losses relate to personal-use or business-use items. Generally, you can deduct casualty losses related to your home, household items and personal vehicles if they’re caused by a federally declared disaster — meaning a disaster that occurred in an area that the U.S. president declares eligible for federal assistance. Casualty losses related to business or income-producing property (for example, rental property) can be deducted regardless of whether they occur in a federally declared disaster area.

Casualty losses are deductible in the year of the loss, usually the year of the casualty event. If your loss stemmed from a federally declared disaster, you can opt to treat it as having occurred in the previous year. You may receive your refund more quickly if you amend the previous year’s return than if you wait until you file your return for the casualty year.

The role of reimbursements

If your casualty loss is covered by insurance, you must reduce the loss by the amount of any reimbursement or expected reimbursement. (You also must reduce the loss by any salvage value). Reimbursement also could lead to capital gains tax liability.

When the amount you receive from insurance or other reimbursements (less any expense you incurred to obtain reimbursement, such as the cost of an appraisal) exceeds the cost or adjusted basis of the property, you have a capital gain. You’ll need to include that gain as income unless you’re eligible to postpone reporting the gain.

You may be able to postpone the reporting obligation if you purchase property that’s similar in service or use to the destroyed property within the specified replacement period. You also can postpone if you buy a controlling interest (at least 80%) in a corporation owning similar property or if you spend the reimbursement to restore the property.

Alternatively, you can offset casualty gains with casualty losses not attributable to a federally declared disaster. This is the only way you can deduct personal-use property casualty losses incurred in areas not declared disaster areas.

The loss amount vs. the deduction

For personal-use property, or business-use or income-producing property that isn’t completely destroyed, your casualty loss is the lesser of:

• The adjusted basis of the property immediately before the loss (generally, your original cost, plus improvements and less depreciation), or

• The drop in fair market value (FMV) of the property as a result of the casualty (that is, the difference between the FMV immediately before and immediately after the casualty).

For business-use or income-producing property that’s completely destroyed, the amount of the loss is the adjusted basis less any salvage value and reimbursements.

If a single casualty involves more than one piece of property, you must figure the loss on each separately. You then combine these losses to determine the casualty loss.

An exception applies to personal-use real property, such as a home. The entire property (including improvements such as landscaping) is treated as one item. The loss is the smaller of the decline in FMV of the entire property and the entire property’s adjusted basis.

Other limits may apply to the amount of the loss you may deduct, too. For personal-use property, you must reduce each casualty loss by $100 (after you’ve subtracted any salvage value and reimbursement).

If you suffer more than one casualty loss during the tax year, you must reduce each loss by $100 and report each on a separate IRS form. If two or more taxpayers have losses from the same casualty, the $100 rule applies separately to each taxpayer.

But that’s not all. For personal-use property, you also must reduce your total casualty losses by 10% of your adjusted gross income, after you’ve applied the $100 rule. As a result, smaller personal-use casualty losses often provide little or no tax benefit.

The requisite records

Documentation is critical to claim a casualty loss deduction. You’ll need to be able to show:

• That you were the owner of the property or, if you leased it, that you were contractually liable to the owner for the damage,

• The type of casualty and when it occurred,

• That the loss was a direct result of the casualty, and

• Whether a claim for reimbursement with a reasonable expectation of recovery exists.

You also must be able to establish your adjusted basis, reimbursements and, for personal-use property, pre- and post-casualty FMVs.

Additional relief

The IRS has granted tax relief this year to victims of numerous natural disasters, including “affected taxpayers” in Alabama, California, Kentucky, Louisiana, Michigan, Mississippi, New Jersey, New York, Oklahoma, Pennsylvania, Tennessee, and Texas. The relief typically extends filing and other deadlines. (For detailed information for your state visit: https://bit.ly/3nzF2ui.)

Note that you can be an affected taxpayer even if you don’t live in a federally declared disaster area. You’re considered affected if records you need to meet a filing or payment deadline postponed during the applicable relief period are located in a covered disaster area. For example, if you don’t live in a disaster area, but your tax preparer does and is unable to pay or file on your behalf, you likely qualify for filing and payment relief.

A team effort

If you’ve incurred casualty losses this year, tax relief could mitigate some of the financial pain. We can help you maximize your tax benefits and ensure compliance with any extensions.

