- The CHIPS Act provides more than $50 billion to boost U.S. semiconductor manufacturing, including current funding opportunities for commercial fabrication facilities and advanced packaging research and development (R&D).

- The Advanced Manufacturing Tax Credit (Section 48D) offers a 25% credit for qualified investments into semiconductor manufacturing facilities placed in service from 2023-2026.

- Companies seeking CHIPS incentives or 48D credit should understand eligibility requirements, review application process details, and connect with specialized tax credits and incentives professionals to ensure maximum benefit.

~

On August 9, 2022, President Joe Biden signed into law the Creating Helpful Incentives to Produce Semiconductors Act of 2022 (commonly referred to as the CHIPS Act). The legislation provides $52.7 billion to increase semiconductor research and development in the United States. The CHIPS Act also established the Advanced Manufacturing Tax Credit (Section 48D), available to entities that manufacture semiconductors.

Recently, the government awarded its first major CHIPS Act grant – providing $1.5 billion to GlobalFoundries, one of the world’s leading semiconductor manufacturers, to expand its semiconductor production in New York and Vermont. That grant is expected to be the first of several announcements in the coming months as the government ramps up CHIPS Act funding.

What is the Purpose of the CHIPS Act?

The intent of CHIPS is simple: the U.S. wants to incentivize domestic companies to manufacture semiconductors. The president called the CHIPS Act a “once-in-a-generation investment in America itself,” as the legislation aims to lower costs and create jobs in the production of these advanced chips.

The COVID-19 pandemic forced the semiconductor industry to operate at a reduced capacity, while lockdowns increased demand for products using semiconductors (computers, tablets, gaming systems, cars, etc.). This created a perfect storm, fueling a shortage of semiconductors. As a result, the U.S. recognized the need to increase its semiconductor output.

However, manufacturing semiconductors is not cheap and requires substantial investments. CHIPS, along with the available tax credit, encourages these investments.

The CHIPS Act includes provisions for:

