Here’s what you need to know to claim it:

- It’s a one-time abatement of any “timeliness” penalties incurred on individual income tax returns (Form 540, Form 540NR, Form 540 2EZ) for tax years beginning on or after January 1, 2022.

- It’s only available to individual taxpayers subject to personal income tax law (so estates, trusts, and fiduciaries aren’t eligible).

- It can be requested verbally or in writing starting on April 17, 2023.

- For California taxpayers who qualify for an extended 2022 income tax return due date because of the California Winter Storms (i.e., most California taxpayers), the “timeliness” penalties that would be abated through this program should not start being imposed until after the new extended due date for that tax year – October 16, 2023.

Which penalties are eligible?

Both the Failure to File Penalty (i.e., you did not file your tax return by the due date nor did you pay by the due date of your tax return) and the Failure to Pay Penalty (i.e., you did not pay the entire amount due by your payment due date) on California individual income tax returns for tax years beginning on or after January 1, 2022 are eligible for the one-time penalty abatement.

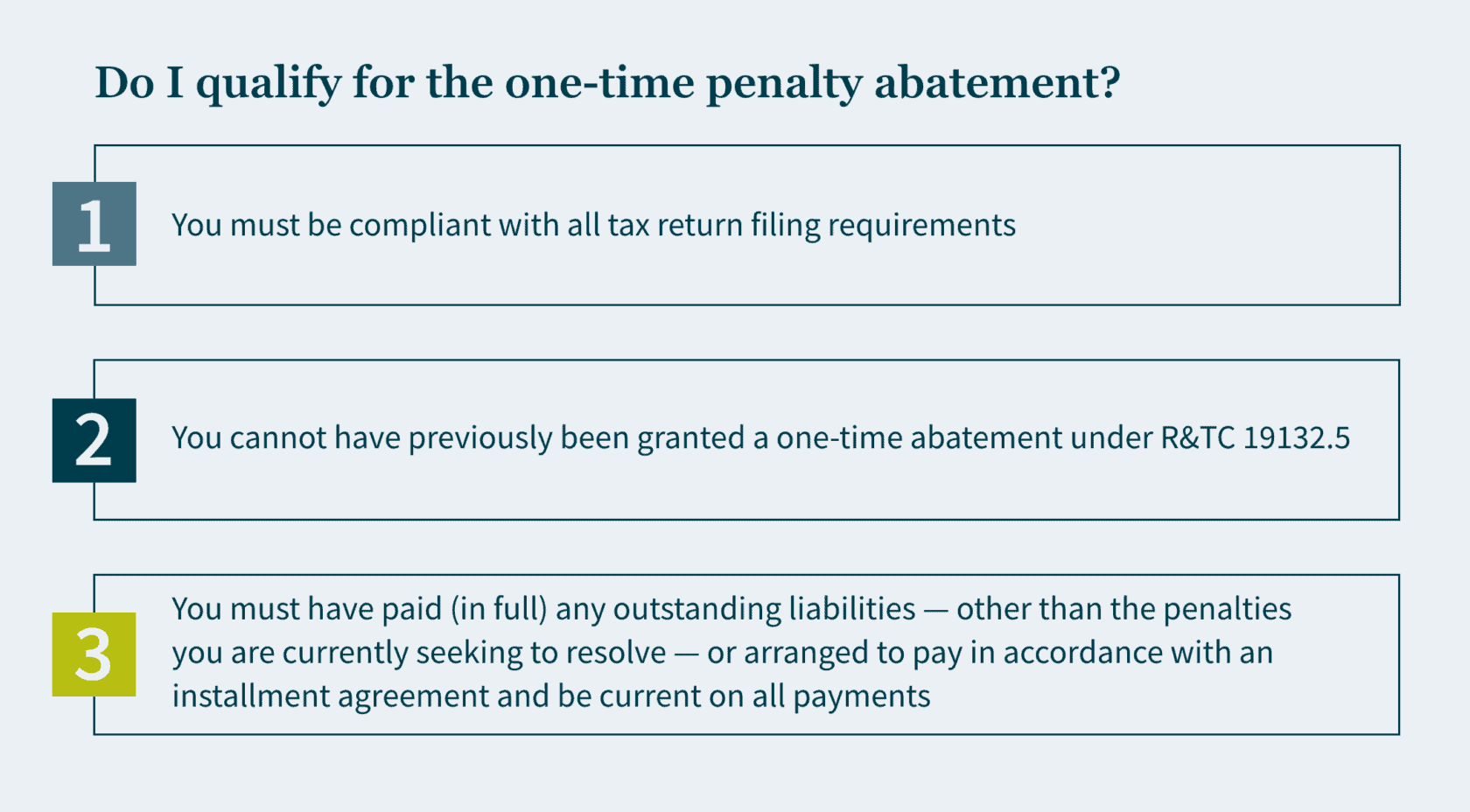

How do I qualify?

How do I request a one-time penalty abatement?

You can mail in a completed Form FTB 2918 or call the FTB at +1 (800) 689-4776 to request penalty abatement.

What if I can provide that I had reasonable cause for late filing or late payment?

If you can demonstrate that you exercised ordinary care and prudence and were nevertheless unable to file your return or pay your taxes on time, then you may qualify for penalty relief due to reasonable cause. Reasonable cause is determined on a case-by-case basis and considers all the facts of your situation.

