- Companies face tax burden challenges related the classification of cannabis as a Schedule I controlled substance and IRC 280E.

- To navigate this, companies may be able to utilize vertical integration strategies and incorporate transfer pricing best practices to minimize tax exposure.

- A transfer pricing study will help identify and risks or opportunities for improvement.

As the cannabis market continues to grow, in the United States cannabis operators continue to face difficulties related to an excessive tax burden due to IRC 280E. One of the most effective strategies for mitigating tax exposure under 280E has been to leverage the benefits of vertical integration.

Since IRC 280E affects the various verticals differently, some cannabis companies are able to isolate activities within distinct business units and maximize Cost of Goods Sold (COGS) calculation to mitigate the impact of IRC 280E.

The potential downside is two-fold. First, IRS tax court cases have made it clear that isolating business units is not a universal solution. And secondly, if not optimally established and documented, transactions between the business units can be problematic and create issues with the IRS.

This article breaks down the impact of IRC 280E, demonstrates the potential benefits of vertical integration, and describes how a proactive transfer pricing strategy can help you maneuver the specific tax and regulatory considerations that affect the industry.

What IRC 280E means for your tax liability

Section 280E penalizes traffickers of Schedule I or II drugs by prohibiting the deduction of “ordinary and necessary” business expenses after reducing gross receipts by COGS, essentially resulting in your federal income tax liability being calculated based on gross income, not net income. For a cannabis operator, COGS typically consist of the cost of acquiring inventory by purchase or production.

Not only are these cannabis companies facing high federal taxes, but there is now an intense level of scrutiny in both federal and state tax audits on intercompany arrangements.

Impact of vertical integration on IRC 280E calculations

Many cannabis companies have become vertically integrated, i.e., combining production function (i.e., cultivation and manufacturing) of cannabis with retail or resale (i.e., distribution) or sometimes all three. Since Section 280E is directly related to selling or the “trafficking” of cannabis-related products, it has the biggest potential impact on retail operations. This means that if a producer can support a higher selling price to its retailer, the retailer will have more COGS from the producer, and the producer will have more costs to deduct because of the allowance of indirect costs.

The business motivation for vertical integration is to better control the supply chain and the end user’s experience. From a tax perspective, cannabis taxpayers want to dis-integrate activities subject to 280E from those for which a position can be argued that they are non-280E activities, such as management services. The Internal Revenue Service (IRS) uses transfer pricing to challenge such segregation and to make allocations between or among the members of a controlled group.

How a transfer pricing study can help your cannabis business

Whether its receives the recent budget infusion or not, the IRS is likely to conduct more transfer pricing audits of the cannabis industry, compared to other industries. These audits frequently result in much higher tax adjustments and significant penalties. In addition, since several states have had budgetary shortfalls due to COVID-19 and other factors, multistate businesses are more frequently being audited by individual states’ tax authorities. If your business has international or domestic intercompany transactions, you’re facing a difficult and uphill battle amid current local, state, and federal tax regulations. The best defense against an IRS transfer pricing audit is a comprehensive transfer pricing study.

A robust transfer pricing study provides the basis with which a company can refute and push back against federal and state claims that their intercompany transactions have no economic or operational substance. As part of a transfer pricing study we will work with you to identify key classes of intercompany transactions, document the pricing of such transactions and reference comparable benchmark data sets to support qualifying transactions. Where transactions fall outside norms, we will work with you to identify differentiating characteristics and seek other data if available, or recommend policy and pricing changes, along with an assessment of the potential exposure.

Taxpayers with inadequate or out of date transfer pricing policies risk an increased likelihood of controversy and transfer pricing adjustments. Thus, even if you have had a transfer pricing study performed in the past, it is important to have it reviewed and updated.

While a transfer pricing study directly reduces a company’s risk of tax assessments and liabilities resulting from tax audits, they also indirectly reduce execution risk when a company is considering an M&A transaction, a capital raise, or go public transaction.

How MGO can help you integrate transfer pricing for the cannabis industry

MGO’s transfer pricing practice has significant experience with the various transfer pricing concerns of the cannabis industry. We also work closely with our federal and state tax practices to assist many cannabis companies with their specific tax and regulatory considerations, which include:

- Section 280E disallowance of ordinary business expense deductions;

- Common supply chain concerns for operators, like state restrictions on inventory and separation of cannabis and industrial hemp;

- Non-plant-touching structures that operate independently from the 280E-affected business lines; and

- Sales and excise taxes specific to the cannabis industry.

To learn more about how we can help support establishing, optimizing, and documenting transfer pricing policies so your business can grow in this dynamic industry, contact us.

]]>The tax relief postpones tax filing and payment deadlines occurring between January 8, 2023, and May 15, 2023, to a new due date of October 15, 2023.

Some of the filings and payments postponed include:

- Individual income tax returns due on April 18

- Business tax returns normally due on March 15 and April 18

- 2022 contributions to IRAs and health savings accounts

- Quarterly estimated tax payments normally due January 17 and April 18

- Quarterly payroll and excise tax returns normally due on January 31 and April 30

The current list of counties that qualify for this relief can be found here.

If you qualify for this postponement, you generally do not need to contact the IRS or FTB to obtain relief. Relief is automatically granted for affected taxpayers who have an address of record located in one of the designated counties. However, if you still receive a late filing or late payment notice and the notice shows the original or extended filing, payment, or deposit due date falling within the postponement period, you should call the number on the notice to have the penalty abated.

If you have questions or need assistance, contact MGO’s experienced State and Local Tax team.

