While it appears that several of the more disadvantageous provisions targeting businesses won’t make it into the final bill, others may. In addition, some temporary provisions are coming to an end, requiring businesses to take action before year end to capitalize on them. As Congress continues to negotiate the final bill, here are some areas where you could act now to reduce your business’s 2021 tax bill.

Research and experimentation

Section 174 research and experimental (R&E) expenditures generally refer to research and development costs in the experimental or laboratory sense. They include costs related to activities intended to uncover information that would eliminate uncertainty about the development or improvement of a product.

Currently, businesses can deduct R&E expenditures in the year they’re incurred or paid. Alternatively, they can capitalize and amortize the costs over at least five years. Software development costs also can be immediately expensed, amortized over five years from the date of completion or amortized over three years from the date the software is placed in service.

However, under the Tax Cuts and Jobs Act (TCJA), that tax treatment is scheduled to expire after 2021. Beginning next year, you can’t deduct R&E costs in the year incurred. Instead, you must amortize such expenses incurred in the United States over five years and expenses incurred outside the country over 15 years. In addition, the TCJA requires that software development costs be treated as Sec. 174 expenses.

The BBBA may include a provision that delays the capitalization and amortization requirements to 2026, but it’s far from a sure thing. You might consider accelerating research expenses into 2021 to maximize your deductions and reduce the amount you may need to begin to capitalize starting next year.

Income and expense timing

Accelerating expenses into the current tax year and deferring income until the next year is a tried-and-true tax reduction strategy for businesses that use cash-basis accounting. These businesses might, for example, delay billing until later in December than they usually do, stock up on supplies and expedite bonus payments.

But the strategy is advised only for businesses that expect to be in the same or a lower tax bracket the following year — and you may expect greater profits in 2022, as the pandemic hopefully winds down. If that’s the case, your deductions could be worth more next year, so you’d want to delay expenses, while accelerating your collection of income. Moreover, under some proposed provisions in the BBBA, certain businesses may find themselves facing higher tax rates in 2022.

For example, the BBBA may expand the net investment income tax (NIIT) to include active business income from pass-through businesses. The owners of pass-through businesses — who report their business income on their individual income tax returns — also could be subject to a new 5% “surtax” on modified adjusted gross income (MAGI) that exceeds $10 million, with an additional 3% on income of more than $25 million.

Capital assets

The traditional approach of making capital purchases before year-end remains effective for reducing taxes in 2021, bearing in mind the timing issues discussed above. Businesses can deduct 100% of the cost of new and used (subject to certain conditions) qualified property in the year the property is placed in service.

You can take advantage of this bonus depreciation by purchasing computer systems, software, vehicles, machinery, equipment and office furniture, among other items. Bonus depreciation also is available for qualified improvement property (generally, interior improvements to nonresidential real property) placed in service this year. Special rules apply to property with a longer production period.

Of course, if you face higher tax rates going forward, depreciation deductions would be worth more in the future. The good news is that you can purchase qualifying property before year-end but wait until your tax filing deadline, including extensions, to determine the optimal approach.

You can also cut your taxes in 2021 with Sec. 179 expensing (deducting the entire cost). It’s available for several types of improvements to nonresidential real property, including roofs, HVAC, fire protection systems, alarm systems and security systems.

The maximum deduction for 2021 is $1.05 million (the maximum deduction also is limited to the amount of income from business activity). The deduction begins phasing out on a dollar-for-dollar basis when qualifying property placed in service this year exceeds $2.62 million. Again, you needn’t decide whether to take the immediate deduction until filing time.

Business meals

Not every tax-cutting tactic has to be dry and dull. One temporary tax provision gives you an incentive to enjoy a little fun.

For 2021 and 2022, businesses can generally deduct 100% (compared with the normal 50%) of qualifying business meals. In addition to meals incurred at and provided by restaurants, qualifying expenses include those for company events, such as holiday parties. As many employees and customers return to the workplace for the first time after extended pandemic-related absences, a company celebration could reap you both a tax break and a valuable chance to reconnect and re-engage.

Stay tuned

The TCJA was signed into law with little more than a week left in 2017. It’s possible the BBBA similarly could come down to the wire, so be prepared to take quick action in the waning days of 2021. Turn to us for the latest information.

]]>Understanding IRS overpayment and underpayment rates

The overpayment rate is the sum of the federal short-term rate plus 3 percentage points. For corporations it is the federal short-term rate plus 2 percentage points. For the portion of a corporate overpayment of tax exceeding $10,000, it is the federal short-term rate plus 0.5%.

The underpayment rate is the sum of the federal short-term rate plus 3 percentage points, except underpayments for large corporations is the sum of the federal short-term rate plus 5 percentage points.

Starting April 1, the new increased rates will be:

• 4% for overpayments (3% for corporations),

• 1.5% for the portion of corporate overpayment exceeding $10,000,

• 4% for underpayments, and

• 6% for large corporate underpayments.

How is interest calculated on unpaid taxes?

Interest accrues on any unpaid tax from the due date of the return until the date of payment in full. The interest rate is determined quarterly. Interest compounds daily and is charged on the sum of all outstanding taxes and penalties.

What are the most common penalties?

Failure to Pay Penalty: If a return is filed but the tax owed was not paid on time, a late payment penalty will be imposed at .5% of the unpaid taxes for each month, or the part of the month the taxes remained unpaid. The penalty will not exceed 25% of the unpaid tax amount. Full monthly charges are applied even if taxes are paid in full before the end of the month.

Failure to File Penalty: Based on how late the tax return is filed and the amount of unpaid tax as of the original payment due date, this penalty is 5% of the unpaid taxes for each month, or the part of the month that a tax return is late. The penalty will not exceed 25% of the unpaid tax amount.

Combined Failure to Pay and Failure to File Penalty: If both penalties are applied in the same month, the Failure to File Penalty will be reduced by the amount of the Failure to Pay Penalty applied in that month. Based on the current penalty percentages, the late payment penalty would remain at .5%, and the late filing penalty would be reduced to 4.5%.

Substantial Underpayment Penalty: This penalty applies to (1) individuals if the tax liability is understated by 10% of the tax required to be shown on the return or $5,000, whichever is greater or (2) to corporations, if the tax liability is understated by 10% (or, if greater, $10,000) or $10,000,000. The penalty is 20% of the portion of the underpayment of tax that was understated on the return.

Negligence or Disregard of Rules or Regulations Penalty: At 20% of the portion of the underpayment of tax, this occurs due to negligence (lack of a reasonable attempt to follow the tax laws) or a disregard for the tax rules, meaning the taxpayer carelessly, recklessly, or intentionally ignores the tax laws.

Underpayment of Estimated Tax Penalty: This penalty applies to corporations or individuals that do not make enough estimated tax payments or are late in paying them when required. The penalty is based on (1) the amount of the underpayment, (2) the period when the underpayment was due and underpaid, and (3) the interest rate for underpayments published quarterly by the IRS. To avoid it, corporations can make quarterly estimated tax payments if they expect to owe $500 or more in estimated tax when they file their return. Individual taxpayers can avoid it if they owe less than $1,000 in tax after subtracting withholding and refundable credits, or if they paid withholding and estimated tax of the lesser of at least 90% of the tax for the current year or 100% of tax shown on the prior year’s return.

Can an IRS penalty or interest be removed or abated?

The IRS can remove or reduce some penalties if the taxpayer acted in good faith and can show reasonable cause for the failure to meet their tax obligations. However, by law, the IRS cannot reduce or remove interest unless the penalty is removed or reduced.

Reasonable cause is based on all the facts and circumstances of each situation, and the IRS will consider any reason establishing that a taxpayer used all ordinary business care and prudence to meet their federal tax obligations but were unable to do so. It is important to note that lack of funds is not reasonable cause for failing to file or pay on time — but it could be considered reasonable cause for the failure-to-pay penalty.

