What is the policy now? Well, the Tax Cuts and Jobs Act (TCJA) of 2017 changed the treatment of R&E costs so that taxpayers must capitalize all R&E costs incurred after December 31, 2021, and amortize them over either a five-year period (domestic costs) or a 15-year period (foreign costs). Previously, taxpayers could either (1) immediately deduct R&E expenditures, or (2) elect to amortize those costs over a period of five or more years, which gave the taxpayer the ability to choose the option that would be the most beneficial for them.

While it is still possible for the legislative process to postpone or repeal mandatory capitalization of Section 174 costs (including retroactively applying any changes to the 2022 tax year), such legislation would need to have bipartisan support due to the currently divided Congress.

In this article, we review what it would mean for your business if the much-anticipated revisions to Section 174 do not occur, and what kind of planning you should do to prepare on the front end. A number of these recommendations will be further refined once additional IRS guidance is provided.

Background on 174 R&E expenditures

R&E expenses for income tax purposes are defined under Section 174 and its regulations. In Treasury Regulation Section 1.174-2(a), R&E expenditures are described as expenditures incurred by the taxpayer in connection with the taxpayer’s trade or business in the experimental or laboratory sense. Section 174(c)(3) – added by the TCJA – also notes that any amount paid or incurred in connection with the development of any software shall also be an R&E expenditure subject to capitalization. Generally, when determining R&E expenses, not only are direct costs of R&E factored in, but also the indirect costs incident to the development or improvement of a product.

Common expenses included in R&E costs under Section 174 are the following. Many of these expenses are considered for Section 174 specifically and are not qualified research expenses for purposes of the R&D credit.

- Attorneys’ fees in connection with filing and completing patent applications.

- Allowance for depreciation or depletion of property to the extent used in connection with R&E.

- Employee wages and employee benefits and costs in connection with R&E.

- Supplies, computer leasing, and contract research costs in connection with R&E.

- Pilot model expenditures.

- Facility expenditures in connection with R&E.

- Ordinary and extraordinary utilities in connection with R&E.

- Travel expenditures incident to R&E.

- Foreign research expenditures.

- Additional overhead expenditures incident to R&E.

*In addition to the above, there are other criteria used for determining what expenses qualify for the R&D credit that do not apply towards determining Section 174 costs.

In contrast, the following are common expenses that are excluded from the expansive definition of R&E costs under Section 174:

- the ordinary testing or inspection of materials or products for quality control;

- efficiency surveys;

- management studies;

- consumer surveys;

- advertising or promotions;

- acquisition of another’s patent, model, production or process;

- research in connection with literary, historical, or similar projects; and

- expenditures for the acquisition or improvement of land.

The current R&E amortization rule explained

The ability to deduct R&E costs changed for all tax years beginning after December 31, 2021. As previously mentioned, these costs can no longer be deducted in full and must be capitalized and then amortized over five years for domestic costs and over 15 years for foreign costs. This amortization starts at the midpoint of the first year that the expenses were incurred, which results in only 10% of domestic costs (1/2 of 20%) being able to be deducted in their first year.

Per IRS guidance, this mandatory change can be implemented as an automatic accounting method change through attaching a statement to a taxpayer’s first income tax return with a year beginning after 2021, in lieu of filing the much more intricate Form 3115. This change should not have an effect on prior tax years, since the automatic method change is implemented on a “cut-off basis.”

Macro effect of mandatory capitalization

As mentioned above, before the prior rule was changed, every R&E expense could be deducted in full in the year they were incurred. While it is expected that the Section 174 expensing rules will revert to this — to some extent — through pressure from persistent lobbyists, this change has not been incorporated into a bill yet.

Some believe the mandatory R&E capitalization and amortization will adversely affect U.S. innovation, potentially resulting in a detrimental impact on our global competitiveness and jobs. For more than 60 years, businesses were able to immediately deduct their R&D expenses in the year those expenses were incurred (or choose to defer based on what worked for them). Now, the amortization of new R&E costs could cost businesses billions in cash taxes.

Significant considerations

Estimated Tax Payments: For taxpayers making estimated tax payments utilizing current year taxable income, consideration should be given to R&E expenditures and how the capitalization of those expenditures may impact taxable income and timing of cash tax payments. A closer look at refining the various accounts in a taxpayer’s books may be needed for this.

Tax Accounting / ASC 740: Taxpayers should be mindful of whether a new deferred tax asset is created, if any adjustment of existing deferred taxes may be necessary, or if a full or partial valuation allowance may be needed.

Other Areas Affected: The amortization requirement also affects other areas of taxable income, including the following:

- increases the deductibility of business interest under Section 163(j),

- increases the deductibility of the QBI (Qualified Business Income) deduction,

- increases the amount of GILTI (global intangible low-taxed income) for controlled foreign corporations,

- potentially adjusts the amount of FDII (foreign derived intangible income) deduction that can be taken,

- changes the amount of R&E expenses allocable for purposes of the foreign tax credit, and

- impacts state taxable income for the few states that do not conform to the capitalization requirement (e.g., California).

R&D credit considerations

The Section 174 capitalization requirements should not directly impact the amount of expenses that can be used for the R&D Tax Credit under Section 41, since the research credit is calculated using a much smaller subset of R&E expenditures than Section 174 and is not limited by the capitalization requirement. As Section 174 is much broader in scope, it applies to expenditures both eligible and ineligible for the research credit.

Another consideration for tax planning is that the research credit will be even more important to assist with reducing the additional tax liability that will be generated by the R&E treatment change, since the credit can help offset some of the tax liability increase. Moreover, the analysis & processes used to determine the R&D credit can be leveraged to identify Section 174 R&E expenses, which helps create some efficiencies in quantifying the overall effect of the mandatory capitalization and amortization requirement.

Extend impacted returns where possible

Tax return extensions are highly recommended for tax returns that have their due dates coming up. Not only is there the pending IRS guidance that may significantly change R&E expense calculations, but also the act of extending tax returns should allow more time for tax returns to be superseded (rather than amended) and should allow for R&D credit claims to be made on originally filed returns.

This is echoed by a September 2021 Chief Counsel Memorandum issued by the IRS, which made the process for claiming a refund under the R&D credit far more stringent. The memorandum relayed that taxpayers must provide more information on business components, identify the research activities performed, and name the individuals who performed each research activity. Given the additional amount of detail needed, taxpayers making R&D credit claims on amended returns — especially small businesses — have a heavier burden than those who make the claim on an originally filed returns.

How will it affect you?

If the mandatory R&E capitalization requirement is not changed, you should consider how the 174 capitalization rules will affect your business and how claiming the R&D credit will help offset the increase in tax liability. If you currently have an R&D credit analysis and/or an ASC 730 financial statement analysis, those studies can be used as starting points to determine the overall effect of Section 174 — keeping in mind that neither analysis includes all the costs included in Section 174.

If the requirement is changed, there are several ways that the R&E expense landscape could turn out for taxpayers. Ideally, Congress will revert to the prior rule regarding R&D expenses. In that situation, you should be able to choose what is best for you — immediately deducting or deferring.

Our perspective

As experienced advisors, MGO can help model the best R&E position for you, through the 2022 tax year and beyond — potentially saving you significant amounts of money. Our holistic tax advisor and business advisor-first philosophy factors not only the direct effects of the R&E capitalization requirement, but also the impact on other areas of your tax returns (e.g., international, transfer pricing, state, and local tax) and what potential savings you can obtain by claiming the R&D credit. Please feel free to reach out to any of our R&E costing profesionals below to get the experienced insight that you deserve.

About the author

Danielle Bradley is a senior manager in MGO’s National Tax Credits and Incentives practice. She focuses on helping businesses identify, substantiate, and defend federal and state tax credits and incentives. She has helped hundreds of companies monetize and defend over $100 million in various tax credits and incentives, such as the Research and Development (R&D) Tax Credit, Orphan Drug Credit, Employee Retention Credit, meals and entertainment deduction, and the current Research and Experimental (R&E) amortization calculations. Danielle has extensive experience in various industries, including software and technology, life sciences, manufacturing, aerospace and defense, and food, beverage and agriculture businesses.

Contact Danielle to further discuss the R&E amortization or other credits and incentives at Danielle Bradley (Tax Credits and Incentives Director), Matthew Sapowith (Tax Partner), or Michael Silvio (Tax Partner).

]]>Executive Summary:

- Implementing basic accounting practices and understanding tax implications can help individuals working independently in creative fields gain clarity, meet obligations, and maximize income.

- Separating business and personal finances, tracking income and expenses, and budgeting for estimated taxes can help creators be proactive in their financial planning.

- Creators earning income across state lines or internationally need to be aware of varying taxation requirements in different jurisdictions.

~

Today’s artists need to view themselves as both businesses and creatives. Whether you are a painter, digital artist, photographer, website designer, YouTuber, Instagrammer, or any type of artist, creator, or influencer, understanding and managing your financial obligations is a crucial aspect of sustaining a thriving career.