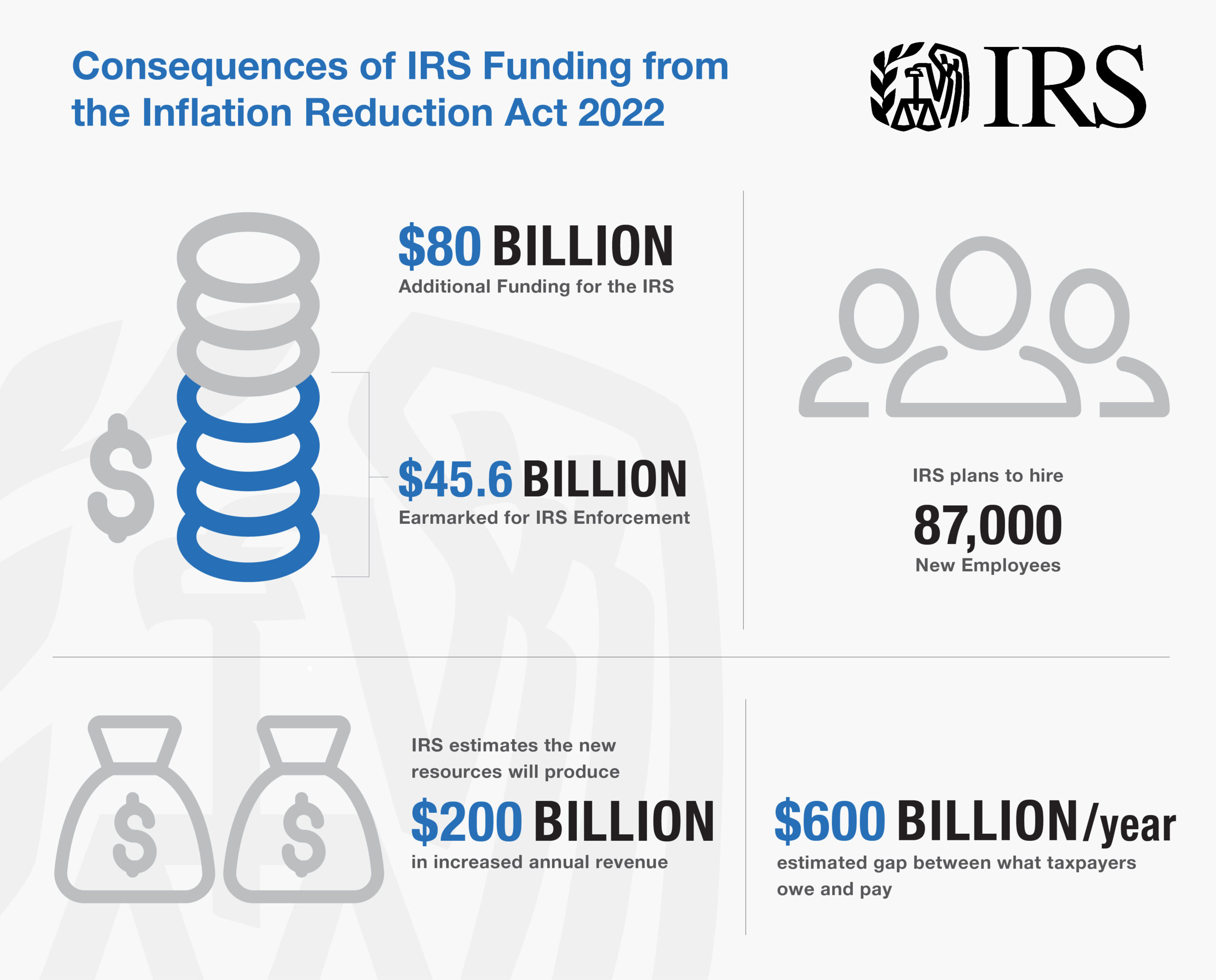

]]>- The Inflation Reduction Act of 2022 includes $80B in funding for the Internal Revenue Service.

- Over half of the funding will be set aside for IRS enforcement so the agency can hire more staff to conduct more audits, hoping to target those who do not pay their taxes.

- This will most likely subject those taxpayers with complex filings to additional scrutiny.

The Inflation Reduction Act of 2022 was recently signed into law with an eye-opening provision: the inclusion of nearly $80 billion in additional funding for the Internal Revenue Service (IRS). $45.6 billion of that is earmarked for IRS enforcement, which will be used to help the underfunded agency hire additional staff and conduct future audits in the hopes of collecting unpaid taxes.

Many publications cite the IRS plans to hire up to 87,000 new employees, though the actual number will be released in the coming months. These new hires will fill positions ranging from auditors to customer service representatives to IT specialists. The IRS has been plagued by more than a decade of budget cuts, which has limited its ability to modernize its old technology and staff appropriately. Since 2010, the agency’s enforcement staff has declined by 30%. The funding appropriate in the Inflation Reduction Act hopes to reverse this trend and bring in an estimated $203 billion in increased revenue.

The MGO Tax Controversy team breaks down what you need to know about this big change that could increase your risk of an audit.

How will the increase in IRS staff affect taxpayers?

Critics of the increase in IRS funding have claimed that the new resources will be used to target low to middle-income Americans and small businesses, burdening them with more audits and examinations. The Treasury Department refutes these claims reiterating they plan to focus primarily on large corporations and the wealthy — those more likely to evade paying their taxes — to close the tax gap, or the difference between what taxpayers pay in taxes and what they actually owe – an estimated to be $600 billion per year.

The IRS hopes the investment in funding will bring in around $203.7 billion in revenue because between 2015 and 2019, IRS audits declined significantly — 75% for Americans making $1 million or more and 33% for filers with low to moderate incomes. Lower-income Americans are mostly wage earners, so their audits are less complex and can be automated. However, more complex filers, notably large corporations and high-net-worth individuals and families – require the hands-on engagement of IRS agents and are most likely to experience increased levels of scrutiny from the new hires.

Ultimately, the average taxpayer should have an improved tax filing experience. New staff will be on hand to answer questions by phone, technology systems will be improved and modernized, and the backlog of unprocessed returns should diminish.

What is the timeline for implementing these changes?

While there is no set timeline, it is likely the way IRS audits work will change with the increase in funding. Currently, software is used to rank each tax return with a numeric score, and higher scores trigger an audit. Other mechanisms the IRS uses to determine candidates for audits include enforcement initiatives referred to as “campaigns” based on various criteria. The new funding will take time to phase in, and so will the hiring and training of new workers. It is expected new auditors will complete a six-month training program, starting small with cases involving a few hundred thousand dollars instead of tens of millions. Forbes performed some creative math to conclude while the funding will increase IRS audits, it is not likely to occur for the next few years.

How can I avoid future audits?

The best way to avoid an audit remains simple: pay your taxes on time and in compliance with tax laws. Simple accounting and documentation best practices are your best friend. If you feel you are at risk for a potential audit, you’ll want to get a head start now by ensuring your records are accurate and have been updated and maintained. Save your receipts and include every detail you can in your bookkeeping logs. If you do get audited in the coming wave, you’ll be glad you have all of this information organized and on-hand.

