- Name, image, and likeness (NIL) deals offer athletes exciting opportunities, but also potential pitfalls if not approached strategically.

- Athletes should educate themselves on taxes, carefully review contracts, and budget with long-term security in mind.

- With guidance on financial obligations, agreements, and smart money management, athletes can maximize NIL benefits while safeguarding their futures.

~

You are a talented young athlete with a growing public profile. You’ve just been offered a Name, Image, and Likeness (NIL) deal, an opportunity that can put some extra money in your pocket or even, in some cases, make a more profound impact on your financial life. It’s an exhilarating time, but it’s also crucial to approach this new chapter with the right knowledge and mindset.

Whether you’re a college or high-school athlete, or the trusted advisor to a young athlete, here are the three most critical actions you should take to avoid common financial pitfalls associated with NIL deals.

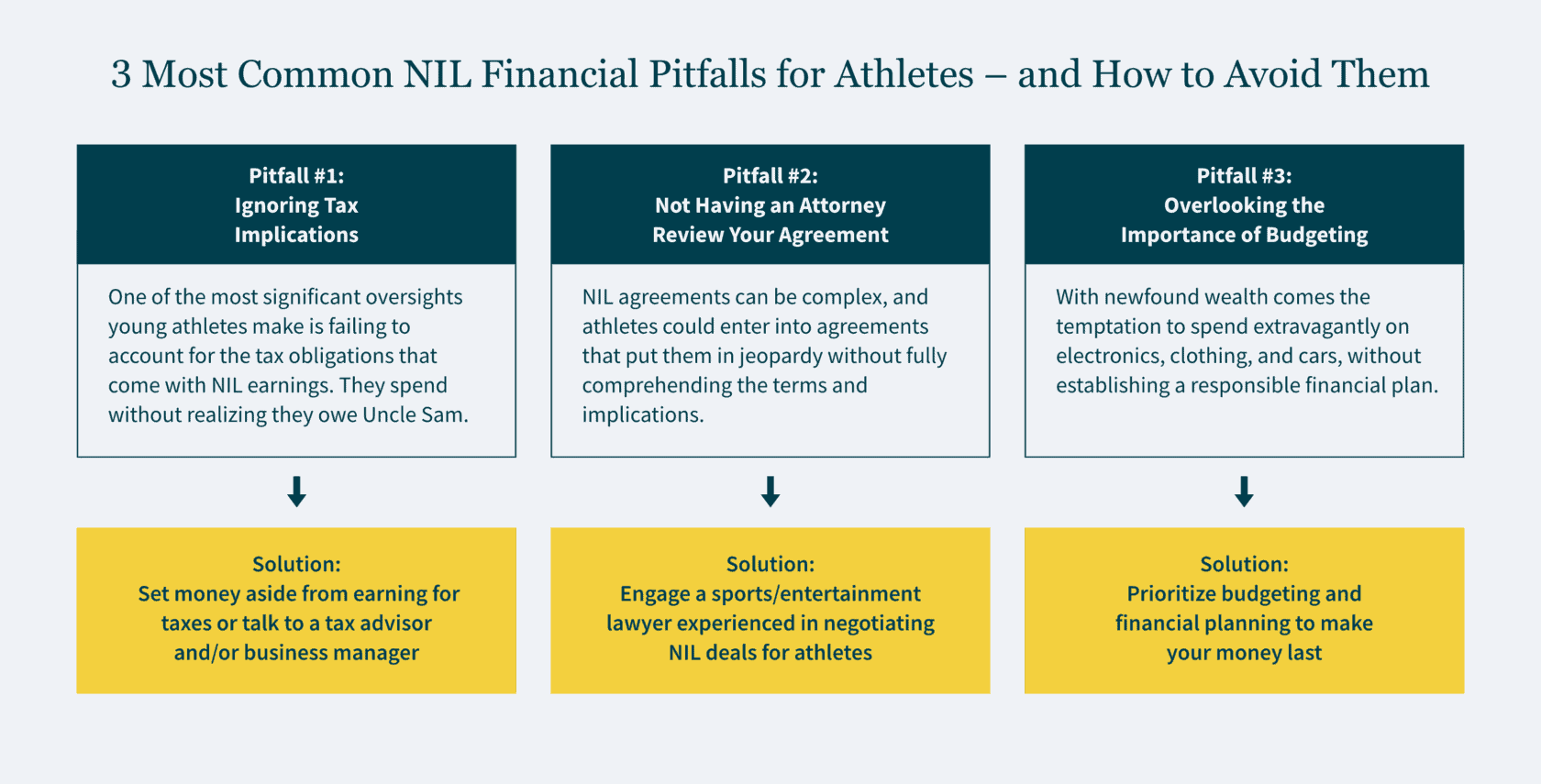

1. Recognize Your Tax Obligation

One of the first hurdles you’ll encounter in the world of NIL deals is taxes. It’s essential to understand that the money you earn from these deals is subject to taxation. Many young athletes overlook this, often because they’ve never had to deal with taxes before.

To avoid potential financial trouble down the road, consider these steps:

- Educate Yourself: Young athletes receiving payments from NIL deals are responsible for paying taxes on that income just like professional athletes. Take the time to learn about taxes, especially how they apply to your earnings. Understanding the basics of taxation will empower you to make informed decisions.

- Consult a Tax Professional: Before signing any NIL agreement, consult with an experienced accountant, tax advisor, or business manager. They can help you calculate your tax obligations, identify potential deductions, and develop a tax strategy tailored to your situation. Along with ensuring any federal, state, and local taxes you owe are paid on time (avoiding penalties), a tax professional can also help you navigate more complex situations – such as earning income across multiple states.

- Practice Smart Spending: Resist the urge to splurge on electronics, clothes, or cars as soon as the money starts rolling in. Create a budget that considers your future tax payments, living expenses, and financial goals. Staying disciplined with your spending is key to long-term financial success.

2. Execute Agreements Cautiously

Navigating NIL deals can be tricky. There are various state laws and school policies to consider, along with a number of legal “gotchas” to avoid. Here’s how you can safeguard your interests:

- Seek Legal Advice: Before signing any NIL agreement, engage a lawyer with experience negotiating NIL and brand endorsements for athletes. An attorney with expertise in sports contracts can help you navigate the important terms in an NIL deal, such as money, exclusivity, length of the agreement, how the brand can use your name, image, and likeness, and an athlete’s delivery requirements. An experienced attorney will help you spot potential pitfalls and ensure the agreement aligns with your long-term goals.

- Beware of “Standard” or Simplistic Agreements: When someone refers to a contract as “standard” or provides an overly simplified agreement, that should throw up a red flag. All it takes is the slightest language in your agreement to give a company unfettered rights to use your name, likeness and image in ways you never intended.

- Follow Regulations: An experienced advisor will help you navigate specific laws and policies set by your state, school, and the NCAA regarding NIL deals. For example, you cannot share photos or videos in your team uniform with logos from other brands without first getting permission from your school or the brands.

3. Budget Wisely for the Long Term

While newfound wealth can be exhilarating, it’s crucial to manage your finances wisely:

- Prioritize Needs Over Wants: When it comes to spending, prioritize essential needs over extravagant wants. Understand this financial windfall may be a one-time occurrence, so focus on building a secure future rather than indulging in immediate gratification.

- Future-Proof Your Earnings: Instead of assuming this is a continuous stream of income, treat each deal as if it were your last. Create a budget that accounts for potential future earnings and uncertainties, ensuring you’re prepared for any scenario.

- Explore Tax Mitigation Strategies: Consider tax mitigation strategies, such as retirement planning and deferral opportunities, to minimize your tax burden. Consulting a financial advisor can help you explore these options.

Make the Most of Your NIL Opportunities

The legalization of NIL in college and high school sports represents an exciting shift for young athletes. It can offer game-changing money, enabling you to take care of your financial needs, along with building your brand for future growth. But with great success also comes great responsibility. Even professional athletes who’ve reached the highest pinnacles of their respective sports can end up without the financial resources they need if they don’t plan ahead.

The good news is by recognizing the potential pitfalls and seeking professional guidance early in your NIL journey, you can better position yourself for long-term financial success. Remember, it’s not just about profiting from your name, image, and likeness today, but also securing your financial future for tomorrow.

How We Can Help:

Our Entertainment, Sports, and Media practice understands the unique challenges athletes face at all stages of their financial journey. Whether you need assistance with tax planning, contract negotiations, or financial strategy, we’re here to guide you toward a successful future in the world of sports and NIL deals.

This article was co-authored by Leron E. Rogers, Partner at Fox Rothschild LLP.