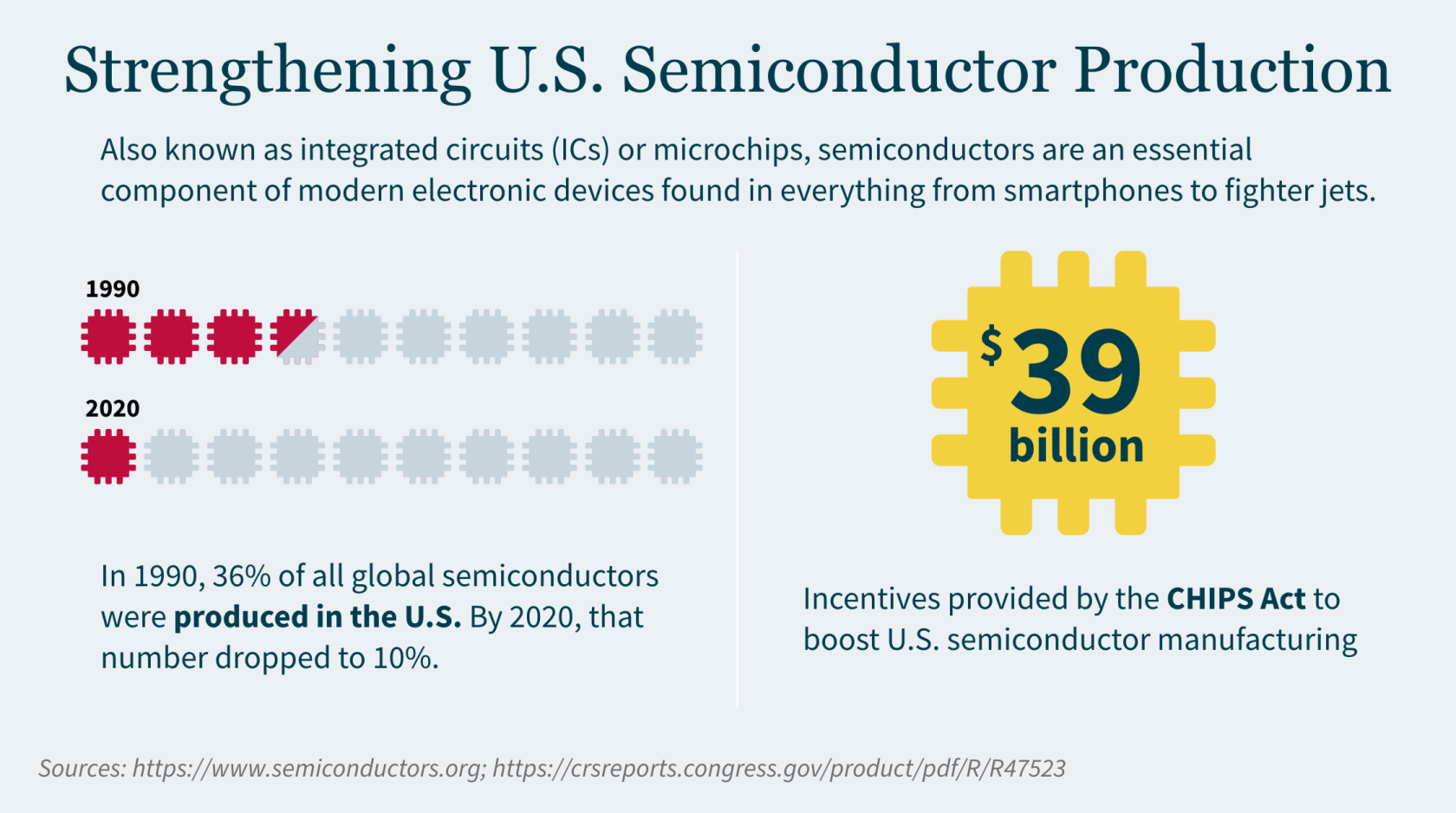

- $39 billion in incentives to build, expand, or modernize domestic facilities and equipment for semiconductor manufacturing, assembly, testing, advanced packaging, or research and development

- $13.2 billion in R&D and workforce development

- $500 million for international information communications technology security and semiconductor supply chain activities

Understanding the Advanced Manufacturing Tax Credit

With the addition of Section 48D to the Internal Revenue Code, CHIPS offers a new tax credit if your company invests in advanced manufacturing facilities or facilities whose primary purpose is manufacturing semiconductors or semiconductor manufacturing equipment.

Eligible businesses can receive a 25% tax credit of “qualified investments”. You can elect to treat the credit as payment against tax (i.e., direct pay) if you do not have sufficient tax liability to utilize the credit, making this essentially a refundable tax credit.

Eligibility criteria for 48D

To be eligible for 48D, you must have made a qualified investment for any taxable year integral to an “advanced manufacturing facility” for semiconductors placed in service during that year. Qualified properties must be:

- Buildings, structural components, or parts of a building (not including administrative services or other functions unrelated to manufacturing)

- Crucial to the operation of the advanced manufacturing facility

- Constructed or built by the taxpayer

- Qualified for amortization or depreciation

Taxpayers that use facilities and equipment outside the U.S. will not be eligible (similar to other investment credit requirements). Other taxpayers ineligible for the credit include:

- Foreign entities noted as “foreign entities of concern” (i.e., foreign terrorist organizations or organizations included on the Office of Foreign Assets Control list).

- Taxpayers that have engaged in significant transactions involving the material expansion of semiconductor manufacturing capacity in China or another foreign country of concern.

- If a taxpayer enters a transaction in a foreign country of concern within 10 years of claiming the credit, it will be recaptured.

48D timing

The tax credit applies to any property placed in service after December 31, 2022, for which construction begins before January 1, 2027. It does not apply after December 31, 2026, nor can you use the tax credit for constructing a property after this date. If construction on a facility began before January 1, 2023, the credit applies only to the portion of the construction started after August 9, 2022.

Application process

In March 2023, the IRS issued proposed regulations addressing direct payment of Section 48D credit. The proposed regulations also require taxpayers to register through an IRS electronic portal before treating Section 48D as a direct payment on a tax return.

The IRS will issue a registration number for each qualified investment for which your company is claiming a credit, and that number must be included on your tax return.

CHIPS Incentive Opportunities

To access CHIPS incentives, your company must first apply for open funding opportunities. To date, the U.S. Department of Commerce has issued three Notice of Funding Opportunities (NOFOs) through the CHIPS for America program:

- Commercial Fabrication Facilities – Currently accepting applicants

- Small-Scale Supplier Projects – No longer accepting applicants, in second phase of process

- National Advanced Packaging Manufacturing Program (NAPMP) Materials & Substrates – Just announced on February 28, 2024

How to apply for open NOFOs

Application forms and instructions are available on the CHIPS Incentives Program application portal. FAQs, guides, and templates can also be found in the “Resources” section of the portal.

