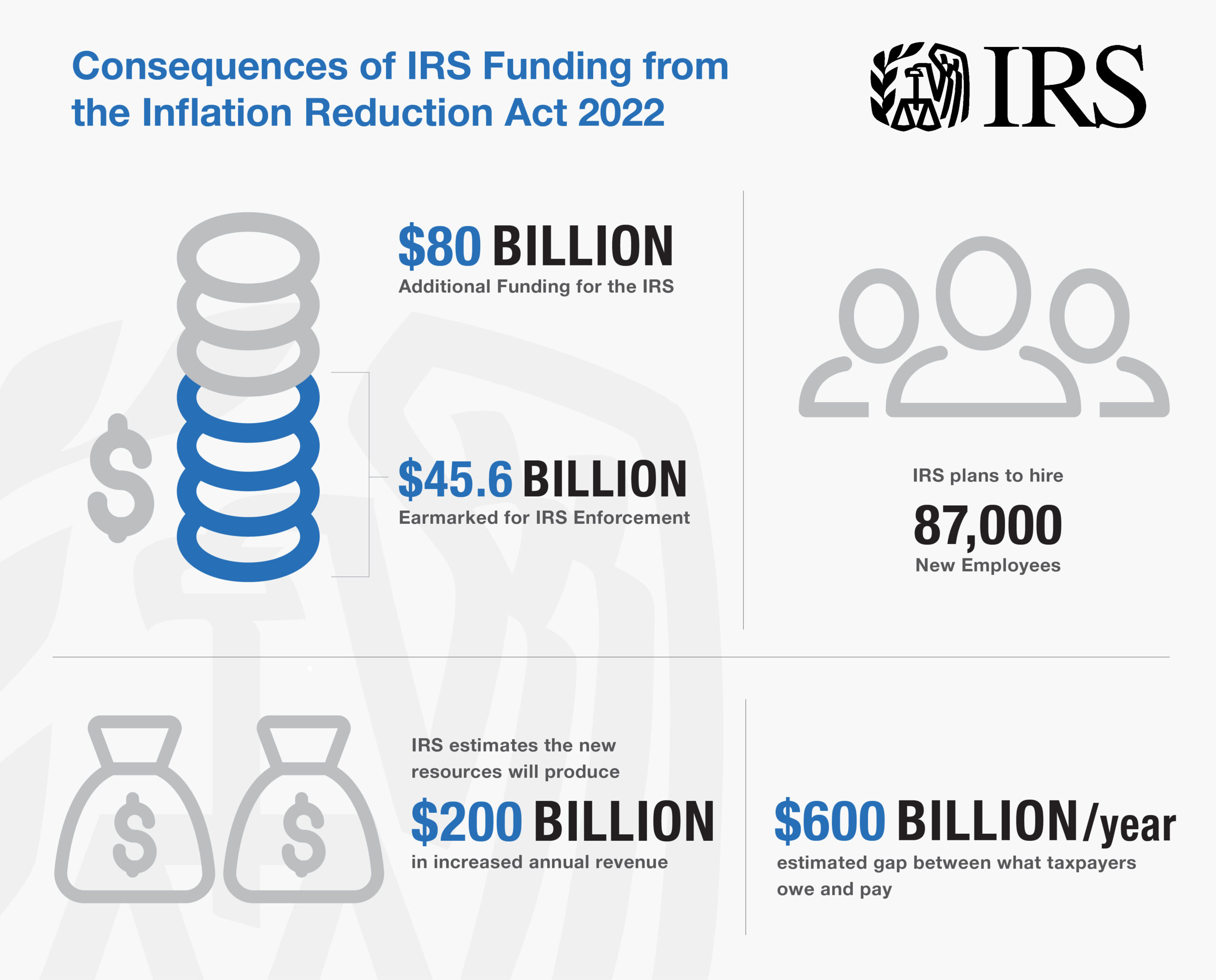

- The Inflation Reduction Act of 2022 includes $80B in funding for the Internal Revenue Service.

- Over half of the funding will be set aside for IRS enforcement so the agency can hire more staff to conduct more audits, hoping to target those who do not pay their taxes.

- This will most likely subject those taxpayers with complex filings to additional scrutiny.

The Inflation Reduction Act of 2022 was recently signed into law with an eye-opening provision: the inclusion of nearly $80 billion in additional funding for the Internal Revenue Service (IRS). $45.6 billion of that is earmarked for IRS enforcement, which will be used to help the underfunded agency hire additional staff and conduct future audits in the hopes of collecting unpaid taxes.

Many publications cite the IRS plans to hire up to 87,000 new employees, though the actual number will be released in the coming months. These new hires will fill positions ranging from auditors to customer service representatives to IT specialists. The IRS has been plagued by more than a decade of budget cuts, which has limited its ability to modernize its old technology and staff appropriately. Since 2010, the agency’s enforcement staff has declined by 30%. The funding appropriate in the Inflation Reduction Act hopes to reverse this trend and bring in an estimated $203 billion in increased revenue.

The MGO Tax Controversy team breaks down what you need to know about this big change that could increase your risk of an audit.

How will the increase in IRS staff affect taxpayers?

Critics of the increase in IRS funding have claimed that the new resources will be used to target low to middle-income Americans and small businesses, burdening them with more audits and examinations. The Treasury Department refutes these claims reiterating they plan to focus primarily on large corporations and the wealthy — those more likely to evade paying their taxes — to close the tax gap, or the difference between what taxpayers pay in taxes and what they actually owe – an estimated to be $600 billion per year.

The IRS hopes the investment in funding will bring in around $203.7 billion in revenue because between 2015 and 2019, IRS audits declined significantly — 75% for Americans making $1 million or more and 33% for filers with low to moderate incomes. Lower-income Americans are mostly wage earners, so their audits are less complex and can be automated. However, more complex filers, notably large corporations and high-net-worth individuals and families – require the hands-on engagement of IRS agents and are most likely to experience increased levels of scrutiny from the new hires.

Ultimately, the average taxpayer should have an improved tax filing experience. New staff will be on hand to answer questions by phone, technology systems will be improved and modernized, and the backlog of unprocessed returns should diminish.

What is the timeline for implementing these changes?

While there is no set timeline, it is likely the way IRS audits work will change with the increase in funding. Currently, software is used to rank each tax return with a numeric score, and higher scores trigger an audit. Other mechanisms the IRS uses to determine candidates for audits include enforcement initiatives referred to as “campaigns” based on various criteria. The new funding will take time to phase in, and so will the hiring and training of new workers. It is expected new auditors will complete a six-month training program, starting small with cases involving a few hundred thousand dollars instead of tens of millions. Forbes performed some creative math to conclude while the funding will increase IRS audits, it is not likely to occur for the next few years.

How can I avoid future audits?

The best way to avoid an audit remains simple: pay your taxes on time and in compliance with tax laws. Simple accounting and documentation best practices are your best friend. If you feel you are at risk for a potential audit, you’ll want to get a head start now by ensuring your records are accurate and have been updated and maintained. Save your receipts and include every detail you can in your bookkeeping logs. If you do get audited in the coming wave, you’ll be glad you have all of this information organized and on-hand.

