- The IRS has intensified enforcement of transfer pricing regulations, significantly increasing potential penalties.

- Organizations can reduce exposure to transfer pricing penalties by ensuring adequate documentation and applying global transfer pricing policies consistently.

- In cases where penalties are imposed, businesses can seek penalty abatement by demonstrating reasonable cause and good faith, substantial compliance with transfer pricing rules, and leveraging effective representation from knowledgeable tax advisors.

~

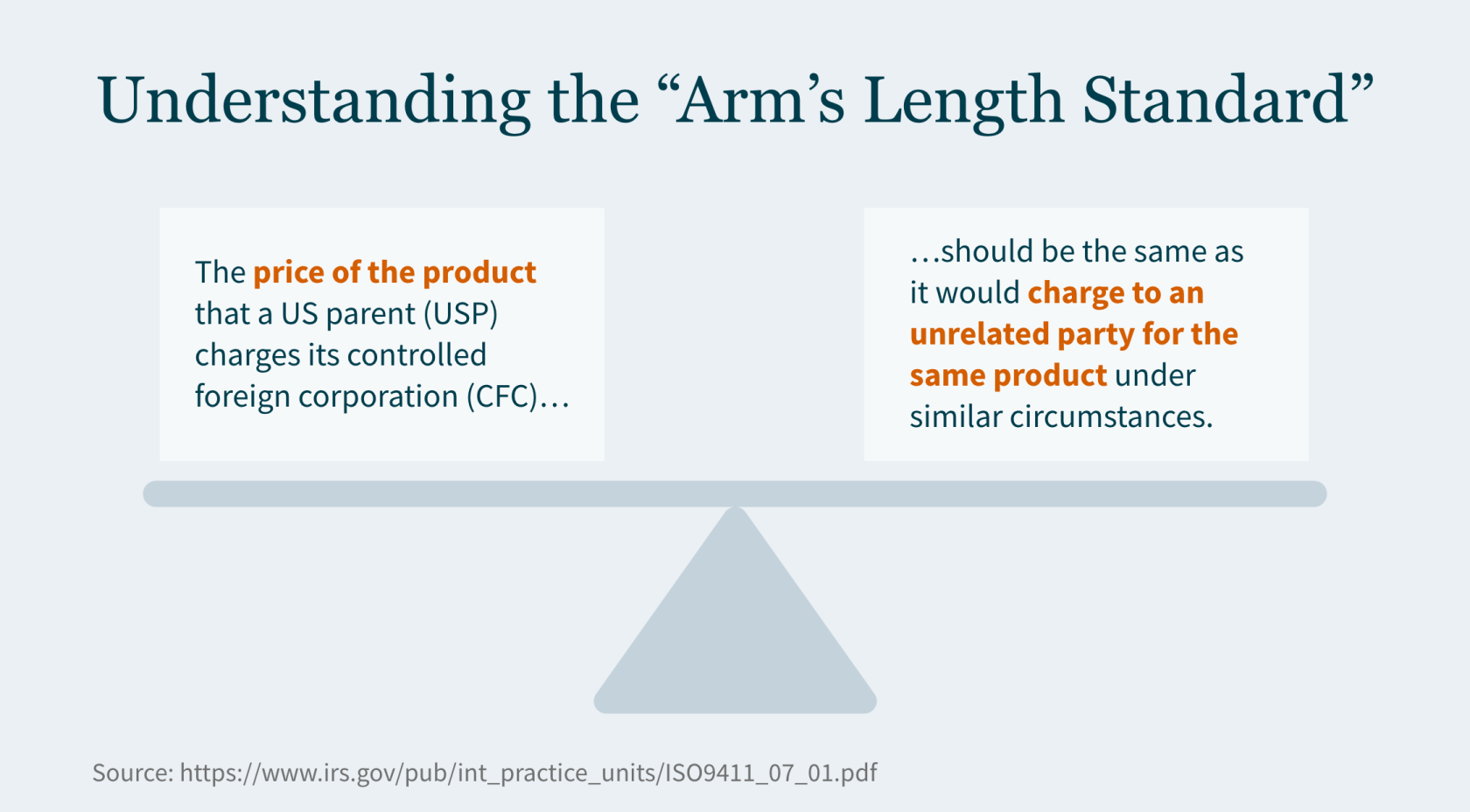

The Internal Revenue Service (IRS) implemented transfer pricing penalties to ensure the intercompany pricing reported on your income tax return is determined in a manner consistent with the arm’s length standard.

Until recently, penalty assessments were rare — not because improper transfer pricing between related parties was rare, but because IRS examiners tended to accept inadequate documentation. That leniency appears to be a thing of the past.

The IRS has indicated it will focus on applying Internal Revenue Code (IRC) Section 6662 penalties where proper documentation is lacking. This trend warrants serious attention if your company engages in cross-border transactions.

Imposing Transfer Pricing Penalties

The IRS can impose penalties when allocations under Section 482 result in substantial or gross increases in taxable income or where there are substantial or gross valuation misstatements concerning the transfer prices themselves.

These penalties can be severe, ranging from 20% to 40% of the tax underpayment, depending on the degree of non-compliance and the taxpayer’s disclosure of relevant information.

Historically, you could avoid these penalties by demonstrating you had reasonably used a transfer pricing method outlined in Section 482 or another method to more reliably determine transfer prices. Taxpayers must also provide contemporaneous documentation within 30 days of a request from the IRS.

The IRS’s Shift Toward Increased Penalty Assertion

The IRS Advisory Council’s 2018 Report noted that, although some transfer pricing documentation quality possibly fell short of the Section 6662 requirements, the IRS had not consistently asserted the penalty. Since then, the IRS has produced guidance addressing common flaws in transfer pricing documentation and best practices, and the agency is now expressing a renewed commitment to applying penalties more frequently and vigorously.

Holly Paz, commissioner of the IRS Large Business and International Division, spoke at several tax practitioner events in late 2022 — including the AICPA’s National Tax Conference, the American Bar Association Section of Taxation’s Philadelphia Tax Conference, and a Bloomberg Tax event. During these events, Paz noted the IRS has had success in litigating transfer pricing cases and is taking a closer look at economic substance and sham transactions — even in cases with transfer pricing documentation — to determine where it is appropriate to assert penalties.

Mitigating Exposure to Transfer Pricing Penalties

In 2020, the IRS published Transfer Pricing Documentation Best Practices Frequently Asked Questions (FAQs). These FAQs point to several features of proper documentation IRS agents look for when determining whether the agency should audit an organization’s transfer pricing methods.

Incorporating these features into your documentation may help reduce your risks:

- Sensitivity analysis – Assess the impact of removing a comparable company from the dataset and determine if such removal alters your position relative to the arm’s-length range. Evaluate how different profit-level indicators might change the results.

- Segmented financial data analysis – Examine if the segmented financial data accurately reflects the arm’s-length nature of the intercompany transaction. Detail the methodology used in constructing this data.

- Profit allocation in intercompany transactions – Analyze profit distribution among entities in the transaction. Ensure equitable economic outcomes for all parties, not just the tested party.

- Description of risks and related-party allocations – Describe associated risks in each intercompany transaction. Explain how profits and losses are allocated among related parties.

- Atypical business circumstances – Identify any unusual business conditions affecting the intercompany transaction. Discuss challenges in the economic analysis due to specific business results for the year.

To navigate this heightened scrutiny, taxpayers must take a proactive approach to document pricing transfer decisions. Steps you can take to avoid commonly seen inadequacies include:

- Providing a detailed description of your business and industry to help IRS agents understand operations and the larger marketplace in which you operate.

- Avoid using a checklist format. Instead, opt for a comprehensive analysis linking facts to the analysis. Base the analysis on well-supported facts, avoiding broad assumptions about the business.

- Ensure consistency in risk allocation with intercompany agreements. Align risk allocation with the comparable companies used in the economic analysis, and clearly explain any adjustments made to comparable companies for risk considerations.

- Prepare a best method selection analysis that justifies rejecting alternative methods for analyzing the intercompany transaction and provides a rationale for the chosen method.

- Clearly outline any adjustments to comparable data, such as working capital or location savings adjustments.

If you believe you have valuation misstatements or understated income tax in previously filed returns, it’s not too late to correct them. Filing a qualified amended return before the IRS contacts you about a transfer pricing audit is a defense against penalties. However, you must pay all taxes associated with the amended returns.

Seeking Penalty Abatement

In instances where penalties are assessed, it may be possible for taxpayers to seek abatement by demonstrating high-quality transfer pricing documentation. You may have a reasonable chance of having penalties abated if you:

- Demonstrate reasonable cause and good faith. Establish that the underpayment was due to reasonable cause, and you acted in good faith.

- Substantial compliance. Show that, despite any errors, you substantially followed the transfer pricing rules.

How We Can Help

The resurgence of transfer pricing penalties is an opportunity to reassess your transfer pricing strategies and compliance mechanisms.