]]>In this overview, our International Tax and Private Client Services teams “uncork” the complexities of tax issues that permeate the winery and vineyard industry so you can seamlessly confront tax challenges and seize tax opportunities. As financial landscapes continue to evolve, understanding these challenges becomes essential for vineyard owners, winemakers, and investors alike in their pursuit of crafting both exquisite wines and sustainable financial success. And as some new seasons start, others come to an end. When the time comes to transition the business, you will likely want a seasoned professional to guide you through.

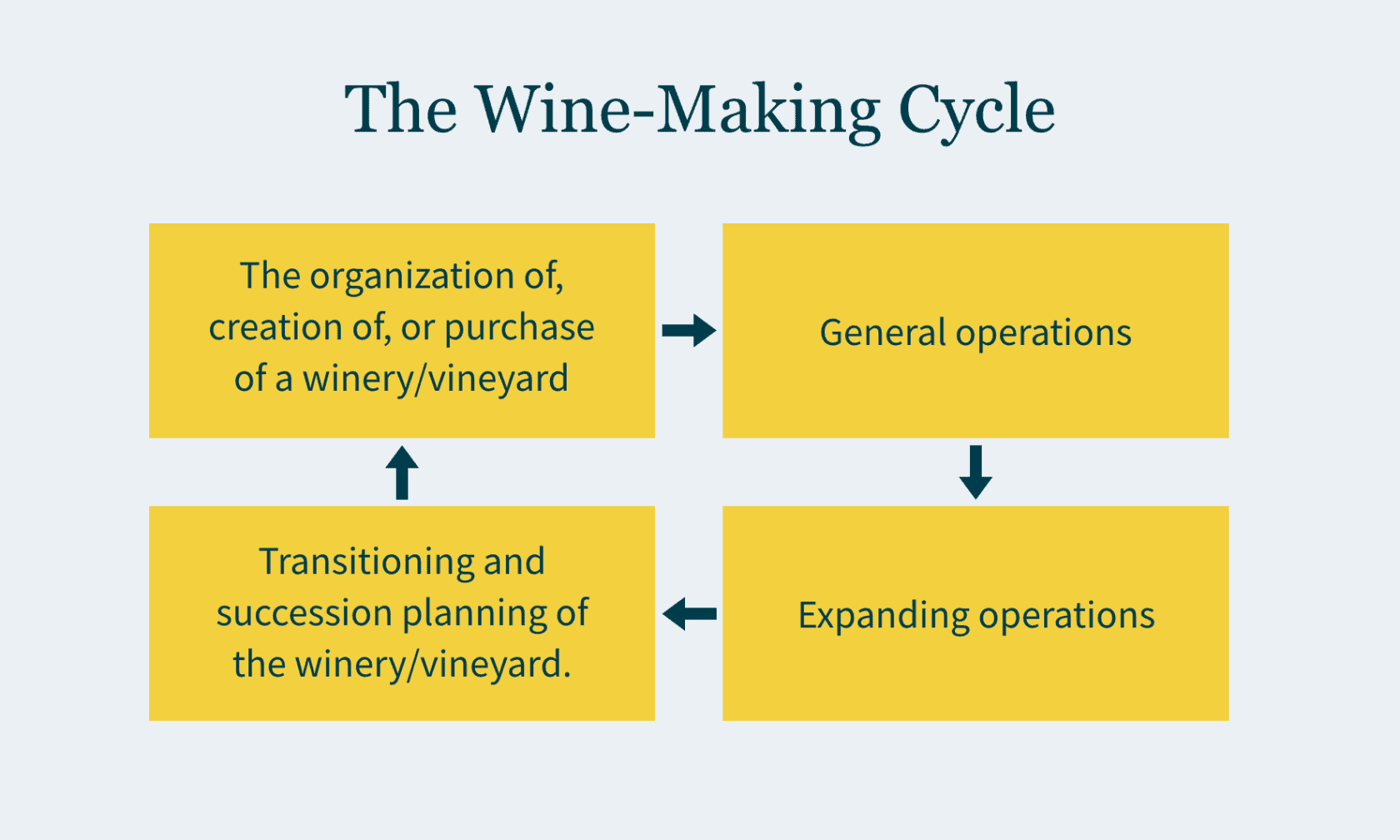

The wine-making cycle

Generally, a vineyard or winery has a business cycle that may take various courses but the course we see most commonly goes as follows:

Organization / Creation / Purchase

The creation of the organization generally entails the creation of an appropriate legal entity. Whether this act should be taxable or not will depend on the tax attributes of the potential owners and should be reviewed to position the organization optimally for taxing purposes.

The purchase of an existing winery or vineyard should be structured in a tax efficient manner such that future depreciation and deductions are maximized for the purchaser. Typically, the maximization of deductions will be at odds with what a seller would desire, so the final decision will stem from negotiations between both the buyer(s) and seller(s). Ultimately, a good due diligence exercise is always warranted in these situations.

Operations

Both metaphorically and physically, the seasons always present themselves with a new beginning for the industry.

There are many ways to operate a winery or vineyard. You may start with raw land—and then have vines, or not. Rocky soil and warm temperatures provide an excellent environment for grapes to make Cabernet Sauvignon, for example. Cooler microclimates and sandier soil offer great growing conditions for Sauvignon Blanc. A vineyard manager may want to “test” some of the grounds and only plant a smaller portion of the plot.

When planting a new crop, it can sometimes take up to three years before a vine produces viable grapes. Veraison is that magical moment when those hard, green grapes transform into plump, juicy clusters. In white grapes, such as those used for Sauvignon Blanc and Chardonnay, the clusters turn from bright green to a more mellow, golden green.

Once your grapes are ready, one may harvest and then crush, press, and start the primary fermentation process. Then the aging and malolactic fermentation sets in. Towards the end of the aging process, winemakers will frequently taste the wine to ensure the flavors are just right. They do this with a “wine thief,” or a special tool that extracts a small amount of wine from the container it is aging in. This is commonly referred to as racking and bottling. Once the process is complete, then one obtains the finished bottle.

Having an appropriate cost accounting system is crucial to tracking the costs that are attributed to each step in the process — and will be the cornerstone to any tax planning you will want to implement.

Having an appropriate cost accounting system should help track the costs that are attributed at each step of the way.

Some of the tax implications that should be considered are provided below.

Qualifying for R&D tax credits

Archaeological records insinuate that wine was first produced in China around 7000 B.C., with the oldest winery in the world in Armenia. So, it’s no secret that wine making has been around for a long time. However, this doesn’t mean winery owners can’t and don’t implement new technologies or approaches to making their cultivation and fermentation methods more innovatively efficient.

And many in the industry do not claim the Research and Development (R&D) tax credit, failing to realize their research activities actually fall into the qualifying research activity (QRA) category. In fact, many daily activities you may already conduct — as well as wages paid to your employees involved in these activities — can qualify.

R&D tax credits enable your business to apply for a dollar-for-dollar reduction of your tax applied to any qualified research and development expenditures you may have. In some circumstances, these credits can be applied against payroll taxes as well. These can provide significant value to your organization, as it provides reduced tax liability and cash back so you can reinvest or apply to other needs. Companies of all sizes are eligible — and the tax definition of “qualified research” is broader than you might think, covering more than research that takes place in a lab. If you develop new or improved products, processes, and/or software to use in your operations, you could be eligible for technologically advancing the industry.

Whether it’s making unique improvements to products already available on the market or inventing something completely new, if you demonstrate you’ve experimented to resolve technological uncertainties and tackle challenges that are new to you, you could qualify. This includes new or improved beverages. The best part? You don’t have to actually achieve your goals in order to qualify.

Examples of qualifying activities

- Improving or creating bottling and packaging processes.

- This includes bottle labeling or equipment, corks, and methods to improve filtration and shelf life. This could include new packaging designs to improve shelf life.

- Optimizing vineyard plots.

- This can mean evaluating soil, water availability, and ground slopes for optimal grape cultivation; soil and rootstock process improvement; plant irrigation system development; and trellis improvements.

- Augmenting your production mix.

- This can include evaluating conditions that affect winemaking like humidity, lighting, and ventilation in your barrels; developing product formulations; experimenting with new combinations for unique flavors; creating new aroma/flavor profiles and ingredient mixing methodologies; experimenting with prototype batches and preservative chemicals; developing new fermenting techniques; developing or refining press-fraction, press-yield or other crush or press trials; etc.

- Recycling efforts and techniques related to waste management along with sustainable energy technologies.

Commonly missed fixed asset tax savings opportunities

Fixed assets — i.e., property, plant, and equipment involved in your winemaking — can prove a powerful tax savings tool if you manage them correctly as well as increase your cash flow, so you can reinvest the savings or hold onto them to endure an uneven or less fruitful year.