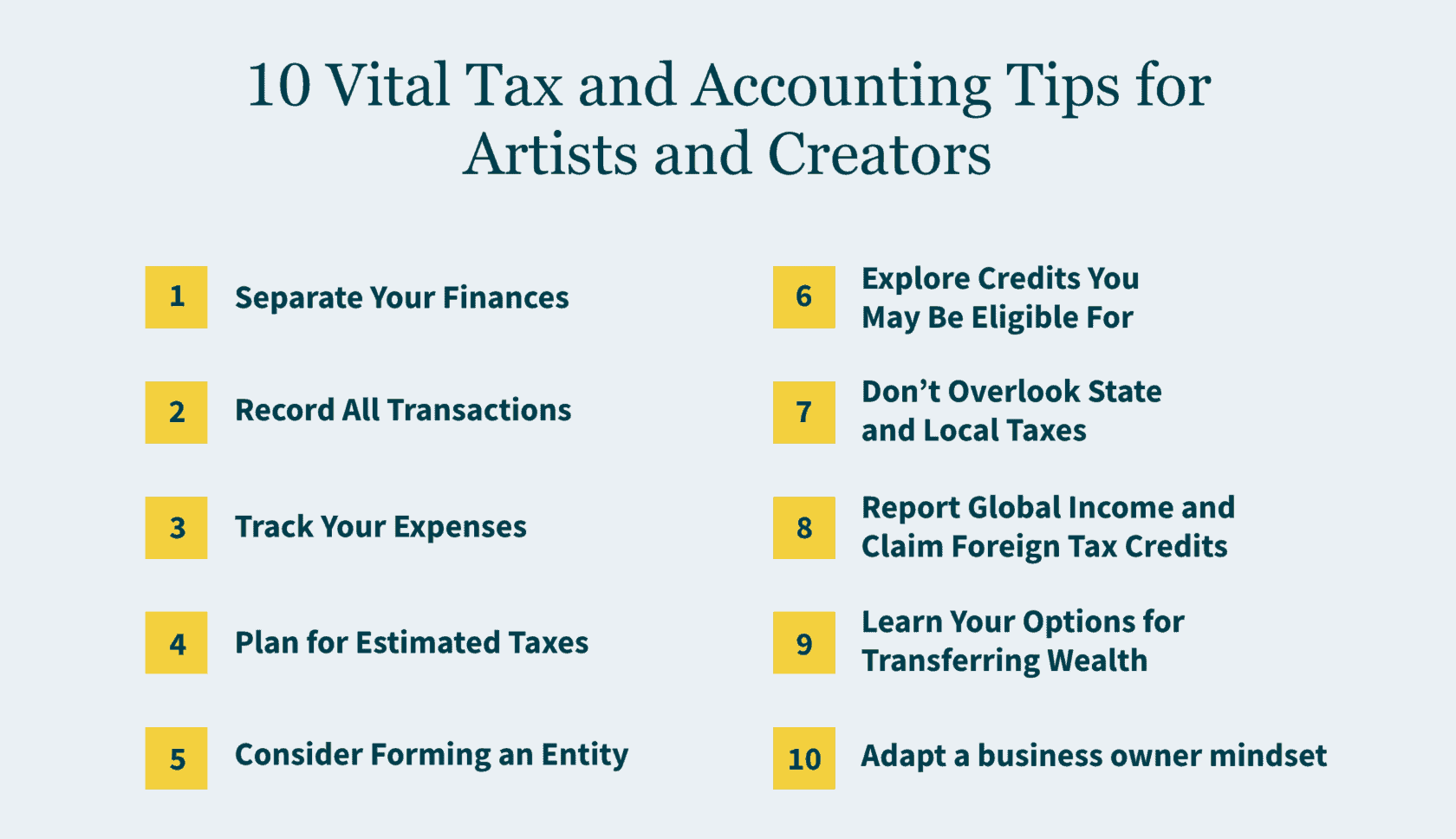

Here are 10 tips to help you meet your tax reporting responsibilities and get the most from your hard-earned income:

1. Separate Your Finances

To make your accounting more efficient and streamline the tax-filing process, it is a smart idea to separate your business and personal finances. Designate a dedicated business account to track income and expenses related to your artistic endeavors. This separation not only simplifies tax reporting but also enhances financial clarity, making it easier to assess the overall health of your creative enterprise.

Tip: Establish a separate account for business transactions, or multiple business accounts to allocate money for categories such as expenses, taxes, and savings.

2. Record All Transactions

Sometimes it can be challenging to determine what constitutes income. That’s why it’s important to track everything. Gifts received by sponsors are often taxable, especially if they are products in exchange for services (e.g., promotion of product). “Donations” from various fundraising activities like Kickstarter are also considered revenue. On the other hand, crypto and non-fungible tokens (NFTs) are considered property. Selling them usually generates a capital gain or loss.

Tip: Log all payments and gifts received, even if you are unsure, so your tax preparer can report appropriately.

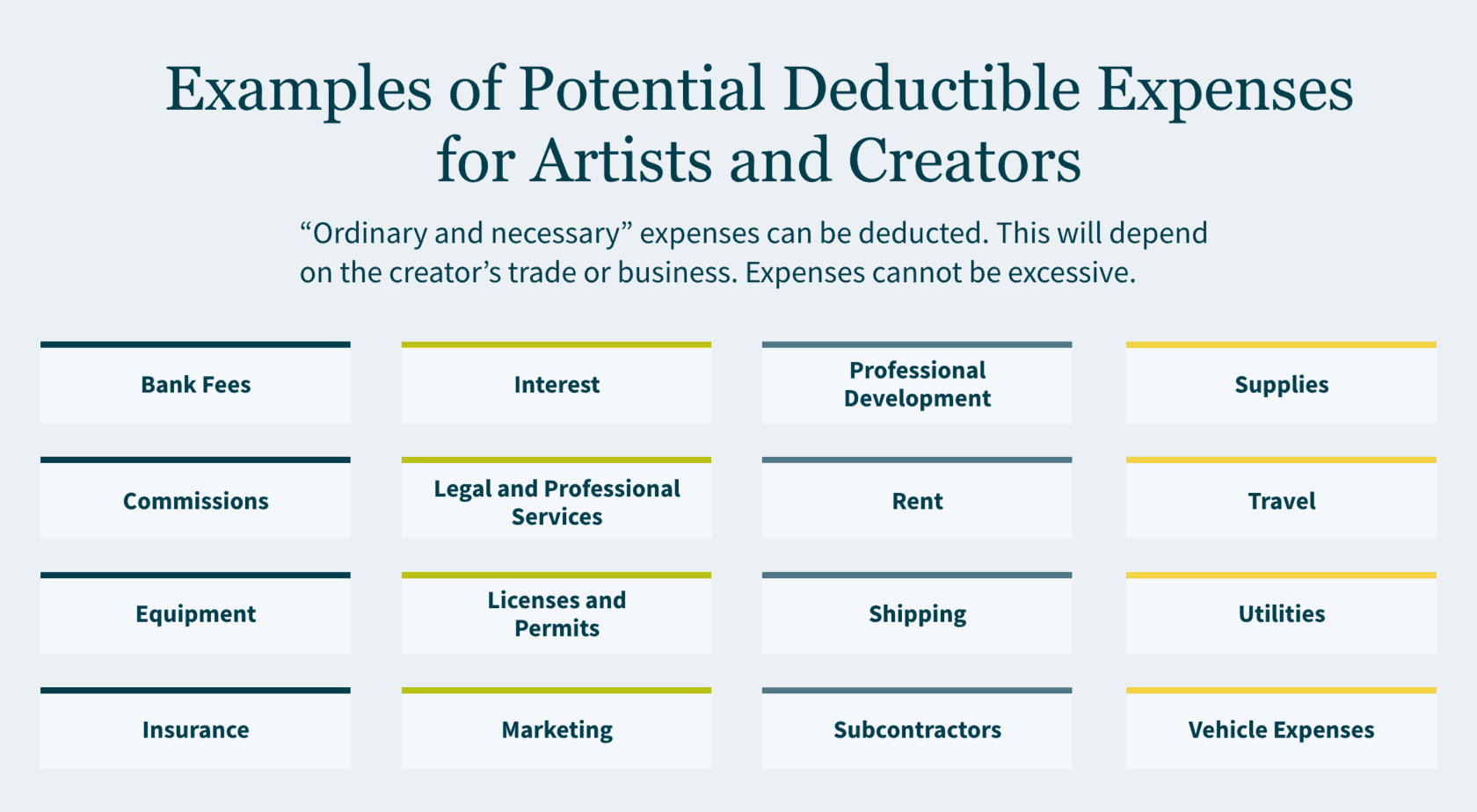

3. Track Your Expenses

Creators and artists can benefit from various tax deductions tailored to their industry. Deductible expenses may include art supplies, equipment, software subscriptions, professional development, and even a portion of your home used as a dedicated workspace. While expenses should not be excessive, any “ordinary and necessary” expenses of your craft can be deducted.

Tip: Save receipts and track expenses in real-time using a spreadsheet, app, or software for easy recording and reporting.

4. Consider Forming an Entity

Creators who run their own business are often independent contractors. Consider setting up an entity for the business — which can help protect your personal assets from your business assets and offer tax savings. S Corporations and LLCs are common for smaller businesses. For larger businesses where investors are coming in, C Corporation may make sense.

Tip: Do some research or talk to a tax professional to find out if setting up an entity makes business and financial sense for you.

5. Explore Credits You May Be Eligible For

Artists also may be eligible for various tax credits that can help offset their tax liability. Research and Development (R&D) credits can be applicable to certain creative processes, rewarding innovation in your artistic pursuits. For instance, software development is considered to be R&D for income tax purposes.

Tip: Consult a tax professional about ways to maximize credits and minimize your tax liability.

6. Don’t Overlook State and Local Taxes (SALT)

Beyond federal taxes, SALT significantly impact overall tax liability. When selling art online (whether physical or digital), be mindful of sales tax requirements, which are determined by local laws. Whether revenue is from “tangible” versus “intangible” products (physical objects versus services, ideas, software, etc.) can dictate where taxation occurs — affecting if your income is subject to sales tax or not.

Tip: Stay informed about varying tax rates, and be cautious of sales and use tax implications tied to transmitting creative art across state lines.