The application process includes the following stages:

- Statement of interest

- Pre-application (optional, but recommended)

- Full application

- Due diligence

- Award preparation and issuance

Statement of interest – To submit a statement of interest, applicants need to register for an account on the CHIPS Incentives Portal. A statement of interest must be submitted at least 21 days prior to submitting a pre-application or full application.

Pre-application – The optional pre-application provides an opportunity to ensure your projects are consistent with program requirements. During this stage, you will receive feedback on strengths and weaknesses of your proposal and recommendations for improvement.

Full application – Both pre-applications and full applications are accepted on a rolling basis.

Due diligence – Your application will undergo review to ensure alignment with evaluation criteria specified in the Notice of Funding Opportunity (NOFO), with the possibility of requests for additional information.

Award preparation and issuance – Before receiving an award, you must have an active registration in the System for Award Management (SAM). It’s a good idea to begin the registration process for SAM.gov early as it may take anywhere from two weeks to six months (due to information verification requirements). Check out SAM.gov’s Entity Registration Checklist.

Maximizing Your Semiconductor Manufacturing Tax Credits and Incentives

Navigating CHIPS’s nuances can be challenging – especially when claiming the available tax credit and determining how it is refundable. Furthermore, companies seeking to increase their semiconductor manufacturing capacity in the U.S. should also assess application and opportunity for federal and state R&D tax credits and incentives.

With more than 30 years of experience, our dedicated Tax Credits and Incentives team can help you maximize your credit benefits, develop the appropriate documentation methodology, assist in calculating and claiming credits, and defend your claims. Our full-service firm, led by experienced CPAs and attorneys, provides a holistic approach to examining your organization and determining how to best reach your goals.

]]>Here is a sneak peek into some of the expected goals of the tax framework:

