- The IRS has intensified enforcement of transfer pricing regulations, significantly increasing potential penalties.

- Organizations can reduce exposure to transfer pricing penalties by ensuring adequate documentation and applying global transfer pricing policies consistently.

- In cases where penalties are imposed, businesses can seek penalty abatement by demonstrating reasonable cause and good faith, substantial compliance with transfer pricing rules, and leveraging effective representation from knowledgeable tax advisors.

~

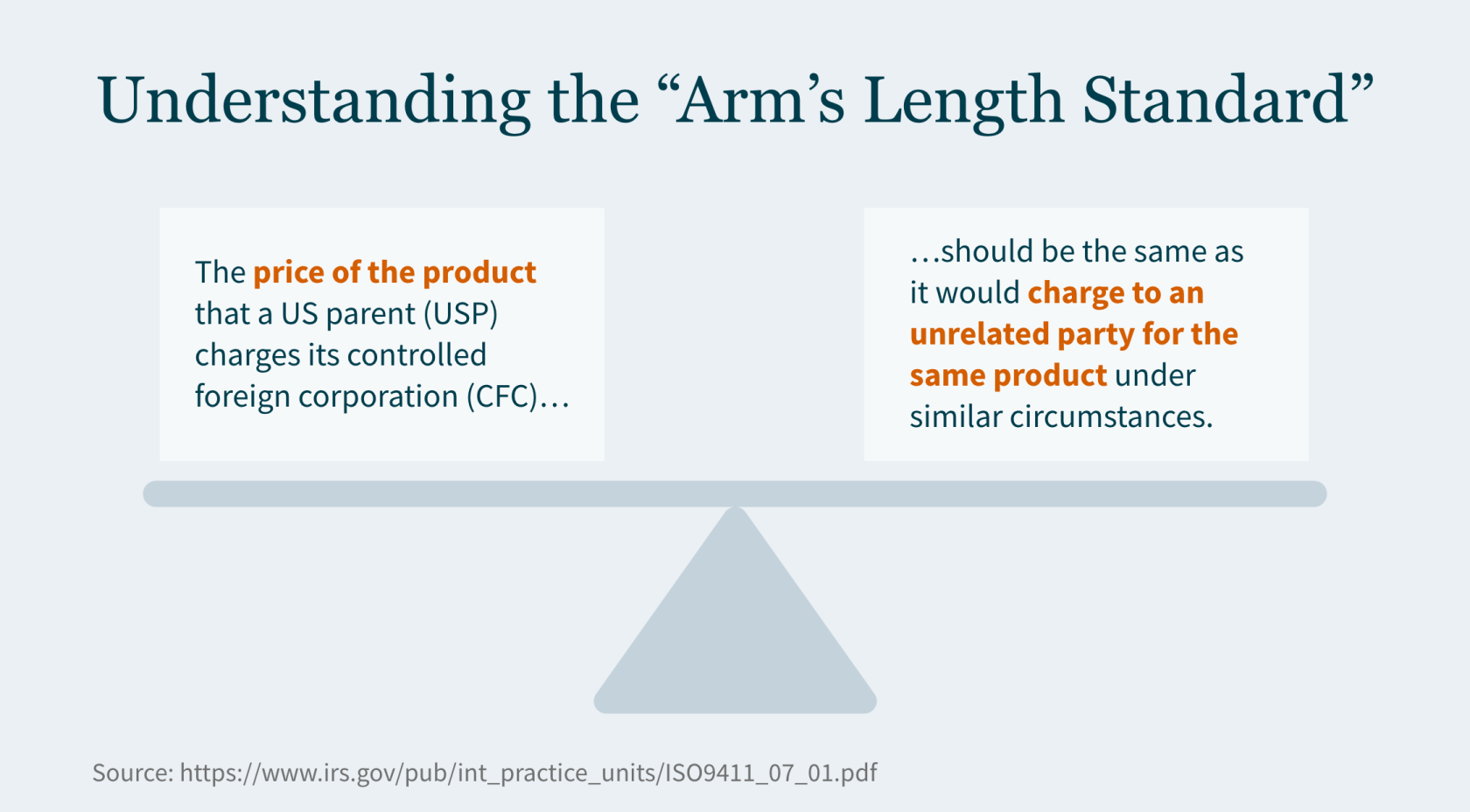

The Internal Revenue Service (IRS) implemented transfer pricing penalties to ensure the intercompany pricing reported on your income tax return is determined in a manner consistent with the arm’s length standard.

Until recently, penalty assessments were rare — not because improper transfer pricing between related parties was rare, but because IRS examiners tended to accept inadequate documentation. That leniency appears to be a thing of the past.

The IRS has indicated it will focus on applying Internal Revenue Code (IRC) Section 6662 penalties where proper documentation is lacking. This trend warrants serious attention if your company engages in cross-border transactions.

Imposing Transfer Pricing Penalties

The IRS can impose penalties when allocations under Section 482 result in substantial or gross increases in taxable income or where there are substantial or gross valuation misstatements concerning the transfer prices themselves.

These penalties can be severe, ranging from 20% to 40% of the tax underpayment, depending on the degree of non-compliance and the taxpayer’s disclosure of relevant information.

Historically, you could avoid these penalties by demonstrating you had reasonably used a transfer pricing method outlined in Section 482 or another method to more reliably determine transfer prices. Taxpayers must also provide contemporaneous documentation within 30 days of a request from the IRS.

The IRS’s Shift Toward Increased Penalty Assertion

The IRS Advisory Council’s 2018 Report noted that, although some transfer pricing documentation quality possibly fell short of the Section 6662 requirements, the IRS had not consistently asserted the penalty. Since then, the IRS has produced guidance addressing common flaws in transfer pricing documentation and best practices, and the agency is now expressing a renewed commitment to applying penalties more frequently and vigorously.

Holly Paz, commissioner of the IRS Large Business and International Division, spoke at several tax practitioner events in late 2022 — including the AICPA’s National Tax Conference, the American Bar Association Section of Taxation’s Philadelphia Tax Conference, and a Bloomberg Tax event. During these events, Paz noted the IRS has had success in litigating transfer pricing cases and is taking a closer look at economic substance and sham transactions — even in cases with transfer pricing documentation — to determine where it is appropriate to assert penalties.

Mitigating Exposure to Transfer Pricing Penalties

In 2020, the IRS published Transfer Pricing Documentation Best Practices Frequently Asked Questions (FAQs). These FAQs point to several features of proper documentation IRS agents look for when determining whether the agency should audit an organization’s transfer pricing methods.

Incorporating these features into your documentation may help reduce your risks:

- Sensitivity analysis – Assess the impact of removing a comparable company from the dataset and determine if such removal alters your position relative to the arm’s-length range. Evaluate how different profit-level indicators might change the results.

- Segmented financial data analysis – Examine if the segmented financial data accurately reflects the arm’s-length nature of the intercompany transaction. Detail the methodology used in constructing this data.

- Profit allocation in intercompany transactions – Analyze profit distribution among entities in the transaction. Ensure equitable economic outcomes for all parties, not just the tested party.

- Description of risks and related-party allocations – Describe associated risks in each intercompany transaction. Explain how profits and losses are allocated among related parties.

- Atypical business circumstances – Identify any unusual business conditions affecting the intercompany transaction. Discuss challenges in the economic analysis due to specific business results for the year.

To navigate this heightened scrutiny, taxpayers must take a proactive approach to document pricing transfer decisions. Steps you can take to avoid commonly seen inadequacies include:

- Providing a detailed description of your business and industry to help IRS agents understand operations and the larger marketplace in which you operate.

- Avoid using a checklist format. Instead, opt for a comprehensive analysis linking facts to the analysis. Base the analysis on well-supported facts, avoiding broad assumptions about the business.

- Ensure consistency in risk allocation with intercompany agreements. Align risk allocation with the comparable companies used in the economic analysis, and clearly explain any adjustments made to comparable companies for risk considerations.

- Prepare a best method selection analysis that justifies rejecting alternative methods for analyzing the intercompany transaction and provides a rationale for the chosen method.

- Clearly outline any adjustments to comparable data, such as working capital or location savings adjustments.