For personalized guidance and assistance navigating these complexities, contact MGO today. Our team of professionals is equipped to help you mitigate risks, confirm compliance, and effectively manage any disputes with tax authorities. Act now to safeguard your business against the pitfalls of transfer pricing penalties.

]]>Executive Summary:

- Implementing basic accounting practices and understanding tax implications can help individuals working independently in creative fields gain clarity, meet obligations, and maximize income.

- Separating business and personal finances, tracking income and expenses, and budgeting for estimated taxes can help creators be proactive in their financial planning.

- Creators earning income across state lines or internationally need to be aware of varying taxation requirements in different jurisdictions.

~

Today’s artists need to view themselves as both businesses and creatives. Whether you are a painter, digital artist, photographer, website designer, YouTuber, Instagrammer, or any type of artist, creator, or influencer, understanding and managing your financial obligations is a crucial aspect of sustaining a thriving career.

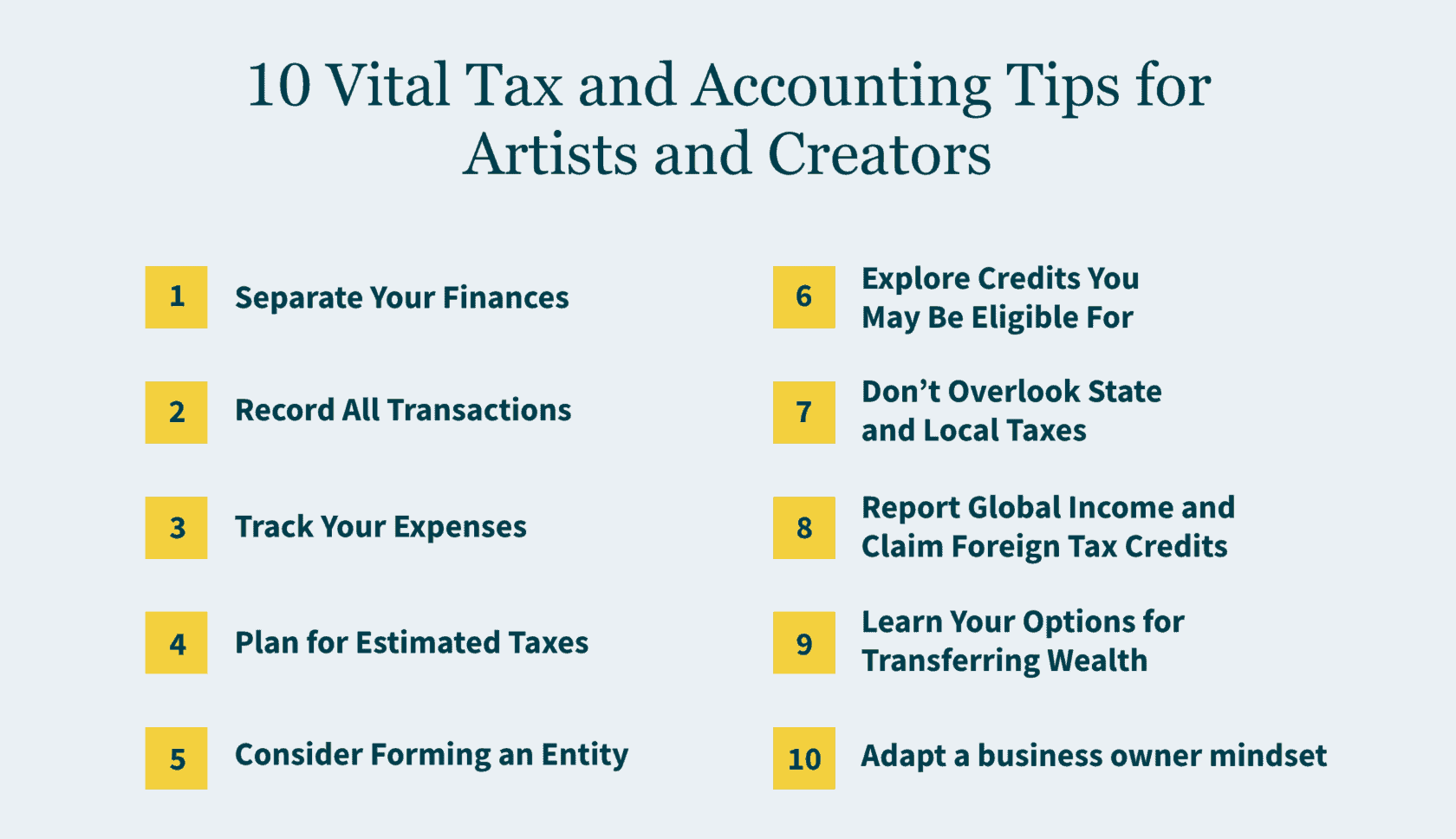

Here are 10 tips to help you meet your tax reporting responsibilities and get the most from your hard-earned income:

1. Separate Your Finances

To make your accounting more efficient and streamline the tax-filing process, it is a smart idea to separate your business and personal finances. Designate a dedicated business account to track income and expenses related to your artistic endeavors. This separation not only simplifies tax reporting but also enhances financial clarity, making it easier to assess the overall health of your creative enterprise.

Tip: Establish a separate account for business transactions, or multiple business accounts to allocate money for categories such as expenses, taxes, and savings.

2. Record All Transactions

Sometimes it can be challenging to determine what constitutes income. That’s why it’s important to track everything. Gifts received by sponsors are often taxable, especially if they are products in exchange for services (e.g., promotion of product). “Donations” from various fundraising activities like Kickstarter are also considered revenue. On the other hand, crypto and non-fungible tokens (NFTs) are considered property. Selling them usually generates a capital gain or loss.

Tip: Log all payments and gifts received, even if you are unsure, so your tax preparer can report appropriately.

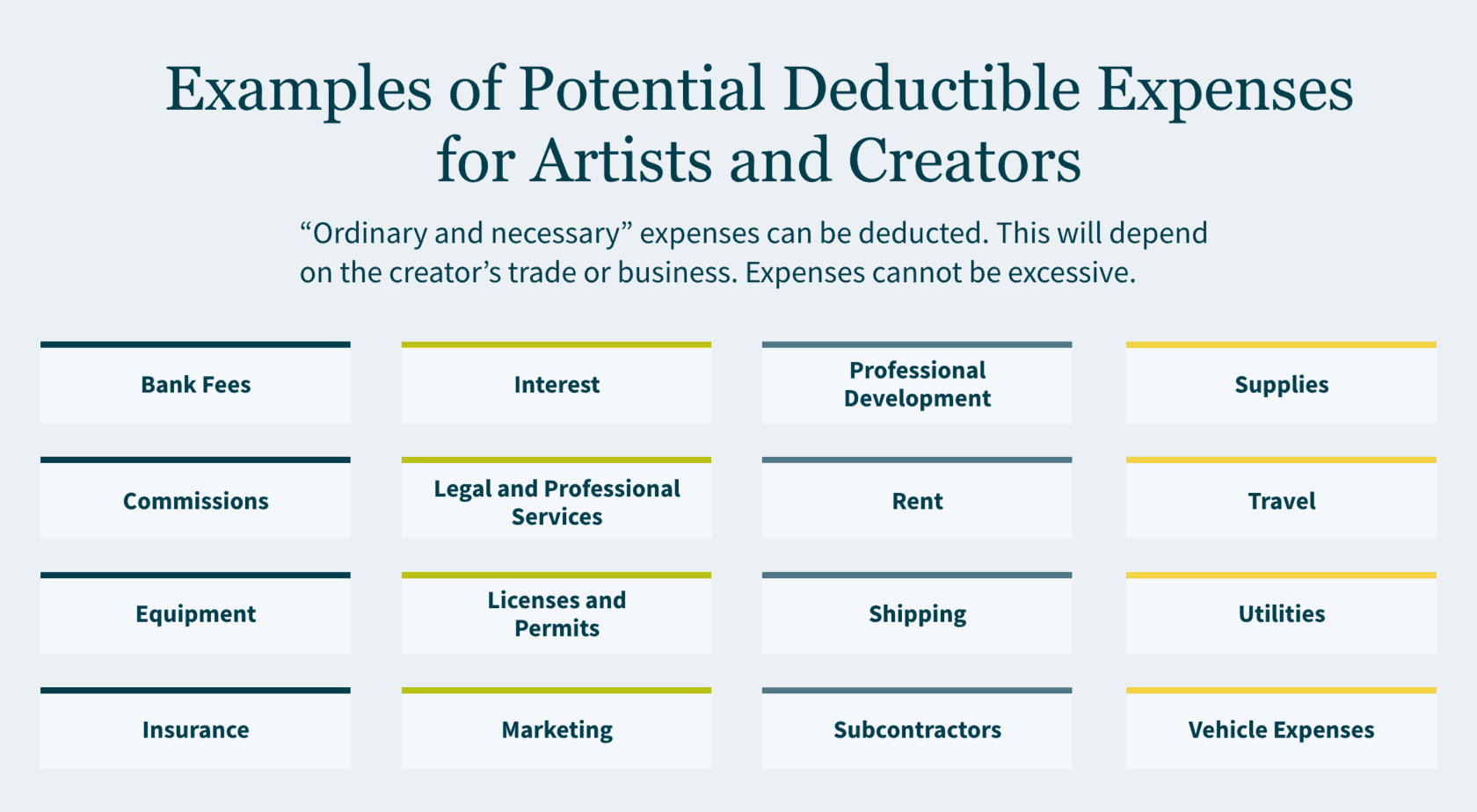

3. Track Your Expenses

Creators and artists can benefit from various tax deductions tailored to their industry. Deductible expenses may include art supplies, equipment, software subscriptions, professional development, and even a portion of your home used as a dedicated workspace. While expenses should not be excessive, any “ordinary and necessary” expenses of your craft can be deducted.

