- State tax authorities are escalating audits of intercompany transactions, as transfer pricing crackdowns in several states are generating millions in tax revenue.

- These state initiatives indicate growing regulatory emphasis on transfer pricing, which may encourage more aggressive audits (especially if budgets tighten).

- Companies operating across state borders should take proactive steps, like conducting transfer pricing studies to validate policies and strengthen defenses before audits strike.

~

A recent Bloomberg article affirms state tax authorities are ramping up audits of intercompany transactions at multistate corporations. The report points to an increase in audits in three “separate-reporting” states following transfer pricing settlement initiatives as a beacon of audit activity to come across other states that take this approach.

While not ideal for multistate operators, this development may not come as a surprise to companies with international operations who have dealt with a myriad of cross-border tax issues in recent years. Close observers of state and local tax (SALT) developments have been predicting for many years the potential that states will be adopting similar positions with respect to transfer pricing. In a 2022 article focused on SALT transfer pricing enforcement, we highlighted several key indicators that more state transfer pricing audits could be on the horizon – including state budget deficits, a surge in auditor and consultant hirings, and renewed interest among states in collaborating on multistate audits.

With confirmation that state-driven transfer pricing audits are on the rise, it is imperative for corporations operating across state borders to assess your transfer pricing risks and fortify your documentation and audit defense strategies.

Surge of Transfer Pricing Audits in Separate-Reporting States

According to the Bloomberg Tax report, the recent spike in transfer pricing audit activity has predominantly affected Southeastern states categorized as separate-reporting states. Currently, there are 17 separate-reporting states in the United States. With the exception of a handful of states like Indiana, Pennsylvania, Iowa, and Delaware, most separate-reporting states are located in the Southeast region.

How separate-reporting states differ from other states in their taxation approach to corporations:

- In separate-reporting states, each corporation within an affiliated group is required to file its individual tax return. This treatment considers them as separate entities with independent income, recognizing intercompany transactions, and allowing for varying tax liabilities.

- In contrast, combined-reporting states require or allow affiliated corporations within a corporate group to file a single tax return, treating them as a unitary business with shared income, often eliminating intercompany transactions.

Notably, two Southeastern states, Louisiana and North Carolina, have recently concluded audit resolution programs that significantly boosted their state revenues. Louisiana’s program generated nearly $38 million, while North Carolina’s efforts resulted in more than $124 million. Meanwhile, New Jersey, a Mid-Atlantic state that abandoned separate reporting in favor of combined reporting in 2019, is in the midst of a transfer pricing resolution program that has already collected almost $30 million. The success of these programs in collecting tax revenue is likely to motivate other states to explore similar initiatives.

The success and subsequent expansion of these programs signify a growing emphasis on transfer pricing at the state tax authority level. State tax agencies are enhancing their knowledge and enforcement activities in this domain, giving auditors more confidence to adjust returns in transfer pricing disputes. This increasing competency may be viewed as a valuable tool by states – both those requiring separate and combined reporting – that are seeking ways to augment revenue streams.

Strengthen Your Transfer Pricing Defenses Before State Audits Strike

To preemptively safeguard your business from a state transfer pricing audit, a proactive approach to validating pricing policies is essential – and a comprehensive transfer pricing study is your primary defense.

Here are three key advantages of conducting a transfer pricing study:

- Document Your Transfer Pricing Policy: A transfer pricing study provides robust documentation that can counter inflated tax assessments by identifying key intercompany transactions, referencing benchmark data, and highlighting any deviations that necessitate policy adjustments. Even if your company has undertaken prior studies, annual updates are indispensable to align with evolving business landscapes and provide tax penalty protection.

- Mitigate Your Risk: Beyond reducing audit risks and potential liabilities, these studies also play a pivotal role in supporting major corporate events like mergers and acquisitions (M&A). By demonstrating pricing compliance, they ensure that domestic affiliates have robust documentation and effective cost allocation analysis, thus preventing over-taxation or under-taxation.

- Ensure Consistency: Minimize uncertainty by achieving uniform entity-specific compensation across state agencies and affiliated entities. Swift collaboration with advisors when audits arise enhances dispute resolution capabilities.

As states continue to gain confidence in challenging transfer pricing, multistate corporations must take proactive measures to ensure the resilience of their intercompany transactions under intensified scrutiny.

Get Ahead of the Game with a Transfer Pricing Study

If your company engages in substantial intercompany transactions across state lines, initiating a review of your current pricing policies, preparing your transfer pricing policies, and ensuring compliance with U.S. transfer pricing rules should be a top priority. Proactive measures can help you stay ahead of potential issues before state auditors come knocking. We have a robust transfer pricing team that works closely with our State and Local (SALT) Tax and Tax Controversy practices. Through a combined effort we can support you through every stage of managing a transfer pricing audit. Talk to our transfer pricing professionals today to find out how we can help you minimize your exposure to transfer pricing audits.

]]>- Name, image, and likeness (NIL) deals offer athletes exciting opportunities, but also potential pitfalls if not approached strategically.

- Athletes should educate themselves on taxes, carefully review contracts, and budget with long-term security in mind.

- With guidance on financial obligations, agreements, and smart money management, athletes can maximize NIL benefits while safeguarding their futures.

~

You are a talented young athlete with a growing public profile. You’ve just been offered a Name, Image, and Likeness (NIL) deal, an opportunity that can put some extra money in your pocket or even, in some cases, make a more profound impact on your financial life. It’s an exhilarating time, but it’s also crucial to approach this new chapter with the right knowledge and mindset.

Whether you’re a college or high-school athlete, or the trusted advisor to a young athlete, here are the three most critical actions you should take to avoid common financial pitfalls associated with NIL deals.

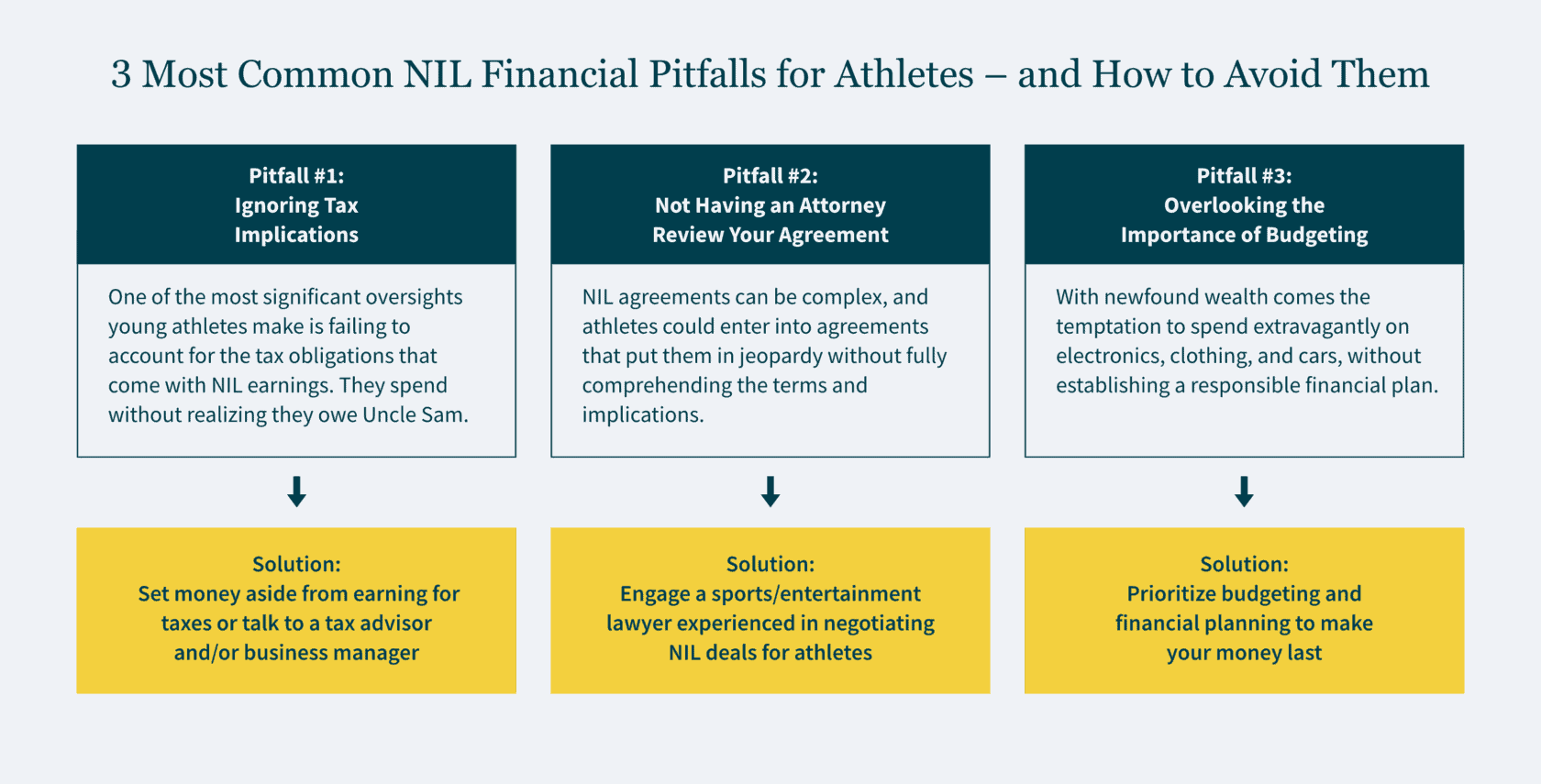

1. Recognize Your Tax Obligation

One of the first hurdles you’ll encounter in the world of NIL deals is taxes. It’s essential to understand that the money you earn from these deals is subject to taxation. Many young athletes overlook this, often because they’ve never had to deal with taxes before.

