- In April, the U.S. Tax Court made news when it ruled in favor of businessman Alon Farhy, who challenged the Internal Revenue Service (IRS)’s authority to assess penalties for the failure to file IRS Form 5471.

- IRS Form 5471 is the Information Return of U.S. Persons With Respect to Certain Foreign Corporations.

- Taxpayers may be interested in filing protective refunds, and they should start the process sooner rather than later—there is a statute of limitations of two years for claiming refunds.

- This case’s ruling could have reverberating effects when it comes to the IRS collecting additional penalties, but only time will tell.

On April 3, 2023, the U.S. Tax Court came to a decision in the case Farhy v. Commissioner, ruling that the Internal Revenue Service (IRS) does not have the statutory authority to assess penalties for the failure to file IRS Form 5471, or the Information Return of U.S. Persons With Respect to Certain Foreign Corporations, against taxpayers. It also ruled that the IRS cannot administratively collect such penalties via levy.

Now that the IRS doesn’t have the authority to assess certain foreign information return penalties according to the court, affected taxpayers may want to file protective refund claims, even if the case goes to appeals — especially given the short statute of limitations of two years for claiming refunds.

Our Tax Controversy team breaks down the Farhy case, as well as what it may mean for your international filings — and the future of the IRS’s penalty collections.

The case

Alon Farhy owned 100% of a Belize corporation from 2003 until 2010, as well as 100% of another Belize corporation from 2005 until 2010. He admitted he participated in an illegal scheme to reduce his income tax and gained immunity from prosecution. However, throughout the time of his ownership of these two companies, he was required to file IRS Forms 5471 for both — but he didn’t.

The IRS then mailed him a notice in February 2016, alerting him of his failure to file. He still didn’t file, and in November 2018, he assessed $10,000 per failure to file, per year — plus a continuation penalty of $50,000 for each year he failed to file. The IRS determined his failures to file were deliberate, and so the penalties were met with the appropriate approval within the IRS.

Farhy didn’t dispute that he didn’t file. He also didn’t deny he failed to pay. Instead, he challenged the IRS’s legal authority to assess IRC section 6038 penalties.

The court’s ruling

The U.S. Tax Court then held that Congress authorized the assessment for a variety of penalties — namely, those found in subchapter B of chapter 68 of subtitle F — but not for those penalties under IRC sections 6038(b)(1) and (2), which apply to Form 5471. Because these penalties were not assessable, the court decided the IRS was prohibited from proceeding with collection, and the only way the IRS can pursue collection of the taxpayer’s penalties was by 28 U.S.C. Sec. 2461(a) — which allows recovery of any penalty by civil court action.

How this court decision affects your international penalty assessments

This case holds that the IRS may not assess penalties under IRC section 6038(b), or failure to file IRS Form 5471. The case’s ruling doesn’t mean you don’t have an obligation to file IRS Form 5471 — or any other required form.

Ultimately, this decision is expected to have a broad reach and will affect most IRS Form 5471 filers, namely category 1, 4, and 5 filers (but not category 2 and 3 filers, who are subject to penalties under IRC section 6679).

However, the case’s impact could permeate even deeper. For years, some practitioners have spoken out against the IRS’s systemic assessment of international information return (IIR) penalties after a return is filed late, making it impossible for taxpayers to avoid deficiency procedures. The court’s decision now reveals how a taxpayer can be protected by the judicial branch when something is deemed unfair. Farhy took a stand, challenged the system, and won — opening the door for potential challenges in the future.

It’s uncertain as to whether the IRS will appeal the court’s decision. But it seems as though the stakes are too high for the IRS not to appeal. While we don’t know what will happen, a former IRS official has stated he expects that, for cases currently pending review by IRS Appeals, Farhy will not be viewed as controlling law yet.

The impact of the ruling is clear and will most likely impact many taxpayers who are contesting — or who have already paid — IRC 6038 penalties. It may also affect other civil penalties where Congress has not prescribed the method of assessment in the future.