Our perspective on the increase in IRS staffing

The IRS has long been criticized because of their inability to provide taxpayers with the level and quality of service they deserve. The increase in funding as part of the Inflation Reduction Act should help. On the other hand, the number of tax audits is likely to increase, and you will want to be ready.

MGO’s dedicated Tax Controversy team can help by providing a holistic look at your tax filings as well as provide guidance for conflict resolution. From prevention to resolution, we guide you every step of the way.

If you’re an operator or investor in the cannabis industry, our Tax Practice recently published the Cannabis IRS Audit Survival Guide, which details everything you need to do to prepare for and navigate a tax audit. You can download the Guide for free here.

About the author

T. Renee Parker is a tax partner and the National Tax Controversy Practice Leader at MGO. With more than 15 years of tax controversy experience, she is a member of the IRS Tax Advocacy Panel and is well-versed in all areas of tax controversy. These include but are not limited to U.S. federal, state, and local tax audits; sales and use/payroll tax audits; international tax compliance related audits; negotiation and settlements with tax authorities; and corresponding and negotiation with tax authorities. Contact Renee at RParker@MGOCPA.com.

]]>Because of these newly tightened conditions, companies may face challenges when raising capital, forcing them to adopt a more thoughtful approach to seek funding. Likewise, investors will want to ensure their priorities are protected and their returns met. The combination of a given borrower’s need for capital and a financer’s desire to seek favorable returns may lead to the creation of agreements that have characteristics of both debt and equity. As such, it is crucial for all parties involved to understand the resulting tax classification and the treatment of these arrangements, so all expectations are met.

The taxation of debt and equity

For borrowers, the difference between debt and equity can be critical because interest payments are generally tax deductible and subject to certain limitations. Dividends or other payments related to equity would not be deductible for U.S. federal income tax purposes.

Enacted as part of the Tax Cuts and Job Act (TCJA) of 2017, one main limit on interest deductibility is the IRC 163(j) limit on the amount of business interest that can be deducted each year. This limit is calculated as 30 percent of adjusted taxable income, which prior to the 2022 tax year closely resembled earnings before interest, taxes, depreciation, and amortization (EBITDA). However, starting with the 2022 tax year adjusted taxable income excludes depreciation and amortization, becoming EBIT. This should result in a lower limit on the amount of interest expense that can be deducted each year. Any interest expense exceeding this annual limit can be carried forward to future years.

Determining if an arrangement is debt or equity for federal income tax purposes

Classifying an arrangement as debt or equity is made on a case-by-case basis depending on the facts and circumstances of a given agreement. While there is currently little guidance in this area beyond case law, the Internal Revenue Service (IRS) has issued a list of factors to consider when questioning whether something is debt or equity. (Keep in mind, however, that the IRS states not one factor is conclusive.) The factors include whether:

- An agreement contains an unconditional promise to pay a sum certain on demand or at maturity,

- A lender can enforce the payment of principal and interest by the borrower, and

- A borrower is thinly capitalized.

The courts have also established a broader — but similar — list of factors to consider when determining whether an instrument should be treated as debt or equity. Both the IRS and the courts have generally placed more weight on whether an instrument provides for the rights and remedies of a creditor, whether the parties intend to establish a debtor-creditor relationship, and if the intent is economically feasible. Some factors include:

- Participation in management (as a result of advances),

- Identity of interest between creditor and stockholder,

- Thinness of capital structure in relation to debt, and

- Ability of a corporation to obtain credit from outside sources.

For international companies, the characterization of debt or equity when considered in a cross-border funding arrangement is important, as withholding tax rates may apply to interest payments and may differ from tax rates applied to dividends. Further, withholding tax obligations occurs when a cash payment is made. If you have a cross-border arrangement, it is crucial to know if you have debt or equity on your hands.

Special rules related to payment-in-kind

Once it is determined that an agreement should be classified as debt for U.S. federal income tax purposes, some borrowers may prefer to set aside interest payments or pay interest with securities, which is often referred to as payment-in-kind (PIK). This is generally done to preserve cash flow for operations and growth of the business. When a borrower chooses this route, U.S. federal income tax rules will impute an interest payment to the lender.

While using a PIK mechanism will not automatically result in the debt being recharacterized as equity for federal income tax purposes, it can support viewing the instrument as equity.

Limits to deductible debt interest

There are limitations that can apply to interest deductibility. As noted above, IRC 163(j) limits deductibility of business interest; for a corporation, this is deemed to be all interest regardless of use. Another provision that can result in interest deductibility limitation is IRC 163(l), which applies to certain convertible notes and similar instruments held by corporations.

For cannabis operators, it is important to consider that IRC 280E disallows interest deductions. Hence, it is highly detrimental for cannabis operators to issue debt from entities that are cannabis plant-touching.

How we can help

Due to the nature of the debt versus equity analysis, companies thinking about fundraising should plan on how they intend to perform the raise and whether to have the raise treated as equity or debt. If debt classification is desired, a borrower should take the steps needed to strengthen the facts of the transaction to support the arrangement as a debt instrument.

MGO’s dedicated tax team has extensive experience advising companies across industries on capital-raising, debt refinancing and restructuring, recapitalizations, and other tax transactions. If you are planning to fundraise, or you are currently in the process of conducting a debt versus equity analysis, contact us today.

About the authors

Maryam Nicholes is a director and the national leader of MGO’s M&A Tax Advisory Services group. She has more than 13 years of experience advising on a wide range of clients, consulting on structuring and implementation of transactions including mergers, acquisitions and dispositions, global reorganizations, and new investment platforms. She also provides planning and related deal modeling regarding global cash tax exposures, repatriation planning, and related debt structuring and workout. Contact Maryam at MNicholes@mgocpa.com.

Matt Sapowith is a tax partner at MGO. He has more than 14 years of tax planning and compliance experience in areas including corporate and partnership taxation, international tax, M&A transaction advisory, transfer pricing, state and local tax, R&D credit, and compensation planning. He assists companies with structuring for multiple business lines, excise tax and sales tax planning and compliance in a variety of industries including technology, financial services, manufacturing and distribution, professional services, retail and consumer goods, cannabis, and cryptocurrency. Contact Matt at MSapowith@mgocpa.com.