To avoid potential financial trouble down the road, consider these steps:

- Educate Yourself: Young athletes receiving payments from NIL deals are responsible for paying taxes on that income just like professional athletes. Take the time to learn about taxes, especially how they apply to your earnings. Understanding the basics of taxation will empower you to make informed decisions.

- Consult a Tax Professional: Before signing any NIL agreement, consult with an experienced accountant, tax advisor, or business manager. They can help you calculate your tax obligations, identify potential deductions, and develop a tax strategy tailored to your situation. Along with ensuring any federal, state, and local taxes you owe are paid on time (avoiding penalties), a tax professional can also help you navigate more complex situations – such as earning income across multiple states.

- Practice Smart Spending: Resist the urge to splurge on electronics, clothes, or cars as soon as the money starts rolling in. Create a budget that considers your future tax payments, living expenses, and financial goals. Staying disciplined with your spending is key to long-term financial success.

2. Execute Agreements Cautiously

Navigating NIL deals can be tricky. There are various state laws and school policies to consider, along with a number of legal “gotchas” to avoid. Here’s how you can safeguard your interests:

- Seek Legal Advice: Before signing any NIL agreement, engage a lawyer with experience negotiating NIL and brand endorsements for athletes. An attorney with expertise in sports contracts can help you navigate the important terms in an NIL deal, such as money, exclusivity, length of the agreement, how the brand can use your name, image, and likeness, and an athlete’s delivery requirements. An experienced attorney will help you spot potential pitfalls and ensure the agreement aligns with your long-term goals.

- Beware of “Standard” or Simplistic Agreements: When someone refers to a contract as “standard” or provides an overly simplified agreement, that should throw up a red flag. All it takes is the slightest language in your agreement to give a company unfettered rights to use your name, likeness and image in ways you never intended.

- Follow Regulations: An experienced advisor will help you navigate specific laws and policies set by your state, school, and the NCAA regarding NIL deals. For example, you cannot share photos or videos in your team uniform with logos from other brands without first getting permission from your school or the brands.

3. Budget Wisely for the Long Term

While newfound wealth can be exhilarating, it’s crucial to manage your finances wisely:

- Prioritize Needs Over Wants: When it comes to spending, prioritize essential needs over extravagant wants. Understand this financial windfall may be a one-time occurrence, so focus on building a secure future rather than indulging in immediate gratification.

- Future-Proof Your Earnings: Instead of assuming this is a continuous stream of income, treat each deal as if it were your last. Create a budget that accounts for potential future earnings and uncertainties, ensuring you’re prepared for any scenario.

- Explore Tax Mitigation Strategies: Consider tax mitigation strategies, such as retirement planning and deferral opportunities, to minimize your tax burden. Consulting a financial advisor can help you explore these options.

Make the Most of Your NIL Opportunities

The legalization of NIL in college and high school sports represents an exciting shift for young athletes. It can offer game-changing money, enabling you to take care of your financial needs, along with building your brand for future growth. But with great success also comes great responsibility. Even professional athletes who’ve reached the highest pinnacles of their respective sports can end up without the financial resources they need if they don’t plan ahead.

The good news is by recognizing the potential pitfalls and seeking professional guidance early in your NIL journey, you can better position yourself for long-term financial success. Remember, it’s not just about profiting from your name, image, and likeness today, but also securing your financial future for tomorrow.

How We Can Help:

Our Entertainment, Sports, and Media practice understands the unique challenges athletes face at all stages of their financial journey. Whether you need assistance with tax planning, contract negotiations, or financial strategy, we’re here to guide you toward a successful future in the world of sports and NIL deals.

This article was co-authored by Leron E. Rogers, Partner at Fox Rothschild LLP.

]]>- Now that a recession seems imminent, it’s important to prepare by adopting state and local tax planning techniques now.

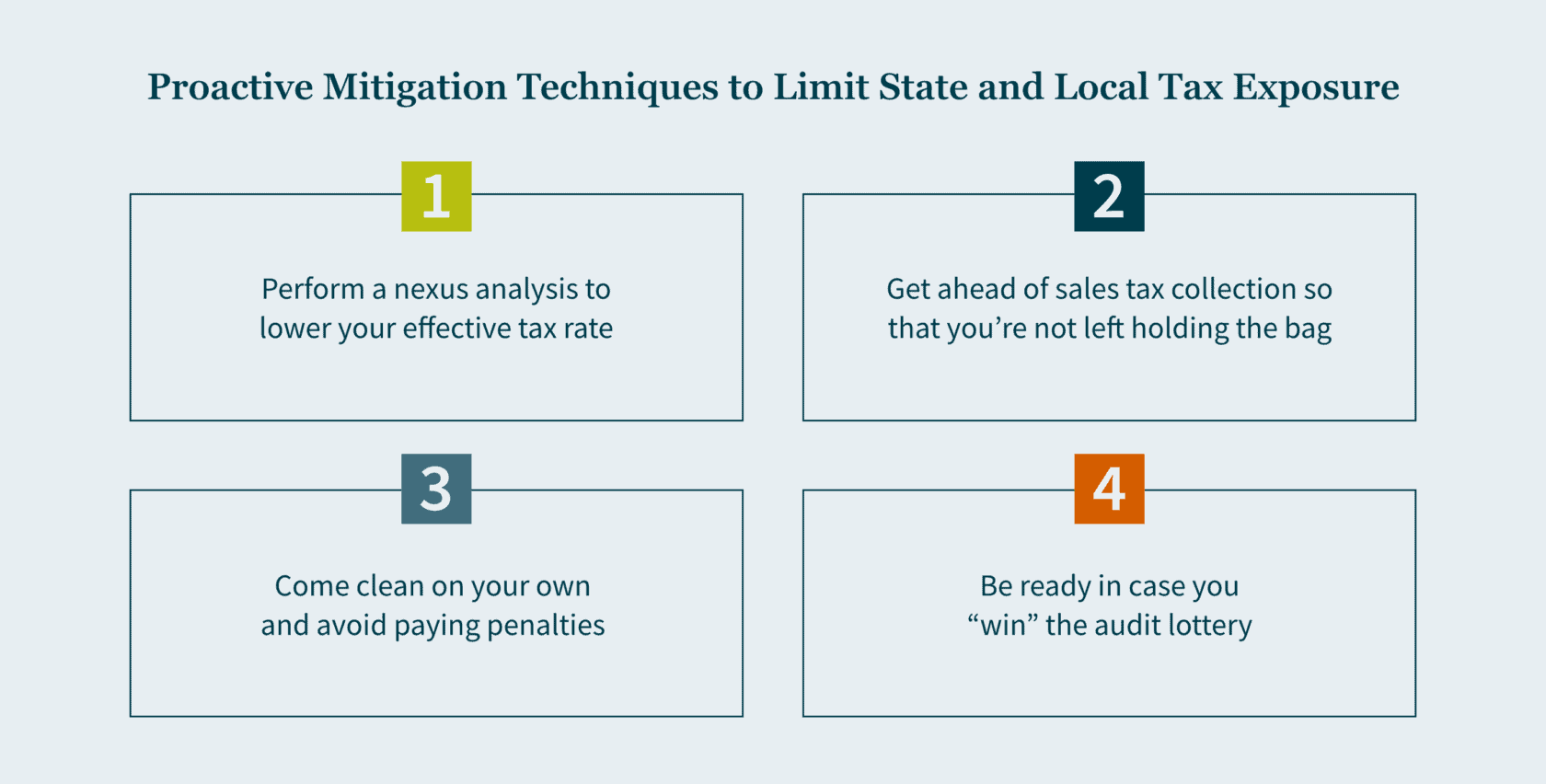

- These techniques include performing a nexus analysis to lower your effective tax rate; getting ahead of sales tax collection so that you’re not left holding the bag; coming clean on your own to avoid penalties; and being ready to win in case you “win” the audit lottery.

- Right now, you should be taking proactive measures to avoid overexposure and capitalize on opportunities that limit your overall tax burden.