Tip: Save receipts and track expenses in real-time using a spreadsheet, app, or software for easy recording and reporting.

4. Consider Forming an Entity

Creators who run their own business are often independent contractors. Consider setting up an entity for the business — which can help protect your personal assets from your business assets and offer tax savings. S Corporations and LLCs are common for smaller businesses. For larger businesses where investors are coming in, C Corporation may make sense.

Tip: Do some research or talk to a tax professional to find out if setting up an entity makes business and financial sense for you.

5. Explore Credits You May Be Eligible For

Artists also may be eligible for various tax credits that can help offset their tax liability. Research and Development (R&D) credits can be applicable to certain creative processes, rewarding innovation in your artistic pursuits. For instance, software development is considered to be R&D for income tax purposes.

Tip: Consult a tax professional about ways to maximize credits and minimize your tax liability.

6. Don’t Overlook State and Local Taxes (SALT)

Beyond federal taxes, SALT significantly impact overall tax liability. When selling art online (whether physical or digital), be mindful of sales tax requirements, which are determined by local laws. Whether revenue is from “tangible” versus “intangible” products (physical objects versus services, ideas, software, etc.) can dictate where taxation occurs — affecting if your income is subject to sales tax or not.

Tip: Stay informed about varying tax rates, and be cautious of sales and use tax implications tied to transmitting creative art across state lines.

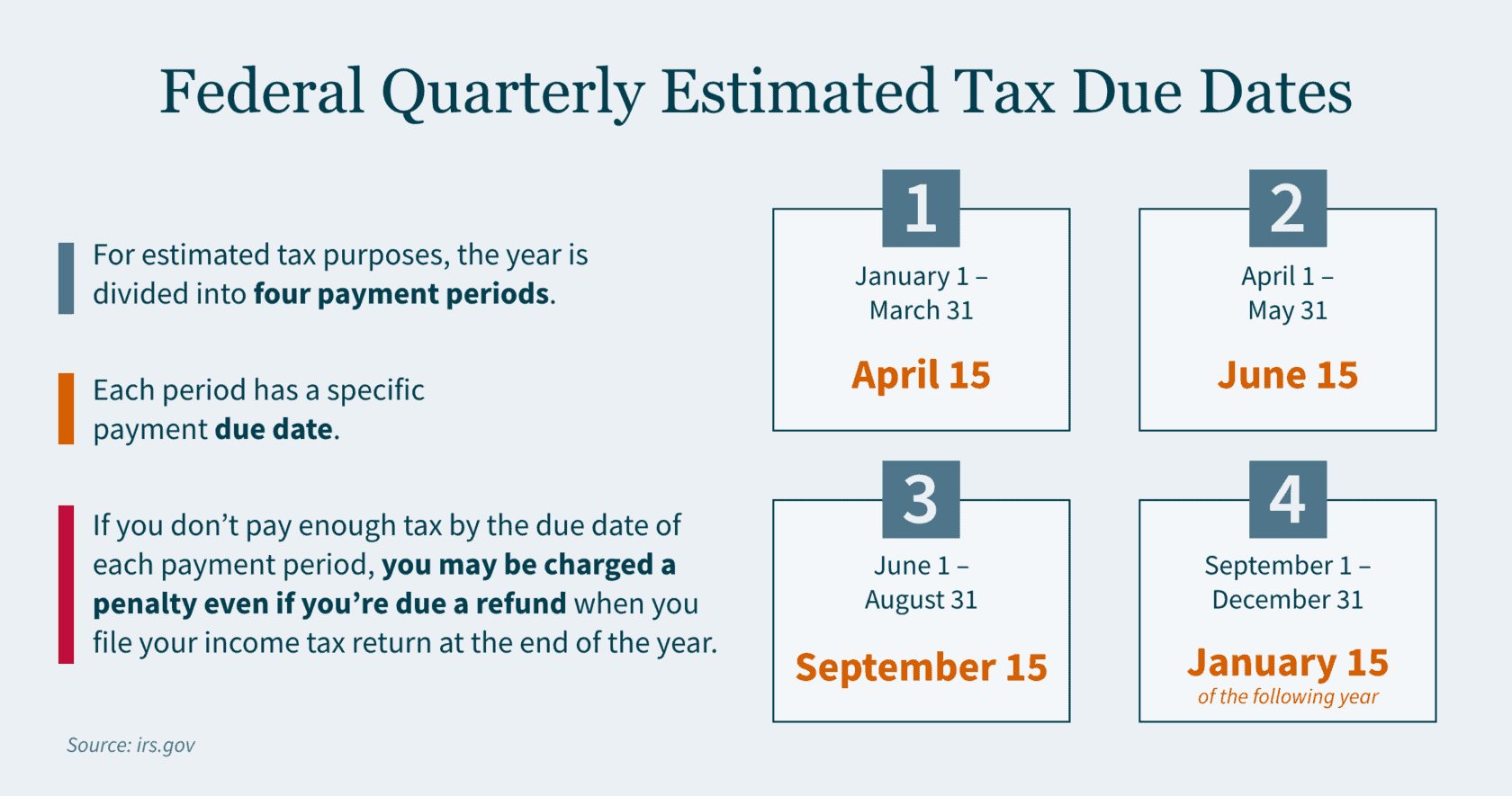

7. Plan for Estimated Taxes

As an independent contractor with variable income streams, you should plan for estimated taxes to avoid financial surprises. These quarterly payments encompass income taxes on your profits plus the self-employment tax (covering Social Security and Medicare). For those earning up to $160,200 in net income, the self-employment tax rate currently stands at 15.3%. The silver lining is that you can deduct half of this self-employment tax when filing your income taxes.

Tip: Set aside a portion of your income for estimated tax payments, ensuring proactive financial planning throughout the year.

8. Report Global Income and Claim Foreign Tax Credits

United States (U.S.) citizens or residents earning abroad must report all worldwide income to the Internal Revenue Service (IRS). If you’re earning income in or from foreign countries, it’s crucial to understand foreign tax credits, filing requirements, and deductibility in various jurisdictions. Every tax jurisdiction may have a different method to tax your creation; and different tax implications may arise based on where brands and intellectual property are created and protected.

Tip: Work with a tax professional to evaluate the potential benefits of foreign tax credits for non-U.S. income.

9. Learn Your Options for Transferring Wealth

Digital assets such as domain names, electronically stored photos, and videos to email and social media accounts all have value. When transferring these as gifts or bequests, there may be tax implications that can be circumvented if the transfer is appropriately structured or organized.

Tip: Consider trusts and estate planning for more tax-efficient wealth transfer.

10. Adapt a Business Owner Mindset

As an artist, embracing a business owner’s perspective is essential for long-term success. Understanding basic financial statements like balance sheets and profit and loss (P&L) statements allows you to gauge profitability, identify your most valuable revenue sources, and streamline your efforts. Elevating your financial literacy empowers you to make more informed decisions — which can lead to greater freedom and flexibility in your artistic career.

Quick Tip: Learn to read a balance sheet and create a basic P&L statement for a clearer financial picture.

Integrate Financial Management into Your Creative Journey

Effective financial planning is like a great work of art — every brushstroke matters. By taking these steps today you can better position yourself to continue pursuing your creative passion tomorrow.

Need a hand with taxes and accounting for your creative venture? Our Entertainment, Sports, and Media practice works with a diverse range of artists — from musicians to photographers to online creators — and our International Tax and State and Local Tax teams can provide guidance to help you address areas like sales tax or foreign tax credits. Reach out to MGO today.

