- In April, the U.S. Tax Court made news when it ruled in favor of businessman Alon Farhy, who challenged the Internal Revenue Service (IRS)’s authority to assess penalties for the failure to file IRS Form 5471.

- IRS Form 5471 is the Information Return of U.S. Persons With Respect to Certain Foreign Corporations.

- Taxpayers may be interested in filing protective refunds, and they should start the process sooner rather than later—there is a statute of limitations of two years for claiming refunds.

- This case’s ruling could have reverberating effects when it comes to the IRS collecting additional penalties, but only time will tell.

On April 3, 2023, the U.S. Tax Court came to a decision in the case Farhy v. Commissioner, ruling that the Internal Revenue Service (IRS) does not have the statutory authority to assess penalties for the failure to file IRS Form 5471, or the Information Return of U.S. Persons With Respect to Certain Foreign Corporations, against taxpayers. It also ruled that the IRS cannot administratively collect such penalties via levy.

Now that the IRS doesn’t have the authority to assess certain foreign information return penalties according to the court, affected taxpayers may want to file protective refund claims, even if the case goes to appeals — especially given the short statute of limitations of two years for claiming refunds.

Our Tax Controversy team breaks down the Farhy case, as well as what it may mean for your international filings — and the future of the IRS’s penalty collections.

The case

Alon Farhy owned 100% of a Belize corporation from 2003 until 2010, as well as 100% of another Belize corporation from 2005 until 2010. He admitted he participated in an illegal scheme to reduce his income tax and gained immunity from prosecution. However, throughout the time of his ownership of these two companies, he was required to file IRS Forms 5471 for both — but he didn’t.

The IRS then mailed him a notice in February 2016, alerting him of his failure to file. He still didn’t file, and in November 2018, he assessed $10,000 per failure to file, per year — plus a continuation penalty of $50,000 for each year he failed to file. The IRS determined his failures to file were deliberate, and so the penalties were met with the appropriate approval within the IRS.

Farhy didn’t dispute that he didn’t file. He also didn’t deny he failed to pay. Instead, he challenged the IRS’s legal authority to assess IRC section 6038 penalties.

The court’s ruling

The U.S. Tax Court then held that Congress authorized the assessment for a variety of penalties — namely, those found in subchapter B of chapter 68 of subtitle F — but not for those penalties under IRC sections 6038(b)(1) and (2), which apply to Form 5471. Because these penalties were not assessable, the court decided the IRS was prohibited from proceeding with collection, and the only way the IRS can pursue collection of the taxpayer’s penalties was by 28 U.S.C. Sec. 2461(a) — which allows recovery of any penalty by civil court action.

How this court decision affects your international penalty assessments

This case holds that the IRS may not assess penalties under IRC section 6038(b), or failure to file IRS Form 5471. The case’s ruling doesn’t mean you don’t have an obligation to file IRS Form 5471 — or any other required form.

Ultimately, this decision is expected to have a broad reach and will affect most IRS Form 5471 filers, namely category 1, 4, and 5 filers (but not category 2 and 3 filers, who are subject to penalties under IRC section 6679).

However, the case’s impact could permeate even deeper. For years, some practitioners have spoken out against the IRS’s systemic assessment of international information return (IIR) penalties after a return is filed late, making it impossible for taxpayers to avoid deficiency procedures. The court’s decision now reveals how a taxpayer can be protected by the judicial branch when something is deemed unfair. Farhy took a stand, challenged the system, and won — opening the door for potential challenges in the future.

It’s uncertain as to whether the IRS will appeal the court’s decision. But it seems as though the stakes are too high for the IRS not to appeal. While we don’t know what will happen, a former IRS official has stated he expects that, for cases currently pending review by IRS Appeals, Farhy will not be viewed as controlling law yet.

The impact of the ruling is clear and will most likely impact many taxpayers who are contesting — or who have already paid — IRC 6038 penalties. It may also affect other civil penalties where Congress has not prescribed the method of assessment in the future.

How you should respond to the court’s decision

You should move quickly to take advantage of the court’s decision, as there is a two-year statute of limitations from the time a tax is paid to make a protective claim for a refund. It’s likely this legislation wouldn’t affect refund claims since that would be governed by the law that existed when the penalties were assessed. Note that per IRC section 6665(a)(2), there is no distinction between payments of tax, addition to tax, penalties, or interest — so all items are treated as tax.

If you’ve previously paid the $10,000 penalty, it’s important to file your protective claim now, unless you’ve entered into an agreement with the IRS to extend the statute of limitations, which can occur during an examination. Requesting a refund won’t ever hurt, but some practitioners believe the IRS may try to keep any penalty money it collected, even if the assessment is invalid— because, in its eyes, the claim may not be. Just know, you can file your protective claim for a refund but may not get it, at least not any time soon.