Despite a seemingly robust economic recovery from the COVID-19 downturn, we are now looking down the barrel of another recession. When polled for a Wall Street Journal survey, more than three in five economists predicted a recession will occur over the next year due to a variety of reasons: inflation has hit a 40-year record high, the Fed has raised interest rates to the highest levels in more than 15 years, and several Fortune 500 companies have implemented mass layoffs. In addition, market volatility prompted by the implosion of Silicon Valley Bank and Credit Suisse has sent regulators around the globe into damage control.

While no one can predict the future — and if the COVID-19 pandemic has taught us anything, it is that the economy won’t follow the course of even the most prescient prognosticators. To prepare for the proverbial rainy day, in the following our State and Local Tax team details state and local tax planning techniques you can adopt now.

Technique #1: Perform a nexus analysis to lower your effective tax rate

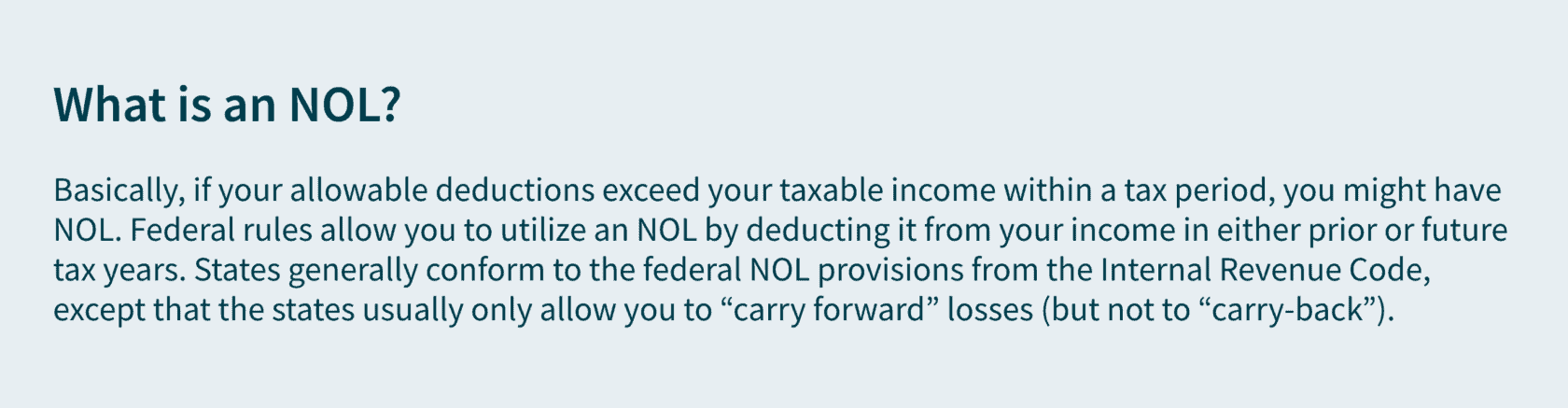

Typically, a nexus analysis is performed “defensively” when you’re under the threat of an audit or to identify potential tax exposure … and that usually means an increase in state tax. But you should also consider performing a nexus analysis “offensively” as a method for lowering your effective tax rate – either by capturing net operating losses (NOLs) in states where you haven’t previously filed or by lowering apportionment in high-tax jurisdictions.

This first idea rests on the principle that you can’t claim NOL deductions on returns you never filed. If your company historically operated at a loss (for tax purposes), a nexus analysis might not have been on your radar; or maybe you had a nexus analysis done, but then decided not to file returns where there wasn’t a material exposure. But if in 2022 or later years, you were or expect to be profitable and you’ve been doing business online or in multiple states, identifying potential prior year state income or franchise tax filings may allow you to claim the benefits of the federal NOLs on your state returns by carrying the losses forward to offset current or future taxes.

Note, current federal rules allow you to carry NOLs forward indefinitely until the loss is fully recovered, but they are limited to 80% of the taxable income in any one tax period. States do not always follow these rules, and moreover, state apportionment rules will affect how much of the NOL is allocated to a given state. Therefore, you’re not likely to see a “one-to-one” application, and you may still owe some taxes, but under the right circumstances, this technique will go a long way towards mitigating exposure for state income taxes that you may owe in the future.

Another way that increasing your state tax filings may decrease your state tax liability is by taking advantage of “economic nexus” developments to “spread out” your state tax liability across jurisdictions where rates may be lower (i.e., reducing your “effective tax rate”). Many states impose “throw-back” rules that require you to treat sales to states where you don’t pay taxes as if those sales should be sourced to your home state. But if, under economic nexus, you should or could be paying tax in those jurisdictions, you may be able to reduce the payment in your home state. Similarly, differences can arise between state’s rules for sourcing sales of services or intangibles that may be particularly helpful when considering how to treat a large item of gain from a sale of a business asset (e.g., stock in a subsidiary, or a valuable piece of intellectual property).

A few example scenarios illustrate these techniques:

- SoftDev Corp. started developing a SaaS product in 2019 and then testing its prototype apps online. They have employees that work remotely from home offices in five states. While SoftDev had potential nexus due to the economic activity in several states and payroll in the other five states, they only filed in their state of corporate domicile because sales were not significant, they had losses on their federal return, and the cost to prepare the other returns exceeded their compliance budget. In 2022, SoftDev expanded its product offering and began seeing significant sales in all 50 states. For federal tax purposes, they have accrued a large NOL that will reduce taxable income for the year (and probably several years to come). It would be wise to perform a nexus analysis at this point to identify whether SoftDev can capture any NOLs in other states – the key qualification being whether there is significant apportionment in the prior years as this will drive the amount of NOL available.

- Cal Widget Co. sells widgets (tangible personal property) it manufactures in California to customers all along the west coast and all its operations, including its one warehouse, are in California. Historically, Cal Widget only files a return in California, where it has 100% apportionment because of the throwback rule, and thus pays 8.84% on all its taxable income. However, by filing in additional states, the throwback rule would not apply to those sales, and thus they wouldn’t be “thrown back” to the California numerator of the apportionment formula. Even without paying tax to the other state, if Cal Widget could show that they would have owed tax under California’s rules, but for the fact that the state does not apply tax under those circumstances, the sales could still be removed from the California numerator. For example, if 50% of sales were to California customers, 25% went to customers in Oregon (average rate = 7%), and the remaining 25% went to Washington (no corporate income tax), using this method, Cal Widget could reduce its effective state income tax rate from 8.84% to 6.17%.

- Big Apple Co. has found a buyer for its signature logo and is anticipating a major gain event in 2023, and they realize that based on prior years, they’ll be paying New York State and City tax on the entire amount of gain because it’s the only state in which they’ve ever filed state income tax returns. If they are proactive, though, they can identify multiple states in which they have received revenue and can justify filing based on “economic nexus” and “market-based” sourcing principles – this won’t change New York’s tax rate, but it will provide a reason to apportion more of the income to source outside of the state and could save significantly on their tax bill.

Oftentimes, businesses are reluctant to really dig deep into nexus issues because they’re afraid of what they might find. And they end up waiting to take action until after they receive notices or their auditors (or worse, potential buyers) start asking about uncertain tax positions and accruals. But a slow-down in business due to the recession may offer you the opportunity to catch up on these nexus issues proactively.

Technique #2: Get ahead of sales tax collection so that you’re not left holding the bag

In a perfect world, when a company is properly accounting for, collecting, and remitting sales tax, there should be no (or at least very little) effect on revenue. Sales tax shouldn’t cost the business anything – instead, the business’ customers should be economically liable for the cost, while the business itself is only responsible for reporting and remitting the tax to the appropriate tax authority.

Problems arise when the business fails to account for sales tax and then only discovers the liability after the transactions have occurred and when it is no longer feasible to collect the individual sales tax amounts from customers. Then a cost that you could have passed through to your customers becomes your cost.

If you’re not currently collecting sales tax, you might consider a few of the “red flags” below:

- Your business generates revenue online through a website, Software-as-a-Service, or another cloud-based product.

- Many states treat SaaS (and similar cloud-based products) as they would other types of software, which are generally taxable.

- What’s more, since you’re selling online, you may be subject to “economic nexus” without ever creating a physical presence in the location.

2. Your business processes payments online on behalf of other businesses making retail sales.

- Since you are the party processing the transaction, you may be required to collect sales tax as a “marketplace facilitator,” even though you’re really just a company providing services to other businesses.

3. Your business provides services, so you haven’t really been concerned about sales tax in the past because you know it generally only applies to tangible personal property (TPP) … but consider whether:

- You make some related sales of TPP when you are providing services (e.g., you design custom web infrastructure and occasionally sell specialized hardware to meet your client’s specifications);

- The services you sell are computer programming and the end-product is typically custom software;

- One division of your business is leasing goods from another division; or

- Your services are taxable because they are dependent on, or related to, sales of TPP (e.g., third party software maintenance).

You can avoid this pitfall and ultimately save money by being proactive about identifying potential sales tax requirements and implementing systems to ensure you are properly collecting the tax.