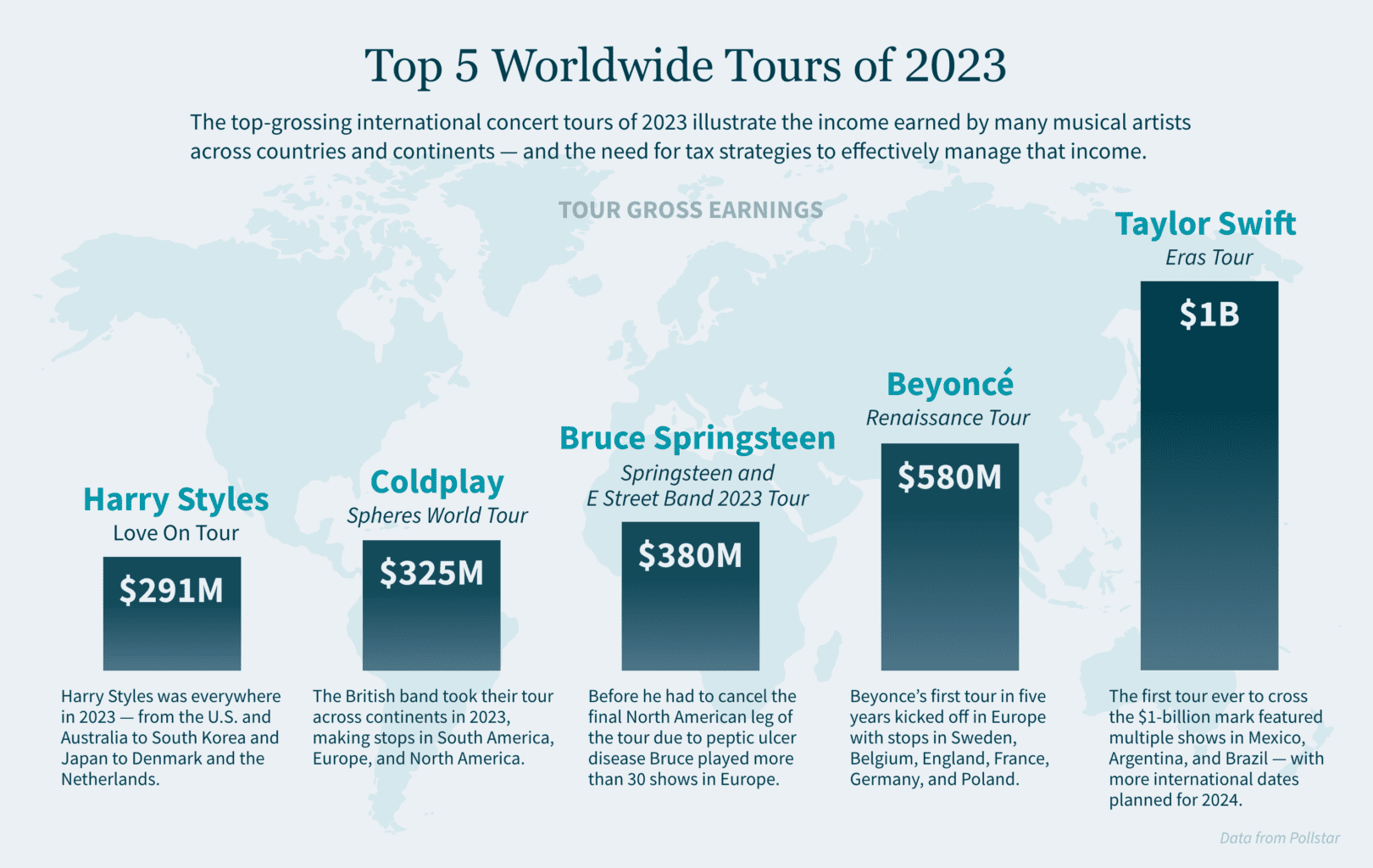

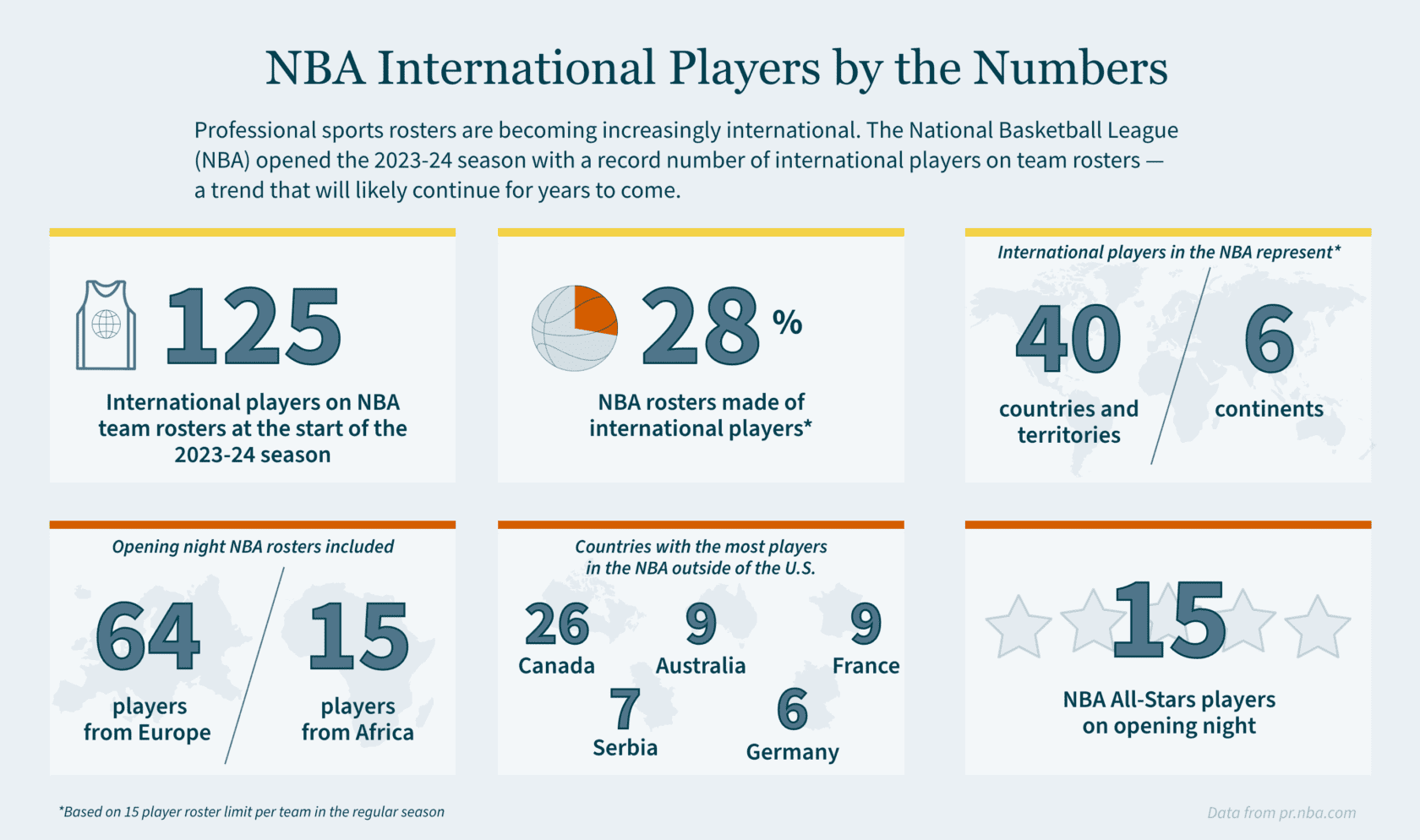

- Agents and managers can help globally earning clients like professional athletes, musical artists, and entertainers strategically manage finances and taxes across borders to maximize earnings.

- For U.S. citizens and residents earning money abroad, key areas for advisors to address include endorsement deals, royalties, foreign properties, foreign tax returns, and tax structuring that considers foreign investments.

- For foreign (non-resident) athletes, artists, and entertainers performing in the U.S., considerations include but are not limited to U.S. taxable income, withholding rules, tax status, Central Withholding Agreements (CWA), and tax treaties.

~

As an agent or manager for athletes, artists, and entertainers, many of your clients likely earn income across borders as they perform worldwide. Strategically managing their finances and taxes is crucial to maximize earnings. Proper planning can help reduce tax burdens and avoid double taxation across jurisdictions. This allows your clients to focus on their careers while you may finesse your assistance to them in optimizing their income with guidance from tax professionals.

Understanding key tax considerations can enable you to put frameworks in place to mitigate your clients’ liabilities. For clients who are citizens or residents of the United States earning money abroad, all worldwide income must be reported to the IRS. However, foreign countries also tax income earned by non-residents. Assessing relevant tax treaties and structuring contracts in an appropriate manner can lead to more advantageous tax treatment.

When your clients have income from various sources both from inside and outside the United States, proactive tax planning is key. Common international income types to consider include:

- Salaries from foreign leagues and tournaments

- Performance fees from concerts and festivals

- Royalties

- Endorsements and sponsorships

- Bonuses and prizes from international tournaments

- Merchandise sales

- Other income earned while playing or performing overseas

How these income types are classified and sourced impacts tax liabilities. Consulting tax professionals before your clients sign any deals allows for upfront planning that can keep more money in your clients’ pockets.