The IRS’s First Time Penalty Abatement Policy (FTA) can provide relief from a penalty if a taxpayer has not incurred penalties previously. To qualify under this policy, the taxpayer (1) did not previously need to file a return or had no penalties for the last 3 years prior to the tax year in which the penalty was received, (2) is current on all required returns or extensions of time to file, and (3) has paid or arranged to pay any tax due.

What options are available if a taxpayer cannot pay the taxes due?

- Short Term Payment Plan: This plan is not available for businesses unless it is a sole proprietor or an independent contractor. There is no setup fee, and the balance must be paid within 180 days. A short-term payment plan is available for individuals if less than $100,00 in combined tax, penalties and interest is due. Penalties and interest accrue until the balance is paid in full.

- Long Term Payment Plan (Installment Agreements): An installment agreement is available for individuals if less than $50,000 is owed or for a business if less than $25,000 is due in combined tax, penalties and interest and all required returns are filed. Penalties and interest accrue until the balance is paid in full. The maximum term for most installment plans is 72 months.

If a taxpayer pays less than the full amount due, how is the partial payment applied?

If a taxpayer makes a partial payment accepted by the IRS, and the taxpayer provides specific written directions as to the application of the payment, then the IRS will apply the payment as instructed by the taxpayer. If the taxpayer does not provide instructions with the partial payment, then the partial payment is applied to periods in order of priority that the IRS determines is in its best interest. The payment will be applied to satisfy the liability in successive periods in descending order of priority until the payment is absorbed. If the partial payment applied to a period is less than the liability for the period then the payment will be applied to the tax, then penalty and finally interest, until the amount is exhausted (Rev. Proc. 2002-26).

Example: The taxpayer incurs the following tax deficiency, penalties and interest:

Year 1: Tax: 6,000, Penalty: $1,800, Interest: $1,200

Year 2: Tax: 7,000, Penalty: $ 0, Interest: $ 1,500

The IRS agrees that the taxpayer can satisfy the total liability of $17,500 for a payment of $15,000. There is no agreement as to the allocation of the payment and the taxpayer does not provide any directions for application of the partial payment. The payment is first applied to the Year 1 tax, penalty, and interest (a total of $9,000), leaving $6,000 to be applied to Year 2. The remaining amount is completely absorbed by the tax due for Year 2, which results in the payment of interest in Year 1, but not for Year 2.

However, if the partial payment accepted by the IRS is less than the total of tax and penalties due in both years and there is no agreement regarding the application of the partial payment, then nothing is allocated to the interest in either year. For example: following the amounts listed above, if the partial payment was $12,000 instead, then the entire amount is applied to the tax and penalty in Year 1 (a total of $7,800) and the remaining amount of $4,200 is applied to the Year 2 tax due. None of the partial payment would be applied to the interest in either year.

Final thoughts

This year, failing to file your tax payments by the April 18 deadline will cost you more. If you are flirting with the deadline, remember that you will owe interest on any unpaid tax from the return’s due date until the day you actually make the payment — and interest will compound daily.

If you have questions and want to ensure you avoid being hit with tax penalties and interest, please reach out to MGO’s Tax team for assistance. You can rely on us to help you mitigate the impact of the interest rate increase.

Forgiveness basics

PPP loans generally are 100% forgivable if the borrower allocates at least 60% of the funds to payroll and eligible nonpayroll costs. Borrowers may apply for forgiveness at any time before their loans’ maturity date. Loans made before June 5, 2020, generally have a two-year maturity; loans made on or after that date have a five-year maturity.

However, if a borrower fails to apply for forgiveness within 10 months after the last day of the “covered period,” its PPP loan payments will no longer be deferred. (The covered period is eight to 24 weeks following disbursement during which the funds must be used.) Such loans will become standard loans, and borrowers will be responsible for repaying the full amount plus 1% interest before the maturity date — unless the loan is subsequently forgiven. The 10-month period soon will expire for many so-called “first-draw” borrowers.

SBA’s process improvements

The popularity of the PPP, as well as the requirement that lenders make forgiveness determinations within 60 days of receiving an application, has left many smaller lenders overwhelmed. Some are even limiting the time periods during which they’ll accept forgiveness applications. This, in turn, has created confusion and concern among borrowers.

In response, the SBA recently issued an Interim Final Rule (IFR). The rule streamlines the forgiveness process for smaller loans through two avenues:

1) Direct borrower forgiveness. The SBA is providing a direct borrower forgiveness process for lenders that choose to opt in. At the time the guidance was released, more than 600 banks had opted in, enabling more than 2.17 million borrowers to apply through a new online portal scheduled to launch on August 4, 2021.

Participating lenders will receive notice when a borrower applies through the SBA platform and will review applications and issue forgiveness decisions inside the platform. The SBA hopes this will reduce the wait time and uncertainly associated with applying through lenders.

2) COVID Revenue Reduction Score. The IFR also creates an alternative process for “second-draw” borrowers with loans of $150,000 or less to document their reduced revenue. To qualify for such loans, a borrower must have experienced a revenue reduction of at least 25% during one quarter of 2020 compared with the same quarter in 2019. If a borrower didn’t produce the necessary documentation when applying for the loan, it must do so on or before the date of application for forgiveness.

To make the revenue reduction confirmation process easier for such loans, an independent SBA contractor will assign every eligible second-draw loan a score based on several factors, including industry, geography, business size and current economic data. The score will be stored in the forgiveness platform and visible to lenders to document revenue reduction. If a borrower’s score doesn’t meet the value required to confirm the reduction, the borrower must provide documentation. If it does, no documentation is required.

Appeals and deferments

The IFR also extends the loan deferment period for borrowers who timely appeal a final SBA loan review decision. Under the previous rule, an appeal didn’t extend the period so borrowers had to begin making payments of principal and interest on the unforgiven amount.

The IFR amends that rule to extend the deferment period until the SBA’s Office of Hearings and Appeals issues a final decision. Appeals must be filed within 30 calendar days of receipt of the final SBA loan review decision, and borrowers should notify their lenders of appeals.

More to come

The SBA will release additional guidance regarding both the direct borrower forgiveness option and the COVID Revenue Reduction Score. We can help with your forgiveness application process and answer any questions you may have about your PPP loan.

]]>The U.S. Small Business Administration (SBA) expanded eligibility in September 2021. While you may not have qualified or considered EIDL funding necessary previously, you might want to reconsider in light of yet another wave of COVID infections. But you’ll have to do so quickly, as the application deadline is December 31, 2021.

Shaky economic ground ahead?

Sen. Joe Manchin (D-WV) released a statement on December 19 announcing that he “cannot vote to move forward” on the BBBA. The $2.1 billion bill that passed in the U.S. House of Representatives includes numerous provisions related to healthcare, energy initiatives, immigration, education, social programs and taxes.

The Democrats lack the votes to pass the proposed legislation in the Senate without Manchin’s support. Yet Senate Majority Leader Chuck Schumer (D-NY) indicated on December 20 that he nonetheless intends to hold a vote on the bill in early 2022. Schumer’s announcement came hours after Goldman Sachs reduced its predictions for U.S. economic growth in 2022 based on Manchin’s statement.

Types of EIDL relief available

The COVID-19 EIDL program was created to make low-interest fixed-rate long-term loans to provide small businesses (including sole proprietorships and independent contractors) the working capital they need to withstand the effects of the pandemic. Three types of funding are available:

Loans. This funding type features a 30-year term and fixed interest rate of 3.75%. The proceeds can be used for any normal operating expense, including payroll, rent or mortgage, utilities, and other ordinary businesses expenses. Since the recent program expansion (see below), funds also can be used to pay or pre-pay business debt incurred at any time, including after submitting the application, and regularly scheduled payments of federal debt.