The Farhy decision could likewise be applied to other US IRS forms, such as 5472, 8865, 8938, 926, 8858, 8854, and some argue the Farhy decision may also be applied to IRS Form 3520.

How MGO can help

Only time will tell if the court’s decision will open the government up to additional criticisms for other penalty assessments. If you have paid your penalties and are wondering what your current options are, MGO’s experienced International Tax team can help you determine if you’re eligible to file a refund claim.

Contact us to learn more.

]]>

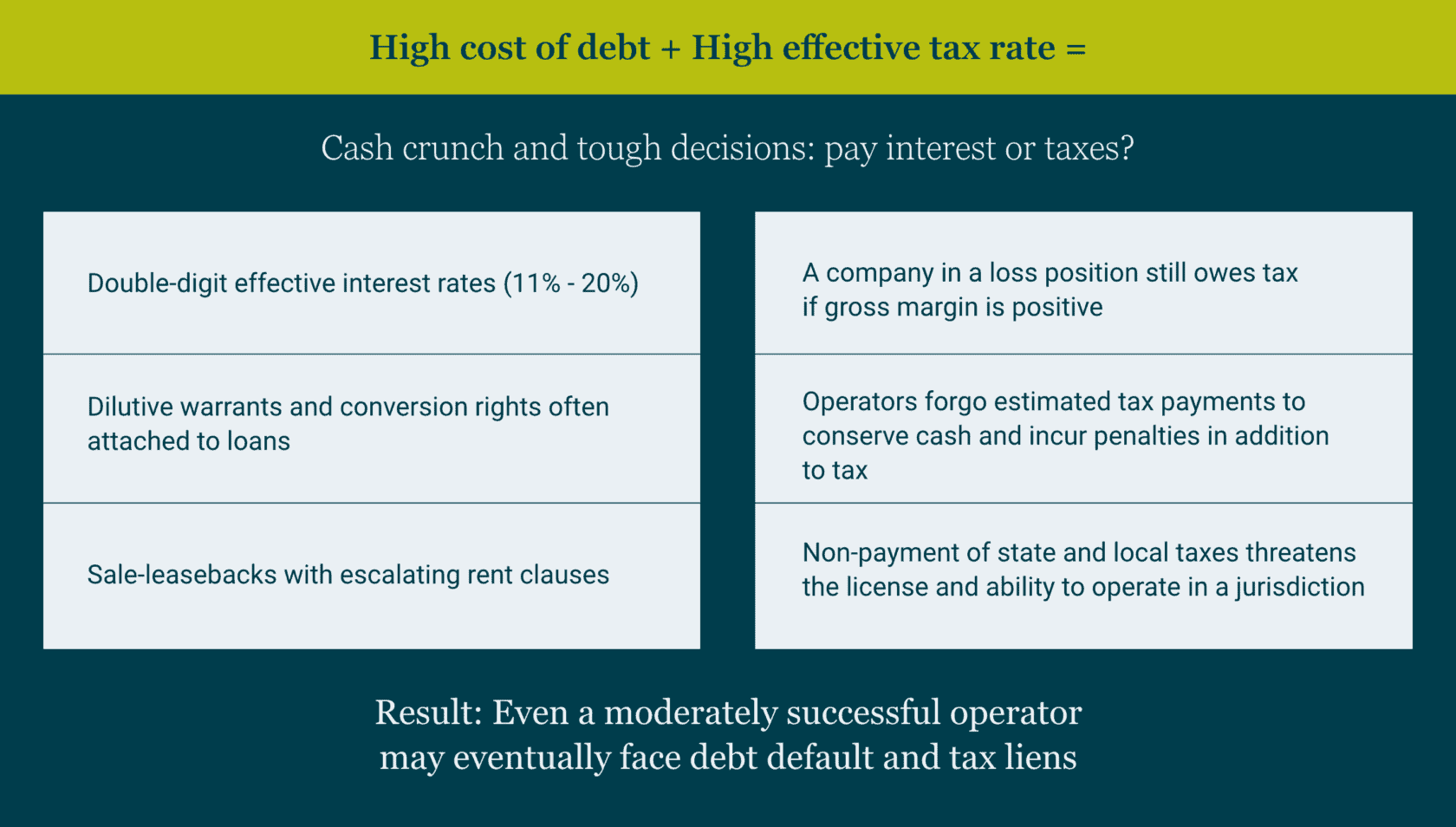

High cost of debt + high effective tax rate = cash crunch and tough decisions

How did cannabis companies arrive at this decision point? The current cash crunch in the industry has been building for years, precipitated in part by banking regulatory constraints and an abnormally high effective federal tax rate.