You may request penalty abatement based on reasonable cause by mailing in a completed Form FTB 2917 or by filling out a reasonable cause request on your MyFTB online account. Penalty abatement based on reasonable cause may – depending on the circumstances – be preferable to using up your one-time penalty abatement request.

How we can help

If you need help with relief for your “timeliness” penalties or if you need help with any other state and local tax matters, please reach out to our experienced State and Local Tax team.

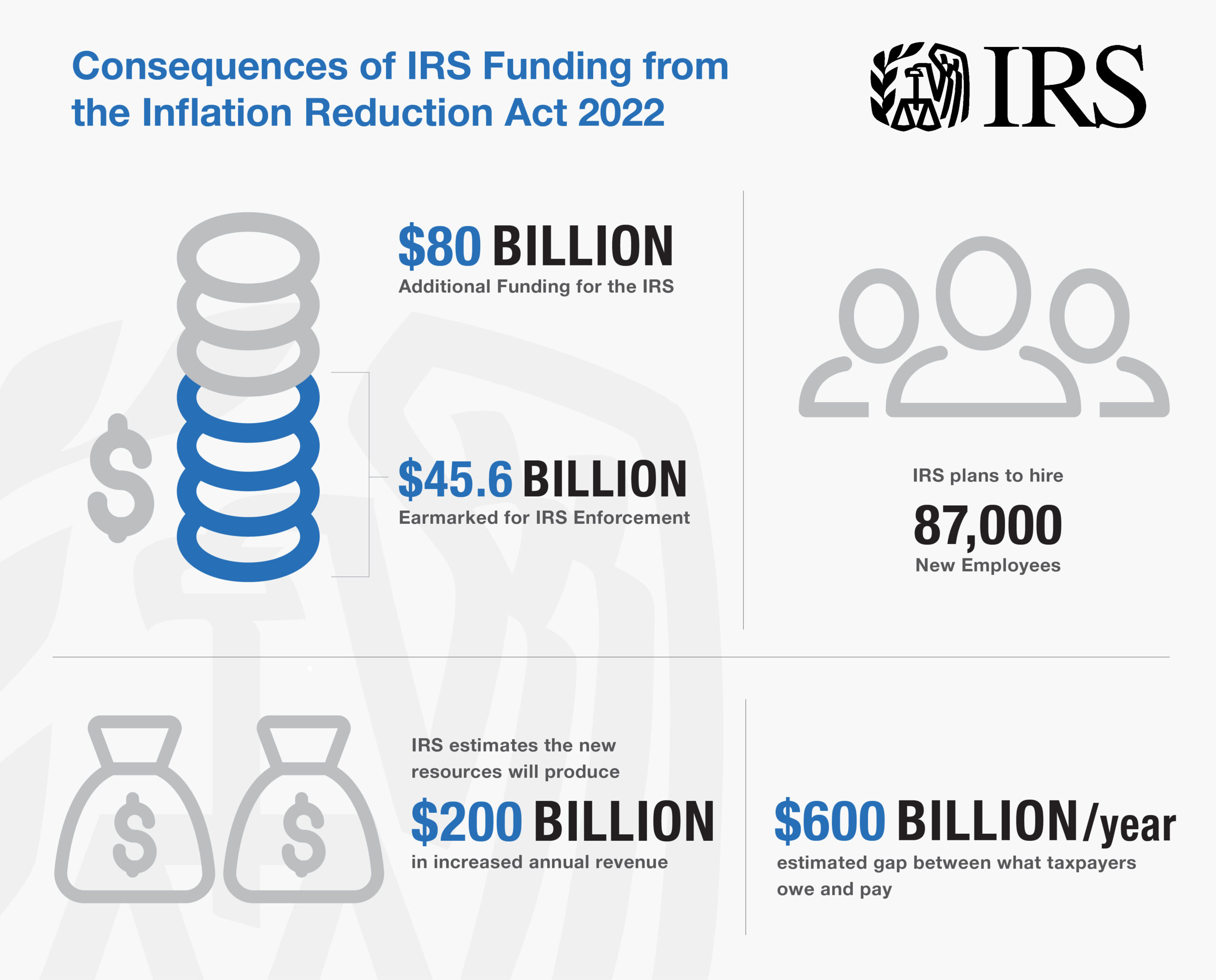

]]>- The Inflation Reduction Act of 2022 includes $80B in funding for the Internal Revenue Service.

- Over half of the funding will be set aside for IRS enforcement so the agency can hire more staff to conduct more audits, hoping to target those who do not pay their taxes.

- This will most likely subject those taxpayers with complex filings to additional scrutiny.

The Inflation Reduction Act of 2022 was recently signed into law with an eye-opening provision: the inclusion of nearly $80 billion in additional funding for the Internal Revenue Service (IRS). $45.6 billion of that is earmarked for IRS enforcement, which will be used to help the underfunded agency hire additional staff and conduct future audits in the hopes of collecting unpaid taxes.

Many publications cite the IRS plans to hire up to 87,000 new employees, though the actual number will be released in the coming months. These new hires will fill positions ranging from auditors to customer service representatives to IT specialists. The IRS has been plagued by more than a decade of budget cuts, which has limited its ability to modernize its old technology and staff appropriately. Since 2010, the agency’s enforcement staff has declined by 30%. The funding appropriate in the Inflation Reduction Act hopes to reverse this trend and bring in an estimated $203 billion in increased revenue.