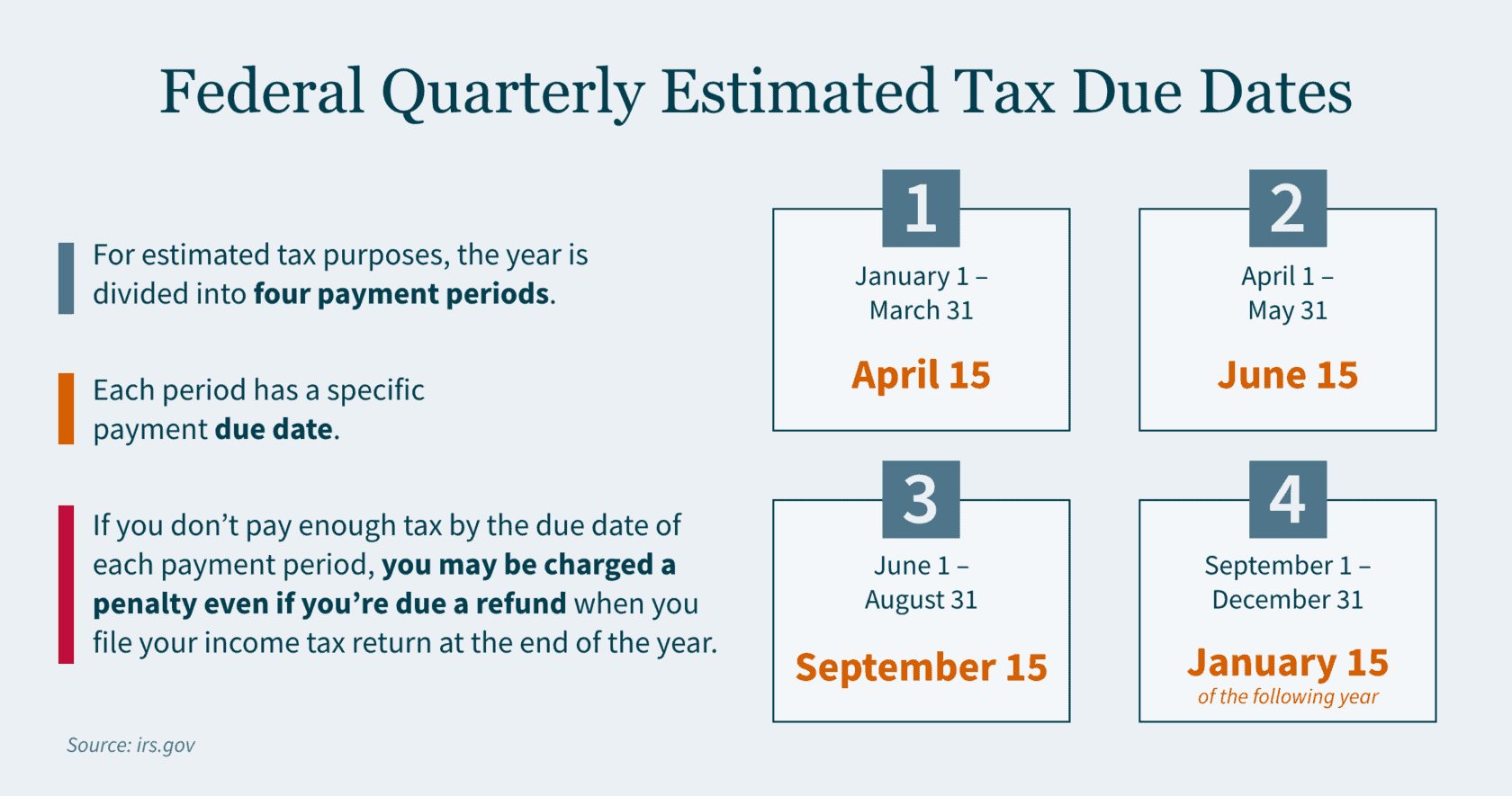

7. Plan for Estimated Taxes

As an independent contractor with variable income streams, you should plan for estimated taxes to avoid financial surprises. These quarterly payments encompass income taxes on your profits plus the self-employment tax (covering Social Security and Medicare). For those earning up to $160,200 in net income, the self-employment tax rate currently stands at 15.3%. The silver lining is that you can deduct half of this self-employment tax when filing your income taxes.

Tip: Set aside a portion of your income for estimated tax payments, ensuring proactive financial planning throughout the year.

8. Report Global Income and Claim Foreign Tax Credits

United States (U.S.) citizens or residents earning abroad must report all worldwide income to the Internal Revenue Service (IRS). If you’re earning income in or from foreign countries, it’s crucial to understand foreign tax credits, filing requirements, and deductibility in various jurisdictions. Every tax jurisdiction may have a different method to tax your creation; and different tax implications may arise based on where brands and intellectual property are created and protected.

Tip: Work with a tax professional to evaluate the potential benefits of foreign tax credits for non-U.S. income.

9. Learn Your Options for Transferring Wealth

Digital assets such as domain names, electronically stored photos, and videos to email and social media accounts all have value. When transferring these as gifts or bequests, there may be tax implications that can be circumvented if the transfer is appropriately structured or organized.

Tip: Consider trusts and estate planning for more tax-efficient wealth transfer.

10. Adapt a Business Owner Mindset

As an artist, embracing a business owner’s perspective is essential for long-term success. Understanding basic financial statements like balance sheets and profit and loss (P&L) statements allows you to gauge profitability, identify your most valuable revenue sources, and streamline your efforts. Elevating your financial literacy empowers you to make more informed decisions — which can lead to greater freedom and flexibility in your artistic career.

Quick Tip: Learn to read a balance sheet and create a basic P&L statement for a clearer financial picture.

Integrate Financial Management into Your Creative Journey

Effective financial planning is like a great work of art — every brushstroke matters. By taking these steps today you can better position yourself to continue pursuing your creative passion tomorrow.

Need a hand with taxes and accounting for your creative venture? Our Entertainment, Sports, and Media practice works with a diverse range of artists — from musicians to photographers to online creators — and our International Tax and State and Local Tax teams can provide guidance to help you address areas like sales tax or foreign tax credits. Reach out to MGO today.

- State tax authorities are escalating audits of intercompany transactions, as transfer pricing crackdowns in several states are generating millions in tax revenue.

- These state initiatives indicate growing regulatory emphasis on transfer pricing, which may encourage more aggressive audits (especially if budgets tighten).

- Companies operating across state borders should take proactive steps, like conducting transfer pricing studies to validate policies and strengthen defenses before audits strike.

~

A recent Bloomberg article affirms state tax authorities are ramping up audits of intercompany transactions at multistate corporations. The report points to an increase in audits in three “separate-reporting” states following transfer pricing settlement initiatives as a beacon of audit activity to come across other states that take this approach.

While not ideal for multistate operators, this development may not come as a surprise to companies with international operations who have dealt with a myriad of cross-border tax issues in recent years. Close observers of state and local tax (SALT) developments have been predicting for many years the potential that states will be adopting similar positions with respect to transfer pricing. In a 2022 article focused on SALT transfer pricing enforcement, we highlighted several key indicators that more state transfer pricing audits could be on the horizon – including state budget deficits, a surge in auditor and consultant hirings, and renewed interest among states in collaborating on multistate audits.

With confirmation that state-driven transfer pricing audits are on the rise, it is imperative for corporations operating across state borders to assess your transfer pricing risks and fortify your documentation and audit defense strategies.

Surge of Transfer Pricing Audits in Separate-Reporting States

According to the Bloomberg Tax report, the recent spike in transfer pricing audit activity has predominantly affected Southeastern states categorized as separate-reporting states. Currently, there are 17 separate-reporting states in the United States. With the exception of a handful of states like Indiana, Pennsylvania, Iowa, and Delaware, most separate-reporting states are located in the Southeast region.

How separate-reporting states differ from other states in their taxation approach to corporations:

- In separate-reporting states, each corporation within an affiliated group is required to file its individual tax return. This treatment considers them as separate entities with independent income, recognizing intercompany transactions, and allowing for varying tax liabilities.

- In contrast, combined-reporting states require or allow affiliated corporations within a corporate group to file a single tax return, treating them as a unitary business with shared income, often eliminating intercompany transactions.

Notably, two Southeastern states, Louisiana and North Carolina, have recently concluded audit resolution programs that significantly boosted their state revenues. Louisiana’s program generated nearly $38 million, while North Carolina’s efforts resulted in more than $124 million. Meanwhile, New Jersey, a Mid-Atlantic state that abandoned separate reporting in favor of combined reporting in 2019, is in the midst of a transfer pricing resolution program that has already collected almost $30 million. The success of these programs in collecting tax revenue is likely to motivate other states to explore similar initiatives.

The success and subsequent expansion of these programs signify a growing emphasis on transfer pricing at the state tax authority level. State tax agencies are enhancing their knowledge and enforcement activities in this domain, giving auditors more confidence to adjust returns in transfer pricing disputes. This increasing competency may be viewed as a valuable tool by states – both those requiring separate and combined reporting – that are seeking ways to augment revenue streams.

Strengthen Your Transfer Pricing Defenses Before State Audits Strike

To preemptively safeguard your business from a state transfer pricing audit, a proactive approach to validating pricing policies is essential – and a comprehensive transfer pricing study is your primary defense.

Here are three key advantages of conducting a transfer pricing study:

- Document Your Transfer Pricing Policy: A transfer pricing study provides robust documentation that can counter inflated tax assessments by identifying key intercompany transactions, referencing benchmark data, and highlighting any deviations that necessitate policy adjustments. Even if your company has undertaken prior studies, annual updates are indispensable to align with evolving business landscapes and provide tax penalty protection.

- Mitigate Your Risk: Beyond reducing audit risks and potential liabilities, these studies also play a pivotal role in supporting major corporate events like mergers and acquisitions (M&A). By demonstrating pricing compliance, they ensure that domestic affiliates have robust documentation and effective cost allocation analysis, thus preventing over-taxation or under-taxation.

- Ensure Consistency: Minimize uncertainty by achieving uniform entity-specific compensation across state agencies and affiliated entities. Swift collaboration with advisors when audits arise enhances dispute resolution capabilities.

As states continue to gain confidence in challenging transfer pricing, multistate corporations must take proactive measures to ensure the resilience of their intercompany transactions under intensified scrutiny.

