SPACs are an increasingly popular alternative to traditional IPOs. For many they serve as an accelerated strategy to raise capital. However, they are not without their own unique risks & challenges.

Surging to a record $170 billion this year, SPACs have been called Wall Street’s biggest gold rush in recent years. However, the flood of new activity has triggered additional skepticism among investors and increased scrutiny by the SEC. More than ever, success in the SPACs market hinges on experience and expertise navigating the unique market challenges and regulatory complexities of the SPAC life-cycle:

- Pre-IPO: SPAC Planning and Formation

- IPO: Go-Public Execution and Reporting

- Pre-Merger: Planning and Integration

- Post-Merger: Transition Management

Private equity companies that were planning an IPO or other significant M&A deal before the COVID-19 pandemic will want to weigh the real-world advantages and disadvantages of a SPACs option. As with all transactions significant, intensive planning, vetting, due diligence and other considerations must be undertaken.

MGO’s Private Equity practice has experience with IPOs, RTOs, M&A deals and the unique characteristics of SPAC acquisitions. To understand your options, and the path ahead, please feel free to reach out to us for a consultation.

OUR SERVICES

- Established Services and Solutions for SPACs Sponsors and Target Companies

- Accounting and GAAP Financial Statements

- IPO Readiness

- Audit Liaison

- Financial Due Diligence

- Tax Planning and Structures

- Transaction Advisory

- Forensic Accounting

Questions? Let’s talk.

Get the conversation started today. Contact Us >

Under this Act, foreign companies traded on any U.S. exchanges are required to have their auditors submit to inspection by the Public Company Accounting Oversight Board (PCAOB) in an effort to establish that they’re neither owned nor controlled by a foreign government. With a wealth of Chinese companies trading in the U.S., the legislation is likely to have a significant impact on Chinese companies and their accounting firms, as well as U.S. investors and the capital market, for years to come.

How the HFCAA works

The Act will amend Section 104 the Sarbanes-Oxley Act of 2002, the comprehensive legislation passed by Congress aimed at overseeing the conduct of public companies. Pursuant to the HFCAA, there will be a number of sizable changes.

• First, the Securities and Exchange Commission (SEC) will now be required to identify companies that are utilizing registered public accounting firms located outside the United States that are preventing audits from the PCAOB.

• Additionally, the SEC must prohibit securities trading of these public companies within U.S. markets following three consecutive years of non-inspection. Under the language of the bill, these companies will be prohibited from trading on either a national securities exchange or “through any other method that is within the jurisdiction of the Commission to regulate, including through the method of trading that is commonly referred to as the ‘over-the-counter’ trading of securities.” It should be noted that in the event an issuer receives a trading prohibition, then the issuer is allowed to have the prohibition overturned as long as it is able to retain an accounting firm that can be fully inspected by the PCAOB.

• Also, as part of the Act, there are disclosure requirements for non-inspection years for foreign issuers of securities that utilize firms to prepare audit reports. For instance, they will need to disclose the percentage of shares owned by foreign government entities. They will also need to disclose whether or not foreign government entities have “controlling financial interest with respect to the issue.”

• Finally, there are also disclosure requirements that specifically involve China. According to the Act, the names of each official of the Chinese Communist Party of the board of directors of either the issuer or “the operating entity with respect to the issuer” must be disclosed in their Form 10-K, Form 20-F, and shell company reports. Additionally, it must be disclosed if the issuer’s articles of incorporation (or “equivalent organizing document”) has “any charter of the Chinese Communist Party, including the text of any such charter.”

Potential impact of the HFCAA

While the HFCAA applies to any U.S.-listed company incorporated outside the United States, including Mainland China, Hong Kong, France, and Belgium, it is generally understood as explicitly targeting Chinese companies under the restrictions imposed by the Chinese government.