The MGO Tax Controversy team breaks down what you need to know about this big change that could increase your risk of an audit.

How will the increase in IRS staff affect taxpayers?

Critics of the increase in IRS funding have claimed that the new resources will be used to target low to middle-income Americans and small businesses, burdening them with more audits and examinations. The Treasury Department refutes these claims reiterating they plan to focus primarily on large corporations and the wealthy — those more likely to evade paying their taxes — to close the tax gap, or the difference between what taxpayers pay in taxes and what they actually owe – an estimated to be $600 billion per year.

The IRS hopes the investment in funding will bring in around $203.7 billion in revenue because between 2015 and 2019, IRS audits declined significantly — 75% for Americans making $1 million or more and 33% for filers with low to moderate incomes. Lower-income Americans are mostly wage earners, so their audits are less complex and can be automated. However, more complex filers, notably large corporations and high-net-worth individuals and families – require the hands-on engagement of IRS agents and are most likely to experience increased levels of scrutiny from the new hires.

Ultimately, the average taxpayer should have an improved tax filing experience. New staff will be on hand to answer questions by phone, technology systems will be improved and modernized, and the backlog of unprocessed returns should diminish.

What is the timeline for implementing these changes?

While there is no set timeline, it is likely the way IRS audits work will change with the increase in funding. Currently, software is used to rank each tax return with a numeric score, and higher scores trigger an audit. Other mechanisms the IRS uses to determine candidates for audits include enforcement initiatives referred to as “campaigns” based on various criteria. The new funding will take time to phase in, and so will the hiring and training of new workers. It is expected new auditors will complete a six-month training program, starting small with cases involving a few hundred thousand dollars instead of tens of millions. Forbes performed some creative math to conclude while the funding will increase IRS audits, it is not likely to occur for the next few years.

How can I avoid future audits?

The best way to avoid an audit remains simple: pay your taxes on time and in compliance with tax laws. Simple accounting and documentation best practices are your best friend. If you feel you are at risk for a potential audit, you’ll want to get a head start now by ensuring your records are accurate and have been updated and maintained. Save your receipts and include every detail you can in your bookkeeping logs. If you do get audited in the coming wave, you’ll be glad you have all of this information organized and on-hand.

Our perspective on the increase in IRS staffing

The IRS has long been criticized because of their inability to provide taxpayers with the level and quality of service they deserve. The increase in funding as part of the Inflation Reduction Act should help. On the other hand, the number of tax audits is likely to increase, and you will want to be ready.

MGO’s dedicated Tax Controversy team can help by providing a holistic look at your tax filings as well as provide guidance for conflict resolution. From prevention to resolution, we guide you every step of the way.

If you’re an operator or investor in the cannabis industry, our Tax Practice recently published the Cannabis IRS Audit Survival Guide, which details everything you need to do to prepare for and navigate a tax audit. You can download the Guide for free here.

About the author

T. Renee Parker is a tax partner and the National Tax Controversy Practice Leader at MGO. With more than 15 years of tax controversy experience, she is a member of the IRS Tax Advocacy Panel and is well-versed in all areas of tax controversy. These include but are not limited to U.S. federal, state, and local tax audits; sales and use/payroll tax audits; international tax compliance related audits; negotiation and settlements with tax authorities; and corresponding and negotiation with tax authorities. Contact Renee at RParker@MGOCPA.com.

]]>Because of these newly tightened conditions, companies may face challenges when raising capital, forcing them to adopt a more thoughtful approach to seek funding. Likewise, investors will want to ensure their priorities are protected and their returns met. The combination of a given borrower’s need for capital and a financer’s desire to seek favorable returns may lead to the creation of agreements that have characteristics of both debt and equity. As such, it is crucial for all parties involved to understand the resulting tax classification and the treatment of these arrangements, so all expectations are met.

The taxation of debt and equity

For borrowers, the difference between debt and equity can be critical because interest payments are generally tax deductible and subject to certain limitations. Dividends or other payments related to equity would not be deductible for U.S. federal income tax purposes.

Enacted as part of the Tax Cuts and Job Act (TCJA) of 2017, one main limit on interest deductibility is the IRC 163(j) limit on the amount of business interest that can be deducted each year. This limit is calculated as 30 percent of adjusted taxable income, which prior to the 2022 tax year closely resembled earnings before interest, taxes, depreciation, and amortization (EBITDA). However, starting with the 2022 tax year adjusted taxable income excludes depreciation and amortization, becoming EBIT. This should result in a lower limit on the amount of interest expense that can be deducted each year. Any interest expense exceeding this annual limit can be carried forward to future years.

Determining if an arrangement is debt or equity for federal income tax purposes

Classifying an arrangement as debt or equity is made on a case-by-case basis depending on the facts and circumstances of a given agreement. While there is currently little guidance in this area beyond case law, the Internal Revenue Service (IRS) has issued a list of factors to consider when questioning whether something is debt or equity. (Keep in mind, however, that the IRS states not one factor is conclusive.) The factors include whether:

- An agreement contains an unconditional promise to pay a sum certain on demand or at maturity,

- A lender can enforce the payment of principal and interest by the borrower, and

- A borrower is thinly capitalized.