5 Key Considerations for U.S.-Based Athletes, Artists, and Entertainers Earning Income Abroad

If you are an advisor to musical artists, professional athletes, film actors, or other performers who are U.S. citizens, residents, or green card holders with foreign income sources, here are five important areas to address:

- Endorsement Deals – How will the construction of a contract impact tax treatment abroad? Will the income be considered U.S. or foreign sourced? What are some ways to proactively plan for potential tax savings?

- Royalties – Can royalties be classified differently if content is published while clients are abroad? How are royalties affected by collaborations with international artists? Is it considered U.S. income if royalties are received while playing or performing abroad?

- Foreign Properties – What are the tax rules surrounding your clients purchasing or renting homes abroad (rules may vary by country)? Did you know that foreign rental income may need to be disclosed on a U.S. tax return? How do investments in foreign countries get reported and taxed?

- Foreign Tax Returns – When is return filing required for extended stays abroad? Can foreign taxes be credited (and is the credit dollar-for-dollar)? What should be expected for payments received as a contractor versus as an employee? Which expenses are deductible in each country? For example, are agent fees, travel expenses, and entertainment deductible?

- Foreign Tax Structuring – Is it better to withhold taxes on gross revenues or after deductible expenses? How do local, state, and regional (provincial, cantonal, district, county) taxes factor in?

With these areas addressed upfront, you can maximize income and minimize overall tax burdens for your clients as opportunities arise.

5 Top Considerations for Foreign Domiciled Athletes, Artists, and Entertainers Performing or Playing in the U.S.

If you are an advisor to athlete, artist, and entertainer clients who are not residents or citizens of the U.S. but earn income in this country, areas that could have an impact on your clients’ taxes include (but are not limited to):

- U.S. Taxable Income – Is U.S.-sourced income taxable? What types of income may this include? Is there a requirement to file a U.S. federal income tax return? Is there an income threshold that must be met?

- Withholding Rules – What are the withholding rules surrounding payments to foreign athletes, artists, and entertainers?

- U.S. Tax Status – How is U.S. tax status determined — residency for income tax and domicile for transfer tax? How is taxation affected with or without a Social Security Number (SSN) or Individual Taxpayer Identification Number (ITIN)?

- Central Withholding Agreements (CWAs) – A CWA is a tool that can help entertainers and athletes who don’t live in the U.S. by having U.S. income tax withheld based on the non-resident’s income. Is a CWA beneficial for the individual’s situation?

- Tax Treaties – Does the individual’s home country have a tax treaty with the U.S.? How does it impact tax liabilities?

Evaluating options surrounding tax statuses, withholding approaches, and applicable treaties can mitigate liabilities and optimize tax treatment for your foreign clients.

Work with Tax Professionals to Help Your Clients Maximize Global Income

As an agent or manager navigating global income for your clients, working with experienced tax professionals is key. Advisors can assess your clients’ situations across jurisdictions to put frameworks in place reducing liabilities and avoiding double taxation. With the right global tax strategy tailored to each client, you can position them to pursue worldwide career opportunities with maximum income and minimum taxes.

Need help navigating the world of international tax for athletes, artists, and entertainers? We have experienced professionals dedicated to both international tax and entertainment, sports, and media (ESM) ready to answer all your questions. Reach out to our International Tax Team today.

]]>- In April, the U.S. Tax Court made news when it ruled in favor of businessman Alon Farhy, who challenged the Internal Revenue Service (IRS)’s authority to assess penalties for the failure to file IRS Form 5471.

- IRS Form 5471 is the Information Return of U.S. Persons With Respect to Certain Foreign Corporations.

- Taxpayers may be interested in filing protective refunds, and they should start the process sooner rather than later—there is a statute of limitations of two years for claiming refunds.

- This case’s ruling could have reverberating effects when it comes to the IRS collecting additional penalties, but only time will tell.

On April 3, 2023, the U.S. Tax Court came to a decision in the case Farhy v. Commissioner, ruling that the Internal Revenue Service (IRS) does not have the statutory authority to assess penalties for the failure to file IRS Form 5471, or the Information Return of U.S. Persons With Respect to Certain Foreign Corporations, against taxpayers. It also ruled that the IRS cannot administratively collect such penalties via levy.

Now that the IRS doesn’t have the authority to assess certain foreign information return penalties according to the court, affected taxpayers may want to file protective refund claims, even if the case goes to appeals — especially given the short statute of limitations of two years for claiming refunds.

Our Tax Controversy team breaks down the Farhy case, as well as what it may mean for your international filings — and the future of the IRS’s penalty collections.

The case

Alon Farhy owned 100% of a Belize corporation from 2003 until 2010, as well as 100% of another Belize corporation from 2005 until 2010. He admitted he participated in an illegal scheme to reduce his income tax and gained immunity from prosecution. However, throughout the time of his ownership of these two companies, he was required to file IRS Forms 5471 for both — but he didn’t.

The IRS then mailed him a notice in February 2016, alerting him of his failure to file. He still didn’t file, and in November 2018, he assessed $10,000 per failure to file, per year — plus a continuation penalty of $50,000 for each year he failed to file. The IRS determined his failures to file were deliberate, and so the penalties were met with the appropriate approval within the IRS.

Farhy didn’t dispute that he didn’t file. He also didn’t deny he failed to pay. Instead, he challenged the IRS’s legal authority to assess IRC section 6038 penalties.

The court’s ruling

The U.S. Tax Court then held that Congress authorized the assessment for a variety of penalties — namely, those found in subchapter B of chapter 68 of subtitle F — but not for those penalties under IRC sections 6038(b)(1) and (2), which apply to Form 5471. Because these penalties were not assessable, the court decided the IRS was prohibited from proceeding with collection, and the only way the IRS can pursue collection of the taxpayer’s penalties was by 28 U.S.C. Sec. 2461(a) — which allows recovery of any penalty by civil court action.

How this court decision affects your international penalty assessments

This case holds that the IRS may not assess penalties under IRC section 6038(b), or failure to file IRS Form 5471. The case’s ruling doesn’t mean you don’t have an obligation to file IRS Form 5471 — or any other required form.

Ultimately, this decision is expected to have a broad reach and will affect most IRS Form 5471 filers, namely category 1, 4, and 5 filers (but not category 2 and 3 filers, who are subject to penalties under IRC section 6679).

However, the case’s impact could permeate even deeper. For years, some practitioners have spoken out against the IRS’s systemic assessment of international information return (IIR) penalties after a return is filed late, making it impossible for taxpayers to avoid deficiency procedures. The court’s decision now reveals how a taxpayer can be protected by the judicial branch when something is deemed unfair. Farhy took a stand, challenged the system, and won — opening the door for potential challenges in the future.

It’s uncertain as to whether the IRS will appeal the court’s decision. But it seems as though the stakes are too high for the IRS not to appeal. While we don’t know what will happen, a former IRS official has stated he expects that, for cases currently pending review by IRS Appeals, Farhy will not be viewed as controlling law yet.

The impact of the ruling is clear and will most likely impact many taxpayers who are contesting — or who have already paid — IRC 6038 penalties. It may also affect other civil penalties where Congress has not prescribed the method of assessment in the future.