Get Ahead of the Game with a Transfer Pricing Study

If your company engages in substantial intercompany transactions across state lines, initiating a review of your current pricing policies, preparing your transfer pricing policies, and ensuring compliance with U.S. transfer pricing rules should be a top priority. Proactive measures can help you stay ahead of potential issues before state auditors come knocking. We have a robust transfer pricing team that works closely with our State and Local (SALT) Tax and Tax Controversy practices. Through a combined effort we can support you through every stage of managing a transfer pricing audit. Talk to our transfer pricing professionals today to find out how we can help you minimize your exposure to transfer pricing audits.

]]>- In April, the U.S. Tax Court made news when it ruled in favor of businessman Alon Farhy, who challenged the Internal Revenue Service (IRS)’s authority to assess penalties for the failure to file IRS Form 5471.

- IRS Form 5471 is the Information Return of U.S. Persons With Respect to Certain Foreign Corporations.

- Taxpayers may be interested in filing protective refunds, and they should start the process sooner rather than later—there is a statute of limitations of two years for claiming refunds.

- This case’s ruling could have reverberating effects when it comes to the IRS collecting additional penalties, but only time will tell.

On April 3, 2023, the U.S. Tax Court came to a decision in the case Farhy v. Commissioner, ruling that the Internal Revenue Service (IRS) does not have the statutory authority to assess penalties for the failure to file IRS Form 5471, or the Information Return of U.S. Persons With Respect to Certain Foreign Corporations, against taxpayers. It also ruled that the IRS cannot administratively collect such penalties via levy.

Now that the IRS doesn’t have the authority to assess certain foreign information return penalties according to the court, affected taxpayers may want to file protective refund claims, even if the case goes to appeals — especially given the short statute of limitations of two years for claiming refunds.

Our Tax Controversy team breaks down the Farhy case, as well as what it may mean for your international filings — and the future of the IRS’s penalty collections.

The case

Alon Farhy owned 100% of a Belize corporation from 2003 until 2010, as well as 100% of another Belize corporation from 2005 until 2010. He admitted he participated in an illegal scheme to reduce his income tax and gained immunity from prosecution. However, throughout the time of his ownership of these two companies, he was required to file IRS Forms 5471 for both — but he didn’t.

The IRS then mailed him a notice in February 2016, alerting him of his failure to file. He still didn’t file, and in November 2018, he assessed $10,000 per failure to file, per year — plus a continuation penalty of $50,000 for each year he failed to file. The IRS determined his failures to file were deliberate, and so the penalties were met with the appropriate approval within the IRS.

Farhy didn’t dispute that he didn’t file. He also didn’t deny he failed to pay. Instead, he challenged the IRS’s legal authority to assess IRC section 6038 penalties.

The court’s ruling

The U.S. Tax Court then held that Congress authorized the assessment for a variety of penalties — namely, those found in subchapter B of chapter 68 of subtitle F — but not for those penalties under IRC sections 6038(b)(1) and (2), which apply to Form 5471. Because these penalties were not assessable, the court decided the IRS was prohibited from proceeding with collection, and the only way the IRS can pursue collection of the taxpayer’s penalties was by 28 U.S.C. Sec. 2461(a) — which allows recovery of any penalty by civil court action.

How this court decision affects your international penalty assessments

This case holds that the IRS may not assess penalties under IRC section 6038(b), or failure to file IRS Form 5471. The case’s ruling doesn’t mean you don’t have an obligation to file IRS Form 5471 — or any other required form.

Ultimately, this decision is expected to have a broad reach and will affect most IRS Form 5471 filers, namely category 1, 4, and 5 filers (but not category 2 and 3 filers, who are subject to penalties under IRC section 6679).

However, the case’s impact could permeate even deeper. For years, some practitioners have spoken out against the IRS’s systemic assessment of international information return (IIR) penalties after a return is filed late, making it impossible for taxpayers to avoid deficiency procedures. The court’s decision now reveals how a taxpayer can be protected by the judicial branch when something is deemed unfair. Farhy took a stand, challenged the system, and won — opening the door for potential challenges in the future.

It’s uncertain as to whether the IRS will appeal the court’s decision. But it seems as though the stakes are too high for the IRS not to appeal. While we don’t know what will happen, a former IRS official has stated he expects that, for cases currently pending review by IRS Appeals, Farhy will not be viewed as controlling law yet.

The impact of the ruling is clear and will most likely impact many taxpayers who are contesting — or who have already paid — IRC 6038 penalties. It may also affect other civil penalties where Congress has not prescribed the method of assessment in the future.

How you should respond to the court’s decision

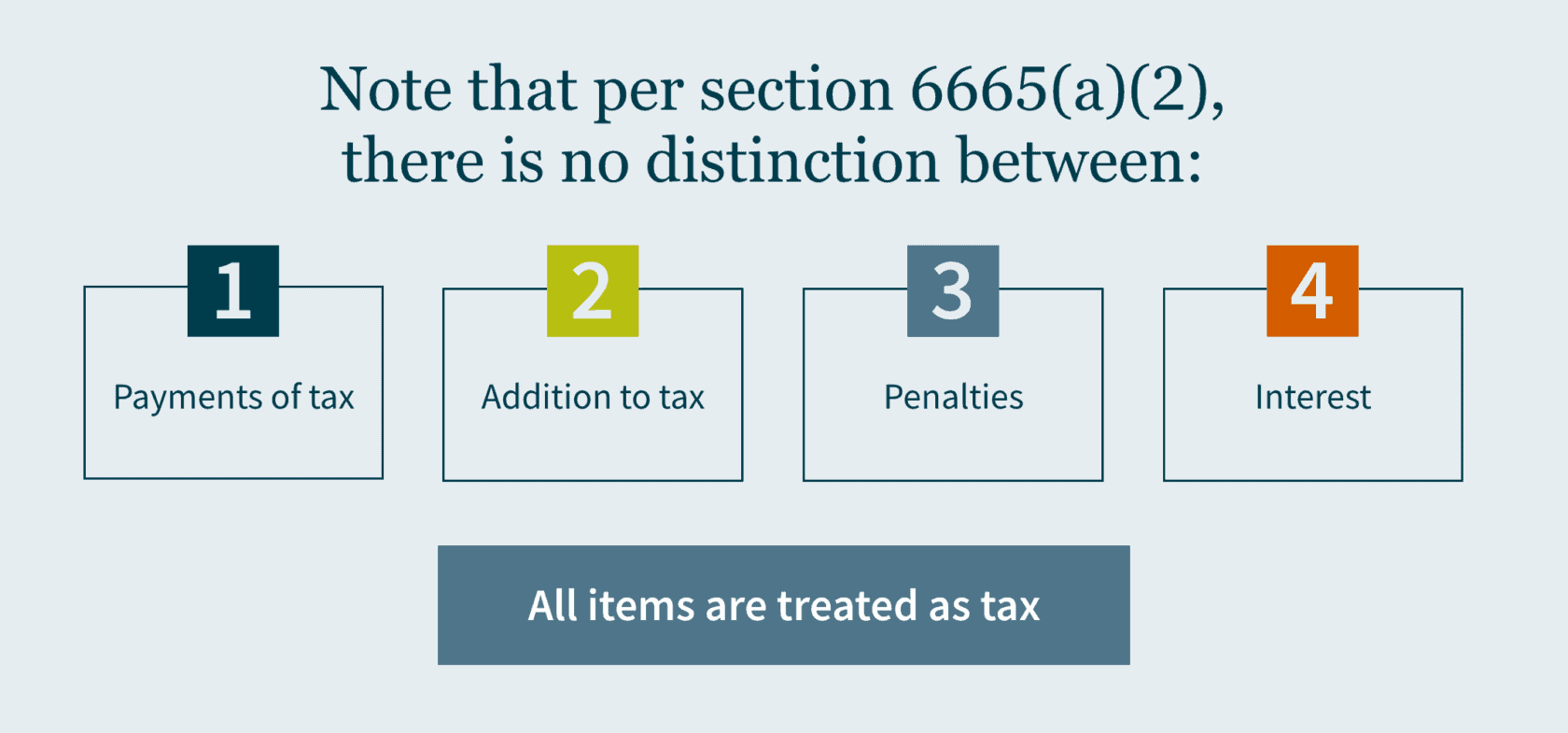

You should move quickly to take advantage of the court’s decision, as there is a two-year statute of limitations from the time a tax is paid to make a protective claim for a refund. It’s likely this legislation wouldn’t affect refund claims since that would be governed by the law that existed when the penalties were assessed. Note that per IRC section 6665(a)(2), there is no distinction between payments of tax, addition to tax, penalties, or interest — so all items are treated as tax.

If you’ve previously paid the $10,000 penalty, it’s important to file your protective claim now, unless you’ve entered into an agreement with the IRS to extend the statute of limitations, which can occur during an examination. Requesting a refund won’t ever hurt, but some practitioners believe the IRS may try to keep any penalty money it collected, even if the assessment is invalid— because, in its eyes, the claim may not be. Just know, you can file your protective claim for a refund but may not get it, at least not any time soon.

The Farhy decision could likewise be applied to other US IRS forms, such as 5472, 8865, 8938, 926, 8858, 8854, and some argue the Farhy decision may also be applied to IRS Form 3520.

How MGO can help

Only time will tell if the court’s decision will open the government up to additional criticisms for other penalty assessments. If you have paid your penalties and are wondering what your current options are, MGO’s experienced International Tax team can help you determine if you’re eligible to file a refund claim.

Contact us to learn more.