If you believe you have valuation misstatements or understated income tax in previously filed returns, it’s not too late to correct them. Filing a qualified amended return before the IRS contacts you about a transfer pricing audit is a defense against penalties. However, you must pay all taxes associated with the amended returns.

Seeking Penalty Abatement

In instances where penalties are assessed, it may be possible for taxpayers to seek abatement by demonstrating high-quality transfer pricing documentation. You may have a reasonable chance of having penalties abated if you:

- Demonstrate reasonable cause and good faith. Establish that the underpayment was due to reasonable cause, and you acted in good faith.

- Substantial compliance. Show that, despite any errors, you substantially followed the transfer pricing rules.

How We Can Help

The resurgence of transfer pricing penalties is an opportunity to reassess your transfer pricing strategies and compliance mechanisms.

For personalized guidance and assistance navigating these complexities, contact MGO today. Our team of professionals is equipped to help you mitigate risks, confirm compliance, and effectively manage any disputes with tax authorities. Act now to safeguard your business against the pitfalls of transfer pricing penalties.

]]>- State tax authorities are escalating audits of intercompany transactions, as transfer pricing crackdowns in several states are generating millions in tax revenue.

- These state initiatives indicate growing regulatory emphasis on transfer pricing, which may encourage more aggressive audits (especially if budgets tighten).

- Companies operating across state borders should take proactive steps, like conducting transfer pricing studies to validate policies and strengthen defenses before audits strike.

~

A recent Bloomberg article affirms state tax authorities are ramping up audits of intercompany transactions at multistate corporations. The report points to an increase in audits in three “separate-reporting” states following transfer pricing settlement initiatives as a beacon of audit activity to come across other states that take this approach.

While not ideal for multistate operators, this development may not come as a surprise to companies with international operations who have dealt with a myriad of cross-border tax issues in recent years. Close observers of state and local tax (SALT) developments have been predicting for many years the potential that states will be adopting similar positions with respect to transfer pricing. In a 2022 article focused on SALT transfer pricing enforcement, we highlighted several key indicators that more state transfer pricing audits could be on the horizon – including state budget deficits, a surge in auditor and consultant hirings, and renewed interest among states in collaborating on multistate audits.

With confirmation that state-driven transfer pricing audits are on the rise, it is imperative for corporations operating across state borders to assess your transfer pricing risks and fortify your documentation and audit defense strategies.

Surge of Transfer Pricing Audits in Separate-Reporting States

According to the Bloomberg Tax report, the recent spike in transfer pricing audit activity has predominantly affected Southeastern states categorized as separate-reporting states. Currently, there are 17 separate-reporting states in the United States. With the exception of a handful of states like Indiana, Pennsylvania, Iowa, and Delaware, most separate-reporting states are located in the Southeast region.

How separate-reporting states differ from other states in their taxation approach to corporations:

- In separate-reporting states, each corporation within an affiliated group is required to file its individual tax return. This treatment considers them as separate entities with independent income, recognizing intercompany transactions, and allowing for varying tax liabilities.

- In contrast, combined-reporting states require or allow affiliated corporations within a corporate group to file a single tax return, treating them as a unitary business with shared income, often eliminating intercompany transactions.

Notably, two Southeastern states, Louisiana and North Carolina, have recently concluded audit resolution programs that significantly boosted their state revenues. Louisiana’s program generated nearly $38 million, while North Carolina’s efforts resulted in more than $124 million. Meanwhile, New Jersey, a Mid-Atlantic state that abandoned separate reporting in favor of combined reporting in 2019, is in the midst of a transfer pricing resolution program that has already collected almost $30 million. The success of these programs in collecting tax revenue is likely to motivate other states to explore similar initiatives.

The success and subsequent expansion of these programs signify a growing emphasis on transfer pricing at the state tax authority level. State tax agencies are enhancing their knowledge and enforcement activities in this domain, giving auditors more confidence to adjust returns in transfer pricing disputes. This increasing competency may be viewed as a valuable tool by states – both those requiring separate and combined reporting – that are seeking ways to augment revenue streams.

Strengthen Your Transfer Pricing Defenses Before State Audits Strike

To preemptively safeguard your business from a state transfer pricing audit, a proactive approach to validating pricing policies is essential – and a comprehensive transfer pricing study is your primary defense.

Here are three key advantages of conducting a transfer pricing study:

- Document Your Transfer Pricing Policy: A transfer pricing study provides robust documentation that can counter inflated tax assessments by identifying key intercompany transactions, referencing benchmark data, and highlighting any deviations that necessitate policy adjustments. Even if your company has undertaken prior studies, annual updates are indispensable to align with evolving business landscapes and provide tax penalty protection.

- Mitigate Your Risk: Beyond reducing audit risks and potential liabilities, these studies also play a pivotal role in supporting major corporate events like mergers and acquisitions (M&A). By demonstrating pricing compliance, they ensure that domestic affiliates have robust documentation and effective cost allocation analysis, thus preventing over-taxation or under-taxation.

- Ensure Consistency: Minimize uncertainty by achieving uniform entity-specific compensation across state agencies and affiliated entities. Swift collaboration with advisors when audits arise enhances dispute resolution capabilities.

As states continue to gain confidence in challenging transfer pricing, multistate corporations must take proactive measures to ensure the resilience of their intercompany transactions under intensified scrutiny.

Get Ahead of the Game with a Transfer Pricing Study

If your company engages in substantial intercompany transactions across state lines, initiating a review of your current pricing policies, preparing your transfer pricing policies, and ensuring compliance with U.S. transfer pricing rules should be a top priority. Proactive measures can help you stay ahead of potential issues before state auditors come knocking. We have a robust transfer pricing team that works closely with our State and Local (SALT) Tax and Tax Controversy practices. Through a combined effort we can support you through every stage of managing a transfer pricing audit. Talk to our transfer pricing professionals today to find out how we can help you minimize your exposure to transfer pricing audits.

]]>- The Internal Revenue Service (IRS) instituted a moratorium on the processing of new Employee Retention Tax Credit (ERTC) claims due to an influx of fraudulent and exaggerated claims — primarily stemming from unscrupulous ERTC mills.

- As of July 31, 2023, the IRS Criminal Investigation division had initiated 252 investigations involving more than $2.8 billion in potentially fraudulent ERTC claims. Fifteen investigations have resulted in federal charges, with six of those resulting in convictions with an average sentence of 21 months.

- Taxpayers who are not certain of their eligibility should consult with a trusted tax professional for a second review and may want to avail themselves of the IRS’s new settlement and/or withdrawal programs.

The IRS recently took a drastic step to impede a wave of ineligible ERTC claims by halting the processing of new refund requests through at least December 31, 2023.

Ineligible ERTC claims have plagued the IRS since Congress enacted the credit in 2020. In fact, the IRS opened its 2023 “Dirty Dozen” list with warnings about common ERTC scams that taxpayers should be wary of. This prominently placed notice — as well as subsequent announcements from the IRS — alerted taxpayers to unscrupulous actors who have been advising employers to claim credits in excess of what they could legitimately qualify for while charging those employers hefty upfront fees or fees contingent on ERTC refunds.

In the wake of a flurry of IRS investigations that identified more than $2.8 billion potentially fraudulent claims, the halt on processing ERTC claims will allow the IRS to further focus their efforts on investigating and ultimately prosecuting fraudulent claims. In the following we’ll detail the impact of the IRS moratorium and provide guidance if you suspect you’ve been exposed to inaccurate or fraudulent ERTC claims.

Background on the ERTC

First established in 2020 by the Coronavirus Aid, Relief, and Economic Security (CARES) Act, the employee retention tax credit was critical — along with Paycheck Protection Program (PPP) — in giving businesses that struggled to navigate the pandemic’s challenges much needed resources to pay employees while the businesses were shut down or facing declining sales.

For most taxpayers, the ERTC was claimed on quarterly payroll tax returns encompassing the period March 13, 2020, through September 30, 2021 (i.e., first quarter of 2020 through the third quarter of 2021). For a small subset of businesses classified as “recovery startup businesses” (as defined below), the ERTC could also be claimed for the fourth quarter of 2021.

