- The CHIPS Act provides more than $50 billion to boost U.S. semiconductor manufacturing, including current funding opportunities for commercial fabrication facilities and advanced packaging research and development (R&D).

- The Advanced Manufacturing Tax Credit (Section 48D) offers a 25% credit for qualified investments into semiconductor manufacturing facilities placed in service from 2023-2026.

- Companies seeking CHIPS incentives or 48D credit should understand eligibility requirements, review application process details, and connect with specialized tax credits and incentives professionals to ensure maximum benefit.

~

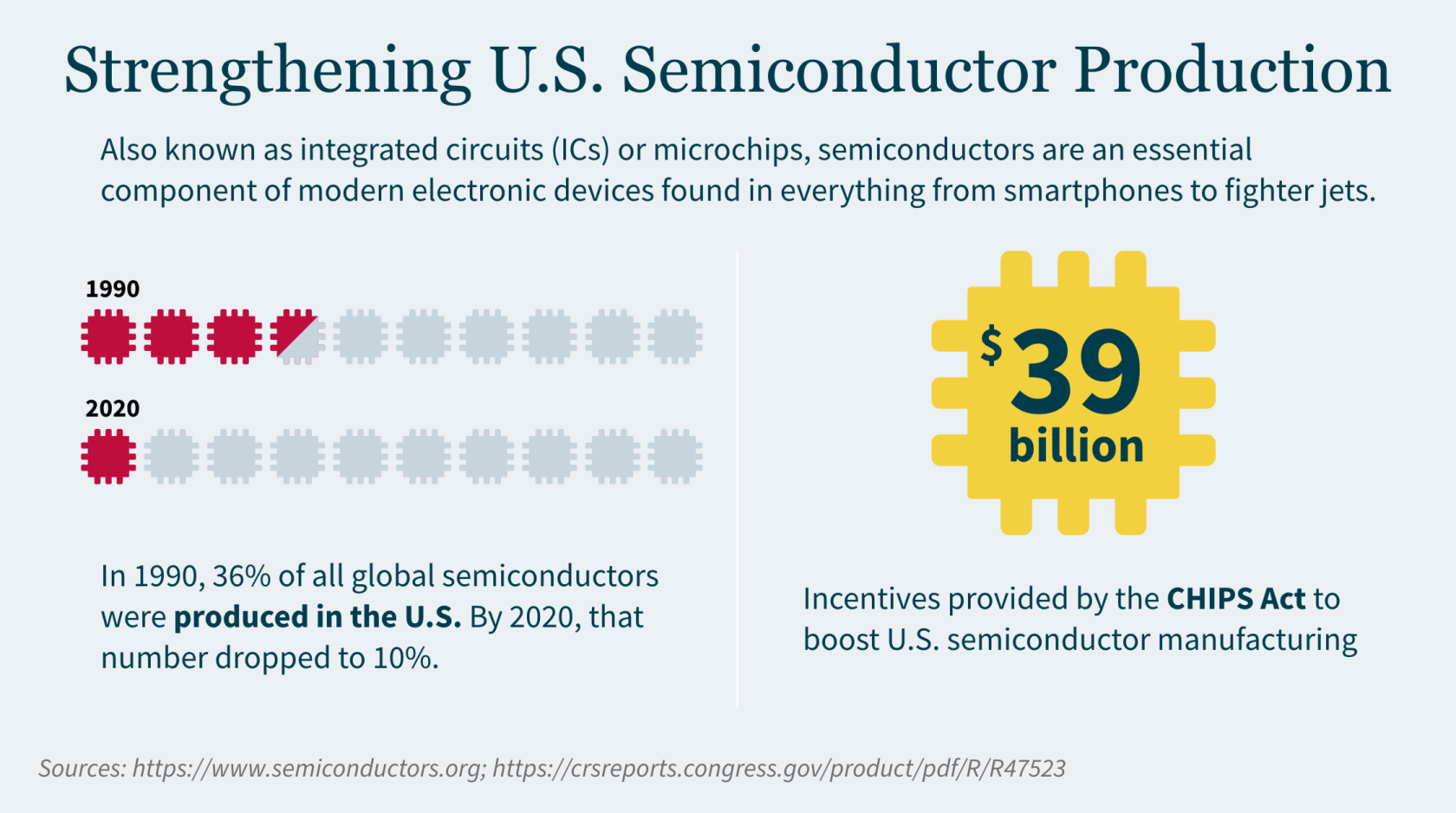

On August 9, 2022, President Joe Biden signed into law the Creating Helpful Incentives to Produce Semiconductors Act of 2022 (commonly referred to as the CHIPS Act). The legislation provides $52.7 billion to increase semiconductor research and development in the United States. The CHIPS Act also established the Advanced Manufacturing Tax Credit (Section 48D), available to entities that manufacture semiconductors.

Recently, the government awarded its first major CHIPS Act grant – providing $1.5 billion to GlobalFoundries, one of the world’s leading semiconductor manufacturers, to expand its semiconductor production in New York and Vermont. That grant is expected to be the first of several announcements in the coming months as the government ramps up CHIPS Act funding.

What is the Purpose of the CHIPS Act?

The intent of CHIPS is simple: the U.S. wants to incentivize domestic companies to manufacture semiconductors. The president called the CHIPS Act a “once-in-a-generation investment in America itself,” as the legislation aims to lower costs and create jobs in the production of these advanced chips.

The COVID-19 pandemic forced the semiconductor industry to operate at a reduced capacity, while lockdowns increased demand for products using semiconductors (computers, tablets, gaming systems, cars, etc.). This created a perfect storm, fueling a shortage of semiconductors. As a result, the U.S. recognized the need to increase its semiconductor output.

However, manufacturing semiconductors is not cheap and requires substantial investments. CHIPS, along with the available tax credit, encourages these investments.

The CHIPS Act includes provisions for:

- $39 billion in incentives to build, expand, or modernize domestic facilities and equipment for semiconductor manufacturing, assembly, testing, advanced packaging, or research and development

- $13.2 billion in R&D and workforce development

- $500 million for international information communications technology security and semiconductor supply chain activities

Understanding the Advanced Manufacturing Tax Credit

With the addition of Section 48D to the Internal Revenue Code, CHIPS offers a new tax credit if your company invests in advanced manufacturing facilities or facilities whose primary purpose is manufacturing semiconductors or semiconductor manufacturing equipment.

Eligible businesses can receive a 25% tax credit of “qualified investments”. You can elect to treat the credit as payment against tax (i.e., direct pay) if you do not have sufficient tax liability to utilize the credit, making this essentially a refundable tax credit.

Eligibility criteria for 48D

To be eligible for 48D, you must have made a qualified investment for any taxable year integral to an “advanced manufacturing facility” for semiconductors placed in service during that year. Qualified properties must be:

- Buildings, structural components, or parts of a building (not including administrative services or other functions unrelated to manufacturing)

- Crucial to the operation of the advanced manufacturing facility

- Constructed or built by the taxpayer

- Qualified for amortization or depreciation

Taxpayers that use facilities and equipment outside the U.S. will not be eligible (similar to other investment credit requirements). Other taxpayers ineligible for the credit include:

- Foreign entities noted as “foreign entities of concern” (i.e., foreign terrorist organizations or organizations included on the Office of Foreign Assets Control list).

- Taxpayers that have engaged in significant transactions involving the material expansion of semiconductor manufacturing capacity in China or another foreign country of concern.

- If a taxpayer enters a transaction in a foreign country of concern within 10 years of claiming the credit, it will be recaptured.

48D timing

The tax credit applies to any property placed in service after December 31, 2022, for which construction begins before January 1, 2027. It does not apply after December 31, 2026, nor can you use the tax credit for constructing a property after this date. If construction on a facility began before January 1, 2023, the credit applies only to the portion of the construction started after August 9, 2022.

Application process

In March 2023, the IRS issued proposed regulations addressing direct payment of Section 48D credit. The proposed regulations also require taxpayers to register through an IRS electronic portal before treating Section 48D as a direct payment on a tax return.

The IRS will issue a registration number for each qualified investment for which your company is claiming a credit, and that number must be included on your tax return.

CHIPS Incentive Opportunities

To access CHIPS incentives, your company must first apply for open funding opportunities. To date, the U.S. Department of Commerce has issued three Notice of Funding Opportunities (NOFOs) through the CHIPS for America program:

- Commercial Fabrication Facilities – Currently accepting applicants

- Small-Scale Supplier Projects – No longer accepting applicants, in second phase of process

- National Advanced Packaging Manufacturing Program (NAPMP) Materials & Substrates – Just announced on February 28, 2024

How to apply for open NOFOs

Application forms and instructions are available on the CHIPS Incentives Program application portal. FAQs, guides, and templates can also be found in the “Resources” section of the portal.

The application process includes the following stages:

- Statement of interest

- Pre-application (optional, but recommended)

- Full application

- Due diligence

- Award preparation and issuance

Statement of interest – To submit a statement of interest, applicants need to register for an account on the CHIPS Incentives Portal. A statement of interest must be submitted at least 21 days prior to submitting a pre-application or full application.

Pre-application – The optional pre-application provides an opportunity to ensure your projects are consistent with program requirements. During this stage, you will receive feedback on strengths and weaknesses of your proposal and recommendations for improvement.

Full application – Both pre-applications and full applications are accepted on a rolling basis.

Due diligence – Your application will undergo review to ensure alignment with evaluation criteria specified in the Notice of Funding Opportunity (NOFO), with the possibility of requests for additional information.

Award preparation and issuance – Before receiving an award, you must have an active registration in the System for Award Management (SAM). It’s a good idea to begin the registration process for SAM.gov early as it may take anywhere from two weeks to six months (due to information verification requirements). Check out SAM.gov’s Entity Registration Checklist.

Maximizing Your Semiconductor Manufacturing Tax Credits and Incentives

Navigating CHIPS’s nuances can be challenging – especially when claiming the available tax credit and determining how it is refundable. Furthermore, companies seeking to increase their semiconductor manufacturing capacity in the U.S. should also assess application and opportunity for federal and state R&D tax credits and incentives.

With more than 30 years of experience, our dedicated Tax Credits and Incentives team can help you maximize your credit benefits, develop the appropriate documentation methodology, assist in calculating and claiming credits, and defend your claims. Our full-service firm, led by experienced CPAs and attorneys, provides a holistic approach to examining your organization and determining how to best reach your goals.

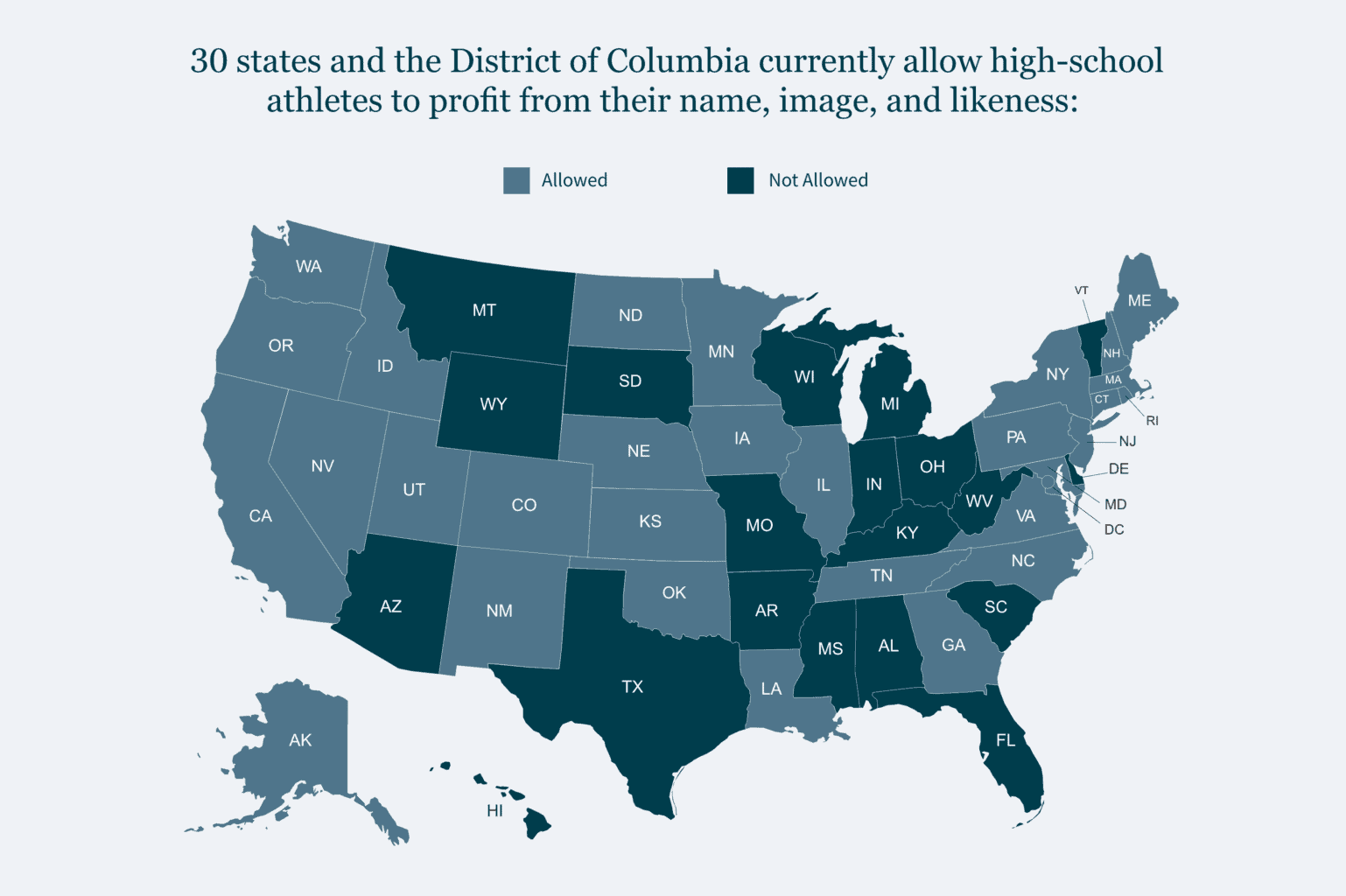

]]>- Name, image, and likeness (NIL) deals offer athletes exciting opportunities, but also potential pitfalls if not approached strategically.