As the below chart illustrates, cannabis companies lack access to traditional banking and market rate loans and have turned to alternative, expensive sources of debt financing bearing effective interest rates as high as 20%. In addition, Internal Revenue Code Section 280E essentially taxes the industry on gross margins, such that even a company that would otherwise be in an overall tax loss position may still owe taxes.

Caught in this double bind, even an operationally successful cannabis company may face a difficult choice: service debt timely at the expense of keeping current with taxes, risking tax liens that threaten the license, or pay taxes when due at the price of defaulting on debt and risking the viability of the business overall.

The tax impact of debt restructuring

Restructuring debt is one route for cannabis companies in distress to remain operational, but debt modification carries potential tax traps for the unwary – both borrower and lender. Depending on the relative value of the debt exchanged, the borrower can realize cancellation of debt income. The insolvency exception to recognizing and paying current tax on this income may not be available to a cannabis company, as the fair value of its assets – including intangibles – may still exceed its liabilities. A lender may also experience a taxable event on the refinancing, either in the form of interest income, or gain due to the valuation of equity received in the exchange.

In any debt refinancing situation, both the borrower and the lender should anticipate and plan for complex tax calculations involving debt discounts (I.e., original issue discount, or OID) and the fair value of company equity in order to determine correct tax treatment. To avoid any last-minute surprises or deal delays, both the borrower and the lender should model the tax treatment on both sides.

Sales of distressed assets and the tax impact

Considerations for the borrower:

- Are the assets to be sold in a different tax filing entity as the borrower?

- Will the flow of cash between entities create a taxable event?

Considerations for the lender:

- What is the borrower’s anticipated cash position after paying tax on the sale?

- Can cannabis business assets be sold in the jurisdiction’s regulatory environment? Or is a sale restricted to equity?

Assignment of income receipt of equity

If the borrower and the lender agree on a debt workout based on assignment of income, or equity ownership, both parties should understand the borrower’s existing tax structure and the impact the restructuring will have on both sides.

The borrower should assess whether a “change in control” has occurred for tax purposes, as the use of tax attributes may be limited. If an assignment of income is structured as a fee, consider the tax treatment of the payment and deductibility under 280E.

A lender who becomes an owner or part of management should consider:

- Depending on how the agreement is structured, the assignment of operating income and participation in management may turn the lender, or the lender’s entity, into a “trafficker” subject to 280E.

The lender should also be cognizant of the borrower’s standing with the taxing authorities and whether the operator can afford both paying down tax liabilities and payments under the terms of the workout. The retention of the cannabis or reseller license that the lender is depending on for cash flow is tied to staying current with state and local taxes. An IRS liability that has progressed to the lien stage unbeknownst to the lender could result in a “sudden” drain of cash from a bank account.

“Workouts” with taxing authorities

Given the current cash crunch in the industry, companies have been known to delay remittance of sales and excise taxes to state and local governments. Companies should be aware that non-payment of these “trustee” taxes can cause a loss of standing to operate legally and carries personal liability for officers and owners of the company. Taxing authorities may have limited sympathy for a distressed taxpayer who falls behind on these types of taxes and taxpayers should pay down any outstanding balances as soon as possible.

If income taxes are past due, it is important to continue to make payments toward the balance on a regular basis. A taxpayer cannot apply for a formal IRS payment plan until a revenue officer is assigned to the case. Also, a taxpayer must usually pay all outstanding taxes that are not overdue and remain “current” on all future taxes in order to establish and remain on an installment agreement. Federal and state revenue officers are generally willing to work with taxpayers in financial distress who act in good faith throughout the process. Engaging a professional representative who understands tax controversy practice and procedure and how to work with revenue officers can make all the difference between establishing a payment plan and facing a tax lien.

How MGO can help

A cannabis company navigating financial distress should engage a tax professional with both industry experience and a high level of tax technical skill to navigate the complex tax impact of a workout or restructuring. MGO’s Cannabis Tax team has both the industry experience and the technical knowledge to assist companies of all sizes during this challenging time.

]]>- Increasing Internal Revenue Service (IRS) budget

- Implementing a corporate tax minimum

- Instituting and increasing tax credits focused on investing in green technologies

Notable items that were not addressed in the IRA include removing the $10,000 SALT cap and mandatory capitalization of research and development (R&D) expenses, both provisions of the Tax Cuts and Jobs Act of 2017.

The bill is over 300 pages in length with a number of wide-ranging components. In the following summary we’ll provide the key points that will be affecting taxpayers in the coming years.

Additional funding to the IRS for tax enforcement

One of the most talked-about provisions involves increased funding for the IRS.