Targeted advances. Businesses located in low-income communities, have no more than 300 employees and have suffered more than a 30% reduction in revenue may qualify for a targeted advance up to $10,000. These advances don’t have to be repaid.

Supplemental targeted advances. Businesses in low-income communities that have no more than 10 employees and saw revenue declines of more than 50% may be eligible for an additional $5,000. Supplemental advances also don’t require repayment.

The recent expansion

The SBA has implemented several changes to make it easier for small businesses to access the COVID-19 EIDL loans. Among other things, the SBA:

- Expanded eligibility from organizations with no more than 500 employees (including affiliates) to encompass businesses in the hardest hit industries with no more than 500 employees per physical location, as long as the business (with affiliates) has no more than 20 locations,

- Increased the maximum loan amount from $500,000 to $2 million,

- Extended the payment deferment period to two years after the loan origination date for all loans (interest will accrue during that period, and principal and interest payments must be made over the remaining 28 years of the loan term), and

- Simplified the affiliation requirements.

The SBA has also limited entities that are part of a single corporate group to a combined total of no more than $10 million in COVID-19 EIDL loans.

Additional eligibility requirements

Applicants must be physically located in the United States or a designated territory and have suffered working capital losses due to the COVID-19 pandemic. In addition, the businesses must have been in operation on or before January 31, 2020.

Businesses (other than sole proprietorships) must have a valid tax identification number. Each owner, member, partner or shareholder of 20% or more must be a U.S. citizen, non-citizen national or qualified alien with a valid Social Security number.

For loans of $500,000 or less, you must have a credit score of at least 570. For larger loans, the credit score must be at least 625. Personal guaranty and collateral requirements may apply, too, depending on the amount of the loan.

The looming deadline

The SBA will accept applications for loans and targeted advances until December 31, 2021. It will continue to process applications after that date, until the funds are exhausted. While the SBA earlier advised businesses seeking supplemental targeted advances to submit applications by December 10, 2021, it later announced it will accept applications until year end. It can’t process applications after the deadline, though, so applications submitted near the deadline might not be processed.

Note that borrowers can request increases, up to their maximum loan eligibility amount, for up to two years after loan origination or until the program funds are exhausted. In addition, the SBA will accept reconsideration and appeal requests received before December 31, 2021, if received on a timely basis. For reconsiderations, that means within six months from the date the application was declined. Appeals must be received within 30 days from the date the reconsideration was declined.

Don’t dawdle

You can apply online for COVID-19 EIDL relief, but the clock is ticking. We can help you determine if you should go this route and help you collect the necessary documentation.

]]>Early termination of the Employee Retention Credit

The IIJA terminates the Employee Retention Credit (ERC) created by the CARES Act earlier than originally planned. The American Rescue Plan Act (ARPA) had extended the credit to eligible employers for the third and fourth quarters of 2021. Under the new law, the ERC — which for 2021 is worth up to $7,000 per qualifying employee per quarter — is no longer available for wages paid after September 30, 2021 (rather than December 31, 2021), except for so-called “recovery startup businesses.”

The ARPA generally defines recovery startup businesses as those that began operating after February 15, 2020, and have annual gross receipts for the three previous tax years of less than or equal to $1 million. These employers can claim the ERC for up to $50,000 total per quarter for the third and fourth quarters of 2021, without showing suspended operations or reduced receipts.

However, clients can still file retractive amendments to claim credits missed (seek refunds) for Q1 – Q4 2020 and Q1 – Q3 2021.

New information reporting on digital assets

The IIJA requires brokers to report to the IRS the cost basis of digital assets transferred by their clients to nonbrokers, similar to how securities brokers report stock and bond trades. “Digital assets” are defined as “any digital representation of value which is recorded on a cryptographically secured distributed ledger or any similar technology.” This definition could ensnare not only cryptocurrencies like Bitcoin and Ethereum, but also certain nonfungible tokens (NFTs). The IIJA expands the definition of the term “broker” to include those who operate trading platforms for digital assets, such as cryptocurrency exchanges.

In addition, the IIJA modifies existing tax law to redefine “cash” subject to reporting to include “any digital representation of value”. As a result, individuals engaged in a trade or business must submit IRS Form 8300, “Report of Cash Payments Over $10,000 Received in a Trade or Business,” when they receive such amounts in one transaction or multiple related transactions.

The digital assets provisions take effect for returns required to be filed, and statements required to be furnished, after December 31, 2023. The IRS is expected to provide guidance before that time, but some businesses may find that accepting cryptocurrencies for payment isn’t worth the reporting burden.

Miscellaneous tax provisions

The IIJA extends several excise taxes used to fund highway spending, extends and modifies certain Superfund excise taxes, and allows private activity bonds for qualified broadband projects and carbon dioxide capture facilities. It extends pension funding relief and expands certain IRS administrative relief for taxpayers affected by federally declared disasters and “significant fires.”

More to come

The majority of the Democrats’ proposed tax law changes, to the extent they survive ongoing negotiations, will be included in the Build Back Better Act (BBBA). The BBBA could, for example, have significant provisions regarding the child tax credit, the cap on the state and local tax deduction, and limits on the business interest expense deduction. We’ll keep you current on the developments that could affect both your personal and business’s bottom lines.

]]>PPP basics

Generally, PPP loans are 100% forgivable given the borrower allocates the funds on a 60/40 basis between payroll and eligible nonpayroll costs. Nonpayroll costs originally solely included mortgage interest, rent, utilities, and interest on any other existing debt. However, the Consolidated Appropriations Act (CAA), which was enacted in late 2020, significantly expanded the eligible nonpayroll costs to include other costs the funds can be applied to, such as certain operating expenses and worker protection expenses.

The CAA also withdrew the original requirement that mandated borrowers deduct the amount of any Small Business Administration (SBA) Economic Injury Disaster Loan (EIDL) advance from the forgiveness amount they received from the PPP. A borrower doesn’t need to include any forgiven amounts in its gross income and can deduct otherwise deductible expenses paid for with forgiven PPP proceeds.

Forgiveness filings

Those who borrowed PPP loans can apply for forgiveness at any time before their loans’ maturity date, and loans made before June 5, 2020, generally have a two-year maturity while loans made on or after that date have a five-year maturity. However, if a borrower does not apply for forgiveness within 10 months after the last day of the “covered period” (the eight-to-24 weeks following disbursement during which the funds must be used), the PPP loan payments will no longer be deferred, and payments must begin to be made to the lender.

This 10-month period is ending for many “first-draw” borrowers. If a business applied early in the program, it might have a covered period that ended on October 30, 2020, meaning it would need to apply for forgiveness by August 30, 2021, to avoid loan repayment responsibilities.

To apply for forgiveness, borrowers file forms with their lenders, who will then submit the forms to the SBA. The type of form that must be filed is dependent on both the amount of the loan and whether a business is a sole proprietor, independent contractor, or self-employed individual with no employees.

The borrower will be notified by the lender if the SBA does not forgive a loan or only partially forgives it. Interest accrues during the time from disbursement of the loan proceeds to SBA remittance to the lender of the forgiven amount, and the borrower must pay any interest that has accrued on any amount not forgiven.

To maximize their employee retention tax credits, some businesses may have delayed filing their forgiveness applications. The reason for this stems from the fact that qualified wages paid after March 12, 2020, through December 31, 2021—that are considered for purposes of calculating the credit amount—cannot be included when calculating eligible payroll costs for PPP loan forgiveness. These businesses should pay careful attention to the date their 10-month period expires as to avoid triggering loan repayment.

Audit action

There is the possibility that borrowers will be audited by the SBA’s Office of Inspector General with support from the IRS and other federal agencies. The SBA automatically audits every loan in excess of $2 million after the borrower applies for forgiveness, but it’s possible that smaller loans could be subject to scrutiny too.