- Athletes should educate themselves on taxes, carefully review contracts, and budget with long-term security in mind.

- With guidance on financial obligations, agreements, and smart money management, athletes can maximize NIL benefits while safeguarding their futures.

~

You are a talented young athlete with a growing public profile. You’ve just been offered a Name, Image, and Likeness (NIL) deal, an opportunity that can put some extra money in your pocket or even, in some cases, make a more profound impact on your financial life. It’s an exhilarating time, but it’s also crucial to approach this new chapter with the right knowledge and mindset.

Whether you’re a college or high-school athlete, or the trusted advisor to a young athlete, here are the three most critical actions you should take to avoid common financial pitfalls associated with NIL deals.

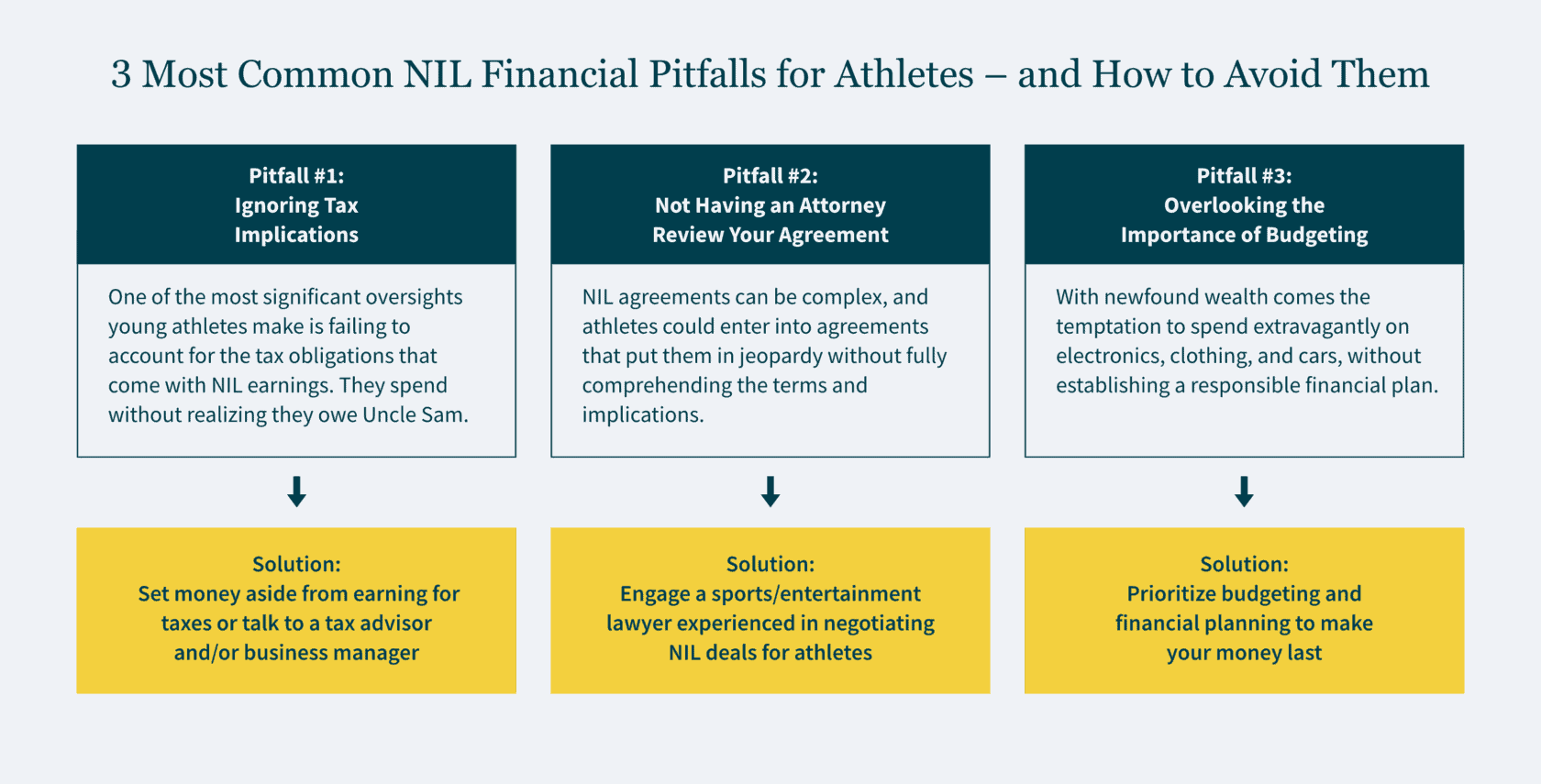

1. Recognize Your Tax Obligation

One of the first hurdles you’ll encounter in the world of NIL deals is taxes. It’s essential to understand that the money you earn from these deals is subject to taxation. Many young athletes overlook this, often because they’ve never had to deal with taxes before.

To avoid potential financial trouble down the road, consider these steps:

- Educate Yourself: Young athletes receiving payments from NIL deals are responsible for paying taxes on that income just like professional athletes. Take the time to learn about taxes, especially how they apply to your earnings. Understanding the basics of taxation will empower you to make informed decisions.

- Consult a Tax Professional: Before signing any NIL agreement, consult with an experienced accountant, tax advisor, or business manager. They can help you calculate your tax obligations, identify potential deductions, and develop a tax strategy tailored to your situation. Along with ensuring any federal, state, and local taxes you owe are paid on time (avoiding penalties), a tax professional can also help you navigate more complex situations – such as earning income across multiple states.

- Practice Smart Spending: Resist the urge to splurge on electronics, clothes, or cars as soon as the money starts rolling in. Create a budget that considers your future tax payments, living expenses, and financial goals. Staying disciplined with your spending is key to long-term financial success.

2. Execute Agreements Cautiously

Navigating NIL deals can be tricky. There are various state laws and school policies to consider, along with a number of legal “gotchas” to avoid. Here’s how you can safeguard your interests:

- Seek Legal Advice: Before signing any NIL agreement, engage a lawyer with experience negotiating NIL and brand endorsements for athletes. An attorney with expertise in sports contracts can help you navigate the important terms in an NIL deal, such as money, exclusivity, length of the agreement, how the brand can use your name, image, and likeness, and an athlete’s delivery requirements. An experienced attorney will help you spot potential pitfalls and ensure the agreement aligns with your long-term goals.

- Beware of “Standard” or Simplistic Agreements: When someone refers to a contract as “standard” or provides an overly simplified agreement, that should throw up a red flag. All it takes is the slightest language in your agreement to give a company unfettered rights to use your name, likeness and image in ways you never intended.

- Follow Regulations: An experienced advisor will help you navigate specific laws and policies set by your state, school, and the NCAA regarding NIL deals. For example, you cannot share photos or videos in your team uniform with logos from other brands without first getting permission from your school or the brands.

3. Budget Wisely for the Long Term

While newfound wealth can be exhilarating, it’s crucial to manage your finances wisely:

- Prioritize Needs Over Wants: When it comes to spending, prioritize essential needs over extravagant wants. Understand this financial windfall may be a one-time occurrence, so focus on building a secure future rather than indulging in immediate gratification.

- Future-Proof Your Earnings: Instead of assuming this is a continuous stream of income, treat each deal as if it were your last. Create a budget that accounts for potential future earnings and uncertainties, ensuring you’re prepared for any scenario.

- Explore Tax Mitigation Strategies: Consider tax mitigation strategies, such as retirement planning and deferral opportunities, to minimize your tax burden. Consulting a financial advisor can help you explore these options.

Make the Most of Your NIL Opportunities

The legalization of NIL in college and high school sports represents an exciting shift for young athletes. It can offer game-changing money, enabling you to take care of your financial needs, along with building your brand for future growth. But with great success also comes great responsibility. Even professional athletes who’ve reached the highest pinnacles of their respective sports can end up without the financial resources they need if they don’t plan ahead.

The good news is by recognizing the potential pitfalls and seeking professional guidance early in your NIL journey, you can better position yourself for long-term financial success. Remember, it’s not just about profiting from your name, image, and likeness today, but also securing your financial future for tomorrow.

How We Can Help:

Our Entertainment, Sports, and Media practice understands the unique challenges athletes face at all stages of their financial journey. Whether you need assistance with tax planning, contract negotiations, or financial strategy, we’re here to guide you toward a successful future in the world of sports and NIL deals.

This article was co-authored by Leron E. Rogers, Partner at Fox Rothschild LLP.

]]>- The Internal Revenue Service (IRS) instituted a moratorium on the processing of new Employee Retention Tax Credit (ERTC) claims due to an influx of fraudulent and exaggerated claims — primarily stemming from unscrupulous ERTC mills.

- As of July 31, 2023, the IRS Criminal Investigation division had initiated 252 investigations involving more than $2.8 billion in potentially fraudulent ERTC claims. Fifteen investigations have resulted in federal charges, with six of those resulting in convictions with an average sentence of 21 months.

- Taxpayers who are not certain of their eligibility should consult with a trusted tax professional for a second review and may want to avail themselves of the IRS’s new settlement and/or withdrawal programs.

The IRS recently took a drastic step to impede a wave of ineligible ERTC claims by halting the processing of new refund requests through at least December 31, 2023.

Ineligible ERTC claims have plagued the IRS since Congress enacted the credit in 2020. In fact, the IRS opened its 2023 “Dirty Dozen” list with warnings about common ERTC scams that taxpayers should be wary of. This prominently placed notice — as well as subsequent announcements from the IRS — alerted taxpayers to unscrupulous actors who have been advising employers to claim credits in excess of what they could legitimately qualify for while charging those employers hefty upfront fees or fees contingent on ERTC refunds.

In the wake of a flurry of IRS investigations that identified more than $2.8 billion potentially fraudulent claims, the halt on processing ERTC claims will allow the IRS to further focus their efforts on investigating and ultimately prosecuting fraudulent claims. In the following we’ll detail the impact of the IRS moratorium and provide guidance if you suspect you’ve been exposed to inaccurate or fraudulent ERTC claims.

Background on the ERTC

First established in 2020 by the Coronavirus Aid, Relief, and Economic Security (CARES) Act, the employee retention tax credit was critical — along with Paycheck Protection Program (PPP) — in giving businesses that struggled to navigate the pandemic’s challenges much needed resources to pay employees while the businesses were shut down or facing declining sales.

For most taxpayers, the ERTC was claimed on quarterly payroll tax returns encompassing the period March 13, 2020, through September 30, 2021 (i.e., first quarter of 2020 through the third quarter of 2021). For a small subset of businesses classified as “recovery startup businesses” (as defined below), the ERTC could also be claimed for the fourth quarter of 2021.