Despite the halt in processing by the IRS, eligible taxpayers are still able to claim the credit by filing amended quarterly payroll tax returns. Amended payroll tax returns for 2020 quarters are able to be processed by the IRS as long as they are filed on or before April 15, 2024, while amended payroll tax returns for 2021 quarters are able to be processed as long as they are filed on or before April 15, 2025.

The credit is calculated based on the “qualified wages” of employees. The maximum amount of payroll tax credit that an employer can claim per employee is $26,000.

Qualification Tests

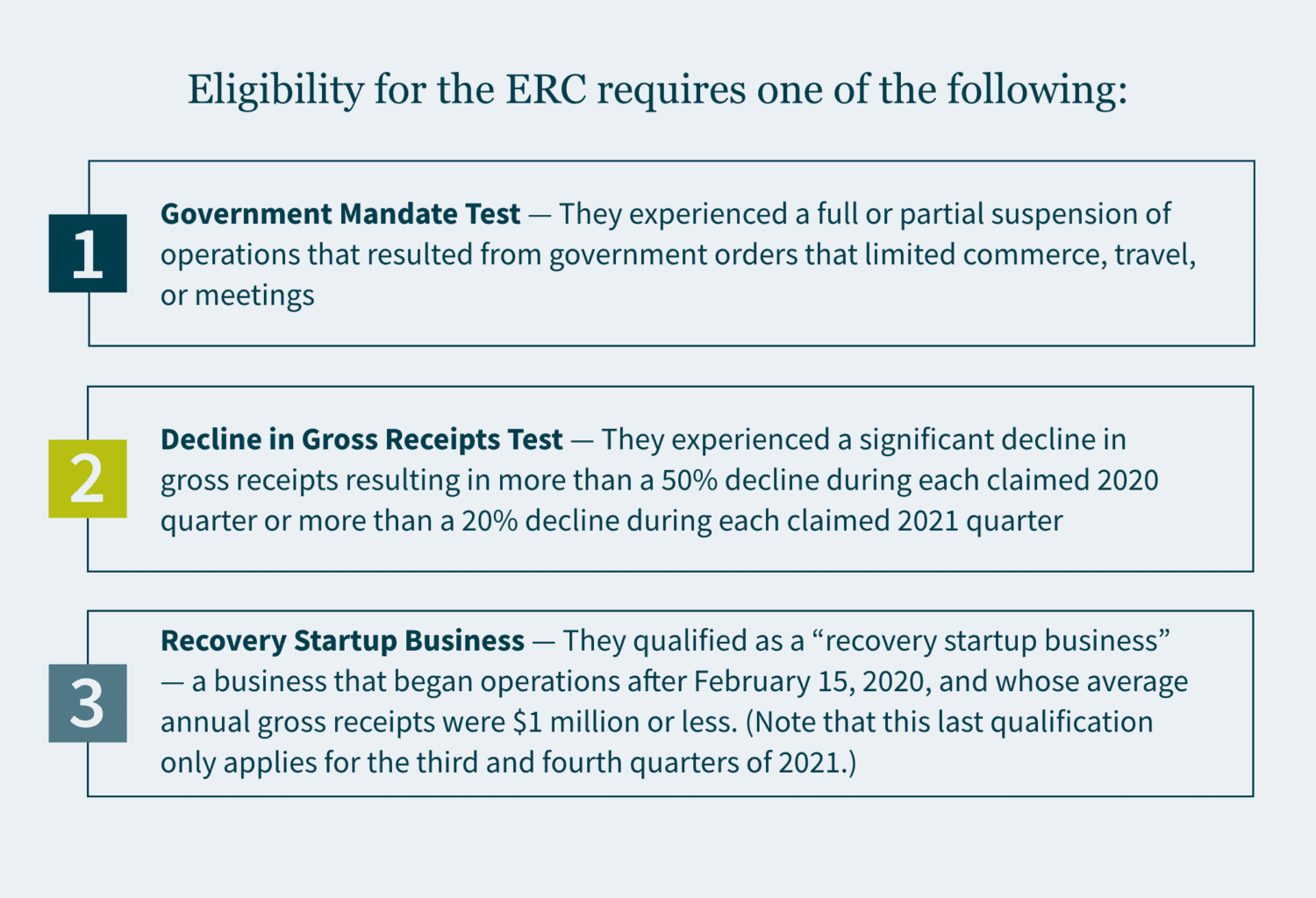

To be eligible for the ERTC, businesses must generally satisfy one of the following criteria for each of the quarters for which they are claiming the credit:

- Government Mandate Test — They experienced a full or partial suspension of operations that resulted from government orders that limited commerce, travel, or meetings.

- Decline in Gross Receipts Test — They experienced a significant decline in gross receipts resulting in more than a 50% decline during each claimed 2020 quarter or more than a 20% decline during each claimed 2021 quarter.

- Recovery Startup Business — They qualified as a “recovery startup business” — a business that began operations after February 15, 2020, and whose average annual gross receipts were $1 million or less. (Note that this last qualification only applies for the third and fourth quarters of 2021.)

The IRS Processing Moratorium

On September 14, 2023, the IRS announced that it would halt the processing of new ERTC claims through at least December 31, 2023. The IRS also stated that it plans to subject its queue of more than 600,000 existing ERTC claims to stricter compliance reviews, increasing the standard processing goal for those claims from 90 days to 180 days — with a potential for a much longer processing time for claims that require further review or audit.

This processing moratorium comes on the heels of a significant influx of claims – many of which the IRS believes are ineligible. The IRS stated that it has received more than 3.6 million ERTC claims over the life of the ERTC program, with about 15% of those claims being received in the 90-day period preceding the processing freeze. This amounts to roughly 50,000 claims still being received a week. To put this in perspective: the IRS has paid out about triple the amount that Congress had originally estimated for the program.

Additionally, as of July 31, 2023, the IRS Criminal Investigation division had initiated 252 investigations involving more than $2.8 billion in potentially fraudulent ERTC claims. Fifteen of the 252 investigations had resulted in federal charges, with six of those resulting in convictions. Four of the six convictions had reached the sentencing phase with an average sentence being 21 months.

The IRS intends on utilizing the moratorium to add more safeguards to the processing of ERTC claims, to protect businesses by decreasing the momentum of the pop-up ERTC mill industry, and to provide several solutions for taxpayers who submitted invalid claims. Those solutions include:

- A claim withdrawal program will be rolled out in Fall 2023 allowing businesses to withdraw ERTC claims that have not been processed or paid, even if those claims are under audit or awaiting audit.

- A claim settlement program rolling out in Fall 2023 that will allow businesses to repay ERTC claims, while also avoiding penalties and future compliance actions. (Note that fraudulent claims may still be subject to criminal referral.)

How to respond to IRS scrutiny of ERTC claims

Given the expected extra scrutiny that businesses can expect to face on their claims, businesses should review ERTC claims that they have made and/or intend to make where there are any doubts regarding the eligibility of those claims:

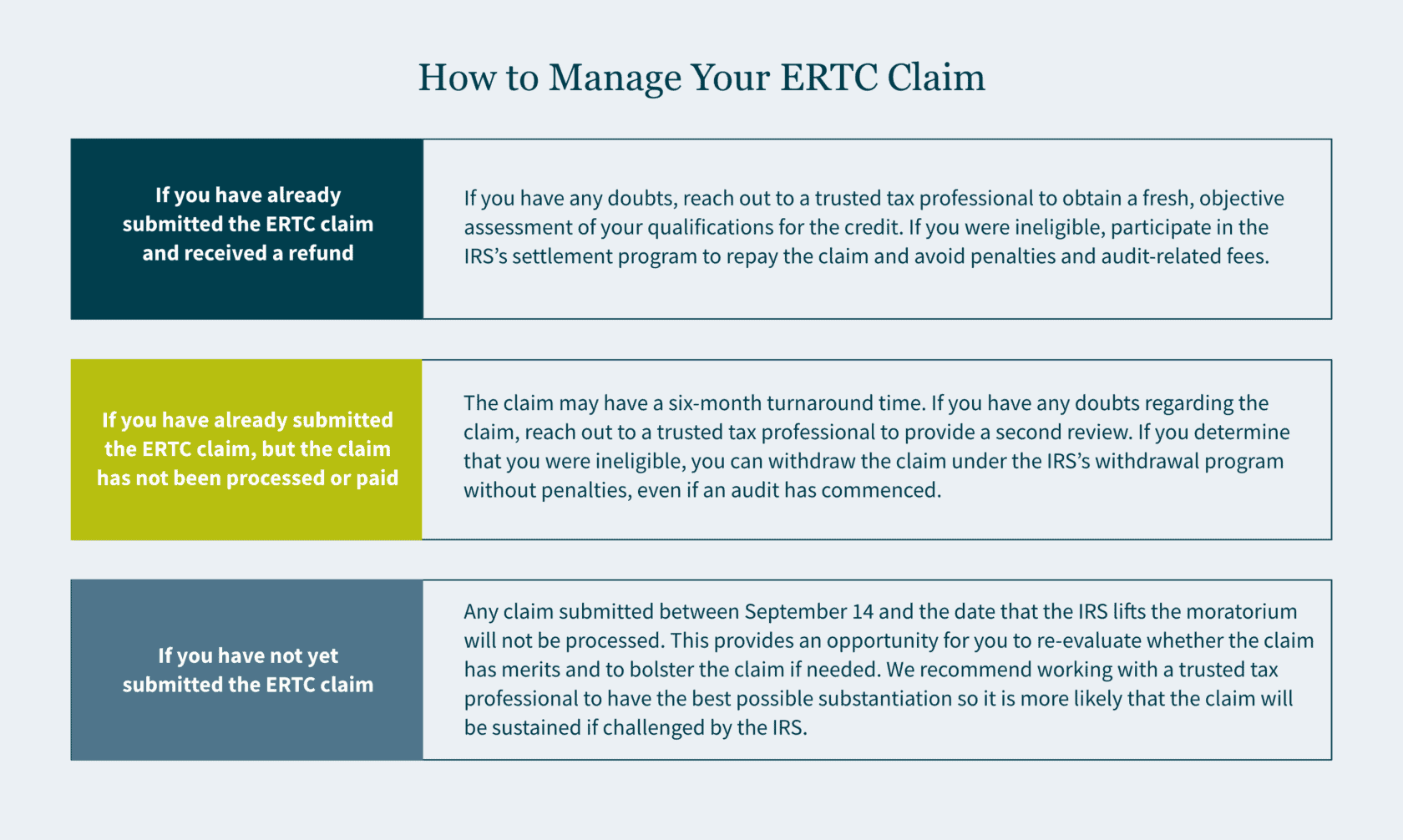

- If you have already submitted the ERTC claim and received a refund: If you have any doubts regarding your eligibility, we recommend reaching out to a trusted tax professional to obtain a fresh, objective assessment of your qualifications for the credit. If you determine that you were ineligible, you can participate in the IRS’s settlement program so that you can repay the claim, avoiding both penalties and audit-related fees.

- If you have already submitted the ERTC claim, but the claim has not been processed or paid: The claim will take longer to process than during the summer — increasing from a three-month turnaround time to a likely six-month turnaround time. If you have any doubts regarding the claim during this period, we recommend reaching out to a trusted tax professional to have a second review of the claim. If you determine that you were ineligible, you can withdraw the claim under the IRS’s withdrawal program without penalties, even if an audit has commenced.

- If you have not yet submitted the ERTC claim: Any claim submitted between September 14 and the date that the IRS lifts the moratorium – currently after December 31, 2023 – will not be processed. This should provide an opportunity for you to re-evaluate whether the claim has merits and to bolster the claim if needed. We recommend working with a trusted tax professional to have the best possible substantiation for your claim so that it is more likely that the claim will be sustained if challenged by the IRS.

How MGO can help

MGO’s ERTC Second Look program is geared towards the types of objective, trustworthy reviews that would benefit you during this time of heightened ERTC claim scrutiny. Our experienced Credits & Incentives team can identify audit red flags, areas that need more substantiation, miscalculations, and incomplete filings. In addition, our Tax Controversy team — in tandem with our Credits & Incentives team — can defend you if any of your ERTC claims are challenged by the IRS, with the ability to represent you during audit, appeals, and tax court. Contact us to learn more.

]]>The tax relief postpones tax filing and payment deadlines occurring between January 8, 2023, and May 15, 2023, to a new due date of October 15, 2023.

Some of the filings and payments postponed include:

- Individual income tax returns due on April 18

- Business tax returns normally due on March 15 and April 18

- 2022 contributions to IRAs and health savings accounts

- Quarterly estimated tax payments normally due January 17 and April 18

- Quarterly payroll and excise tax returns normally due on January 31 and April 30

The current list of counties that qualify for this relief can be found here.

If you qualify for this postponement, you generally do not need to contact the IRS or FTB to obtain relief. Relief is automatically granted for affected taxpayers who have an address of record located in one of the designated counties. However, if you still receive a late filing or late payment notice and the notice shows the original or extended filing, payment, or deposit due date falling within the postponement period, you should call the number on the notice to have the penalty abated.

If you have questions or need assistance, contact MGO’s experienced State and Local Tax team.

]]>- The Inflation Reduction Act of 2022 includes $80B in funding for the Internal Revenue Service.

- Over half of the funding will be set aside for IRS enforcement so the agency can hire more staff to conduct more audits, hoping to target those who do not pay their taxes.

- This will most likely subject those taxpayers with complex filings to additional scrutiny.