Despite the audit safe harbor for loans of $2 million or less established by the SBA, this carveout solely applies to the examination of the borrower’s good faith certification on the loan application that states “the current economic uncertainty makes the loan request necessary to support the ongoing operations” of the business. Those borrowers will also no longer need to complete a burdensome, time-consuming Loan Necessity Questionnaire, as the SBA recently notified lenders that this loan necessity requirement for loans more than $2 million has been eliminated.

However, all borrowers still have the potential to be audited on matters like eligibility (like the number of employees), calculation of the loan amount, how the funds were used, and entitlement to forgiveness. Borrowers that receive poor audit findings may be required to repay their loans and, depending on what kinds of missteps were recovered, could face civil penalties and persecution under the federal False Claims Act.

Those businesses that received loans of more than $2 million should not wait to prepare for their audits. By beginning to work with their CPAs now, they can gather and organize the documents and information auditors are likely to request, including:

• Financial statements,

• Income and employment tax returns,

• Payroll records for all pay periods within the applicable covered period,

• Calculation of full-time equivalent employees, and

• Bank and other records related to how the funds were used (for example, canceled checks, utility bills, leases, and mortgage statements).

It is important to note that some of this documentation will overlap with what is required when filing the application for loan forgiveness.

Act now

Businesses always have their plates full, so it isn’t surprising that many may not have been focused on the various dates that matter to their PPP loans. Now is the time to ensure that you file your forgiveness application promptly with the necessary documentation already gathered to survive any SBA audit that may follow. Contact us for assistance.

]]>R&D tax credit criteria

The R&D tax credit rewards companies for conducting research and development in the United States. The R&D umbrella is broad and can encompass several different types of activities. To qualify as an R&D activity, one must meet each of the following criteria:

- Technological in nature. Activities must be based on hard science.

- Qualified purpose. Activities must be intended to develop a new or improved product or process.

- Technological uncertainty. Activities must be aimed at eliminating uncertainty with respect to the development of a product or process.

- Process of experimentation. Activities must involve a systemic or iterative approach of evaluating different alternatives to eliminate ambiguity.

Small businesses and startup benefit

The most beneficial guidance that affects eligible small businesses and startups is the option to elect up to $250,000 per year of their qualifying research expenses to offset the FICA employer portion of payroll tax. To qualify for this, a business must have current year annual gross receipts of less than $5 million and must not have any gross receipts five years prior to the current year claim. The payroll tax election must also be made on a prompt income tax return, including extensions.

Before this guidance was enacted, small businesses who had eligible research expenses but possessed little to no income tax liability were not able to capitalize on the R&D credit. Now, taxpayers can capture potential payroll tax savings of up to $1,250,000 over five years.

Newer legislation also allows some taxpayers and eligible small businesses—defined as corporations that aren’t publicly traded, a partnership, or a sole proprietorship with average annual gross receipts not exceeding $50 million for three taxable years before the current taxable year—too small to absorb the entire R&D tax credit to get the credit against their alternative minimum tax (AMT) liability. Since the tax reform law passed in 2017, AMT has been repealed for C corps beginning in 2018 but remains in place for individuals, including those who possess ownership in S corps or partnership.

About the author

Michael Silvio is a partner at MGO. He has more than 25 years of experience in public accounting and tax and has served a variety of public and private businesses in the manufacturing, distribution, pharmaceutical, and biotechnology sectors.

Start a grant application here: https://careliefgrant.com/partners/county/

Basics of the COVID-19 relief grant program

The program, which allocates $500 million in financial relief to small businesses and nonprofits that have been impacted by the COVID-19 pandemic, was first announced by Gov. Newsom and the California state legislature on November 30th, 2020.

All California-based small businesses (including sole proprietors, home-based businesses, and independent contractors) and not-for-profits with a yearly gross revenue of $2.5 million or less, and have been in operation since at least June 1, 2019, may be eligible for the grant. It is worth noting that applicants with multiple business entities/franchises/locations, etc. are not eligible for multiple grants and are only allowed to apply once using their eligible small business with the highest revenue.

Grant awards by entity revenue

The grant award ranges from $5,000 to $25,000 based on your operation’s annual gross revenue as reported in the most recent federal tax return.

Gross Annual Revenue – Grant Award

$1,000 to $100,000 – $5,000

Greater than $100,000 up to $1,000,000 – $15,000

Greater than $1,000,000 up to $2,500,000 – $25,000

The award is a true grant, not a loan that has to be forgiven. The funds are intended to be used as working capital for your business’s operating expenses – payroll, rent, loan payments, COVID-protective measures, etc.

Award selection process

The grants are not issued on a “first-come, first-served” basis; rather all applications will be assessed following the close of each application round. The program prioritizes distribution based on key factors, including:

- Geographic distribution based on COVID-19 health and safety restrictions;

- County status and regional stay-at-home orders;

- Industry sectors most impacted by the pandemic;

- Underserved small business groups:

- e.g., majority-owned and run by women, persons of color, or veterans, or located in low-to-moderate income and rural communities.

The Small Business COVID-19 Relief Grant Program will be offered in two “Rounds” – with the first Round running from December 30, 2020 to January 13, 2021 at 11:59pm. Everyone who applies during a Round will be given equal consideration. Awards will be announced after each Round closes. The timing of the second and final Round is to be determined.

If you apply in the Round 1 and are not successful, your application will be carried over for consideration in Round 2 without the need to reapply. Businesses can only receive one grant even though there will be two Rounds.

For more information, visit careliefgrant.com

]]>Background on the Executive Order

In an August 8, 2020 memorandum to the Secretary of the Treasury entitled, “Deferring Payroll Tax Obligations in Light of the Ongoing COVID-19 Disaster,” President Trump directed Treasury Secretary Mnuchin to use his authority to defer the withholding, deposit and payment of employee Social Security tax on wages (i.e., 6.2% of employee wages) or Railroad Retirement tax on compensation paid to certain employees during the period September 1 through December 31, 2020. The memorandum instructed the Treasury Department to issue guidance explaining how to implement the deferral and to explore avenues, including legislation, to eliminate the obligation to pay the deferred taxes. Secretary Mnuchin made comments in an August 10 interview that employers would not be required to offer the deferral.

Drawing a line between mandatory and voluntary tax deferral

One of the most pressing questions following the President’s executive order was whether organizations were required to, or could opt-out, of the payroll tax deferral. Although the IRS Notice does not specifically state whether the employee payroll tax deferral is mandatory, the deferral appears to be voluntary, which lines up with Treasury Secretary Mnuchin’s widely reported comments.

Internal Revenue Code Section 7508A (which is the basis for the memorandum and the Notice) allows the President to postpone certain tax deadlines due to a disaster, such as COVID-19. However, Section 7508A does not give the President authority to require taxpayers to use the extended deadline. In other words, even if a deadline is postponed, a taxpayer could continue to adhere to the normal deadlines. As a result, employers can continue to withhold employee Social Security tax or Railroad Retirement tax from September 1 to December 31, 2020 if they do not wish to avail themselves of the deadline extension.

The Notice clearly places responsibility on employers for withholding and depositing the deferred taxes, and states that penalties generally would apply for any failure to comply (although the Notice states that employers can “make arrangements to otherwise collect the total Applicable Taxes from the employee”). Neither the memorandum nor the Notice eliminates the tax liability.

It appears that the employee payroll tax deferral does not apply to self-employed individuals, since it only applies to Social Security tax and Railroad Retirement tax and does not include Self-Employment Contributions Act (SECA) taxes.

Too late for many employers to benefit from deferral option

Since the guidance was released so close to the first available deferral date (i.e., September 1), employers have very little time to modify payroll procedures and payroll systems to allow employees the deferral on the first pay cycle in September.