Despite the halt in processing by the IRS, eligible taxpayers are still able to claim the credit by filing amended quarterly payroll tax returns. Amended payroll tax returns for 2020 quarters are able to be processed by the IRS as long as they are filed on or before April 15, 2024, while amended payroll tax returns for 2021 quarters are able to be processed as long as they are filed on or before April 15, 2025.

The credit is calculated based on the “qualified wages” of employees. The maximum amount of payroll tax credit that an employer can claim per employee is $26,000.

Qualification Tests

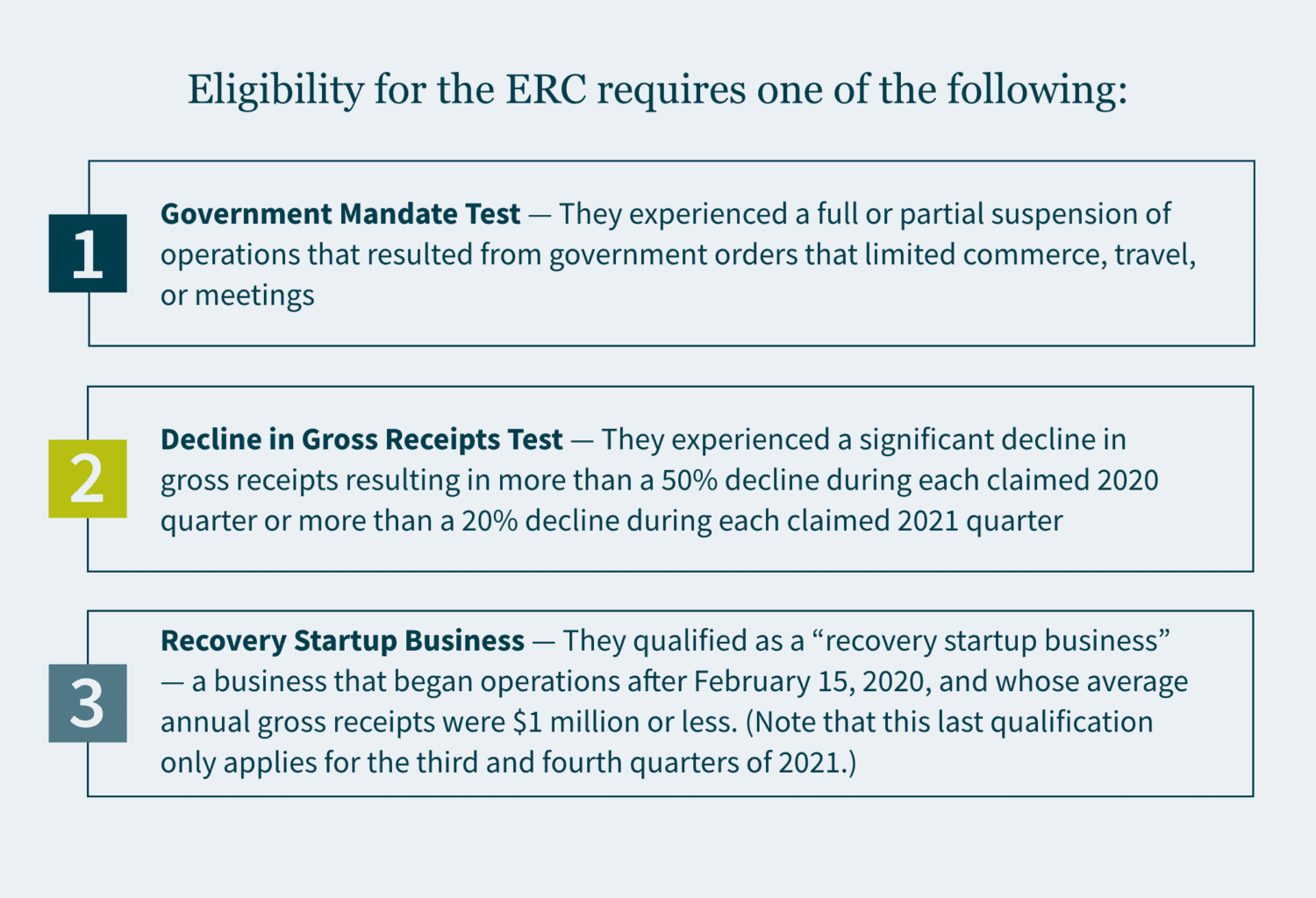

To be eligible for the ERTC, businesses must generally satisfy one of the following criteria for each of the quarters for which they are claiming the credit:

- Government Mandate Test — They experienced a full or partial suspension of operations that resulted from government orders that limited commerce, travel, or meetings.

- Decline in Gross Receipts Test — They experienced a significant decline in gross receipts resulting in more than a 50% decline during each claimed 2020 quarter or more than a 20% decline during each claimed 2021 quarter.

- Recovery Startup Business — They qualified as a “recovery startup business” — a business that began operations after February 15, 2020, and whose average annual gross receipts were $1 million or less. (Note that this last qualification only applies for the third and fourth quarters of 2021.)

The IRS Processing Moratorium

On September 14, 2023, the IRS announced that it would halt the processing of new ERTC claims through at least December 31, 2023. The IRS also stated that it plans to subject its queue of more than 600,000 existing ERTC claims to stricter compliance reviews, increasing the standard processing goal for those claims from 90 days to 180 days — with a potential for a much longer processing time for claims that require further review or audit.

This processing moratorium comes on the heels of a significant influx of claims – many of which the IRS believes are ineligible. The IRS stated that it has received more than 3.6 million ERTC claims over the life of the ERTC program, with about 15% of those claims being received in the 90-day period preceding the processing freeze. This amounts to roughly 50,000 claims still being received a week. To put this in perspective: the IRS has paid out about triple the amount that Congress had originally estimated for the program.

Additionally, as of July 31, 2023, the IRS Criminal Investigation division had initiated 252 investigations involving more than $2.8 billion in potentially fraudulent ERTC claims. Fifteen of the 252 investigations had resulted in federal charges, with six of those resulting in convictions. Four of the six convictions had reached the sentencing phase with an average sentence being 21 months.

The IRS intends on utilizing the moratorium to add more safeguards to the processing of ERTC claims, to protect businesses by decreasing the momentum of the pop-up ERTC mill industry, and to provide several solutions for taxpayers who submitted invalid claims. Those solutions include:

- A claim withdrawal program will be rolled out in Fall 2023 allowing businesses to withdraw ERTC claims that have not been processed or paid, even if those claims are under audit or awaiting audit.

- A claim settlement program rolling out in Fall 2023 that will allow businesses to repay ERTC claims, while also avoiding penalties and future compliance actions. (Note that fraudulent claims may still be subject to criminal referral.)

How to respond to IRS scrutiny of ERTC claims

Given the expected extra scrutiny that businesses can expect to face on their claims, businesses should review ERTC claims that they have made and/or intend to make where there are any doubts regarding the eligibility of those claims:

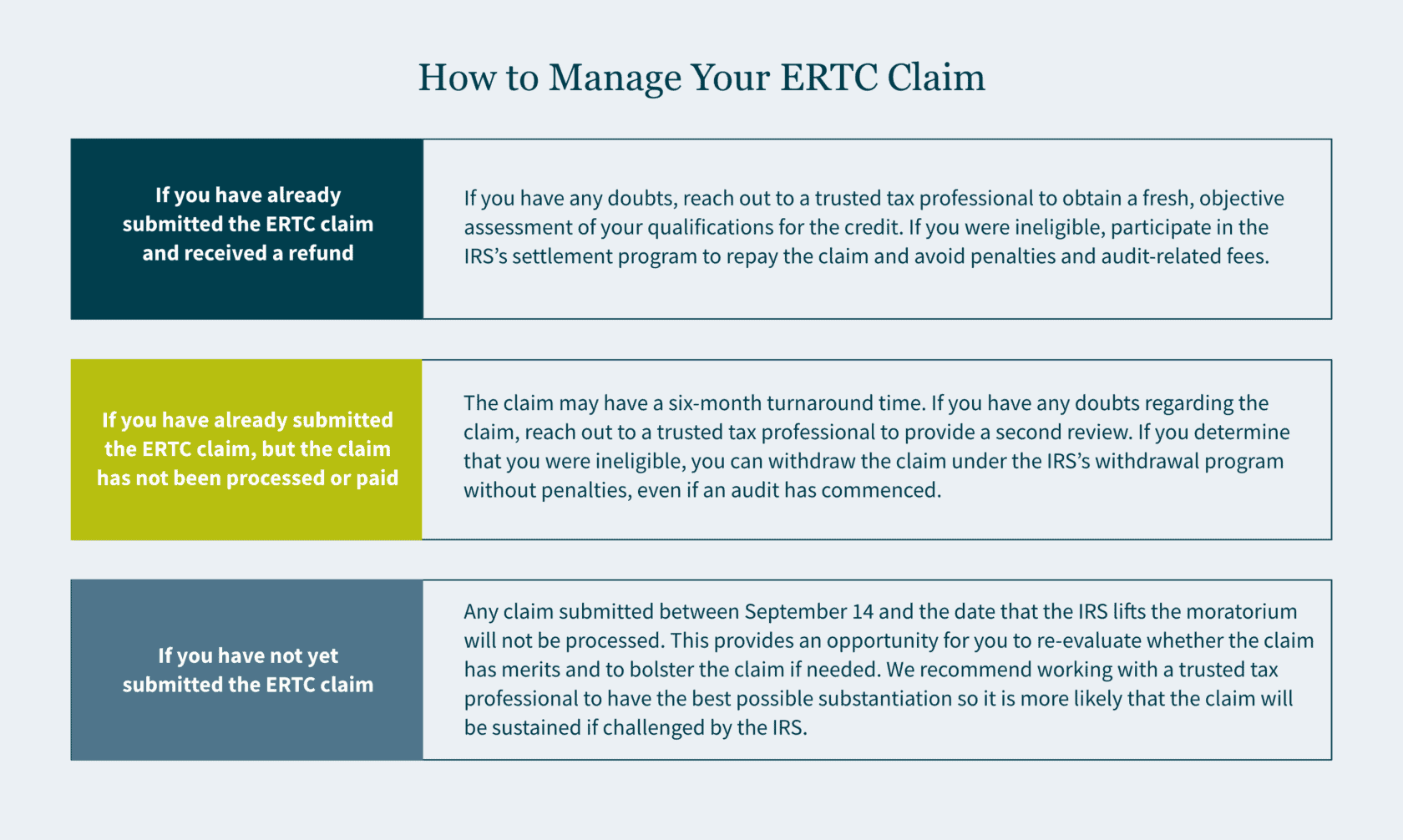

- If you have already submitted the ERTC claim and received a refund: If you have any doubts regarding your eligibility, we recommend reaching out to a trusted tax professional to obtain a fresh, objective assessment of your qualifications for the credit. If you determine that you were ineligible, you can participate in the IRS’s settlement program so that you can repay the claim, avoiding both penalties and audit-related fees.

- If you have already submitted the ERTC claim, but the claim has not been processed or paid: The claim will take longer to process than during the summer — increasing from a three-month turnaround time to a likely six-month turnaround time. If you have any doubts regarding the claim during this period, we recommend reaching out to a trusted tax professional to have a second review of the claim. If you determine that you were ineligible, you can withdraw the claim under the IRS’s withdrawal program without penalties, even if an audit has commenced.

- If you have not yet submitted the ERTC claim: Any claim submitted between September 14 and the date that the IRS lifts the moratorium – currently after December 31, 2023 – will not be processed. This should provide an opportunity for you to re-evaluate whether the claim has merits and to bolster the claim if needed. We recommend working with a trusted tax professional to have the best possible substantiation for your claim so that it is more likely that the claim will be sustained if challenged by the IRS.

How MGO can help

MGO’s ERTC Second Look program is geared towards the types of objective, trustworthy reviews that would benefit you during this time of heightened ERTC claim scrutiny. Our experienced Credits & Incentives team can identify audit red flags, areas that need more substantiation, miscalculations, and incomplete filings. In addition, our Tax Controversy team — in tandem with our Credits & Incentives team — can defend you if any of your ERTC claims are challenged by the IRS, with the ability to represent you during audit, appeals, and tax court. Contact us to learn more.

]]>- California now has a new tax credit called the High-Road Cannabis Tax Credit (HRCTC) available for eligible cannabis retailers and microbusinesses.

- The credit is available for tax years starting after January 1, 2023, through December 31, 2027, and can be applied against current year (and future) income taxes.

- To claim it, you must make a “tentative credit reservation.”