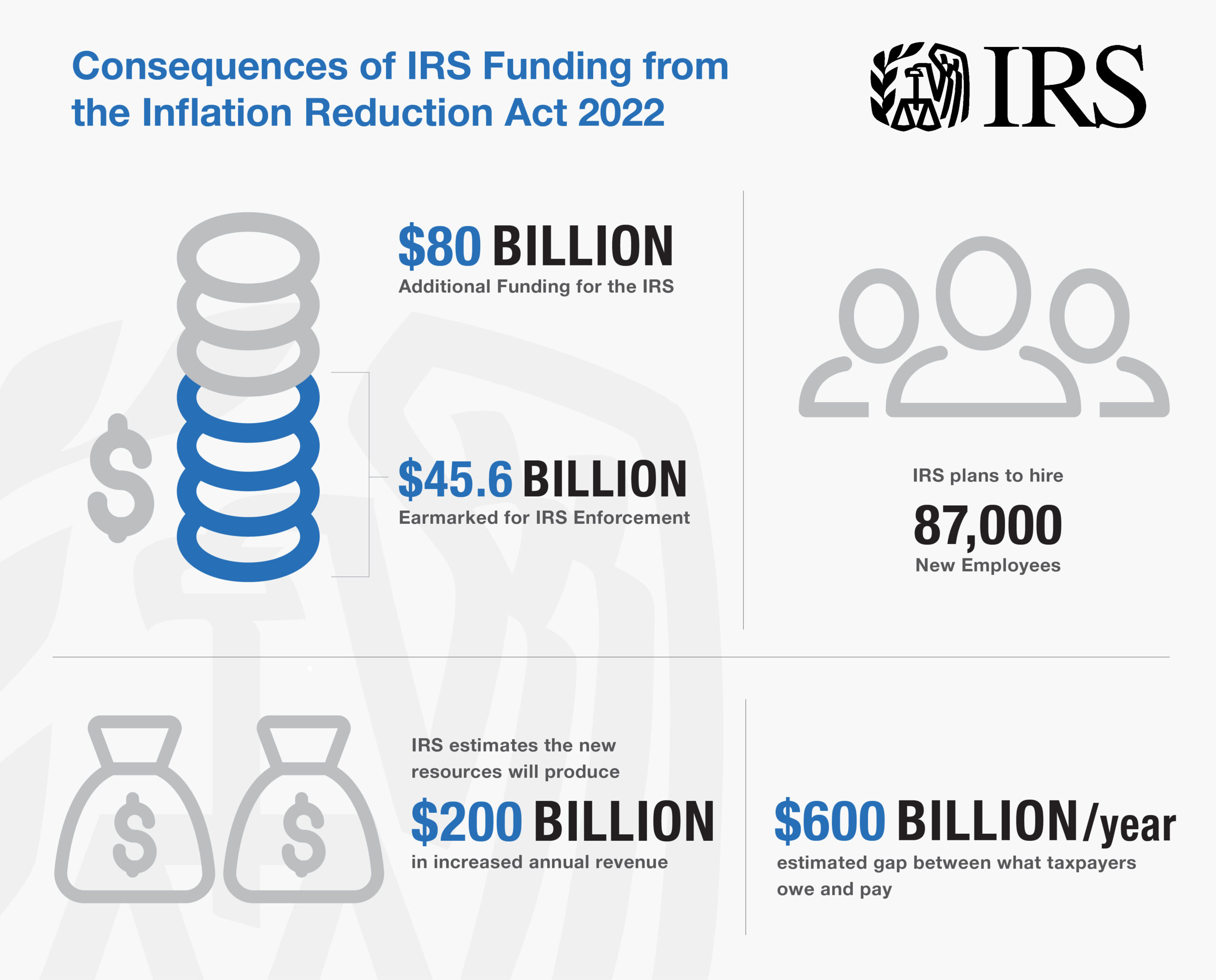

The Inflation Reduction Act of 2022 was recently signed into law with an eye-opening provision: the inclusion of nearly $80 billion in additional funding for the Internal Revenue Service (IRS). $45.6 billion of that is earmarked for IRS enforcement, which will be used to help the underfunded agency hire additional staff and conduct future audits in the hopes of collecting unpaid taxes.

Many publications cite the IRS plans to hire up to 87,000 new employees, though the actual number will be released in the coming months. These new hires will fill positions ranging from auditors to customer service representatives to IT specialists. The IRS has been plagued by more than a decade of budget cuts, which has limited its ability to modernize its old technology and staff appropriately. Since 2010, the agency’s enforcement staff has declined by 30%. The funding appropriate in the Inflation Reduction Act hopes to reverse this trend and bring in an estimated $203 billion in increased revenue.

The MGO Tax Controversy team breaks down what you need to know about this big change that could increase your risk of an audit.

How will the increase in IRS staff affect taxpayers?

Critics of the increase in IRS funding have claimed that the new resources will be used to target low to middle-income Americans and small businesses, burdening them with more audits and examinations. The Treasury Department refutes these claims reiterating they plan to focus primarily on large corporations and the wealthy — those more likely to evade paying their taxes — to close the tax gap, or the difference between what taxpayers pay in taxes and what they actually owe – an estimated to be $600 billion per year.

The IRS hopes the investment in funding will bring in around $203.7 billion in revenue because between 2015 and 2019, IRS audits declined significantly — 75% for Americans making $1 million or more and 33% for filers with low to moderate incomes. Lower-income Americans are mostly wage earners, so their audits are less complex and can be automated. However, more complex filers, notably large corporations and high-net-worth individuals and families – require the hands-on engagement of IRS agents and are most likely to experience increased levels of scrutiny from the new hires.

Ultimately, the average taxpayer should have an improved tax filing experience. New staff will be on hand to answer questions by phone, technology systems will be improved and modernized, and the backlog of unprocessed returns should diminish.

What is the timeline for implementing these changes?

While there is no set timeline, it is likely the way IRS audits work will change with the increase in funding. Currently, software is used to rank each tax return with a numeric score, and higher scores trigger an audit. Other mechanisms the IRS uses to determine candidates for audits include enforcement initiatives referred to as “campaigns” based on various criteria. The new funding will take time to phase in, and so will the hiring and training of new workers. It is expected new auditors will complete a six-month training program, starting small with cases involving a few hundred thousand dollars instead of tens of millions. Forbes performed some creative math to conclude while the funding will increase IRS audits, it is not likely to occur for the next few years.

How can I avoid future audits?

The best way to avoid an audit remains simple: pay your taxes on time and in compliance with tax laws. Simple accounting and documentation best practices are your best friend. If you feel you are at risk for a potential audit, you’ll want to get a head start now by ensuring your records are accurate and have been updated and maintained. Save your receipts and include every detail you can in your bookkeeping logs. If you do get audited in the coming wave, you’ll be glad you have all of this information organized and on-hand.

Our perspective on the increase in IRS staffing

The IRS has long been criticized because of their inability to provide taxpayers with the level and quality of service they deserve. The increase in funding as part of the Inflation Reduction Act should help. On the other hand, the number of tax audits is likely to increase, and you will want to be ready.

MGO’s dedicated Tax Controversy team can help by providing a holistic look at your tax filings as well as provide guidance for conflict resolution. From prevention to resolution, we guide you every step of the way.

If you’re an operator or investor in the cannabis industry, our Tax Practice recently published the Cannabis IRS Audit Survival Guide, which details everything you need to do to prepare for and navigate a tax audit. You can download the Guide for free here.

About the author

T. Renee Parker is a tax partner and the National Tax Controversy Practice Leader at MGO. With more than 15 years of tax controversy experience, she is a member of the IRS Tax Advocacy Panel and is well-versed in all areas of tax controversy. These include but are not limited to U.S. federal, state, and local tax audits; sales and use/payroll tax audits; international tax compliance related audits; negotiation and settlements with tax authorities; and corresponding and negotiation with tax authorities. Contact Renee at RParker@MGOCPA.com.

]]>- Increasing Internal Revenue Service (IRS) budget

- Implementing a corporate tax minimum

- Instituting and increasing tax credits focused on investing in green technologies

Notable items that were not addressed in the IRA include removing the $10,000 SALT cap and mandatory capitalization of research and development (R&D) expenses, both provisions of the Tax Cuts and Jobs Act of 2017.

The bill is over 300 pages in length with a number of wide-ranging components. In the following summary we’ll provide the key points that will be affecting taxpayers in the coming years.

Additional funding to the IRS for tax enforcement

One of the most talked-about provisions involves increased funding for the IRS.

Key details:

- Approximately $80 billion in funding over the next 10 years for tax services, operations support, business system modernization, and enforcement

- Enforcement – $46 billion

- Operations support – $25 billion

- Business systems modernization – $5 billion

- Taxpayer services – $3 billion

- An estimated $124 to $200 billion will be generated from enforcement and compliance efforts

- Enforcement is focused on taxpayers – both corporate and non-corporate – with income greater than $400,000

Extension of the business loss limitation of noncorporate taxpayers

The IRA extends the excess business loss limitation for noncorporate taxpayers.

Key details:

- Two year extension on IRC Sec. 461(l) until December 31, 2028

- IRC Sec. 461(l) limits noncorporate taxpayers from deducting business losses above thresholds that are annually indexed for inflation

- These limits are $540,000 for married filing jointly and $270,000 for single and married filing single for the 2022 tax year

- Suspended amounts are converted to net operating losses and may be able to be used in subsequent years

Excise tax on repurchases of corporate stock

The IRA includes a 1% excise tax on stock repurchases by domestic public companies listed on an established securities market. The tax applies to repurchases executed after December 31st, 2022.

Key details:

- 1% excise tax on the full market value (FMV) of stock repurchased by publicly traded US corporations

- Will impact redemptions and certain acquisitions and repurchases of publicly traded foreign corporation stock

- Not an income tax for purposes of ASC 740

- Includes special rules for “applicable foreign corporations” and “surrogate foreign corporations”

- Notable exceptions:

- Stock is contributed to employer sponsored retirement plan

- Stock repurchase is part of a corporate reorganization

- Total value of stock repurchased during the taxable year does not exceed $1 million

- Repurchase by securities dealer in ordinary course of business

- If the repurchase qualifies as a dividend

- If the repurchase is by a regulated investment company (RIC) or a real estate investment trust (REIT)

15% corporate alternative minimum tax

The IRA reinstates the corporate alternative minimum tax (AMT) for large corporations, which had been previously eliminated by the Trump Administration’s Tax Cuts and Jobs Act.

Two key elements to note is that this revised AMT only impacts corporations with annual profits exceeding $1 billion, and includes carve-outs for certain manufacturers and subsidiaries of private equity firms.