How you should respond to the court’s decision

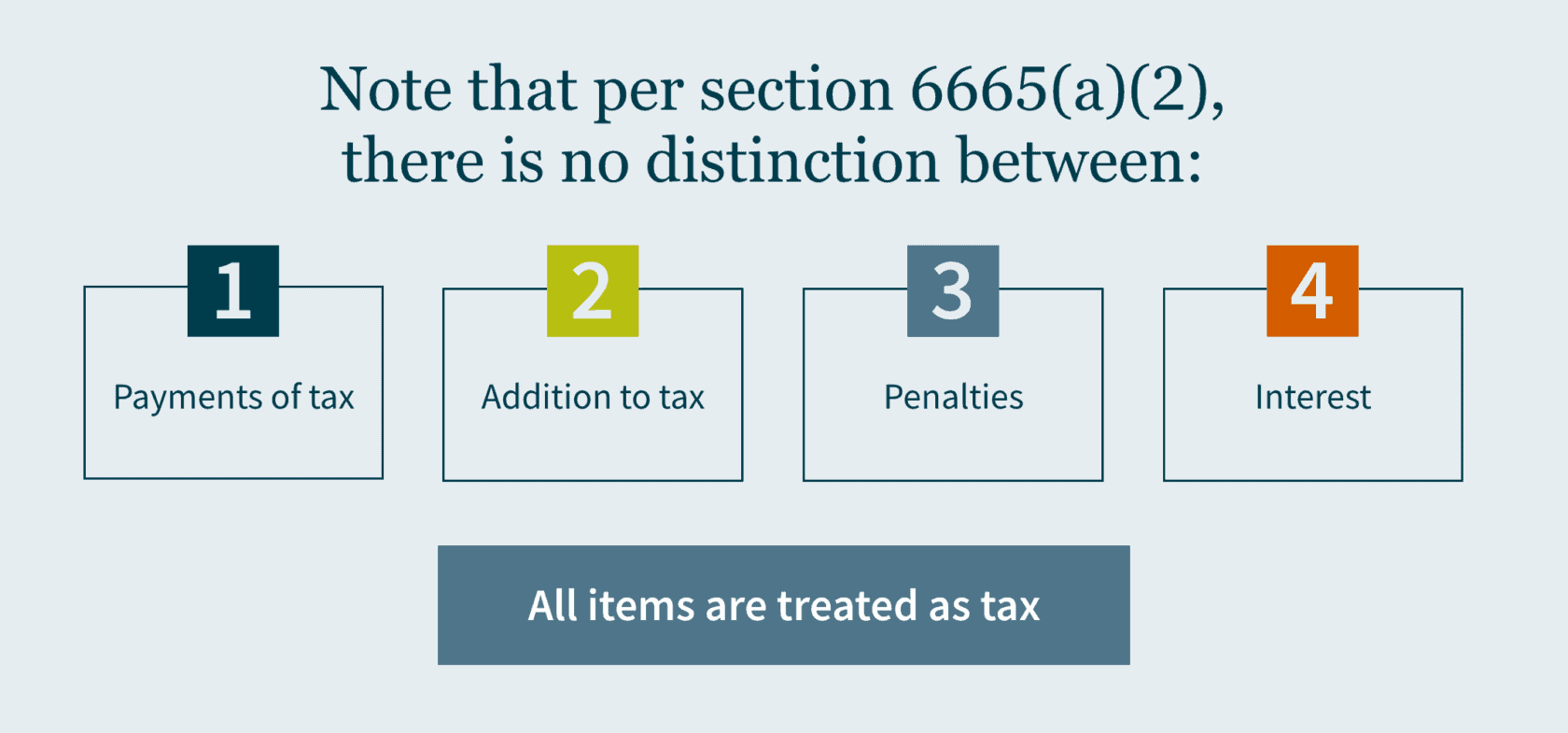

You should move quickly to take advantage of the court’s decision, as there is a two-year statute of limitations from the time a tax is paid to make a protective claim for a refund. It’s likely this legislation wouldn’t affect refund claims since that would be governed by the law that existed when the penalties were assessed. Note that per IRC section 6665(a)(2), there is no distinction between payments of tax, addition to tax, penalties, or interest — so all items are treated as tax.

If you’ve previously paid the $10,000 penalty, it’s important to file your protective claim now, unless you’ve entered into an agreement with the IRS to extend the statute of limitations, which can occur during an examination. Requesting a refund won’t ever hurt, but some practitioners believe the IRS may try to keep any penalty money it collected, even if the assessment is invalid— because, in its eyes, the claim may not be. Just know, you can file your protective claim for a refund but may not get it, at least not any time soon.

The Farhy decision could likewise be applied to other US IRS forms, such as 5472, 8865, 8938, 926, 8858, 8854, and some argue the Farhy decision may also be applied to IRS Form 3520.