Technique #3: Come clean on your own and avoid paying penalties

If your business sells products or services in multiple states, you could face unexpected tax liabilities for failing to comply with each state’s various income, franchise, gross receipts, sales and use, property, or other taxes. You may already be aware of the issue, and maybe you even have an accrual for the liability. And compounding any such liability are the interest and penalties that could be asserted if the state eventually discovers the business activity. But you don’t have to wait for the state to come after you, and if you’re proactive, you’ll probably be able to mitigate or remove all the penalties.

Virtually every state has a Voluntary Disclosure Program, under which you can execute a voluntary disclosure agreement (VDA) between your business and the tax authority to limit your liability for back-taxes. One benefit is that the VDA will limit the “lookback” period (otherwise a state can look back as far as the business had activity); this will often reduce the potential tax liability itself. Another benefit of a VDA is that any penalties that might have applied for late filing or payment are waived (though interest usually still applies). Finally, by going through the VDA process you are put in contact with a tax authority representative who can help you to determine precisely what rules apply to the business – they won’t exactly be a “tax adviser” but sometimes simply getting a hold of someone who will address your questions is challenge. And the certainty you will get from the process will give you comfort that your tax compliance process going forward is correct.

On top of state VDA programs, many states will offer amnesty programs. They usually are only available for a brief period (e.g., six months), have similar terms to a VDA, but are more relaxed in terms of eligibility. Let’s say you’ve been filing for five years, and you stop doing business in a certain state. You receive penalties and notices, and you ignore them — you aren’t doing business there anymore. But during the recession, you need to expand back into that state for additional customers. If you want to resume your business there, an active amnesty program may allow you to set up shop without having to pay penalties on the missed filings.

With the country entering a recession, business profits are likely to decrease, and so too will state revenues; under these circumstances, state governments are more likely to offer these amnesty programs as they seek to expand the tax rolls. Be on the lookout if a VDA isn’t an option for you.

Technique #4: Be ready in case you “win” the audit lottery

Not only do state governments seek out delinquent taxpayers through amnesty and VDA programs during a recession, but they may also seek out additional tax revenue through audits. For state income taxes, we’re likely to see a surge in audits surrounding online work and remote workers because of increased popularity in remote work over the last few years. In addition, states perennially test a business’ “unitary” status (i.e., whether a given item of income should be apportioned between several states or allocated to the corporate domicile) and therefore any significant sales of business assets in the last couple of years may make you a target.

Ultimately, this is the time to be more introspective: look back on your last few years and figure out if you had any gaps in recording. If there are opportunities to capture NOLs or other additional savings, bookmark those too. It’s best to be prepared, because while there’s no guarantee you’ll be met with an audit, there’s no question that state governments increase their audit activity during a recession.

How MGO can help

A recession affects everyone, and state and local governments are no exception — which, in turn, affects you and your business. These techniques can help you prepare for whatever’s coming, ensuring you’re ready for potential audits and losses along the way. MGO’s State and Local Tax team provides experienced guidance to help you avoid overexposure and capitalize on opportunities that limit your overall tax burden.

]]>Here’s what you need to know to claim it:

- It’s a one-time abatement of any “timeliness” penalties incurred on individual income tax returns (Form 540, Form 540NR, Form 540 2EZ) for tax years beginning on or after January 1, 2022.

- It’s only available to individual taxpayers subject to personal income tax law (so estates, trusts, and fiduciaries aren’t eligible).

- It can be requested verbally or in writing starting on April 17, 2023.

- For California taxpayers who qualify for an extended 2022 income tax return due date because of the California Winter Storms (i.e., most California taxpayers), the “timeliness” penalties that would be abated through this program should not start being imposed until after the new extended due date for that tax year – October 16, 2023.

Which penalties are eligible?

Both the Failure to File Penalty (i.e., you did not file your tax return by the due date nor did you pay by the due date of your tax return) and the Failure to Pay Penalty (i.e., you did not pay the entire amount due by your payment due date) on California individual income tax returns for tax years beginning on or after January 1, 2022 are eligible for the one-time penalty abatement.

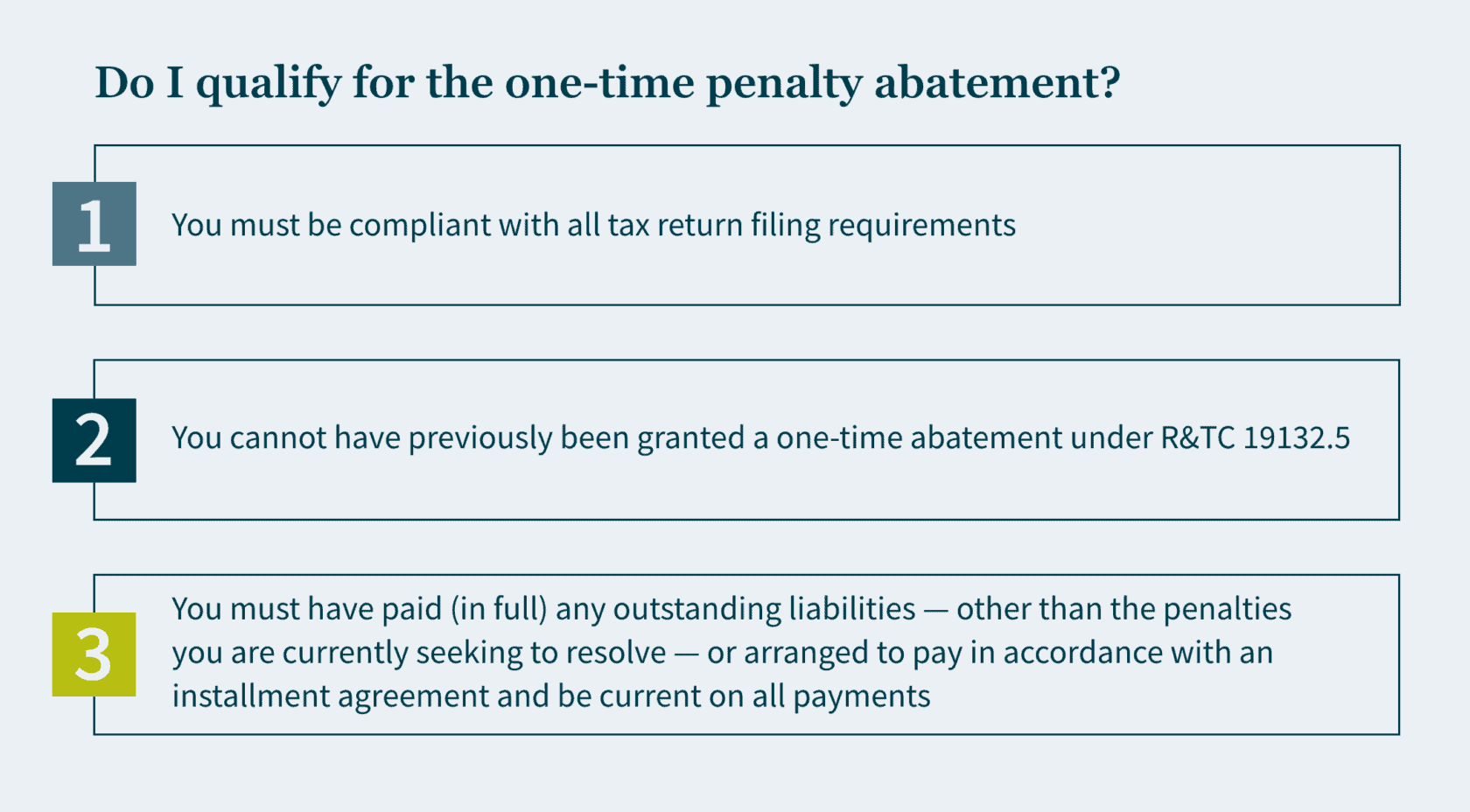

How do I qualify?

How do I request a one-time penalty abatement?

You can mail in a completed Form FTB 2918 or call the FTB at +1 (800) 689-4776 to request penalty abatement.

What if I can provide that I had reasonable cause for late filing or late payment?

If you can demonstrate that you exercised ordinary care and prudence and were nevertheless unable to file your return or pay your taxes on time, then you may qualify for penalty relief due to reasonable cause. Reasonable cause is determined on a case-by-case basis and considers all the facts of your situation.

You may request penalty abatement based on reasonable cause by mailing in a completed Form FTB 2917 or by filling out a reasonable cause request on your MyFTB online account. Penalty abatement based on reasonable cause may – depending on the circumstances – be preferable to using up your one-time penalty abatement request.

How we can help

If you need help with relief for your “timeliness” penalties or if you need help with any other state and local tax matters, please reach out to our experienced State and Local Tax team.