Key details:

- Approximately $80 billion in funding over the next 10 years for tax services, operations support, business system modernization, and enforcement

- Enforcement – $46 billion

- Operations support – $25 billion

- Business systems modernization – $5 billion

- Taxpayer services – $3 billion

- An estimated $124 to $200 billion will be generated from enforcement and compliance efforts

- Enforcement is focused on taxpayers – both corporate and non-corporate – with income greater than $400,000

Extension of the business loss limitation of noncorporate taxpayers

The IRA extends the excess business loss limitation for noncorporate taxpayers.

Key details:

- Two year extension on IRC Sec. 461(l) until December 31, 2028

- IRC Sec. 461(l) limits noncorporate taxpayers from deducting business losses above thresholds that are annually indexed for inflation

- These limits are $540,000 for married filing jointly and $270,000 for single and married filing single for the 2022 tax year

- Suspended amounts are converted to net operating losses and may be able to be used in subsequent years

Excise tax on repurchases of corporate stock

The IRA includes a 1% excise tax on stock repurchases by domestic public companies listed on an established securities market. The tax applies to repurchases executed after December 31st, 2022.

Key details:

- 1% excise tax on the full market value (FMV) of stock repurchased by publicly traded US corporations

- Will impact redemptions and certain acquisitions and repurchases of publicly traded foreign corporation stock

- Not an income tax for purposes of ASC 740

- Includes special rules for “applicable foreign corporations” and “surrogate foreign corporations”

- Notable exceptions:

- Stock is contributed to employer sponsored retirement plan

- Stock repurchase is part of a corporate reorganization

- Total value of stock repurchased during the taxable year does not exceed $1 million

- Repurchase by securities dealer in ordinary course of business

- If the repurchase qualifies as a dividend

- If the repurchase is by a regulated investment company (RIC) or a real estate investment trust (REIT)

15% corporate alternative minimum tax

The IRA reinstates the corporate alternative minimum tax (AMT) for large corporations, which had been previously eliminated by the Trump Administration’s Tax Cuts and Jobs Act.

Two key elements to note is that this revised AMT only impacts corporations with annual profits exceeding $1 billion, and includes carve-outs for certain manufacturers and subsidiaries of private equity firms.

Key details:

- 15% tax on adjusted financial statement income (i.e., this would be a book minimum tax)

- Affects tax years beginning after December 31, 2022

- Applies to corporations with profits over $1 billion based off adjusted financial income

- For US corporations with foreign parents, it would apply to income earned in the US of $100 million or more of average annual earnings in three prior years and where the overall international financial reporting group has income of $1 billion or more

- Treatment of split offs remains uncertain. Even though these are tax-free reorganizations for tax purposes, gain is recorded for financial accounting purposes

- Joint Committee on Taxation expects that this new tax would apply to only about 150 corporate taxpayers, approximately equal to 30% of the Fortune 500

Tax credit additions and modifications

A significant number of provisions add or enhance credits and incentives that pertain to domestic research and green energy initiatives. Noteworthy changes include:

Increased small business payroll tax credits for research activities:

- Qualified payroll tax credit for increasing research activities raised from $250,000 to $500,000

- First $250,000 will be applied against the FICA payroll tax liability. Second $250,000 will be applied against the employer portion of Medicare payroll tax.

- Applies for taxable years beginning after December 31, 2022

- Limited to tax imposed for calendar quarter with unused amounts being carried forward

- Qualifying small businesses are required to have less than $5 million in gross receipts in current year and no gross receipts prior to the 5 year period ending with the current year

Green initiative tax credits and incentives:

- Credits for purchasing new and previously-owned clean vehicles

- Extension of IRC Sec. 45L – New Energy Efficient Home Credit – extended to qualified new energy efficient homes acquired before January 1, 2033. Increase value of available credit for single-family homes to $2,500 and modified the credit available for multi-family homes.

- Extension, increase, and modifications to IRC Sec. 25C nonbusiness energy property credit

- Extension and modification of IRC Sec. 25D residential clean energy credit

- IRC Sec. 48 energy credit for businesses and investors

- Expansion of qualifying property, extension of credit including phasedown and phaseout rules, and introduction of incentives

- Credit for producing energy from renewable sources (IRC Sec. 45)

- Retroactive for facilities placed in service after December 31, 2021

- Extends beginning of construction deadline to projects beginning construction before January 1, 2025 including solar energy facilities

- Increased energy credit for solar and wind facilities in certain low-income communities

- New credit for clean hydrogen production

- New credit for zero-emission nuclear power

- Extension of incentives for biodiesel, renewal diesel, and alternative fuels

- Extension of biofuel producer credit

- New income and excise tax credits allowed for sustainable aviation fuel

- Modification of IRC Sec. 179D – Energy Efficient Commercial Buildings Deductions

- Modification of building qualifications

- Deduction increased from $1.88 per square foot to up to $5 per qualified square foot

- Changes in depreciation for certain green energy properties

Final thoughts

The Inflation Reduction Act should have wide-ranging impacts on taxpayers, especially large corporations and high-net-worth individuals. In the coming weeks our tax leaders will dive into the specifics of the legislation, outline immediate and long-term impacts, and provide tax-planning strategies and considerations.