Some of the tax opportunities you can capitalize on in the wine industry include:

- Reducing your current-year tax liabilities,

- Increasing your current-year cash flow, and

- Deferring your tax liabilities to later years.

Depreciated assets are one area you might overlook. Because wine production requires a significant amount of equipment you might not think about initially (like infrastructure and process-related electrical and plumbing hookups in your facility), you can count them in the total share of your property’s acquisition or constructed cost. The higher the percentage in assets available for shorter recovery periods, the more tax deferral opportunities you may have. Careful categorizing of assets between personal property v. real property can mean a substantial difference in tax benefit including amount and timing in a given year.

If you have implemented ways to make your winery more environmentally friendly, you may also capitalize on energy efficiency incentives. With an intensifying focus on environmental, social, and governance (ESG) permeating more industries, you can take advantage of available credits and deductions, which are measured against your facility’s ability to utilize alternative power systems (like solar energy) or the installation of energy efficient heating, ventilation, air condition, and lighting.

American viticulture areas

When you first purchase a vineyard, you have the option of acquiring an American Viticulture Area (AVA) intangible asset, whose value is recovered over 15 years through amortization. This provides annual deductions that lower your taxable income — a beneficial opportunity as it shifts the value out of the land that is normally not able to be depreciated.

Didn’t measure an AVA intangible when you bought your vineyard? That’s okay. An AVCA valuation can be performed — and any missed amortization deductions will be taken out from your application year.

Once the domestic tax planning is well oiled, some wineries and vineyards decide to expand.

Expanding operations

Many owners tend to expand their domestic operations, or some even venture overseas. Going offshore presents its own diverse challenges, some of which are described below.

International tax challenges

Exporting your wine abroad is a huge step — and one that can yield significant brand recognition and financial gain. Navigating the challenges associated with crossing borders and marketing in foreign markets coupled with international tax can prove extremely complex for wineries and vineyards because tax regulations vary from country to country, significantly impacting your operations and profitability. The taxes one may need to contend will be beverage taxes, customs and duties, tariffs and income tax, to name a few.

First and foremost, it’s critical that you work directly with experienced tax professionals who are knowledgeable not only about the area where your vineyard is located but also about the laws in the countries where you are exporting to. They can help you remain compliant amid the many seemingly convoluted challenges you face.

Because many countries have double taxation agreements (DTAs) to prevent the same income from being taxed twice, you should understand how these work between your home country and the countries you do business in. You certainly don’t want to be taxed twice!

Another way to successfully traverse these challenges is ensuring your transfer pricing practices are aligned with international guidelines. You’ll want your pricing transactions to remain fair between related entities to avoid tax evasion or an excessive tax burden in specific jurisdictions.

In general, it’s important to ensure you’re well versed in the tax laws of the countries you’re exporting to or operating in. That’s why a tax professional can come in handy. Different countries have different rules about importing, excise taxes, value-added taxes (VAT), and other forms of taxation that can majorly affect your business if you’re not complying.

This brings us to compliance with your reporting. Reporting all your international transactions and income is critical to avoiding penalties or legal issues. You’ll also need to consider any customs duties and tariffs, which may impact how successfully your wine competes in international markets. International tax regulations can change frequently at the hands of political, legal, or economic factors. Stay up to date on changes that could impact your business operations—or tax liabilities.

And just like the U.S. provides tax incentives, some countries do as well to encourage foreign investment and exportation. Your winery or vineyard could take advantage of these if they are available.

International tax compliance when exporting your wine can be complex. It also involves risk. Because every situation is different, you must tailor your approach based on the specific circumstances of your winery with advice from a professional knowledgeable in international tax. They can ensure you are adhering to the most updated regulations as well as maximizing your tax efficiency while remaining compliant.

From simply exporting abroad to setting up local in-country distribution operations we may assist by tailoring a strategy that best meshes with your company. A strategy many exporters use is an IC-DISC. The IC-DISC (Interest Charge-Domestic International Sales Corporation) is a federal income tax incentive for U.S. companies that may export their California wines outside of the United States. Domestic U.S. entities and sole proprietorships are eligible to receive this federal income tax savings. Our team may guide you as to whether an IC-DISC or other strategies are more suitable for you and your winery or vineyard.

Transition and succession planning

Whether you’re passing the business to the next generation or selling to a new owner, transition planning is crucial for taxes in the winery business, as it helps to ensure a smooth and successful transfer of ownership and management. However, transitioning a winery business involves complex financial transactions like asset transfers and potential restructuring. Tax efficiency is key to minimizing potential tax liabilities that could arise from poorly executed transfers. Here are some things to consider.

Minimizing your capital gains tax

Depending on if your winery has appreciated in value since its inception, transferring ownership can trigger capital gains tax. Strategizing the timing and structure of the transfer can potentially minimize these taxes through options like installment sales, gifting, or estate planning techniques. In fact, if the winery has been owned by a corporation, you might be able to sell your stock in that corporation with no taxable gains at all and/or rollover the gain into a new business, income tax free.

Navigating estate and gift tax considerations

Many wineries or vineyards are family affairs. If this is the case, you might face estate and gift tax implications. Taking advantage of exemptions and deductions can help you reduce the impact of estate and gift taxes.

Creating a smooth succession plan

Whether or not you’ve seen the popular show Succession, you know that sometimes, passing something as large as a corporation down to the next generation can cause some drama. That’s why succession planning is critical — it smooths the handover of management and ownership, which will help maintain your business’s stability and profitability. This can include a phased transition, training and development of successors, and establishing clear roles and responsibilities.

Optimizing your business structure

Different business structures have different tax implications. Knowing how to take advantage of your current structure’s tax efficiency and being open to changing it if that could prove advantageous before a transition occurs can pay dividends.

Assessing your value

Knowing the accurate value of your winery business is essential for tax purposes to calculate estate taxes or establish a fair selling price. Conducting a professional appraisal can ensure your business’s value is appropriately assessed.

Determining if you qualify for tax breaks

Some areas offer tax incentives for qualified business transfers, including reduced rates for capital gains taxes or other tax breaks. If you conduct transition planning, you can understand and leverage these applicable incentives.

Complying with tax laws and regulations.

Because tax laws and regulations can vary widely depending on where your winery or vineyard is located — not to mention they change over time — transition planning helps you stay aware of relevant tax regulations over the course of the transfer process, so you don’t incur penalties or legal issues.

Transition planning is a strategic process that analyzes the various tax implications that could affect a seamless and financially sound transition of ownership and management in your business. Tax professionals with experience in the wine industry can help you develop a transition plan tailored to your exact circumstances.

How we can help

Making and selling great wine is your top priority — which is why we’re here to help you navigate the tax challenges and seize the opportunities that can accompany following that passion. Our Private Client Services and International Tax teams are rooted in California, one of the most wine-centric regions in the world. We understand the nuances of your work while providing an external, holistic eye to help you grow and succeed. Contact us today.