Our perspective on the increase in IRS staffing

The IRS has long been criticized because of their inability to provide taxpayers with the level and quality of service they deserve. The increase in funding as part of the Inflation Reduction Act should help. On the other hand, the number of tax audits is likely to increase, and you will want to be ready.

MGO’s dedicated Tax Controversy team can help by providing a holistic look at your tax filings as well as provide guidance for conflict resolution. From prevention to resolution, we guide you every step of the way.

If you’re an operator or investor in the cannabis industry, our Tax Practice recently published the Cannabis IRS Audit Survival Guide, which details everything you need to do to prepare for and navigate a tax audit. You can download the Guide for free here.

About the author

T. Renee Parker is a tax partner and the National Tax Controversy Practice Leader at MGO. With more than 15 years of tax controversy experience, she is a member of the IRS Tax Advocacy Panel and is well-versed in all areas of tax controversy. These include but are not limited to U.S. federal, state, and local tax audits; sales and use/payroll tax audits; international tax compliance related audits; negotiation and settlements with tax authorities; and corresponding and negotiation with tax authorities. Contact Renee at RParker@MGOCPA.com.

]]>Because of these newly tightened conditions, companies may face challenges when raising capital, forcing them to adopt a more thoughtful approach to seek funding. Likewise, investors will want to ensure their priorities are protected and their returns met. The combination of a given borrower’s need for capital and a financer’s desire to seek favorable returns may lead to the creation of agreements that have characteristics of both debt and equity. As such, it is crucial for all parties involved to understand the resulting tax classification and the treatment of these arrangements, so all expectations are met.

The taxation of debt and equity

For borrowers, the difference between debt and equity can be critical because interest payments are generally tax deductible and subject to certain limitations. Dividends or other payments related to equity would not be deductible for U.S. federal income tax purposes.

Enacted as part of the Tax Cuts and Job Act (TCJA) of 2017, one main limit on interest deductibility is the IRC 163(j) limit on the amount of business interest that can be deducted each year. This limit is calculated as 30 percent of adjusted taxable income, which prior to the 2022 tax year closely resembled earnings before interest, taxes, depreciation, and amortization (EBITDA). However, starting with the 2022 tax year adjusted taxable income excludes depreciation and amortization, becoming EBIT. This should result in a lower limit on the amount of interest expense that can be deducted each year. Any interest expense exceeding this annual limit can be carried forward to future years.

Determining if an arrangement is debt or equity for federal income tax purposes

Classifying an arrangement as debt or equity is made on a case-by-case basis depending on the facts and circumstances of a given agreement. While there is currently little guidance in this area beyond case law, the Internal Revenue Service (IRS) has issued a list of factors to consider when questioning whether something is debt or equity. (Keep in mind, however, that the IRS states not one factor is conclusive.) The factors include whether:

- An agreement contains an unconditional promise to pay a sum certain on demand or at maturity,

- A lender can enforce the payment of principal and interest by the borrower, and

- A borrower is thinly capitalized.

The courts have also established a broader — but similar — list of factors to consider when determining whether an instrument should be treated as debt or equity. Both the IRS and the courts have generally placed more weight on whether an instrument provides for the rights and remedies of a creditor, whether the parties intend to establish a debtor-creditor relationship, and if the intent is economically feasible. Some factors include:

- Participation in management (as a result of advances),

- Identity of interest between creditor and stockholder,

- Thinness of capital structure in relation to debt, and

- Ability of a corporation to obtain credit from outside sources.

For international companies, the characterization of debt or equity when considered in a cross-border funding arrangement is important, as withholding tax rates may apply to interest payments and may differ from tax rates applied to dividends. Further, withholding tax obligations occurs when a cash payment is made. If you have a cross-border arrangement, it is crucial to know if you have debt or equity on your hands.

Special rules related to payment-in-kind

Once it is determined that an agreement should be classified as debt for U.S. federal income tax purposes, some borrowers may prefer to set aside interest payments or pay interest with securities, which is often referred to as payment-in-kind (PIK). This is generally done to preserve cash flow for operations and growth of the business. When a borrower chooses this route, U.S. federal income tax rules will impute an interest payment to the lender.

While using a PIK mechanism will not automatically result in the debt being recharacterized as equity for federal income tax purposes, it can support viewing the instrument as equity.

Limits to deductible debt interest

There are limitations that can apply to interest deductibility. As noted above, IRC 163(j) limits deductibility of business interest; for a corporation, this is deemed to be all interest regardless of use. Another provision that can result in interest deductibility limitation is IRC 163(l), which applies to certain convertible notes and similar instruments held by corporations.

For cannabis operators, it is important to consider that IRC 280E disallows interest deductions. Hence, it is highly detrimental for cannabis operators to issue debt from entities that are cannabis plant-touching.

How we can help

Due to the nature of the debt versus equity analysis, companies thinking about fundraising should plan on how they intend to perform the raise and whether to have the raise treated as equity or debt. If debt classification is desired, a borrower should take the steps needed to strengthen the facts of the transaction to support the arrangement as a debt instrument.

MGO’s dedicated tax team has extensive experience advising companies across industries on capital-raising, debt refinancing and restructuring, recapitalizations, and other tax transactions. If you are planning to fundraise, or you are currently in the process of conducting a debt versus equity analysis, contact us today.

About the authors

Maryam Nicholes is a director and the national leader of MGO’s M&A Tax Advisory Services group. She has more than 13 years of experience advising on a wide range of clients, consulting on structuring and implementation of transactions including mergers, acquisitions and dispositions, global reorganizations, and new investment platforms. She also provides planning and related deal modeling regarding global cash tax exposures, repatriation planning, and related debt structuring and workout. Contact Maryam at MNicholes@mgocpa.com.

Matt Sapowith is a tax partner at MGO. He has more than 14 years of tax planning and compliance experience in areas including corporate and partnership taxation, international tax, M&A transaction advisory, transfer pricing, state and local tax, R&D credit, and compensation planning. He assists companies with structuring for multiple business lines, excise tax and sales tax planning and compliance in a variety of industries including technology, financial services, manufacturing and distribution, professional services, retail and consumer goods, cannabis, and cryptocurrency. Contact Matt at MSapowith@mgocpa.com.

]]>- Increasing Internal Revenue Service (IRS) budget

- Implementing a corporate tax minimum

- Instituting and increasing tax credits focused on investing in green technologies

Notable items that were not addressed in the IRA include removing the $10,000 SALT cap and mandatory capitalization of research and development (R&D) expenses, both provisions of the Tax Cuts and Jobs Act of 2017.

The bill is over 300 pages in length with a number of wide-ranging components. In the following summary we’ll provide the key points that will be affecting taxpayers in the coming years.

Additional funding to the IRS for tax enforcement

One of the most talked-about provisions involves increased funding for the IRS.

Key details:

- Approximately $80 billion in funding over the next 10 years for tax services, operations support, business system modernization, and enforcement

- Enforcement – $46 billion

- Operations support – $25 billion

- Business systems modernization – $5 billion

- Taxpayer services – $3 billion

- An estimated $124 to $200 billion will be generated from enforcement and compliance efforts

- Enforcement is focused on taxpayers – both corporate and non-corporate – with income greater than $400,000

Extension of the business loss limitation of noncorporate taxpayers

The IRA extends the excess business loss limitation for noncorporate taxpayers.