This Act could lead to an increase in the number Chinese and Hong Kong-based issuers being delisted from U.S. exchanges in the coming years. In fact, according to the list of public companies affected by obstacles to PCAOB inspections, there are more than 200 Chinese companies currently audited by CPA firms in mainland China and Hong Kong that would be negatively impacted. These companies, including popular stocks such as Alibaba Group Holding Ltd – ADR, Baidu Inc, JD.com Inc, and Nio Inc – ADR, could feel the brunt of this new legislation.

Note that the Big Four accounting firms in China are independent from the Big Four in the U.S. and do not meet the audit requirements of the PCAOB since they are under the China’s national security laws and the Chinese Securities Law, which prohibit Chinese companies from providing records “relating to securities business activities” overseas without approval by the Chinese securities regulator. Besides, the imminent enactment would certainly discourage new listing of Chinese companies in the U.S. as it could result in a discount on the trading prices as investors may factor in the potential de-listing risk.

However, it remains to be seen how the SEC implementation will roll out within 90 days of the HFCAA’s enactment, which could be greatly influenced by the new leadership of the SEC. According to Bloomberg, President-elect Joe Biden is expected to pick Gary Gensler to head the SEC.

Additionally, because of the three-year compliance timeline in the Act, Chinese companies may consider several options to mitigate the impending risks. The most likely one is to engage a reputable U.S.-based CPA firm, preferably one that has an established China Group, who understands both the Chinese business climate and the U.S. accounting rules, and most importantly obtain a clean compliance record with PCAOB. Yet, it’s also critical that companies consider other factors such as the investor and make sustainable long-term plan to maintain a legitimate and confident position in US capital markets.

If you have any questions

MGO’s SEC practice has a dedicated China Group experienced with Chinese IPOs, RTOs, M&A deals and the unique characteristics of SPAC acquisitions. To understand your options, and the path ahead, please feel free to reach out to us for a consultation.

Mergers with SPACs have always been an alternative to traditional IPOs. With the IPO market effectively minimized for the time being, SPAC mergers are an increasingly desirable public market liquidity option for private companies.