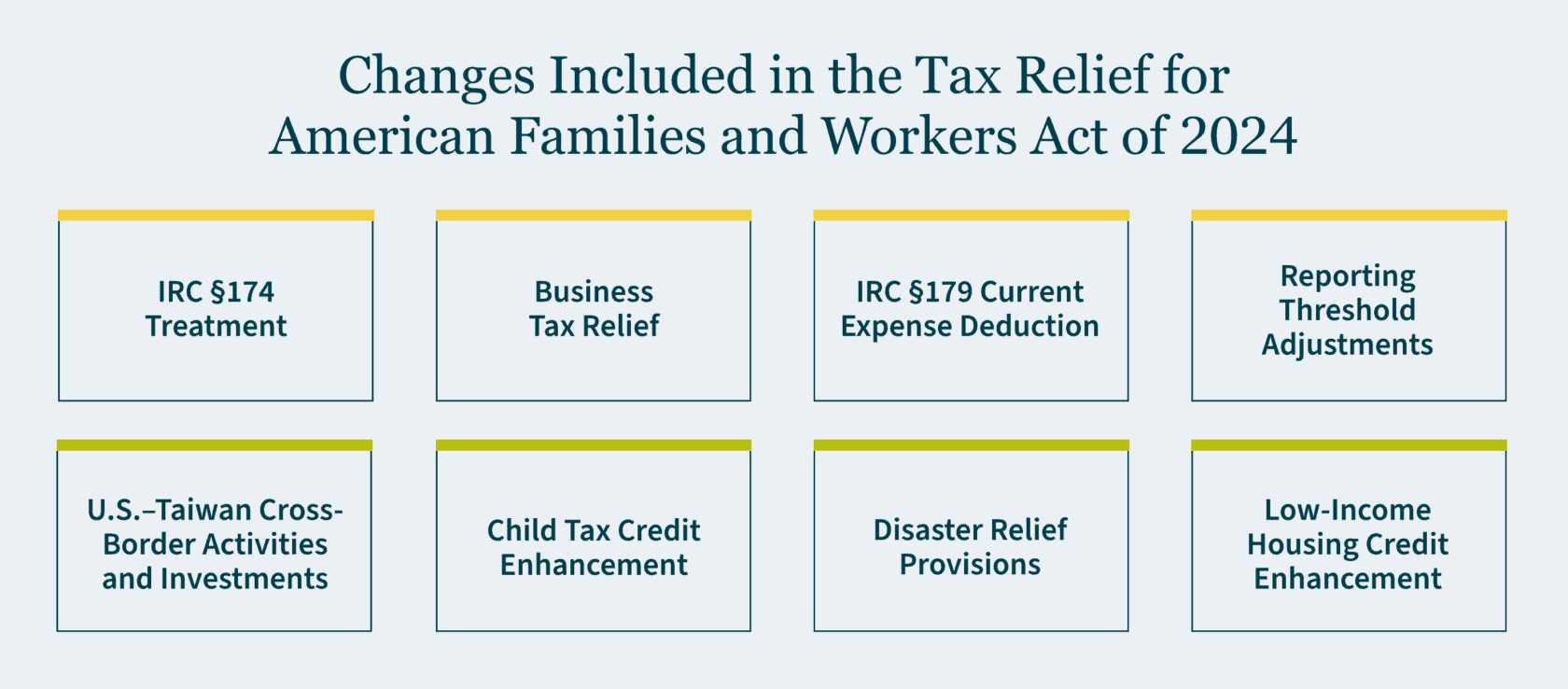

IRC §174 Treatment

- Boost innovation and competitiveness by allowing U.S. R&D expenses to be deducted in the year incurred — in comparison to the current 174 mandatory capitalization over five years, that has been in effect since the 2022 tax year. This change is anticipated to be retroactive to the beginning of 2022 and go through 2025. This should create an opportunity to decrease taxable income on an amended 2022 income tax return.

- 174 capitalization would still be required for foreign expenditures over 15 years.

Business Tax Relief

- Retroactive deferral until 2026 of the reduction in the 100% bonus depreciation deduction.

- Removal of depreciation, amortization, and depletion deductions from the calculation of adjusted taxable income for the IRC 163(j) business interest expense limitation. This change is also anticipated to be retroactive to the beginning of 2022 and be effective through 2025. This may create an opportunity to decrease taxable income and/or increase tax attributes for the 2022 tax year through an amended 2022 income tax return.

IRC §179 Current Expense Deduction

- Increase in the maximum amount to $1.29 million and the investment limitation cap to $3.22 million for property placed in service in 2024, with inflation adjustments for post-2023 tax years.

Reporting Threshold Adjustments

- Increase in the reporting threshold for filing Form 1099-NEC and 1099-MISC from $600 to $1,000, applicable to payments made after 2023, with inflation adjustments from 2024.

U.S.–Taiwan Cross-Border Activities and Investments

- The bill creates a new section 894A of the Internal Revenue Code (“IRC”), providing substantial benefits to Taiwan residents (“qualified residents of Taiwan”), similar to those that are provided in the 2016 United States Model Income Tax Convention (“U.S. Model Tax Treaty”). Since the legislation requires full reciprocal benefits, it does not come into full effect until Taiwan provides the same set of benefits to U.S. persons with income subject to tax in Taiwan, similar to the reciprocal operation of a tax treaty.

Child Tax Credit Enhancement

- Increase in the maximum refundable Child Tax Credit from $1,600 to $1,800 in 2023, $1,900 in 2024, and $2,000 in 2025.

- Revision of the refundable portion, calculated on a per-child basis.

Disaster Relief Provisions

- Retroactive exclusion of qualified wildfire relief payments from gross income.

- Introduction of disaster-related personal casualty loss provisions and treatment of disaster relief payments for victims of the East Palestine, Ohio, train derailment.

Low-Income Housing Credit Enhancement

- Enhancing the Low-Income Housing Tax Credit, by restoring the 12.5% LIHTC ceiling for taxable years beginning after December 31, 2022.

What should your business do in the meantime?

R&D/174 Proposed Changes – There likely is no immediate timeline sensitivity for the 174 capitalization requirement currently, unless you are a fiscal year filer or have an upcoming tax provision. In the event you have a return being filed in Q1, we recommend connecting with your tax credits service provider to discuss timeline for a formal analysis and processes. Please note that the anticipated changes are only to U.S. expenditures and therefore any foreign-based expenditures would still require capitalization over 15 years. A formal 174 analysis is recommended to support the research expenditures and to be able to apply the most favorable treatment of either immediately deducting or deferring, in the event of a bill passing and depending on whether the expense is a domestic or international expense.