- Expenditures that qualify include wages for full-time employees; safety-related equipment, training, and services; and workforce development and safety.

While the cannabis industry in California has been struggling on many levels, tax credit relief has come in the form of excise tax changes for distributors and has now arrived for retailers. The High-Road Cannabis Tax Credit is a new tax credit from the California Franchise Tax Board (FTB) available for cannabis retailers or microbusinesses for taxable years beginning January 1, 2023, through December 31, 2027. In order to capitalize on this opportunity, eligible calendar-year taxpayers must make a tentative credit reservation during the month of July to claim the credit on their 2023 CA income tax return.

Who qualifies for the HRCTC

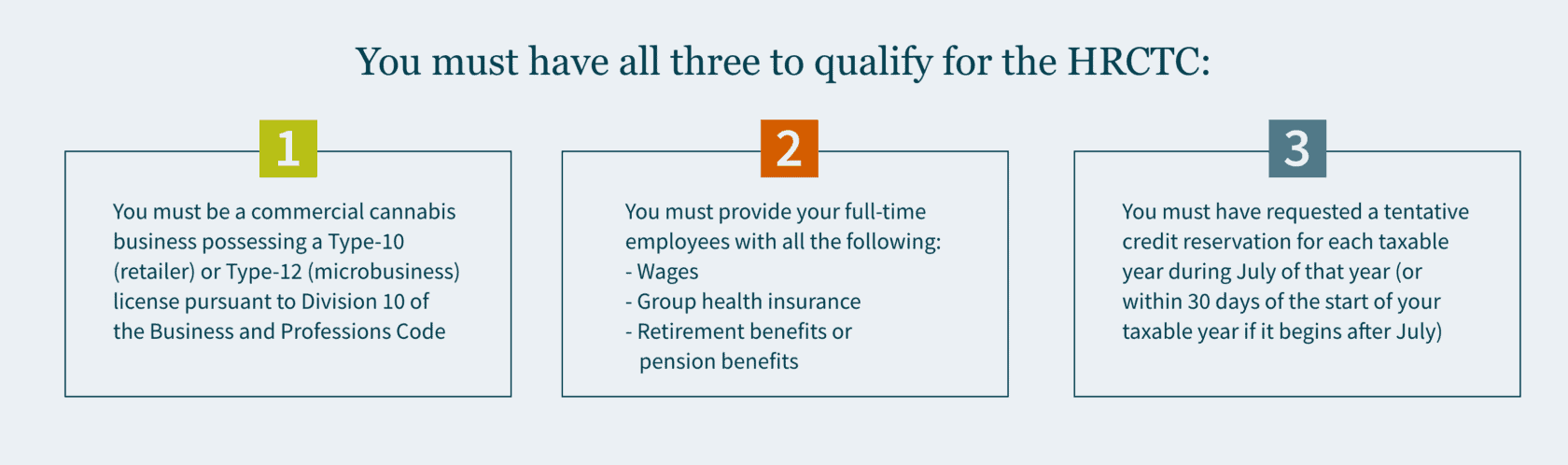

To be eligible, you would need to meet three basic requirements.

Which expenditures qualify for the HRCTC

There are several types of expenditures eligible for the credit with specific parameters that you would need to meet to qualify for them. Qualified expenditures are amounts that you have paid or incurred for any of the following expenses.

Wages for full-time employees

Not every employee has to meet these requirements — but for those that do, their wages count as a qualified expenditure. First, full-time employees must be paid for no less than an average of 35 hours per week — or they must be a salaried employee paid compensation for full-time employment.

In addition, full-time employees must be paid no less than 150% ($23.25) but no more than 350% ($54.25) of the state minimum wage. To meet the 150% minimum wage requirement, you may include the following employee benefits in qualified wages: group health insurance, childcare support, employer contributions to employer-provided retirement plans, or contributions to employer-provided pension benefits. But if you pay employees wages that surpass more than 350% of the state minimum wage, those wages are not considered a qualified expenditure.

Safety-related equipment, training, and services

Expenditures related to safety, training, and providing services can also qualify if they meet the following criteria:

- Equipment primarily used by the employees of the cannabis licensee to ensure personal and occupational safety, or the safety of the business’s customers.

- Training for nonmanagement employees on workplace hazards. (This includes safety audits, security guards, security cameras, and fire risk mitigation.)

Workforce development and safety

Qualified training for your employees includes:

- Joint labor management training programs

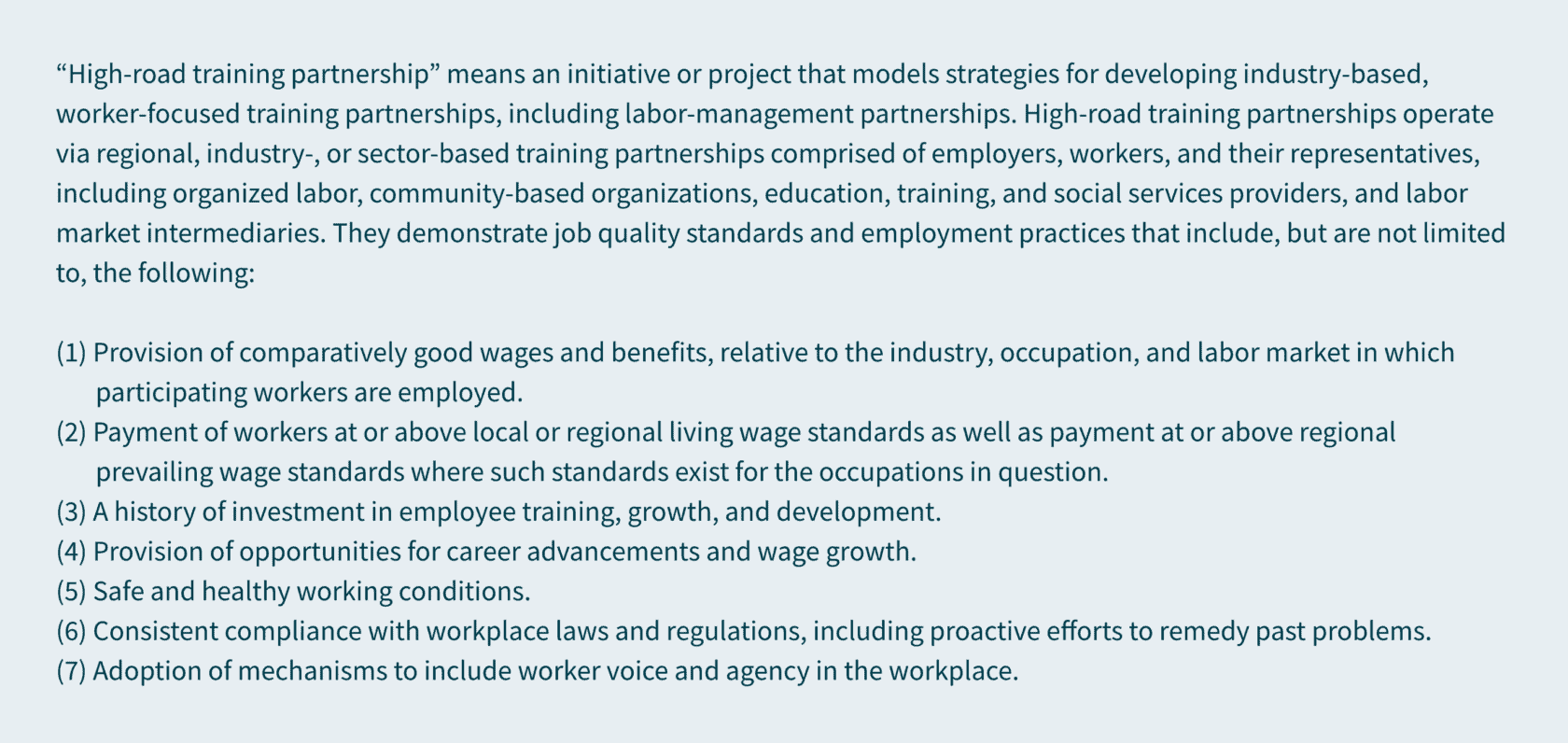

- Membership in a joint apprenticeship training committee registered by the Division of Apprentice Standards, and a state-recognized “high-road training partnership” (as defined in Section 14005 of the Unemployment Insurance Code).

Available credit

The amount of available credit is equal to 25% of qualified expenditures. The aggregate credit that can be claimed by each taxpayer (as determined on a combined reporting basis) is a maximum of $250,000 per year. Any unused credit can be carried over to the following eight taxable years. Availability is limited as the total cumulative amount of HRCTC available to all taxpayers is $20 million.

To claim the HRCTC on your California tax return, you must reduce any deduction or credit otherwise allowed for any qualified expenditure by the amount of the HRCTC allowed.

How do I make a tentative credit reservation — and when?

You must make a tentative credit reservation (TCR) with the FTB to claim the credit. This reservation must be made online and once you’ve done so, you’ll receive an immediate confirmation. FTB currently reports that the system will be up and running by July 1, 2023, but you can start preparing now.

How we can help

The HRCTC is a valuable tax credit opportunity for any commercial cannabis business operating in California. Determining if you qualify and calculating how much you can save could be complex. Our extensive experience in cannabis, cannabis tax, and state and local tax enables us to help you take advantage of this tax credit so you can stay focused on thriving in this ever-growing, culture-shaping industry.

Reach out to MGO’s State and Local Tax team to find out whether you qualify for this tax credit opportunity and determine how much you could potentially save.

]]>

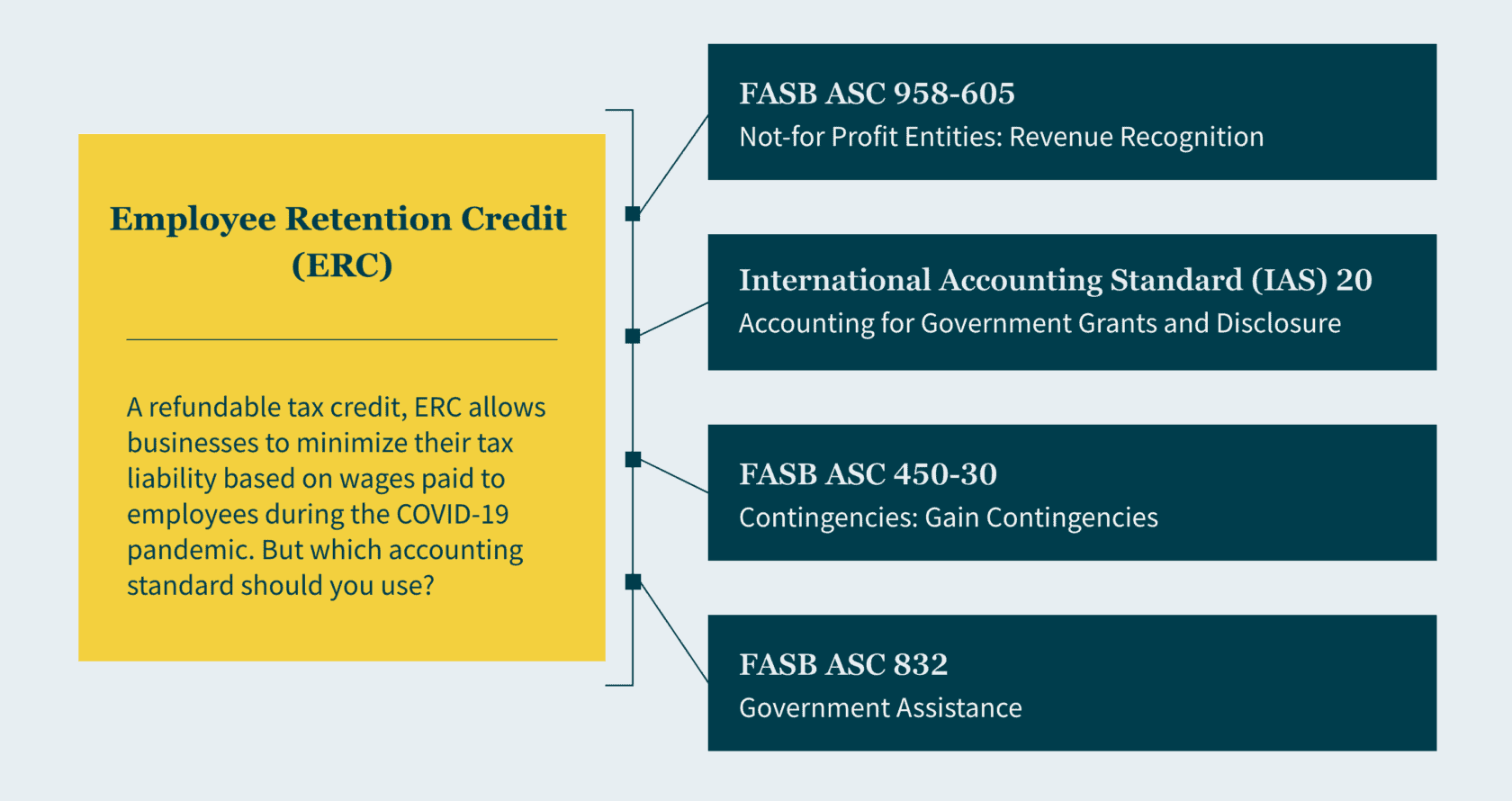

- There is still uncertainty about how to account for the refundable Employee Retention Credit in your books, because you can’t account for it the same way you can account for the Paycheck Protection Program loan.