What the numbers tell us

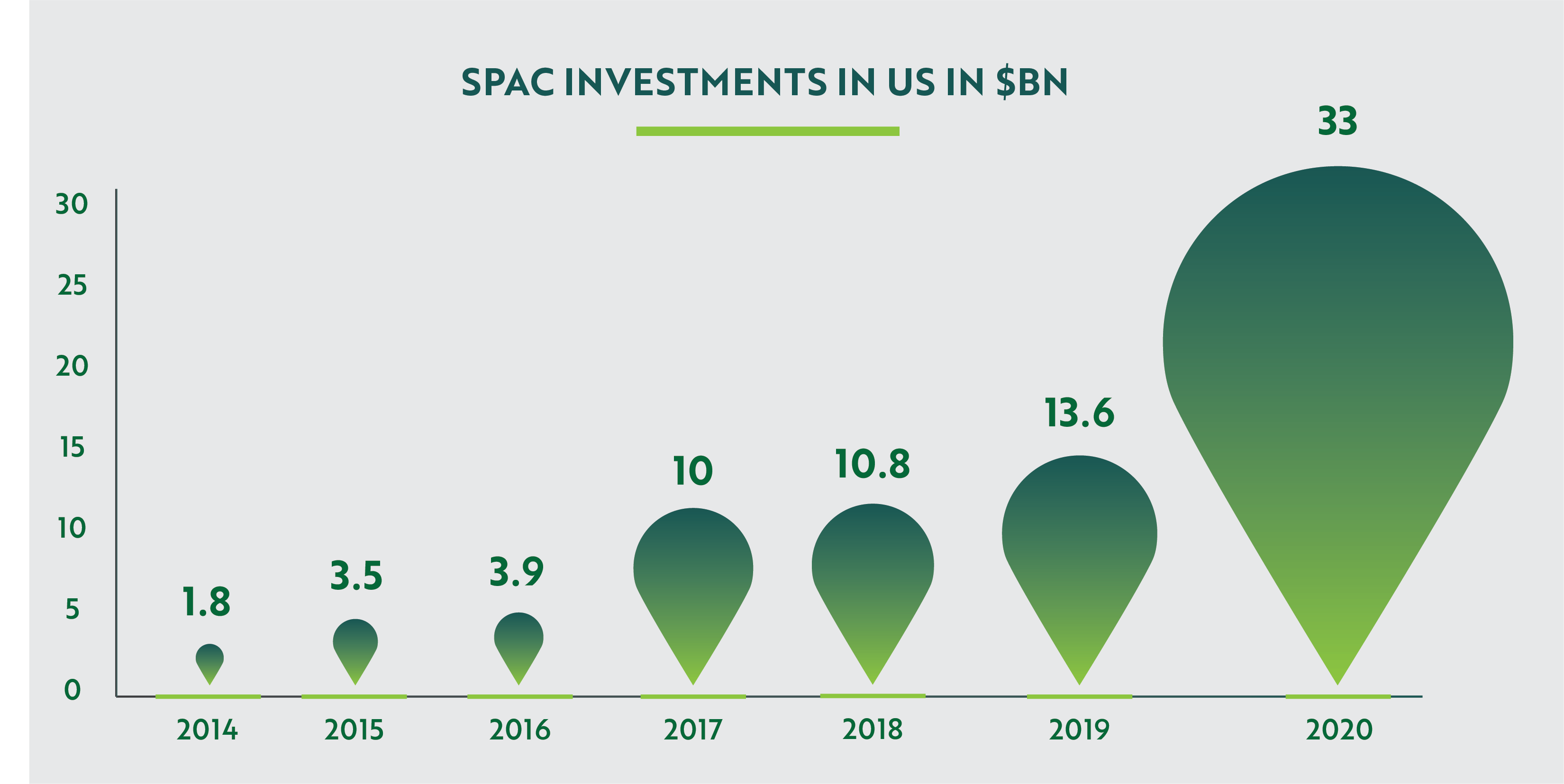

2020 is a record-shattering year for a revitalized SPAC market. According to data provided by ELLO Capital, there have been 95 SPAC IPOs so far in 2020, raising $37.8 billion (average size: $397 million). That compares with 59 in all of 2019, which raised $13.6 billion (average size: $230 million).

On July 22, 2020, Pershing Square founder Bill Ackman raised $4 billion in the IPO of Pershing Square Tontine Holdings Ltd., the largest SPAC IPO to date. With an initial target of $3 billion, the SPAC included a unique pricing approach: a fixed pool of warrants to be distributed to shareholders who accept a subsequent deal – increasing the take for approvers.

“COVID-19 is likely a direct cause of the acceleration in SPACs this year, as global lockdown policies have restricted travel and the ability to do roadshows. As a result, SPACs have largely replaced traditional IPOs,” said Mark Young, co-founding partner of Bridge Point Capital. “Plus, SPACS appeal to the high-growth technology sector, which has led the market recovery post-February correction, and continue to drive grwoth in the work-from-home economy.”

SPACs: rules of the road

- Speed is the name of the game – Leveraging the market expertise of leadership team, a SPAC can raise funds in a matter of days, without the time and resource demands of a roadshow.

- Minimum value is set – The acquired company/companies must have a minimum value, generally 80% of the fund the SPAC has in escrow following the IPO. Multiple closings, obviously, complicate the otherwise-simple SPAC process and inject completion risk into the transaction.

- The clock is ticking – There’s a deadline reality for both the SPAC and the target: If the SPAC doesn’t close the deal by the deadline, it must return the funds it raised in its offering. On the flip side, getting near the deadline can help give a target company some leverage.

- Valuation risk – Investors in SPACs are very much like IPO investors: there is an expectation that they are buying at a discount and there is significant growth potential around the corner. They are not looking for turnaround stories. In turn, SPACs are perceived as focused on growth verticals.

- Shareholder approval required – The SPAC is a public company that inherits all the baggage – reporting/regulatory demands, liabilities, etc. – of a public company. Approval by target company shareholders likely will be required. And the SPAC would need to file a proxy statement and secure approval from the Securities and Exchange Commission.