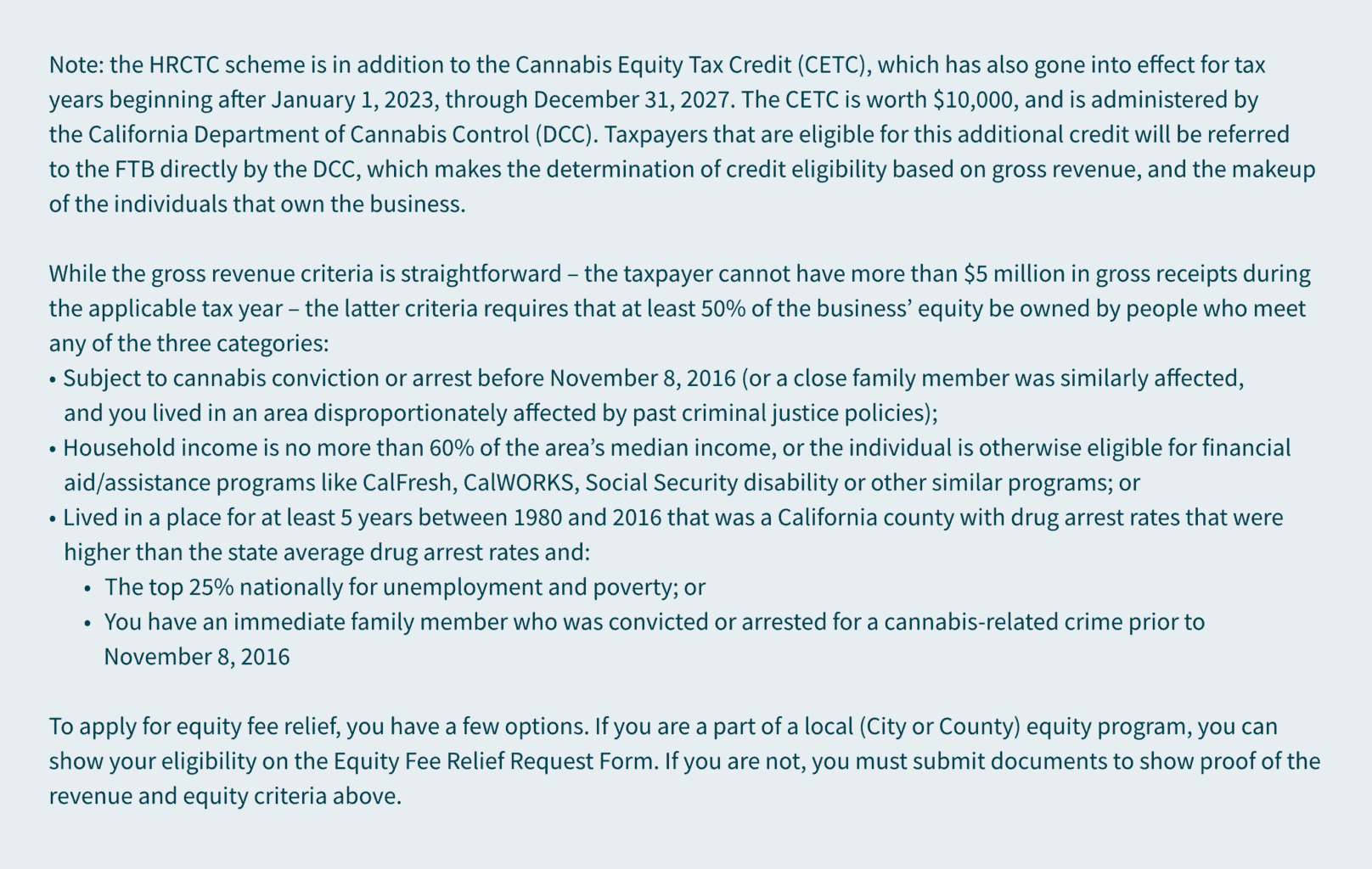

]]>- California now has a new tax credit called the High-Road Cannabis Tax Credit (HRCTC) available for eligible cannabis retailers and microbusinesses.

- The credit is available for tax years starting after January 1, 2023, through December 31, 2027, and can be applied against current year (and future) income taxes.

- To claim it, you must make a “tentative credit reservation.”

- Expenditures that qualify include wages for full-time employees; safety-related equipment, training, and services; and workforce development and safety.

While the cannabis industry in California has been struggling on many levels, tax credit relief has come in the form of excise tax changes for distributors and has now arrived for retailers. The High-Road Cannabis Tax Credit is a new tax credit from the California Franchise Tax Board (FTB) available for cannabis retailers or microbusinesses for taxable years beginning January 1, 2023, through December 31, 2027. In order to capitalize on this opportunity, eligible calendar-year taxpayers must make a tentative credit reservation during the month of July to claim the credit on their 2023 CA income tax return.

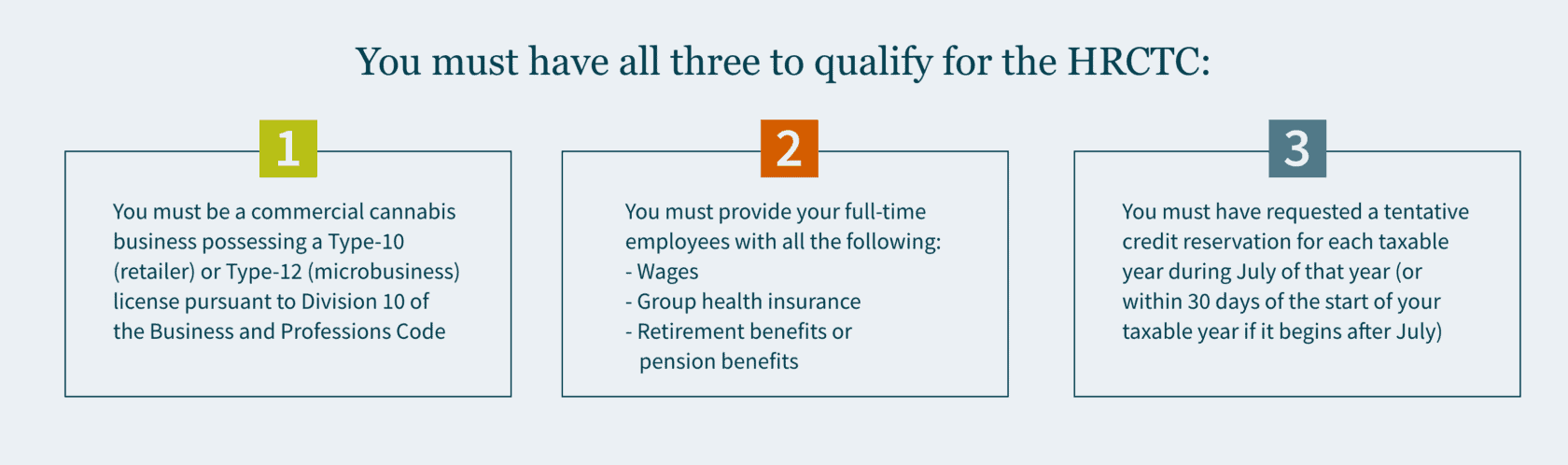

Who qualifies for the HRCTC

To be eligible, you would need to meet three basic requirements.

Which expenditures qualify for the HRCTC

There are several types of expenditures eligible for the credit with specific parameters that you would need to meet to qualify for them. Qualified expenditures are amounts that you have paid or incurred for any of the following expenses.

Wages for full-time employees

Not every employee has to meet these requirements — but for those that do, their wages count as a qualified expenditure. First, full-time employees must be paid for no less than an average of 35 hours per week — or they must be a salaried employee paid compensation for full-time employment.

In addition, full-time employees must be paid no less than 150% ($23.25) but no more than 350% ($54.25) of the state minimum wage. To meet the 150% minimum wage requirement, you may include the following employee benefits in qualified wages: group health insurance, childcare support, employer contributions to employer-provided retirement plans, or contributions to employer-provided pension benefits. But if you pay employees wages that surpass more than 350% of the state minimum wage, those wages are not considered a qualified expenditure.

Safety-related equipment, training, and services

Expenditures related to safety, training, and providing services can also qualify if they meet the following criteria:

- Equipment primarily used by the employees of the cannabis licensee to ensure personal and occupational safety, or the safety of the business’s customers.

- Training for nonmanagement employees on workplace hazards. (This includes safety audits, security guards, security cameras, and fire risk mitigation.)