Under the current IRS rules, it is not possible to “recover” the tax that already was withheld and remitted, but was eligible for the deferral, without causing issues with the employer tax filings and the imposition of penalties. Retroactive changes generally are not allowed simply because a taxpayer failed to use an available extension. This is consistent with the IRS’s position on employers that failed to timely defer the employer’s share of Social Security taxes (6.2%) as permitted under the CARES Act.

Key insights from the IRS guidance

The following are summaries of key points from the IRS issuance.

Dates and Eligibility

- The employee payroll tax deferral applies to wages and compensation paid on a pay date during the period beginning on September 1, 2020 and ending on December 31, 2020.

- The employee payroll tax deferral applies only if wages or compensation paid to an employee for a biweekly pay period are less than $4,000, or the equivalent amount with respect to other pay period frequencies. This threshold is determined on a pay period-by-period basis.

What it means:

Employees who are paid hourly or whose wages vary from pay period to pay period may not benefit from the payroll tax deferral in every pay period depending on whether the amount of wages exceeds the biweekly threshold of $4,000, or the equivalent. Employers should review with their IT departments or payroll service providers to ensure that the payroll system is configured correctly to determine who is eligible to participate in the employee payroll tax deferral on a pay period-by-pay period basis.

Deferral and Repayment Periods

- The due date for the deferred withholding and payment of the employee Social Security tax and Railroad Retirement tax is postponed until the period beginning on January 1, 2021 and ending on April 30, 2021.

- Employers are responsible for the deferred taxes and must withhold and pay the deferred taxes ratably from wages and compensation paid between January 1, 2021 and April 30, 2021 or interest, penalties and additions to tax will begin to accrue on May 1, 2021 with respect to any unpaid deferred taxes. If the employee’s wages are not sufficient for the withholdings, the employer can pursue payment from the employee.

What it means:

The very short-term deferral and repayment period results in a modest benefit.

For example: An employee who earns the Federal minimum wage would have an increased biweekly paycheck of $36 (or $324 for nine pay periods, from September 1 to December 31, 2020).

For employees that earn the maximum $3,999 every two weeks for nine pay periods, the benefit is $2,231. ($3,999 x 6.2% x 9 pay periods).

Unless something happens to dramatically improve the employee’s household income before January 1, 2021, the repayment of taxes ratably over the first four months of 2021 may create a greater hardship than their current cash flow shortage.

The dilemma facing employers

Many questions remain in terms of how the employee payroll tax deferral will impact employees and employers, how the deferred payroll taxes are to be reported and what changes must be made to an employer’s payroll system. Until the IRS provides further guidance regarding these outstanding questions and concerns, employers that consider implementing the employee payroll tax deferral should exercise care by putting safeguards in place to ensure that they do not fall victim to the IRS penalties.

Since the employee payroll tax deferral takes effect as early as September 1, 2020, employers that consider implementing the tax deferral likely will face a dilemma due to some of the unanswered questions unless the IRS issues additional guidance soon. For example:

- Can a participating employer apply the same deferral policy to all employees, or must the employees be allowed to choose?

- What are the consequences if an employee unexpectedly leaves the employer before paying the deferred tax?

- If the employer cannot collect the taxes from former employees, is the employer liable for the tax or failure to withhold penalties?

- What if the employee does not earn enough wages during the period between January and April of 2021 due to disability, leave of absence, etc., to pay for the deferred tax?

- Does the employer report the deferred payroll tax as tax withheld on the employer’s quarterly tax returns (i.e., Form 941) and Forms W-2?

- What happens if the employer did not defer the payroll tax, but the government later decides to forgive the deferred taxes? Will the employer or the employees be able to recover the tax that would have been forgiven had the tax been deferred?

- Will the IRS provide a mechanism (e.g., revising the employer’s Form 941) to allow employers to “recover” the tax that was already withheld and remitted, but was eligible for the deferral, without causing issues with the employer tax filings and incurring penalties?

- What if an employee receives a supplemental wage payment (e.g., bonus) outside of a normal pay period, how will that be treated for the purpose of the $4,000 eligibility threshold?

We will continue to provide updates on the Employee Payroll Tax Deferall program as more information becomes available. If you are unclear on the impact on your organization, or you would like a consultation, please reach out to our dedicated tax team: contact us now

]]>Deal structure can be viewed as the “Terms and Conditions” of an M&A deal. It lays out the rights and obligations of both parties, and provides a roadmap for completing the deal successfully. While deal structures are necessarily complex, they typically fall within three overall strategies, each with distinct advantages and disadvantages: Merger, Asset Acquisition and Stock Purchase.

In the following we will address these options, and common alternatives within each category, and provide guidance on their effectiveness in the cannabis and hemp markets.

Key considerations of an M&A structure

Before we get to the actual M&A structure options, it is worth addressing a couple essential factors that play a role in the value of an M&A deal for both sides. Each transaction structure has a unique relationship to these factors and may be advantageous or disadvantageous to both parties.

Transfer of Liabilities: Any company in the legally complex and highly-regulated cannabis and hemp industries bears a certain number of liabilities. When a company is acquired in a stock deal or is merged with, in most cases, the resulting entity takes on those liabilities. The one exception being asset deals, where a buyer purchases all or select assets instead of the equity of the target. In asset deals, liabilities are not required to be transferred.

Shareholder/Third-Party Consent: A layer of complexity for all transaction structures is presented by the need to get consent from related parties. Some degree of shareholder consent is a requirement for mergers and stock/share purchase agreements, and depending on the Target company, getting consent may be smooth, or so difficult it derails negotiations.

Beyond that initial line of consent, deals are likely to require “third party” consent from the Target company’s existing contract holders – which can include suppliers, landlords, employee unions, etc. This is a particularly important consideration in deals where a “change of control” occurs. When the Target company is dissolved as part of the transaction process, the Acquirer is typically required to re-negotiate or enter into new contracts with third parties. Non-tangible assets, including intellectual property, trademarks and patents, and operating licenses, present a further layer of complexity where the Acquirer is often required to have the ownership of those assets formally transferred to the new entity.

Tax Impact: The structure of a deal will ultimately determine which aspects are taxed and which are tax-free. For example, asset acquisitions and stock/share purchases have tax consequences for both the Acquirer and Target companies. However, some merger types can be structured so that at least a part of the sale proceeds can be tax-deferred.

As this can have a significant impact on the ROI of any deal, a deep dive into tax implications (and liabilities) is a must. In the following, we will address the tax implications of each structure in broad strokes, but for more detail please see our article on M&A Tax Implications (COMING SOON).