- Redemption risk – Here’s an interesting twist: At the time of the transaction, the SPAC’s public shareholders can redeem their stock. The risk: the SPAC’s cash availability – which might be needed to complete the transaction – could take a hit if the redemptions are significant.

- Warrants also in play – Sometimes the purchase price includes stock; the value of those shares are impacted by the associated rights. In most cases, the warrants can be exercised at a premium to the original offering price. What can happen: the valuation of stock included in purchase price may rise above, or fall below, the value of the stock issued to a target. The driving factor: can a deal actually get done.

- Navigate the de-SPAC phase – Definition: the time between the definitive agreement and closing. What needs to be done: communicate details of the transaction to the SPAC’s stakeholders. The goal: optimize the story, educate sales people, engage analysts – protect value.

The record so far

• DraftKings (NASDAQ: DKNG): Shares in the online fantasy and gambling company jumped to $18.69 per share when the merger agreement was announced in December, and then edged up to $19.35 per share on the first day of trading, Since then, the price has climbed to about $44.00 per share before settling back into the $37.00-$40.00 area. Its current market capitalization is over $13.5 billion.

• Virgin Galactic (NYSE: SPCE.N): The Richard Branson-backed competitor to Elon Musk’s SpaceX and Jeff Bezos’ Blue Origin, Virgin Galactic shares currently trade in around $17.00-$20.00, about double their late October day-one level, and more than three times their low of $6.90 per share. The stock has reached a high of $42.49 per share, and the company’s current market capitalization is $3.9 billion.

• Nikola (NASDAQ: NKLA): The green truck company has been on a roller-coaster ride since its late June debut. It has climbed as high as $93.99 at one point and currently trades at about $37.00 per share. Market capitalization is just under $14 billion.

Leading the way is a pending deal from Churchill Capital Corp. III, which has agreed to acquire health-cost management services provider MultiPlan for $11 billion. This would make it the largest ever SPAC deal.

“The healthcare and life sciences industries are two sectors likely to continue driving SPAC growth in the COVID-19 era,” said Nadia Tian, co-founding partner of Bridge Point Capital. “This is because healthcare traditionally outperforms the market in a recession, SPACs allow biotech companies to have more cash on hand than a traditional IPO, and the government and consumers are especially focused on these areas as we search for solutions to the COVID-19 outbreak.”

Final thoughts

Private companies that were planning an IPO or other significant M&A deal before the global economic downturn caused by the COVID-19 pandemic may want to seriously consider a SPAC deal. As with all transactions significant, intensive planning, vetting, due diligence and other considerations must be undertaken.

MGO’s dedicated SEC practice has experience with IPOs, RTOs, M&A deals and the unique characteristics of SPAC acquisitions. To understand your options, and the path ahead, please feel free to reach out to us for a consultation.

]]>Special Purpose Acquisition Companies, or SPACs, have been steadily rising in prominence over the last year, earning headlines with a number of eye-popping capital raises and making acquisitions that took high-profile companies public, including Virgin Galactic and electric carmaker Nikola. Previous, a relatively niche investment vehicle, many cannabis and hemp industry operators are still not clear as to how these investment companies operate, and what one should do if approached by a SPAC for an acquisition. In the following we will lay out the basics of SPACs and provide key considerations for cannabis operators and entrepreneurs approached by, or courting, investors.