- The standards you can choose from are FASB ASC 958-605, International Accounting Standard (IAS) 20, FASB ASC 450-30, and FASB ASC 832.

- Depending on the standard you choose, you might have to consider the timing of recognition, the presentation of a grant income line, and financial ratios.

The Paycheck Protection Program (PPP) and the Employee Retention Credit (ERC) were powerful economic stimulus programs instituted during the COVID-19 pandemic to provide financial relief to struggling businesses. Both programs were the first initiatives of their kind, and as a result, there remains some uncertainty about what standards apply when accounting for them in your financial statements and records.

If you’re wondering how to distinguish the two, as well as determine the standard you should be utilizing, Angel Naval, a leader in our Client Accounting Solutions practice, breaks it down.

The PPP versus the ERC

Created to aid businesses facing financial challenges through the pandemic, there are several key differences between the PPP and the ERC.

The PPP is a loan and was created for small businesses with less than 500 employees in mind, giving them the funds needed to cover payroll and other eligible expenses. This includes hiring back employees who were laid off and covering applicable overhead. The loans are forgiven if the proper criteria are met (I.e., maintaining payroll and keeping consistent employee numbers).

A subset of the PPP loan, the ERC is a refundable tax credit that allows businesses to reduce their tax liability based on the qualified wages they’ve paid to their employees during the pandemic. It was created for businesses of all sizes to capitalize on in order to avoid layoffs. They can claim up to $5,000 per employee in 2020 and $7,000 per employee per quarter in 2021.

Determining the appropriate accounting standard for ERCs

If you took advantage of the ERC, currently, there is no straightforward way of accounting for it. Put simply, the ERC is a gray area because it’s so new, and there isn’t a straightforward way of accounting for it. Plus, ERCs are payroll credits, not income tax credits — and while FASB has extensive guidance for accounting for income taxes in ASC 740, it doesn’t for payroll taxes. Even the American Institute of Certified Public Accountants (AICPA) has suggested different standards, so it’s up to you to apply your best judgement based on the facts and circumstances of your business. Some things to consider:

- The timing of recognition,

- The financial ratios important to you, and

- Whether you want to present a grant income line.

For income statement presentation, according to AICPA’s December 2022 report, more public entities are crediting the associated expense rather than recognizing the amounts on a separate line item.

For example, you may think you can account for the ERC the same way you can for the PPP, but you can’t. As we differentiated above, the PPP is a loan and the ERC is a payroll credit, therefore the PPP is subject to debt and liability standards and the ERC is not. While the PPP did come first, those companies that have paid payroll taxes but still qualified for the ERC are still able to retroactively claim the credit.

For prospective applications, for-profit entities can adhere to guidance in one of the following.

FASB ASC 958-605

If you’re applying the revenue recognition model under ASC 958-605, ERCs are treated as conditional contributions. In this case, companies must have met the program’s eligibility conditions to record revenue (and no amounts can be recorded until all criteria are evaluated and “substantially” met according to regulations). Given the conditions are met, a refund receivable and income should be recognized in the period the entity determines the conditions have been substantially met. This standard requires that gross revenue be recorded, and it doesn’t permit any netting of revenue against related expenses.

Some barriers to meeting ASC 958-605’s requirements include the eligibility requirements, like meeting the rules for a decline in gross receipts as well as incurring qualifying expenses (i.e., payroll costs). To file for the ERC, you’ll need to decide whether preparing the related ERC form and filing it with the government presents a barrier you’ll need to overcome. Note administrative and other small stipulations do not represent a barrier.

IAS 20

If you’re applying IAS 20, you can’t recognize the ERC until the “reasonable assurance” threshold is met in correlation with ERC’s conditions and receiving the credit. In this case, “reasonable assurance” translates to “probable” under GAAP standards and is easier to satisfy than “substantially met” in Subtopic 958-605. Once you’ve provided reasonable assurance that conditions will be met, the earnings impact of the government grants is recorded over the periods in which you recognize as expenses the related costs that the grants are intended to cover. So, you’ll need to estimate the amount of the credit you expect to keep.

IAS 20 allows you to record and present either the gross amount as other income or net the credit against other related payroll expenses. For every quarter that a company meets the recognition criteria, it records a receivable and either other income or net expense.

FASB ASC 450-30

If you’re interested in applying FASB ASC 450-30, please note amounts related to the ERC wouldn’t be recognized under this model until all uncertainties regarding the disposition of the credit are resolved — and there’s less detail on the disclosure, measurement, and recognition requirements as compared to the other standard models. For this reason, the AICPA doesn’t believe this model to be a preferred accounting policy for the ERC.

FASB ASC 832

If you’re applying this model, you must disclose several specifics about transactions with a government within its scope. These entail the nature of the transactions, which includes a description of the transactions as well as the form in which it has been received, whether it’s cash or other assets. You must also detail the accounting policies you used to account for the transactions. Any line items on the balance sheet and income statement that are affected by the transactions must be accounted for too — plus, the amounts applicable to each financial statement line item in the current reporting period.

How MGO can help

While there are clear accounting standards for the PPP, there is still some uncertainty surrounding the ERC. Depending on the standard you choose, you may have to consider the timing of recognition, financial ratios, and whether to present a grant income line. Therefore, businesses need to apply their best judgment based on the facts and circumstances of their business when accounting for ERCs. Our Client Accounting Solutions team has extensive experience helping clients navigate complex tax regulations post-pandemic. Contact us to learn more about which standard you should be using for federal relief programs.

About the author

Angel Naval oversees our West Coast Financial Advisory Services practice and provides value-added guidance for your corporate finance, financial planning, and business process needs.

]]>What is the policy now? Well, the Tax Cuts and Jobs Act (TCJA) of 2017 changed the treatment of R&E costs so that taxpayers must capitalize all R&E costs incurred after December 31, 2021, and amortize them over either a five-year period (domestic costs) or a 15-year period (foreign costs). Previously, taxpayers could either (1) immediately deduct R&E expenditures, or (2) elect to amortize those costs over a period of five or more years, which gave the taxpayer the ability to choose the option that would be the most beneficial for them.

While it is still possible for the legislative process to postpone or repeal mandatory capitalization of Section 174 costs (including retroactively applying any changes to the 2022 tax year), such legislation would need to have bipartisan support due to the currently divided Congress.

In this article, we review what it would mean for your business if the much-anticipated revisions to Section 174 do not occur, and what kind of planning you should do to prepare on the front end. A number of these recommendations will be further refined once additional IRS guidance is provided.

Background on 174 R&E expenditures

R&E expenses for income tax purposes are defined under Section 174 and its regulations. In Treasury Regulation Section 1.174-2(a), R&E expenditures are described as expenditures incurred by the taxpayer in connection with the taxpayer’s trade or business in the experimental or laboratory sense. Section 174(c)(3) – added by the TCJA – also notes that any amount paid or incurred in connection with the development of any software shall also be an R&E expenditure subject to capitalization. Generally, when determining R&E expenses, not only are direct costs of R&E factored in, but also the indirect costs incident to the development or improvement of a product.

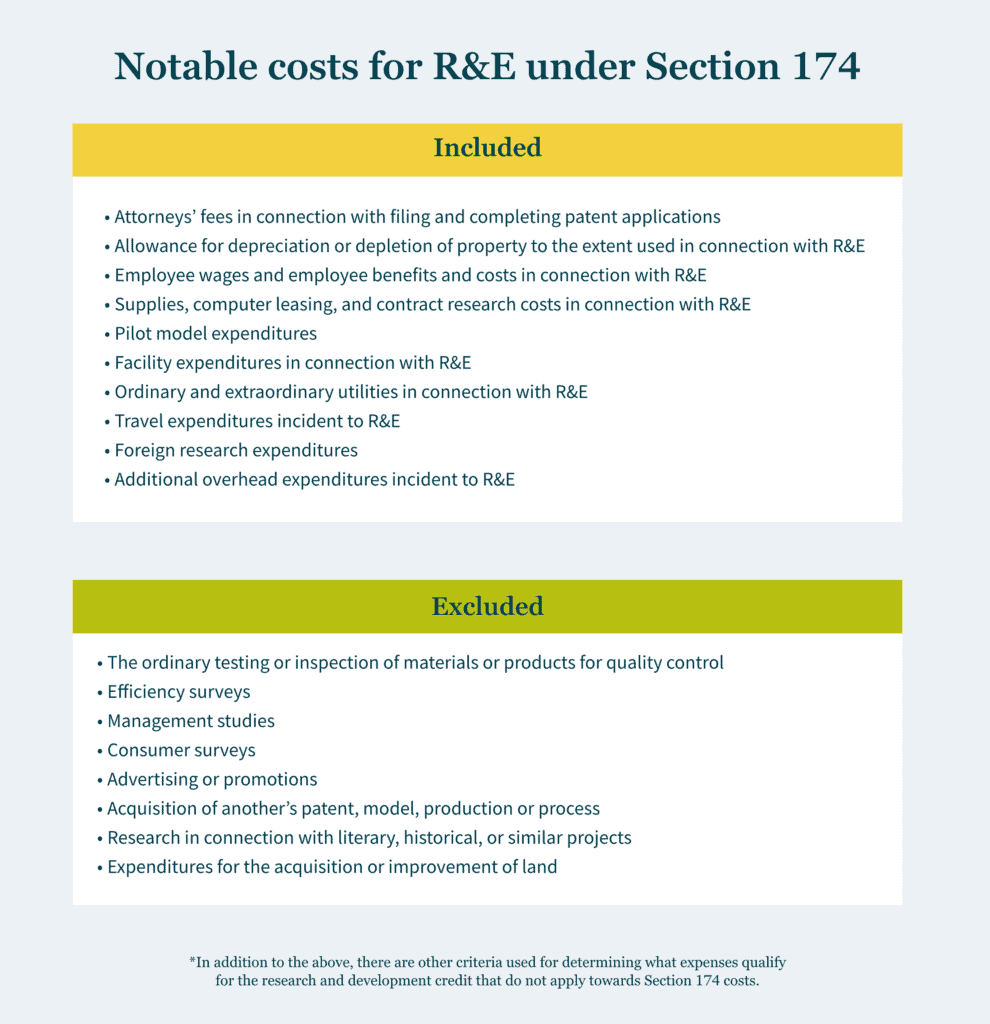

Common expenses included in R&E costs under Section 174 are the following. Many of these expenses are considered for Section 174 specifically and are not qualified research expenses for purposes of the R&D credit.

- Attorneys’ fees in connection with filing and completing patent applications.

- Allowance for depreciation or depletion of property to the extent used in connection with R&E.

- Employee wages and employee benefits and costs in connection with R&E.

- Supplies, computer leasing, and contract research costs in connection with R&E.

- Pilot model expenditures.

- Facility expenditures in connection with R&E.

- Ordinary and extraordinary utilities in connection with R&E.

- Travel expenditures incident to R&E.

- Foreign research expenditures.

- Additional overhead expenditures incident to R&E.

*In addition to the above, there are other criteria used for determining what expenses qualify for the R&D credit that do not apply towards determining Section 174 costs.

In contrast, the following are common expenses that are excluded from the expansive definition of R&E costs under Section 174:

- the ordinary testing or inspection of materials or products for quality control;

- efficiency surveys;

- management studies;

- consumer surveys;

- advertising or promotions;

- acquisition of another’s patent, model, production or process;

- research in connection with literary, historical, or similar projects; and

- expenditures for the acquisition or improvement of land.