How MGO can help

Only time will tell if the court’s decision will open the government up to additional criticisms for other penalty assessments. If you have paid your penalties and are wondering what your current options are, MGO’s experienced International Tax team can help you determine if you’re eligible to file a refund claim.

Contact us to learn more.

]]>

- California Governor Newsom strives to amend the personal income tax laws to prevent wealthy taxpayers from utilizing Incomplete Gift Non-Grantor trusts.

- California residents use this by transferring assets into trusts held by nonresident trustees in states without income tax.

- If this legislation passes, taxpayers will no longer be able to take advantage of the strategy.

If you reduce California income tax with an ING, Newsom is onto you

Californian legislators propose to amend the personal income tax laws to close a little-known-but-effective loophole for the wealthy by targeting Incomplete Gift Non-Grantor (ING) trusts set up in other states with more favorable income tax rules. To date, California residents have had the opportunity to transfer assets into these trusts held by nonresident trustees in states without income tax, utilizing the state’s sourcing rules to avoid the tax. If approved, this new legislation will put a stop to this tax planning strategy.

Taxing the rich in California

As it stands, the ING trust is not commonly used. There are about 1,500 California residents with this trust in states without income tax — and if implemented, California would see a minimal revenue increase (about $30 million in the first year and $15 million in the following years). However, this would put an end to a tax planning strategy the wealthy have been using to their benefit for about 20 years.

Because California is home to more billionaires than any other state at the same time as it also has the highest rate of poverty in the U.S., the concept of taxing the rich holds a certain appeal. In the past, Newsom has opposed proposals to raise taxes — but this proposal was included in the governor’s $223.6 billion budget plan for the next fiscal year, which begins in July. Whether the item survives the legislative process remains to be seen, but if New York’s passage of a similar law in 2014 is any indication, we are likely to see the end of this tax planning strategy for California’s ultra-rich.

Moreover, this proposal has a retroactive element, differentiating it from New York’s and opening it up to potential lawsuits (New York trust holders had a five-month period to move their accounts to a different type of trust without incurring the tax). Newsom is pushing for the measure to begin the calendar year after its implementation.

How the ING works (worked)

What is an ING, and why is Newsom trying to prevent its use? California taxpayers can transfer their assets into out-of-state, incomplete, non-grantor trusts (INGs), which constitute separate, taxable entities under state and federal tax law, and this move avoids California income tax on any appreciation or gains from those assets because it is “sourced” to another state based on the location of the trustee (i.e., the bank or whatever financial institution offers the trustee services in the other state). The non-grantor aspect comes into play when the taxpayer establishing the trust (the “grantor”) gives up control over managing investments or distributing assets to the trustee (contrast with a “grantor trust” in which the grantor continues to control how money is invested/distributed within the trust during their lifetime). For the trust to be deemed “incomplete,” the grantors specify how the money can be used.

Some of the states where these trusts are typically established include Florida, Wyoming, Delaware, Nevada, Tennessee, and South Dakota. For example, a California resident (TP) may decide to transfer stock in their business into an ING established in South Dakota. If TP held the stock directly, then as a resident, all the dividends (or if he sold it, the gain) would be taxable by California on their personal income tax return. But since TP doesn’t hold the asset – the ING does – the ING recognizes the income relating to the stock. California’s current rules provide that the income is sourced to (and thus taxable in) the state where the trustee is domiciled, and for this ING that location is South Dakota, which, incidentally, does not tax this sort of income.

Newsom is hoping that by eliminating this tax-free option, the state of California will be able to increase tax revenue in a way that will not alienate a large number of voters.

How MGO can help

If you are a California resident and currently use an ING as a tax strategy, there are steps to take now to avoid a negative impact. MGO’s experienced Private Client Services team can help you identify and implement an effective response.

]]>The tax relief postpones tax filing and payment deadlines occurring between January 8, 2023, and May 15, 2023, to a new due date of October 15, 2023.

Some of the filings and payments postponed include:

- Individual income tax returns due on April 18

- Business tax returns normally due on March 15 and April 18

- 2022 contributions to IRAs and health savings accounts

- Quarterly estimated tax payments normally due January 17 and April 18

- Quarterly payroll and excise tax returns normally due on January 31 and April 30

The current list of counties that qualify for this relief can be found here.