]]>- Increasing Internal Revenue Service (IRS) budget

- Implementing a corporate tax minimum

- Instituting and increasing tax credits focused on investing in green technologies

Notable items that were not addressed in the IRA include removing the $10,000 SALT cap and mandatory capitalization of research and development (R&D) expenses, both provisions of the Tax Cuts and Jobs Act of 2017.

The bill is over 300 pages in length with a number of wide-ranging components. In the following summary we’ll provide the key points that will be affecting taxpayers in the coming years.

Additional funding to the IRS for tax enforcement

One of the most talked-about provisions involves increased funding for the IRS.

Key details:

- Approximately $80 billion in funding over the next 10 years for tax services, operations support, business system modernization, and enforcement

- Enforcement – $46 billion

- Operations support – $25 billion

- Business systems modernization – $5 billion

- Taxpayer services – $3 billion

- An estimated $124 to $200 billion will be generated from enforcement and compliance efforts

- Enforcement is focused on taxpayers – both corporate and non-corporate – with income greater than $400,000

Extension of the business loss limitation of noncorporate taxpayers

The IRA extends the excess business loss limitation for noncorporate taxpayers.

Key details:

- Two year extension on IRC Sec. 461(l) until December 31, 2028

- IRC Sec. 461(l) limits noncorporate taxpayers from deducting business losses above thresholds that are annually indexed for inflation

- These limits are $540,000 for married filing jointly and $270,000 for single and married filing single for the 2022 tax year

- Suspended amounts are converted to net operating losses and may be able to be used in subsequent years

Excise tax on repurchases of corporate stock

The IRA includes a 1% excise tax on stock repurchases by domestic public companies listed on an established securities market. The tax applies to repurchases executed after December 31st, 2022.

Key details:

- 1% excise tax on the full market value (FMV) of stock repurchased by publicly traded US corporations

- Will impact redemptions and certain acquisitions and repurchases of publicly traded foreign corporation stock

- Not an income tax for purposes of ASC 740

- Includes special rules for “applicable foreign corporations” and “surrogate foreign corporations”

- Notable exceptions:

- Stock is contributed to employer sponsored retirement plan

- Stock repurchase is part of a corporate reorganization

- Total value of stock repurchased during the taxable year does not exceed $1 million

- Repurchase by securities dealer in ordinary course of business

- If the repurchase qualifies as a dividend

- If the repurchase is by a regulated investment company (RIC) or a real estate investment trust (REIT)

15% corporate alternative minimum tax

The IRA reinstates the corporate alternative minimum tax (AMT) for large corporations, which had been previously eliminated by the Trump Administration’s Tax Cuts and Jobs Act.

Two key elements to note is that this revised AMT only impacts corporations with annual profits exceeding $1 billion, and includes carve-outs for certain manufacturers and subsidiaries of private equity firms.

Key details:

- 15% tax on adjusted financial statement income (i.e., this would be a book minimum tax)

- Affects tax years beginning after December 31, 2022

- Applies to corporations with profits over $1 billion based off adjusted financial income

- For US corporations with foreign parents, it would apply to income earned in the US of $100 million or more of average annual earnings in three prior years and where the overall international financial reporting group has income of $1 billion or more

- Treatment of split offs remains uncertain. Even though these are tax-free reorganizations for tax purposes, gain is recorded for financial accounting purposes

- Joint Committee on Taxation expects that this new tax would apply to only about 150 corporate taxpayers, approximately equal to 30% of the Fortune 500

Tax credit additions and modifications

A significant number of provisions add or enhance credits and incentives that pertain to domestic research and green energy initiatives. Noteworthy changes include:

Increased small business payroll tax credits for research activities:

- Qualified payroll tax credit for increasing research activities raised from $250,000 to $500,000

- First $250,000 will be applied against the FICA payroll tax liability. Second $250,000 will be applied against the employer portion of Medicare payroll tax.

- Applies for taxable years beginning after December 31, 2022

- Limited to tax imposed for calendar quarter with unused amounts being carried forward

- Qualifying small businesses are required to have less than $5 million in gross receipts in current year and no gross receipts prior to the 5 year period ending with the current year

Green initiative tax credits and incentives:

- Credits for purchasing new and previously-owned clean vehicles

- Extension of IRC Sec. 45L – New Energy Efficient Home Credit – extended to qualified new energy efficient homes acquired before January 1, 2033. Increase value of available credit for single-family homes to $2,500 and modified the credit available for multi-family homes.

- Extension, increase, and modifications to IRC Sec. 25C nonbusiness energy property credit

- Extension and modification of IRC Sec. 25D residential clean energy credit

- IRC Sec. 48 energy credit for businesses and investors

- Expansion of qualifying property, extension of credit including phasedown and phaseout rules, and introduction of incentives

- Credit for producing energy from renewable sources (IRC Sec. 45)

- Retroactive for facilities placed in service after December 31, 2021

- Extends beginning of construction deadline to projects beginning construction before January 1, 2025 including solar energy facilities

- Increased energy credit for solar and wind facilities in certain low-income communities

- New credit for clean hydrogen production

- New credit for zero-emission nuclear power

- Extension of incentives for biodiesel, renewal diesel, and alternative fuels

- Extension of biofuel producer credit

- New income and excise tax credits allowed for sustainable aviation fuel

- Modification of IRC Sec. 179D – Energy Efficient Commercial Buildings Deductions

- Modification of building qualifications

- Deduction increased from $1.88 per square foot to up to $5 per qualified square foot

- Changes in depreciation for certain green energy properties

Final thoughts

The Inflation Reduction Act should have wide-ranging impacts on taxpayers, especially large corporations and high-net-worth individuals. In the coming weeks our tax leaders will dive into the specifics of the legislation, outline immediate and long-term impacts, and provide tax-planning strategies and considerations.

]]>The comment period for these proposed rules lasted for two months, ending on May 9, 2022. During that time, the SEC received more than 100 comments from various sectors, including legal, government, business, and nonprofit. These comments vacillated from critical to supportive, but many had several concerns about the rule’s provisions. For those curious about the specific apprehensions, our Technology and Cybersecurity team analyzes them, as well as the suggested solutions, in this article.