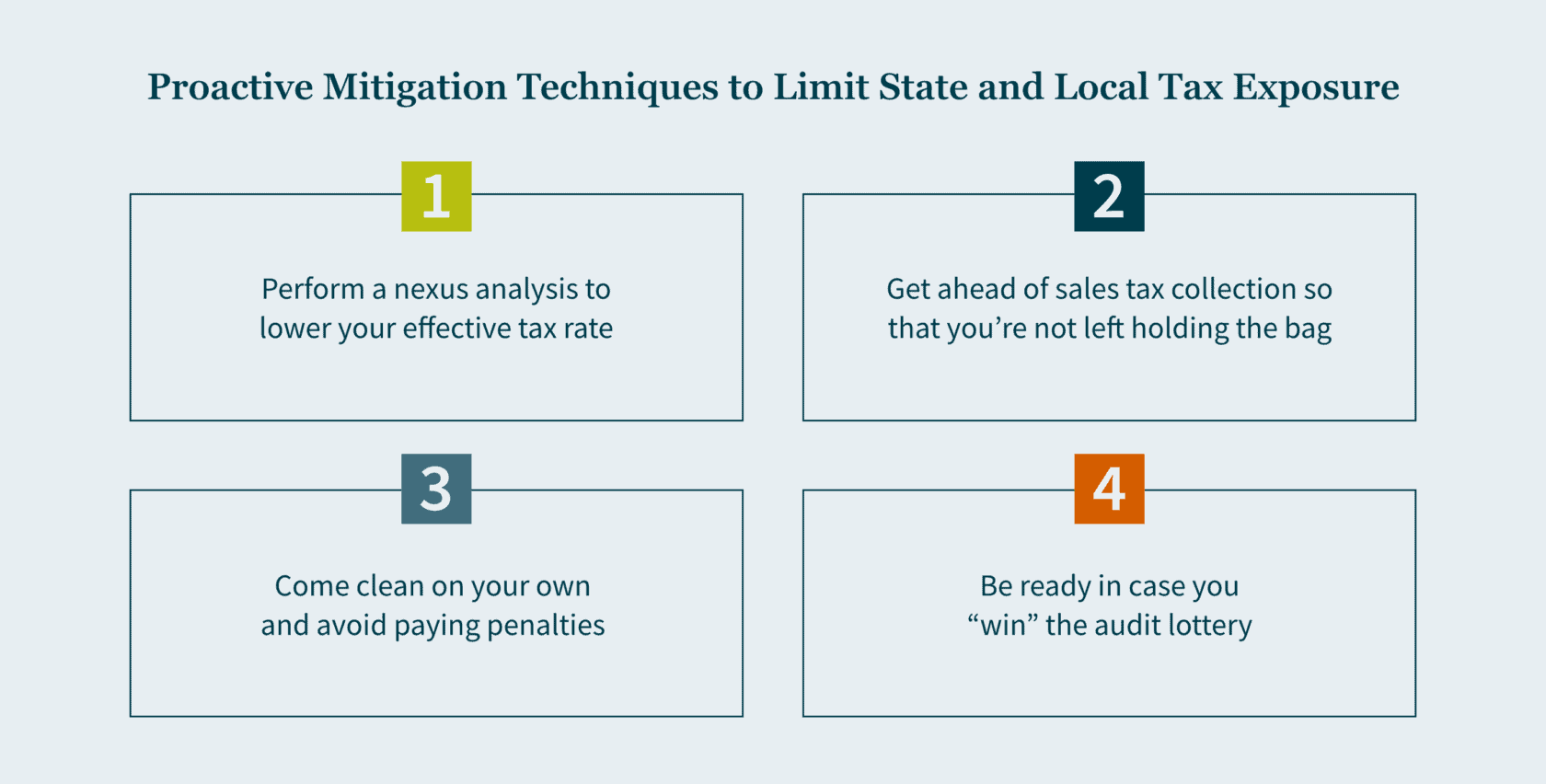

]]>- Now that a recession seems imminent, it’s important to prepare by adopting state and local tax planning techniques now.

- These techniques include performing a nexus analysis to lower your effective tax rate; getting ahead of sales tax collection so that you’re not left holding the bag; coming clean on your own to avoid penalties; and being ready to win in case you “win” the audit lottery.

- Right now, you should be taking proactive measures to avoid overexposure and capitalize on opportunities that limit your overall tax burden.

Despite a seemingly robust economic recovery from the COVID-19 downturn, we are now looking down the barrel of another recession. When polled for a Wall Street Journal survey, more than three in five economists predicted a recession will occur over the next year due to a variety of reasons: inflation has hit a 40-year record high, the Fed has raised interest rates to the highest levels in more than 15 years, and several Fortune 500 companies have implemented mass layoffs. In addition, market volatility prompted by the implosion of Silicon Valley Bank and Credit Suisse has sent regulators around the globe into damage control.

While no one can predict the future — and if the COVID-19 pandemic has taught us anything, it is that the economy won’t follow the course of even the most prescient prognosticators. To prepare for the proverbial rainy day, in the following our State and Local Tax team details state and local tax planning techniques you can adopt now.

Technique #1: Perform a nexus analysis to lower your effective tax rate

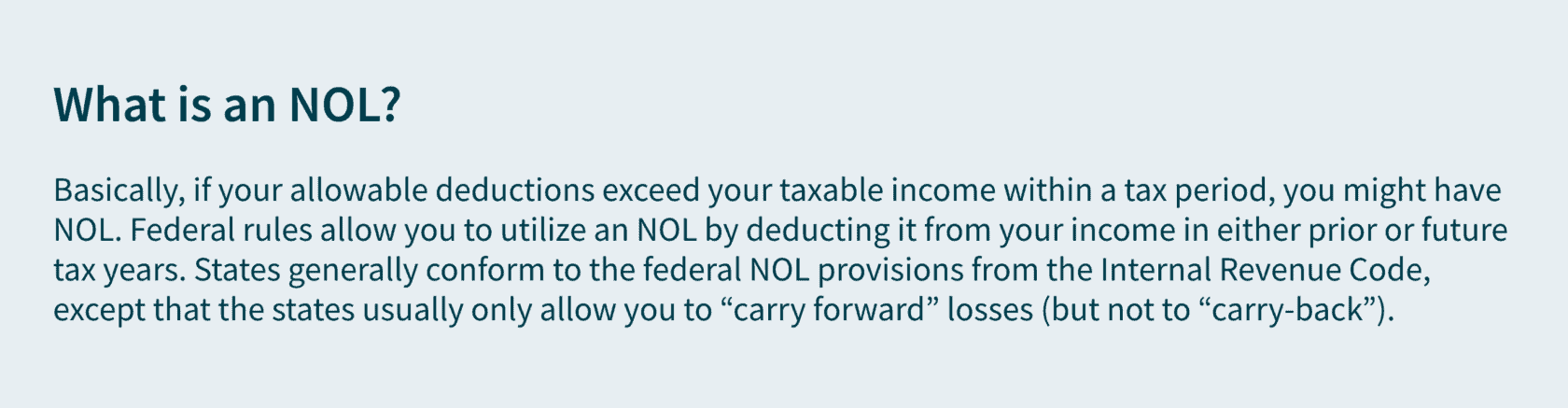

Typically, a nexus analysis is performed “defensively” when you’re under the threat of an audit or to identify potential tax exposure … and that usually means an increase in state tax. But you should also consider performing a nexus analysis “offensively” as a method for lowering your effective tax rate – either by capturing net operating losses (NOLs) in states where you haven’t previously filed or by lowering apportionment in high-tax jurisdictions.

This first idea rests on the principle that you can’t claim NOL deductions on returns you never filed. If your company historically operated at a loss (for tax purposes), a nexus analysis might not have been on your radar; or maybe you had a nexus analysis done, but then decided not to file returns where there wasn’t a material exposure. But if in 2022 or later years, you were or expect to be profitable and you’ve been doing business online or in multiple states, identifying potential prior year state income or franchise tax filings may allow you to claim the benefits of the federal NOLs on your state returns by carrying the losses forward to offset current or future taxes.

Note, current federal rules allow you to carry NOLs forward indefinitely until the loss is fully recovered, but they are limited to 80% of the taxable income in any one tax period. States do not always follow these rules, and moreover, state apportionment rules will affect how much of the NOL is allocated to a given state. Therefore, you’re not likely to see a “one-to-one” application, and you may still owe some taxes, but under the right circumstances, this technique will go a long way towards mitigating exposure for state income taxes that you may owe in the future.

Another way that increasing your state tax filings may decrease your state tax liability is by taking advantage of “economic nexus” developments to “spread out” your state tax liability across jurisdictions where rates may be lower (i.e., reducing your “effective tax rate”). Many states impose “throw-back” rules that require you to treat sales to states where you don’t pay taxes as if those sales should be sourced to your home state. But if, under economic nexus, you should or could be paying tax in those jurisdictions, you may be able to reduce the payment in your home state. Similarly, differences can arise between state’s rules for sourcing sales of services or intangibles that may be particularly helpful when considering how to treat a large item of gain from a sale of a business asset (e.g., stock in a subsidiary, or a valuable piece of intellectual property).

A few example scenarios illustrate these techniques:

- SoftDev Corp. started developing a SaaS product in 2019 and then testing its prototype apps online. They have employees that work remotely from home offices in five states. While SoftDev had potential nexus due to the economic activity in several states and payroll in the other five states, they only filed in their state of corporate domicile because sales were not significant, they had losses on their federal return, and the cost to prepare the other returns exceeded their compliance budget. In 2022, SoftDev expanded its product offering and began seeing significant sales in all 50 states. For federal tax purposes, they have accrued a large NOL that will reduce taxable income for the year (and probably several years to come). It would be wise to perform a nexus analysis at this point to identify whether SoftDev can capture any NOLs in other states – the key qualification being whether there is significant apportionment in the prior years as this will drive the amount of NOL available.