]]>California’s workaround is in effect for the 2021 tax year and will continue to be available through the 2025 tax year (although it could expire earlier if the federal $10,000 limitation is repealed by Congress prior to its current sunset date of January 1, 2026).

The state tax credit, which is nonrefundable, can be carried over for five years. Nonresidents and part-year residents do not have to prorate the credit to account for their non-California income.

How to elect

California’s workaround is available for partnerships (including those structured as LLCs) and S corporations that only have individuals, trusts, estates, and/or corporations as owners. Publicly traded partnerships, partnerships owned by other partnerships, members of a combined reporting group, and disregarded entities do not qualify. (Disregarded Single-Member LLCs are not eligible to make the election, but will not make the entity ineligible if they are an owner of an otherwise eligible PTE).

Not all the owners of the pass-through entity need to consent to the election. Those that do not consent are not included in the calculation of the PTE Tax. To take advantage of the workaround, the pass-through entity needs to make the election annually on its state tax return. In addition, payments towards the PTE Tax need to be made by specified due dates.

• For the 2021 tax year, 100% of the PTE Tax needs to be paid by the due date for the pass-through entity’s state tax return without extensions – March 15, 2022.

• In later years, the PTE tax needs to be paid in two installments: the first installment is due by June 15 of the tax year for which the election is being made, and the second installment is due by the due date for the pass-through entity’s state tax return for that tax year without extensions (i.e., the following March 15). The minimum amount for the first installment is $1,000.

What to consider

The biggest benefit to the owners of a pass-through entity is the ability to claim a federal tax deduction for their share of the pass-through entity’s state income tax paid to California, but there is another potential benefit. In future years (starting with the 2022 tax year) PTE Tax payments may create some “float” for the owners in terms of the timing and amount of their individual estimated tax payments:

- Individuals in California need to pay 70% of their estimated tax liability through quarterly payments on April 15 and June 15, while the PTE Tax only requires that one installment of 50% of the total tax be paid in by June 15.

- Individuals in California need to pay the remaining 30% of their estimated tax liability by January 15 of the following year (i.e., the 4th quarter payment), while the PTE Tax only requires the remaining 50% be paid in by March 15.

However, despite these benefits, other factors should be considered before making the election:

- If the pass-through entity provides most of the income for an owner and that owner’s top California tax rate is less than or equal to 9.3%, the state tax credit cannot be used in full before it expires. On the other hand, since the election is made annually, you could avoid accruing too much carryover by opting not to elect in a following year.

- It’s unclear how California’s workaround will interact with pass-through entity tax regimes enacted by other states, especially their associated state tax credits. California provides credits against most other states’ taxes, but guidance has not been provided to indicate that it will afford the same treatment to other state PTE Taxes paid. Multi-state operators may not be able to reduce California taxable income by the amounts of other states’ similar taxes.

- The 9.3% flat rate may not be sufficient to cover the full tax liability for higher income owners.

- The PTE tax credit does not reduce the amount of tax due below California’s Tentative Minimum Tax (TMT), and thus may not be as beneficial for taxpayers subject to the TMT.

- There are considerations pertaining to cash management, since the pass-through entity would be paying the PTE Tax, not the owners.

- Non-resident withholding (7% for individuals) is not offset by the withholding requirements for the PTE Election. Non-resident taxpayers making the election would therefore be required to pay in tax at 16.3% among the quarterly and bi-annual installments, then claim a refund up to the amount of the 7% withholding. But because the 9.3% PTE Tax is non-refundable, to the extent that withholding exceeds tax due, it would need to be claimed in a later year.

How we can help

This PTE Election is a little complicated, but it is worth the effort to explore. MGO’s state and local tax professionals can advise you on the numerous pass-through entity tax regimes being passed by states to counter the federal limitation on deducting state taxes. Our cumulative experience as SALT specialists can help you determine if you are able to benefit from pass-through entity taxes and how to appropriately use them. Reach out to our team of experienced practitioners for your state and local tax needs.

]]>Proactive tax planning during the M&A process is one of the key methods to drive value before, during, and after the transaction. In the cannabis and hemp industries, tax planning takes on a special importance due to the various regulatory concerns at the federal, state, and local levels and the overwhelming impact of IRC Section 280E.

In the simplest terms, the crux of tax discussions at the deal structure level are based on the competing interests of the Acquirer and the Target company’s owners – the former seeking to maximize future tax benefits, and the latter seeks to minimize or defer the tax liabilities relating to the gain from the transaction. In the following, we lay out the tax fundamentals guiding optimal value for both sides of an M&A transaction.