Most common concerns regarding the SEC’s cybersecurity proposal

Within the comments provided on the proposal, there were eight key issues broached along with solutions to these issues.

1. The four-day incident notice deadline

Many commenters believe being given a mere four days to report a cybersecurity incident was not enough time to truly analyze the incident and complete an accurate report. Worried a harried or slapdash report could yield even more security risks, they proposed more flexible solutions to provide accurate disclosures, like:

- A 30-day reporting deadline;

- Government-permitted reporting delays (as needed);

- A modification in the disclosure framework to ensure state notification statutes are exemplified; and

- Additional time for smaller companies to investigate, report, and fully disclose the situation as needed.

2. Law enforcement and national security exceptions

Feedback for the proposed rules also stated some specific incidents should benefit from delayed reporting exceptions, namely those that need to involve law enforcement or security investigations on a larger scale.

This solution allows those grappling with more challenging and involved cybersecurity incidents to remain compliant with the law while doing what is necessary to complete an investigation and strengthen security to prevent future incidents. It also gives law enforcement more freedom to complete their efforts — and prevents publicity that could tip off the attackers, who could then cover their tracks.

3. The definition of key terms

The SEC uses several words that could be misconstrued, have multiple meanings, or are not succinct enough to require disclosures surrounding them. These words, as pointed out in the comments, include:

- Cybersecurity threat,

- Cybersecurity incident, or

- Information systems.

To solve this and streamline compliance reporting requirements, commentors believe the SEC should utilize the thorough and uniform definitions employed by the National Institute of Standards and Technology (NIST), as well as those used in the Cybersecurity Incident Reporting for Critical Infrastructure Act of 2022 (CIRCIA), SEC’s Release Number 33-11028, and the 2016 Presidential Policy Directive on United States Cyber Incident Coordination.

In addition, the SEC can break down each incident or threat into a tier system to accurately encapsulate the severity each tier entails, better describing the impact on the organization.

4. The disclosure of the board of directors’ cybersecurity expertise

Comments also touched on the requirement to include the experience the members of a company’s board of directors have, finding it unnecessary to disclose and tedious to acquire. The suggestions given included eliminating this narrow requirement (primarily because if a board member(s) does not have heavy cybersecurity experience, that could reflect negatively on the company’s prioritization of cybersecurity) even if the company does, in fact, take cybersecurity seriously.

They also call for “cybersecurity expertise” to be defined using broad criteria so smaller companies can meet the requirement without struggling to find an “expert” just to tick a box — or to allow the requirement to meet with a leader at different level in the company besides the board of directors.

5. The accumulation of immaterial events requirement

Another criticism of the proposed rules targets the requirement to list previously undisclosed immaterial cybersecurity incidents, which many comments revealed to find unnecessary and vague, as an incident to one company may be deemed immaterial but found material to another. The lack of consistency and definition means their solution is to either scratch the requirement or, alternatively, provide more guidance on what these incidents should entail to be included, as well as an example of one — and set a one-year limit, as this requirement does not include one.

6. Security program disclosures

Requiring a company to disclose security program-related protocols and plans, like strategies and risk management tactics would, comments to the proposal argue, make the company more vulnerable to future security breaches — as well as inadvertently divulge protected information. To mitigate this, critics suggest removing the requirement to keep companies (and their security plans) safe, allowing a vague summary of the program to meet the requirement; or introducing a confidentiality clause.

7. Fear of regulatory discord

As cybersecurity becomes a bigger issue for all industries across the country, the SEC’s proposal could contradict other states’ laws and requirements regarding cybersecurity (and their varying definitions, triggers, timings, and more). This could create confusion for companies who want to remain compliant in the event of a cyberattack but are unsure of which requirements they must meet to determine if a breach has, in fact, occurred. Readers of the proposed rule believe creating standardized terms and requirements can help. Plus, the SEC should demonstrate how it will work with the other regulations so companies can align their requirements in a streamlined way.

8. Safe harbor provisions

It seemed to many if a company has already reported a material cybersecurity risk, it is redundant to be required to report it again via the Form 8-K. The provided (short) timeframe, too, could cause issues — in the case of a third-party breach, a company may hurry to complete the form without confirming it to be reliable or accurate, defeating the entire point of the form.

This requirement invited split opinions. Some comments mentioned two “safe harbors” (i.e., double reporting) is a good thing, helping the SEC to promote consistent disclosure. Others, however, stated that including both would be redundant, especially with a tight deadline and the lack of clear definitions for these incidents.

Our perspective on the response to the SEC’s cybersecurity proposal

As the SEC strives to increase transparency and prevent malicious cyberattacks, cybersecurity disclosure requirements will continue to change and strengthen. The number of comments received on this proposed rule indicates that companies across industries are not only invested in what these disclosure requirements mean, but they are willing to do what is necessary (albeit logical) to enhance and standardize the way they protect themselves and disclose risk.

Looking forward, the SEC will take these comments into consideration for the next draft of the proposal.

How we can help

While you wait for the next draft of the proposal, remember to stay vigilant—not only to protect your organization, but also to maintain compliance. To stay up to date, bookmark the SEC’s Cybersecurity news and our Technology and Cybersecurity insight library.

Professional service firms like MGO help verify you are compliant and strengthen your overall cybersecurity — so these incidents are less likely to occur, and if they do, you will be ready to mitigate risks at once. Let us know if you are ready to assess your cybersecurity or get started on a SOC for Cybersecurity.

For insights tailored to your company and industry, schedule a conversation with our Technology and Cybersecurity team today.

]]>Understanding IRS overpayment and underpayment rates

The overpayment rate is the sum of the federal short-term rate plus 3 percentage points. For corporations it is the federal short-term rate plus 2 percentage points. For the portion of a corporate overpayment of tax exceeding $10,000, it is the federal short-term rate plus 0.5%.

The underpayment rate is the sum of the federal short-term rate plus 3 percentage points, except underpayments for large corporations is the sum of the federal short-term rate plus 5 percentage points.

Starting April 1, the new increased rates will be:

• 4% for overpayments (3% for corporations),

• 1.5% for the portion of corporate overpayment exceeding $10,000,

• 4% for underpayments, and

• 6% for large corporate underpayments.

How is interest calculated on unpaid taxes?