The courts have also established a broader — but similar — list of factors to consider when determining whether an instrument should be treated as debt or equity. Both the IRS and the courts have generally placed more weight on whether an instrument provides for the rights and remedies of a creditor, whether the parties intend to establish a debtor-creditor relationship, and if the intent is economically feasible. Some factors include:

- Participation in management (as a result of advances),

- Identity of interest between creditor and stockholder,

- Thinness of capital structure in relation to debt, and

- Ability of a corporation to obtain credit from outside sources.

For international companies, the characterization of debt or equity when considered in a cross-border funding arrangement is important, as withholding tax rates may apply to interest payments and may differ from tax rates applied to dividends. Further, withholding tax obligations occurs when a cash payment is made. If you have a cross-border arrangement, it is crucial to know if you have debt or equity on your hands.

Special rules related to payment-in-kind

Once it is determined that an agreement should be classified as debt for U.S. federal income tax purposes, some borrowers may prefer to set aside interest payments or pay interest with securities, which is often referred to as payment-in-kind (PIK). This is generally done to preserve cash flow for operations and growth of the business. When a borrower chooses this route, U.S. federal income tax rules will impute an interest payment to the lender.

While using a PIK mechanism will not automatically result in the debt being recharacterized as equity for federal income tax purposes, it can support viewing the instrument as equity.

Limits to deductible debt interest

There are limitations that can apply to interest deductibility. As noted above, IRC 163(j) limits deductibility of business interest; for a corporation, this is deemed to be all interest regardless of use. Another provision that can result in interest deductibility limitation is IRC 163(l), which applies to certain convertible notes and similar instruments held by corporations.

For cannabis operators, it is important to consider that IRC 280E disallows interest deductions. Hence, it is highly detrimental for cannabis operators to issue debt from entities that are cannabis plant-touching.

How we can help

Due to the nature of the debt versus equity analysis, companies thinking about fundraising should plan on how they intend to perform the raise and whether to have the raise treated as equity or debt. If debt classification is desired, a borrower should take the steps needed to strengthen the facts of the transaction to support the arrangement as a debt instrument.

MGO’s dedicated tax team has extensive experience advising companies across industries on capital-raising, debt refinancing and restructuring, recapitalizations, and other tax transactions. If you are planning to fundraise, or you are currently in the process of conducting a debt versus equity analysis, contact us today.

About the authors

Maryam Nicholes is a director and the national leader of MGO’s M&A Tax Advisory Services group. She has more than 13 years of experience advising on a wide range of clients, consulting on structuring and implementation of transactions including mergers, acquisitions and dispositions, global reorganizations, and new investment platforms. She also provides planning and related deal modeling regarding global cash tax exposures, repatriation planning, and related debt structuring and workout. Contact Maryam at MNicholes@mgocpa.com.

Matt Sapowith is a tax partner at MGO. He has more than 14 years of tax planning and compliance experience in areas including corporate and partnership taxation, international tax, M&A transaction advisory, transfer pricing, state and local tax, R&D credit, and compensation planning. He assists companies with structuring for multiple business lines, excise tax and sales tax planning and compliance in a variety of industries including technology, financial services, manufacturing and distribution, professional services, retail and consumer goods, cannabis, and cryptocurrency. Contact Matt at MSapowith@mgocpa.com.

]]>- Increasing Internal Revenue Service (IRS) budget

- Implementing a corporate tax minimum

- Instituting and increasing tax credits focused on investing in green technologies

Notable items that were not addressed in the IRA include removing the $10,000 SALT cap and mandatory capitalization of research and development (R&D) expenses, both provisions of the Tax Cuts and Jobs Act of 2017.

The bill is over 300 pages in length with a number of wide-ranging components. In the following summary we’ll provide the key points that will be affecting taxpayers in the coming years.

Additional funding to the IRS for tax enforcement

One of the most talked-about provisions involves increased funding for the IRS.

Key details:

- Approximately $80 billion in funding over the next 10 years for tax services, operations support, business system modernization, and enforcement

- Enforcement – $46 billion

- Operations support – $25 billion

- Business systems modernization – $5 billion

- Taxpayer services – $3 billion

- An estimated $124 to $200 billion will be generated from enforcement and compliance efforts

- Enforcement is focused on taxpayers – both corporate and non-corporate – with income greater than $400,000

Extension of the business loss limitation of noncorporate taxpayers

The IRA extends the excess business loss limitation for noncorporate taxpayers.

Key details:

- Two year extension on IRC Sec. 461(l) until December 31, 2028

- IRC Sec. 461(l) limits noncorporate taxpayers from deducting business losses above thresholds that are annually indexed for inflation

- These limits are $540,000 for married filing jointly and $270,000 for single and married filing single for the 2022 tax year

- Suspended amounts are converted to net operating losses and may be able to be used in subsequent years

Excise tax on repurchases of corporate stock

The IRA includes a 1% excise tax on stock repurchases by domestic public companies listed on an established securities market. The tax applies to repurchases executed after December 31st, 2022.