How you should respond to the court’s decision

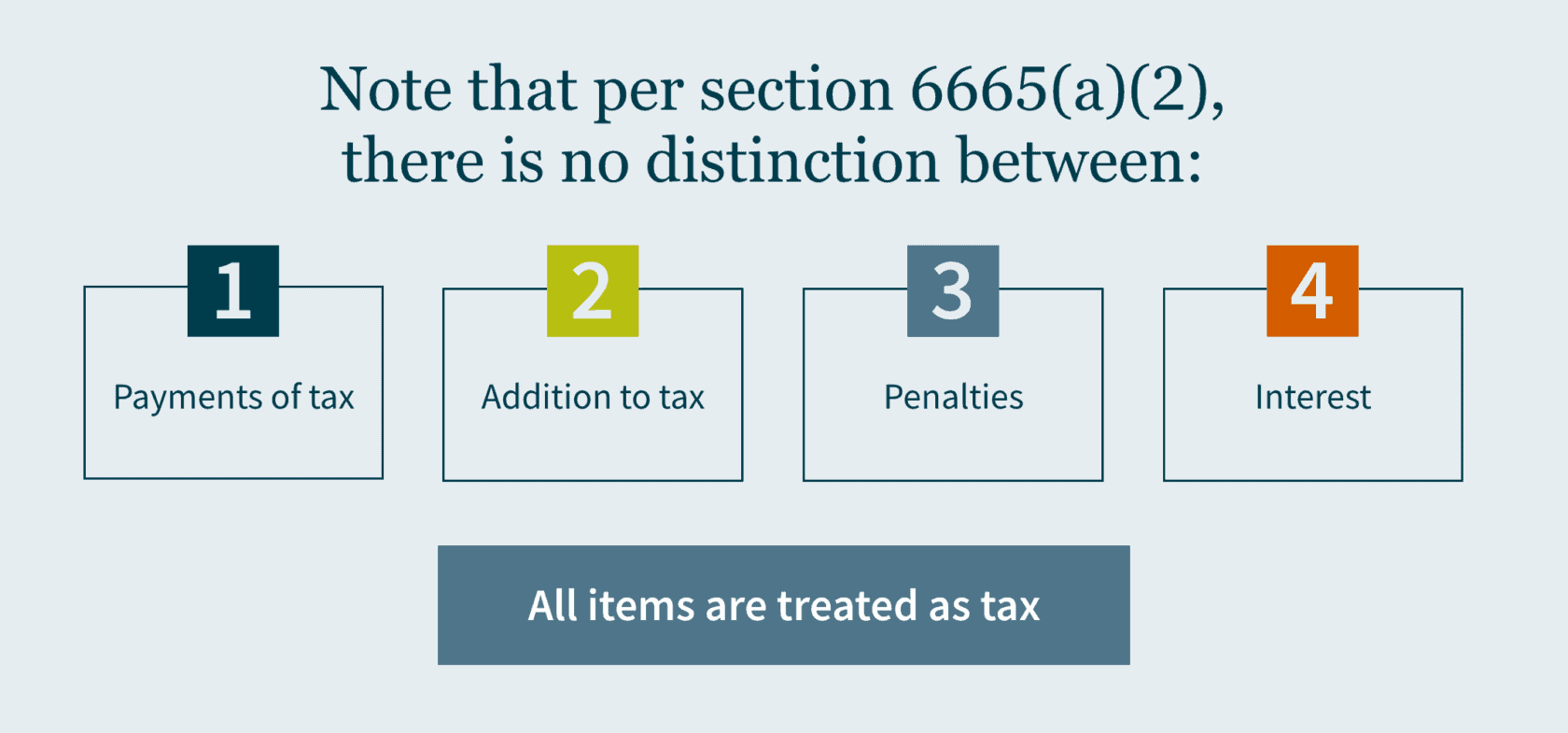

You should move quickly to take advantage of the court’s decision, as there is a two-year statute of limitations from the time a tax is paid to make a protective claim for a refund. It’s likely this legislation wouldn’t affect refund claims since that would be governed by the law that existed when the penalties were assessed. Note that per IRC section 6665(a)(2), there is no distinction between payments of tax, addition to tax, penalties, or interest — so all items are treated as tax.

If you’ve previously paid the $10,000 penalty, it’s important to file your protective claim now, unless you’ve entered into an agreement with the IRS to extend the statute of limitations, which can occur during an examination. Requesting a refund won’t ever hurt, but some practitioners believe the IRS may try to keep any penalty money it collected, even if the assessment is invalid— because, in its eyes, the claim may not be. Just know, you can file your protective claim for a refund but may not get it, at least not any time soon.

The Farhy decision could likewise be applied to other US IRS forms, such as 5472, 8865, 8938, 926, 8858, 8854, and some argue the Farhy decision may also be applied to IRS Form 3520.

How MGO can help

Only time will tell if the court’s decision will open the government up to additional criticisms for other penalty assessments. If you have paid your penalties and are wondering what your current options are, MGO’s experienced International Tax team can help you determine if you’re eligible to file a refund claim.

Contact us to learn more.

]]>

- Recent global events have emphasized the need for reviewing and strengthening the supply chain for manufacturers from both an operational and cost savings perspective.

- A “China Plus One” strategy is a good start but may prove inadequate depending on the nature of a disruption.

- Supply chain backup plans need to be agile, flexible, and built with contingencies for undetermined issues.

- Raising prices may address some concerns but also causes customer issues and is not a long-term solution.

During the COVID-19 pandemic, organizations across different trades and industries faced a number of operational obstacles caused by supply chain disruptions. From economic uncertainty, to labor shortages, to rising costs, leaders had to find alternatives to create an agile and adaptable framework for this ever-changing market. With the global tax overhaul where juristidictions are racing for the middle and not the bottom, companies are faced with continuous change.

Our International Tax and Transfer Pricing leaders have developed methods and problem-solving techniques for local and global networks. These approaches help businesses address their supply chain challenges, as well as give guidance on how to continually evaluate and adjust their strategic initiatives while considering tax and transfer pricing risks in their supply chain decisions. The proverbial tax tail should not wag the dog but it should not be ignored either. Companies should consider performing transfer pricing analyses to determine how to allocate the financial impact of the changes to the supply chain among related entities and ensure appropriate remuneration to those entities involved in supply chain initiatives for their respective functions performed and risk incurred in the process.

In this article, we will answer three of our most-asked questions and provide the necessary steps to transform and optimize supply chains amid constant uncertainty — now and in the future.

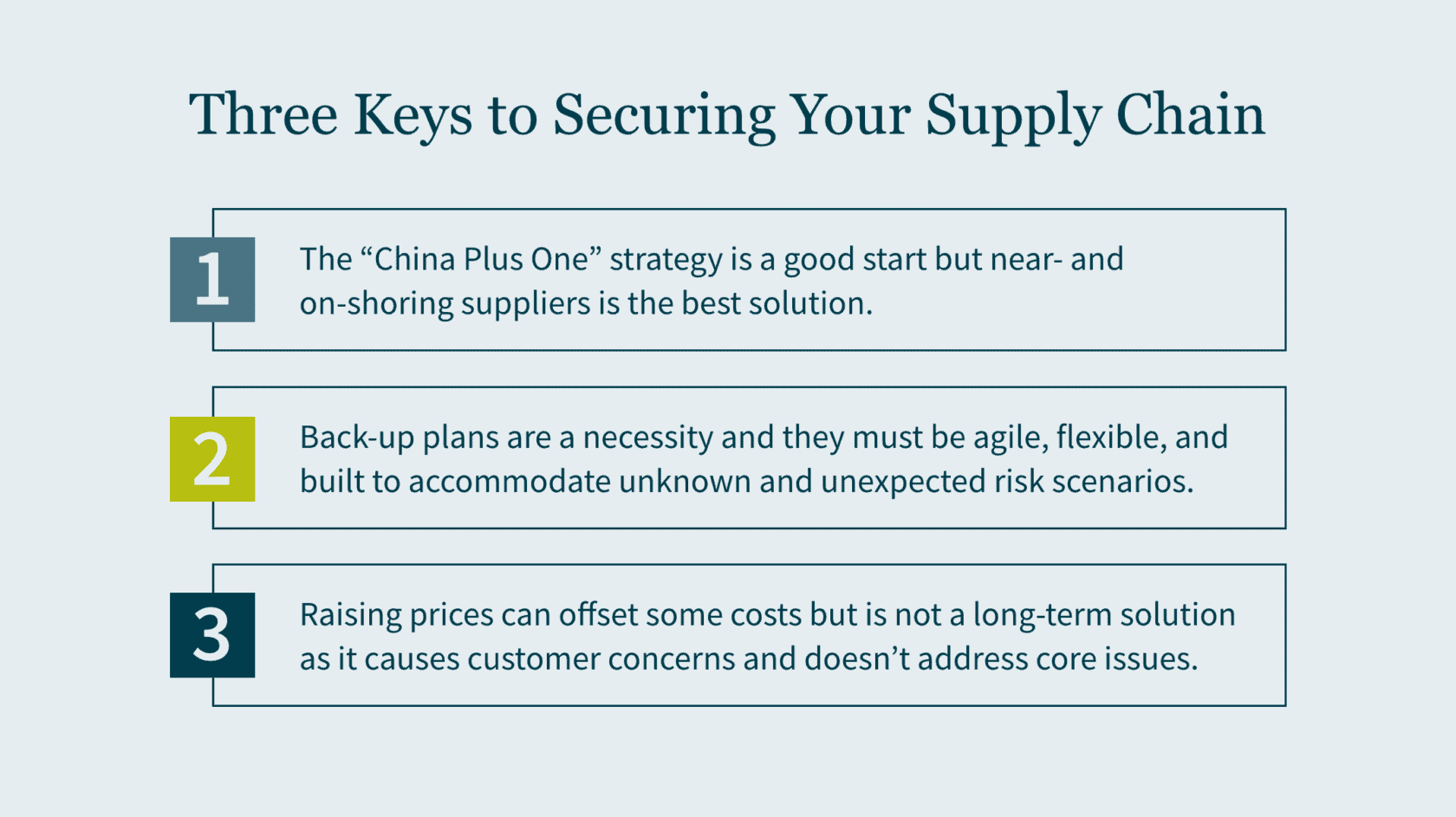

#1: Can adopting the “China Plus One” strategy diversify my supply chain?