Key details:

- Two year extension on IRC Sec. 461(l) until December 31, 2028

- IRC Sec. 461(l) limits noncorporate taxpayers from deducting business losses above thresholds that are annually indexed for inflation

- These limits are $540,000 for married filing jointly and $270,000 for single and married filing single for the 2022 tax year

- Suspended amounts are converted to net operating losses and may be able to be used in subsequent years

Excise tax on repurchases of corporate stock

The IRA includes a 1% excise tax on stock repurchases by domestic public companies listed on an established securities market. The tax applies to repurchases executed after December 31st, 2022.

Key details:

- 1% excise tax on the full market value (FMV) of stock repurchased by publicly traded US corporations

- Will impact redemptions and certain acquisitions and repurchases of publicly traded foreign corporation stock

- Not an income tax for purposes of ASC 740

- Includes special rules for “applicable foreign corporations” and “surrogate foreign corporations”

- Notable exceptions:

- Stock is contributed to employer sponsored retirement plan

- Stock repurchase is part of a corporate reorganization

- Total value of stock repurchased during the taxable year does not exceed $1 million

- Repurchase by securities dealer in ordinary course of business

- If the repurchase qualifies as a dividend

- If the repurchase is by a regulated investment company (RIC) or a real estate investment trust (REIT)

15% corporate alternative minimum tax

The IRA reinstates the corporate alternative minimum tax (AMT) for large corporations, which had been previously eliminated by the Trump Administration’s Tax Cuts and Jobs Act.

Two key elements to note is that this revised AMT only impacts corporations with annual profits exceeding $1 billion, and includes carve-outs for certain manufacturers and subsidiaries of private equity firms.

Key details:

- 15% tax on adjusted financial statement income (i.e., this would be a book minimum tax)

- Affects tax years beginning after December 31, 2022

- Applies to corporations with profits over $1 billion based off adjusted financial income

- For US corporations with foreign parents, it would apply to income earned in the US of $100 million or more of average annual earnings in three prior years and where the overall international financial reporting group has income of $1 billion or more

- Treatment of split offs remains uncertain. Even though these are tax-free reorganizations for tax purposes, gain is recorded for financial accounting purposes

- Joint Committee on Taxation expects that this new tax would apply to only about 150 corporate taxpayers, approximately equal to 30% of the Fortune 500

Tax credit additions and modifications

A significant number of provisions add or enhance credits and incentives that pertain to domestic research and green energy initiatives. Noteworthy changes include:

Increased small business payroll tax credits for research activities:

- Qualified payroll tax credit for increasing research activities raised from $250,000 to $500,000

- First $250,000 will be applied against the FICA payroll tax liability. Second $250,000 will be applied against the employer portion of Medicare payroll tax.

- Applies for taxable years beginning after December 31, 2022

- Limited to tax imposed for calendar quarter with unused amounts being carried forward

- Qualifying small businesses are required to have less than $5 million in gross receipts in current year and no gross receipts prior to the 5 year period ending with the current year

Green initiative tax credits and incentives:

- Credits for purchasing new and previously-owned clean vehicles

- Extension of IRC Sec. 45L – New Energy Efficient Home Credit – extended to qualified new energy efficient homes acquired before January 1, 2033. Increase value of available credit for single-family homes to $2,500 and modified the credit available for multi-family homes.

- Extension, increase, and modifications to IRC Sec. 25C nonbusiness energy property credit

- Extension and modification of IRC Sec. 25D residential clean energy credit

- IRC Sec. 48 energy credit for businesses and investors

- Expansion of qualifying property, extension of credit including phasedown and phaseout rules, and introduction of incentives

- Credit for producing energy from renewable sources (IRC Sec. 45)

- Retroactive for facilities placed in service after December 31, 2021

- Extends beginning of construction deadline to projects beginning construction before January 1, 2025 including solar energy facilities

- Increased energy credit for solar and wind facilities in certain low-income communities

- New credit for clean hydrogen production

- New credit for zero-emission nuclear power

- Extension of incentives for biodiesel, renewal diesel, and alternative fuels

- Extension of biofuel producer credit

- New income and excise tax credits allowed for sustainable aviation fuel

- Modification of IRC Sec. 179D – Energy Efficient Commercial Buildings Deductions

- Modification of building qualifications

- Deduction increased from $1.88 per square foot to up to $5 per qualified square foot

- Changes in depreciation for certain green energy properties

Final thoughts

The Inflation Reduction Act should have wide-ranging impacts on taxpayers, especially large corporations and high-net-worth individuals. In the coming weeks our tax leaders will dive into the specifics of the legislation, outline immediate and long-term impacts, and provide tax-planning strategies and considerations.

]]>Employee Retention Tax Credit

The Employee Retention Tax Credit (ERTC) is a refundable tax credit created by the Coronavirus Aid, Relief and Economic Security (CARES) Act, to encourage businesses to keep employees on their payroll. For 2020, the credit is 70% of up to $10,000 in wages paid by an employer whose business was fully or partially suspended because of COVID-19 or whose gross receipts declined by more than 50%

For 2021, an employer can receive 70 percent of the first $10,000 of qualified wages paid per employee in each qualifying quarter. The credit applies to wages paid from March 13, 2020, through December 31, 2021. And the cost of employer-paid health benefits can be considered part of employees’ qualified wages.

It’s an attractive credit if you qualify.

Eligible businesses

The credit applies to all employers regardless of size, including tax exempt organizations that had a full or partial shutdown because of a government order limiting commerce due to COVID-19 during 2020 or 2021. With the exceptions of state and local governments or small businesses that take Small Business Administration loans, this credit is available to almost everyone.

Of course, there is some fine print:

• To qualify, gross receipts must have declined more than 50 percent during a 2020 or 2021 calendar quarter, when compared to the same quarter in the prior year.

• For employers with 100 or fewer full-time employees, all employee wages qualify for the credit, whether the employer is open for business or shutdown.

• For employers with more than 100 full-time employees, qualified wages are wages paid to employees when they are not providing services due to COVID-19-related circumstances.

One bright point about the ERTC is that employers can be immediately reimbursed for the credit by reducing the amount of payroll taxes they would usually have withheld from employees’ wages. That was a nice touch by the IRS.

Retroactive claims for the ERTC

Although it appears the IRS tried to make this as easy as possible, you may still need a tax professional to sort it out. For instance, if your business had a substantial decline in gross receipts but has now recovered, you can still claim the credit for the difficult period

Retroactive claims for refunds will probably be delayed because currently everything is delayed at the IRS. The credit can be claimed on amended payroll tax returns as long as the statute of limitations remains open, which is three years from the date of filing. So you have some time to claim the credit, but why wait?

Keep December 2021 in mind

The economy is in a state of change, and it is fair to say that we are once again in uncharted territory. On the positive side, there seems to be significant resources and support for businesses from both government and consumers. You and your tax professional should keep your eyes open for credits and benefits to make sure you don’t miss any opportunitie

The ERTC expires in December 2021. Though it may be difficult to think about year-end in the middle of the summer, you’ll want to figure out your position on this credit before December. A tax professional can help you understand the ERTC and help you decide on your next step.