Key details:

- 1% excise tax on the full market value (FMV) of stock repurchased by publicly traded US corporations

- Will impact redemptions and certain acquisitions and repurchases of publicly traded foreign corporation stock

- Not an income tax for purposes of ASC 740

- Includes special rules for “applicable foreign corporations” and “surrogate foreign corporations”

- Notable exceptions:

- Stock is contributed to employer sponsored retirement plan

- Stock repurchase is part of a corporate reorganization

- Total value of stock repurchased during the taxable year does not exceed $1 million

- Repurchase by securities dealer in ordinary course of business

- If the repurchase qualifies as a dividend

- If the repurchase is by a regulated investment company (RIC) or a real estate investment trust (REIT)

15% corporate alternative minimum tax

The IRA reinstates the corporate alternative minimum tax (AMT) for large corporations, which had been previously eliminated by the Trump Administration’s Tax Cuts and Jobs Act.

Two key elements to note is that this revised AMT only impacts corporations with annual profits exceeding $1 billion, and includes carve-outs for certain manufacturers and subsidiaries of private equity firms.

Key details:

- 15% tax on adjusted financial statement income (i.e., this would be a book minimum tax)

- Affects tax years beginning after December 31, 2022

- Applies to corporations with profits over $1 billion based off adjusted financial income

- For US corporations with foreign parents, it would apply to income earned in the US of $100 million or more of average annual earnings in three prior years and where the overall international financial reporting group has income of $1 billion or more

- Treatment of split offs remains uncertain. Even though these are tax-free reorganizations for tax purposes, gain is recorded for financial accounting purposes

- Joint Committee on Taxation expects that this new tax would apply to only about 150 corporate taxpayers, approximately equal to 30% of the Fortune 500

Tax credit additions and modifications

A significant number of provisions add or enhance credits and incentives that pertain to domestic research and green energy initiatives. Noteworthy changes include:

Increased small business payroll tax credits for research activities:

- Qualified payroll tax credit for increasing research activities raised from $250,000 to $500,000

- First $250,000 will be applied against the FICA payroll tax liability. Second $250,000 will be applied against the employer portion of Medicare payroll tax.

- Applies for taxable years beginning after December 31, 2022

- Limited to tax imposed for calendar quarter with unused amounts being carried forward

- Qualifying small businesses are required to have less than $5 million in gross receipts in current year and no gross receipts prior to the 5 year period ending with the current year

Green initiative tax credits and incentives:

- Credits for purchasing new and previously-owned clean vehicles

- Extension of IRC Sec. 45L – New Energy Efficient Home Credit – extended to qualified new energy efficient homes acquired before January 1, 2033. Increase value of available credit for single-family homes to $2,500 and modified the credit available for multi-family homes.

- Extension, increase, and modifications to IRC Sec. 25C nonbusiness energy property credit

- Extension and modification of IRC Sec. 25D residential clean energy credit

- IRC Sec. 48 energy credit for businesses and investors

- Expansion of qualifying property, extension of credit including phasedown and phaseout rules, and introduction of incentives

- Credit for producing energy from renewable sources (IRC Sec. 45)

- Retroactive for facilities placed in service after December 31, 2021

- Extends beginning of construction deadline to projects beginning construction before January 1, 2025 including solar energy facilities

- Increased energy credit for solar and wind facilities in certain low-income communities

- New credit for clean hydrogen production

- New credit for zero-emission nuclear power

- Extension of incentives for biodiesel, renewal diesel, and alternative fuels

- Extension of biofuel producer credit

- New income and excise tax credits allowed for sustainable aviation fuel

- Modification of IRC Sec. 179D – Energy Efficient Commercial Buildings Deductions

- Modification of building qualifications

- Deduction increased from $1.88 per square foot to up to $5 per qualified square foot

- Changes in depreciation for certain green energy properties

Final thoughts

The Inflation Reduction Act should have wide-ranging impacts on taxpayers, especially large corporations and high-net-worth individuals. In the coming weeks our tax leaders will dive into the specifics of the legislation, outline immediate and long-term impacts, and provide tax-planning strategies and considerations.

]]>Specific scams that mask as abusive or fraudulent tax avoidance strategies to be aware of include concealing assets in offshore accounts and improper reporting of digital assets, manipulation of high-income taxpayers to file their tax returns, abusive syndicated conservation easements, and abusive micro-captive insurance arrangements. Read more to round out the annual list for the 2022 filing season.

Tips for taxpayers on emerging scams

To avoid compromising yourself with these “too good to be true” schemes, taxpayers should stay wary, as these scams adopt a wide range of communication methods, including:

- Emails

- Phone calls

- Social media posts

- Targeted online advertisements

You must also consider each source before putting any of these arrangements on your tax returns — because ultimately, you are the one responsible for what is on the return, not the promoter who reached out to you and made a promise they failed to uphold. To mitigate risk, an anxious taxpayer should turn to trustworthy tax professionals to assist with their returns.

Read on to learn about these Dirty Dozen scams targeted primarily to high-net-worth individuals who may be trying to knowingly — or unknowingly — avoid filing.

Scam #9: Concealing Assets in Offshore Accounts and the Improper Reporting of Digital Assets

We hear Switzerland is beautiful this time of year … and so do some high-net-worth individuals looking to conceal their assets in offshore accounts (and yes, that does include cryptocurrency and other digital assets). As more taxpayers look to complex international tax avoidance schemes, the IRS is more determined than ever to “protect the integrity of the U.S. tax system” by enforcing tax responsibilities.