It is also recommended to assess how the modification of the research and experimentation expense treatment would affect an amended 2022 return and forecasts for the 2023 tax year, especially for businesses that had material domestic research and experimentation expenditures. If all research and experimentation expenditures in the 2022 tax year were foreign, there will be no related change.

Other Business Tax Reliefs and Proposed Modifications – Please connect with your specialty tax service provider to discuss the timeline for your return filings and address forecasts and changes that may be created from these proposed changes. We have summarized a few recommendations and examples:

International

- All U.S. citizens and U.S. resident taxpayers with activities within Taiwan should review their activities in light of these provisions to determine if reduced withholding taxes or minimization of creating a taxable presence is possible. All Taiwan residents with activities in the U.S. should review U.S. activities for similar issues.

Private Client Services

- Assess how the proposed enhancements of the Child Tax Credit and Assistance for Disaster-Impacted Communities affect your personal deductions and 2023 tax liability.

State and Local Taxation

- Evaluate variances in state conformity for the various changes. While some states have rolling conformity and will match changes at the federal level, others have fixed conformity and will not necessarily adopt these changes without further legislation.

Corporate Taxation

- Evaluate the need to file an amended return to “unwind” the 2022 Sec. 174 research and development amortization to deduct those costs in full for 2022. This could provide significant refund opportunities.

- Assess how the removal of depreciation, amortization, and depletion deductions from the calculation of adjusted taxable income for the IRC 163(j) business interest expense limitation affects taxable income and liability.

It is essential to note that despite this bipartisan breakthrough, the absence of an actual bill and the uncertainties surrounding the enactment of these provisions in a divided Congress should remain critical considerations.

Our perspective

As experienced advisors, MGO can help model the best position for you through the 2023 tax year and beyond — potentially saving you significant amounts of money. Our holistic tax advisor and business advisor-first philosophy factors into not only the direct effects of the current legislation (i.e., the proposed tax framework summarized in this article), but also the impact on other areas of your tax returns (e.g., international, transfer pricing, state and local tax) and what potential savings you can obtain by claiming credits and incentives. Please feel free to reach out to any of our MGO professionals below to get the experienced insight that you deserve.

Contact our leaders in the following areas for their specialty or to further address proposals in the tax framework discussed.

- Danielle Bradley, Credits and Incentives

- Matthew Sapowith, Specialty Tax Leader

- Michael Silvio, Credits and Incentives

- Michael Mansour, Corporate Taxation

- Dustin Grizzle, Private Client Services

- John Apuzzo, International Tax Services

- The Internal Revenue Service (IRS) instituted a moratorium on the processing of new Employee Retention Tax Credit (ERTC) claims due to an influx of fraudulent and exaggerated claims — primarily stemming from unscrupulous ERTC mills.

- As of July 31, 2023, the IRS Criminal Investigation division had initiated 252 investigations involving more than $2.8 billion in potentially fraudulent ERTC claims. Fifteen investigations have resulted in federal charges, with six of those resulting in convictions with an average sentence of 21 months.

- Taxpayers who are not certain of their eligibility should consult with a trusted tax professional for a second review and may want to avail themselves of the IRS’s new settlement and/or withdrawal programs.

The IRS recently took a drastic step to impede a wave of ineligible ERTC claims by halting the processing of new refund requests through at least December 31, 2023.

Ineligible ERTC claims have plagued the IRS since Congress enacted the credit in 2020. In fact, the IRS opened its 2023 “Dirty Dozen” list with warnings about common ERTC scams that taxpayers should be wary of. This prominently placed notice — as well as subsequent announcements from the IRS — alerted taxpayers to unscrupulous actors who have been advising employers to claim credits in excess of what they could legitimately qualify for while charging those employers hefty upfront fees or fees contingent on ERTC refunds.

In the wake of a flurry of IRS investigations that identified more than $2.8 billion potentially fraudulent claims, the halt on processing ERTC claims will allow the IRS to further focus their efforts on investigating and ultimately prosecuting fraudulent claims. In the following we’ll detail the impact of the IRS moratorium and provide guidance if you suspect you’ve been exposed to inaccurate or fraudulent ERTC claims.

Background on the ERTC

First established in 2020 by the Coronavirus Aid, Relief, and Economic Security (CARES) Act, the employee retention tax credit was critical — along with Paycheck Protection Program (PPP) — in giving businesses that struggled to navigate the pandemic’s challenges much needed resources to pay employees while the businesses were shut down or facing declining sales.