The fundamentals of SPACS

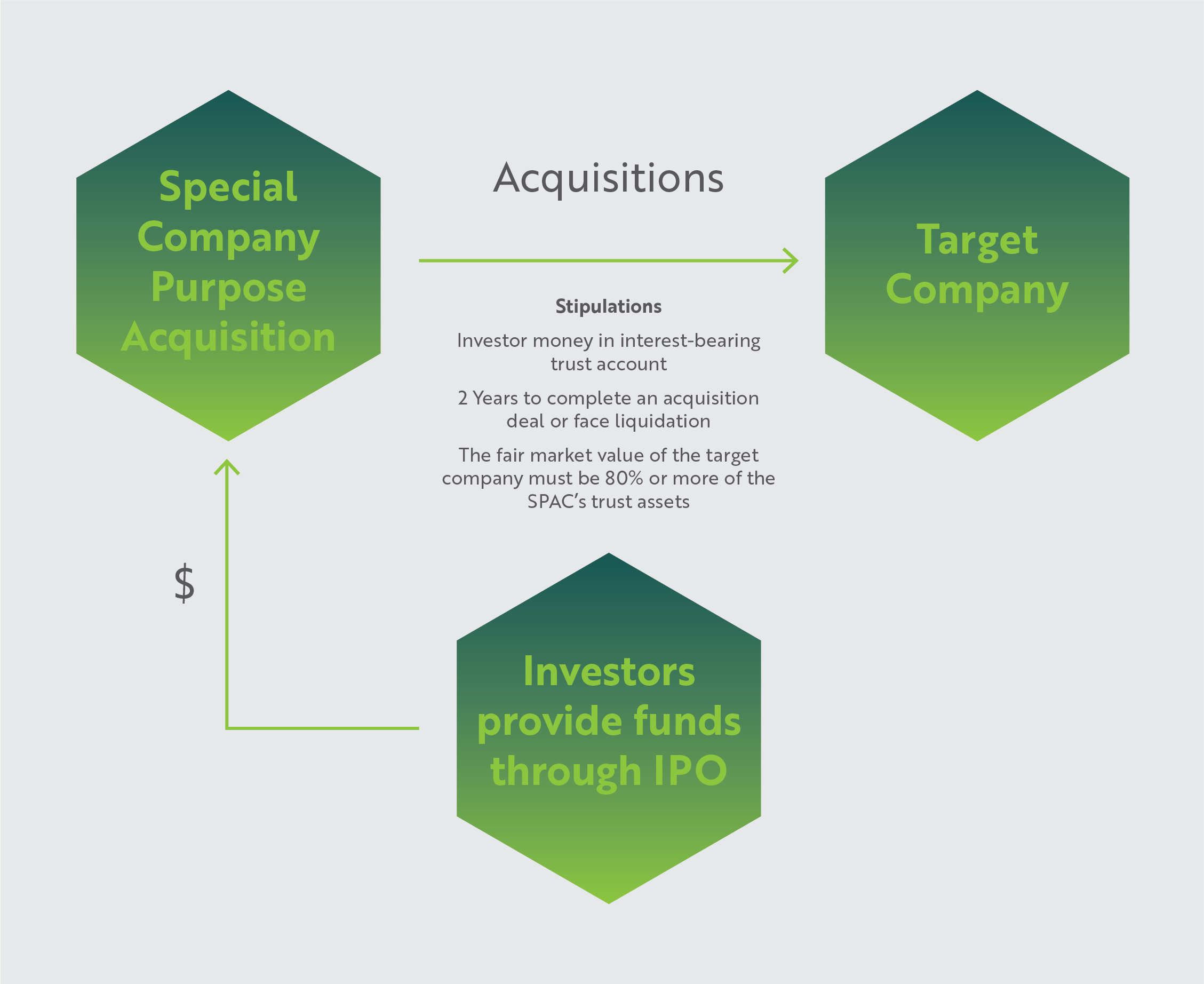

Simply defined, a SPAC is a shell company formed by founders/sponsors in order to raise investments through an IPO to acquire an existing company/companies. The key players involved are:

- Founders/Sponsors: Generally subject matter experts in their industry fields with credible market reputations.

- IPO Investors: Typically include institutional investors, equity funds, and the general public.

- Target company: A private company in the industry/sector stated as the SPAC’s focus during the IPO process.

As a regulatory stipulation, the Target company cannot be identified at the time of the IPO, and investors pour money into this instrument mainly on the basis of the founders’ reputation and the sector of investment – thus SPACs are also known as ‘blank check’ companies.