]]>Accelerate and defer with care

One of the most reliable year-end tactics for reducing taxes has long been to accelerate your deductible expenses and defer your income. For example, self-employed individuals who use cash-basis accounting can delay invoices until late December and move up the planned purchase of equipment or the payment of estimated state income taxes from early next year to this year.

This technique has always carried the caveat that you generally shouldn’t pursue it if you expect to be in a higher tax bracket the following year. Potential provisions in the BBBA also may make it advisable for certain taxpayers to reverse the strategy for 2021 — that is, accelerate income and defer deductible expenses.

The current version of the BBBA would impose a new “surtax” of 5% on modified adjusted gross income (MAGI) that exceeds $10 million, with an additional 3% on income of more than $25 million. As a result, the highest earners could pay a 45% federal marginal income tax on wages and business income (the current 37% income tax rate plus 8%). It could be even higher when combined with the net investment income tax, which might be expanded to include active business income for pass-through entities.

In addition, there’s a proposal to temporarily increase the $10,000 cap on the state and local tax deduction to $80,000. Individuals in high-tax states should consider whether there may be an advantage to accelerating a 2022 property or estimated state income tax payment into 2021, or whether the deduction might be more valuable next year, particularly if they’ll face a higher effective tax rate.

Leverage your losses

Taxpayers with substantial capital gains in 2021 could benefit from “harvesting” their losses before year-end. Capital losses can be used to offset capital gains, and up to $3,000 ($1,500 for married persons filing separately) of excess losses (those that exceed the amount of gains for the year) can be applied against ordinary income. Any remaining losses can be carried forward indefinitely.

Beware, however, of the wash-sale rule. Generally, the rule prohibits the deduction of a loss if you acquire “substantially identical” investments within 30 days, before or after, of the date of the sale.

Taxpayers who itemize their deductions could compound their tax benefits by donating the proceeds from the sale of a depreciated investment to a charity. They can both offset realized gains and claim a charitable contribution deduction for the donation.

Satisfy your charitable inclinations

For 2021, charitable contributions can reduce taxes for both itemizers and non-itemizers. Taxpayers who take the standard deduction can claim an above-the-line deduction of $300 ($600 for married couples filing jointly) for cash contributions to qualified charitable organizations.

The adjusted gross income limit for cash donations is 100% for 2021; it’s scheduled to return to 60% for 2022. That means you could offset all of your taxable income with charitable contributions this year. (Donations to donor advised funds and private foundations don’t qualify, though.)

Taxpayers who don’t generally itemize can benefit by “bunching” their charitable contributions. In other words, delaying or accelerating contributions into a tax year to exceed the standard deduction and claim itemized deductions. For example, if you usually make your donations at the end of the year, you could bunch donations in alternative years — say, donate in January and December of 2022 and January and December of 2024.

Retired taxpayers who are age 70½ and older can reduce their taxable income by making qualified charitable contributions of up to $100,000 from their non-Roth IRAs. Retired or not, individuals age 72 and older can use such contributions to satisfy their annual required minimum distributions (RMDs). Note that RMDs were suspended for 2020 but are effective for 2021.

So long as the assets would be considered long-term if they were sold, donations of appreciated assets offer a double-barreled tax benefit. You avoid the capital gains tax on the appreciation and can deduct the asset’s fair market value as of the date of the gift.

Convert traditional IRAs to Roth IRAs

As in 2020, when many taxpayers saw lower than typical income, 2021 could be a smart time to convert funds in traditional pre-tax IRAs to an after-tax Roth IRA. Roth IRAs have no RMDs, and distributions are tax-free.

You’ll have to pay income tax on the converted funds, but it’s better to do so while subject to lower tax rates. Similarly, if you convert securities that have dropped in value, your tax may well be lower now than down the road — and any subsequent appreciation while in the Roth IRA will be tax-free.

It’s worth noting that President Biden had proposed including a provision in the BBBA that would limit the ability of wealthy individuals to engage in Roth conversions. There was a lot of back-and-forth with respect to these provisions, and the latest version of the House bill includes certain restrictions. Whether these provisions will make it past any Senate amendments remains to be seen, but the proposal could be a harbinger of future proposed restrictions.

Proceed with caution

The strategies outlined above always come with pros and cons, but perhaps never more so than now, when potentially significant tax legislation that would take effect next year is under negotiation. We can help you chart the best course in light of any developments.