If you qualify for this postponement, you generally do not need to contact the IRS or FTB to obtain relief. Relief is automatically granted for affected taxpayers who have an address of record located in one of the designated counties. However, if you still receive a late filing or late payment notice and the notice shows the original or extended filing, payment, or deposit due date falling within the postponement period, you should call the number on the notice to have the penalty abated.

If you have questions or need assistance, contact MGO’s experienced State and Local Tax team.

]]>Here’s are some of its biggest changes we think our New York clients should be aware of.

$1 M Economic Nexus Threshold for New York City Business Corporation Tax (BTC)

The City now conforms to New York State (NYS) franchise tax rules by utilizing a bright-line, economic nexus standard (i.e., a non-resident business may be subject to tax based solely on receipts derived from activity in New York). Those companies deriving $1 million or more in receipts will create nexus for purposes of the BTC (also corporations with less than $1 million, but at least $10,000 from NYC, will have nexus if they are part of a unitary group that has at least $1 million in NYC receipts). This new law emulates New York State’s “deriving receipts” language.

Those corporations filing in the state of New York (not NYC) should review any NYC activity they have to determine if they have nexus with NYC under the new requirements. And any corporate partners of partnerships that have nexus with the City should verify if they have new NYC filing requirements to attend to.

New York City Pass Through-Entity Tax (NYC PTET) Available in 2022

This allows eligible taxpayers (partnerships and subchapter S corporations) to elect to pay this entity-level income tax for 2022 (previously intended to take effect for 2023 tax year). The deadline to pay tax and make the election for the 2022 tax year is March 15, 2023.) Note: this tax is separate from NYS’ PTET, for which the deadline was not only extended but the amount of benefit for resident S corporations was increased — read more about those updates here.

Tax Relief from Receipt of COVID-related Grants

This provides a guide for the exclusion of income for New York City tax purposes, including NYC’s Small Business Resilience Grant Program and the COVID-19 Small Business Recovery Grant Program.

It is also worth noting the governor has also recently announced a first-in-the-nation Seed Funding Grant Program, which provides grants to support early stage, micro and small businesses in a recovering NY economy so they can continue to grow and operate.

MGO can help

If you have questions about other aspects of the new bill, contact our experienced State and Local Tax team.

]]>Specific scams that mask as abusive or fraudulent tax avoidance strategies to be aware of include concealing assets in offshore accounts and improper reporting of digital assets, manipulation of high-income taxpayers to file their tax returns, abusive syndicated conservation easements, and abusive micro-captive insurance arrangements. Read more to round out the annual list for the 2022 filing season.

Tips for taxpayers on emerging scams

To avoid compromising yourself with these “too good to be true” schemes, taxpayers should stay wary, as these scams adopt a wide range of communication methods, including:

- Emails

- Phone calls

- Social media posts

- Targeted online advertisements

You must also consider each source before putting any of these arrangements on your tax returns — because ultimately, you are the one responsible for what is on the return, not the promoter who reached out to you and made a promise they failed to uphold. To mitigate risk, an anxious taxpayer should turn to trustworthy tax professionals to assist with their returns.

Read on to learn about these Dirty Dozen scams targeted primarily to high-net-worth individuals who may be trying to knowingly — or unknowingly — avoid filing.

Scam #9: Concealing Assets in Offshore Accounts and the Improper Reporting of Digital Assets

We hear Switzerland is beautiful this time of year … and so do some high-net-worth individuals looking to conceal their assets in offshore accounts (and yes, that does include cryptocurrency and other digital assets). As more taxpayers look to complex international tax avoidance schemes, the IRS is more determined than ever to “protect the integrity of the U.S. tax system” by enforcing tax responsibilities.

Whether it entails offshore banks, brokerage accounts, nominee entities, employee leasing schemes, foreign trusts, structured transactions, or private annuities, all are designed to hide the true owner of an account — which is illegal, considering U.S. taxpayers are taxed on all the income they make, not just what they keep in the country. But scammers know you may not want to give up some of your hard-earned assets to Uncle Sam. So, what do they do? They sell you a convincing story: you can easily evade the government and hide your assets through digital asset holdings; they claim these are “undetectable by tax authorities.” The catch? They are definitely detectable. By believing these fraudsters, you run the risk of being criminally charged or penalized, so in the end, it is better to report your assets — yes, all of them — when you file.