For most taxpayers, the ERTC was claimed on quarterly payroll tax returns encompassing the period March 13, 2020, through September 30, 2021 (i.e., first quarter of 2020 through the third quarter of 2021). For a small subset of businesses classified as “recovery startup businesses” (as defined below), the ERTC could also be claimed for the fourth quarter of 2021.

Despite the halt in processing by the IRS, eligible taxpayers are still able to claim the credit by filing amended quarterly payroll tax returns. Amended payroll tax returns for 2020 quarters are able to be processed by the IRS as long as they are filed on or before April 15, 2024, while amended payroll tax returns for 2021 quarters are able to be processed as long as they are filed on or before April 15, 2025.

The credit is calculated based on the “qualified wages” of employees. The maximum amount of payroll tax credit that an employer can claim per employee is $26,000.

Qualification Tests

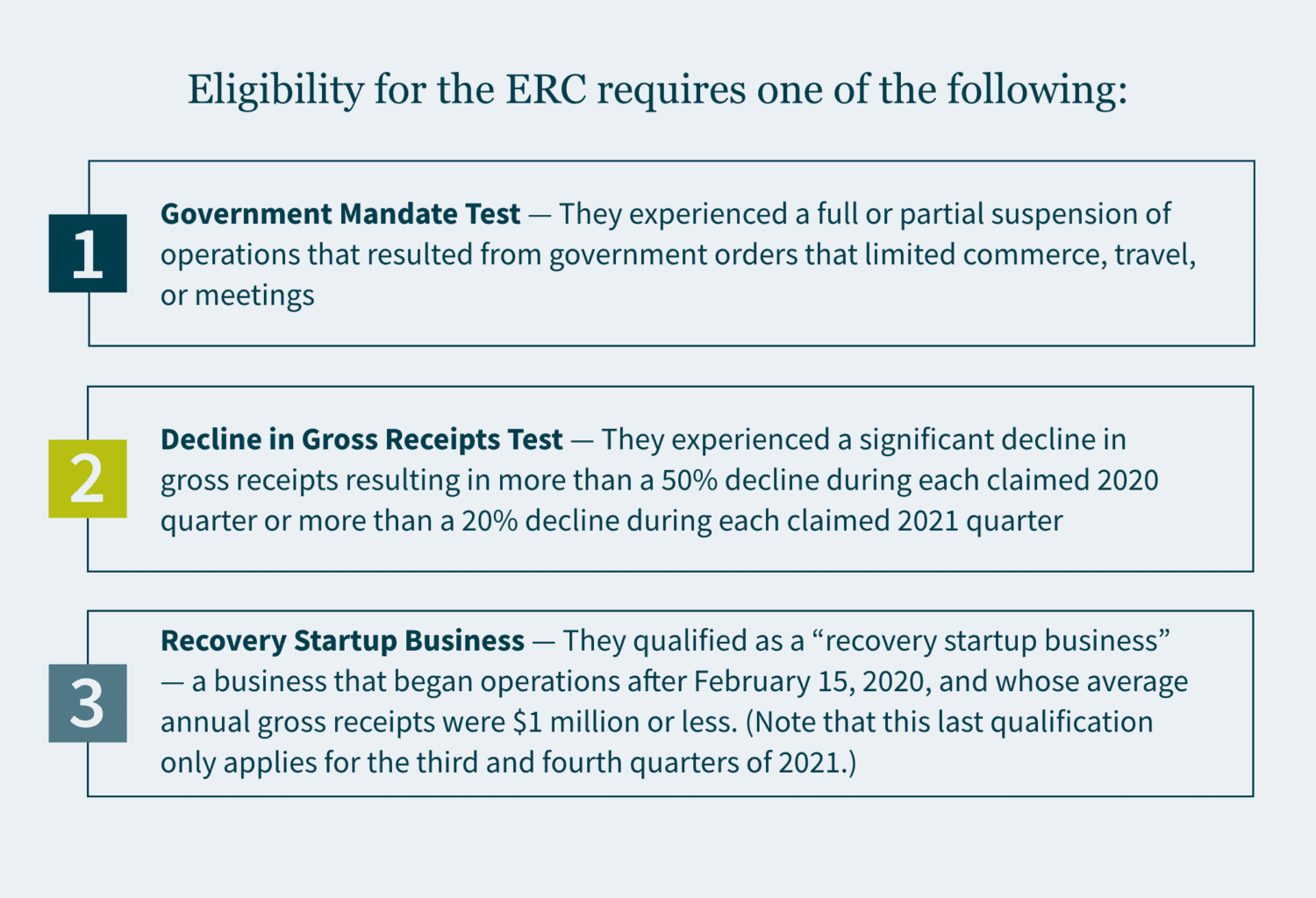

To be eligible for the ERTC, businesses must generally satisfy one of the following criteria for each of the quarters for which they are claiming the credit:

- Government Mandate Test — They experienced a full or partial suspension of operations that resulted from government orders that limited commerce, travel, or meetings.

- Decline in Gross Receipts Test — They experienced a significant decline in gross receipts resulting in more than a 50% decline during each claimed 2020 quarter or more than a 20% decline during each claimed 2021 quarter.

- Recovery Startup Business — They qualified as a “recovery startup business” — a business that began operations after February 15, 2020, and whose average annual gross receipts were $1 million or less. (Note that this last qualification only applies for the third and fourth quarters of 2021.)

The IRS Processing Moratorium

On September 14, 2023, the IRS announced that it would halt the processing of new ERTC claims through at least December 31, 2023. The IRS also stated that it plans to subject its queue of more than 600,000 existing ERTC claims to stricter compliance reviews, increasing the standard processing goal for those claims from 90 days to 180 days — with a potential for a much longer processing time for claims that require further review or audit.