The current R&E amortization rule explained

The ability to deduct R&E costs changed for all tax years beginning after December 31, 2021. As previously mentioned, these costs can no longer be deducted in full and must be capitalized and then amortized over five years for domestic costs and over 15 years for foreign costs. This amortization starts at the midpoint of the first year that the expenses were incurred, which results in only 10% of domestic costs (1/2 of 20%) being able to be deducted in their first year.

Per IRS guidance, this mandatory change can be implemented as an automatic accounting method change through attaching a statement to a taxpayer’s first income tax return with a year beginning after 2021, in lieu of filing the much more intricate Form 3115. This change should not have an effect on prior tax years, since the automatic method change is implemented on a “cut-off basis.”

Macro effect of mandatory capitalization

As mentioned above, before the prior rule was changed, every R&E expense could be deducted in full in the year they were incurred. While it is expected that the Section 174 expensing rules will revert to this — to some extent — through pressure from persistent lobbyists, this change has not been incorporated into a bill yet.

Some believe the mandatory R&E capitalization and amortization will adversely affect U.S. innovation, potentially resulting in a detrimental impact on our global competitiveness and jobs. For more than 60 years, businesses were able to immediately deduct their R&D expenses in the year those expenses were incurred (or choose to defer based on what worked for them). Now, the amortization of new R&E costs could cost businesses billions in cash taxes.

Significant considerations

Estimated Tax Payments: For taxpayers making estimated tax payments utilizing current year taxable income, consideration should be given to R&E expenditures and how the capitalization of those expenditures may impact taxable income and timing of cash tax payments. A closer look at refining the various accounts in a taxpayer’s books may be needed for this.

Tax Accounting / ASC 740: Taxpayers should be mindful of whether a new deferred tax asset is created, if any adjustment of existing deferred taxes may be necessary, or if a full or partial valuation allowance may be needed.

Other Areas Affected: The amortization requirement also affects other areas of taxable income, including the following:

- increases the deductibility of business interest under Section 163(j),

- increases the deductibility of the QBI (Qualified Business Income) deduction,

- increases the amount of GILTI (global intangible low-taxed income) for controlled foreign corporations,

- potentially adjusts the amount of FDII (foreign derived intangible income) deduction that can be taken,

- changes the amount of R&E expenses allocable for purposes of the foreign tax credit, and

- impacts state taxable income for the few states that do not conform to the capitalization requirement (e.g., California).

R&D credit considerations

The Section 174 capitalization requirements should not directly impact the amount of expenses that can be used for the R&D Tax Credit under Section 41, since the research credit is calculated using a much smaller subset of R&E expenditures than Section 174 and is not limited by the capitalization requirement. As Section 174 is much broader in scope, it applies to expenditures both eligible and ineligible for the research credit.

Another consideration for tax planning is that the research credit will be even more important to assist with reducing the additional tax liability that will be generated by the R&E treatment change, since the credit can help offset some of the tax liability increase. Moreover, the analysis & processes used to determine the R&D credit can be leveraged to identify Section 174 R&E expenses, which helps create some efficiencies in quantifying the overall effect of the mandatory capitalization and amortization requirement.

Extend impacted returns where possible

Tax return extensions are highly recommended for tax returns that have their due dates coming up. Not only is there the pending IRS guidance that may significantly change R&E expense calculations, but also the act of extending tax returns should allow more time for tax returns to be superseded (rather than amended) and should allow for R&D credit claims to be made on originally filed returns.

This is echoed by a September 2021 Chief Counsel Memorandum issued by the IRS, which made the process for claiming a refund under the R&D credit far more stringent. The memorandum relayed that taxpayers must provide more information on business components, identify the research activities performed, and name the individuals who performed each research activity. Given the additional amount of detail needed, taxpayers making R&D credit claims on amended returns — especially small businesses — have a heavier burden than those who make the claim on an originally filed returns.

How will it affect you?

If the mandatory R&E capitalization requirement is not changed, you should consider how the 174 capitalization rules will affect your business and how claiming the R&D credit will help offset the increase in tax liability. If you currently have an R&D credit analysis and/or an ASC 730 financial statement analysis, those studies can be used as starting points to determine the overall effect of Section 174 — keeping in mind that neither analysis includes all the costs included in Section 174.

If the requirement is changed, there are several ways that the R&E expense landscape could turn out for taxpayers. Ideally, Congress will revert to the prior rule regarding R&D expenses. In that situation, you should be able to choose what is best for you — immediately deducting or deferring.

Our perspective

As experienced advisors, MGO can help model the best R&E position for you, through the 2022 tax year and beyond — potentially saving you significant amounts of money. Our holistic tax advisor and business advisor-first philosophy factors not only the direct effects of the R&E capitalization requirement, but also the impact on other areas of your tax returns (e.g., international, transfer pricing, state, and local tax) and what potential savings you can obtain by claiming the R&D credit. Please feel free to reach out to any of our R&E costing profesionals below to get the experienced insight that you deserve.

About the author

Danielle Bradley is a senior manager in MGO’s National Tax Credits and Incentives practice. She focuses on helping businesses identify, substantiate, and defend federal and state tax credits and incentives. She has helped hundreds of companies monetize and defend over $100 million in various tax credits and incentives, such as the Research and Development (R&D) Tax Credit, Orphan Drug Credit, Employee Retention Credit, meals and entertainment deduction, and the current Research and Experimental (R&E) amortization calculations. Danielle has extensive experience in various industries, including software and technology, life sciences, manufacturing, aerospace and defense, and food, beverage and agriculture businesses.

Contact Danielle to further discuss the R&E amortization or other credits and incentives at Danielle Bradley, Matthew Sapowith (Tax Partner), or Michael Silvio (Tax Partner).

]]>- President Biden has signed the Inflation Reduction Act of 2022 into law.

- This large package contains many new tax credits to incentivize taxpayers to “go green” with energy from renewable resources while simultaneously receiving financial relief.

- It also extends or adds to currently existing credits for additional tax-saving opportunities.

On August 16, President Joe Biden signed the Inflation Reduction Act (IRA) of 2022 into law. Within the large tax reform package are numerous “green” tax credits focused on providing financial relief to taxpayers while incentivizing them to make sustainable choices and combat climate change.

These new credits are aimed at motivating taxpayers to use energy from renewable sources, prioritizing options like wind and solar. The IRA also introduces new credits and strengthens or extends existing credits that provide tax relief for purchasing new and used clean-energy vehicles and installing energy efficient heating and cooling systems. Additionally, companies that cut their methane emissions can access certain credits, while those that do not could face penalties.

The rules and regulations around claiming these green credits can be complicated. In this article, our Tax Credits and Incentives team breaks down how individuals and organizations can capitalize on these tax saving opportunities.

Swap gas guzzlers for an electric vehicle

Taxpayers that purchase a new or used “clean car” can qualify for this consumer tax credit. Vehicles considered clean are those that use a battery partly or fully manufactured in North America and built with materials extracted or processed in one of the countries currently in a free-trade agreement with the U.S.

Your income is a factor in how much you can reap in tax credits. If a taxpayer makes less than $150,000 annually (or has a combined family income below $300,000), the taxpayer can get up to $7,500 for new electric vehicles that qualify. Note the money would be applied at the point of sale, so the taxpayer’s monthly payments would be lowered (as opposed to reducing the tax bill months down the line).

Previously, the federal tax credit for electric vehicles did not include cars from manufacturers that already sold at least 200,000 models (GM, Toyota, and Tesla were excluded). This bill unravels that; instead, there is now a price threshold per vehicle. To qualify for the credit, bigger vehicles like SUVs, pickup trucks, and vans would have to cost less than $80,000 to qualify for the credits. Smaller vehicles are capped at $55,000. So, if you have your eye on a super sporty electric vehicle, you may be out of luck.

Taxpayers can also get $4,000 off a used electric vehicle if it is sold by a dealer for $25,000 or less — but only if they individually make up to $75,000 annually or $150,000 jointly. The addition of credits for used electric vehicle purchases is a win for the industry, and advocates of the bill are hopeful that this incentive will encourage an increase in electric vehicle adoption.

Modifying your home to be more energy efficient

To incentivize taxpayers to make their homes more energy efficient, the bill’s $4.28 billion High-Efficiency Electric Home Rebate Program provides rebates for low- and moderate-income households when they replace fossil-fuel boilers, furnaces, water heaters, and stoves with more efficient electric devices powered by renewable energy.

Some taxpayers will need to upgrade their electrical panels before they are able to install the new appliances. They can take advantage of up to $4,000 to do so. Furthermore, if they are interested in making their home generally more energy efficient, they can capitalize on a rebate of up to $1,600 given to seal and insulate their house, as well as up to $2,500 to improve their home’s wiring.

In terms of appliances, taxpayers can get up to $8,000 to install heat pumps that both heat and cool their home, plus as much as $1,750 for a heat-pump water heater. To offset the cost of a heat-pump dryer or electric stove, taxpayers can claim up to $840. It is estimated by making these changes, they can save significantly on their future energy bills.

There are several parameters for these rebates. First, the program runs through September 30, 2031 — so you do have time to implement these changes to your home. The maximum amount taxpayers can collect is $14,000, and to qualify, their household income cannot exceed $150% of the median income in the area they live. For those who do not qualify, there is a tax credit of up to $2,000 available to install heat pumps, plus up to $1,200 annually to install new windows, doors, or an induction stove.

Save when installing solar panels

Lastly, taxpayers can collect a 30% tax credit for installing residential solar panels through December 31, 2034. The credit decreases to 26% if you wait until after December 31, 2032. Taxpayers can also install solar battery systems to qualify for the tax credit.

New “green” tax credits

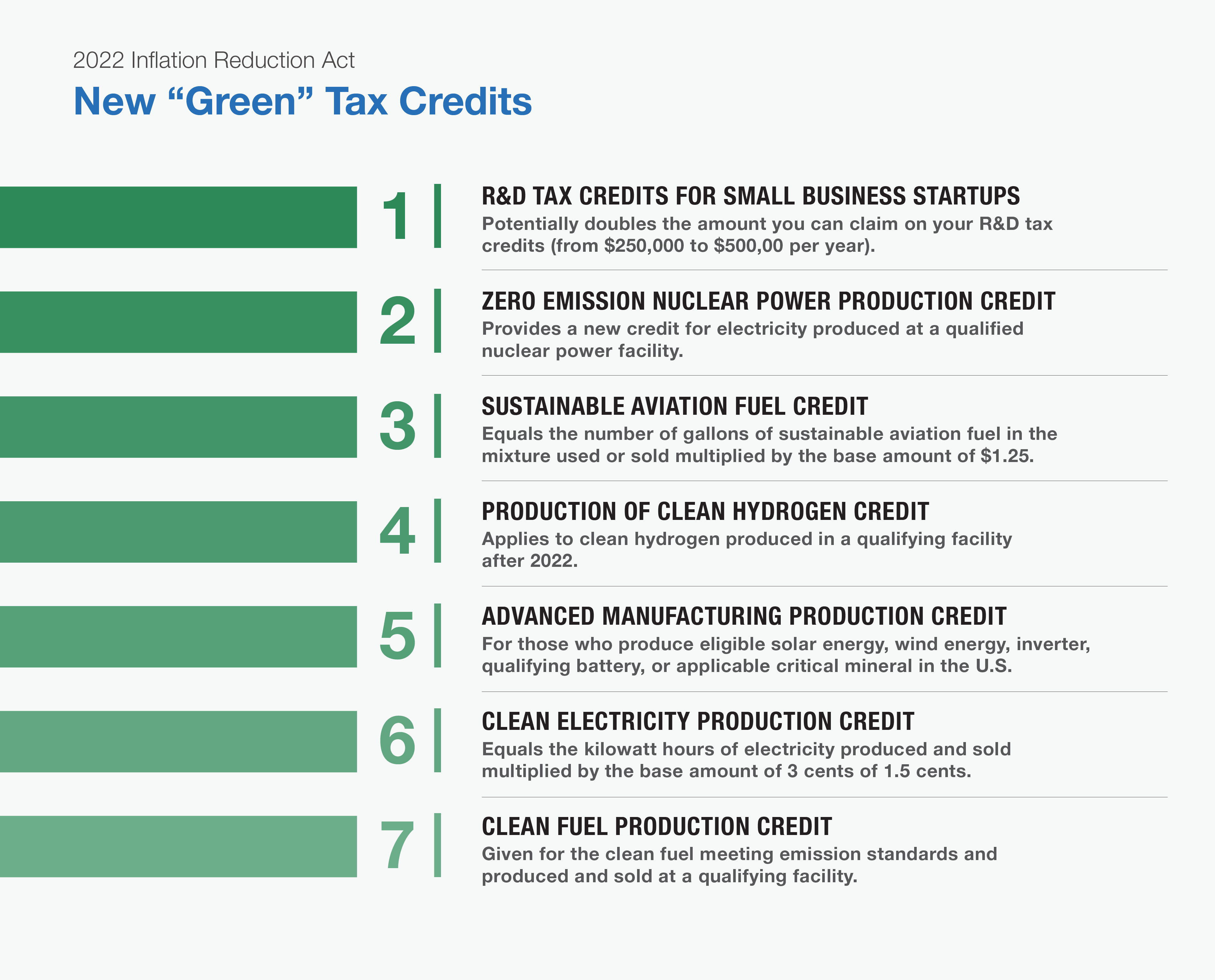

There are other ways taxpayers can take advantage of going green. Here are some of the new tax credits to capitalize on.