About the author

Michael Silvio is a partner at MGO. He has more than 25 years of experience in public accounting and tax and has served a variety of public and private businesses in the manufacturing, distribution, pharmaceutical, and biotechnology sectors.

]]>To generate the revenue needed to fully fund the American Jobs Plan, the Made in America Tax Plan proposes reversing the corporate tax decrease that was the centerpiece of the Trump Administration’s Tax Cuts and Jobs Act of 2017. President Biden’s tax plan also proposes a number of other changes, mostly concerning international taxation, with the stated goal of incentivizing job creation and investment in the U.S.

In the following, we discuss practical tax considerations and potential planning points that corporations should consider to prepare for the proposed changes and provide the key provisions of the Made in America Tax Plan.

Planning considerations

With the announcement of the Made in America Tax Plan, major tax changes could be in the forecast. However, it is difficult to predict the ultimate changes or how seismic they will be. The fact sheet released by the White House is in many respects light on detail, and a comprehensive explanation of each proposal will not be available until the Treasury Department releases its “Green Book” this spring. Moreover, each proposal will likely face considerable pushback from Congressional Republicans, and the enactment of any proposal will minimally require the unanimous support of Senate Democrats and the support of the overwhelming majority of House Democrats.

Accordingly, the President’s more ambitious proposals could very well face Congressional gridlock, and may require considerable revision to amass the support necessary for enactment. Compounding this conundrum, several cabinet members, including Treasury Secretary Janet Yellen, have repeatedly indicated that proposed changes will be introduced iteratively, in separate legislation. That, combined with the lengthy congressional reconciliation process, makes it difficult to predict when any one proposal might be enacted, let alone become effective.

The difficulty forecasting the tax plan’s ultimate impact and the likelihood of a prolonged legislative process make interim tax planning exceptionally difficult, as tax professionals cannot reliably predict what is coming, or when. The Biden Administration has not provided any concrete details about timing, but in the fastest possible timeline, legislation could be introduced within the next six weeks, and voted into law within the next six months, with some changes potentially becoming effective for the 2022 tax year. However, the timetable could be considerably longer.

That said, there are financial, operational, and other remedial measures that companies can implement in 2021 to mitigate the eventual impact of Biden’s tax plan. First and foremost, companies should work with their tax advisors to model the potential impact of each of the proposals and, to the extent possible, include milder variants of each proposal (e.g., if the corporate income tax rate were raised to 25% rather than 28%). Using the results of these modeling efforts, companies should devise a strategic plan that accounts for the likeliest changes and identifies both interim and post-enactment measures that to mitigate the impact of potential changes.

Taxpayers and their advisors should also communicate with lawmakers about how each proposal would impact their bottom line, profitability, hiring practices, or other aspects of their business that could be negatively affected by these proposals.

Businesses should consider ceasing international expansion to the extent the tax plan’s proposals would undermine or negate the benefits. However, in some instances, it may well be advantageous to accelerate international expansion or the offshoring of certain operations. Modeling results can inform whether such measures would be beneficial or to a company’s detriment.

Despite the uncertainty, some tax planning measures may well be advisable in 2021. For example, the likelihood that the corporate income tax rate will be increasing could make it advisable to accelerate income recognition in 2021 under a preferable tax rate. Other timing measures could also prove beneficial, such as deferring losses and deductions to a later tax year, refraining from accelerating the deduction of prepaid expenses, capitalizing R&D expenses, or electing out of bonus depreciation. Businesses should work with their tax advisors to identify those measures which should be implemented in the interim period, before any tax law changes are implemented.

Key elements of the Made in America Tax Plan

Set the corporate tax rate at 28 percent

“The President’s tax plan will ensure that corporations pay their fair share of taxes by increasing the corporate tax rate to 28 percent. His plan will return corporate tax revenue as a share of the economy to around its 21st century average from before the 2017 tax law and well below where it stood before the 1980s. This will help fund critical investments in infrastructure, clean energy, R&D, and more to maintain the competitiveness of the United States and grow the economy.”

Discourage offshoring by strengthening the global minimum tax for U.S. multinational corporations

“Right now, the tax code rewards U.S. multinational corporations that shift profits and jobs overseas with a tax exemption for the first ten percent return on foreign assets, and the rest is taxed at half the domestic tax rate. Moreover, the 2017 tax law allows companies to use the taxes they pay in high-tax countries to shield profits in tax havens, encouraging offshoring of jobs. The President’s tax reform proposal will increase the minimum tax on U.S. corporations to 21 percent and calculate it on a country-by-country basis so it hits profits in tax havens. It will also eliminate the rule that allows U.S. companies to pay zero taxes on the first 10 percent of return when they locate investments in foreign countries. By creating incentives for investment here in the United States, we can reward companies that help to grow the U.S. economy and create a more level playing field between domestic companies and multinationals.”

End the race to the bottom around the world

“The United States can lead the world to end the race to the bottom on corporate tax rates. A minimum tax on U.S. corporations alone is insufficient. That can still allow foreign corporations to strip profits out of the United States, and U.S. corporations can potentially escape U.S. tax by inverting and switching their headquarters to foreign countries. This practice must end. President Biden is also proposing to encourage other countries to adopt strong minimum taxes on corporations, just like the United States, so that foreign corporations aren’t advantaged and foreign countries can’t try to get a competitive edge by serving as tax havens. This plan also denies deductions to foreign corporations on payments that could allow them to strip profits out of the United States if they are based in a country that does not adopt a strong minimum tax. It further replaces an ineffective provision in the 2017 tax law that tried to stop foreign corporations from stripping profits out of the United States. The United States is now seeking a global agreement on a strong minimum tax through multilateral negotiations. This provision makes our commitment to a global minimum tax clear. The time has come to level the playing field and no longer allow countries to gain a competitive edge by slashing corporate tax rates.”

Prevent U.S. corporations from inverting or claiming tax havens as their residence

“Under current law, U.S. corporations can acquire or merge with a foreign company to avoid U.S. taxes by claiming to be a foreign company, even though their place of management and operations are in the United States. President Biden is proposing to make it harder for U.S. corporations to invert. This will backstop the other reforms which should address the incentive to do so in the first place.”

Deny companies expense deductions for offshoring jobs and credit expenses for onshoring

“President Biden’s reform proposal will also make sure that companies can no longer write off expenses that come from offshoring jobs. This is a matter of fairness. U.S. taxpayers shouldn’t subsidize companies shipping jobs abroad. Instead, President Biden is also proposing to provide a tax credit to support onshoring jobs.”

Eliminate a loophole for intellectual property that encourages offshoring jobs and invest in effective R&D incentives

“The President’s ambitious reform of the tax code also includes reforming the way it promotes research and development. This starts with a complete elimination of the tax incentives in the Trump tax law for ‘Foreign Derived Intangible Income’ (FDII), which gave corporations a tax break for shifting assets abroad and is ineffective at encouraging corporations to invest in R&D. All of the revenue from repealing the FDII deduction will be used to expand more effective R&D investment incentives.”

Enact A minimum tax on large corporations’ book income

“The President’s tax reform will also ensure that large, profitable corporations cannot exploit loopholes in the tax code to get by without paying U.S. corporate taxes. A 15 percent minimum tax on the income corporations use to report their profits to investors—known as ‘book income’—will backstop the tax plan’s other ambitious reforms and apply only to the very largest corporations.”