- Cal Widget Co. sells widgets (tangible personal property) it manufactures in California to customers all along the west coast and all its operations, including its one warehouse, are in California. Historically, Cal Widget only files a return in California, where it has 100% apportionment because of the throwback rule, and thus pays 8.84% on all its taxable income. However, by filing in additional states, the throwback rule would not apply to those sales, and thus they wouldn’t be “thrown back” to the California numerator of the apportionment formula. Even without paying tax to the other state, if Cal Widget could show that they would have owed tax under California’s rules, but for the fact that the state does not apply tax under those circumstances, the sales could still be removed from the California numerator. For example, if 50% of sales were to California customers, 25% went to customers in Oregon (average rate = 7%), and the remaining 25% went to Washington (no corporate income tax), using this method, Cal Widget could reduce its effective state income tax rate from 8.84% to 6.17%.

- Big Apple Co. has found a buyer for its signature logo and is anticipating a major gain event in 2023, and they realize that based on prior years, they’ll be paying New York State and City tax on the entire amount of gain because it’s the only state in which they’ve ever filed state income tax returns. If they are proactive, though, they can identify multiple states in which they have received revenue and can justify filing based on “economic nexus” and “market-based” sourcing principles – this won’t change New York’s tax rate, but it will provide a reason to apportion more of the income to source outside of the state and could save significantly on their tax bill.

Oftentimes, businesses are reluctant to really dig deep into nexus issues because they’re afraid of what they might find. And they end up waiting to take action until after they receive notices or their auditors (or worse, potential buyers) start asking about uncertain tax positions and accruals. But a slow-down in business due to the recession may offer you the opportunity to catch up on these nexus issues proactively.

Technique #2: Get ahead of sales tax collection so that you’re not left holding the bag

In a perfect world, when a company is properly accounting for, collecting, and remitting sales tax, there should be no (or at least very little) effect on revenue. Sales tax shouldn’t cost the business anything – instead, the business’ customers should be economically liable for the cost, while the business itself is only responsible for reporting and remitting the tax to the appropriate tax authority.

Problems arise when the business fails to account for sales tax and then only discovers the liability after the transactions have occurred and when it is no longer feasible to collect the individual sales tax amounts from customers. Then a cost that you could have passed through to your customers becomes your cost.

If you’re not currently collecting sales tax, you might consider a few of the “red flags” below:

- Your business generates revenue online through a website, Software-as-a-Service, or another cloud-based product.

- Many states treat SaaS (and similar cloud-based products) as they would other types of software, which are generally taxable.

- What’s more, since you’re selling online, you may be subject to “economic nexus” without ever creating a physical presence in the location.

2. Your business processes payments online on behalf of other businesses making retail sales.

- Since you are the party processing the transaction, you may be required to collect sales tax as a “marketplace facilitator,” even though you’re really just a company providing services to other businesses.

3. Your business provides services, so you haven’t really been concerned about sales tax in the past because you know it generally only applies to tangible personal property (TPP) … but consider whether:

- You make some related sales of TPP when you are providing services (e.g., you design custom web infrastructure and occasionally sell specialized hardware to meet your client’s specifications);

- The services you sell are computer programming and the end-product is typically custom software;

- One division of your business is leasing goods from another division; or

- Your services are taxable because they are dependent on, or related to, sales of TPP (e.g., third party software maintenance).

You can avoid this pitfall and ultimately save money by being proactive about identifying potential sales tax requirements and implementing systems to ensure you are properly collecting the tax.

Technique #3: Come clean on your own and avoid paying penalties

If your business sells products or services in multiple states, you could face unexpected tax liabilities for failing to comply with each state’s various income, franchise, gross receipts, sales and use, property, or other taxes. You may already be aware of the issue, and maybe you even have an accrual for the liability. And compounding any such liability are the interest and penalties that could be asserted if the state eventually discovers the business activity. But you don’t have to wait for the state to come after you, and if you’re proactive, you’ll probably be able to mitigate or remove all the penalties.

Virtually every state has a Voluntary Disclosure Program, under which you can execute a voluntary disclosure agreement (VDA) between your business and the tax authority to limit your liability for back-taxes. One benefit is that the VDA will limit the “lookback” period (otherwise a state can look back as far as the business had activity); this will often reduce the potential tax liability itself. Another benefit of a VDA is that any penalties that might have applied for late filing or payment are waived (though interest usually still applies). Finally, by going through the VDA process you are put in contact with a tax authority representative who can help you to determine precisely what rules apply to the business – they won’t exactly be a “tax adviser” but sometimes simply getting a hold of someone who will address your questions is challenge. And the certainty you will get from the process will give you comfort that your tax compliance process going forward is correct.

On top of state VDA programs, many states will offer amnesty programs. They usually are only available for a brief period (e.g., six months), have similar terms to a VDA, but are more relaxed in terms of eligibility. Let’s say you’ve been filing for five years, and you stop doing business in a certain state. You receive penalties and notices, and you ignore them — you aren’t doing business there anymore. But during the recession, you need to expand back into that state for additional customers. If you want to resume your business there, an active amnesty program may allow you to set up shop without having to pay penalties on the missed filings.

With the country entering a recession, business profits are likely to decrease, and so too will state revenues; under these circumstances, state governments are more likely to offer these amnesty programs as they seek to expand the tax rolls. Be on the lookout if a VDA isn’t an option for you.

Technique #4: Be ready in case you “win” the audit lottery

Not only do state governments seek out delinquent taxpayers through amnesty and VDA programs during a recession, but they may also seek out additional tax revenue through audits. For state income taxes, we’re likely to see a surge in audits surrounding online work and remote workers because of increased popularity in remote work over the last few years. In addition, states perennially test a business’ “unitary” status (i.e., whether a given item of income should be apportioned between several states or allocated to the corporate domicile) and therefore any significant sales of business assets in the last couple of years may make you a target.

Ultimately, this is the time to be more introspective: look back on your last few years and figure out if you had any gaps in recording. If there are opportunities to capture NOLs or other additional savings, bookmark those too. It’s best to be prepared, because while there’s no guarantee you’ll be met with an audit, there’s no question that state governments increase their audit activity during a recession.

How MGO can help

A recession affects everyone, and state and local governments are no exception — which, in turn, affects you and your business. These techniques can help you prepare for whatever’s coming, ensuring you’re ready for potential audits and losses along the way. MGO’s State and Local Tax team provides experienced guidance to help you avoid overexposure and capitalize on opportunities that limit your overall tax burden.

]]>Here’s what you need to know to claim it:

- It’s a one-time abatement of any “timeliness” penalties incurred on individual income tax returns (Form 540, Form 540NR, Form 540 2EZ) for tax years beginning on or after January 1, 2022.

- It’s only available to individual taxpayers subject to personal income tax law (so estates, trusts, and fiduciaries aren’t eligible).

- It can be requested verbally or in writing starting on April 17, 2023.

- For California taxpayers who qualify for an extended 2022 income tax return due date because of the California Winter Storms (i.e., most California taxpayers), the “timeliness” penalties that would be abated through this program should not start being imposed until after the new extended due date for that tax year – October 16, 2023.

Which penalties are eligible?

Both the Failure to File Penalty (i.e., you did not file your tax return by the due date nor did you pay by the due date of your tax return) and the Failure to Pay Penalty (i.e., you did not pay the entire amount due by your payment due date) on California individual income tax returns for tax years beginning on or after January 1, 2022 are eligible for the one-time penalty abatement.