In recent years, most U.S.-based businesses and consumers have learned that global supply chains have become too dependent on China. Prior to 2020, business leaders had already begun shifting away from China in the wake of the previous administration’s tariff challenges, intangible property (IP) disputes, and the ensuing trade war. Factory and port shutdowns in China in the early days of the pandemic and the issues that have followed were wakeup calls for those that hadn’t implemented alternative sources of supply. An enduring lesson of the past few years is that sole sourcing from any vendor or vendors in one location comes with a high-risk level. In renewing the supply chain, companies must consider the economic climate, the political environment, the ease of doing business, and personnel availability. Tax and transfer pricing is generally not in the forefront nor should it be. But giving it some thought after consider the already mentioned items may pay significant dividends.

Building redundancy into the supply chain at different tiers and maintaining inventory levels have become necessary steps for international manufacturers.The China Plus One strategy has been on the radar of companies that operate in China for several years, but the need to diversify supply chains is now a priority, with many manufacturers actively pursuing supplementary sourcing from another country in Southeast Asia. However, the supply chain crisis of the past two years shows this strategy may also be failing. As long as the goods produced are an ocean away from the markets that consume them, uncertainty from various disruptive factors can lead to shortages, higher costs, lower revenues, and customer dissatisfaction.

Actions moving forward:

Along with decoupling from China, truly de-risking the supply chain comes down to three factors:

- Optionality

- Redundancy

- Market proximity

While fully onshoring production and supply sources may not be operationally, economically, or logistically feasible, the supply network is less risky when it is closer to the market where it is widely consumed.

Consider engaging or contracting new stateside suppliers and local manufacturers to better serve the U.S. market. You should also review your supply base for any overreliance on a single source or geography. After that, you can research the best options to decrease the distance between where your products are produced and purchased. Insourcing, onshoring, nearshoring and acquisitions are all viable options. The approach that makes sense for your business must consider cost, capacity, quality, control, and reputation. Regardless of your approach, the goal should be to improve supply chain resilience and flexibility so you can better manage disruptions.

#2: Does having a back-up plan reduce supply chain disruptions?

Preparation and readiness may help with how your company fares during industry interruptions. A back-up plan should have built-in agility so it can be adapted and activated quickly based on a variety of external factors.

In recent years, manufacturers learned static backup plans were not adequate to address rapidly changing global conditions. These backup strategies were not agile enough to be effective amid complex disruption. Consequently, manufacturers were challenged to get the level of service they needed from existing suppliers or quickly identify new suppliers, resulting in processes that simply were not feasible from an implementation or sustainable cost standpoint.

Backup plans are a necessity, but they’re generally based on known risks. As global supply chains grow more intertwined and the universe of uncertainty expands, new risks and variables come into play. You can’t just plan for one contingency; you need to weigh the possible outcomes for multiple options across different scenarios. Changes in manufacturing locations and sourcing strategies aren’t the only scenarios worth evaluating, nor is resilience to disruption the only outcome worth measuring. For example, if you’re considering expanding into a new market or adding to your product mix, those strategic adjustments should be factored into your supply chain model and assessed for plausibility. Tax liabilities, trade compliance risks, and total cost to serve are no less critical considerations than deliverability or lead times.

The reality is you cannot prepare for every contingency, so scenario planning needs to evolve to detect signals of disruption earlier and enable greater agility in supply chain decision-making when the unexpected occurs. For example, if your company is planning on vertical integration thath will be the cause of significant in-country hiring, you must assess the benefits of employment credits and incentives that can help reduce overhead costs.

Actions moving forward:

Review your supply chain model to:

- reflect current constraints;

- incorporate points of vulnerability; and

- conduct a scenario planning exercise to address a specific problem or inform your next strategic move.

Ideally, you should simulate multiple scenarios to pressure test the supply chain, anticipate issues, and chart the best path forward when disruption hits. Scenario planning should become a regular business practice so you can quickly respond to unforeseen events.

#3: Will raising prices offset the increasing costs of materials and logistics?

Although raising prices is not the only way to successfully reduce costs, there are some tradeoffs that will have to be considered. Higher costs are an unfortunate reality for most manufacturers in the current supply chain environment. Because cost reductions are not easy to accomplish, many companies are shifting their focus to cost containment within areas of their supply chains that they can control. Higher costs are a sure way of reducing taxable income and where possible, selectively deciding where the spend will occur in the supply chain may not reduce the impact of inflation or costs being spent – however it may impact the amount of tax dollars being spent. Tax, like all other costs, is an expense that should be viewed and considered for cost reduction measures.

For example, intercompany movements are often rife with inefficiency or seldom get the level of scrutiny they deserve. If parts and finished goods are shipped intercompany, ask why: Is there a value add, is it because your business has always done it that way, or is it an enabling factor to hedge against process inefficiencies? If your global supply chain is failing to consistently meet the needs of local markets, does the original rationale for keeping production and sources of supply at a distance still stand? Or would it be beneficial to establish a near or local market capability? Using models like a contract manufacturer can be a quicker way to further evaluate whether it makes sense to establish an in-house capability.

It’s also a good time to revisit lean initiatives that you may have previously dismissed or deprioritized—though be cautious of prioritizing efficiency at the expense of resilience. And beyond your own four walls, there are a few foundational measures of good supply chain hygiene that may help with cost takeout:

- Shift from transportation spot rates to contract rates to stabilize pricing.

- Ensure you have contracts with alternate suppliers; don’t rely on a single source.

- Encourage your customers to optimize order volume for full truck or container loads through more rigorous enforcement of transactional service standards.

These measures may help manage costs to some degree but are unlikely to completely offset them. By raising prices, you will more than likely create frustration and confusion among your customers. However, if you find yourself absolutely needing to raise prices, it’s better to be upfront and honest rather than taking a below-the-radar approach.

Another way to address rising costs, rather than passing additional costs onto all your customers, is to consider segmenting them and developing pricing strategies based on level of priority.

Actions moving forward:

Perform an in-depth analysis of your customer base and product suite to understand the most and least profitable segments. Consider implementing a price segmentation strategy that shifts the heaviest burden of cost increases to your least profitable customers. Also, take a close look at your least profitable product segments and how they line up with cost distribution. Do you have slow-moving SKUs driving a disproportionate amount of costs? It may make sense to rationalize them.

We can help strengthen your supply chain

Now is the perfect time for manufacturers to gain competitive advantage by optimizing production and delivery processes and prioritizing long-term spending goals. Our International Tax and Transfer Pricing and Management Advisory practice leaders are ready to assess your current supply chain, identify potential points of weakness, adjusting transfer pricing policies, and assist you in implementing strengthening procedures. Reach out to our team to learn how we can reduce your risk and power production.

]]>- Many international companies are struggling with their supply chain management amid external factors playing out on the global stage.

- To mitigate the challenges, you should be aware of the current trends in supply management as well as strategies to improve your resilience and flexibility.

- Current trends include AI and automation, supply chain as a service, circular supply chains, risk management and stability, and sustainability.

- Diversifying your supply chain and creating a backup plan can help you remain agile.

- Know the tax implications of your supply chain.

The last two years have seen major disruption in supply chain management — and throughout 2023, that turbulence is expected to continue. The freight supply and demand equation was a common issue during the pandemic and recovery period. We’re now seeing how the Russian-Ukraine conflict is reshaping the global supply chain for many companies. And amid all the economic uncertainty, supply shortages, and rising costs, the U.S. and EU (European Union) have been heavily investing in infrastructure, putting even more pressure on China with the U.S.-imposed tariffs’ strenuous implications.

While managing your supply chain is currently a challenge, you’re not completely at the mercy of these external factors which are generally outside of your control. There are strategies to mitigate the impact to your supply chain: your goals should be to both improve your supply chain resilience and flexibility to allow you to better manage the disruptions — those foreseen and unforeseen.

Our International Tax team breaks down some of the current trends and strategies to be aware of.

Trends in supply chain management

Some of the main trends in supply chain management include artificial intelligence and automation, supply chain as a service, circular supply chains, risk management and stability, and an increased focus on sustainability. Now, more than ever, mid-market multinational companies must be strategic. These additional constraints cause strain on these companies that are being forced to pivot to address these issues among additional disruption.

Odds are, you’ve been rethinking the way you currently manage your supply chain — because the global situations aren’t changing. The China tariffs are unlikely to disband soon, and there seems to be no end in sight to the Russia-Ukraine conflict.

Diversifying your supply chain

Many agree that the global supply chain was too dependent on China, and now companies are considering breaking away from the Asia Pacific region to look at the Mexican maquiladora or IMMEX programs. Both these programs are, for all intents and purposes, synonymous, save for one detail: the IMMEX added shelter companies as a modality. Under this shelter program, companies may set up operations in Mexico without establishing a legal Mexican entity.