Eliminate tax preferences for fossil fuels and make sure polluting industries pay for environmental clean up

“The current tax code includes billions of dollars in subsidies, loopholes, and special foreign tax credits for the fossil fuel industry. As part of the President’s commitment to put the country on a path to net-zero emissions by 2050, his tax reform proposal will eliminate all these special preferences. The President is also proposing to restore payments from polluters into the Superfund Trust Fund so that polluting industries help fairly cover the cost of cleanups.”

Ramping up enforcement against corporations

“All of these measures will make it much harder for the largest corporations to avoid or evade taxes by eliminating parts of the tax code that are too easily abused. This will be paired with an investment in enforcement to make sure corporations pay their fair share. Typical workers’ wages are reported to the IRS and their employer withholds, so they pay all the taxes they owe. By contrast, large corporations have at their disposal loopholes they exploit to avoid or evade tax liabilities, and an army of high-paid tax advisors and accountants who help them get away with this. At the same time, an under-funded IRS lacks the capacity to scrutinize these suspect tax maneuvers: A decade ago, essentially all large corporations were audited annually by the IRS; today, audit rates are less than 50 percent. This plan will reverse these trends, and make sure that the Internal Revenue Service has the resources it needs to effectively enforce the tax laws against corporations. This will be paired with a broader enforcement initiative to be announced in the coming weeks that will address tax evasion among corporations and high-income Americans.”

Final thoughts

The stated goals of Biden’s Made in America Tax Plan is to “raise over $2 trillion over the next 15 years and more than pay for the mostly one-time investments in the American Jobs Plan and then reduce deficits on a permanent basis.” Whether these changes will ultimately be implemented or have the desired effect remains to be seen. In the meantime, US-based corporations, especially those with international operations, must prepare for significant changes to their tax reporting and obligations, despite the difficulty they will face in accurately predicting what those change will be.

]]>The tax and economic policies of the 2020 presidential candidates, and their respective parties, are of historical importance. Tax policy is a core driver of consumer behavior and the winning candidate will determine the course for getting the economy back on track following the downturn triggered by the COVID-19 pandemic.

With a Biden victory all but certain, individuals must pay close attention to how his campaign’s proposed policies will affect their total tax liability and be prepared to make any changes or updates, in some cases, during the weeks ending the 2020 tax year.

2020 prospective results overview

Biden Victory | 50/50 Senate Split

In the case of a 50/50 split in the Senate, the tie-breaking vote goes to the Vice President, giving de facto Senate leadership to the party in the White House.

The Biden campaign’s proposed tax plan focuses on rolling back tax breaks and “loopholes” for corporations and high-net-worth individuals, specifically related to changes made in the 2017 Tax Cuts and Jobs Act (TCJA). Biden also proposed a number of significant tax breaks and stimulus efforts targeted at spurring growth in historically-disadvantaged communities and the renewable energy sector, while simultaneously rolling back fossil fuel industry subsidies.

Economic Stimulus

In the case of a Biden/Democratic win, it seems unlikely that an out-going President Trump will be motivated to support a new COVID-19 economic stimulus plan before leaving office. On the other hand, an incoming President Biden will likely immediately push for stimulus upon taking office, and will be successful with control over the Senate.

Biden Victory | Republican Senate Majority

Any outcome that has White House and Senate leadership at loggerheads will likely result in the blocking of any major economic and tax policy changes. With Senate Majority Leader Mitch McConnell’s re-election, there is little reason to suspect he’ll alter his long-standing obstructionist stance against Democrat-sponsored and supported bills.

Tax planning considerations

Proposed Change to Estate Taxes

Maximizing lifetime estate exclusion

There are numerous ways to accomplish this while maintaining some control over the assets (SLATs and 678 trusts):

- Adjust long term planning for gifts that cannot be completed by year end by utilizing traditional estate planning (GRATs, CLATS, and IDGT).

- Decant grantor trusts into non-grantor trusts.

Elimination of Preferential Rate for Capital Gains

Consider strategies to accelerate capital gain income, including:

- Electing out of installment sales.

- Not completing in-process 1031 transactions.

- Selling appreciated property that is not intended to be held long term.

39% Marginal Tax Rate for Income Over $400,000

- Defer Loss Harvesting.

- Exercise NSOs and consider 83b election when appropriate.

- Convert to a Roth IRA and accelerate tax.

Social Security Tax Expansion

Reorganize or elect to be taxed as a C-Corporation:

- C-corp owners with $400,000-$1,000,000 of income could have an effective rate on dividends of 45.1%

- C-corp owners with greater than $1,000,000 of income could have an effective rate on dividends of 51.9%

Executive Compensation

- Incentive Stock Options (ISOs) – No FICA tax on option spread

- Non-Qualified Stock Options (NQSOs) – FICA tax on option spread is delayed until exercise

- Deferred Compensation – There may be timing benefits down the road

Final thoughts

A Democrat-led White House and Congress has the most drastic potential impact on immediate tax planning. However, pressure to create a COVID-19 relief bill will likely be the priority for the in-coming administration, pushing any substantive tax reform to an effective date after 2022. Even so, understanding proposed changes and early planning are recommended to minimize any negative impact stemming from tax reform.

]]>Everything changes, except when it doesn’t

Time and time again we’ve seen reactions to various accounting scandals, after which new policies, procedures, and legislation are created and implemented. An example of this is the Sarbanes-Oxley Act (SOX) of 2002, which was a direct result of the accounting scandals at Enron, WorldCom, Global Crossing, Tyco, and Arthur Andersen.

SOX was established to provide additional auditing and financial regulations for publicly held companies to address the failures in corporate governance. Primarily it sets forth a requirement that the governing board, through the use of an audit committee, fulfill its corporate governance and oversight responsibilities for financial reporting by implementing a system that includes internal controls, risk management, and internal and external audit functions.

Governments experience challenges and oversight responsibility similar to those encountered by corporate America. Governance risks can be mitigated by applying the provisions of SOX to the public sector.

Some states and local governments have adopted similar requirements to SOX but, unfortunately, in many cases only after cataclysmic events have already taken place. In California, we only need to look back at the bankruptcy of Orange County and the securities fraud investigation surrounding the City of San Diego as examples of audit committees that were established in response to a breakdown in governance.