Workforce development and safety

Qualified training for your employees includes:

- Joint labor management training programs

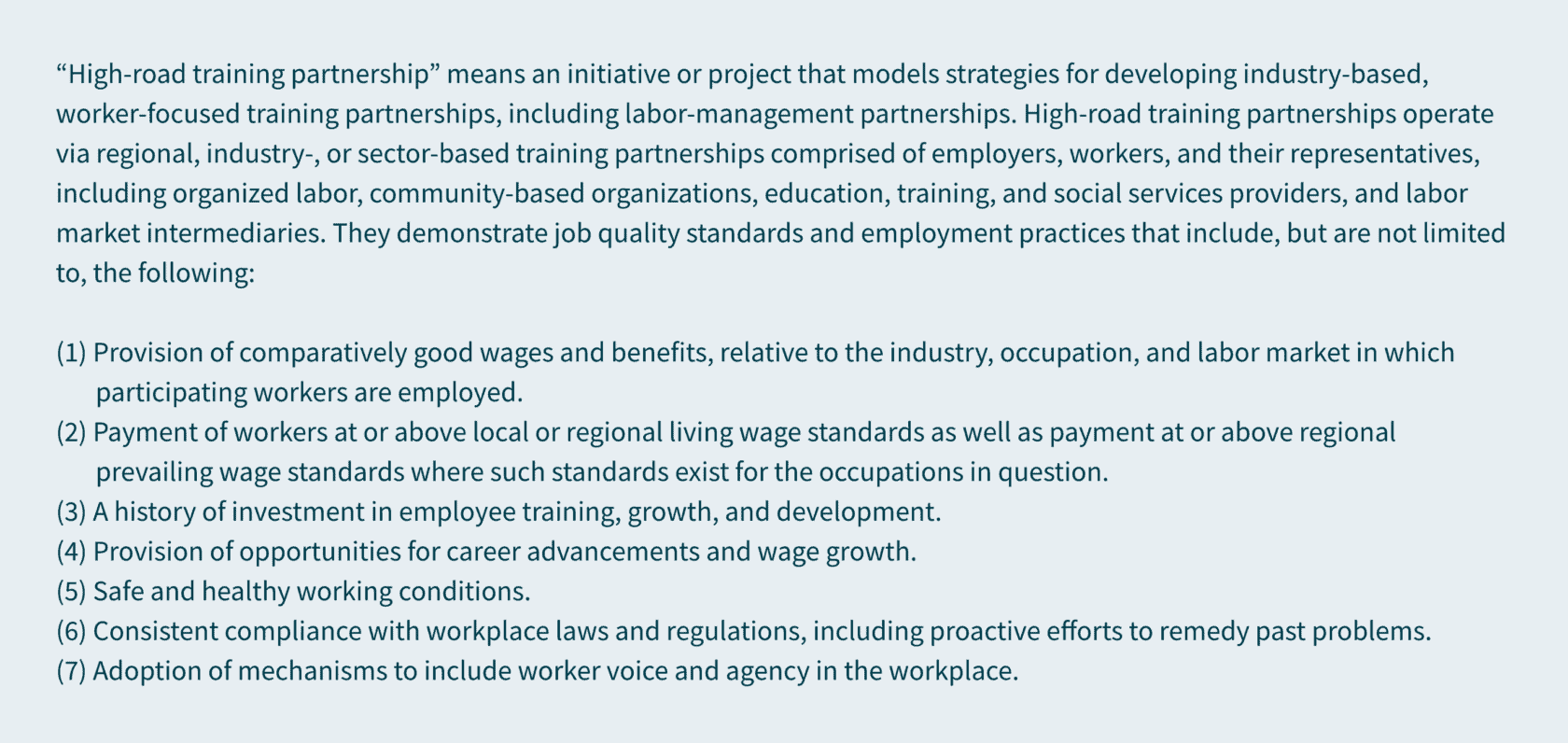

- Membership in a joint apprenticeship training committee registered by the Division of Apprentice Standards, and a state-recognized “high-road training partnership” (as defined in Section 14005 of the Unemployment Insurance Code).

Available credit

The amount of available credit is equal to 25% of qualified expenditures. The aggregate credit that can be claimed by each taxpayer (as determined on a combined reporting basis) is a maximum of $250,000 per year. Any unused credit can be carried over to the following eight taxable years. Availability is limited as the total cumulative amount of HRCTC available to all taxpayers is $20 million.

To claim the HRCTC on your California tax return, you must reduce any deduction or credit otherwise allowed for any qualified expenditure by the amount of the HRCTC allowed.

How do I make a tentative credit reservation — and when?

You must make a tentative credit reservation (TCR) with the FTB to claim the credit. This reservation must be made online and once you’ve done so, you’ll receive an immediate confirmation. FTB currently reports that the system will be up and running by July 1, 2023, but you can start preparing now.

How we can help

The HRCTC is a valuable tax credit opportunity for any commercial cannabis business operating in California. Determining if you qualify and calculating how much you can save could be complex. Our extensive experience in cannabis, cannabis tax, and state and local tax enables us to help you take advantage of this tax credit so you can stay focused on thriving in this ever-growing, culture-shaping industry.

Reach out to MGO’s State and Local Tax team to find out whether you qualify for this tax credit opportunity and determine how much you could potentially save.

]]>

- The Supreme Court of Washington State issued a landmark ruling maintaining the constitutionality of the state’s capital gains tax (CGT) by determining that it’s an excise tax, or a tax on a good or service (and not a property tax).

- It’s imposed at a rate of 7% and taxpayers can claim a standard deduction of $250,000.

- There are other deductions, like long-term gains from the sales of qualified family-owned small businesses and charitable contributions of more than $250,000.

- You may be able to apply a tax credit.

On March 24, 2023, the Supreme Court of Washington State (SCOWA) ruled 7-2 to uphold the constitutionality of the state’s controversial capital gains tax. Thus, by the April 18, 2023, deadline, Washington residents recognizing capital gains income (and nonresidents engaged in transactions occurring within the state) in 2022 will have to calculate this new tax and pay accordingly.

Our State and Local Tax team breaks down what you need to know about this divisive tax with an impending deadline.

The details about CGT

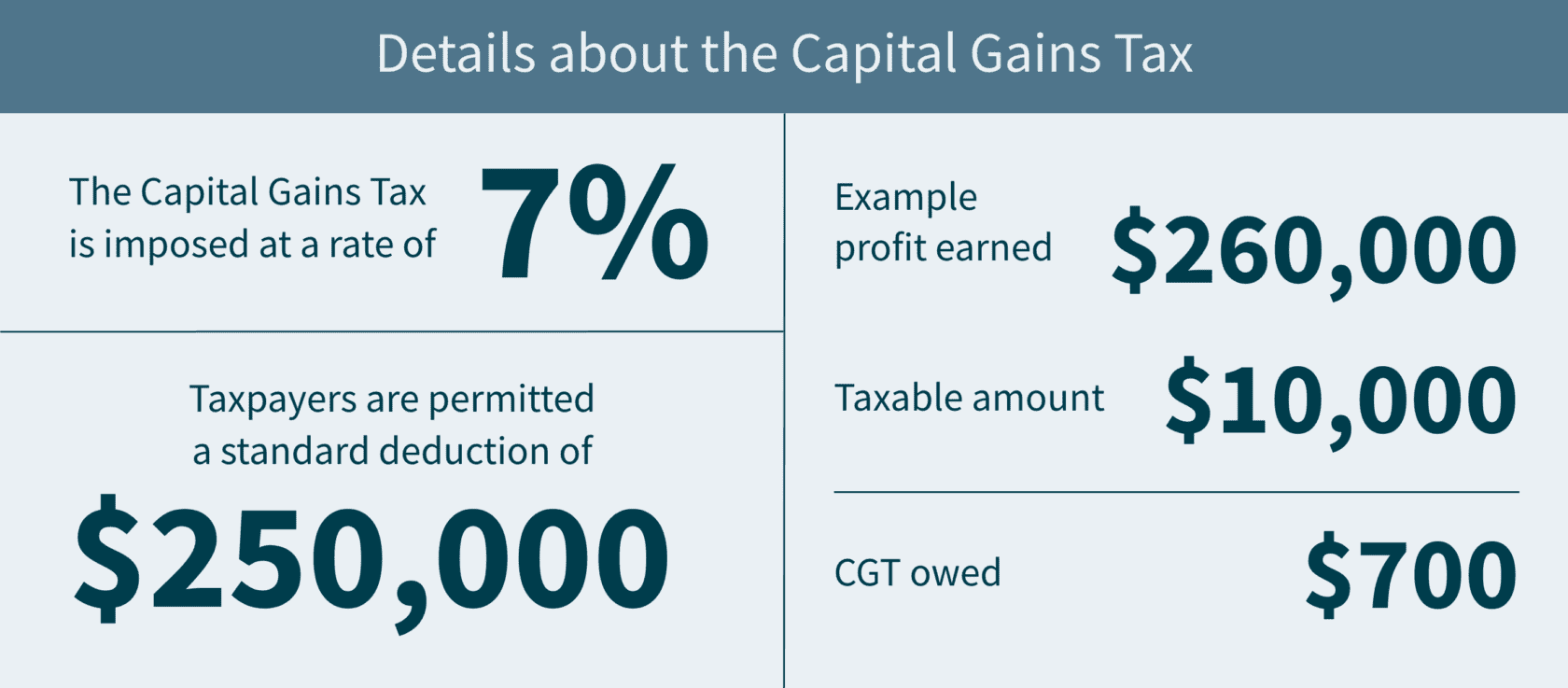

The CGT was created when Washington enacted Senate Bill 5096 in April 2021 with the intention of having the excise tax proceeds — projected to be nearly $415 million — fund the state’s early education and childcare programs. Charged on long-term Washington-allocated capital gains, the CGT is imposed at a rate of 7% of an individual’s federal capital gain from a sale or exchange of long-term investments that exceed $250,000. This includes stocks, bonds, businesses, and other assets.