Key details:

- 15% tax on adjusted financial statement income (i.e., this would be a book minimum tax)

- Affects tax years beginning after December 31, 2022

- Applies to corporations with profits over $1 billion based off adjusted financial income

- For US corporations with foreign parents, it would apply to income earned in the US of $100 million or more of average annual earnings in three prior years and where the overall international financial reporting group has income of $1 billion or more

- Treatment of split offs remains uncertain. Even though these are tax-free reorganizations for tax purposes, gain is recorded for financial accounting purposes

- Joint Committee on Taxation expects that this new tax would apply to only about 150 corporate taxpayers, approximately equal to 30% of the Fortune 500

Tax credit additions and modifications

A significant number of provisions add or enhance credits and incentives that pertain to domestic research and green energy initiatives. Noteworthy changes include:

Increased small business payroll tax credits for research activities:

- Qualified payroll tax credit for increasing research activities raised from $250,000 to $500,000

- First $250,000 will be applied against the FICA payroll tax liability. Second $250,000 will be applied against the employer portion of Medicare payroll tax.

- Applies for taxable years beginning after December 31, 2022

- Limited to tax imposed for calendar quarter with unused amounts being carried forward

- Qualifying small businesses are required to have less than $5 million in gross receipts in current year and no gross receipts prior to the 5 year period ending with the current year

Green initiative tax credits and incentives:

- Credits for purchasing new and previously-owned clean vehicles

- Extension of IRC Sec. 45L – New Energy Efficient Home Credit – extended to qualified new energy efficient homes acquired before January 1, 2033. Increase value of available credit for single-family homes to $2,500 and modified the credit available for multi-family homes.

- Extension, increase, and modifications to IRC Sec. 25C nonbusiness energy property credit

- Extension and modification of IRC Sec. 25D residential clean energy credit

- IRC Sec. 48 energy credit for businesses and investors

- Expansion of qualifying property, extension of credit including phasedown and phaseout rules, and introduction of incentives

- Credit for producing energy from renewable sources (IRC Sec. 45)

- Retroactive for facilities placed in service after December 31, 2021

- Extends beginning of construction deadline to projects beginning construction before January 1, 2025 including solar energy facilities

- Increased energy credit for solar and wind facilities in certain low-income communities

- New credit for clean hydrogen production

- New credit for zero-emission nuclear power

- Extension of incentives for biodiesel, renewal diesel, and alternative fuels

- Extension of biofuel producer credit

- New income and excise tax credits allowed for sustainable aviation fuel

- Modification of IRC Sec. 179D – Energy Efficient Commercial Buildings Deductions

- Modification of building qualifications

- Deduction increased from $1.88 per square foot to up to $5 per qualified square foot

- Changes in depreciation for certain green energy properties

Final thoughts

The Inflation Reduction Act should have wide-ranging impacts on taxpayers, especially large corporations and high-net-worth individuals. In the coming weeks our tax leaders will dive into the specifics of the legislation, outline immediate and long-term impacts, and provide tax-planning strategies and considerations.

]]>Specific scams that mask as abusive or fraudulent tax avoidance strategies to be aware of include concealing assets in offshore accounts and improper reporting of digital assets, manipulation of high-income taxpayers to file their tax returns, abusive syndicated conservation easements, and abusive micro-captive insurance arrangements. Read more to round out the annual list for the 2022 filing season.

Tips for taxpayers on emerging scams

To avoid compromising yourself with these “too good to be true” schemes, taxpayers should stay wary, as these scams adopt a wide range of communication methods, including:

- Emails

- Phone calls

- Social media posts

- Targeted online advertisements

You must also consider each source before putting any of these arrangements on your tax returns — because ultimately, you are the one responsible for what is on the return, not the promoter who reached out to you and made a promise they failed to uphold. To mitigate risk, an anxious taxpayer should turn to trustworthy tax professionals to assist with their returns.

Read on to learn about these Dirty Dozen scams targeted primarily to high-net-worth individuals who may be trying to knowingly — or unknowingly — avoid filing.

Scam #9: Concealing Assets in Offshore Accounts and the Improper Reporting of Digital Assets

We hear Switzerland is beautiful this time of year … and so do some high-net-worth individuals looking to conceal their assets in offshore accounts (and yes, that does include cryptocurrency and other digital assets). As more taxpayers look to complex international tax avoidance schemes, the IRS is more determined than ever to “protect the integrity of the U.S. tax system” by enforcing tax responsibilities.

Whether it entails offshore banks, brokerage accounts, nominee entities, employee leasing schemes, foreign trusts, structured transactions, or private annuities, all are designed to hide the true owner of an account — which is illegal, considering U.S. taxpayers are taxed on all the income they make, not just what they keep in the country. But scammers know you may not want to give up some of your hard-earned assets to Uncle Sam. So, what do they do? They sell you a convincing story: you can easily evade the government and hide your assets through digital asset holdings; they claim these are “undetectable by tax authorities.” The catch? They are definitely detectable. By believing these fraudsters, you run the risk of being criminally charged or penalized, so in the end, it is better to report your assets — yes, all of them — when you file.

Scam #10: High-Income Individuals Who Don’t File Tax Returns

Believe it or not, there are some taxpayers who choose to just … not file a tax return. And believe it or not, there are scamming professionals out there aiming to convince you this is a good idea. The IRS takes this seriously. If you are considering this option, remember the Failure to File Penalty is higher than the Failure to Pay Penalty, meaning you are better off filing an accurate, timely return (and setting up a payment plan, if you are concerned about that) rather than not filing and hoping you get out of paying whatever taxes you owe.

Scam #11: Abusive Syndicated Conservation Easements

In this scam, dishonest promoters manipulate a part of the tax law that allows for conservation easements by inflating appraisals of underdeveloped land (i.e., the guise of a real estate investment) and engaging in bogus partnerships without a business purpose. These “deals” rarely help you out; instead, they benefit the promoters, who charge high fees, and clog the tax system with fraudulent tax deductions. (In the last five years, the IRS determined billions of dollars of deductions were wrongly claimed!) And if you are caught — which, you should expect to be, because the IRS takes a microscope to every single one of these “deals” — you can expect large fines and potential time in court.

Scam #12: Abusive Micro-Captive Insurance Arrangements

A high priority for the IRS, this scam sees professionals like accountants and wealth planners convince entity owners to pay for what they believe to be insurance coverage against unlikely events, events that are already being covered, or disingenuous business needs. Complete with sky-high premiums, the abusive structure does the opposite of protecting your organization’s tax safety — it opens you up to more risk as a ”micro-captive” to these “professionals” taking advantage of you. Be on the lookout for an offshore version of this too.

Consequences of falling for a Dirty Dozen scheme

It is important for taxpayers who have already taken part in transactions like these — or those who are thinking about doing so — to consult a tax professional before claiming any tax benefits they think they are owed.

Those taxpayers who have already claimed the purported tax benefits of one of these four “Dirty Dozen” arrangements on a tax return should file an amended return and go to an independent professional for guidance. If necessary, the IRS will examine the tax benefits from transactions like the ones depicted in the list and inflict penalties related to accuracy ranging from 20% to 40%, or a civil fraud penalty of 75% on any taxpayer who underpaid.

Our perspective on the latest batch of “Dirty Dozen” scams

This is not, of course, an exhaustive list of every scam the IRS has its eye on this year. But it does include some of the more common trends. The best advice we can give? If something looks too good to be true … it probably is. Consult your tax professional for guidance and know that it is in your best interest to stay aware of these nefarious arrangements, so you do not fall susceptible to additional penalties.

And remember, you cannot hide income from the IRS!

MGO’s Tax team brings more than 30 years of experience and is well versed in reviewing your return for compliance. We also stay up to date on the risks, pitfalls, and warnings issued by the IRS so you don’t have to. If you think you have been involved in or are in the process of being involved in one of the Dirty Dozen scams, we can help. Contact us today.

]]>Tips for taxpayers on emerging scams

To avoid compromising yourself with these “too good to be true” schemes, taxpayers should stay wary, as these scams adopt a wide range of communication methods, including:

- Emails

- Phone calls

- Social media posts

- Targeted online advertisements

You must also consider each source before putting any of these arrangements on your tax returns — because ultimately, you are the one responsible for what is on the return, not the promoter who reached out to you and made a promise they failed to uphold. To mitigate risk, an anxious taxpayer should turn to trustworthy tax professionals to assist with their returns.

Read on to learn which scams are next on the Dirty Dozen list.