Scam #10: High-Income Individuals Who Don’t File Tax Returns

Believe it or not, there are some taxpayers who choose to just … not file a tax return. And believe it or not, there are scamming professionals out there aiming to convince you this is a good idea. The IRS takes this seriously. If you are considering this option, remember the Failure to File Penalty is higher than the Failure to Pay Penalty, meaning you are better off filing an accurate, timely return (and setting up a payment plan, if you are concerned about that) rather than not filing and hoping you get out of paying whatever taxes you owe.

Scam #11: Abusive Syndicated Conservation Easements

In this scam, dishonest promoters manipulate a part of the tax law that allows for conservation easements by inflating appraisals of underdeveloped land (i.e., the guise of a real estate investment) and engaging in bogus partnerships without a business purpose. These “deals” rarely help you out; instead, they benefit the promoters, who charge high fees, and clog the tax system with fraudulent tax deductions. (In the last five years, the IRS determined billions of dollars of deductions were wrongly claimed!) And if you are caught — which, you should expect to be, because the IRS takes a microscope to every single one of these “deals” — you can expect large fines and potential time in court.

Scam #12: Abusive Micro-Captive Insurance Arrangements

A high priority for the IRS, this scam sees professionals like accountants and wealth planners convince entity owners to pay for what they believe to be insurance coverage against unlikely events, events that are already being covered, or disingenuous business needs. Complete with sky-high premiums, the abusive structure does the opposite of protecting your organization’s tax safety — it opens you up to more risk as a ”micro-captive” to these “professionals” taking advantage of you. Be on the lookout for an offshore version of this too.

Consequences of falling for a Dirty Dozen scheme

It is important for taxpayers who have already taken part in transactions like these — or those who are thinking about doing so — to consult a tax professional before claiming any tax benefits they think they are owed.

Those taxpayers who have already claimed the purported tax benefits of one of these four “Dirty Dozen” arrangements on a tax return should file an amended return and go to an independent professional for guidance. If necessary, the IRS will examine the tax benefits from transactions like the ones depicted in the list and inflict penalties related to accuracy ranging from 20% to 40%, or a civil fraud penalty of 75% on any taxpayer who underpaid.

Our perspective on the latest batch of “Dirty Dozen” scams

This is not, of course, an exhaustive list of every scam the IRS has its eye on this year. But it does include some of the more common trends. The best advice we can give? If something looks too good to be true … it probably is. Consult your tax professional for guidance and know that it is in your best interest to stay aware of these nefarious arrangements, so you do not fall susceptible to additional penalties.

And remember, you cannot hide income from the IRS!

MGO’s Tax team brings more than 30 years of experience and is well versed in reviewing your return for compliance. We also stay up to date on the risks, pitfalls, and warnings issued by the IRS so you don’t have to. If you think you have been involved in or are in the process of being involved in one of the Dirty Dozen scams, we can help. Contact us today.

]]>To read more about how California’s PTET works from our Insight Library, see here and here.

California’s PTET considerations

To make the election in California for tax year 2022, eligible entities must pay in the greater of $1,000, or 50% of the 2021 PTET liability, by June 15, using FTB 3893. Entities that fail to make this “safe harbor” payment will not be able to make the election on the 2022 tax return. (Note: The election can only be made on an entity’s timely filed original tax return.)

New York extends its 2022 PTET deadline

Previously, the deadline for making the 2022 election was March 15, 2022, but recent legislation not only extended the deadline but also increased the amount of benefit for resident S corporations. Under the prior legislation S corps could only make the election as to the portion of income that is sourced to NY; however, new legislation (A10080/S8948) enables S corporations, for which all owners are New York residents, to include income from all sources, which has the effect of increasing the amount of available credit on the individual owners’ returns. And because these rules went into effect after the PTET election due date for tax year 2022, New York extended its PTET election deadlines for all taxpayers. Now, passthrough entities can make their PTET election any time by or before September 15, 2022.

Accompanying the deadline extension is a new schedule of estimated payments, contingent on when the eligible entity makes the election. Taxpayers must still pay the entire amount of estimated PTET liability by the end of the year (90% of the PTET shown on the entity’s return for the taxable year; or 100% of the PTET shown on the preceding year’s return). However, instead of owing 25% each quarter (March 15, June 15, September 15, and December 15), taxpayers that make the election prior to June 15, 2022, only need to pay an amount equal to 25% of the required annual PTET liability by June 15, followed by 50% due in September, and the remaining 25% by December 15. And taxpayers that make the election after June 15 but before September 15, must submit a payment equal to 50% of the annual liability by September 15, with the other 50% due December 15.