Whether it entails offshore banks, brokerage accounts, nominee entities, employee leasing schemes, foreign trusts, structured transactions, or private annuities, all are designed to hide the true owner of an account — which is illegal, considering U.S. taxpayers are taxed on all the income they make, not just what they keep in the country. But scammers know you may not want to give up some of your hard-earned assets to Uncle Sam. So, what do they do? They sell you a convincing story: you can easily evade the government and hide your assets through digital asset holdings; they claim these are “undetectable by tax authorities.” The catch? They are definitely detectable. By believing these fraudsters, you run the risk of being criminally charged or penalized, so in the end, it is better to report your assets — yes, all of them — when you file.

Scam #10: High-Income Individuals Who Don’t File Tax Returns

Believe it or not, there are some taxpayers who choose to just … not file a tax return. And believe it or not, there are scamming professionals out there aiming to convince you this is a good idea. The IRS takes this seriously. If you are considering this option, remember the Failure to File Penalty is higher than the Failure to Pay Penalty, meaning you are better off filing an accurate, timely return (and setting up a payment plan, if you are concerned about that) rather than not filing and hoping you get out of paying whatever taxes you owe.

Scam #11: Abusive Syndicated Conservation Easements

In this scam, dishonest promoters manipulate a part of the tax law that allows for conservation easements by inflating appraisals of underdeveloped land (i.e., the guise of a real estate investment) and engaging in bogus partnerships without a business purpose. These “deals” rarely help you out; instead, they benefit the promoters, who charge high fees, and clog the tax system with fraudulent tax deductions. (In the last five years, the IRS determined billions of dollars of deductions were wrongly claimed!) And if you are caught — which, you should expect to be, because the IRS takes a microscope to every single one of these “deals” — you can expect large fines and potential time in court.

Scam #12: Abusive Micro-Captive Insurance Arrangements

A high priority for the IRS, this scam sees professionals like accountants and wealth planners convince entity owners to pay for what they believe to be insurance coverage against unlikely events, events that are already being covered, or disingenuous business needs. Complete with sky-high premiums, the abusive structure does the opposite of protecting your organization’s tax safety — it opens you up to more risk as a ”micro-captive” to these “professionals” taking advantage of you. Be on the lookout for an offshore version of this too.

Consequences of falling for a Dirty Dozen scheme

It is important for taxpayers who have already taken part in transactions like these — or those who are thinking about doing so — to consult a tax professional before claiming any tax benefits they think they are owed.

Those taxpayers who have already claimed the purported tax benefits of one of these four “Dirty Dozen” arrangements on a tax return should file an amended return and go to an independent professional for guidance. If necessary, the IRS will examine the tax benefits from transactions like the ones depicted in the list and inflict penalties related to accuracy ranging from 20% to 40%, or a civil fraud penalty of 75% on any taxpayer who underpaid.

Our perspective on the latest batch of “Dirty Dozen” scams

This is not, of course, an exhaustive list of every scam the IRS has its eye on this year. But it does include some of the more common trends. The best advice we can give? If something looks too good to be true … it probably is. Consult your tax professional for guidance and know that it is in your best interest to stay aware of these nefarious arrangements, so you do not fall susceptible to additional penalties.

And remember, you cannot hide income from the IRS!

MGO’s Tax team brings more than 30 years of experience and is well versed in reviewing your return for compliance. We also stay up to date on the risks, pitfalls, and warnings issued by the IRS so you don’t have to. If you think you have been involved in or are in the process of being involved in one of the Dirty Dozen scams, we can help. Contact us today.

]]>Accelerate and defer with care

One of the most reliable year-end tactics for reducing taxes has long been to accelerate your deductible expenses and defer your income. For example, self-employed individuals who use cash-basis accounting can delay invoices until late December and move up the planned purchase of equipment or the payment of estimated state income taxes from early next year to this year.

This technique has always carried the caveat that you generally shouldn’t pursue it if you expect to be in a higher tax bracket the following year. Potential provisions in the BBBA also may make it advisable for certain taxpayers to reverse the strategy for 2021 — that is, accelerate income and defer deductible expenses.

The current version of the BBBA would impose a new “surtax” of 5% on modified adjusted gross income (MAGI) that exceeds $10 million, with an additional 3% on income of more than $25 million. As a result, the highest earners could pay a 45% federal marginal income tax on wages and business income (the current 37% income tax rate plus 8%). It could be even higher when combined with the net investment income tax, which might be expanded to include active business income for pass-through entities.

In addition, there’s a proposal to temporarily increase the $10,000 cap on the state and local tax deduction to $80,000. Individuals in high-tax states should consider whether there may be an advantage to accelerating a 2022 property or estimated state income tax payment into 2021, or whether the deduction might be more valuable next year, particularly if they’ll face a higher effective tax rate.

Leverage your losses

Taxpayers with substantial capital gains in 2021 could benefit from “harvesting” their losses before year-end. Capital losses can be used to offset capital gains, and up to $3,000 ($1,500 for married persons filing separately) of excess losses (those that exceed the amount of gains for the year) can be applied against ordinary income. Any remaining losses can be carried forward indefinitely.