Taking your audit committee on the right mission

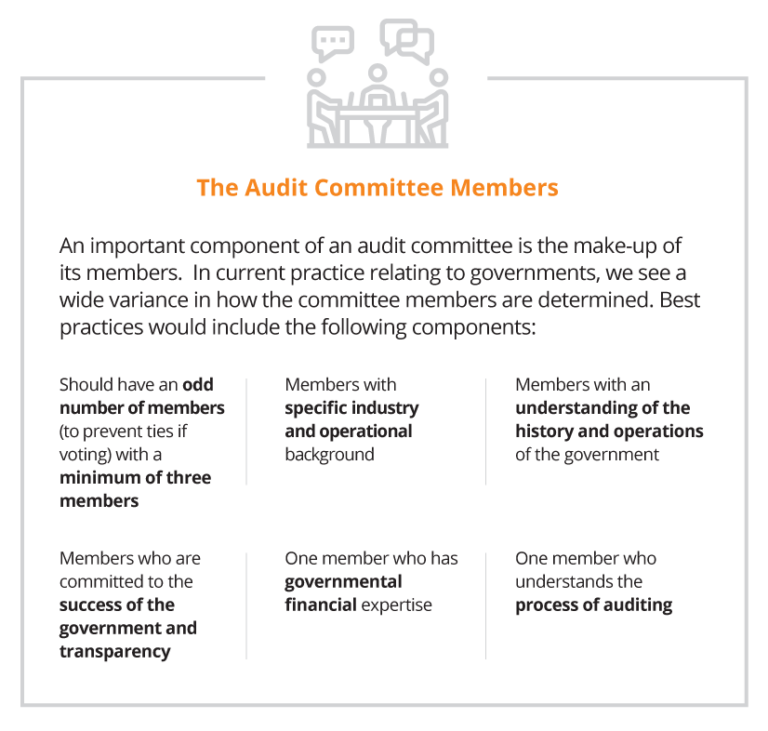

Governments typically establish audit committees for a number of reasons, which include addressing the risk of fraud, improving audit capabilities, strengthening internal controls, and using it as a tool that increases accountability and transparency. As a result, the mission of the audit committee often includes responsibility for:

- Oversight of the external audit.

- Oversight of the internal audit function.

- Oversight for internal controls and risk management.

Chart(er) your course

Most successful audit committees are created by a formal mandate by the governing board and, in some cases, a voter-approved charter. Mandates establish the mission of the committee and define the responsibilities and activities that the audit committee is expected to accomplish. A wide variety of items can be included in the mandate.

Creating the governing board’s resolution is the first step on the road to your audit committee’s success.

Follow the leader(ship)

In practice we see a combination of these attributes, ranging from the full board acting as the audit committee, committees with one or more independent outsiders appointed by the board, and/or members from management and combinations of all of the above. While there are advantages and disadvantages for all of these approaches, each government needs to evaluate how to work within their own governance structure to best arrive at the most workable solution.

Strike the right balance between cost and risk

The overriding responsibility of the audit committee is to perform its oversight responsibilities related to the significant risks associated with the financial reporting and operational results of the government. This is followed closely by the need to work with management, internal auditors and the external auditors in identifying and implementing the appropriate internal controls that will reduce those risks to an acceptable level. While the cost of establishing and enforcing a level of zero risk tolerance is cost prohibitive, the audit committee should be looking for the proper balance of cost and a reduced level of risk.

Engage your audit committee with regular meetings

Depending on the complexity and activity levels of the government, the audit committee should meet at least three times a year. In larger governments, with robust systems and reporting, it’s a good practice to call for monthly meetings with the ability to add special purpose meetings as needed. These meetings should address the following:

External Auditors

- Confirmation of the annual financial statement and compliance audit, including scope and timing.

- Ad hoc reporting on issues where potential fraud or abuse have been identified.

- Receipt and review of the final financial statements and auditor’s reports

- Opinion on the financial statements and compliance audit;

- Internal controls over financial reporting and grants; and

- Violations of laws and regulations.

Internal Auditors

- Review of updated risk assessments over identified areas of risk.

- Review of annual audit plan, including status of the prior year’s efforts.

- Status reports of ongoing and completed audits.

- Reporting of the status of corrective action plans, including conditions noted, management’s response, steps taken to correct the conditions, expected time-line for full implementation of the corrective action and planned timing to verify the corrective action plan has been implemented.

Establish resources that are at the ready

Audit committees should be given the resources and authority to acquire additional expertise as and when required. These resources may include, but are not limited to, technical experts in accounting, auditing, operations, debt offerings, securities lending, cybersecurity, and legal services.

Taking extra steps now will save time later

While no system can guarantee breakdowns will not occur, a properly established audit committee will demonstrate for both elected officials and executive management that on behalf of their constituents they have taken the proper steps to reduce these risks to an acceptable tolerance level. History has shown over and over again that breakdowns in governance lead to fraud, waste and abuse. Don’t be deluded into thinking that it will never happen to your organization. Make sure it doesn’t happen on your watch.

]]>The credit was permanently extended with the passing of the Protecting Americans from Tax Hikes Act of 2015, a welcome reprieve from the credit’s history, where it often expired only to later be temporarily extended, sometimes retroactively. Now that the credit is permanent and has been expanded to benefit certain small businesses and startups, government contractors can incorporate the credit into their tax planning discussions.

Federal tax changes boost R&D

Recently, the value of the credit was enhanced by the Tax Cuts and Jobs Act of 2017 (TCJA), as reflected in BDO’s Tax Outlook Survey.

By reducing the maximum corporate tax rate from 35 to 21 percent, the TCJA effectively increased the credit’s value by 22 percent, from 65 percent when the maximum corporate rate was 35 percent, to 79 percent today.

In addition, by eliminating the corporate Alternative Minimum Tax (AMT), the TCJA affords AMT taxpayers, who generally couldn’t use the credit against their AMT, the opportunity to use their credits down to 25 percent of the amount their net regular tax liability exceeds $25,000. Changes to the AMT regime for individual taxpayers could also increase the amount of benefit allowed to owners of pass-through entities.

Not all contracts limit eligibility

A common misconception in the government contracting industry is that activities don’t qualify for the credit if the government or a third-party finances a contractor’s R&D activities. This isn’t always true: if the contract with the government or other third-party provides that the contractor bears the economic risk if the work fails and that the contractor retains substantial rights in the work’s results, the contractor’s activities can still qualify even if reimbursed by the government or another unrelated third-party.

Don’t overlook software

More good news for government contractors arrived with the Treasury’s final regulations in late 2016. These regulations narrowed the definition of “internal use software” (IUS) activities, which generally must meet a higher standard to qualify. Now, the development of more software, including software to provide services, can qualify more easily, without meeting the higher IUS standards.

MGO’s take

If government contractors pay employees or contractors who are software developers, process engineers, energy consultants, mechanical designers, or other technical personnel, they’re likely to be eligible for the credit. The same is true for government contractors who are trying to develop or improve cybersecurity solutions, aerospace equipment, defense components, cloud computing solutions, and the like.

With the recent taxpayer-friendly developments around the credit and U.S. taxes in general, government contractors should consider how they are impacted and whether they’re missing out on a significant tax-savings opportunity.

This article originally appeared in BDO USA, LLP’s “Government Contracting” newsletter (Summer 2018). Copyright © 2018 BDO USA, LLP. All rights reserved. www.bdo.com

]]>1. The corporate tax rate was permanently reduced from 35 percent to 21 percent.

The top corporate tax rate has been permanently reduced from 35 percent to a flat rate of 21 percent, beginning in 2018. Unlike all other provisions in the new law, including tax breaks for individuals, the new corporate tax rate provision does not expire.

2. There’s a tax break for owners of pass-through entities.

The new law provides owners of pass-through businesses — which include individuals, estates, and trusts — with a deduction of up to 20 percent of their domestic qualified business income, whether it is attributable to income earned through an S corporation, partnership, sole proprietorship, or disregarded entity. Without the new deduction, taxpayers would pay 2018 taxes on their share of qualified earnings at rates up to 37 percent. With the new 20 percent deduction, the tax rate on such income could be as low as 29.6 percent. It should again be noted that certain service industries are excluded from the preferential rate, unless taxable income is below $207,500 (for single filers) and $415,000 (for joint filers), under which the benefit of the deduction is phased out.