You can find links here to make the election and submit payments online.

MGO’s insights

If you missed making the CA election on the 2021 return, the silver lining is that you can now “lock in” eligibility with a payment of only $1,000 on June 15, regardless of the amount of taxable income the entity ultimately reports. If you did make the election on the 2021 return, be sure to pay at least 50% of prior year liability (and consider adding a cushion for good measure), as there does not appear to be a “reasonable cause” exception to the rule.

And remember, most tax professionals have interpreted IRS Notice 2020-75 to allow the entity only to claim a deduction for the expenses actually incurred during the applicable tax year — regardless of whether the entity is on a cash or accrual basis accounting method. This means that if you intend to experience the full benefit of a state’s SALT Cap Workaround on your 2022 tax return, you will need to submit the full amount of PTET liability before the end of the year. Amounts paid after the end of the year but before the return deadline (March 15, for most taxpayers) will be deducted on the following year’s federal tax return regardless of when they are credited to state tax liability.

Thus, if the entity made the election in 2021 and paid the PTET before December 31, 2021, then it should (or should have already) claimed the entire amount of PTET credit as an ordinary expense deduction on its tax return (and reported on the owners’ K-1s, generally, line 13). But if the payment was submitted between January 1 and March 15, 2022, that payment, plus the upcoming payments, will be deducted on the 2022 return alongside the other payments made during the tax year.

Final perspectives

To take advantage of the 2022 CA and NY SALT Cap workarounds, make sure to submit your payment by June 15, 2022 for the California PTET, and your election and any necessary payments by September 15, 2022 for the New York PTET.

Only state PTET payments made during the entity’s fiscal tax year are deductible on that year’s federal tax return, so in addition to meeting the state’s minimum estimated tax requirements to ensure eligibility, consider making grossed-up estimated payments before year end to maximize the economic effect of the deduction on the 2022 return.

The PTET rules are different in every state, and with a near-constant stream of amendments and clarifications from state legislators and tax agencies, you may be unsure what is due when. MGO’s tax team can provide you with reminders for payment submission deadlines and calculate amounts due to help you navigate this opportunity for tax savings.

Please get in touch and see how New York, California, or another state’s PTET can benefit your business.

]]>The SEEF tax rate is $1.10 per ounce of adult-use cannabis sold. New Jersey cultivators must also file the SF-100 monthly tax return to report the amount of usable ounces sold for the adult-use market (even if no sales or transfers of cannabis occur).

This first SEEF payment will cover less than two weeks of the sales made from the start date on March 18, 2022. Moving forward, the SEEF payment is always due by 11:59 p.m. on the 20th day of the month after the end of the previous filing period. If the due date falls on a weekend or legal holiday, the return and payment are due the following business day.

Letters with instructions for making the tax filings were sent out to the licensees in early May.

Some technicalities to keep in mind as you prepare to file:

- Medical cannabis is NOT subject to SEEF.

- SEEF is solely imposed on the Cultivator and is not due again on sales from manufacturers, processors, or retailer sales.

- It will not be paid again at another license level, regardless of whether the cannabis is later for sale as-is or if it has been converted to edible form.

- All cannabis types and categories are subject to the same SEEF rate when sold by a cultivator, no matter the strain, potency, trim or shake — anything that falls under the definition of “usable” cannabis.

In addition to the SEEF, NJ Cannabis operators will also need to contend with sales taxes and locally imposed gross receipts taxes:

- Retail sales of recreational cannabis are subject to the state’s ordinary sales tax under N.J.S.A. 54:32B-3(a). Sales of medical cannabis are not subject to sales tax, but are subject to a special 2% tax until the end of June.

- Depending on the locality, cannabis operators may be subject to the following gross receipts tax rates:

- Cultivation, Manufacturer, Retail – 2%

- Wholesale (Distribution) – 1%

- Returns are generally due quarterly in April, July, October, and January.

If you have any questions about calculating or paying NJ cannabis taxes, or any other state’s cannabis tax, please reach out to our leading cannabis tax practice.

]]>Specifically, under SB 113:

- Businesses will be able to fully utilize NOLs and R&D credits for the tax year 2022.

- There will be expanded eligibility and application of California’s Pass-through Entity Elective Tax (PEET) through several new provisions:

- Qualified net income now includes guaranteed payments.

- MGO Insight: This will significantly increase the value of the PEET for owners/operators of pass-through service providers.