Target company tax classification

A key element to the discussion between the Acquirer and the Target’s owners is the tax classification of the Target company, since this affects a number of transaction structuring decisions. The most common tax classification types are the following:

C Corporation – This is the general form of a corporation. A C Corporation is taxed at the entity level. In addition, distributions to shareholders are typically subject to a second level of tax.

S Corporation – This is a corporation with an S Election. An S Corporation is generally treated as a passthrough entity for income tax purposes, although certain items may be subject to entity level taxation.

Partnership – A partnership is treated as a passthrough entity for income tax purposes. Taxation occurs at the partner level.

Disregarded (as separate from its tax owner) – All income is taxed to the tax owner of the disregarded entity. A common legal form for a disregarded entity is a single-member limited liability company (LLC).

Asset vs. stock acquisitions

This topic was addressed in our article focused on transaction structuring but represents such an essential touchstone that a more in-depth examination is warranted.

Broadly speaking there are two fundamental structures to an M&A transaction, each with its own tax implications: asset acquisition and stock acquisition.

Asset acquisition

The Acquirer purchases some or all of the Target’s assets. The Acquirer can also assume some, all, or none of the Target’s liabilities. (Note that certain successor liabilities can also transfer over.) Target may then either continue operations or liquidate following the transaction.

Tax Impact on Target/Target Owners:

C Corporation: Gain on the asset sale should be subject to tax at the entity level. In addition, any distributions of the proceeds from the transaction should generally be subject to a second level of taxation at the shareholder level.

S Corporation: Gain on the asset sale should typically be subject to tax at the shareholder level. However, certain built-in gains originating from a prior C Corporation conversion could be taxed at the entity level.

Partnership: Gain on the transaction should be subject to tax at the partner level.

Besides the general tax impact by entity type, there are also different classifications of the gain from the transaction:

- Capital Gain – This generally results from the sale of capital assets and assets used in a trade or business.

- Ordinary Gain – This can result from the sale of ordinary income assets (e.g., accounts receivable, inventory) and from depreciation recapture from previously depreciated assets. The amount of ordinary gain can have an effect on a number of tax attributes, as well as how much of a sale can be deferred through installment sale treatment. In addition, for Target Owners that are taxed on the gain as individuals, this gain can result in a higher effective tax rate than capital gain.

Tax Impact on Acquirer:

The Target’s assets that are acquired are typically stepped-up to fair market value, which may potentially generate additional depreciation and amortization deductions, subject to any Section 280E limitations.

Stock acquisition

An equity transaction involves the sale of equity by the Target company’s owners to the Acquirer. Generally, all assets and liabilities of the Target company are transferred in the process. This often includes the Target’s tax liabilities and uncertain tax positions (although there are certain exceptions for partnerships).

As such, the Acquirer may find itself liable for tax audit adjustments.

This is especially relevant in the cannabis industry, where Section 280E audits can result in significant tax liabilities. As part of the diligence process, Section 280E exposure should be identified and quantified. In addition, indemnifications, representation & warranties, and tax representation responsibilities should consider the impact of Section 280E.

Tax Impact on Target/Target Owners:

C Corporation: Gain on the equity sale should be subject to tax at the Target owner level, resulting in a single level of taxation. If the stock meets the qualifications for Qualified Small Business Stock and the requisite 5 year holding period is met (i.e., the Section 1202 exclusion), up to $10 million of the gain can be excluded by Target owners that are not corporations.

S Corporation: Gain on the equity sale should be subject to tax at the shareholder level. S Corporation shareholders do not qualify for the Section 1202 exclusion.

Partnership: Gain on the equity sale should be subject to tax at the partner level.

Usually, gain on the sale of an ownership interest is characterized as capital gain. This is especially important for individuals who have held the equity for more than a year, since they may qualify for preferential tax rates. However, note that partnerships with “hot assets” will have a portion of this gain recharacterized as ordinary gain.

Tax Impact on Acquirer:

An Acquirer purchasing a corporate Target’s stock does not obtain a step-up in the basis of Target, resulting in the Acquirer typically not being able to take the additional tax deductions described above for an asset purchase. However, depending on the circumstances, an IRC 338 election ((g) or (h)(10)) or an IRC 336(e) election may be available to treat the stock acquisition as an asset acquisition for US tax purposes. Tax modelling is often recommended to determine whether making such an election is advisable, especially considering that the election may result in adjustments to purchase price to reflect any additional tax costs or to reflect a premium for allowing the election.

An Acquirer purchasing a partnership Target’s equity also generally does not obtain a step-up in the basis in assets, unless a Section 754 election is in place or the Acquirer is acquiring 100% of the Target’s equity. As a result, a Section 754 election is often made in order to step-up the inside basis of the partnership’s assets to match the outside basis of the ownership interests held by the partners.