3. There might be huge tax benefits to changing your company’s current choice of entity.

Taxpayers should consider evaluating the choice of entity used to operate their businesses. The 21 percent reduced corporate tax rate may increase the popularity of corporations. However, factors such as the new 20 percent deduction for pass-through income, expected use of after-tax cash earnings, and potential exit values will significantly complicate these analyses. The potential after-tax cash benefits ultimately realized by owners could make choice-of-entity determinations one of the most important decisions taxpayers will now make.

4. There have been significant changes to the international tax system.

In connection with these changes, some U.S. shareholders who own stock in certain foreign corporations will have to pay a one-time “transition tax” on their share of accumulated overseas earnings. Other changes include a “participation exemption,” which is a 100 percent dividend-received deduction that permits certain domestic C corporations to receive dividends from their foreign subsidiaries without being taxed on such dividends when certain conditions are satisfied. There is also a new requirement that certain U.S. shareholders of controlled foreign corporations (CFCs) include in income their share of the “global intangible low-taxed income” of such CFCs. Finally, there are new measures to deter base erosion and promote U.S. production.

5. The corporate AMT and DPAD are dead, but Research Tax Credits live on.

The law repeals the Section 199 Domestic Production Activities Deduction (DPAD) and the corporate Alternative Minimum Tax (AMT) for tax years beginning after 2017. The Research Tax Credit was retained and is now more valuable given the reduction of the corporate tax rate from 35 percent to 21 percent.

6. They’ve scrapped NOL carrybacks and limited the use of carryforwards.

Previously, businesses were able to offset current taxable income by claiming net operating losses (NOLs), generally eligible for a two-year carryback and 20-year carryforward. Now NOLs for tax years ending after 2017 cannot be carried back, but can be indefinitely carried forward. In addition, NOLs for tax years beginning in 2018 will be subject to an 80 percent limitation. Companies will have to track their NOLs in different buckets and consider cost-recovery strategy on depreciable assets in applying the 80 percent limitation.

7. Tax reform’s impact on accounting methods may change when revenue is recognized, but new provisions could also lead to temporary and permanent tax benefits.

Under the new law, accrual basis taxpayers must now recognize income no later than the taxable year in which such income is taken into account as revenue in an applicable financial statement.

However, new provisions also provide favorable methods of accounting that were not previously available. That, coupled with the reduction in tax rates, creates a favorable and unique environment for filing accounting method changes.

There are many method changes still available for the 2017 tax year. Taxpayers should evaluate current accounting methods to identify any actionable opportunities to accelerate deductions and defer income for the 2017 tax year, which could result in significant tax savings.

8. There are new rules for bonus depreciation and full expensing on new and used property.

The new tax law allows a 100 percent first-year deduction — up from 50 percent — for the adjusted basis of qualifying assets placed in service after Sept. 27, 2017, and before Jan. 1, 2023, with a gradual phase down in subsequent years before sunsetting after 2026. The definition of qualifying property was also expanded to include used property purchased in an arm’s-length transaction. Businesses should pay close attention to any qualifying asset acquisitions made during the fourth quarter of 2017, as the full expensing can be taken on the 2017 return if the property was acquired and placed in service after Sept. 27, 2017.

Additionally, under new tax law, taxpayers may now deduct up to $1 million under Section 179 for properties placed in service beginning in 2018 — double the previous allowable amount. The phase-out threshold is increased to $2.5 million and will be indexed for inflation in future years and the types of qualifying property has been expanded.

9. The availability of the cash method of accounting expanded for small businesses.

Beginning in 2018, the average annual gross receipts threshold for businesses to use the cash method increases from $5 million to $25 million. Additionally, small businesses who meet the $25 million gross receipts threshold are not required to account for inventories and are exempt from the uniform capitalization rules. The $25 million is indexed for inflation for tax years beginning after 2018.

10. Now is the time to assess total rewards strategies.

Tax reform significantly impacts various components of an employer’s total compensation program — namely the expansion of the $1 million deduction cap on pay to covered employees; disallowed deductions for transportation fringe benefits provided to employees; income inclusion for employer-paid moving expenses; further deduction limitations on certain meal and entertainment expenses; and a two-year tax credit for employer-paid family and medical leave programs. As the IRS releases guidance, employers must immediately modify their payroll systems to reflect tax reform changes impacting individual taxpayers.

For more information about the impact of tax reform on the Government Contracting industry, please reach out to us.

]]>This Tax Alert provides an overview of some of the most significant modifications to the U.S. international tax provisions affecting businesses and individuals. We urge clients to evaluate the impact of tax reform and discuss relevant changes with their tax advisors since many of the new provisions may bring about unintended tax consequences with respect to properly implemented structures under the previous U.S. international tax regime. Overall, the changes expand the base of cross-border income to which current U.S. taxation applies.

Additional tax alerts for Individuals | Business

Details of international provisions

Introduction of Participation Exemption System for foreign income

The Act introduces a dividend exemption system that applies to distributions made after December 31, 2017, which generally provides for a 100% dividend received deduction (“DRD”) for the foreign-sourced portion of dividends received by a domestic C corporation from a specified 10%-owned foreign corporation (other than a Passive Foreign Investment Company – “PFIC”) of which it is a U.S. shareholder, provided certain conditions are satisfied. The DRD is available only to C corporations that are not regulated investment companies (“RICs”) or real estate investment trusts (“REITs”).

Note that dividends received from PFICs do not qualify for the DRD and domestic C corporations may not claim foreign tax credits or a deduction for foreign taxes paid or accrued with respect to any dividend allowed the DRD.

To the extent earnings of foreign corporations are neither subpart F income nor subject to the minimum tax rule discussed below, the new participation exemption system moves the U.S. away from a worldwide taxation system towards a territorial tax system for earnings of foreign corporations.

Sales or transfers involving specified 10%-owned foreign corporations

Certain deemed dividends under Code section 1248 – resulting from the sale or exchange of stock of a specified 10%-owned foreign corporation held for over one year – qualify for the 100% DRD under the new law.

The provision also allows a U.S. shareholder to claim a 100% DRD on deemed dividends under section 964(e) resulting from the gain on the sale of foreign stock by a controlled foreign corporation (“CFC”).

Two new loss limitation rules are included in the provision, which are applicable to transfers and distributions made after December 31, 2017:

- A domestic corporation that is allowed a DRD is required to reduce its basis in the stock of the foreign corporation by an amount equal to the DRD, solely for purposes of determining the domestic corporation’s loss on the sale of stock of the foreign corporation.

- A domestic corporation is required to recapture certain foreign branch losses if it transfers substantially all of the assets of a foreign branch to a 10%-owned foreign corporation of which it is a United States shareholder after the transfer. The active trade or business exception of section 367(a)(3) is repealed for transfers made after December 31, 2017, which disfavors the use of foreign branches.