- Individual taxpayers can apply the PEET state credit against tentative minimum tax.

- MGO Insight: By removing the 7% tentative minimum tax threshold, more of the PEET credit can be used in a given year, resulting in less carryovers and less concerns about electing into the PEET in consecutive years.

- Passthrough entities with owners that are partnerships are now eligible to make the PEET election.

- SMLLCs that are pass-through entity owners can now claim the PEET credit.

- MGO Insight: By removing the limitation on partnership owners and SMLLCs, more pass-through businesses will be able to benefit from the PEET including lower-tier partnerships.

- New credit usage ordering rules increase the benefit for taxpayers that claim the Other State Tax (OST) Credit.

- MGO Insight: OST credits are now specifically utilized before PEET credits, which should significantly reduce credit leakage for taxpayers with income in multiple states. (Prior to this, there was ambiguity on the ordering of credits and concerns that certain OST credits would not be able to be fully utilized.)

- The law also includes some beneficial retroactive relief:

- California will fully conform to the federal treatment of Restaurant Revitalization grants, retroactive to the 2020 tax year, and partially conform to the federal exclusion of Shuttered Venue Operator grants, retroactive to the 2020 tax year.

- Producers of qualified motion pictures benefit from increased flexibility to use sales & use tax credits against income taxes and sales & use tax; the prohibition period for this benefit has been shortened to only the 2020 and 2021 tax years. In addition, certain producers will have the ability to obtain an immediate refund for the 2021 tax year on sales & use tax in excess of the $5 million cap.

In addition to the tax benefits signed into law by SB 113, Gov. Newsom also signed SB 114, which creates COVID leave rules for 2022 that should benefit California workers:

- Employers with more than 25 employees will be required to provide up to 80 hours of COVID-19-related paid supplemental sick and family leave for the period January 1, 2022 (retroactive) through September 30, 2022. No additional tax benefits or credits have been provided in relation to this additional requirement.

With higher-than-anticipated tax revenues during the COVID pandemic, California improved the availability of various tax benefits, resulting in significant potential tax savings for California taxpayers in 2022 and later tax years that should help boost the state’s economic recovery.

]]>Early termination of the Employee Retention Credit

The IIJA terminates the Employee Retention Credit (ERC) created by the CARES Act earlier than originally planned. The American Rescue Plan Act (ARPA) had extended the credit to eligible employers for the third and fourth quarters of 2021. Under the new law, the ERC — which for 2021 is worth up to $7,000 per qualifying employee per quarter — is no longer available for wages paid after September 30, 2021 (rather than December 31, 2021), except for so-called “recovery startup businesses.”

The ARPA generally defines recovery startup businesses as those that began operating after February 15, 2020, and have annual gross receipts for the three previous tax years of less than or equal to $1 million. These employers can claim the ERC for up to $50,000 total per quarter for the third and fourth quarters of 2021, without showing suspended operations or reduced receipts.

However, clients can still file retractive amendments to claim credits missed (seek refunds) for Q1 – Q4 2020 and Q1 – Q3 2021.

New information reporting on digital assets

The IIJA requires brokers to report to the IRS the cost basis of digital assets transferred by their clients to nonbrokers, similar to how securities brokers report stock and bond trades. “Digital assets” are defined as “any digital representation of value which is recorded on a cryptographically secured distributed ledger or any similar technology.” This definition could ensnare not only cryptocurrencies like Bitcoin and Ethereum, but also certain nonfungible tokens (NFTs). The IIJA expands the definition of the term “broker” to include those who operate trading platforms for digital assets, such as cryptocurrency exchanges.

In addition, the IIJA modifies existing tax law to redefine “cash” subject to reporting to include “any digital representation of value”. As a result, individuals engaged in a trade or business must submit IRS Form 8300, “Report of Cash Payments Over $10,000 Received in a Trade or Business,” when they receive such amounts in one transaction or multiple related transactions.

The digital assets provisions take effect for returns required to be filed, and statements required to be furnished, after December 31, 2023. The IRS is expected to provide guidance before that time, but some businesses may find that accepting cryptocurrencies for payment isn’t worth the reporting burden.

Miscellaneous tax provisions

The IIJA extends several excise taxes used to fund highway spending, extends and modifies certain Superfund excise taxes, and allows private activity bonds for qualified broadband projects and carbon dioxide capture facilities. It extends pension funding relief and expands certain IRS administrative relief for taxpayers affected by federally declared disasters and “significant fires.”