Doubling of R&D Tax Credits for Small Business Startups — Would potentially allow recipients to double the amount they can claim on any R&D tax credits (from $250,000 to $500,000 per year against payroll taxes).

Zero Emission Nuclear Power Production Credit — Provides a new business credit for electricity produced by a taxpayer at a qualified nuclear power facility before the date of enactment.

Sustainable Aviation Fuel Credit – Creates a new business credit for each gallon of sustainable aviation fuel sold or used as part of a qualified fuel mixture. The credit equals the number of gallons of sustainable aviation fuel in the mixture multiplied by the base amount of $1.25. There are increases available if the taxpayer meets certain greenhouse gas emissions reductions, and it applies to fuel sold or used in 2023 and 2024.

Production of Clean Hydrogen Credit — Given to producers of clean hydrogen during the ten-year period beginning on the date a qualifying facility is originally placed in service. It applies to clean hydrogen produced after 2022.

Advanced Manufacturing Production Credit — Provides a new production credit for each eligible solar energy component, wind energy component, eligible inverter, qualifying battery component, and applicable critical mineral produced by a taxpayer in the U.S. (or in U.S. possession and sold to an unrelated person). It applies to components and minerals produced and sold after 2022.

Clean Electricity Production Credit — New business credit for clean electricity facilities placed in service after 2024 (where the greenhouse gas emissions rate is not greater than zero). The credit amount equals the kilowatt hours of electricity produced and sold multiplied by the base amount of 3 cents or 1.5 cents. The credit will phase out one year after the later of 2032 or the year when annual greenhouse gas emissions from U.S. production are equal to less than 25% of the 2022 emissions rate (whichever comes first).

Clean Electricity Investment Credit — New investment credit for clean electricity property investments in energy storage technology and qualified facilities placed in service after 2024 where the greenhouse gas emissions rate is not greater than zero. It phases out after the later of 2032 or when the annual greenhouse gas emissions from U.S. electricity production are equal to or less than 25% of the 2022 emission rate (whichever comes first).

Clean Fuel Production Credit — Creates a business credit for the clean fuel a taxpayer produces at a qualifying facility and sells for qualifying purposes. The fuel must meet certain emissions standards.

Extension and modification of “green” tax credits

Several tax credits already in existence were extended and modified in the Inflation Reduction Act. They include:

Renewable Electricity Production Tax Credit (PTC) — Extends the beginning of construction deadline for certain renewable electricity production facilities through the end of 2024, as well as reduces the base amount of credit with the potential to qualify for five times that amount. It applies to facilities placed in service after 2021, and increases the credit amounts for domestic content, energy communities, and hydropower.

Energy Investment Tax (ITC) — Extends the beginning of construction deadline for some types of energy property, including qualified fuel cell property, for one year through the end of 2024. It extends the beginning of construction deadline for geothermal equipment through the end of 2034 and permits the credit for new types of energy property like energy storage technology, microgrid controller property, and qualified biogas.

Carbon Oxide Sequestration Credit — Extends and enhances carbon oxide sequestration credits for qualified industrial facilities and direct air capture facilities IF construction begins before 2033. It also lowers the minimum carbon capture requirement, and generally applies to those facilities and equipment placed in service post-2022.

Tax Credits for Biodiesel, Renewable Diesel, and Alternative Fuels — Extends these tax credits through 2024 and apply to fuel sold or used after 2021.

Second Generation Biofuel Credit — Extends tax credits to second generation biofuel through 2024 and applies to second generation biofuel production after 2021.

Nonbusiness Energy Property Credit — Extends this credit through 2023, as well as changes the credit rate to 30% for both qualified energy efficiency improvements and residential energy property expenditures. It replaces the $500 lifetime limit with a $1200 annual limit, modifies the limits for specific types of property, and modifies standards for qualified energy efficiency improvements on property placed in service after 2022.

Residential Energy Efficient Property Credit — Extends the residential energy-efficient property credit through 2034 and replaces the credit for biomass fuel property expenditures with a new credit for battery storage technology expenditures on those made after 2022.

New Energy Efficient Home Credit — Extends the business credit for contractors who manufacture or construct energy efficient homes through 2032. It applies to dwellings acquired by the contractor after 2022.

Alternative Fuel Vehicle Refueling Property Credit — Extends the tax credit through 2032 and increases the credit limit to $100,000 per item of depreciable refueling property and $1,000 per item of non-depreciable refueling property.

Advanced Energy Project Credit — Extends the competitively awarded investment tax credit for clean energy and energy efficiency manufacturing projects. It provides as much as $10 billion of new credit allocations effective in early 2023.

Increase in Energy Credit for Solar and Wind Facilities — In order to qualify, one must have a maximum net output of less than five megawatts and must be in a low-income community, on American Indian land, or part of a low-income residential building project (or low-income economic benefit project), effective in early 2023.

Reinstatement of Superfund Hazardous Substance Financing Rate — Reinstates a financing rate on crude oil and imported petroleum products at a rate of 16.4 cents per gallon through 2032.

Our perspective on the Inflation Reduction Act’s tax credits

Looking ahead, it is imperative that you are ready to capitalize on these tax credits. Getting into the weeds with some of the qualifications, however, could prove challenging, and working with a professional services firm could make all the difference in ensuring you take advantage of the credits you qualify for.

At MGO, our dedicated Tax Credits and Incentives team brings more than 30 years of experience in helping you structure your expenses in a way that will help you acquire appropriate documentation, assist in calculating and claiming credits, and maximize the amount you can receive. Our full-service firm, led by experienced CPAs and attorneys, provides a holistic approach to examining your organization and determining how you can best reach your goals.

About the author

Michael Silvio is a partner at MGO. He has more than 25 years of experience in public accounting and tax and has served a variety of public and private businesses in the manufacturing, distribution, pharmaceutical, and biotechnology sectors.

]]>We recently released an article detailing the red flags to look out when dealing with tax credits and incentives providers. If you think you could be at risk for future IRS issues, there is much you can do now to take a proactive approach and mitigate future negative impact. In the following, we break down steps you can take now to better understand and manage your exposure.

An overview of tax credits and incentives

Designed to encourage investment and development, job creation, growth, and certain business activities, tax credits and incentives provide an opportunity to reduce the amount of tax owed for performing certain activities. Credits and incentives are categorically different than tax deductions, which reduce the amount of taxable income.

These incentives often target desirable industries or activities like research and development, job creation for at-risk populations, and expanded growth in underdeveloped areas. When leveraged correctly, credits and incentives can be a powerful tool to funnel back resources into your organization to fuel activities you are already doing. Even more enticing, these credits can often apply retroactively if you determine you qualify for certain credits or incentives after the fact.

There are three basic types of tax credits: nonrefundable, refundable, and partially refundable. A few of the different types of tax credits pertaining to businesses in different classifications, industries, or activities performed include R&D tax credits, the employee retention tax credits, IRC Section 179D, and the work opportunity tax credit. To learn more about their eligibility rules, visit our previous article.

Understanding the risk of IRS tax audits

There is a three-year statute of limitations from the due date of the tax return or the filing date (whatever is later) for the IRS to assess your filings. That means if you think you may be exposed but escaped the IRS’ notice, you could still receive an audit notice for previous years’ returns. And if you do get audited, and the IRS determines you owe back taxes, you will get charged penalties and interest dating back to the infraction itself.

This is even more risky when considering the IRS’s extreme backlog. These IRS tax audits can sometimes take years to complete and if your credit and incentive calculations are the topic of interest, you’ll need to halt any future credit analysis until the situation is resolved. Meanwhile, you’ll be devoting crucial resources, time, and effort working with the IRS for something that yields no financial value and distracts from more conducive business activities.

Reasons to get a head-start and address issues now

Even though there is no guarantee you will get audited, you are still taking a risk if you do not address potential tax credit and incentive exposures in your organization. It may seem easy to “roll the dice” and hope the issue will remain uncovered, but it could come at a cost — especially if you are planning to make some big moves, like engaging in transaction of your business (M&A), going public, or embarking on another major transaction.

During the due diligence period of these transactions, it is almost certain any uncovered tax issues will emerge. You will likely not recover the value of these credits or remain on the hook for potential liability. Even worse, the exposure of these issues reflects negatively on your accounting and control system, potentially lowering the purchase value of your organization or undermining whatever deal you had in place prior to the due diligence. Often your transaction partners will start to question your organization’s trustworthiness, and reputation … due to something that may be no fault of your own.

So, you’ve been exposed … but haven’t received an IRS audit notice

Here is the deal: you know for certain you have been exposed, but you have not been notified by the IRS yet. You probably have a lot of questions — will you get an audit notice? Have you escaped unscathed? Do you need to address the issues preemptively, just in case? It may be overwhelming to decide how to proceed once you realize the exposure.

We suggest working with a qualified CPA firm to review your tax filings. A full-service accounting firm will review your organization holistically at a minimum rate, uncover any exposures, and deliver valuable peace of mind. If the firm does find issues, you have two options:

- Update your credit and incentive filings moving forward.

- While this will likely decrease the amount you can deduct, it exemplifies transparency.

- Issue a Voluntary Disclosure (VA) if the exposure is significant and you do not have a lot of time to fix the issue.

- Essentially, you are volunteering to correct your mistakes by recalculating the credits claimed and paying back the difference.

- While this may sting a little, the IRS looks favorably upon organizations who are proactive to fix the issue by filing a VA and they are likely to waive any penalties or interest you would have had to pay.

You’ve received an IRS audit notice. Now what?

Well, it happened. You received an audit note from the IRS. Before you panic, here is what you need to do:

- Start preparing your documentation right away. The sooner you have your ducks in a row, the sooner you are prepared to handle the audit.

- Check the contract you signed with your original provider and verify if they provide controversy support services for situations like these.

- If they do, reexamine the quality of their work. Do they have any of the red flags mentioned in this article? Could something they have done have caused the audit?

- Consider engaging a qualified CPA firm as your new provider to handle the subsequent controversy support. Someone you trust can get you ready for any available credits and incentives moving forward, too.

- If you used a provider that displays any red flags, you could have some leverage for a reasonable cause defense. Because the “professional” firm handled it for you and made a mistake, you could utilize a first-time penalty abatement, which means you can get relief from a penalty if you:

- Did not previously have to file a return or if you do not have any penalties for the three years before the tax year you received a penalty;

- Filed all currently required returns or an extension of time to file;

and - Paid or have arranged to pay any tax due.

- Verify your contract with the original provider to determine if you have any recourse to seek compensation from them. If the IRS does issue any penalties, you will want to ensure you do not have to pay.