Beware, however, of the wash-sale rule. Generally, the rule prohibits the deduction of a loss if you acquire “substantially identical” investments within 30 days, before or after, of the date of the sale.

Taxpayers who itemize their deductions could compound their tax benefits by donating the proceeds from the sale of a depreciated investment to a charity. They can both offset realized gains and claim a charitable contribution deduction for the donation.

Satisfy your charitable inclinations

For 2021, charitable contributions can reduce taxes for both itemizers and non-itemizers. Taxpayers who take the standard deduction can claim an above-the-line deduction of $300 ($600 for married couples filing jointly) for cash contributions to qualified charitable organizations.

The adjusted gross income limit for cash donations is 100% for 2021; it’s scheduled to return to 60% for 2022. That means you could offset all of your taxable income with charitable contributions this year. (Donations to donor advised funds and private foundations don’t qualify, though.)

Taxpayers who don’t generally itemize can benefit by “bunching” their charitable contributions. In other words, delaying or accelerating contributions into a tax year to exceed the standard deduction and claim itemized deductions. For example, if you usually make your donations at the end of the year, you could bunch donations in alternative years — say, donate in January and December of 2022 and January and December of 2024.

Retired taxpayers who are age 70½ and older can reduce their taxable income by making qualified charitable contributions of up to $100,000 from their non-Roth IRAs. Retired or not, individuals age 72 and older can use such contributions to satisfy their annual required minimum distributions (RMDs). Note that RMDs were suspended for 2020 but are effective for 2021.

So long as the assets would be considered long-term if they were sold, donations of appreciated assets offer a double-barreled tax benefit. You avoid the capital gains tax on the appreciation and can deduct the asset’s fair market value as of the date of the gift.

Convert traditional IRAs to Roth IRAs

As in 2020, when many taxpayers saw lower than typical income, 2021 could be a smart time to convert funds in traditional pre-tax IRAs to an after-tax Roth IRA. Roth IRAs have no RMDs, and distributions are tax-free.

You’ll have to pay income tax on the converted funds, but it’s better to do so while subject to lower tax rates. Similarly, if you convert securities that have dropped in value, your tax may well be lower now than down the road — and any subsequent appreciation while in the Roth IRA will be tax-free.

It’s worth noting that President Biden had proposed including a provision in the BBBA that would limit the ability of wealthy individuals to engage in Roth conversions. There was a lot of back-and-forth with respect to these provisions, and the latest version of the House bill includes certain restrictions. Whether these provisions will make it past any Senate amendments remains to be seen, but the proposal could be a harbinger of future proposed restrictions.

Proceed with caution

The strategies outlined above always come with pros and cons, but perhaps never more so than now, when potentially significant tax legislation that would take effect next year is under negotiation. We can help you chart the best course in light of any developments.

]]>Employee Retention Tax Credit

The Employee Retention Tax Credit (ERTC) is a refundable tax credit created by the Coronavirus Aid, Relief and Economic Security (CARES) Act, to encourage businesses to keep employees on their payroll. For 2020, the credit is 70% of up to $10,000 in wages paid by an employer whose business was fully or partially suspended because of COVID-19 or whose gross receipts declined by more than 50%

For 2021, an employer can receive 70 percent of the first $10,000 of qualified wages paid per employee in each qualifying quarter. The credit applies to wages paid from March 13, 2020, through December 31, 2021. And the cost of employer-paid health benefits can be considered part of employees’ qualified wages.

It’s an attractive credit if you qualify.

Eligible businesses

The credit applies to all employers regardless of size, including tax exempt organizations that had a full or partial shutdown because of a government order limiting commerce due to COVID-19 during 2020 or 2021. With the exceptions of state and local governments or small businesses that take Small Business Administration loans, this credit is available to almost everyone.

Of course, there is some fine print:

• To qualify, gross receipts must have declined more than 50 percent during a 2020 or 2021 calendar quarter, when compared to the same quarter in the prior year.

• For employers with 100 or fewer full-time employees, all employee wages qualify for the credit, whether the employer is open for business or shutdown.

• For employers with more than 100 full-time employees, qualified wages are wages paid to employees when they are not providing services due to COVID-19-related circumstances.

One bright point about the ERTC is that employers can be immediately reimbursed for the credit by reducing the amount of payroll taxes they would usually have withheld from employees’ wages. That was a nice touch by the IRS.

Retroactive claims for the ERTC

Although it appears the IRS tried to make this as easy as possible, you may still need a tax professional to sort it out. For instance, if your business had a substantial decline in gross receipts but has now recovered, you can still claim the credit for the difficult period

Retroactive claims for refunds will probably be delayed because currently everything is delayed at the IRS. The credit can be claimed on amended payroll tax returns as long as the statute of limitations remains open, which is three years from the date of filing. So you have some time to claim the credit, but why wait?

Keep December 2021 in mind

The economy is in a state of change, and it is fair to say that we are once again in uncharted territory. On the positive side, there seems to be significant resources and support for businesses from both government and consumers. You and your tax professional should keep your eyes open for credits and benefits to make sure you don’t miss any opportunitie

The ERTC expires in December 2021. Though it may be difficult to think about year-end in the middle of the summer, you’ll want to figure out your position on this credit before December. A tax professional can help you understand the ERTC and help you decide on your next step.