]]>

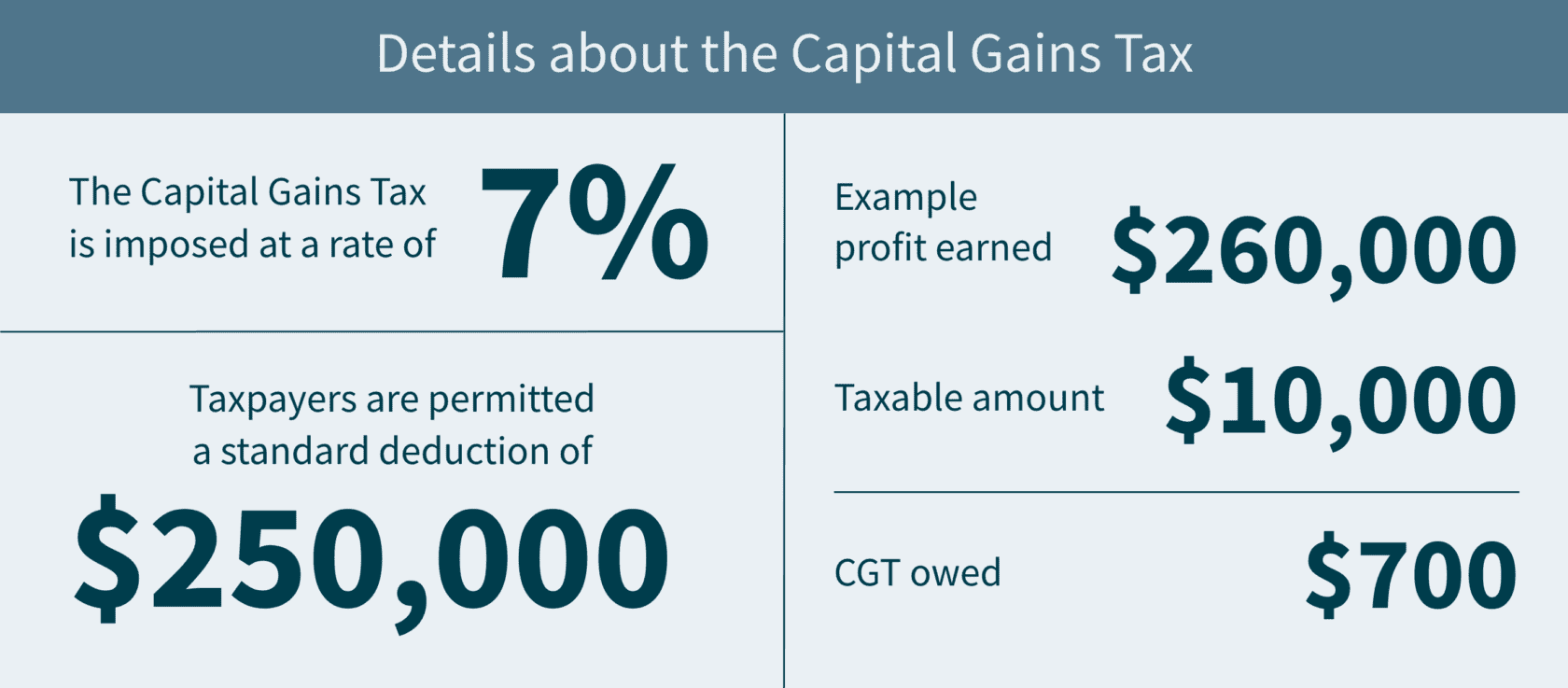

- The Supreme Court of Washington State issued a landmark ruling maintaining the constitutionality of the state’s capital gains tax (CGT) by determining that it’s an excise tax, or a tax on a good or service (and not a property tax).

- It’s imposed at a rate of 7% and taxpayers can claim a standard deduction of $250,000.

- There are other deductions, like long-term gains from the sales of qualified family-owned small businesses and charitable contributions of more than $250,000.

- You may be able to apply a tax credit.

On March 24, 2023, the Supreme Court of Washington State (SCOWA) ruled 7-2 to uphold the constitutionality of the state’s controversial capital gains tax. Thus, by the April 18, 2023, deadline, Washington residents recognizing capital gains income (and nonresidents engaged in transactions occurring within the state) in 2022 will have to calculate this new tax and pay accordingly.

Our State and Local Tax team breaks down what you need to know about this divisive tax with an impending deadline.

The details about CGT

The CGT was created when Washington enacted Senate Bill 5096 in April 2021 with the intention of having the excise tax proceeds — projected to be nearly $415 million — fund the state’s early education and childcare programs. Charged on long-term Washington-allocated capital gains, the CGT is imposed at a rate of 7% of an individual’s federal capital gain from a sale or exchange of long-term investments that exceed $250,000. This includes stocks, bonds, businesses, and other assets.

The controversy of CGT

This bill has generated controversy since its inception — mostly because it is categorized as an excise tax and not an income tax (Washington is one of nine states that doesn’t have income tax due to limitations in the state constitution on the state government assessing a tax on “property”). As a reminder, an excise tax is a legislated tax on the sale of specific services, activities, or goods.

In March 2022, the Douglas County Superior Court in Washington deemed the CGT unconstitutional as an impermissible income tax that is only masquerading as an excise tax. The Court defined gains as income, and therefore property under the Washington Constitution, that the state impermissibly taxed at a non-uniform rate (i.e., the tax doesn’t apply to every resident equally, but only those whose profits exceed the $250,000 threshold). In the past, Washington’s Supreme Court has considered income as property — and property must be taxed at a flat rate.

Since state revenue relies on sales and business taxes, taxpayers who earn the least will end up paying a higher share of their income in tax. This notion has split public opinion. Community groups and labor unions believe the tax is not just legal, it’s necessary because of its capability to create a more equitable tax system. But organizations with business interests in mind find it to be bad public policy in addition to violating the constitution.

However, the Washington Supreme Court ruled to uphold the tax, agreeing it is constitutional as an excise tax — “levied on the sale or exchange of capital assets, not on capital assets or gains themselves.” In other words, the Court reasoned that the tax is tied not to the person’s ownership interest in the property (which would be unconstitutional), but on the transaction itself.

Calculating your tax base

Adjusted capital gains

As mentioned, the new tax is imposed on your adjusted capital gains allocated to Washington, minus allowable deductions and exemptions. First, it starts with your federal net long-term capital gain for the tax year. It’s then adjusted by adding back long-term capital losses from sales or exchanges that are exempt or not allocated to the state. Finally, you subtract your long-term capital gains from sales or exchanges that are exempt or not allocated to the state.

Deductions

There are several deductions allowed against adjusted capital gains. Individual taxpayers are permitted a $250,000 standard deduction in calculating the CGT. But married or state-registered domestic partners that file a single federal tax return collectively have only a single $250,000 deduction. For example, if you earned $260,000 in profit from selling bonds in the past year, only $10,000 would be taxed, and the CGT owed would be $700. And if you and your husband together earned $260,000 from selling bonds, you wouldn’t get to “double” the standard deduction – you’d have the same tax bill.

Additional deductions include long-term gains from the sales of qualified family-owned small businesses, and charitable contributions. Associated regulations do treat the sale or transfer of an interest in a “qualified family-owned small business” as a separate deduction from the charitable deduction. (Note that the “qualified family-owned small business” is not the same as the federal Qualified Small Business Stock (QSBS) tax exclusion — there are separate requirements). To receive the charitable deduction, you would need to contribute over $250,000, not exceeding a deduction of $100,000 in total. Consequently, if you donate $350,000, you’ll receive the maximum deduction.

Exemptions

Certain long-term capital gains and losses from sales of capital assets are not subject to the tax. These exempt items include sales or exchanges of the following types of assets:

- Livestock;

- Timber;

- Real estate, and land structures; and

- Capital assets held in IRAs, 401(k) plans, and other qualified retirement plans

Allocating your capital gains and losses

If you were living in Washington at the time of a sale or exchange of intangibles (e.g., stocks, bonds, etc.), related long-term capital gains and losses are allocated to Washington.

In addition, gains or losses from the sale or exchange of other (tangible) personal property is allocated to Washington if:

- The property was in Washington at any time during the tax year when the sale/exchange occurred,

- You were a Washington resident at the time of the sale/exchange, and

- You were “not subject to the payment of an income tax or excise tax legally imposed” by another jurisdiction* on that long-term capital gain or loss.

* Jurisdiction is defined to include not only U.S. states, political subdivisions, territories, and possessions, but also foreign countries and political subdivisions of foreign countries.

Good news: a tax credit is available

If you’re interested in applying a tax credit against this new tax, you might be able to. Any Washington capital gains tax can qualify as a credit against the Washington business and occupation (B&O) tax — given that the B&O tax includes the gain from a transaction subject to capital gains tax (because it applies to ALL gross receipts regardless of character).

In addition, a credit can be applied for an income or excise tax legally imposed by another jurisdiction on capital gains “derived from capital assets within the other taxing jurisdiction to the extent such capital gains are included in the taxpayer’s Washington capital gains.”

Filing your returns

Remember, a Washington capital gains tax return is required only if tax is owed — and it must be filed on or before the due date of your federal income tax return, including extensions. But the payment of the tax is required BY the original due date of your federal income tax return, NOT including extensions. Any filing and payments must be done online using the MyDOR portal by April 18, 2023, for most taxpayers.

How MGO can help

Keep in mind that while this tax will more than likely impact Washington residents the most, if you are a nonresident whose capital gains from the sales and exchanges of your tangible personal property is allocated to Washington, you could be affected too. Accordingly, anyone with a large gain event (other than the sale of real property) during 2022 or later years, should consider whether this tax may affect them.

MGO’s State and Local Tax team can help you prepare and file this return and manage any of the other surprises that can occur in state and local tax. Contact us if you have additional questions about how the capital gains tax impacts your finances, or if you’re interested in additional strategies to boost your tax efficiency.