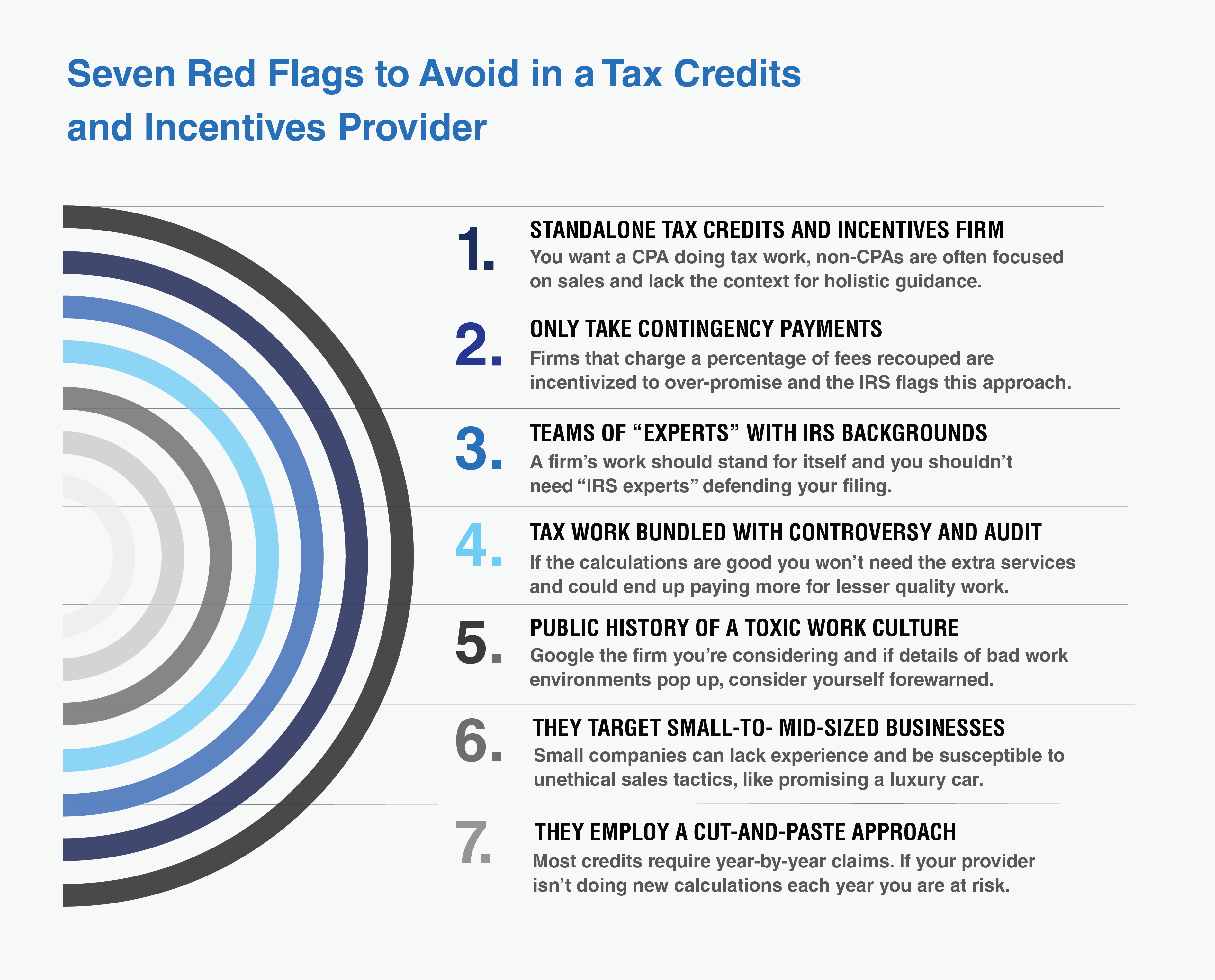

Standalone firms vs. full-service accounting firms

Let’s say you haven’t received an IRS notice, and you do not think you are in danger of receiving one. How can you ensure you will not in the future? It comes down to choosing a firm to help you maximize the potential of these tax credits and incentives.

The bottom line: it is imperative you work with a certified public accounting (CPA) firm instead of a standalone firm. Because standalone firms often use lower-cost, less-experienced recent graduates who are not certified public accountants, there is a distinct lack of knowledge and background in the accounting fundamentals, causing you to be misled by those unequipped to help with complex tax matters. You also run the risk of being oversold benefits by aggressive firms that not only exaggerate the amount you are receiving from the tax credits and incentives, but also behave in a way that attracts IRS attention and jeopardizes your firm.

A full-service accounting firm, on the other hand, knows how to look at an organization holistically — and it has many more capabilities and professionals with experience. It looks at things through various lenses and can advise how certain positions will impact current and future tax positions. Full-service firms also likely have an in-house controversy team that has handled hundreds of audits successfully—so you will be in good hands.

Our perspective

Tax credits and incentives provide plenty of benefits you do not want to miss out on, and their often-complex application and qualification processes are reason enough to hire a professional accountant to help you maximize your returns. Unfortunately, we often see organizations placing their trust in the wrong providers and they end up suffering the consequences of an IRS audit. For many, it is simply easier and safer to cut off the relationship with the initial provider and start fresh with a professional firm you know you can trust.

At MGO, our dedicated Tax Credits and Incentives team brings more than 30 years of experience fixing these types of issues and working with the IRS to limit the damage. We provide cleanup in the event you are being audited by the IRS (or could be audited in the future), and help you identify areas where you can claim tax credits and incentives for next time. If you are concerned, our best advice is to get ahead of it with an opinion you can trust — before the IRS decides to investigate themselves.

About the author

Michael Silvio is a partner at MGO. He has more than 25 years of experience in public accounting and tax and has served a variety of public and private businesses in the manufacturing, distribution, pharmaceutical, and biotechnology sectors.

]]>Both in terms of tax liability and compliance responsibilities, this change is a big deal for those legal cannabis companies that have been struggling to survive under California’s cannabis tax regime, which, in some parts of the state, are the highest in the nation. Perhaps more importantly, it signifies that the state government is finally addressing the tax crisis that has made it nearly impossible for many California cannabis operators to grow and thrive.

Tax credits and incentives provided by AB 195

Hampered by complex regulations and high taxes, cannabis operators in the legal market have struggled, even as California’s tax revenue has soared. But the reforms, now official, provide a positive sign for legal operators that the state is moving in the right direction to support the industry.

Not only will AB 195 eliminate the cultivation tax and shift the excise tax to the retailer, but it will also put into action several other reforms. These include:

- Capping the excise tax rate at 15% for three fiscal years (though it could increase after July 1, 2025);

- Permitting social equity licensees to keep 20% of the excise taxes they collect so they can reinvest in their businesses;

- Equity licensees’ ability to collect a one-time $10,000 tax credit (to qualify, the firms must be licensed under programs to ensure representation in the industry from members of underserved communities/those harmed by prohibition policies);

- Lowering the number of workers that a business can employ before having to meet requirements to create a labor peace agreement; and

- Creating $40 million in available tax credits, which consist of:

- $20 million for some storefront retail and microbusinesses

- $20 million for cannabis equity operators

Decreasing the tax markup — and what the relief means for operators

California residents pay high taxes across the board. But the California cannabis industry and their customers suffer more than most. In addition to the 15% excise tax, there are sales and use taxes that can reach up to 11%, as well as local business taxes that can go as high as 15% depending on location. Prior to its elimination, the state cultivation tax was required by the Cannabis Tax Law to reflect adjustments for inflation — and many jurisdictions layer in even more taxes on distribution, manufacturing, and cultivation activities before the product even reaches the consumer.

Growers have long since been calling for relief, and in fall of 2021, wholesale prices collapsed, making it difficult for independent cultivation operators to make a profit. The governor said help was coming, although it was not until May of 2022 that the potential budget change that would cut the cultivation tax to zero was announced. This may not help growers who have already fallen susceptible to these sky-high taxes, but it delivers much-needed relief to those who are still currently struggling with rising inflation and reduced demand after peak COVID-19 pandemic levels.

The decrease also backs the governor’s commitment to minimize the presence of illicit growers on the scene. “Black market” operators that don’t pay taxes are able to offer products to their customers at much lower prices while still turning a profit. High tax rates that pass through to customers inevitably drive customers away and undercut the legal and licensed businesses, hurting those who are following the rules.

Why shifting tax collection from the distributor to the retailer is a win for the industry

While the removal of the cultivation tax presents a clear and immediate benefit, shifting the tax collection obligation from the distributor to the retailer is perhaps less obviously, but maybe even more, impactful to cannabis operators — and helps to put the legal cannabis industry on more equal footing with other industries.

Under the prior system, distributors were responsible for collecting both the cultivation tax from cultivators (by reducing the amount paid) and the excise tax from retailers. In the case of the latter tax, whenever the transaction involved unrelated parties (“arm’s length”) where the distributor is unaware of the ultimate selling price, the “average market selling price” that forms the tax base was determined using the CDTFA’s biannually published “mark-up” rate of 180% of the actual, wholesale price charged (reduced to 175% through the end of 2022). Consequently, for these transactions (which make up the majority of those in the industry), the mark-up rate has the effect of increasing the rate of the excise tax from 15% to 27%.

Theoretically, after paying the marked-up rate, retailers can recoup the outlay when they make the ultimate sale to the consumer, which (other than the cultivation tax) would make the tax scheme business-neutral (i.e., it should not create additional costs for businesses). However, in practice, there are several problems with California’s approach.

First, the timing of the tax payments under this system increases pressure on cash-flow for an already cash-strapped industry. Like many businesses, cannabis distributors do not always pay or get paid at the time of the transaction; instead, contractual payment terms often allow for a certain period to pass after transferring the goods before the cash consideration is due to the seller. This period allows the purchaser (i.e., retailer) a window of time in which to sell the goods and then have cash with which to satisfy the payment obligation to the distributor. But under California’s system, the excise tax is due to the state at the time it transfers to the retailer and before the infusion of cash from the consumer —placing the onus on the businesses to cover the consumer’s excise tax liability.

The second problem created by the system stems from the mismatch between the mark-up rate and reality. On the front end, most retailers need to pay tax on a presumed profit margin of 80% above the wholesale cost, regardless of what their actual margin would be (given spoilage, consumer demand, and the variety of market factors that affect cost). And even though the laws allow the retailer to simply pass through the cost, inventory-tracking and point-of-sale software often lack the complexity to do more than simply attach an additional 15% to the invoice (like how the software adds sales tax). In addition to this potential for leakage, retailers must contend with market price constraints as in any other industry — except in this industry, legal operators must also compete with a plethora of illegal operators who can undercut prices by ignoring the taxes.

AB-195’s changes, therefore, not only reduce tax for the industry overall, but also alleviate some of the compliance inefficiencies created by California’s cannabis tax regime. As of July 1, 2022, cannabis distributors are no longer required to collect and remit cultivation tax, and beginning January 1, 2023, they will no longer be required to collect and remit the excise tax. Thus, instead of using the mark-up rate to determine tax before it is sold and needing to “cover” the tax burden of the ultimate consumer, distributors will no longer be responsible for complying with a consumption tax. And in addition to alleviating cash flow issues, this shift also fixes retailers’ leakage problems by removing the unrealistic mark-up and allowing retailers to directly charge the consumer the exact tax due on products that actually make their way through the commercial process, and in the customer’s possession.

Our perspective on the tax changes impacting California’s cannabis industry

Many industry leaders are praising the administration for making real moves to rein in overbearing regulations for an industry that brings in a lot of money in tax revenue to the state ($817 million, to be exact, for fiscal year 2020-2021).

While these changes are a positive sign for the cannabis industry and its legal operators, many are still calling for additional reforms — in fact, some say taxes should be cut even more if legal cannabis wants a chance of competing on price with the illegal market. Cannabis retailers especially are expressing dissatisfaction, as they did not receive a direct tax cut like growers did with AB-195. Many critics also think social equity operators deserve even stronger aid as they are already at a disadvantage.

MGO is a national leader in both tax advisory and cannabis accounting and financial best practices. We can help you identify tax opportunities, prepare documentation, and take other steps to reduce your tax exposure. If you have any questions about California’s tax change and how it could affect your business, please reach out to our leading cannabis tax practice.

About the authors

Matt Sapowith is a tax partner at MGO with more than 13 years of tax planning and compliance experience in areas including corporate and partnership taxation, international tax, M&A transaction advisory, transfer pricing, state and local tax, R&D credit, and compensation planning. He has worked with companies in many industries, including cannabis. Contact Matt at MSapowith@mgocpa.com.

Nolan Shutler is a Director at MGO and National State and Local Tax Lead for SALT consulting and indirect taxes. Contact Nolan at nshutler@mgocpa.com.

]]>In recent years, a number of firms have emerged specializing in credits and incentives and building large businesses by over-promising and under-delivering these tax consulting services. While credits and incentives are enticing, they must be handled with extreme care, as the consequences of getting it wrong can be serious.

At MGO, we not only help you determine if you are eligible for these valuable tax credits and incentives, but we also perform damage control and clean-up following bad actors’ broken promises and sloppy work. We have seen firsthand the fallout from their poor performance and how it affects clients. In this article, we will help you understand what to look for in a tax credits and incentives provider and recognize and avoid IRS red flags so you can safely capitalize on these opportunities.

An overview of tax credits and incentives

Designed to encourage investment and development, job creation, growth, and certain business activities, tax credits and incentives provide an opportunity to reduce the amount of tax owed for performing certain activities. Credits and incentives are categorically different than tax deductions, which reduce the amount of taxable income.