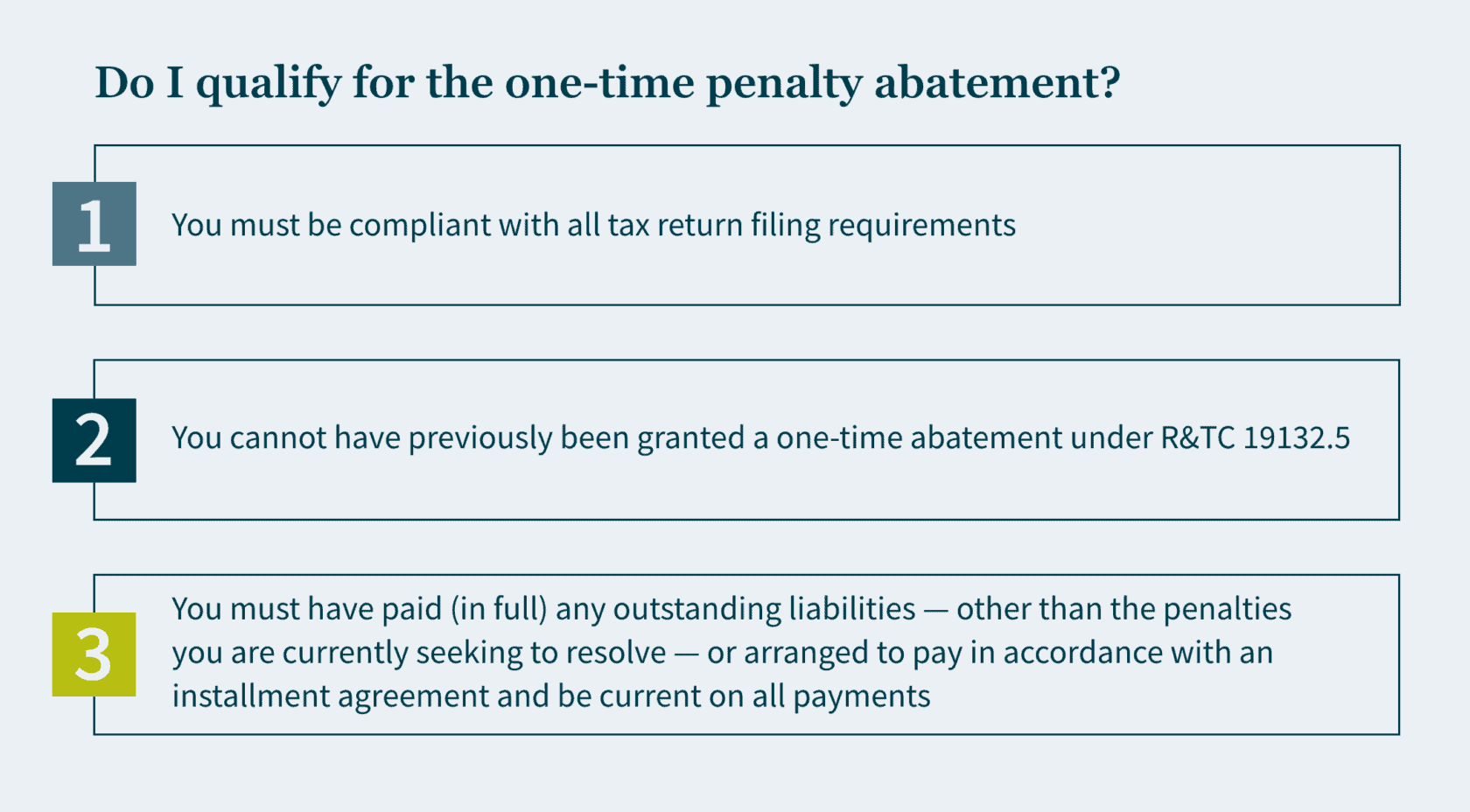

How do I qualify?

How do I request a one-time penalty abatement?

You can mail in a completed Form FTB 2918 or call the FTB at +1 (800) 689-4776 to request penalty abatement.

What if I can provide that I had reasonable cause for late filing or late payment?

If you can demonstrate that you exercised ordinary care and prudence and were nevertheless unable to file your return or pay your taxes on time, then you may qualify for penalty relief due to reasonable cause. Reasonable cause is determined on a case-by-case basis and considers all the facts of your situation.

You may request penalty abatement based on reasonable cause by mailing in a completed Form FTB 2917 or by filling out a reasonable cause request on your MyFTB online account. Penalty abatement based on reasonable cause may – depending on the circumstances – be preferable to using up your one-time penalty abatement request.

How we can help

If you need help with relief for your “timeliness” penalties or if you need help with any other state and local tax matters, please reach out to our experienced State and Local Tax team.

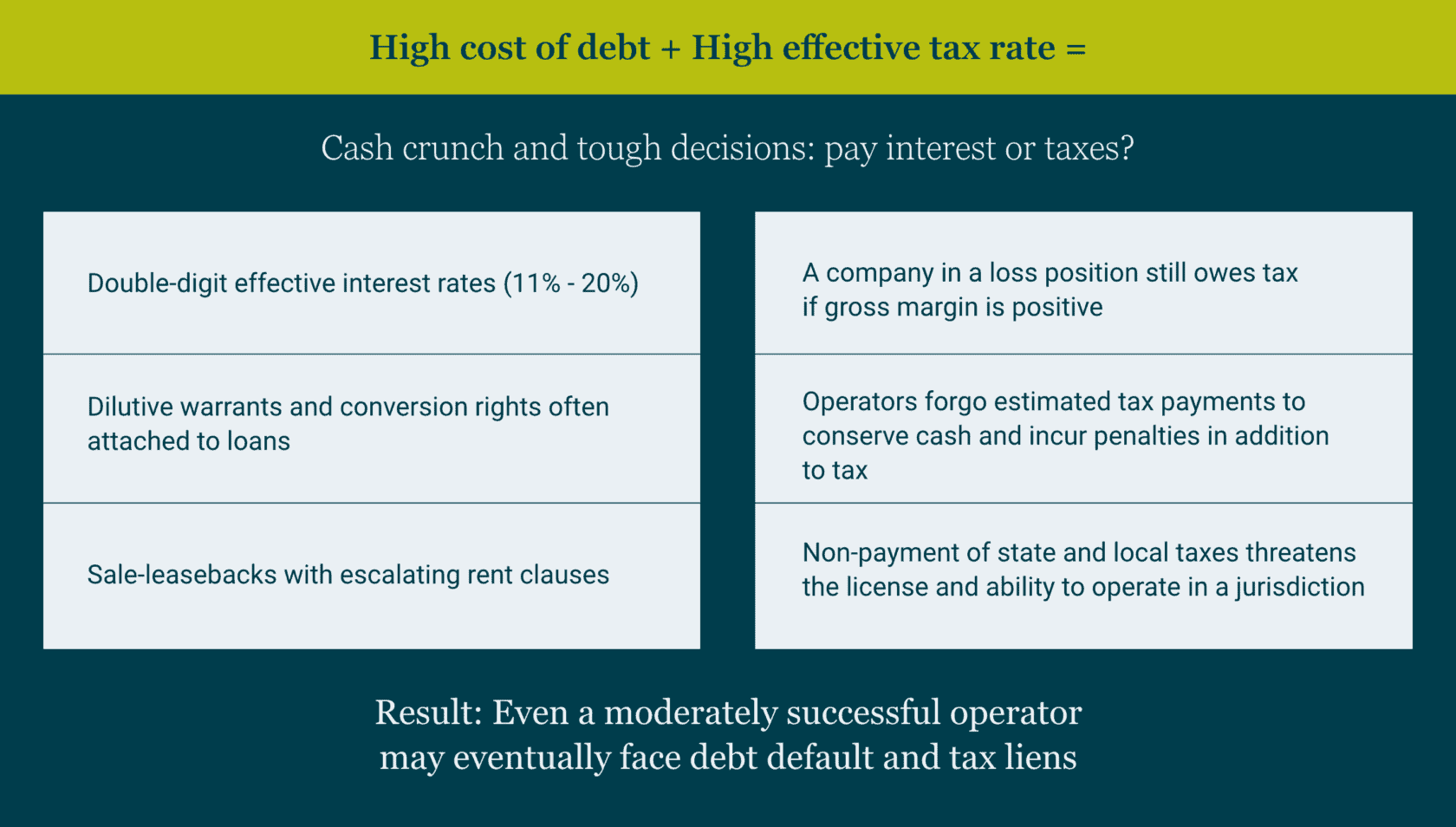

]]>High cost of debt + high effective tax rate = cash crunch and tough decisions

How did cannabis companies arrive at this decision point? The current cash crunch in the industry has been building for years, precipitated in part by banking regulatory constraints and an abnormally high effective federal tax rate.

As the below chart illustrates, cannabis companies lack access to traditional banking and market rate loans and have turned to alternative, expensive sources of debt financing bearing effective interest rates as high as 20%. In addition, Internal Revenue Code Section 280E essentially taxes the industry on gross margins, such that even a company that would otherwise be in an overall tax loss position may still owe taxes.

Caught in this double bind, even an operationally successful cannabis company may face a difficult choice: service debt timely at the expense of keeping current with taxes, risking tax liens that threaten the license, or pay taxes when due at the price of defaulting on debt and risking the viability of the business overall.

The tax impact of debt restructuring

Restructuring debt is one route for cannabis companies in distress to remain operational, but debt modification carries potential tax traps for the unwary – both borrower and lender. Depending on the relative value of the debt exchanged, the borrower can realize cancellation of debt income. The insolvency exception to recognizing and paying current tax on this income may not be available to a cannabis company, as the fair value of its assets – including intangibles – may still exceed its liabilities. A lender may also experience a taxable event on the refinancing, either in the form of interest income, or gain due to the valuation of equity received in the exchange.