This processing moratorium comes on the heels of a significant influx of claims – many of which the IRS believes are ineligible. The IRS stated that it has received more than 3.6 million ERTC claims over the life of the ERTC program, with about 15% of those claims being received in the 90-day period preceding the processing freeze. This amounts to roughly 50,000 claims still being received a week. To put this in perspective: the IRS has paid out about triple the amount that Congress had originally estimated for the program.

Additionally, as of July 31, 2023, the IRS Criminal Investigation division had initiated 252 investigations involving more than $2.8 billion in potentially fraudulent ERTC claims. Fifteen of the 252 investigations had resulted in federal charges, with six of those resulting in convictions. Four of the six convictions had reached the sentencing phase with an average sentence being 21 months.

The IRS intends on utilizing the moratorium to add more safeguards to the processing of ERTC claims, to protect businesses by decreasing the momentum of the pop-up ERTC mill industry, and to provide several solutions for taxpayers who submitted invalid claims. Those solutions include:

- A claim withdrawal program will be rolled out in Fall 2023 allowing businesses to withdraw ERTC claims that have not been processed or paid, even if those claims are under audit or awaiting audit.

- A claim settlement program rolling out in Fall 2023 that will allow businesses to repay ERTC claims, while also avoiding penalties and future compliance actions. (Note that fraudulent claims may still be subject to criminal referral.)

How to respond to IRS scrutiny of ERTC claims

Given the expected extra scrutiny that businesses can expect to face on their claims, businesses should review ERTC claims that they have made and/or intend to make where there are any doubts regarding the eligibility of those claims:

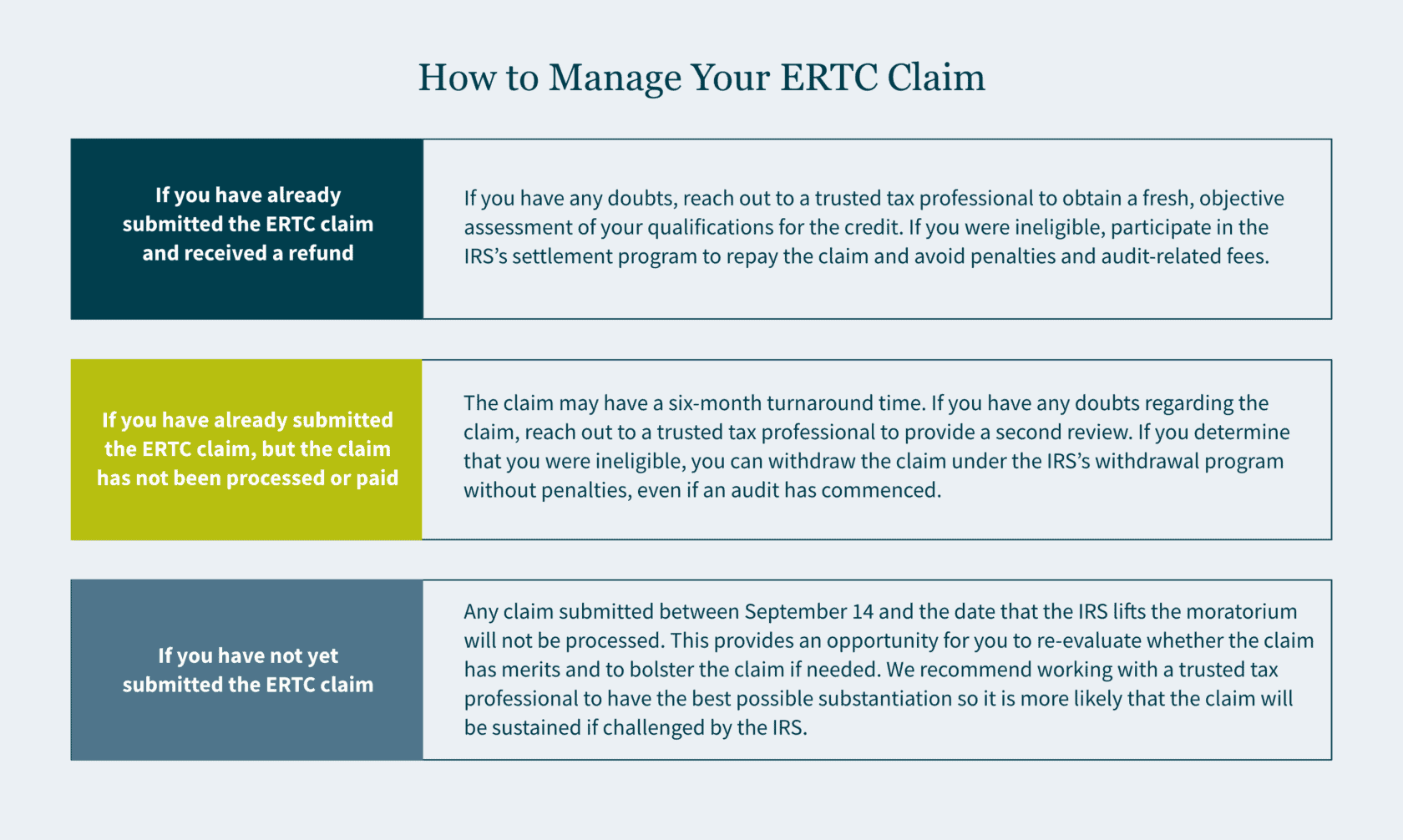

- If you have already submitted the ERTC claim and received a refund: If you have any doubts regarding your eligibility, we recommend reaching out to a trusted tax professional to obtain a fresh, objective assessment of your qualifications for the credit. If you determine that you were ineligible, you can participate in the IRS’s settlement program so that you can repay the claim, avoiding both penalties and audit-related fees.

- If you have already submitted the ERTC claim, but the claim has not been processed or paid: The claim will take longer to process than during the summer — increasing from a three-month turnaround time to a likely six-month turnaround time. If you have any doubts regarding the claim during this period, we recommend reaching out to a trusted tax professional to have a second review of the claim. If you determine that you were ineligible, you can withdraw the claim under the IRS’s withdrawal program without penalties, even if an audit has commenced.

- If you have not yet submitted the ERTC claim: Any claim submitted between September 14 and the date that the IRS lifts the moratorium – currently after December 31, 2023 – will not be processed. This should provide an opportunity for you to re-evaluate whether the claim has merits and to bolster the claim if needed. We recommend working with a trusted tax professional to have the best possible substantiation for your claim so that it is more likely that the claim will be sustained if challenged by the IRS.

How MGO can help

MGO’s ERTC Second Look program is geared towards the types of objective, trustworthy reviews that would benefit you during this time of heightened ERTC claim scrutiny. Our experienced Credits & Incentives team can identify audit red flags, areas that need more substantiation, miscalculations, and incomplete filings. In addition, our Tax Controversy team — in tandem with our Credits & Incentives team — can defend you if any of your ERTC claims are challenged by the IRS, with the ability to represent you during audit, appeals, and tax court. Contact us to learn more.

]]>