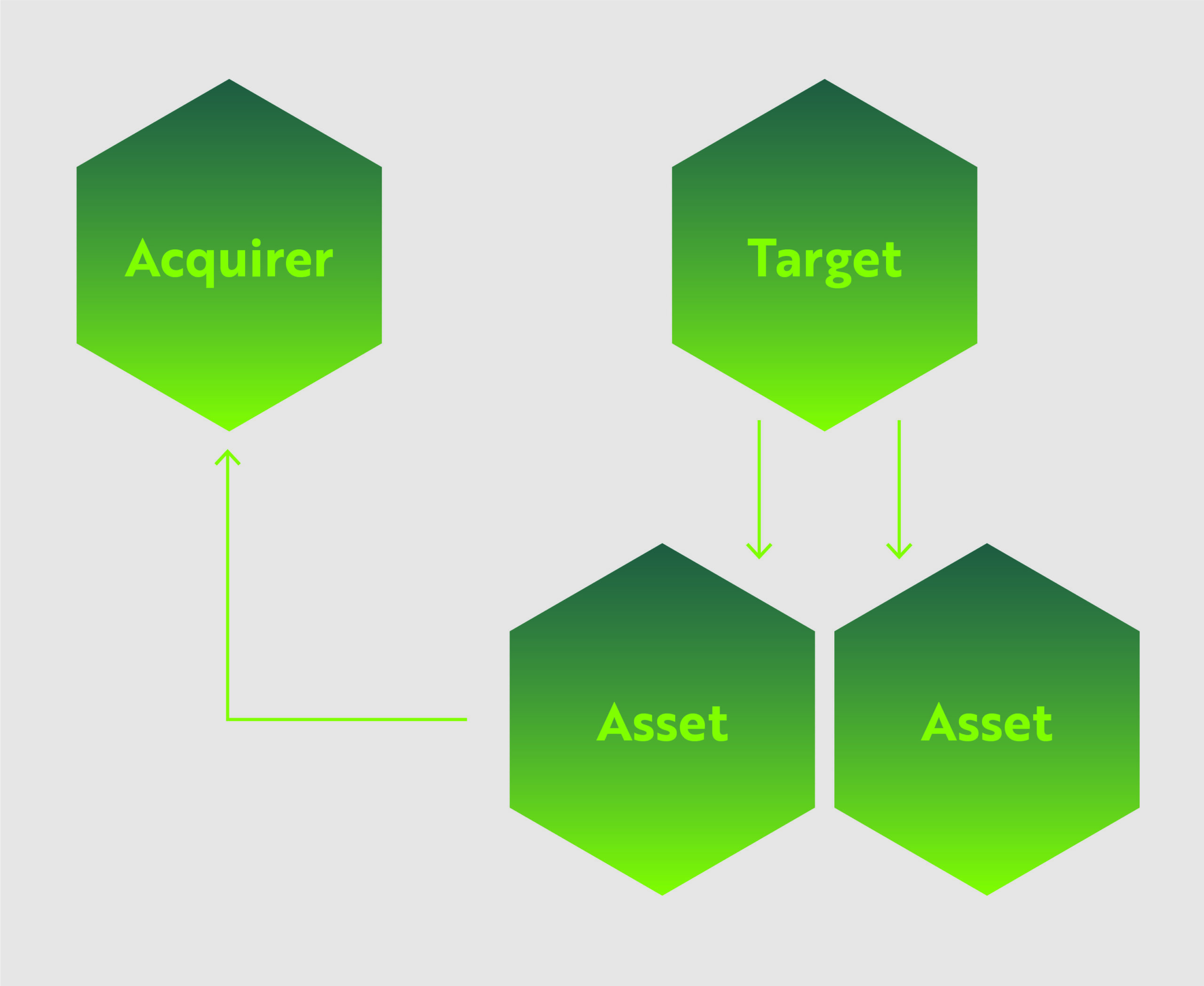

Asset acquisitions

In this structure, the Acquirer identifies specific or all assets held by the Target company, which can include equipment, real estate, leases, inventory, equipment and patents, and pays an agreed-upon value, in cash and/or stock, for those assets. The Target company may continue operation after the deal.

This is one of the most common transaction structures, as the Acquirer can identify the specific assets that match their business plan and avoid burdensome or undesirable aspects of the Target company. From the Target company’s perspective, they can offload under-performing/non-core assets or streamline operations, and either continue operating, pivot, or unwind their company.

For the cannabis industry, asset sales are often preferred as many companies are still working out their operational specifics and the exchange of assets can be mutually beneficial.

Advantages/Disadvantages

Transfer of Liabilities: One of the strongest advantages of an asset deal structure is that the process of negotiating the assets for sale will include discussion of related liabilities. In many cases, the Acquirer can avoid taking on certain liabilities, depending on the types of assets discussed. This gives the Acquirer an added line of defense for protecting itself against inherited liabilities.

Shareholder/Third-Party Consent: Asset acquisitions are unique among the M&A transaction structures in that they do not necessarily require a stockholder majority agreement to conduct the deal.

However, because the entire Target company entity is not transferred in the deal, consent of third-parties can be a major roadblock. Unfortunately, as stated in our M&A Strategy article, many cannabis markets licenses are inextricably linked to the organization/ownership group that applied for and received the license. This means that acquiring an asset, for example a cultivation facility, does not necessarily mean the license to operate the facility can be included in the deal, and would likely require re-application or negotiation with regulatory authorities.

Tax Impact: A major consideration is the potential tax implications of an asset deal. Both the Acquirer and Target company will face immediate tax consequences following the deal. The Acquirer has a slight advantage in that a “step-up” in basis typically occurs, allowing the acquirer to depreciate the assets following the deal. Whereas the Target company is liable for the corporate tax of the sale and will also pay taxes on dividends from the sale.

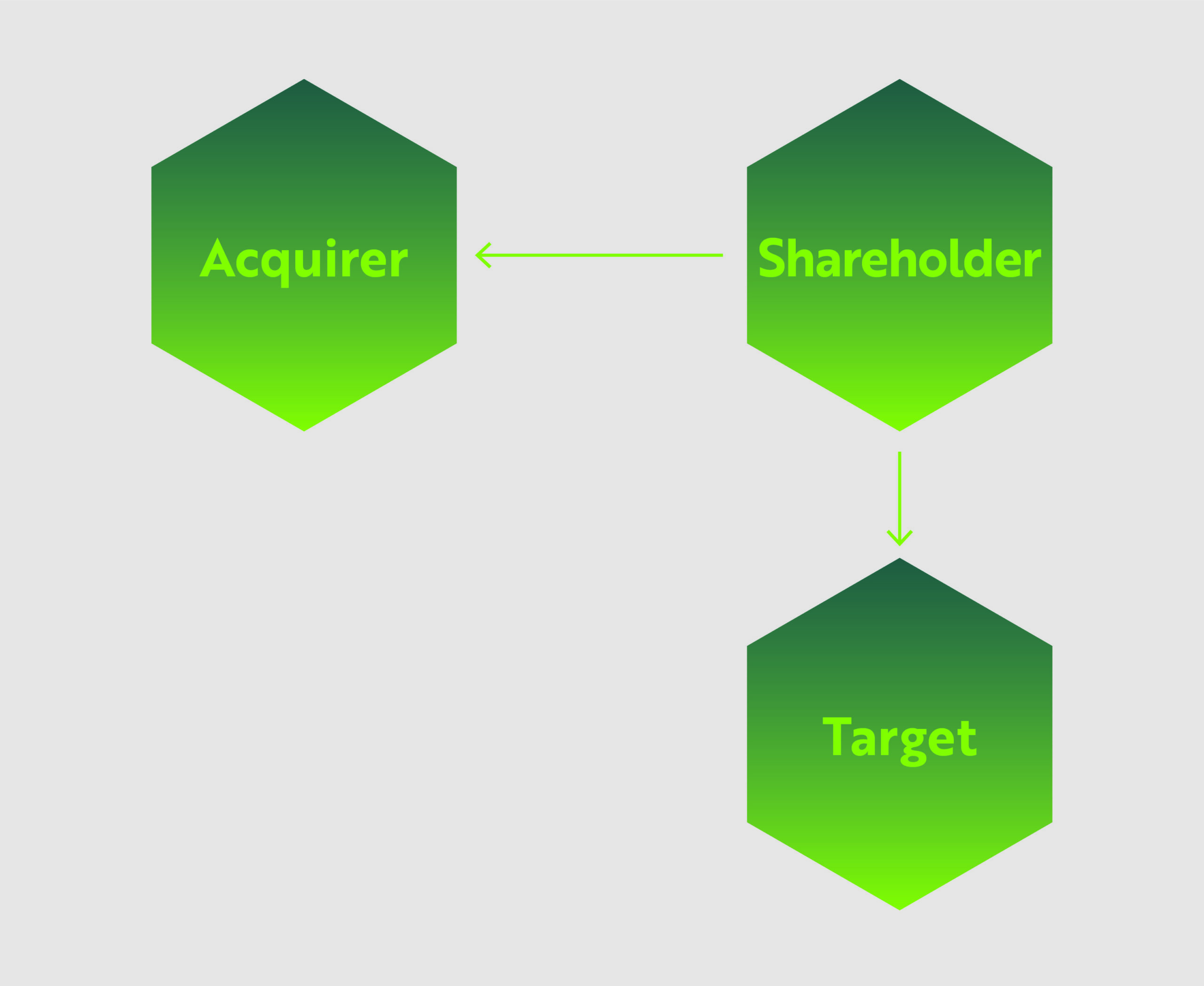

Stock/share purchase

In some ways, a stock/share purchase is a more efficient version of a merger. In this structure, the acquiring company simply purchases the ownership shares of the Target business. The companies do not necessarily merge and the Target company retains its name, structure, operations and business contracts. The Target business simply has a new ownership group.