]]>What is the policy now? Well, the Tax Cuts and Jobs Act (TCJA) of 2017 changed the treatment of R&E costs so that taxpayers must capitalize all R&E costs incurred after December 31, 2021, and amortize them over either a five-year period (domestic costs) or a 15-year period (foreign costs). Previously, taxpayers could either (1) immediately deduct R&E expenditures, or (2) elect to amortize those costs over a period of five or more years, which gave the taxpayer the ability to choose the option that would be the most beneficial for them.

While it is still possible for the legislative process to postpone or repeal mandatory capitalization of Section 174 costs (including retroactively applying any changes to the 2022 tax year), such legislation would need to have bipartisan support due to the currently divided Congress.

In this article, we review what it would mean for your business if the much-anticipated revisions to Section 174 do not occur, and what kind of planning you should do to prepare on the front end. A number of these recommendations will be further refined once additional IRS guidance is provided.

Background on 174 R&E expenditures

R&E expenses for income tax purposes are defined under Section 174 and its regulations. In Treasury Regulation Section 1.174-2(a), R&E expenditures are described as expenditures incurred by the taxpayer in connection with the taxpayer’s trade or business in the experimental or laboratory sense. Section 174(c)(3) – added by the TCJA – also notes that any amount paid or incurred in connection with the development of any software shall also be an R&E expenditure subject to capitalization. Generally, when determining R&E expenses, not only are direct costs of R&E factored in, but also the indirect costs incident to the development or improvement of a product.

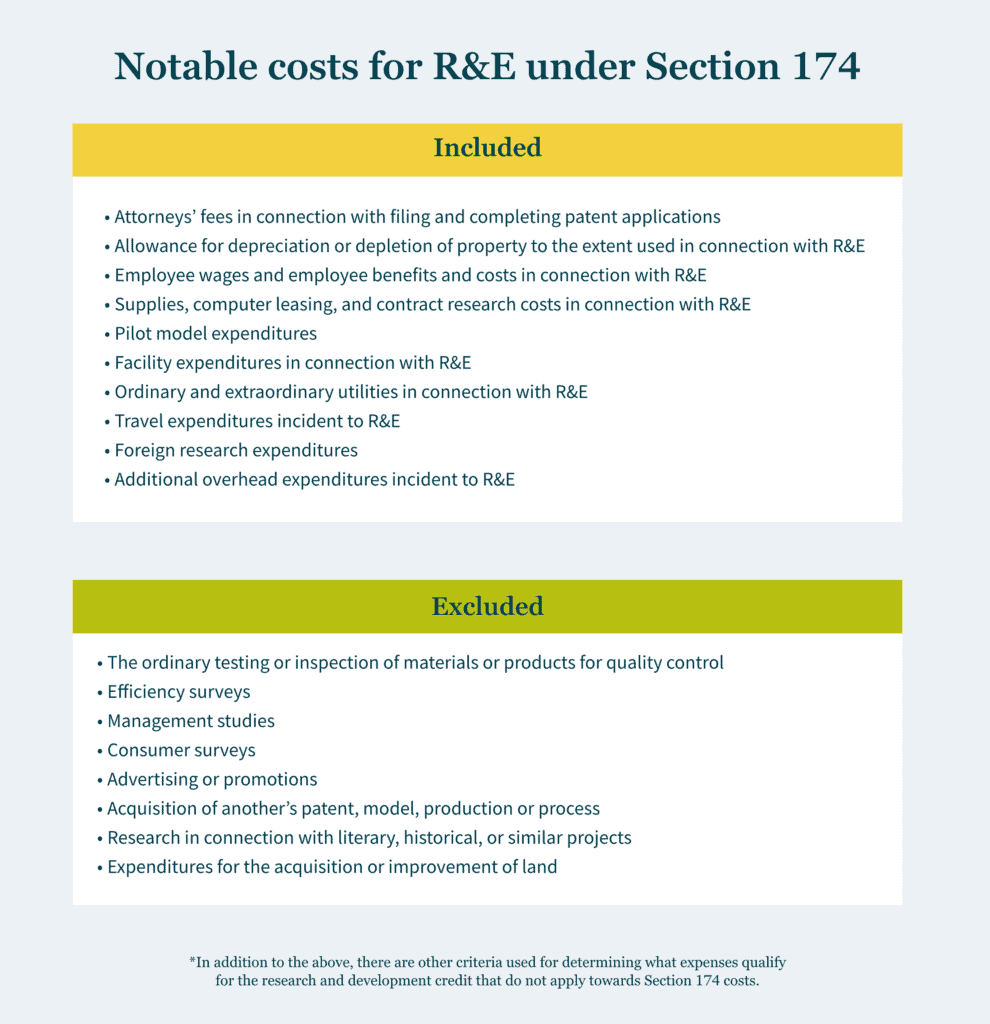

Common expenses included in R&E costs under Section 174 are the following. Many of these expenses are considered for Section 174 specifically and are not qualified research expenses for purposes of the R&D credit.

- Attorneys’ fees in connection with filing and completing patent applications.

- Allowance for depreciation or depletion of property to the extent used in connection with R&E.

- Employee wages and employee benefits and costs in connection with R&E.

- Supplies, computer leasing, and contract research costs in connection with R&E.

- Pilot model expenditures.

- Facility expenditures in connection with R&E.

- Ordinary and extraordinary utilities in connection with R&E.

- Travel expenditures incident to R&E.

- Foreign research expenditures.

- Additional overhead expenditures incident to R&E.

*In addition to the above, there are other criteria used for determining what expenses qualify for the R&D credit that do not apply towards determining Section 174 costs.

In contrast, the following are common expenses that are excluded from the expansive definition of R&E costs under Section 174:

- the ordinary testing or inspection of materials or products for quality control;

- efficiency surveys;

- management studies;

- consumer surveys;

- advertising or promotions;

- acquisition of another’s patent, model, production or process;

- research in connection with literary, historical, or similar projects; and

- expenditures for the acquisition or improvement of land.

The current R&E amortization rule explained

The ability to deduct R&E costs changed for all tax years beginning after December 31, 2021. As previously mentioned, these costs can no longer be deducted in full and must be capitalized and then amortized over five years for domestic costs and over 15 years for foreign costs. This amortization starts at the midpoint of the first year that the expenses were incurred, which results in only 10% of domestic costs (1/2 of 20%) being able to be deducted in their first year.

Per IRS guidance, this mandatory change can be implemented as an automatic accounting method change through attaching a statement to a taxpayer’s first income tax return with a year beginning after 2021, in lieu of filing the much more intricate Form 3115. This change should not have an effect on prior tax years, since the automatic method change is implemented on a “cut-off basis.”

Macro effect of mandatory capitalization

As mentioned above, before the prior rule was changed, every R&E expense could be deducted in full in the year they were incurred. While it is expected that the Section 174 expensing rules will revert to this — to some extent — through pressure from persistent lobbyists, this change has not been incorporated into a bill yet.

Some believe the mandatory R&E capitalization and amortization will adversely affect U.S. innovation, potentially resulting in a detrimental impact on our global competitiveness and jobs. For more than 60 years, businesses were able to immediately deduct their R&D expenses in the year those expenses were incurred (or choose to defer based on what worked for them). Now, the amortization of new R&E costs could cost businesses billions in cash taxes.

Significant considerations

Estimated Tax Payments: For taxpayers making estimated tax payments utilizing current year taxable income, consideration should be given to R&E expenditures and how the capitalization of those expenditures may impact taxable income and timing of cash tax payments. A closer look at refining the various accounts in a taxpayer’s books may be needed for this.

Tax Accounting / ASC 740: Taxpayers should be mindful of whether a new deferred tax asset is created, if any adjustment of existing deferred taxes may be necessary, or if a full or partial valuation allowance may be needed.

Other Areas Affected: The amortization requirement also affects other areas of taxable income, including the following:

- increases the deductibility of business interest under Section 163(j),

- increases the deductibility of the QBI (Qualified Business Income) deduction,

- increases the amount of GILTI (global intangible low-taxed income) for controlled foreign corporations,

- potentially adjusts the amount of FDII (foreign derived intangible income) deduction that can be taken,

- changes the amount of R&E expenses allocable for purposes of the foreign tax credit, and

- impacts state taxable income for the few states that do not conform to the capitalization requirement (e.g., California).

R&D credit considerations

The Section 174 capitalization requirements should not directly impact the amount of expenses that can be used for the R&D Tax Credit under Section 41, since the research credit is calculated using a much smaller subset of R&E expenditures than Section 174 and is not limited by the capitalization requirement. As Section 174 is much broader in scope, it applies to expenditures both eligible and ineligible for the research credit.

Another consideration for tax planning is that the research credit will be even more important to assist with reducing the additional tax liability that will be generated by the R&E treatment change, since the credit can help offset some of the tax liability increase. Moreover, the analysis & processes used to determine the R&D credit can be leveraged to identify Section 174 R&E expenses, which helps create some efficiencies in quantifying the overall effect of the mandatory capitalization and amortization requirement.

Extend impacted returns where possible

Tax return extensions are highly recommended for tax returns that have their due dates coming up. Not only is there the pending IRS guidance that may significantly change R&E expense calculations, but also the act of extending tax returns should allow more time for tax returns to be superseded (rather than amended) and should allow for R&D credit claims to be made on originally filed returns.

This is echoed by a September 2021 Chief Counsel Memorandum issued by the IRS, which made the process for claiming a refund under the R&D credit far more stringent. The memorandum relayed that taxpayers must provide more information on business components, identify the research activities performed, and name the individuals who performed each research activity. Given the additional amount of detail needed, taxpayers making R&D credit claims on amended returns — especially small businesses — have a heavier burden than those who make the claim on an originally filed returns.

How will it affect you?

If the mandatory R&E capitalization requirement is not changed, you should consider how the 174 capitalization rules will affect your business and how claiming the R&D credit will help offset the increase in tax liability. If you currently have an R&D credit analysis and/or an ASC 730 financial statement analysis, those studies can be used as starting points to determine the overall effect of Section 174 — keeping in mind that neither analysis includes all the costs included in Section 174.