]]>As the cannabis industry continues to evolve and mature, perhaps the single biggest obstacle to profitability remains: IRC Section 280E. By prohibiting expense deductions for businesses that produce, sell or distribute Schedule I and II substances, the Federal government is imposing an effective tax rate two to three times higher than traditional businesses.

While there has been no progress on 280E reform at the Federal level in 2020, legal decisions in recent years, such as the cases involving retailers Harborside Inc. and Alternative Health Care, have impacted the application of 280E and provided some clarity on what cannabis companies need to consider and prepare for with tax season on the horizon.

Extensive documentation is key to navigating 280E

The first rule of navigating 280E is that all cannabis businesses must document absolutely everything. If they don’t, then it is very, very unlikely that they will prevail during an audit or if they find themselves in Tax Court. Throughout the course of doing business, inventory and costs need to be diligently documented. By keeping thorough records, you strengthen your potential case, and at the very least may win some points for demonstrating “good faith” intent.

That is what happened in the Harborside case, where the Oakland-based company was hit with an $11 million IRS bill for back taxes from 2007 and 2012. In that case, Harborside had been comprehensive in its documentation and was able to substantiate all of its claims as it related to deductions. As a result, they were not assessed inaccuracy penalties and documentation played a role in lowering their debt owed.

Understanding Cost of Goods Sold and 280E

Another lesson from recent cases relates to calculating the Cost of Goods Sold (COGS), where a reduction is made during the process of calculating gross income. IRS regulation 471 states that if the usage of inventories is deemed necessary to determine a taxpayer’s income, then an inventory shall be taken by the best accounting practices in that trade. Per 471, there are different regulations whether a taxpayer is a reseller or a producer. For instance, for producers, inventory calculations should include the costs of raw materials and necessary indirect production costs.

In the Harborside case, the company claimed that for calculating COGS, IRC Section 263A was the correct approach. Under 263A, taxpayers are required to capitalize both direct and indirect costs related to actual personal property that it produces. Harborside argued that being disallowed from using 263A resulted in the company having to pay taxes on an amount in excess of their gross income.

The decision of the Court confirmed the IRS approach, dealing a blow to cannabis companies. Per the Court’s ruling, there were a number of aspects that impact the way cannabis can approach how they calculate COGS. Given the different approaches under 471 for those deemed either a “producer” or a “reseller,” companies need to understand how they will be classified, as it has a major impact on their accounting processes.

Tax structuring considerations for 280E

Another important aspect for cannabis retailers to consider is how they are structuring their business. In a case decided last year, Los Angeles-based Alternative Health Care tried to avoid 280E by having a management company operate its storefront. The management company was responsible for a number of critical day-to-day operations, such as paying employees. Given that Alternative Health Care wasn’t in charge of the storefront, it argued that it wasn’t subject to the tax laws of 280E. However, their argument lost in court and resulted in an expansion of the types of companies that are considered liable under 280E.

There may be a number of reasons why a cannabis retailer would want to avoid liability under 280E. But just because a management company is technically in charge, liability also extends to them. If a company is considering using a different company to handle its day-to-day business, there needs to be an understanding that 280E is still applicable and that trying to get around this can end up being costly.

There are many other benefits to structuring a cannabis company in a strategic way. It can allow specific business units to be utilized in a tax efficient manner and enhance a company’s ability to take advantage of special tax deductions. Additionally, a company can make bookkeeping much easier, while simultaneously reducing risks by separating certain business units. Structuring can also open up other opportunities down the line when it comes to joint ventures or shareholder investments.

Preparing for cannabis audits

Recent court decisions (and other rumors) have stoked fears that there will be an increase in audits of cannabis companies. There is no guarantee that there will be more audits or that a certain retailer will be audited in the next year. However, audits can happen, so it is paramount that a company protects itself in every way they possibly can.

Overall, it is always best to be prepared. As stated previously, document everything. Maintain all necessary paperwork. If you avoid being audited, there are many other benefits to appropriately documented financial and operational records. But if one crops up, you minimize the risk of potential penalties and create a much smoother process.

The bottom line on 280E

While changes to precedent and recent case developments have altered the 280E landscape, as the cannabis sector grows, and revenue numbers rise, greater attention is given to the industry by regulatory authorities. As a result, companies must make taking a strategic approach to 280E compliance a top priority.

]]>