Advantages/Disadvantages

Transfer of Liabilities: Since the entirety of the company comes under new ownership, all related liabilities are also transferred.

Shareholder/Third Party Consent: To complete a stock deal, the Acquirer needs shareholder approval, which is not problematic in many circumstances. But if the deal is for 100% of a company and/or the Target company has a plenitude of minority shareholders, getting shareholder approval can be difficult, and in some cases, make a deal impossible.

Because assets and contracts remain in the name of the Target company, third party consent is typically not required unless the relevant contracts contain specific prohibitions against assignment when there is a change of control.

Tax Impact: The primary concern for this deal is the unequal tax burdens for the Acquirer vs the Shareholders of the Target company. This structure is ideal for Target company shareholders because it avoids the double taxation that typically occurs with asset sales. Whereas Acquirers face several potentially unfavorable tax outcomes. Firstly, the Target company’s assets do not get adjusted to fair market value, and instead, continue with their historical tax basis. This denies the Acquirer any benefits from depreciation or amortization of the assets (although admittedly not as important in the cannabis industry due to 280E). Additionally, the Acquirer inherits any tax liabilities and uncertain tax positions from the Target company, raising the risk profile of the transaction.

Three types of mergers

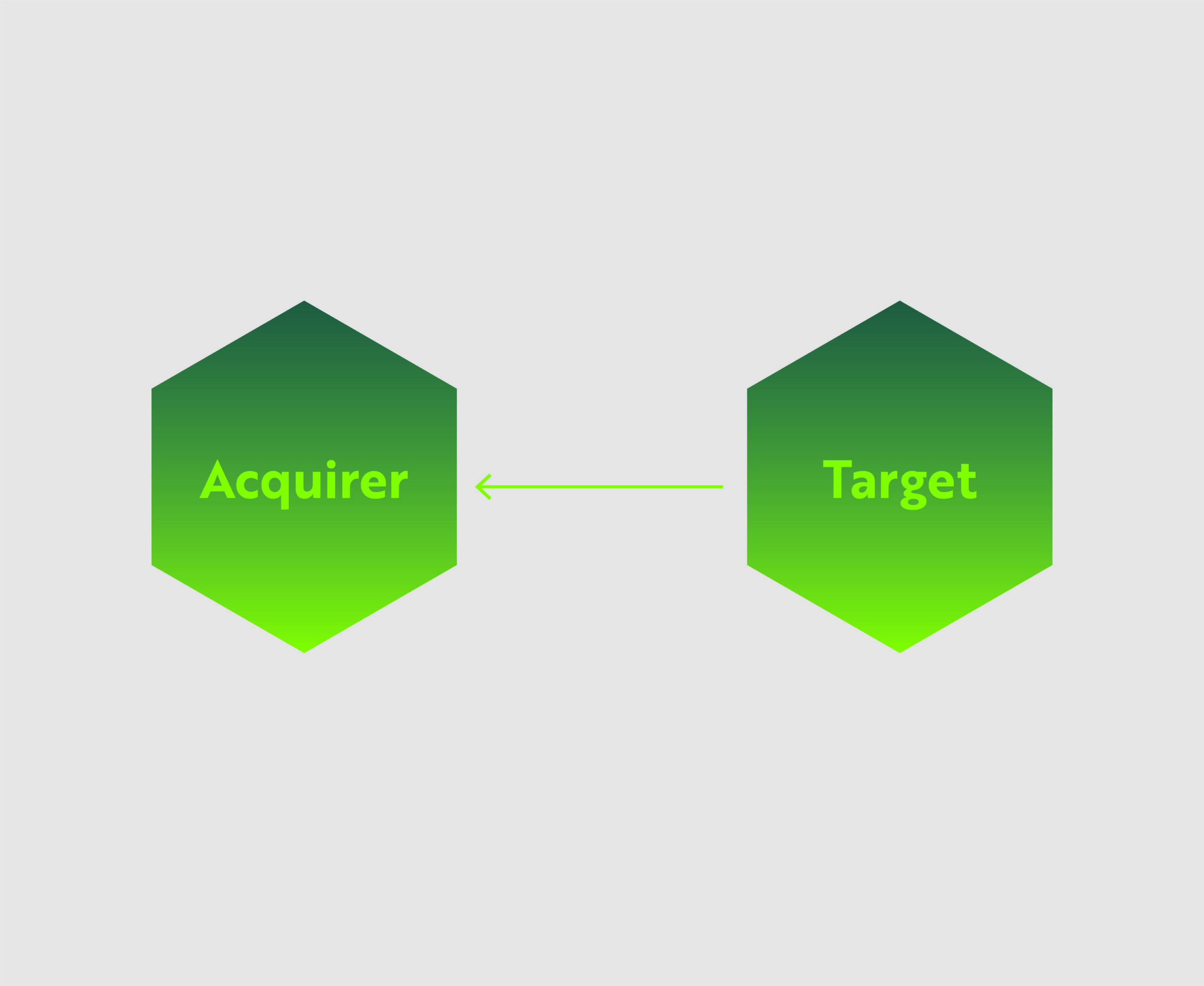

1: Direct merger

In the most straight-forward option, the Acquiring company simply acquires the entirety of the target company, including all assets and liabilities. Target company shareholders are either bought out of their shares with cash, promissory notes, or given compensatory shares of the Acquiring company. The Target company is then considered dissolved upon completion of the deal.