SPACs have many safety criteria for protecting investor interests. For example, investor money is generally kept in escrow in an interest-bearing trust account, and can be used only for acquisition purposes. The interest is used to cover certain operational SPAC costs until a transaction closes. Also, SPACs are time bound – a SPAC typically has two years to complete an acquisition or face liquidation, in which case the money is returned to the investors. (However, this period is extendable upon meeting certain conditions.) And finally, for the M&A transaction to be regulatory admissible, the fair market value of the target company must be 80% or more of the SPAC’s trust assets.

SPACs are generally beneficial to all parties concerned: sponsors/founders get liquidity to implement their ideas as well as ‘founder shares’ for their efforts; investors get an ‘expert’ backed investment platform to invest in; and the target company gets sound management expertise and liquidity. The IPO process is also faster for SPACs compared to traditional IPOs due to simplified documentation and listing procedures.

SPAC Structure

History and growing popularity of SPACs

SPACs have been in existence since the 1990s, but they became more popular in the early 2000s when entrepreneurs and mid-market public investors started seeking out private equity alternatives, more direct market options for raising funds, as well as suitable risk return options. Nowadays, SPACs are increasingly being used in various industries, to take companies public, and in situations where financing is scarce. At the moment, SPACs are having a major impact in technology and other high-growth sectors, exemplified by transactions involving DraftKings, Virgin Galactic, and Nikola. In the United States, the SPAC public offering structure, like many other financial instruments, is governed by the Securities and Exchange Commission (SEC).