In any debt refinancing situation, both the borrower and the lender should anticipate and plan for complex tax calculations involving debt discounts (I.e., original issue discount, or OID) and the fair value of company equity in order to determine correct tax treatment. To avoid any last-minute surprises or deal delays, both the borrower and the lender should model the tax treatment on both sides.

Sales of distressed assets and the tax impact

Considerations for the borrower:

- Are the assets to be sold in a different tax filing entity as the borrower?

- Will the flow of cash between entities create a taxable event?

Considerations for the lender:

- What is the borrower’s anticipated cash position after paying tax on the sale?

- Can cannabis business assets be sold in the jurisdiction’s regulatory environment? Or is a sale restricted to equity?

Assignment of income receipt of equity

If the borrower and the lender agree on a debt workout based on assignment of income, or equity ownership, both parties should understand the borrower’s existing tax structure and the impact the restructuring will have on both sides.

The borrower should assess whether a “change in control” has occurred for tax purposes, as the use of tax attributes may be limited. If an assignment of income is structured as a fee, consider the tax treatment of the payment and deductibility under 280E.

A lender who becomes an owner or part of management should consider:

- Depending on how the agreement is structured, the assignment of operating income and participation in management may turn the lender, or the lender’s entity, into a “trafficker” subject to 280E.

The lender should also be cognizant of the borrower’s standing with the taxing authorities and whether the operator can afford both paying down tax liabilities and payments under the terms of the workout. The retention of the cannabis or reseller license that the lender is depending on for cash flow is tied to staying current with state and local taxes. An IRS liability that has progressed to the lien stage unbeknownst to the lender could result in a “sudden” drain of cash from a bank account.

“Workouts” with taxing authorities

Given the current cash crunch in the industry, companies have been known to delay remittance of sales and excise taxes to state and local governments. Companies should be aware that non-payment of these “trustee” taxes can cause a loss of standing to operate legally and carries personal liability for officers and owners of the company. Taxing authorities may have limited sympathy for a distressed taxpayer who falls behind on these types of taxes and taxpayers should pay down any outstanding balances as soon as possible.

If income taxes are past due, it is important to continue to make payments toward the balance on a regular basis. A taxpayer cannot apply for a formal IRS payment plan until a revenue officer is assigned to the case. Also, a taxpayer must usually pay all outstanding taxes that are not overdue and remain “current” on all future taxes in order to establish and remain on an installment agreement. Federal and state revenue officers are generally willing to work with taxpayers in financial distress who act in good faith throughout the process. Engaging a professional representative who understands tax controversy practice and procedure and how to work with revenue officers can make all the difference between establishing a payment plan and facing a tax lien.

How MGO can help

A cannabis company navigating financial distress should engage a tax professional with both industry experience and a high level of tax technical skill to navigate the complex tax impact of a workout or restructuring. MGO’s Cannabis Tax team has both the industry experience and the technical knowledge to assist companies of all sizes during this challenging time.

]]>The U.S. Small Business Administration (SBA) expanded eligibility in September 2021. While you may not have qualified or considered EIDL funding necessary previously, you might want to reconsider in light of yet another wave of COVID infections. But you’ll have to do so quickly, as the application deadline is December 31, 2021.

Shaky economic ground ahead?

Sen. Joe Manchin (D-WV) released a statement on December 19 announcing that he “cannot vote to move forward” on the BBBA. The $2.1 billion bill that passed in the U.S. House of Representatives includes numerous provisions related to healthcare, energy initiatives, immigration, education, social programs and taxes.

The Democrats lack the votes to pass the proposed legislation in the Senate without Manchin’s support. Yet Senate Majority Leader Chuck Schumer (D-NY) indicated on December 20 that he nonetheless intends to hold a vote on the bill in early 2022. Schumer’s announcement came hours after Goldman Sachs reduced its predictions for U.S. economic growth in 2022 based on Manchin’s statement.

Types of EIDL relief available

The COVID-19 EIDL program was created to make low-interest fixed-rate long-term loans to provide small businesses (including sole proprietorships and independent contractors) the working capital they need to withstand the effects of the pandemic. Three types of funding are available:

Loans. This funding type features a 30-year term and fixed interest rate of 3.75%. The proceeds can be used for any normal operating expense, including payroll, rent or mortgage, utilities, and other ordinary businesses expenses. Since the recent program expansion (see below), funds also can be used to pay or pre-pay business debt incurred at any time, including after submitting the application, and regularly scheduled payments of federal debt.

Targeted advances. Businesses located in low-income communities, have no more than 300 employees and have suffered more than a 30% reduction in revenue may qualify for a targeted advance up to $10,000. These advances don’t have to be repaid.

Supplemental targeted advances. Businesses in low-income communities that have no more than 10 employees and saw revenue declines of more than 50% may be eligible for an additional $5,000. Supplemental advances also don’t require repayment.

The recent expansion

The SBA has implemented several changes to make it easier for small businesses to access the COVID-19 EIDL loans. Among other things, the SBA:

- Expanded eligibility from organizations with no more than 500 employees (including affiliates) to encompass businesses in the hardest hit industries with no more than 500 employees per physical location, as long as the business (with affiliates) has no more than 20 locations,

- Increased the maximum loan amount from $500,000 to $2 million,

- Extended the payment deferment period to two years after the loan origination date for all loans (interest will accrue during that period, and principal and interest payments must be made over the remaining 28 years of the loan term), and

- Simplified the affiliation requirements.

The SBA has also limited entities that are part of a single corporate group to a combined total of no more than $10 million in COVID-19 EIDL loans.

Additional eligibility requirements

Applicants must be physically located in the United States or a designated territory and have suffered working capital losses due to the COVID-19 pandemic. In addition, the businesses must have been in operation on or before January 31, 2020.

Businesses (other than sole proprietorships) must have a valid tax identification number. Each owner, member, partner or shareholder of 20% or more must be a U.S. citizen, non-citizen national or qualified alien with a valid Social Security number.

For loans of $500,000 or less, you must have a credit score of at least 570. For larger loans, the credit score must be at least 625. Personal guaranty and collateral requirements may apply, too, depending on the amount of the loan.

The looming deadline

The SBA will accept applications for loans and targeted advances until December 31, 2021. It will continue to process applications after that date, until the funds are exhausted. While the SBA earlier advised businesses seeking supplemental targeted advances to submit applications by December 10, 2021, it later announced it will accept applications until year end. It can’t process applications after the deadline, though, so applications submitted near the deadline might not be processed.

Note that borrowers can request increases, up to their maximum loan eligibility amount, for up to two years after loan origination or until the program funds are exhausted. In addition, the SBA will accept reconsideration and appeal requests received before December 31, 2021, if received on a timely basis. For reconsiderations, that means within six months from the date the application was declined. Appeals must be received within 30 days from the date the reconsideration was declined.

Don’t dawdle

You can apply online for COVID-19 EIDL relief, but the clock is ticking. We can help you determine if you should go this route and help you collect the necessary documentation.

]]>Employee Retention Tax Credit

The Employee Retention Tax Credit (ERTC) is a refundable tax credit created by the Coronavirus Aid, Relief and Economic Security (CARES) Act, to encourage businesses to keep employees on their payroll. For 2020, the credit is 70% of up to $10,000 in wages paid by an employer whose business was fully or partially suspended because of COVID-19 or whose gross receipts declined by more than 50%

For 2021, an employer can receive 70 percent of the first $10,000 of qualified wages paid per employee in each qualifying quarter. The credit applies to wages paid from March 13, 2020, through December 31, 2021. And the cost of employer-paid health benefits can be considered part of employees’ qualified wages.

It’s an attractive credit if you qualify.

Eligible businesses

The credit applies to all employers regardless of size, including tax exempt organizations that had a full or partial shutdown because of a government order limiting commerce due to COVID-19 during 2020 or 2021. With the exceptions of state and local governments or small businesses that take Small Business Administration loans, this credit is available to almost everyone.

Of course, there is some fine print:

• To qualify, gross receipts must have declined more than 50 percent during a 2020 or 2021 calendar quarter, when compared to the same quarter in the prior year.

• For employers with 100 or fewer full-time employees, all employee wages qualify for the credit, whether the employer is open for business or shutdown.

• For employers with more than 100 full-time employees, qualified wages are wages paid to employees when they are not providing services due to COVID-19-related circumstances.

One bright point about the ERTC is that employers can be immediately reimbursed for the credit by reducing the amount of payroll taxes they would usually have withheld from employees’ wages. That was a nice touch by the IRS.