Scam #6: Offer in Compromise “Mills”

This scam, known as an Offer in Consequence (OIC) mill, targets taxpayers who struggle to pay their taxes and may face debt as a consequence for their delinquency or noncompliance. It is commonly seen right after the filing season concludes as these taxpayers stress about what they might owe. What is the OIC? It is an agreement between you and the IRS that resolves your tax debt, and these mills claim to be able to settle your tax debt on the cheap. But the reality is, only the IRS has the authority to settle or compromise your federal tax liabilities, and it is based on certain circumstances. Utilizing local advertising, the mills boast they can get you a great deal, even if they know you do not actually qualify — and if they do get you a “deal,” it is the same deal you would have received if you had worked directly with the IRS (and if you had gone to the IRS first, you would not have paid potentially thousands in fees to these fraudsters).

Before you trust an OIC mill or invest your time in submitting an offer yourself, check out the IRS’s Offer in Compromise Pre-Qualifier Tool to determine your eligibility. The site also has a host of resources to utilize when it comes to tackling these offers — the right way.

Other dishonest tax preparation tactics include:

- Ghost preparers who do not sign the tax returns they prepare for you,

- Inflated refund promises, and

- Preparers who:

- Only take cash,

- Do not provide you with a receipt,

- Fabricate income so you qualify for certain tax credits,

- Direct your refunds into their accounts, or

- Claim fake deductions so the refund is bigger (which they, in turn, get a cut of).

Scam #7: Suspicious communications in all forms, including text, email, and by phone

These scams strive to make you feel fearful or surprised so scammers can trick you into divulging your personal information, which they can then steal to file fake tax returns and access financial accounts. Whether it entails a phone call, a text message, or an email, these methods have been around for years, and it is no question why they are still in circulation today: they work. And while they evolve and change depending on what is going on in the country (many currently reference stimulus checks or the COVID-19 pandemic), these are the basic methods.

Text message scams:

sent to smartphones and sometimes include website links that can seem reputable — but they are not. Remember, the IRS will not send you text messages regarding personal tax issues, and they definitely do not reach out via social media. If you receive a text that claims to be from the IRS, you can report it by taking a screenshot of the message and emailing it to phishing@irs.gov along with the date, time, and time zone you received it and your phone number. And, it may go without saying, but we are going to say it anyway: do not open the attachments or links in these messages!

Email scams:

work similarly to text message scams, but they appear in your inbox instead of your messages. Just like texts, the IRS will not contact you by email to request personal information — they use regular mail. You can report suspicious emails to the IRS at the email address above.

Phone scams:

have several different pre-recorded voicemail scripts, but nearly all are threatening and include language meant to scare you into answering with your personal information. Threats include issuing a warrant for your arrest if you ignore them, getting deported, or revoking your license. Be wary of any and all phone numbers you do not recognize; these scammers can fake caller ID numbers, so you are unable to check who is calling.

Here are some things the IRS will not do over the phone:

- Ask for your credit or debit card information,

- Make “right now” demands for you to pay what you owe,

- Threaten to call the authorities if you do not pay, and

- Demand you pay immediately using methods like a gift card or wire transfer.

Scam #8: Spear phishing attacks to steal identities

Spear phishing deploys an email scam aimed at stealing a professional firm’s software credentials so the scammers can steal data and identities to file tax returns for refunds, which they will then pocket. The most recent phishing email convincingly utilizes the IRS logo with a subject line telling you action is required because your account has been put on hold. If you click on the link within the body of the email, malware could be downloaded to your computer, or you will be directed to a site with popular tax software preparation providers’ logos. Once you select a logo, you will be asked to input your credentials (which will be stolen and most likely used to file fraudulent tax returns).

The IRS labels spear phishing as a very serious problem because it can be “tailored to attack and steal the computer system credentials of any small business with a client data base,” including tax professionals’ firms. Their suggestion? Never let your guard down when it comes to your cybersecurity. Any client-based enterprise can be targeted.

Consequences of falling for a Dirty Dozen scheme

It is important for taxpayers who have already taken part in transactions like these — or those who are thinking about doing so — to consult tax professionals before claiming any tax benefits they think they are owed.

Taxpayers who have already claimed the purported tax benefits of one of these four “Dirty Dozen” arrangements on a tax return should file an amended return and go to an independent professional for guidance. If necessary, the IRS will examine the tax benefits from transactions like the ones depicted in the list and inflict penalties related to accuracy ranging from 20% to 40%, or a civil fraud penalty of 75% on any taxpayer who underpaid.

Our perspective on the latest batch of “Dirty Dozen” scams

This is not, of course, an exhaustive list of every scam the IRS has its eye on this year. But it does include some of the more common trends. The best advice we can give? If something looks too good to be true … it probably is. Consult your tax professional for guidance and know that it is in your best interest to stay aware of these nefarious arrangements, so you do not fall susceptible to additional penalties.

Stay tuned for more deep dives into the IRS’s Dirty Dozen list.

And remember: if you owe taxes, the IRS will almost always mail you a bill first!

MGO’s Tax team brings more than 30 years of experience and is well versed in reviewing your return for compliance. We also stay up to date on the risks, pitfalls, and warnings issued by the IRS so you don’t have to. If you think you have been involved in or are in the process of being involved in one of the Dirty Dozen scams, we can help. Contact us today.

We recently released an article detailing the red flags to look out when dealing with tax credits and incentives providers. If you think you could be at risk for future IRS issues, there is much you can do now to take a proactive approach and mitigate future negative impact. In the following, we break down steps you can take now to better understand and manage your exposure.

An overview of tax credits and incentives

Designed to encourage investment and development, job creation, growth, and certain business activities, tax credits and incentives provide an opportunity to reduce the amount of tax owed for performing certain activities. Credits and incentives are categorically different than tax deductions, which reduce the amount of taxable income.

These incentives often target desirable industries or activities like research and development, job creation for at-risk populations, and expanded growth in underdeveloped areas. When leveraged correctly, credits and incentives can be a powerful tool to funnel back resources into your organization to fuel activities you are already doing. Even more enticing, these credits can often apply retroactively if you determine you qualify for certain credits or incentives after the fact.

There are three basic types of tax credits: nonrefundable, refundable, and partially refundable. A few of the different types of tax credits pertaining to businesses in different classifications, industries, or activities performed include R&D tax credits, the employee retention tax credits, IRC Section 179D, and the work opportunity tax credit. To learn more about their eligibility rules, visit our previous article.

Understanding the risk of IRS tax audits

There is a three-year statute of limitations from the due date of the tax return or the filing date (whatever is later) for the IRS to assess your filings. That means if you think you may be exposed but escaped the IRS’ notice, you could still receive an audit notice for previous years’ returns. And if you do get audited, and the IRS determines you owe back taxes, you will get charged penalties and interest dating back to the infraction itself.

This is even more risky when considering the IRS’s extreme backlog. These IRS tax audits can sometimes take years to complete and if your credit and incentive calculations are the topic of interest, you’ll need to halt any future credit analysis until the situation is resolved. Meanwhile, you’ll be devoting crucial resources, time, and effort working with the IRS for something that yields no financial value and distracts from more conducive business activities.

Reasons to get a head-start and address issues now

Even though there is no guarantee you will get audited, you are still taking a risk if you do not address potential tax credit and incentive exposures in your organization. It may seem easy to “roll the dice” and hope the issue will remain uncovered, but it could come at a cost — especially if you are planning to make some big moves, like engaging in transaction of your business (M&A), going public, or embarking on another major transaction.

During the due diligence period of these transactions, it is almost certain any uncovered tax issues will emerge. You will likely not recover the value of these credits or remain on the hook for potential liability. Even worse, the exposure of these issues reflects negatively on your accounting and control system, potentially lowering the purchase value of your organization or undermining whatever deal you had in place prior to the due diligence. Often your transaction partners will start to question your organization’s trustworthiness, and reputation … due to something that may be no fault of your own.

So, you’ve been exposed … but haven’t received an IRS audit notice

Here is the deal: you know for certain you have been exposed, but you have not been notified by the IRS yet. You probably have a lot of questions — will you get an audit notice? Have you escaped unscathed? Do you need to address the issues preemptively, just in case? It may be overwhelming to decide how to proceed once you realize the exposure.