Interest accrues on any unpaid tax from the due date of the return until the date of payment in full. The interest rate is determined quarterly. Interest compounds daily and is charged on the sum of all outstanding taxes and penalties.

What are the most common penalties?

Failure to Pay Penalty: If a return is filed but the tax owed was not paid on time, a late payment penalty will be imposed at .5% of the unpaid taxes for each month, or the part of the month the taxes remained unpaid. The penalty will not exceed 25% of the unpaid tax amount. Full monthly charges are applied even if taxes are paid in full before the end of the month.

Failure to File Penalty: Based on how late the tax return is filed and the amount of unpaid tax as of the original payment due date, this penalty is 5% of the unpaid taxes for each month, or the part of the month that a tax return is late. The penalty will not exceed 25% of the unpaid tax amount.

Combined Failure to Pay and Failure to File Penalty: If both penalties are applied in the same month, the Failure to File Penalty will be reduced by the amount of the Failure to Pay Penalty applied in that month. Based on the current penalty percentages, the late payment penalty would remain at .5%, and the late filing penalty would be reduced to 4.5%.

Substantial Underpayment Penalty: This penalty applies to (1) individuals if the tax liability is understated by 10% of the tax required to be shown on the return or $5,000, whichever is greater or (2) to corporations, if the tax liability is understated by 10% (or, if greater, $10,000) or $10,000,000. The penalty is 20% of the portion of the underpayment of tax that was understated on the return.

Negligence or Disregard of Rules or Regulations Penalty: At 20% of the portion of the underpayment of tax, this occurs due to negligence (lack of a reasonable attempt to follow the tax laws) or a disregard for the tax rules, meaning the taxpayer carelessly, recklessly, or intentionally ignores the tax laws.

Underpayment of Estimated Tax Penalty: This penalty applies to corporations or individuals that do not make enough estimated tax payments or are late in paying them when required. The penalty is based on (1) the amount of the underpayment, (2) the period when the underpayment was due and underpaid, and (3) the interest rate for underpayments published quarterly by the IRS. To avoid it, corporations can make quarterly estimated tax payments if they expect to owe $500 or more in estimated tax when they file their return. Individual taxpayers can avoid it if they owe less than $1,000 in tax after subtracting withholding and refundable credits, or if they paid withholding and estimated tax of the lesser of at least 90% of the tax for the current year or 100% of tax shown on the prior year’s return.

Can an IRS penalty or interest be removed or abated?

The IRS can remove or reduce some penalties if the taxpayer acted in good faith and can show reasonable cause for the failure to meet their tax obligations. However, by law, the IRS cannot reduce or remove interest unless the penalty is removed or reduced.

Reasonable cause is based on all the facts and circumstances of each situation, and the IRS will consider any reason establishing that a taxpayer used all ordinary business care and prudence to meet their federal tax obligations but were unable to do so. It is important to note that lack of funds is not reasonable cause for failing to file or pay on time — but it could be considered reasonable cause for the failure-to-pay penalty.

The IRS’s First Time Penalty Abatement Policy (FTA) can provide relief from a penalty if a taxpayer has not incurred penalties previously. To qualify under this policy, the taxpayer (1) did not previously need to file a return or had no penalties for the last 3 years prior to the tax year in which the penalty was received, (2) is current on all required returns or extensions of time to file, and (3) has paid or arranged to pay any tax due.

What options are available if a taxpayer cannot pay the taxes due?

- Short Term Payment Plan: This plan is not available for businesses unless it is a sole proprietor or an independent contractor. There is no setup fee, and the balance must be paid within 180 days. A short-term payment plan is available for individuals if less than $100,00 in combined tax, penalties and interest is due. Penalties and interest accrue until the balance is paid in full.

- Long Term Payment Plan (Installment Agreements): An installment agreement is available for individuals if less than $50,000 is owed or for a business if less than $25,000 is due in combined tax, penalties and interest and all required returns are filed. Penalties and interest accrue until the balance is paid in full. The maximum term for most installment plans is 72 months.

If a taxpayer pays less than the full amount due, how is the partial payment applied?

If a taxpayer makes a partial payment accepted by the IRS, and the taxpayer provides specific written directions as to the application of the payment, then the IRS will apply the payment as instructed by the taxpayer. If the taxpayer does not provide instructions with the partial payment, then the partial payment is applied to periods in order of priority that the IRS determines is in its best interest. The payment will be applied to satisfy the liability in successive periods in descending order of priority until the payment is absorbed. If the partial payment applied to a period is less than the liability for the period then the payment will be applied to the tax, then penalty and finally interest, until the amount is exhausted (Rev. Proc. 2002-26).

Example: The taxpayer incurs the following tax deficiency, penalties and interest:

Year 1: Tax: 6,000, Penalty: $1,800, Interest: $1,200

Year 2: Tax: 7,000, Penalty: $ 0, Interest: $ 1,500

The IRS agrees that the taxpayer can satisfy the total liability of $17,500 for a payment of $15,000. There is no agreement as to the allocation of the payment and the taxpayer does not provide any directions for application of the partial payment. The payment is first applied to the Year 1 tax, penalty, and interest (a total of $9,000), leaving $6,000 to be applied to Year 2. The remaining amount is completely absorbed by the tax due for Year 2, which results in the payment of interest in Year 1, but not for Year 2.

However, if the partial payment accepted by the IRS is less than the total of tax and penalties due in both years and there is no agreement regarding the application of the partial payment, then nothing is allocated to the interest in either year. For example: following the amounts listed above, if the partial payment was $12,000 instead, then the entire amount is applied to the tax and penalty in Year 1 (a total of $7,800) and the remaining amount of $4,200 is applied to the Year 2 tax due. None of the partial payment would be applied to the interest in either year.

Final thoughts

This year, failing to file your tax payments by the April 18 deadline will cost you more. If you are flirting with the deadline, remember that you will owe interest on any unpaid tax from the return’s due date until the day you actually make the payment — and interest will compound daily.

If you have questions and want to ensure you avoid being hit with tax penalties and interest, please reach out to MGO’s Tax team for assistance. You can rely on us to help you mitigate the impact of the interest rate increase.