More to come

The majority of the Democrats’ proposed tax law changes, to the extent they survive ongoing negotiations, will be included in the Build Back Better Act (BBBA). The BBBA could, for example, have significant provisions regarding the child tax credit, the cap on the state and local tax deduction, and limits on the business interest expense deduction. We’ll keep you current on the developments that could affect both your personal and business’s bottom lines.

]]>California’s workaround is in effect for the 2021 tax year and will continue to be available through the 2025 tax year (although it could expire earlier if the federal $10,000 limitation is repealed by Congress prior to its current sunset date of January 1, 2026).

The state tax credit, which is nonrefundable, can be carried over for five years. Nonresidents and part-year residents do not have to prorate the credit to account for their non-California income.

How to elect

California’s workaround is available for partnerships (including those structured as LLCs) and S corporations that only have individuals, trusts, estates, and/or corporations as owners. Publicly traded partnerships, partnerships owned by other partnerships, members of a combined reporting group, and disregarded entities do not qualify. (Disregarded Single-Member LLCs are not eligible to make the election, but will not make the entity ineligible if they are an owner of an otherwise eligible PTE).

Not all the owners of the pass-through entity need to consent to the election. Those that do not consent are not included in the calculation of the PTE Tax. To take advantage of the workaround, the pass-through entity needs to make the election annually on its state tax return. In addition, payments towards the PTE Tax need to be made by specified due dates.

• For the 2021 tax year, 100% of the PTE Tax needs to be paid by the due date for the pass-through entity’s state tax return without extensions – March 15, 2022.

• In later years, the PTE tax needs to be paid in two installments: the first installment is due by June 15 of the tax year for which the election is being made, and the second installment is due by the due date for the pass-through entity’s state tax return for that tax year without extensions (i.e., the following March 15). The minimum amount for the first installment is $1,000.

What to consider

The biggest benefit to the owners of a pass-through entity is the ability to claim a federal tax deduction for their share of the pass-through entity’s state income tax paid to California, but there is another potential benefit. In future years (starting with the 2022 tax year) PTE Tax payments may create some “float” for the owners in terms of the timing and amount of their individual estimated tax payments:

- Individuals in California need to pay 70% of their estimated tax liability through quarterly payments on April 15 and June 15, while the PTE Tax only requires that one installment of 50% of the total tax be paid in by June 15.

- Individuals in California need to pay the remaining 30% of their estimated tax liability by January 15 of the following year (i.e., the 4th quarter payment), while the PTE Tax only requires the remaining 50% be paid in by March 15.

However, despite these benefits, other factors should be considered before making the election:

- If the pass-through entity provides most of the income for an owner and that owner’s top California tax rate is less than or equal to 9.3%, the state tax credit cannot be used in full before it expires. On the other hand, since the election is made annually, you could avoid accruing too much carryover by opting not to elect in a following year.

- It’s unclear how California’s workaround will interact with pass-through entity tax regimes enacted by other states, especially their associated state tax credits. California provides credits against most other states’ taxes, but guidance has not been provided to indicate that it will afford the same treatment to other state PTE Taxes paid. Multi-state operators may not be able to reduce California taxable income by the amounts of other states’ similar taxes.

- The 9.3% flat rate may not be sufficient to cover the full tax liability for higher income owners.

- The PTE tax credit does not reduce the amount of tax due below California’s Tentative Minimum Tax (TMT), and thus may not be as beneficial for taxpayers subject to the TMT.

- There are considerations pertaining to cash management, since the pass-through entity would be paying the PTE Tax, not the owners.

- Non-resident withholding (7% for individuals) is not offset by the withholding requirements for the PTE Election. Non-resident taxpayers making the election would therefore be required to pay in tax at 16.3% among the quarterly and bi-annual installments, then claim a refund up to the amount of the 7% withholding. But because the 9.3% PTE Tax is non-refundable, to the extent that withholding exceeds tax due, it would need to be claimed in a later year.

How we can help

This PTE Election is a little complicated, but it is worth the effort to explore. MGO’s state and local tax professionals can advise you on the numerous pass-through entity tax regimes being passed by states to counter the federal limitation on deducting state taxes. Our cumulative experience as SALT specialists can help you determine if you are able to benefit from pass-through entity taxes and how to appropriately use them. Reach out to our team of experienced practitioners for your state and local tax needs.

]]>