If the requirement is changed, there are several ways that the R&E expense landscape could turn out for taxpayers. Ideally, Congress will revert to the prior rule regarding R&D expenses. In that situation, you should be able to choose what is best for you — immediately deducting or deferring.

Our perspective

As experienced advisors, MGO can help model the best R&E position for you, through the 2022 tax year and beyond — potentially saving you significant amounts of money. Our holistic tax advisor and business advisor-first philosophy factors not only the direct effects of the R&E capitalization requirement, but also the impact on other areas of your tax returns (e.g., international, transfer pricing, state, and local tax) and what potential savings you can obtain by claiming the R&D credit. Please feel free to reach out to any of our R&E costing profesionals below to get the experienced insight that you deserve.

About the author

Danielle Bradley is a senior manager in MGO’s National Tax Credits and Incentives practice. She focuses on helping businesses identify, substantiate, and defend federal and state tax credits and incentives. She has helped hundreds of companies monetize and defend over $100 million in various tax credits and incentives, such as the Research and Development (R&D) Tax Credit, Orphan Drug Credit, Employee Retention Credit, meals and entertainment deduction, and the current Research and Experimental (R&E) amortization calculations. Danielle has extensive experience in various industries, including software and technology, life sciences, manufacturing, aerospace and defense, and food, beverage and agriculture businesses.

Contact Danielle to further discuss the R&E amortization or other credits and incentives at Danielle Bradley, Matthew Sapowith (Tax Partner), or Michael Silvio (Tax Partner).

]]>The tax relief postpones tax filing and payment deadlines occurring between January 8, 2023, and May 15, 2023, to a new due date of October 15, 2023.

Some of the filings and payments postponed include:

- Individual income tax returns due on April 18

- Business tax returns normally due on March 15 and April 18

- 2022 contributions to IRAs and health savings accounts

- Quarterly estimated tax payments normally due January 17 and April 18

- Quarterly payroll and excise tax returns normally due on January 31 and April 30

The current list of counties that qualify for this relief can be found here.

If you qualify for this postponement, you generally do not need to contact the IRS or FTB to obtain relief. Relief is automatically granted for affected taxpayers who have an address of record located in one of the designated counties. However, if you still receive a late filing or late payment notice and the notice shows the original or extended filing, payment, or deposit due date falling within the postponement period, you should call the number on the notice to have the penalty abated.

If you have questions or need assistance, contact MGO’s experienced State and Local Tax team.

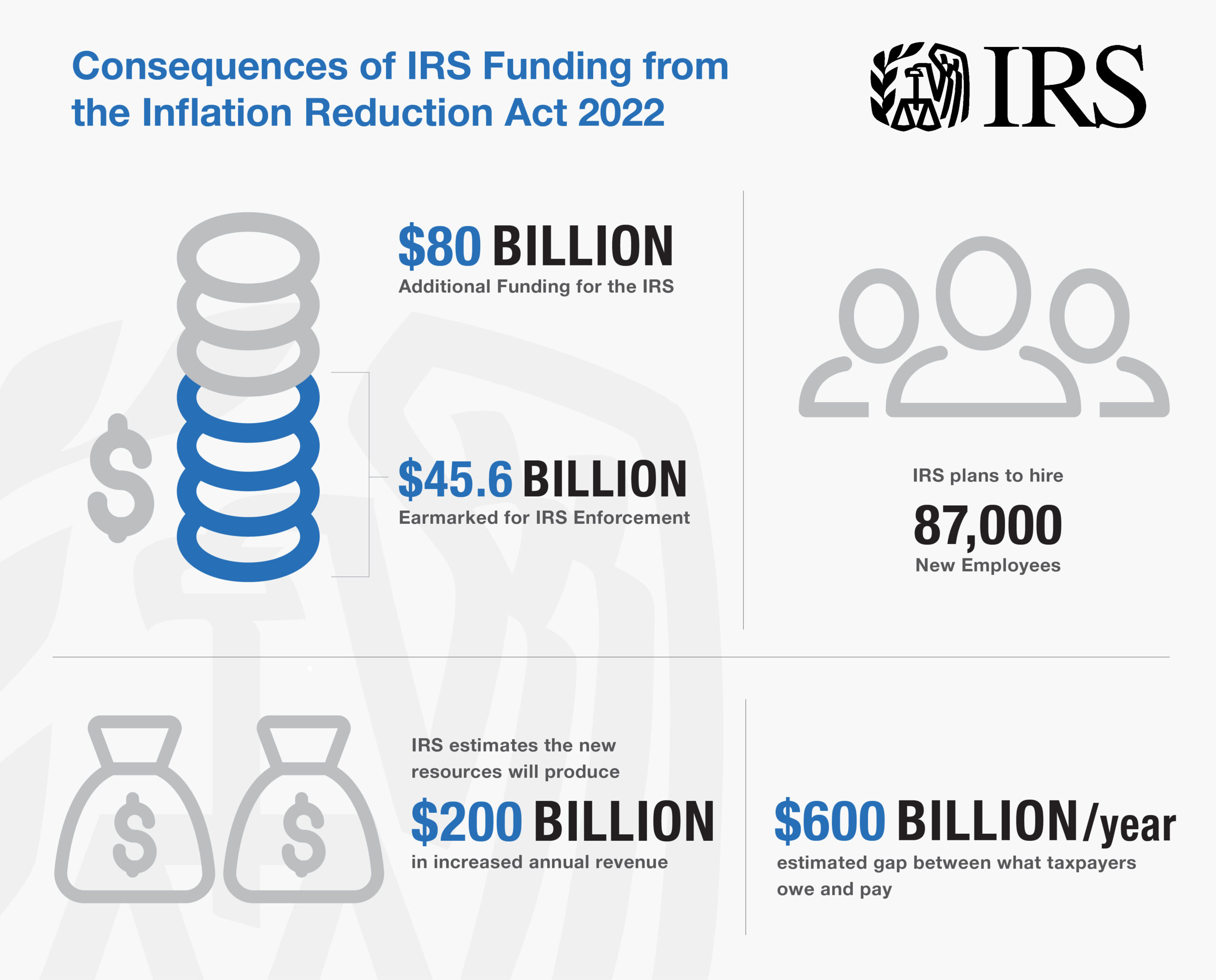

]]>- The Inflation Reduction Act of 2022 includes $80B in funding for the Internal Revenue Service.

- Over half of the funding will be set aside for IRS enforcement so the agency can hire more staff to conduct more audits, hoping to target those who do not pay their taxes.

- This will most likely subject those taxpayers with complex filings to additional scrutiny.

The Inflation Reduction Act of 2022 was recently signed into law with an eye-opening provision: the inclusion of nearly $80 billion in additional funding for the Internal Revenue Service (IRS). $45.6 billion of that is earmarked for IRS enforcement, which will be used to help the underfunded agency hire additional staff and conduct future audits in the hopes of collecting unpaid taxes.

Many publications cite the IRS plans to hire up to 87,000 new employees, though the actual number will be released in the coming months. These new hires will fill positions ranging from auditors to customer service representatives to IT specialists. The IRS has been plagued by more than a decade of budget cuts, which has limited its ability to modernize its old technology and staff appropriately. Since 2010, the agency’s enforcement staff has declined by 30%. The funding appropriate in the Inflation Reduction Act hopes to reverse this trend and bring in an estimated $203 billion in increased revenue.

The MGO Tax Controversy team breaks down what you need to know about this big change that could increase your risk of an audit.

How will the increase in IRS staff affect taxpayers?

Critics of the increase in IRS funding have claimed that the new resources will be used to target low to middle-income Americans and small businesses, burdening them with more audits and examinations. The Treasury Department refutes these claims reiterating they plan to focus primarily on large corporations and the wealthy — those more likely to evade paying their taxes — to close the tax gap, or the difference between what taxpayers pay in taxes and what they actually owe – an estimated to be $600 billion per year.

The IRS hopes the investment in funding will bring in around $203.7 billion in revenue because between 2015 and 2019, IRS audits declined significantly — 75% for Americans making $1 million or more and 33% for filers with low to moderate incomes. Lower-income Americans are mostly wage earners, so their audits are less complex and can be automated. However, more complex filers, notably large corporations and high-net-worth individuals and families – require the hands-on engagement of IRS agents and are most likely to experience increased levels of scrutiny from the new hires.

Ultimately, the average taxpayer should have an improved tax filing experience. New staff will be on hand to answer questions by phone, technology systems will be improved and modernized, and the backlog of unprocessed returns should diminish.

What is the timeline for implementing these changes?

While there is no set timeline, it is likely the way IRS audits work will change with the increase in funding. Currently, software is used to rank each tax return with a numeric score, and higher scores trigger an audit. Other mechanisms the IRS uses to determine candidates for audits include enforcement initiatives referred to as “campaigns” based on various criteria. The new funding will take time to phase in, and so will the hiring and training of new workers. It is expected new auditors will complete a six-month training program, starting small with cases involving a few hundred thousand dollars instead of tens of millions. Forbes performed some creative math to conclude while the funding will increase IRS audits, it is not likely to occur for the next few years.

How can I avoid future audits?

The best way to avoid an audit remains simple: pay your taxes on time and in compliance with tax laws. Simple accounting and documentation best practices are your best friend. If you feel you are at risk for a potential audit, you’ll want to get a head start now by ensuring your records are accurate and have been updated and maintained. Save your receipts and include every detail you can in your bookkeeping logs. If you do get audited in the coming wave, you’ll be glad you have all of this information organized and on-hand.

Our perspective on the increase in IRS staffing

The IRS has long been criticized because of their inability to provide taxpayers with the level and quality of service they deserve. The increase in funding as part of the Inflation Reduction Act should help. On the other hand, the number of tax audits is likely to increase, and you will want to be ready.