Employee Retention Tax Credit

The Employee Retention Tax Credit (ERTC) is a refundable tax credit created by the Coronavirus Aid, Relief and Economic Security (CARES) Act, to encourage businesses to keep employees on their payroll. For 2020, the credit is 70% of up to $10,000 in wages paid by an employer whose business was fully or partially suspended because of COVID-19 or whose gross receipts declined by more than 50%

For 2021, an employer can receive 70 percent of the first $10,000 of qualified wages paid per employee in each qualifying quarter. The credit applies to wages paid from March 13, 2020, through December 31, 2021. And the cost of employer-paid health benefits can be considered part of employees’ qualified wages.

It’s an attractive credit if you qualify.

Eligible businesses

The credit applies to all employers regardless of size, including tax exempt organizations that had a full or partial shutdown because of a government order limiting commerce due to COVID-19 during 2020 or 2021. With the exceptions of state and local governments or small businesses that take Small Business Administration loans, this credit is available to almost everyone.

Of course, there is some fine print:

• To qualify, gross receipts must have declined more than 50 percent during a 2020 or 2021 calendar quarter, when compared to the same quarter in the prior year.

• For employers with 100 or fewer full-time employees, all employee wages qualify for the credit, whether the employer is open for business or shutdown.

• For employers with more than 100 full-time employees, qualified wages are wages paid to employees when they are not providing services due to COVID-19-related circumstances.

One bright point about the ERTC is that employers can be immediately reimbursed for the credit by reducing the amount of payroll taxes they would usually have withheld from employees’ wages. That was a nice touch by the IRS.

Retroactive claims for the ERTC

Although it appears the IRS tried to make this as easy as possible, you may still need a tax professional to sort it out. For instance, if your business had a substantial decline in gross receipts but has now recovered, you can still claim the credit for the difficult period

Retroactive claims for refunds will probably be delayed because currently everything is delayed at the IRS. The credit can be claimed on amended payroll tax returns as long as the statute of limitations remains open, which is three years from the date of filing. So you have some time to claim the credit, but why wait?

Keep December 2021 in mind

The economy is in a state of change, and it is fair to say that we are once again in uncharted territory. On the positive side, there seems to be significant resources and support for businesses from both government and consumers. You and your tax professional should keep your eyes open for credits and benefits to make sure you don’t miss any opportunitie

The ERTC expires in December 2021. Though it may be difficult to think about year-end in the middle of the summer, you’ll want to figure out your position on this credit before December. A tax professional can help you understand the ERTC and help you decide on your next step.

About the author

Michael Silvio is a partner at MGO. He has more than 25 years of experience in public accounting and tax and has served a variety of public and private businesses in the manufacturing, distribution, pharmaceutical, and biotechnology sectors.

]]>Amid the uncertainty and concerns surrounding the COVID-19 outbreak, healthcare providers, public-health specialists, government officials and investors (and the general public) are looking to the biotech industry to create a “game-saving” vaccine against the novel coronavirus.

This optimism, and pressure, is particularly visible in the stock market where – even during the carnage of recent weeks – the biotech industry has held up better than others: the year-to-date decline of the Nasdaq Biotech Index, for instance, was only about half the selloff suffered by the broader market.

And while the industry arguably has performed well, it nevertheless has encountered difficulty on several critical fronts:

- Clinical trial delays and suspensions

- Supply chain failures

- Approval and application delays

“The COVID-19 pandemic represents a significant, ongoing public health threat and has created an unprecedented burden on healthcare systems across the globe,” says Jay Luly, Chief Executive Officer of Enanta Pharmaceuticals. “With the safety of our clinical trial participants in mind, coupled with a desire to alleviate many of the resource constraints at clinical trial sites, Enanta has proactively decided to make adjustments to some of our clinical programs.”

In the following, we take a deeper look at these three issues and the impact they are having on the industry, as well as an analysis of some the potential changes that could impact the biotech industry going forward.

Impact on clinical trials

There is unanimous agreement that COVID-19 already is causing significant delays and suspensions in clinical trials. Why this is important: Absent trial data, new drug filings likely will be delayed … meaning some important new medicines will take longer to reach the market.

BIO, the industry trade group, cites two additional issues that could affect trial schedules. They are:

- Missing or delayed data collection from ongoing clinical trials, particularly at hospital sites overwhelmed by COVID-19 cases

- Difficulties getting new clinical trials up and running because patients are reluctant to enroll or unable to visit hospitals

This is no small matter. Biotech and pharma, together, have some 120 Phase 3 clinical trials (with top-line data readouts) expected before the end of the year, according to BioMedTracker.

Eli Lilly, for instance, said it will delay the start of new clinical trials and suspend enrollment in “most” ongoing studies. Trials in which patient enrollment has already been completed will continue. Lilly is listed as the sponsor of 86 clinical trials currently enrolling patients, including 30 in Phase 3, according to ClinicalTrials.gov. Another 78 studies are active but no longer recruiting patients.

Others recently taking similar actions include Pfizer, Merck, Bristol Myers Squibb, Provention Bio and Galapagos. Each has paused the launch of some new studies, as well as enrollment in some ongoing studies.

The FDA has issued new guidelines designed to help the companies maneuver through this challenging period. Among other things, it offers standards for ensuring the safety of trial participants and maintaining compliance with good clinical practice.

It’s impossible to know how many clinical trials will be affected adversely by the coronavirus outbreak, but the BioMedTracker database features 120 Phase 3 clinical trials being conducted by biotech and pharma companies with market values greater than $300 million. All of these clinical trials were expected to announce top-line results before the end of the year.

At stake are some closely followed drugs with blockbuster projections:

- Asthma medicine tezepelumab from Amgen and AstraZeneca

- Rare disease treatment mitapivat from Agios Pharma

- Heart failure drug omecamtiv mecarbil from Amgen and Cytokinetics

- Hemophilia therapy fitusiran from Sanofi and Alnylam Pharma

The database also includes mid-stage, or Phase 2, clinical trials, some of which could also serve as the basis for FDA submissions. Some 160 such studies have trial results scheduled for this year.

Another potential problem is the fact that the industry outsources much of the day-to-day operations of clinical trials to contract research organizations (CROs) like IQVIA Holdings (IQV), PRA Health Sciences (PRAH), Syneos Health (SYNH), and Medpace Holdings (MEDP). These CROs monitor clinical sites by assigning teams to the clinics to verify data in the trial database accurately reflects the patient’s medical records.