We suggest working with a qualified CPA firm to review your tax filings. A full-service accounting firm will review your organization holistically at a minimum rate, uncover any exposures, and deliver valuable peace of mind. If the firm does find issues, you have two options:

- Update your credit and incentive filings moving forward.

- While this will likely decrease the amount you can deduct, it exemplifies transparency.

- Issue a Voluntary Disclosure (VA) if the exposure is significant and you do not have a lot of time to fix the issue.

- Essentially, you are volunteering to correct your mistakes by recalculating the credits claimed and paying back the difference.

- While this may sting a little, the IRS looks favorably upon organizations who are proactive to fix the issue by filing a VA and they are likely to waive any penalties or interest you would have had to pay.

You’ve received an IRS audit notice. Now what?

Well, it happened. You received an audit note from the IRS. Before you panic, here is what you need to do:

- Start preparing your documentation right away. The sooner you have your ducks in a row, the sooner you are prepared to handle the audit.

- Check the contract you signed with your original provider and verify if they provide controversy support services for situations like these.

- If they do, reexamine the quality of their work. Do they have any of the red flags mentioned in this article? Could something they have done have caused the audit?

- Consider engaging a qualified CPA firm as your new provider to handle the subsequent controversy support. Someone you trust can get you ready for any available credits and incentives moving forward, too.

- If you used a provider that displays any red flags, you could have some leverage for a reasonable cause defense. Because the “professional” firm handled it for you and made a mistake, you could utilize a first-time penalty abatement, which means you can get relief from a penalty if you:

- Did not previously have to file a return or if you do not have any penalties for the three years before the tax year you received a penalty;

- Filed all currently required returns or an extension of time to file;

and - Paid or have arranged to pay any tax due.

- Verify your contract with the original provider to determine if you have any recourse to seek compensation from them. If the IRS does issue any penalties, you will want to ensure you do not have to pay.

Standalone firms vs. full-service accounting firms

Let’s say you haven’t received an IRS notice, and you do not think you are in danger of receiving one. How can you ensure you will not in the future? It comes down to choosing a firm to help you maximize the potential of these tax credits and incentives.

The bottom line: it is imperative you work with a certified public accounting (CPA) firm instead of a standalone firm. Because standalone firms often use lower-cost, less-experienced recent graduates who are not certified public accountants, there is a distinct lack of knowledge and background in the accounting fundamentals, causing you to be misled by those unequipped to help with complex tax matters. You also run the risk of being oversold benefits by aggressive firms that not only exaggerate the amount you are receiving from the tax credits and incentives, but also behave in a way that attracts IRS attention and jeopardizes your firm.

A full-service accounting firm, on the other hand, knows how to look at an organization holistically — and it has many more capabilities and professionals with experience. It looks at things through various lenses and can advise how certain positions will impact current and future tax positions. Full-service firms also likely have an in-house controversy team that has handled hundreds of audits successfully—so you will be in good hands.

Our perspective

Tax credits and incentives provide plenty of benefits you do not want to miss out on, and their often-complex application and qualification processes are reason enough to hire a professional accountant to help you maximize your returns. Unfortunately, we often see organizations placing their trust in the wrong providers and they end up suffering the consequences of an IRS audit. For many, it is simply easier and safer to cut off the relationship with the initial provider and start fresh with a professional firm you know you can trust.

At MGO, our dedicated Tax Credits and Incentives team brings more than 30 years of experience fixing these types of issues and working with the IRS to limit the damage. We provide cleanup in the event you are being audited by the IRS (or could be audited in the future), and help you identify areas where you can claim tax credits and incentives for next time. If you are concerned, our best advice is to get ahead of it with an opinion you can trust — before the IRS decides to investigate themselves.

About the author

Michael Silvio is a partner at MGO. He has more than 25 years of experience in public accounting and tax and has served a variety of public and private businesses in the manufacturing, distribution, pharmaceutical, and biotechnology sectors.

]]>Playing on the fear and uncertainty many taxpayers have felt over the past few years in the wake of the pandemic, scammers are working aim to steal sensitive personal information from taxpayers like you. In the following we’ll discuss specific scams to be aware of, including false stimulus payments, fraudulent unemployment claims, fake offers of employment via social media, and bogus charitable donations.

Tips for taxpayers on emerging scams

To avoid compromising yourself with these “too good to be true” schemes, taxpayers should stay wary, as these scams adopt a wide range of communication methods, including:

- Emails

- Phone calls

- Social media posts

- Targeted online advertisements

You must also consider each source before putting any of these arrangements on your tax returns — because ultimately, you are the one responsible for what is on the return, not the promoter who reached out to you and made a promise they failed to uphold. To mitigate risk, an anxious taxpayer should turn to trustworthy tax professionals to assist with their returns.

Read on to learn which scams fall under this Dirty Dozen category.

Scam #5: Pandemic-Related Scams

Economic Impact Payment and Tax Refund Scams

This scam involves identity thieves who use text messages, phone calls, or emails to ask individuals to click a link, verify a date, or provide bank account information to access Economic Impact Payments (EIPs), or stimulus payments.

Reminiscent of tax refund scams, you should act defensively by ignoring these calls and deleting suspicious emails or texts without opening them — the IRS will never contact an individual by phone, email, text, or social media to acquire sensitive information.

Mailbox theft is another worry associated with this scam, so we encourage you to exercise vigilance and the report suspected mail loss to postal inspectors.

Unemployment Fraud (and, subsequently, inaccurate taxpayer 1099-Gs)

As many people lost their jobs and unemployment rates rose during the pandemic, many taxpayers applied for and received unemployment compensation to stay afloat. But they were not the only ones who applied; defrauders went to work stealing the personal information of those who had not applied and proceeded to file unemployment compensation claims for themselves to ultimately steal the payments.

If this happened, you may receive Form 1099-G to report unreceived unemployment compensation. Then request a corrected form to file compliantly, stating only the unemployment compensation and income you did receive.

Fake Employment Offers Via Social Media

In a similar vein, scams continue to capitalize on those who faced unemployment throughout the pandemic by littering social media with fake job postings to entice out-of-work job seekers to provide their personal information. This can then be used to steal your identify or file a fraudulent tax return, so the scammer ends up with your tax refund.

Fake Charities Created to Steal Your Money

While fake charities aren’t exactly new to the scammer scene, the threat has grown throughout the pandemic. Because taxpayers can claim a deduction on their federal tax returns by donating money or goods to a qualified charity, giving back can be enticing. But taxpayers should always verify the charity in which they are donating to — note the exact name, web address, and mailing address, and confirm it is a legitimate organization and not a knock-off meant to confuse.

The IRS also recommends using this search tool to ensure a charity’s validity. Remember, a charity should never pressure an individual to donate right away, and do not donate using a gift card or money wire — only credit card or check, and only after you have performed your due diligence in verifying the charity’s legitimacy.

Consequences of falling for a Dirty Dozen scheme

It is important for taxpayers who have already taken part in transactions like these — or those who are thinking about doing so — to consult tax professionals before claiming any tax benefits they think they are owed.

Those taxpayers who have already claimed the purported tax benefits of one of these four “Dirty Dozen” arrangements on a tax return should file an amended return and go to an independent professional for guidance. If necessary, the IRS will examine the tax benefits from transactions like the ones depicted in the list and inflict penalties related to accuracy ranging from 20% to 40%, or a civil fraud penalty of 75% on any taxpayer who underpaid.

Our perspective on the latest batch of “Dirty Dozen” scams

This is not, of course, an exhaustive list of every scam the IRS has its eye on this year. But it does include some of the more common trends. The best advice we can give? If something looks too good to be true… it probably is. Consult your tax professional for guidance and know that it is in your best interest to stay aware of these nefarious arrangements, so you do not fall susceptible to additional penalties.

Stay tuned for more deep dives into the IRS’s Dirty Dozen list.

MGO’s Tax team brings more than 30 years of experience and is well versed in ensuring your tax returns are compliant. We also stay up to date on the risks, pitfalls, and warnings issued by the IRS so you don’t have to. If you think you have been involved in or are in the process of being involved in one of the Dirty Dozen scams, we can help. Contact us today.

]]>