Retroactive claims for the ERTC

Although it appears the IRS tried to make this as easy as possible, you may still need a tax professional to sort it out. For instance, if your business had a substantial decline in gross receipts but has now recovered, you can still claim the credit for the difficult period

Retroactive claims for refunds will probably be delayed because currently everything is delayed at the IRS. The credit can be claimed on amended payroll tax returns as long as the statute of limitations remains open, which is three years from the date of filing. So you have some time to claim the credit, but why wait?

Keep December 2021 in mind

The economy is in a state of change, and it is fair to say that we are once again in uncharted territory. On the positive side, there seems to be significant resources and support for businesses from both government and consumers. You and your tax professional should keep your eyes open for credits and benefits to make sure you don’t miss any opportunitie

The ERTC expires in December 2021. Though it may be difficult to think about year-end in the middle of the summer, you’ll want to figure out your position on this credit before December. A tax professional can help you understand the ERTC and help you decide on your next step.

About the author

Michael Silvio is a partner at MGO. He has more than 25 years of experience in public accounting and tax and has served a variety of public and private businesses in the manufacturing, distribution, pharmaceutical, and biotechnology sectors.

]]>Of the long list of relief efforts, one of the most significant changes for businesses small and large was not something new, but rather a correction to the Tax Cuts and Jobs Act (TCJA) of 2018 regarding qualified improvement property (QIP). Here’s why that minor fix could have a major impact by providing much-needed liquidity in the midst of a pandemic.

Understanding the “Retail Glitch”

As the TCJA came together, Congress added language that renewed 100% bonus depreciation for QIP that was acquired after September 23, 2018, and began being used by January 1, 2023. This is depreciation that included properties that had a life of up to 20 years. During the whirlwind drafting sessions that took place before the bill was finalized, drafters failed to include an amendment that included a 15-year recovery period for QIP, even though it was clear they had intended to do so. The omission, known as the “Retail Glitch,” meant that QIP was subject to a 39-year recovery period rather than the intended 15, and that businesses would not be able to write it off.

Fixing the glitch

The CARES Act addressed the error in the TCJA by including QIP as a 15-year MACRS asset and 20-year ADS asset, allowing businesses in hard-hit industries like hospitality, retail, and restaurants, to retroactively write-off any investments they have made into their spaces dating back to the enactment of the TCJA on December 22, 2017. The impact of this is significant, as fixing the error allows leaseholders and building owners to immediately retrieve the costs of improvement-related investments they have made in their property since December 2017, which are now classified as bonus depreciation under the CARES Act.

Why QIP changes are critical

This provision of the CARES Act is so important because it is an immediate injection of cash to thousands of businesses who are likely experiencing severe cash flow issues. The QIP classification includes any renovation to the interior of a non-domicile property that was made after the building began business use and applies mostly to industries that often revamp their facilities. Additionally, because the bill is retroactive, it is likely that many businesses will be able to access liquidity from several past projects, allowing them to potentially further ease financial burdens.

Getting the cash

As with any major piece of legislation, specifics on how to access the depreciation that the CARES Act entitles business owners to is scarce. However, industry professionals have found several methods to file for the money, the simplest of which is to work with your tax services provider to file amended returns for tax years 2018 and 2019. Other options exist as well, including filing superseding returns or filing a Form 3115, which is an application for change in accounting method. Because the QIP change will have widespread effects, it is anticipated that when the IRS issues formal guidance they will automatically allow the change to be made.

Small businesses and corporate America alike are struggling at this moment, and the future is uncertain. Taking advantage of the QIP amendment to the tax code is strategically imperative for any business that needs a boost in financial health in the short and long term.

For guidance applying the new QIP changes or filing amended tax returns, please reach out to schedule a consultation.

]]>To help combat the economic fallout from the pandemic, the federal government has introduced sweeping legislation to provide emergency relief via loan and grant programs and tax breaks, credits and other incentives.

Sources of relief include:

- SBA Economic Injury Disaster Loans (EIDLS)

- SBA Paycheck Protection Program (PPP)

- Families First Coronavirus Response Act (FFCRA) Tax Credits

- CARES Act Employee Retention Tax Credit

- CARES Act Employer Tax Payment Deferral

Millions of dollars of emergency relief is now available to qualifying organizations, some of which is eligible for 100% forgiveness. Unfortunately application processes are complex and time-sensitive, strict usage rules determine what can be forgiven, and changes to tax code are complex.

MGO has created the attached one-page summary to provide basic details on what your organization may be eligible for, and the levels of relief available.

If you need assistance applying for loans, or applying tax incentives, please do not hesitate to reach out to our team.

]]>As the cannabis industry continues to evolve and mature, perhaps the single biggest obstacle to profitability remains: IRC Section 280E. By prohibiting expense deductions for businesses that produce, sell or distribute Schedule I and II substances, the Federal government is imposing an effective tax rate two to three times higher than traditional businesses.

While there has been no progress on 280E reform at the Federal level in 2020, legal decisions in recent years, such as the cases involving retailers Harborside Inc. and Alternative Health Care, have impacted the application of 280E and provided some clarity on what cannabis companies need to consider and prepare for with tax season on the horizon.

Extensive documentation is key to navigating 280E

The first rule of navigating 280E is that all cannabis businesses must document absolutely everything. If they don’t, then it is very, very unlikely that they will prevail during an audit or if they find themselves in Tax Court. Throughout the course of doing business, inventory and costs need to be diligently documented. By keeping thorough records, you strengthen your potential case, and at the very least may win some points for demonstrating “good faith” intent.

That is what happened in the Harborside case, where the Oakland-based company was hit with an $11 million IRS bill for back taxes from 2007 and 2012. In that case, Harborside had been comprehensive in its documentation and was able to substantiate all of its claims as it related to deductions. As a result, they were not assessed inaccuracy penalties and documentation played a role in lowering their debt owed.

Understanding Cost of Goods Sold and 280E

Another lesson from recent cases relates to calculating the Cost of Goods Sold (COGS), where a reduction is made during the process of calculating gross income. IRS regulation 471 states that if the usage of inventories is deemed necessary to determine a taxpayer’s income, then an inventory shall be taken by the best accounting practices in that trade. Per 471, there are different regulations whether a taxpayer is a reseller or a producer. For instance, for producers, inventory calculations should include the costs of raw materials and necessary indirect production costs.

In the Harborside case, the company claimed that for calculating COGS, IRC Section 263A was the correct approach. Under 263A, taxpayers are required to capitalize both direct and indirect costs related to actual personal property that it produces. Harborside argued that being disallowed from using 263A resulted in the company having to pay taxes on an amount in excess of their gross income.

The decision of the Court confirmed the IRS approach, dealing a blow to cannabis companies. Per the Court’s ruling, there were a number of aspects that impact the way cannabis can approach how they calculate COGS. Given the different approaches under 471 for those deemed either a “producer” or a “reseller,” companies need to understand how they will be classified, as it has a major impact on their accounting processes.

Tax structuring considerations for 280E

Another important aspect for cannabis retailers to consider is how they are structuring their business. In a case decided last year, Los Angeles-based Alternative Health Care tried to avoid 280E by having a management company operate its storefront. The management company was responsible for a number of critical day-to-day operations, such as paying employees. Given that Alternative Health Care wasn’t in charge of the storefront, it argued that it wasn’t subject to the tax laws of 280E. However, their argument lost in court and resulted in an expansion of the types of companies that are considered liable under 280E.

There may be a number of reasons why a cannabis retailer would want to avoid liability under 280E. But just because a management company is technically in charge, liability also extends to them. If a company is considering using a different company to handle its day-to-day business, there needs to be an understanding that 280E is still applicable and that trying to get around this can end up being costly.

There are many other benefits to structuring a cannabis company in a strategic way. It can allow specific business units to be utilized in a tax efficient manner and enhance a company’s ability to take advantage of special tax deductions. Additionally, a company can make bookkeeping much easier, while simultaneously reducing risks by separating certain business units. Structuring can also open up other opportunities down the line when it comes to joint ventures or shareholder investments.

Preparing for cannabis audits

Recent court decisions (and other rumors) have stoked fears that there will be an increase in audits of cannabis companies. There is no guarantee that there will be more audits or that a certain retailer will be audited in the next year. However, audits can happen, so it is paramount that a company protects itself in every way they possibly can.

Overall, it is always best to be prepared. As stated previously, document everything. Maintain all necessary paperwork. If you avoid being audited, there are many other benefits to appropriately documented financial and operational records. But if one crops up, you minimize the risk of potential penalties and create a much smoother process.

The bottom line on 280E

While changes to precedent and recent case developments have altered the 280E landscape, as the cannabis sector grows, and revenue numbers rise, greater attention is given to the industry by regulatory authorities. As a result, companies must make taking a strategic approach to 280E compliance a top priority.

]]>