Tax attributes (e.g., net operating losses, credits) of the Target company transfer over in an equity transaction. However, they may be subject to limitations due to the ownership change (e.g., Section 382). As a result, a review of the availability of tax attributes post-transaction is often factored into the transaction structuring considerations.

Cash vs. stock vs. debt: the perfect storm of tax-free acquisitions

The other major determinant of the tax implications of an M&A equity deal is the form of consideration paid by the Acquirer. Consideration typically comes in some combination of cash, stock, or debt.

In the notably cash-poor cannabis and hemp industries, equity consideration is commonly used to lower the cash flow needs in M&A. However, the proliferation of distressed assets and over-extended operations have made debt assumptions an emerging and increasingly common form of consideration as well. Consequently, an Acquirer willing to pay in cash is relatively unique and brings significant advantage to the M&A negotiation table.

As the percentage of equity consideration in the transaction increases, the opportunity to have at least a portion of the transaction be tax-free also increases:

Corporations – The transaction may be able to be structured as a reorganization (and sometimes a contribution) if the equity consideration is at least 40%. This usually results in no gain recognition for the equity portion of the consideration. The cash/debt portion would still be taxable.

Partnership – The transaction may be able to be structured as a part-sale/part-contribution. This would result in the contribution portion being nontaxable (subject to certain exceptions).

Navigating tax credits

A thorough review of the potential tax benefits and credits available to a Target can influence the structure of an M&A deal and increase the appeal for the Acquirer. Tax credits and incentives in particular can result in significant tax savings. Even cannabis operators subject to Section 280E can qualify for significant credits and incentives at the state & local levels. For instance, cannabis operators have been able to qualify for job creation credits, social equity incentives, and reduced local tax rates.

International transactions

One final consideration to take into account with M&A is the potential for an international transaction. This can occur in a foreign “go public” transaction or an expansion into international operations. These types of deals add an additional (and possibly unfamiliar) layer of tax considerations to a deal structure. Often, US tax planners familiar with the US tax intricacies of the transaction coordinate with their foreign counterparts to iron out the details of the transaction to ensure that the transaction is tax efficient in all of the respective jurisdictions.

As part of an international transaction, some form of Acquirer structuring usually occurs in order to take advantage of various tax incentives (e.g., treaty benefits) while mitigating exposures such as Subpart F. This can be as simple as forming a new holding company and as complicated as a detailed international structure that considers IP placement, supply chain, and transfer pricing.

Final thoughts

Ultimately, any M&A deal will require careful tax planning to minimize tax burdens and maximize the value of the deal. As an important aspect of the M&A process, tax planning is one of the best ways to ensure that both sides of the transaction get the best deal possible.

Catch up on previous articles in this series and see what’s coming next…

]]>As the cannabis industry continues to evolve and mature, perhaps the single biggest obstacle to profitability remains: IRC Section 280E. By prohibiting expense deductions for businesses that produce, sell or distribute Schedule I and II substances, the Federal government is imposing an effective tax rate two to three times higher than traditional businesses.

While there has been no progress on 280E reform at the Federal level in 2020, legal decisions in recent years, such as the cases involving retailers Harborside Inc. and Alternative Health Care, have impacted the application of 280E and provided some clarity on what cannabis companies need to consider and prepare for with tax season on the horizon.

Extensive documentation is key to navigating 280E

The first rule of navigating 280E is that all cannabis businesses must document absolutely everything. If they don’t, then it is very, very unlikely that they will prevail during an audit or if they find themselves in Tax Court. Throughout the course of doing business, inventory and costs need to be diligently documented. By keeping thorough records, you strengthen your potential case, and at the very least may win some points for demonstrating “good faith” intent.

That is what happened in the Harborside case, where the Oakland-based company was hit with an $11 million IRS bill for back taxes from 2007 and 2012. In that case, Harborside had been comprehensive in its documentation and was able to substantiate all of its claims as it related to deductions. As a result, they were not assessed inaccuracy penalties and documentation played a role in lowering their debt owed.

Understanding Cost of Goods Sold and 280E

Another lesson from recent cases relates to calculating the Cost of Goods Sold (COGS), where a reduction is made during the process of calculating gross income. IRS regulation 471 states that if the usage of inventories is deemed necessary to determine a taxpayer’s income, then an inventory shall be taken by the best accounting practices in that trade. Per 471, there are different regulations whether a taxpayer is a reseller or a producer. For instance, for producers, inventory calculations should include the costs of raw materials and necessary indirect production costs.

In the Harborside case, the company claimed that for calculating COGS, IRC Section 263A was the correct approach. Under 263A, taxpayers are required to capitalize both direct and indirect costs related to actual personal property that it produces. Harborside argued that being disallowed from using 263A resulted in the company having to pay taxes on an amount in excess of their gross income.