MGO’s dedicated Tax Controversy team can help by providing a holistic look at your tax filings as well as provide guidance for conflict resolution. From prevention to resolution, we guide you every step of the way.

If you’re an operator or investor in the cannabis industry, our Tax Practice recently published the Cannabis IRS Audit Survival Guide, which details everything you need to do to prepare for and navigate a tax audit. You can download the Guide for free here.

About the author

T. Renee Parker is a tax partner and the National Tax Controversy Practice Leader at MGO. With more than 15 years of tax controversy experience, she is a member of the IRS Tax Advocacy Panel and is well-versed in all areas of tax controversy. These include but are not limited to U.S. federal, state, and local tax audits; sales and use/payroll tax audits; international tax compliance related audits; negotiation and settlements with tax authorities; and corresponding and negotiation with tax authorities. Contact Renee at RParker@MGOCPA.com.

]]>While it appears that several of the more disadvantageous provisions targeting businesses won’t make it into the final bill, others may. In addition, some temporary provisions are coming to an end, requiring businesses to take action before year end to capitalize on them. As Congress continues to negotiate the final bill, here are some areas where you could act now to reduce your business’s 2021 tax bill.

Research and experimentation

Section 174 research and experimental (R&E) expenditures generally refer to research and development costs in the experimental or laboratory sense. They include costs related to activities intended to uncover information that would eliminate uncertainty about the development or improvement of a product.

Currently, businesses can deduct R&E expenditures in the year they’re incurred or paid. Alternatively, they can capitalize and amortize the costs over at least five years. Software development costs also can be immediately expensed, amortized over five years from the date of completion or amortized over three years from the date the software is placed in service.

However, under the Tax Cuts and Jobs Act (TCJA), that tax treatment is scheduled to expire after 2021. Beginning next year, you can’t deduct R&E costs in the year incurred. Instead, you must amortize such expenses incurred in the United States over five years and expenses incurred outside the country over 15 years. In addition, the TCJA requires that software development costs be treated as Sec. 174 expenses.

The BBBA may include a provision that delays the capitalization and amortization requirements to 2026, but it’s far from a sure thing. You might consider accelerating research expenses into 2021 to maximize your deductions and reduce the amount you may need to begin to capitalize starting next year.

Income and expense timing

Accelerating expenses into the current tax year and deferring income until the next year is a tried-and-true tax reduction strategy for businesses that use cash-basis accounting. These businesses might, for example, delay billing until later in December than they usually do, stock up on supplies and expedite bonus payments.

But the strategy is advised only for businesses that expect to be in the same or a lower tax bracket the following year — and you may expect greater profits in 2022, as the pandemic hopefully winds down. If that’s the case, your deductions could be worth more next year, so you’d want to delay expenses, while accelerating your collection of income. Moreover, under some proposed provisions in the BBBA, certain businesses may find themselves facing higher tax rates in 2022.

For example, the BBBA may expand the net investment income tax (NIIT) to include active business income from pass-through businesses. The owners of pass-through businesses — who report their business income on their individual income tax returns — also could be subject to a new 5% “surtax” on modified adjusted gross income (MAGI) that exceeds $10 million, with an additional 3% on income of more than $25 million.

Capital assets

The traditional approach of making capital purchases before year-end remains effective for reducing taxes in 2021, bearing in mind the timing issues discussed above. Businesses can deduct 100% of the cost of new and used (subject to certain conditions) qualified property in the year the property is placed in service.

You can take advantage of this bonus depreciation by purchasing computer systems, software, vehicles, machinery, equipment and office furniture, among other items. Bonus depreciation also is available for qualified improvement property (generally, interior improvements to nonresidential real property) placed in service this year. Special rules apply to property with a longer production period.

Of course, if you face higher tax rates going forward, depreciation deductions would be worth more in the future. The good news is that you can purchase qualifying property before year-end but wait until your tax filing deadline, including extensions, to determine the optimal approach.

You can also cut your taxes in 2021 with Sec. 179 expensing (deducting the entire cost). It’s available for several types of improvements to nonresidential real property, including roofs, HVAC, fire protection systems, alarm systems and security systems.

The maximum deduction for 2021 is $1.05 million (the maximum deduction also is limited to the amount of income from business activity). The deduction begins phasing out on a dollar-for-dollar basis when qualifying property placed in service this year exceeds $2.62 million. Again, you needn’t decide whether to take the immediate deduction until filing time.

Business meals

Not every tax-cutting tactic has to be dry and dull. One temporary tax provision gives you an incentive to enjoy a little fun.

For 2021 and 2022, businesses can generally deduct 100% (compared with the normal 50%) of qualifying business meals. In addition to meals incurred at and provided by restaurants, qualifying expenses include those for company events, such as holiday parties. As many employees and customers return to the workplace for the first time after extended pandemic-related absences, a company celebration could reap you both a tax break and a valuable chance to reconnect and re-engage.

Stay tuned

The TCJA was signed into law with little more than a week left in 2017. It’s possible the BBBA similarly could come down to the wire, so be prepared to take quick action in the waning days of 2021. Turn to us for the latest information.

]]>Specific scams that mask as abusive or fraudulent tax avoidance strategies to be aware of include concealing assets in offshore accounts and improper reporting of digital assets, manipulation of high-income taxpayers to file their tax returns, abusive syndicated conservation easements, and abusive micro-captive insurance arrangements. Read more to round out the annual list for the 2022 filing season.

Tips for taxpayers on emerging scams

To avoid compromising yourself with these “too good to be true” schemes, taxpayers should stay wary, as these scams adopt a wide range of communication methods, including:

- Emails

- Phone calls

- Social media posts

- Targeted online advertisements

You must also consider each source before putting any of these arrangements on your tax returns — because ultimately, you are the one responsible for what is on the return, not the promoter who reached out to you and made a promise they failed to uphold. To mitigate risk, an anxious taxpayer should turn to trustworthy tax professionals to assist with their returns.

Read on to learn about these Dirty Dozen scams targeted primarily to high-net-worth individuals who may be trying to knowingly — or unknowingly — avoid filing.

Scam #9: Concealing Assets in Offshore Accounts and the Improper Reporting of Digital Assets

We hear Switzerland is beautiful this time of year … and so do some high-net-worth individuals looking to conceal their assets in offshore accounts (and yes, that does include cryptocurrency and other digital assets). As more taxpayers look to complex international tax avoidance schemes, the IRS is more determined than ever to “protect the integrity of the U.S. tax system” by enforcing tax responsibilities.

Whether it entails offshore banks, brokerage accounts, nominee entities, employee leasing schemes, foreign trusts, structured transactions, or private annuities, all are designed to hide the true owner of an account — which is illegal, considering U.S. taxpayers are taxed on all the income they make, not just what they keep in the country. But scammers know you may not want to give up some of your hard-earned assets to Uncle Sam. So, what do they do? They sell you a convincing story: you can easily evade the government and hide your assets through digital asset holdings; they claim these are “undetectable by tax authorities.” The catch? They are definitely detectable. By believing these fraudsters, you run the risk of being criminally charged or penalized, so in the end, it is better to report your assets — yes, all of them — when you file.

Scam #10: High-Income Individuals Who Don’t File Tax Returns

Believe it or not, there are some taxpayers who choose to just … not file a tax return. And believe it or not, there are scamming professionals out there aiming to convince you this is a good idea. The IRS takes this seriously. If you are considering this option, remember the Failure to File Penalty is higher than the Failure to Pay Penalty, meaning you are better off filing an accurate, timely return (and setting up a payment plan, if you are concerned about that) rather than not filing and hoping you get out of paying whatever taxes you owe.

Scam #11: Abusive Syndicated Conservation Easements

In this scam, dishonest promoters manipulate a part of the tax law that allows for conservation easements by inflating appraisals of underdeveloped land (i.e., the guise of a real estate investment) and engaging in bogus partnerships without a business purpose. These “deals” rarely help you out; instead, they benefit the promoters, who charge high fees, and clog the tax system with fraudulent tax deductions. (In the last five years, the IRS determined billions of dollars of deductions were wrongly claimed!) And if you are caught — which, you should expect to be, because the IRS takes a microscope to every single one of these “deals” — you can expect large fines and potential time in court.

Scam #12: Abusive Micro-Captive Insurance Arrangements

A high priority for the IRS, this scam sees professionals like accountants and wealth planners convince entity owners to pay for what they believe to be insurance coverage against unlikely events, events that are already being covered, or disingenuous business needs. Complete with sky-high premiums, the abusive structure does the opposite of protecting your organization’s tax safety — it opens you up to more risk as a ”micro-captive” to these “professionals” taking advantage of you. Be on the lookout for an offshore version of this too.

Consequences of falling for a Dirty Dozen scheme

It is important for taxpayers who have already taken part in transactions like these — or those who are thinking about doing so — to consult a tax professional before claiming any tax benefits they think they are owed.

Those taxpayers who have already claimed the purported tax benefits of one of these four “Dirty Dozen” arrangements on a tax return should file an amended return and go to an independent professional for guidance. If necessary, the IRS will examine the tax benefits from transactions like the ones depicted in the list and inflict penalties related to accuracy ranging from 20% to 40%, or a civil fraud penalty of 75% on any taxpayer who underpaid.

Our perspective on the latest batch of “Dirty Dozen” scams

This is not, of course, an exhaustive list of every scam the IRS has its eye on this year. But it does include some of the more common trends. The best advice we can give? If something looks too good to be true … it probably is. Consult your tax professional for guidance and know that it is in your best interest to stay aware of these nefarious arrangements, so you do not fall susceptible to additional penalties.

And remember, you cannot hide income from the IRS!

MGO’s Tax team brings more than 30 years of experience and is well versed in reviewing your return for compliance. We also stay up to date on the risks, pitfalls, and warnings issued by the IRS so you don’t have to. If you think you have been involved in or are in the process of being involved in one of the Dirty Dozen scams, we can help. Contact us today.

]]>