About the author

Michael Silvio is a partner at MGO. He has more than 25 years of experience in public accounting and tax and has served a variety of public and private businesses in the manufacturing, distribution, pharmaceutical, and biotechnology sectors.

]]>Of the long list of relief efforts, one of the most significant changes for businesses small and large was not something new, but rather a correction to the Tax Cuts and Jobs Act (TCJA) of 2018 regarding qualified improvement property (QIP). Here’s why that minor fix could have a major impact by providing much-needed liquidity in the midst of a pandemic.

Understanding the “Retail Glitch”

As the TCJA came together, Congress added language that renewed 100% bonus depreciation for QIP that was acquired after September 23, 2018, and began being used by January 1, 2023. This is depreciation that included properties that had a life of up to 20 years. During the whirlwind drafting sessions that took place before the bill was finalized, drafters failed to include an amendment that included a 15-year recovery period for QIP, even though it was clear they had intended to do so. The omission, known as the “Retail Glitch,” meant that QIP was subject to a 39-year recovery period rather than the intended 15, and that businesses would not be able to write it off.

Fixing the glitch

The CARES Act addressed the error in the TCJA by including QIP as a 15-year MACRS asset and 20-year ADS asset, allowing businesses in hard-hit industries like hospitality, retail, and restaurants, to retroactively write-off any investments they have made into their spaces dating back to the enactment of the TCJA on December 22, 2017. The impact of this is significant, as fixing the error allows leaseholders and building owners to immediately retrieve the costs of improvement-related investments they have made in their property since December 2017, which are now classified as bonus depreciation under the CARES Act.

Why QIP changes are critical

This provision of the CARES Act is so important because it is an immediate injection of cash to thousands of businesses who are likely experiencing severe cash flow issues. The QIP classification includes any renovation to the interior of a non-domicile property that was made after the building began business use and applies mostly to industries that often revamp their facilities. Additionally, because the bill is retroactive, it is likely that many businesses will be able to access liquidity from several past projects, allowing them to potentially further ease financial burdens.

Getting the cash

As with any major piece of legislation, specifics on how to access the depreciation that the CARES Act entitles business owners to is scarce. However, industry professionals have found several methods to file for the money, the simplest of which is to work with your tax services provider to file amended returns for tax years 2018 and 2019. Other options exist as well, including filing superseding returns or filing a Form 3115, which is an application for change in accounting method. Because the QIP change will have widespread effects, it is anticipated that when the IRS issues formal guidance they will automatically allow the change to be made.

Small businesses and corporate America alike are struggling at this moment, and the future is uncertain. Taking advantage of the QIP amendment to the tax code is strategically imperative for any business that needs a boost in financial health in the short and long term.

For guidance applying the new QIP changes or filing amended tax returns, please reach out to schedule a consultation.

]]>Details of California’s nexus law

California used the South Dakota law as a relative guide, where the threshold – or nexus – for collecting taxes by online retailers begins once sales reach $100,000 or 200 transactions in the state. California instructs retailers to begin collecting the 7.25% state tax on the sale of tangible personal property for delivery into the California once sales reach $500,000, but with no transaction threshold.

Furthermore, Special Notice L-591 was issued by the CDTFA to also take effect on April 1. This notice requires retailers to collect local use taxes once a threshold of $100,000 or 200 transactions has been reached within that locality or district, regardless of sales or transactions in another district within the state.

Another component of the new law addresses the sale of goods to California residents through platforms such as Amazon, eBay, Etsy and others, where the platform or “marketplace” facilitates the transaction. The marketplace facilitator must register as a seller with the CDTFA, collect sales tax on behalf of the seller, and remit the tax to the California tax department. This particular phase of the law is not scheduled to become effective until October 1, 2019.

Although the new California law will undoubtedly impact many online retailers, there is a provision that may provide some relief to smaller businesses. The temporary provision states that for businesses selling tangible personal property into California that is less than $1 million through the tax period ending December 31, 2022, taxes and fees may be waived by the CDFTA if the retailer registers with the state and was not required to do so prior to the law becoming effective.

More complications for retailers

It is estimated that anywhere from $1 billion to $2 billion of tax revenue went uncollected from out of state retailers and that the new law could provide an additional $500 million in tax revenue to the state.

Much of this depends on how simple California makes the tracking, reporting and payment of tax revenue by online retailers. While the collection of revenue based on a single, state-wide tax rate might be simple enough, the additional district taxes may potentially add complexity to the issue, making it more difficult to collect. Some states are offering allowances when retailers use automated tax software to track and collect taxes and not holding the retailer accountable if mistakes are made due to the software. This may be relatively easy at the state level but difficult at the district level, as every address must adhere to the latest zoning requirements for specific districts while also ensuring alignment according to the tax software being used.

What consumers must understand

For consumers in California, there may not be a significant change in the rate in which they buy online, as many are already paying sales tax on goods purchased this way. Any concern consumers have regarding a revoking of the Internet Tax Freedom Act (ITFA) should be alleviated, as the ITFA only prohibits states from levying tax on internet access, not the sale of tangible personal property.

It is likely that California will see additional tax revenue with the implementation of this new law. How much revenue will remain to be seen, especially with the $500,000 threshold as well as the provisional leniency for smaller businesses until 2022.

]]>