Some clinics, however, have stopped allowing clinical trial monitors on site. And that means companies are unable to “lock” the database (an essential step that precedes analyzing the data).

Patient behavior, too, is having an impact on trials.

A survey by Continuum Clinical, a consulting firm that works with drug makers and trial sites, found that:

- One-third of clinical trial sites expect COVID-19 to have a “big or extremely big” impact on their ability to recruit patients for new trials or keep enrolled patients in existing studies

- 39 percent of 170 clinical trial sites in the U.S. believe patients will be much less or somewhat less likely to enroll in new trials

- 25 percent of the sites expect patients currently enrolled in a trial to be much less or somewhat less willing to continue participating

COVID-19’s impact on supply chains

Expect supply disruptions or shortages of critical medical products in the U.S. So says Dr. Stephen Hahn, FDA Commissioner.

What’s affected:

- Manufacturing and importing active pharmaceutical ingredients (APIs) and excipients

- Manufacturing facilities will be stretched by employee absences

- Training of employees assuming new responsibilities will be critical

- Independent laboratory testing associated with manufacturing may be slowed due to demands for testing related to COVID-19

The agency has been active: It has contacted more than 180 drug companies to discuss the requirement to notify the FDA of supply disruptions and to ask them to evaluate their supply chain. The agency says its focus is on China, but that all supply chains will be impacted.

Application/approval delays

Application and approval timelines also could be at risk. Wall Street analysts worry the COVID-19 outbreak could result in regulatory employees having to work from home for an extended period, regulators becoming infected, or FDA bandwidth being overwhelmed by the virus itself.

Moreover, in instances where a sponsor has an new drug application (NDA), abbreviated new drug application (ANDA), biologic license application (BLA) or application supplement pending with the FDA, they could encounter delays and find the agency not in alignment with their timetables.

Industry press also has reported that the Center for Drug Evaluation and Research (CDER) has cancelled all non-essential travel for the next few weeks. Additionally, all CDER outside meetings, conferences and workshops will be postponed through April. FDA staff have further been encouraged to hold teleconferences rather than in-person meetings with external persons.

Biotech and lifesciences going forward

Predictions, of course, are somewhat chancy given the multiple unknowns at this point. However, there are some emerging developments that seem more likely than others to have enduring impact. Here are five to consider.

Virtual Trials

Given the concerns about interruptions and postponements to clinical trials, virtual trials are likely to become the rule, rather than the exception, in the not-too-distant future. What the FDA currently suggests: virtual visits, phone interviews, self-administration and remote monitoring. These adjustments already are being used during this period of quarantines, travel limitations and closings and the new procedures may get locked in over time.

Friendly FDA

Biotech companies should encounter a very friendly FDA. Over the past 10 years, the agency’s annual approval rate of novel drugs has more than doubled, reaching 48 last year. There’s no reason to believe that trend is going to change. And that should be good news for biotech companies and their pipelines.

Scrutiny of Imports

Imported drug products are facing increased scrutiny at U.S. ports of entry and it’s hard to see the U.S. backing off from that standard in the future. The FDA warns it may deny entry of unsafe products, conduct physical examinations and/or product samplings, review a company’s previous compliance history, and request records in advance/instead of on-site drug inspections.

Restructured Supply Chains

China-based companies are critical components of the international supply chains of multiple industries. Biotech is one of them. Pricing, subcontracting and other factors have contributed to the growth and entrenchment of this structure. Now, however, the chaos caused by COVID-19 has underscored the unprecedented country risk that has been created in the process. Expect efforts aimed at regionalizing supply chains, developing second sources and creating proprietary stockpiles.

More Private/Public Partnerships

Look for greater cooperation between public and private organizations. Real-time example: Governor JB Pritzker’s recent announcement of a new partnership between the state of Illinois and the Illinois Manufacturers’ Association (IMA) and the Illinois Biotechnology Innovation Organization (iBIO) to increase in-state production of essential supplies.

According to the CBCC press release, the emergency regulations are meant to address the vaping crisis: “The emergency regulations are designed to help consumers identify licensed cannabis retail stores, assist law enforcement, and support the legal cannabis market, where products such as vape cartridges are routinely tested to protect public health and safety.”

The code certificate needs to be posted within three feet of any public entrance to a cannabis dispensary or “in a locked display case mounted on the outside wall of the premises.” In addition to paper, the QR code certificate can be printed on glass, metal, or other material. It needs to be 8 ½ inches by 11 inches, the size of a standard sheet of paper. The code itself needs to be 3.75 inches by 3.75 inches.

The regulatory change was pursued by the CBCC to allow consumers and law enforcement officials to be able to quickly discern the origin of a product and ensure its safety after the code is scanned. QR codes will help consumers know they are purchasing a product from a vendor in the legal market.

The cartridges that caused the illnesses that led to the vaping crisis last year originated in the underground market. As of February 18th, 2020, the CDC reported 2,807 cases of illness associated with e-cigarettes across the U.S. and 68 cases resulted in deaths, with four of those in California.

“The proposed regulations will help consumers avoid purchasing cannabis goods from unlicensed businesses by providing a simple way to confirm licensure immediately before entering the premises or receiving a delivery,” said CBCC Chief Lori Ajax.

Unfortunately, illegal cartridges with a lethal amount of Vitamin E look nearly identical to those from legal retailers, as do underground sellers who maintain brick and mortar stores. And because they are underground, they do not comply with regulations. Recent estimates have shown that in California, the underground black market is more than twice the size of the legal market.

Those with smartphones will be able to scan the QR codes to ensure the product comes from a licensed retailer. When they scan the code, it will send them to the BCC’s License Search database where they will be able to see the business license number, license type, its official name, contact information, business structure, premise address, license status, issue date, expiration date, and activities.

In addition, you can see whether the business holds a license for adult use, medical, or both. The database also includes phone numbers and email addresses for all the businesses. In addition, you can see if they hold multiple licenses. Many of the businesses also have links to their respective websites. Active licenses are listed along with those who are suspended, canceled, revoked, inactive, or expired.

While the emergency regulations present another regulatory hurdle for compliant California cannabis businesses, the silver lining is that legal market operators can now advertise their compliance with safety standards – an additional edge in the battle to win market share from black market operators.

]]>