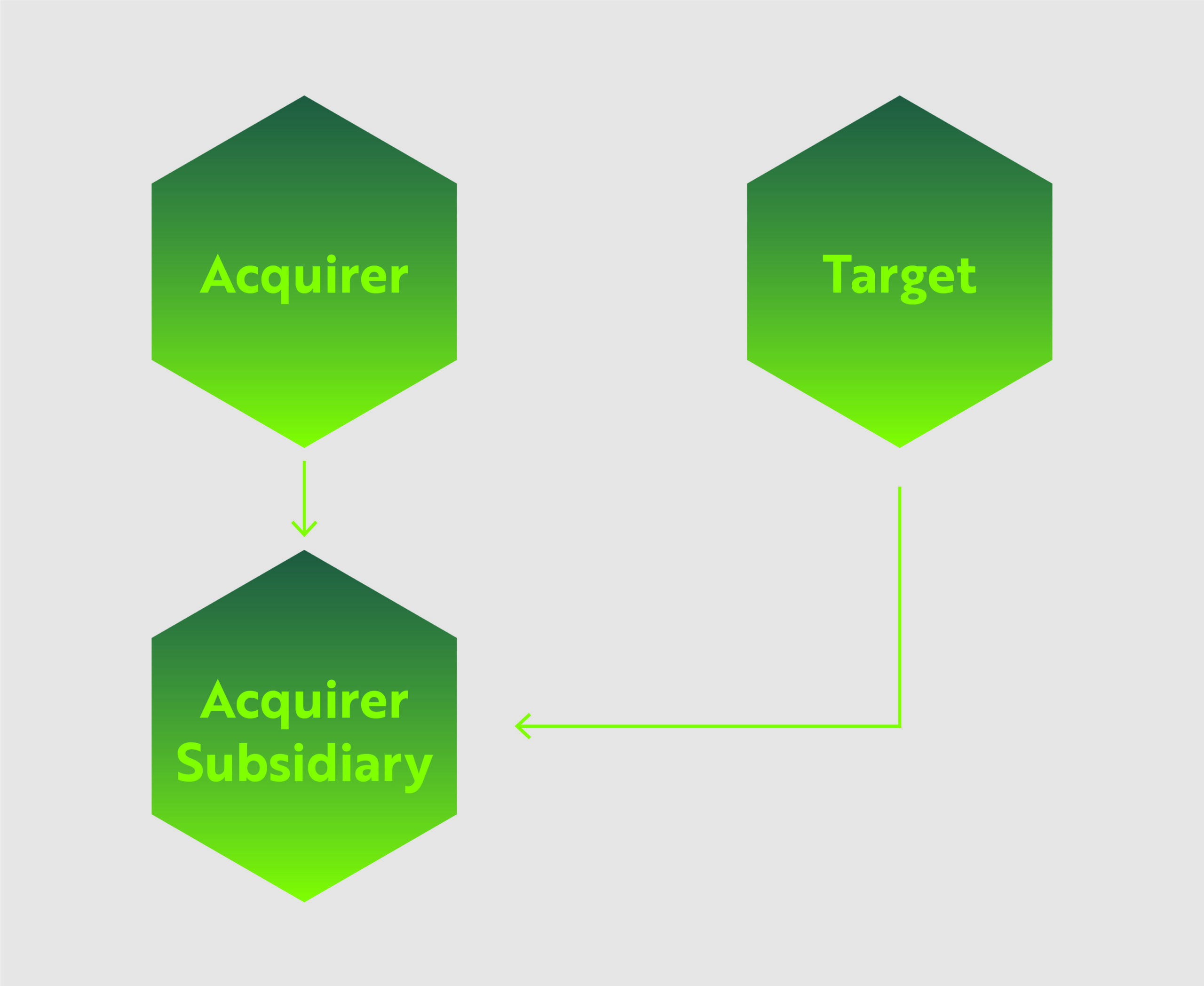

2: Forward indirect merger

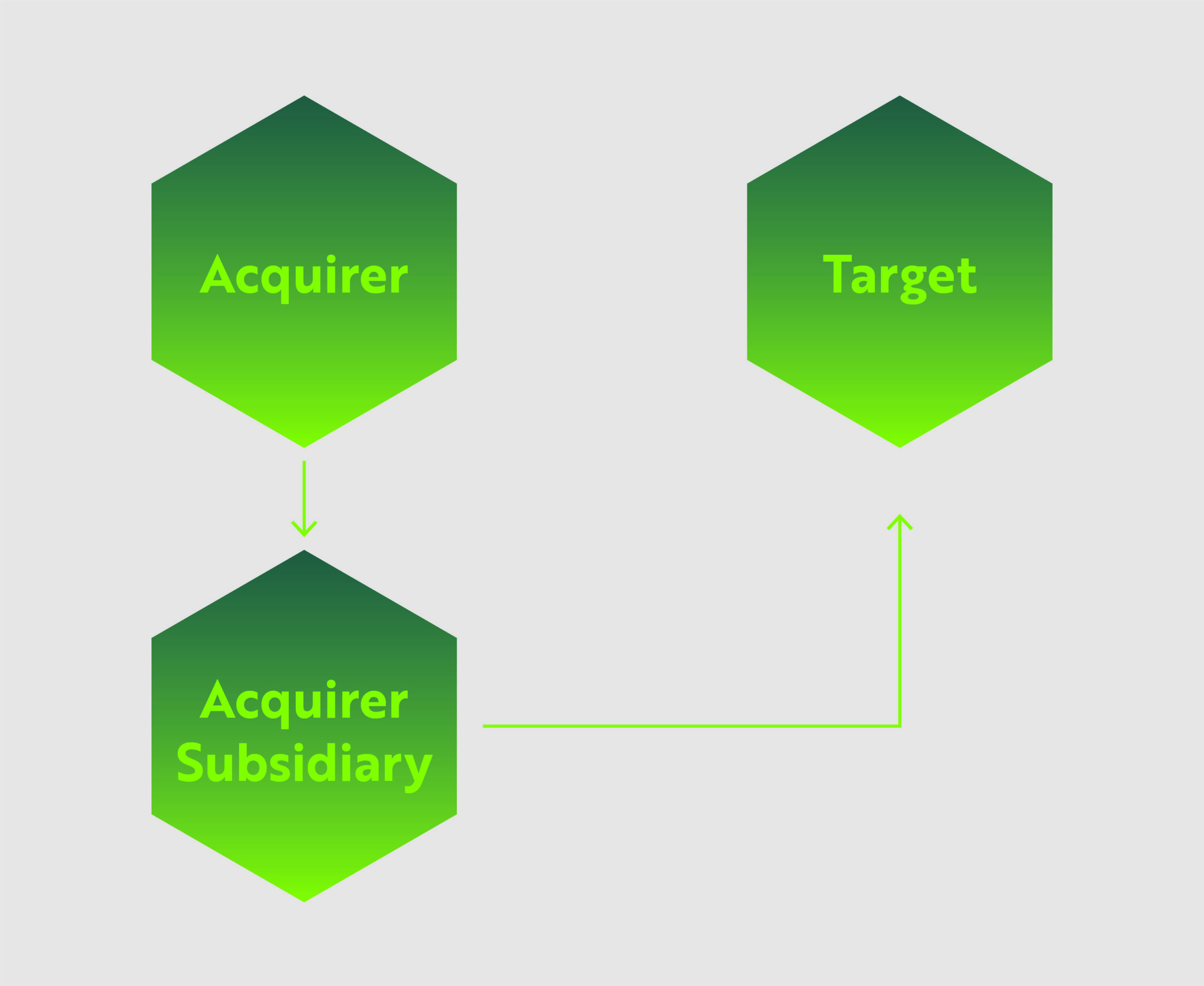

Also known as a forward triangular merger, the Acquiring company merges the Target company into a subsidiary of the Acquirer. The Target company is dissolved upon completion of the deal.

3: Reverse indirect merger

The third merger option is called the reverse triangular merger. In this deal the Acquirer uses a wholly-owned subsidiary to merge with the Target company. In this instance, the Target company is the surviving entity.

This is one of the most common merger types because not only is the Acquirer protected from certain liabilities due to the use of the subsidiary, but the Target company’s assets and contracts are preserved. In the cannabis industry, this is particularly advantageous because Acquirers can avoid a lot of red tape when entering a new market by simply taking up the licenses and business deals of the Target company.

Advantages/Disadvantages

Transfer of Liabilities: In option #1, the acquirer assumes all liabilities from the Target company. Options #2 and #3, provide some protection as the use of the subsidiary helps shield the Acquirer from certain liabilities.

Shareholder/Third Party Consent: Mergers can be performed without 100% shareholder approval. Typically, the Acquirer and Target company leadership will determine a mutually acceptable stockholder approval threshold.

Options #1 and #2, where the Target company is ultimately dissolved, will require re-negotiation of certain contracts and licenses. Whereas in option #3, as long as the Target company remains in operation, the contracts and licenses will likely remain intact, barring any “change of control” conditions.

Tax Impact: Ultimately, the tax implications of the merger options are complex and depend on whether cash or shares are used. Some mergers and reorganizations can be structured so that at least a part of the sale proceeds, in the form of acquirer’s stock, can receive tax-deferred treatment.

In conclusion

Each deal structure comes with its own tax advantages (or disadvantages), business continuity implications, and legal requirements. All of these factors must be considered and balanced during the negotiating process.

Catch up on previous articles in this series and see what’s coming next…

]]>