The decision of the Court confirmed the IRS approach, dealing a blow to cannabis companies. Per the Court’s ruling, there were a number of aspects that impact the way cannabis can approach how they calculate COGS. Given the different approaches under 471 for those deemed either a “producer” or a “reseller,” companies need to understand how they will be classified, as it has a major impact on their accounting processes.

Tax structuring considerations for 280E

Another important aspect for cannabis retailers to consider is how they are structuring their business. In a case decided last year, Los Angeles-based Alternative Health Care tried to avoid 280E by having a management company operate its storefront. The management company was responsible for a number of critical day-to-day operations, such as paying employees. Given that Alternative Health Care wasn’t in charge of the storefront, it argued that it wasn’t subject to the tax laws of 280E. However, their argument lost in court and resulted in an expansion of the types of companies that are considered liable under 280E.

There may be a number of reasons why a cannabis retailer would want to avoid liability under 280E. But just because a management company is technically in charge, liability also extends to them. If a company is considering using a different company to handle its day-to-day business, there needs to be an understanding that 280E is still applicable and that trying to get around this can end up being costly.

There are many other benefits to structuring a cannabis company in a strategic way. It can allow specific business units to be utilized in a tax efficient manner and enhance a company’s ability to take advantage of special tax deductions. Additionally, a company can make bookkeeping much easier, while simultaneously reducing risks by separating certain business units. Structuring can also open up other opportunities down the line when it comes to joint ventures or shareholder investments.

Preparing for cannabis audits

Recent court decisions (and other rumors) have stoked fears that there will be an increase in audits of cannabis companies. There is no guarantee that there will be more audits or that a certain retailer will be audited in the next year. However, audits can happen, so it is paramount that a company protects itself in every way they possibly can.

Overall, it is always best to be prepared. As stated previously, document everything. Maintain all necessary paperwork. If you avoid being audited, there are many other benefits to appropriately documented financial and operational records. But if one crops up, you minimize the risk of potential penalties and create a much smoother process.

The bottom line on 280E

While changes to precedent and recent case developments have altered the 280E landscape, as the cannabis sector grows, and revenue numbers rise, greater attention is given to the industry by regulatory authorities. As a result, companies must make taking a strategic approach to 280E compliance a top priority.

]]>Details of California’s nexus law

California used the South Dakota law as a relative guide, where the threshold – or nexus – for collecting taxes by online retailers begins once sales reach $100,000 or 200 transactions in the state. California instructs retailers to begin collecting the 7.25% state tax on the sale of tangible personal property for delivery into the California once sales reach $500,000, but with no transaction threshold.

Furthermore, Special Notice L-591 was issued by the CDTFA to also take effect on April 1. This notice requires retailers to collect local use taxes once a threshold of $100,000 or 200 transactions has been reached within that locality or district, regardless of sales or transactions in another district within the state.

Another component of the new law addresses the sale of goods to California residents through platforms such as Amazon, eBay, Etsy and others, where the platform or “marketplace” facilitates the transaction. The marketplace facilitator must register as a seller with the CDTFA, collect sales tax on behalf of the seller, and remit the tax to the California tax department. This particular phase of the law is not scheduled to become effective until October 1, 2019.

Although the new California law will undoubtedly impact many online retailers, there is a provision that may provide some relief to smaller businesses. The temporary provision states that for businesses selling tangible personal property into California that is less than $1 million through the tax period ending December 31, 2022, taxes and fees may be waived by the CDFTA if the retailer registers with the state and was not required to do so prior to the law becoming effective.

More complications for retailers

It is estimated that anywhere from $1 billion to $2 billion of tax revenue went uncollected from out of state retailers and that the new law could provide an additional $500 million in tax revenue to the state.

Much of this depends on how simple California makes the tracking, reporting and payment of tax revenue by online retailers. While the collection of revenue based on a single, state-wide tax rate might be simple enough, the additional district taxes may potentially add complexity to the issue, making it more difficult to collect. Some states are offering allowances when retailers use automated tax software to track and collect taxes and not holding the retailer accountable if mistakes are made due to the software. This may be relatively easy at the state level but difficult at the district level, as every address must adhere to the latest zoning requirements for specific districts while also ensuring alignment according to the tax software being used.

What consumers must understand

For consumers in California, there may not be a significant change in the rate in which they buy online, as many are already paying sales tax on goods purchased this way. Any concern consumers have regarding a revoking of the Internet Tax Freedom Act (ITFA) should be alleviated, as the ITFA only prohibits states from levying tax on internet access, not the sale of tangible personal property.

It is likely that California will see additional tax revenue with the implementation of this new law. How much revenue will remain to be seen, especially with the $500,000 threshold as well as the provisional leniency for smaller businesses until 2022.

]]>