The controversy of CGT

This bill has generated controversy since its inception — mostly because it is categorized as an excise tax and not an income tax (Washington is one of nine states that doesn’t have income tax due to limitations in the state constitution on the state government assessing a tax on “property”). As a reminder, an excise tax is a legislated tax on the sale of specific services, activities, or goods.

In March 2022, the Douglas County Superior Court in Washington deemed the CGT unconstitutional as an impermissible income tax that is only masquerading as an excise tax. The Court defined gains as income, and therefore property under the Washington Constitution, that the state impermissibly taxed at a non-uniform rate (i.e., the tax doesn’t apply to every resident equally, but only those whose profits exceed the $250,000 threshold). In the past, Washington’s Supreme Court has considered income as property — and property must be taxed at a flat rate.

Since state revenue relies on sales and business taxes, taxpayers who earn the least will end up paying a higher share of their income in tax. This notion has split public opinion. Community groups and labor unions believe the tax is not just legal, it’s necessary because of its capability to create a more equitable tax system. But organizations with business interests in mind find it to be bad public policy in addition to violating the constitution.

However, the Washington Supreme Court ruled to uphold the tax, agreeing it is constitutional as an excise tax — “levied on the sale or exchange of capital assets, not on capital assets or gains themselves.” In other words, the Court reasoned that the tax is tied not to the person’s ownership interest in the property (which would be unconstitutional), but on the transaction itself.

Calculating your tax base

Adjusted capital gains

As mentioned, the new tax is imposed on your adjusted capital gains allocated to Washington, minus allowable deductions and exemptions. First, it starts with your federal net long-term capital gain for the tax year. It’s then adjusted by adding back long-term capital losses from sales or exchanges that are exempt or not allocated to the state. Finally, you subtract your long-term capital gains from sales or exchanges that are exempt or not allocated to the state.

Deductions

There are several deductions allowed against adjusted capital gains. Individual taxpayers are permitted a $250,000 standard deduction in calculating the CGT. But married or state-registered domestic partners that file a single federal tax return collectively have only a single $250,000 deduction. For example, if you earned $260,000 in profit from selling bonds in the past year, only $10,000 would be taxed, and the CGT owed would be $700. And if you and your husband together earned $260,000 from selling bonds, you wouldn’t get to “double” the standard deduction – you’d have the same tax bill.

Additional deductions include long-term gains from the sales of qualified family-owned small businesses, and charitable contributions. Associated regulations do treat the sale or transfer of an interest in a “qualified family-owned small business” as a separate deduction from the charitable deduction. (Note that the “qualified family-owned small business” is not the same as the federal Qualified Small Business Stock (QSBS) tax exclusion — there are separate requirements). To receive the charitable deduction, you would need to contribute over $250,000, not exceeding a deduction of $100,000 in total. Consequently, if you donate $350,000, you’ll receive the maximum deduction.

Exemptions

Certain long-term capital gains and losses from sales of capital assets are not subject to the tax. These exempt items include sales or exchanges of the following types of assets:

- Livestock;

- Timber;

- Real estate, and land structures; and

- Capital assets held in IRAs, 401(k) plans, and other qualified retirement plans

Allocating your capital gains and losses

If you were living in Washington at the time of a sale or exchange of intangibles (e.g., stocks, bonds, etc.), related long-term capital gains and losses are allocated to Washington.

In addition, gains or losses from the sale or exchange of other (tangible) personal property is allocated to Washington if:

- The property was in Washington at any time during the tax year when the sale/exchange occurred,

- You were a Washington resident at the time of the sale/exchange, and

- You were “not subject to the payment of an income tax or excise tax legally imposed” by another jurisdiction* on that long-term capital gain or loss.

* Jurisdiction is defined to include not only U.S. states, political subdivisions, territories, and possessions, but also foreign countries and political subdivisions of foreign countries.

Good news: a tax credit is available

If you’re interested in applying a tax credit against this new tax, you might be able to. Any Washington capital gains tax can qualify as a credit against the Washington business and occupation (B&O) tax — given that the B&O tax includes the gain from a transaction subject to capital gains tax (because it applies to ALL gross receipts regardless of character).

In addition, a credit can be applied for an income or excise tax legally imposed by another jurisdiction on capital gains “derived from capital assets within the other taxing jurisdiction to the extent such capital gains are included in the taxpayer’s Washington capital gains.”

Filing your returns

Remember, a Washington capital gains tax return is required only if tax is owed — and it must be filed on or before the due date of your federal income tax return, including extensions. But the payment of the tax is required BY the original due date of your federal income tax return, NOT including extensions. Any filing and payments must be done online using the MyDOR portal by April 18, 2023, for most taxpayers.

How MGO can help

Keep in mind that while this tax will more than likely impact Washington residents the most, if you are a nonresident whose capital gains from the sales and exchanges of your tangible personal property is allocated to Washington, you could be affected too. Accordingly, anyone with a large gain event (other than the sale of real property) during 2022 or later years, should consider whether this tax may affect them.

MGO’s State and Local Tax team can help you prepare and file this return and manage any of the other surprises that can occur in state and local tax. Contact us if you have additional questions about how the capital gains tax impacts your finances, or if you’re interested in additional strategies to boost your tax efficiency.

]]>- California Governor Newsom strives to amend the personal income tax laws to prevent wealthy taxpayers from utilizing Incomplete Gift Non-Grantor trusts.

- California residents use this by transferring assets into trusts held by nonresident trustees in states without income tax.

- If this legislation passes, taxpayers will no longer be able to take advantage of the strategy.

If you reduce California income tax with an ING, Newsom is onto you

Californian legislators propose to amend the personal income tax laws to close a little-known-but-effective loophole for the wealthy by targeting Incomplete Gift Non-Grantor (ING) trusts set up in other states with more favorable income tax rules. To date, California residents have had the opportunity to transfer assets into these trusts held by nonresident trustees in states without income tax, utilizing the state’s sourcing rules to avoid the tax. If approved, this new legislation will put a stop to this tax planning strategy.

Taxing the rich in California

As it stands, the ING trust is not commonly used. There are about 1,500 California residents with this trust in states without income tax — and if implemented, California would see a minimal revenue increase (about $30 million in the first year and $15 million in the following years). However, this would put an end to a tax planning strategy the wealthy have been using to their benefit for about 20 years.

Because California is home to more billionaires than any other state at the same time as it also has the highest rate of poverty in the U.S., the concept of taxing the rich holds a certain appeal. In the past, Newsom has opposed proposals to raise taxes — but this proposal was included in the governor’s $223.6 billion budget plan for the next fiscal year, which begins in July. Whether the item survives the legislative process remains to be seen, but if New York’s passage of a similar law in 2014 is any indication, we are likely to see the end of this tax planning strategy for California’s ultra-rich.

Moreover, this proposal has a retroactive element, differentiating it from New York’s and opening it up to potential lawsuits (New York trust holders had a five-month period to move their accounts to a different type of trust without incurring the tax). Newsom is pushing for the measure to begin the calendar year after its implementation.

How the ING works (worked)

What is an ING, and why is Newsom trying to prevent its use? California taxpayers can transfer their assets into out-of-state, incomplete, non-grantor trusts (INGs), which constitute separate, taxable entities under state and federal tax law, and this move avoids California income tax on any appreciation or gains from those assets because it is “sourced” to another state based on the location of the trustee (i.e., the bank or whatever financial institution offers the trustee services in the other state). The non-grantor aspect comes into play when the taxpayer establishing the trust (the “grantor”) gives up control over managing investments or distributing assets to the trustee (contrast with a “grantor trust” in which the grantor continues to control how money is invested/distributed within the trust during their lifetime). For the trust to be deemed “incomplete,” the grantors specify how the money can be used.

Some of the states where these trusts are typically established include Florida, Wyoming, Delaware, Nevada, Tennessee, and South Dakota. For example, a California resident (TP) may decide to transfer stock in their business into an ING established in South Dakota. If TP held the stock directly, then as a resident, all the dividends (or if he sold it, the gain) would be taxable by California on their personal income tax return. But since TP doesn’t hold the asset – the ING does – the ING recognizes the income relating to the stock. California’s current rules provide that the income is sourced to (and thus taxable in) the state where the trustee is domiciled, and for this ING that location is South Dakota, which, incidentally, does not tax this sort of income.

Newsom is hoping that by eliminating this tax-free option, the state of California will be able to increase tax revenue in a way that will not alienate a large number of voters.

How MGO can help

If you are a California resident and currently use an ING as a tax strategy, there are steps to take now to avoid a negative impact. MGO’s experienced Private Client Services team can help you identify and implement an effective response.

]]>Giving state and local governments the resources to protect against hackers

The SLCIA updates the Homeland Security Act of 2002 to give the DHS leeway to utilize centers like the Cybersecurity and Infrastructure Security Agency (CISA) and Multi-State Information Sharing and Analysis Center (MS-ISAC). This will allow them to work with state, local, tribal, and territorial governments as needed, upon request.