New mandatory repatriation

As a transition to the new participation exemption regime, a mandatory repatriation provision is included targeting previously untaxed earnings and increasing subpart F income by the shareholder’s pro rata share of each specified foreign corporation’s net untaxed post-’86 historical E&P, determined as of November 2 or December 31, 2017 (a measuring date). However, this mandatory inclusion is reduced (but not below zero) by an allocable portion of the taxpayer’s share of foreign E&P deficit of each specified foreign corporation and the taxpayer’s share of its affiliated group’s aggregate unused E&P deficit. Earnings attributable to the shareholder’s aggregate foreign cash position or liquid assets are subject to tax at a 15.5% rate, while earnings attributable to illiquid assets are subject to tax at an 8% rate.

The tax liability is payable over a period of up to eight years, at the election of the U.S. shareholder.

A special rule applies to S corporations under the mandatory repatriation provisions. S corporation shareholders may elect to continue to defer taxation of such foreign income until the S corporation changes its status, sells a substantial amount of its assets, ceases to conduct business, or the electing shareholder transfers their S corporation stock.

Non-corporate U.S. shareholders are exposed to the new mandatory repatriation rule if the specified foreign corporation is a CFC or any foreign corporation with at least one domestic corporate U.S. shareholder, even though the 100% dividend received deduction from foreign subsidiaries only applies to corporate U.S. shareholders under the Act.

Foreign tax credits and sourcing of income modifications

Foreign tax credits are allowed under the new law only with respect to foreign income taxes associated with the taxable portion of the U.S. shareholder’s net mandatory inclusion. Foreign tax credits are disallowed with respect to foreign income taxes attributable to the participation deduction. Taxpayers may not elect to take a deduction for foreign taxes that are disallowed as foreign tax credits.

The U.S. shareholder’s section 78 gross-up should also reflect the portion of foreign taxes attributable to the U.S. shareholder’s net mandatory inclusion.

The deemed paid foreign tax credit provisions under Code Section 902 are repealed while the deemed paid foreign tax credit provisions for subpart F inclusions under Code Section 960 are retained but modified, providing a credit on a current year basis. Foreign tax credits will be counted on an annual basis and will no longer be pooled.

Foreign taxes attributable to distributions of previously taxed income (“PTI”) are also regulated under the Act

The Act also revises the sourcing rules for income from inventory sales. Income from inventory sales is now sourced entirely based on the place of production and not allocated 50/50 to the place of production and the place of sale (based on title passage).

A separate foreign tax credit limitation basket is created under the new law for foreign branch income.

The Act repeals the fair market value method of interest expense apportionment. Taxpayers are now required to allocate and apportion interest expense of members of an affiliated group using the adjusted basis of assets.

New provisions regarding foreign passive and intangible income

The Act has new provisions that adopt a minimum tax on “global intangible low-taxed income” (“GILTI”) and a new special deduction for certain “foreign-derived intangible income” (“FDII”), subject to certain exceptions.

Regardless of whether distributions are actually made by a CFC during the tax year and similarly to the manner in which subpart F income inclusions operate, a U.S. shareholder of a CFC is now required to include in income its pro rata share of GILTI allocated to the CFC for the CFC’s tax year that ends with or within its own tax year.

GILTI provisions target a portion of the CFCs’ active (non-Subpart F) income and tax it at an effective tax rate of 10.5% prior to 2026 — generally speaking, the targeted portion is equal to the net income over a routine or ordinary return, defined as the excess of an implied 10% rate of return on the adjusted basis of the CFC’s tangible depreciable property used in generating the active income.

In conjunction with the new minimum GILTI tax regime, excess returns earned directly by a U.S. corporation from foreign sales (including licenses and leases) or services defined as FDII are now also subject to a 13.125% effective tax rate (increased to 16.406% starting in 2026). FDII is the amount of a U.S. corporation’s “deemed intangible income” that is attributable to sales of property (including licenses and leases) to foreign persons for use outside the U.S. or the performance of services for foreign persons or with respect to property outside the U.S.

Corporate shareholders are allowed a deduction equal to maximum 50% of GILTI (reduced to 37.5% starting in 2026) plus any corresponding Code section 78 gross-up plus maximum 37.5% of taxpayer’s FDII (reduced to 21.875% starting in 2026) – combined, these three components comprise the GILTI deduction. Not that the total GILTI deduction cannot exceed a corporation’s taxable income. S corporations or domestic corporations that are RICs or REITs are not allowed to claim this deduction. Transfers to foreign related persons generally do not qualify for FDII benefits.

U.S. shareholders can make a Code Section 962 election with respect to GILTI inclusions, which subjects the shareholder to tax on the GILTI inclusion based on corporate rates, and allows the electing shareholder to claim foreign tax credits on the inclusion as if the shareholder were a domestic corporation.

Modification to subpart F rules

The inclusion based on the withdrawal of previously excluded subpart F income from qualified investment is repealed.

The provision that provides for the inclusion of foreign base company oil-related income is repealed; hence, previously excluded foreign shipping income of a foreign subsidiary is no longer subject to current U.S. taxation under the subpart F rules if there is a net decrease in qualified shipping investments.

Stock attribution rules for determining status of a foreign corporation as a CFC are modified, which makes it more likely for a foreign corporation to be treated as a CFC as a result of the stock of certain related foreign persons being attributed downward to a U.S. citizen. As a result, for example, stock owned by a foreign corporation would be treated as constructively owned by its wholly-owned domestic subsidiary for purposes of determining the U.S. shareholder status of the subsidiary and the CFC status of the foreign corporation.

The new law eliminates the requirement that a corporation be a CFC for 30 days before subpart F inclusions apply.

Prevention of base erosion

The Act includes additional anti-base erosion measures, including a Base Erosion Anti- Abuse Tax (“BEAT”) for certain payments paid or accrued in tax years beginning after December 31, 2017. In general, the BEAT imposes a minimum tax on certain deductible payments made to foreign affiliates, including royalties and management fees, but excluding cost of goods sold.

Income shifting through intangible property transfers is further limited. This includes treating goodwill and going concern value and workforce in place as section 936(h)(3)(B) intangibles and, requiring the use of the aggregate basis valuation method in the case of transfers of multiple intangible properties in one or more related transactions. This applies if it is determined that an aggregate basis achieves a more reliable result than an asset-by-asset approach.

Deductions for certain related party interest or royalty payments paid or accrued in certain hybrid transactions or with certain hybrid entities are now disallowed under certain circumstances. The Act provides that the Secretary of State shall issue regulations or other guidance as may be necessary or appropriate to carry out the purposes of the provision for branches (domestic or foreign) and domestic entities, even if such branches or entities do not meet the statutory definition of a hybrid entity.

New rules were incorporated to limit the deductibility of interest within a corporate group.

Surrogate foreign corporations are not eligible for the reduced rate on dividends under the Act.

MGO insights

The Tax Cuts and Jobs Act is the largest overhaul of the tax system in over three decades and will have a significant impact on U.S.-based multinational companies as well as inbound businesses. The bill fundamentally changes the landscape of U.S. international taxation. We recommend that companies, individuals, and flow through entities engaged in cross border business discuss their specific situation with MGO’s experienced international tax professionals and consultants – we are here to help you navigate the changes of this comprehensive tax reform.

]]>