Source: SPAC Research

SPACs as a force in cannabis and hemp

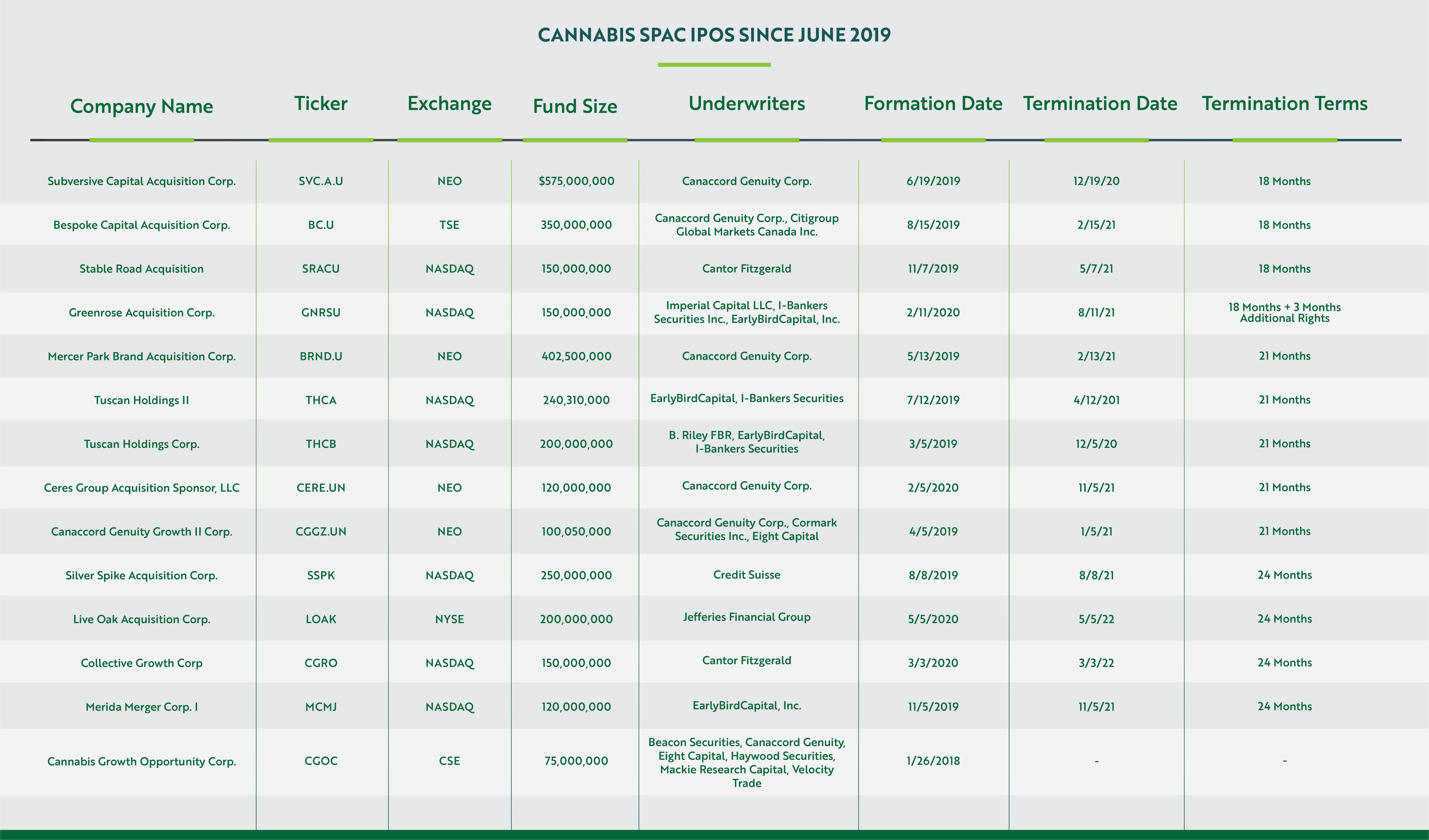

On May 1, 2020, founder and former CEO of Canopy Growth, Bruce Linton, rang the Nasdaq’s opening bell on the day he took his new venture public – a SPAC called Collective Growth Corp. – raising $150 million. While not the first SPAC to enter the cannabis space, Linton’s high-profile in the cannabis and hemp industries introduced the idea of SPACs to many industry operators and investors.

According to analysis provided by ELLO Capital, cannabis SPACs raised over $3 billion between June, 2019 and July, 2020. Not all of the funds have been utilized to date, so the clock is ticking on the ~two year window following the initial capital raise.

Considering the proliferation of distressed assets and companies struggling with the cash crunch, general economic turndown, and other complexities inherent to today’s cannabis industry, SPACs are likely to offer lifelines to a significant number operators – building new market leaders and reshaping the cannabis industry in the process.

Source: ELLO Capital

Guidance for cannabis industry companies

When a SPAC makes an acquisition, it can follow any of the standard transaction structures – asset acquisition, stock/share purchase, or merger – and the resultant entity combines the SPAC and the Target company into a publicly traded operating company.

So, what should cannabis and hemp operators and entrepreneurs do if approached by a SPAC for an acquisition? Of course, it’s a personal decision whether to go public or not, but for companies in need of liquidity or seeking an exit, merging with/selling to a SPAC can be quite advantageous, especially in the present market context. For one, a SPAC acquisition can help to raise the Target company’s sale price, due to increased competition as private equity and SPACs compete for the same targets. Furthermore, SPAC founders’ reputation and their choice of your company can also bring increased attractiveness/investor interest and richer valuations.

Since SPACs are traditionally led by experienced founders, the IPO process often runs smoothly and efficiently. Because there is typically no roadshow or series of investor presentations, the timeline and resources are more optimal than an IPO. And finally, for companies without experienced management, SPAC control can help provide the requisite expertise and talent.

It is important to note that SPACs listed on US exchanges, including Linton’s Collective Growth Corp, are necessarily focused on the legal hemp sector, since SEC regulatory guidelines prohibit adult-use and medical cannabis companies from going public in the US. However, several SPACs are listed on Canadian exchanges, which creates the potential for investments in US-based cannabis businesses.

Final thoughts

In the last year, broad market conditions have elevated the importance of SPACs across all industries. The cannabis and hemp industries are no different and SPACs represent a welcome investment source in these tough times. SPACs are bringing investment back into the industry, importantly from ‘so far on the bench’ institutional investors, which is particularly important for companies who want liquidity at a time when other avenues are drying up.

Catch up on previous articles in this series and see what’s coming next…

]]>