This collaboration will encourage conducting cybersecurity exercises and hosting trainings meant to address current or future cyber risks or incidents. It will also provide operational and technical assistance to state and local governments to implement security resources, tools, and procedures to improve overall protection against attacks. The goal is to provide state and local governments with the support they need to defend themselves from hackers.

Resources to bolster government security capabilities

The SLCIA establishes a $500 million DHS grant program that will empower government institutions to increase their focus on cybersecurity. The bill also:

- Requires CISA to develop a strategy to improve cybersecurity of state, local, tribal, and territorial governments, enabling them to identify federal resources to capitalize on as well as set baseline objectives for their efforts;

- Indicates state, local, tribal, and territorial governments must develop a comprehensive cybersecurity plan to guide their usage of any grant money they receive;

- Establishes a state and local cybersecurity resiliency committee made up of representatives from state, local, tribal, and territorial governments to provide awareness of cybersecurity needs; and

- Enjoins CISA to assess the feasibility of a rotational program for the detail of approved government employees holding cyber positions.

The bill gives state and local governments the push they need to begin defending their networks. This can include the development of new strategies to boost their cybersecurity capabilities and acquisition of the funding needed to ensure their implementation. By investing in cybersecurity ahead of an attack, an entity is more likely to save money and protect its data.

Assessing eligibility for cybersecurity grants

Cybersecurity grants are available to municipalities of all sizes — but it’s important to start strategizing now by considering your IT infrastructure and cybersecurity frameworks. By applying for the grants, you indicate that you are taking your entity’s security seriously and taking the proper steps to qualify.

The State and Local Cybersecurity Improvement Act will provide up to $1 billion in grants for state, local, tribal, and territorial governments, allowing them to directly address their cybersecurity threats and risks. The program’s funding starts at $2 million for 2022, $400 million for 2023, $300 million for 2024, and $100 million for 2025.

To be eligible, an entity must:

- Maintain responsibility for monitoring, managing, and tracking its information systems, applications, and those user accounts owned and operated by the government;

- Show it has a process of continuously prioritizing the assessment of its cybersecurity vulnerabilities and threat mitigation practices; and

- Have a tangible plan that outlines:

- How to manage and audit network traffic.

- How the government plans to use the information to improve its systems’ resiliency and strength.

Our perspective

While the bill is still waiting on the Committee on Homeland Security and Governmental Affairs there are some things you can do to make sure you are ready. State and local governments should focus on building teams that can handle the grant application process — and be prepared to implement once awarded. This bill indicates that governments are past the point of merely updating a firewall or running a generic virus program — things like multifactor authentication and zero-trust architecture are viewed as the next steps (which was required for federal agencies in a 2021 executive order).

How we can help

Prior to starting the grant application process, your IT leaders should start thinking about how to handle security gaps with various procedures and consistent tests. MGO can help. Our Technology and Cybersecurity team can provide guidance as you prepare for the future.

About the authors

Francisco Colon is a Partner at MGO with extensive experience in external audit, fraud examinations, litigation support, operational and internal controls reviews, and buyer/seller due diligence. He specifically focuses on assisting organizations with evaluating and updating their internal controls with a focus on strategic alignment and fraud litigation deterrence management in a variety of industries, including tribal government, gaming, technology, cannabis, hospitality, government contracting, distribution, manufacturing, and private equity. Contact Francisco at FColon@mgocpa.com.

]]>To read more about how California’s PTET works from our Insight Library, see here and here.

California’s PTET considerations

To make the election in California for tax year 2022, eligible entities must pay in the greater of $1,000, or 50% of the 2021 PTET liability, by June 15, using FTB 3893. Entities that fail to make this “safe harbor” payment will not be able to make the election on the 2022 tax return. (Note: The election can only be made on an entity’s timely filed original tax return.)

New York extends its 2022 PTET deadline

Previously, the deadline for making the 2022 election was March 15, 2022, but recent legislation not only extended the deadline but also increased the amount of benefit for resident S corporations. Under the prior legislation S corps could only make the election as to the portion of income that is sourced to NY; however, new legislation (A10080/S8948) enables S corporations, for which all owners are New York residents, to include income from all sources, which has the effect of increasing the amount of available credit on the individual owners’ returns. And because these rules went into effect after the PTET election due date for tax year 2022, New York extended its PTET election deadlines for all taxpayers. Now, passthrough entities can make their PTET election any time by or before September 15, 2022.

Accompanying the deadline extension is a new schedule of estimated payments, contingent on when the eligible entity makes the election. Taxpayers must still pay the entire amount of estimated PTET liability by the end of the year (90% of the PTET shown on the entity’s return for the taxable year; or 100% of the PTET shown on the preceding year’s return). However, instead of owing 25% each quarter (March 15, June 15, September 15, and December 15), taxpayers that make the election prior to June 15, 2022, only need to pay an amount equal to 25% of the required annual PTET liability by June 15, followed by 50% due in September, and the remaining 25% by December 15. And taxpayers that make the election after June 15 but before September 15, must submit a payment equal to 50% of the annual liability by September 15, with the other 50% due December 15.

You can find links here to make the election and submit payments online.

MGO’s insights

If you missed making the CA election on the 2021 return, the silver lining is that you can now “lock in” eligibility with a payment of only $1,000 on June 15, regardless of the amount of taxable income the entity ultimately reports. If you did make the election on the 2021 return, be sure to pay at least 50% of prior year liability (and consider adding a cushion for good measure), as there does not appear to be a “reasonable cause” exception to the rule.

And remember, most tax professionals have interpreted IRS Notice 2020-75 to allow the entity only to claim a deduction for the expenses actually incurred during the applicable tax year — regardless of whether the entity is on a cash or accrual basis accounting method. This means that if you intend to experience the full benefit of a state’s SALT Cap Workaround on your 2022 tax return, you will need to submit the full amount of PTET liability before the end of the year. Amounts paid after the end of the year but before the return deadline (March 15, for most taxpayers) will be deducted on the following year’s federal tax return regardless of when they are credited to state tax liability.

Thus, if the entity made the election in 2021 and paid the PTET before December 31, 2021, then it should (or should have already) claimed the entire amount of PTET credit as an ordinary expense deduction on its tax return (and reported on the owners’ K-1s, generally, line 13). But if the payment was submitted between January 1 and March 15, 2022, that payment, plus the upcoming payments, will be deducted on the 2022 return alongside the other payments made during the tax year.

Final perspectives

To take advantage of the 2022 CA and NY SALT Cap workarounds, make sure to submit your payment by June 15, 2022 for the California PTET, and your election and any necessary payments by September 15, 2022 for the New York PTET.

Only state PTET payments made during the entity’s fiscal tax year are deductible on that year’s federal tax return, so in addition to meeting the state’s minimum estimated tax requirements to ensure eligibility, consider making grossed-up estimated payments before year end to maximize the economic effect of the deduction on the 2022 return.

The PTET rules are different in every state, and with a near-constant stream of amendments and clarifications from state legislators and tax agencies, you may be unsure what is due when. MGO’s tax team can provide you with reminders for payment submission deadlines and calculate amounts due to help you navigate this opportunity for tax savings.

Please get in touch and see how New York, California, or another state’s PTET can benefit your business.

]]>The SEEF tax rate is $1.10 per ounce of adult-use cannabis sold. New Jersey cultivators must also file the SF-100 monthly tax return to report the amount of usable ounces sold for the adult-use market (even if no sales or transfers of cannabis occur).

This first SEEF payment will cover less than two weeks of the sales made from the start date on March 18, 2022. Moving forward, the SEEF payment is always due by 11:59 p.m. on the 20th day of the month after the end of the previous filing period. If the due date falls on a weekend or legal holiday, the return and payment are due the following business day.

Letters with instructions for making the tax filings were sent out to the licensees in early May.

Some technicalities to keep in mind as you prepare to file:

- Medical cannabis is NOT subject to SEEF.

- SEEF is solely imposed on the Cultivator and is not due again on sales from manufacturers, processors, or retailer sales.

- It will not be paid again at another license level, regardless of whether the cannabis is later for sale as-is or if it has been converted to edible form.

- All cannabis types and categories are subject to the same SEEF rate when sold by a cultivator, no matter the strain, potency, trim or shake — anything that falls under the definition of “usable” cannabis.

In addition to the SEEF, NJ Cannabis operators will also need to contend with sales taxes and locally imposed gross receipts taxes:

- Retail sales of recreational cannabis are subject to the state’s ordinary sales tax under N.J.S.A. 54:32B-3(a). Sales of medical cannabis are not subject to sales tax, but are subject to a special 2% tax until the end of June.

- Depending on the locality, cannabis operators may be subject to the following gross receipts tax rates:

- Cultivation, Manufacturer, Retail – 2%

- Wholesale (Distribution) – 1%

- Returns are generally due quarterly in April, July, October, and January.

If you have any questions about calculating or paying NJ cannabis taxes, or any other state’s cannabis tax, please reach out to our leading cannabis tax practice.

]]>