These programs have been in existence since the 1960s, so they’ve proven their worth — however, they don’t work for everyone, so it’s worth perusing other options. It’s important to remember that sourcing from vendors in only one location, regardless of where that location is geographically, is accompanied by elevated risk.

To mitigate this, you should not only diversify your supply chain but also create redundancies to avoid a single point of failure. In addition, bringing your sources of supply closer to where you operate also reduces the opportunity for risk. Engage with new suppliers and manufacturers in the Americas, for instance, and analyze your current suppliers to see if there is any one region you rely on more heavily already, then minimize the distance between your production and purchasing — without, of course, sacrificing quality, cost, control, and reputation. By optimizing your global footprint, you can maximize your production opportunities, minimize risk, and scout new vendors and locations for future efficiency.

Devising a backup plan for supply chain disruptions to address multiple contingencies

At the end of the day, we know that no matter how sophisticated or agile your supply chain backup plan is, external factors — which are never static — can affect things in unexpected ways. With rapidly and ceaselessly changing global conditions, there’s no way to account for everything you could encounter.

But there are ways to prepare. Plan for multiple contingencies, weighing their outcomes. Don’t forget to think broadly and for new opportunities — for example, if you’re looking at expanding into new markets or territories or want to add a new product line, you must assess their plausibleness under a variety of conditions (and not just logistical conditions, like lead times and delivery … but also tax liabilities and compliance, too).

Keep your supply chain planning agile and ready to evolve by reviewing its current model and updating it to ensure it reflects the restraints and vulnerabilities you’re presently dealing with. By making a step-by-step plan — for multiple scenarios — you can chart your path forward, regardless of what unfolds on the global stage in these uncertain times.

How MGO can help

Knowing the tax implications of your supply chain is crucial to your global success, and our experienced International Tax team can help you navigate the supply chain turmoil — no matter how turbulent. By reviewing your current supply chain model to determine where your processes can be strengthened and made more efficient, as well as pinpointing your vulnerabilities, we can help you hone your supply chain’s true potential while safeguarding it against whatever comes next.

About the authors

John Apuzzo is the leader of our International Tax Practice. He supports public and private companies, and high-net-worth individuals, as they conduct business on the global stage. His passion for developing optimal tax strategies helps his clients reinvest in their businesses and enjoy the wealth they have worked so hard to earn.

Mandy Li is a transfer pricing partner and provides strategic and tactical transfer pricing solutions to public and private multinational organizations. She supports highly complex global engagements, with an emphasis on transactions moving to and from the China region.

]]>In Notice 2021-39, the IRS released guidance providing penalty relief for filers who made “good faith efforts” to adopt the new schedules. More recently, in response to continued concern and feedback from taxpayers and practitioners, the IRS has indicated that under certain circumstances taxpayers will be entirely relieved of the need to file the new forms this year.

A tough tax season for the IRS

The announcement of additional relief comes as IRS Commissioner Charles Rettig has acknowledged that the agency faces “enormous challenges” this tax season. For example, millions of taxpayers are still waiting for prior years’ returns to be processed thanks to a monumental backlog.

To address such issues, he says, the IRS has taken “extraordinary measures,” including mandatory overtime for IRS employees, the creation and assignment of “surge teams,” and the temporary suspension of the mailing of certain automated compliance notices to taxpayers. In addition, the partial suspension of the filing requirements for Schedules K-2 and K-3 might ease the burden for both affected taxpayers and the IRS.

K-2 and K-3 filing requirements

Provisions of the Tax Cuts and Jobs Act, which was enacted in 2017, require taxpayers to provide significantly more information to calculate their U.S. tax liability for items of international tax relevance. The Schedule K-2 reports such items, and the Schedule K-3 reports a partner’s distributive share of those items.

Schedules K-2 and K-3 must be filed with a partnership’s Form 1065, “U.S. Return of Partnership Income,” or an S corporation’s Form 1120-S, “U.S. Income Tax Return for an S Corporation.” These new schedules require more detailed and complete reporting than the entities may have provided in the past.

Schedules K-2 and K-3 replace portions of Schedule K and numerous unformatted statements attached to earlier versions of Schedule K-1. Previously, partners and S corporation shareholders could obtain the information included on the schedules through various statements or schedules the respective entity opted to provide, if any.

In January of 2022, the IRS surprised many in the tax community when it posted changes to the instructions for the schedules. Under the revised instructions, an entity may need to report information on the schedules even if it had no foreign partners, foreign source income, assets generating such income, or foreign taxes paid or accrued.

For example, if a partner claims a credit for foreign taxes paid, the partner might need certain information from the partnership to file his or her own tax return. Although some narrow exceptions apply, this change expanded the pool of taxpayers required to file the schedules.

Latest exception

Under the latest guidance, announced February 16th through an IRS FAQ, partnerships and S corporations do not need to file the schedules if they satisfy all the following requirements for the 2021 tax year:

- The direct partners in the domestic partnership are not foreign partnerships, corporations, individuals, estates or trusts, and

- The domestic partnership or S corporation has no foreign activity, including 1) foreign taxes paid or accrued, or 2) ownership of assets that generate, have generated or may be expected to generate foreign-source income.

- For the 2020 tax year, the domestic partnership or S corporation did not provide its partners or shareholders — nor did they request — information regarding any foreign transactions.

- The domestic partnership or S corporation has no knowledge that partners or shareholders are requesting such information for the 2021 tax year.

Entities that meet these criteria are not required to file Schedules K-2 and K-3. But there is an important caveat; if such a partnership or S corporation is notified by a partner or shareholder that it needs all or part of the information included on Schedule K-3 to complete its tax return, the entity must provide that information.

Moreover, if the partner or shareholder notifies the entity of this need before the entity files its own return, the entity no longer satisfies the criteria for the exception. As a result, it must provide Schedule K-3 to the partner or shareholder and file the schedules with the IRS.

“Good faith exception”

In addition to the FAQ exemption, Notice 2021-39, released in June 2021, exempts affected taxpayers from penalties for the 2021 tax year if they make a good faith effort to comply with the filing requirements for Schedules K-2 and K-3. While some are calling this a “good faith” exception, there’s some irony in this, given that the IRS is not exactly acting in good faith itself.

When determining whether a filer has established such an effort, the IRS considers, among other things:

- The extent to which the filer has made changes to its systems, processes, and procedures for collecting and processing the information required to file the schedules;

- The extent to which the filer has obtained information from partners, shareholders, or a controlled foreign partnership or, if not obtained, applied reasonable assumptions; and

- The steps taken by the filer to modify the partnership or S corporation agreement or governing instrument to facilitate the sharing of information with partners and shareholders that is relevant to determining whether and how to file the schedules.

The IRS will not impose the relevant penalties for any incorrect or incomplete reporting on the schedules if it determines the taxpayer exercised the requisite good faith efforts.

Temporary reprieves

Both the IRS FAQ exception and the “good faith exception” explicitly refer to 2021 tax year filings. In the absence of additional or updated guidance, partnerships and S corporations should expect and prepare to file the schedules for 2022 and later tax years.

MGO tax advisors are available

If you have questions, MGO can help. Please reach out to our partnership and international tax professionals for assistance. We can help keep you in compliance with these new requirements.

]]>OECD BEPS 2.0 overview

The OECD/G20 Inclusive Framework on BEPS released Blueprints on Pillar One and Pillar Two. The Blueprints address the tax challenges of the digitalization of the economy and propose fundamental changes to global tax rules. All multinational businesses will feel the impact of the changes.

BEPS 2.0 contains two parallel elements: Pillar One would revise profit allocation and nexus rules to allocate more taxing rights to market countries. Pillar Two would establish new global minimum tax rules to ensure that all business income is subject to at least a minimum level of tax.

The application of Pillar One rules is limited to MNEs that have a consolidated revenue above €750 million ($914 million) and also have in-scope revenues outside the domestic market above a threshold that is not yet defined. The three basic elements of Pillar One:

• A new taxing right for market jurisdictions based upon a share of a business’ residual profits (Amount A)

• A fixed return for certain distribution and marketing activities physically in a market jurisdiction (Amount B)

• Enhanced dispute prevention and resolution mechanisms to improve tax certainty

What is Amount A?

Amount A grants market jurisdictions new taxing rights using a formula that is not based on the arm’s length principle. Taxing rights are based on an active and sustained engagement in a market jurisdiction rather than a company’s physical presence. The two broad sets of businesses subject to Amount A are consumer-facing businesses (CFB), and automated digital services (ADS).

The Amount A formula is made up of three distinct components:

• A profitability threshold will isolate residual profits potentially subject to reallocation.

• A reallocation percentage will define the share of residual profits (actual profits minus the profitability threshold) or allocable tax base of the market jurisdictions.

• An allocation key will be used to allocate the tax base among the eligible jurisdictions.

The Blueprint does not yet define the profitability threshold or reallocation percentage threshold, but these will be determined through additional work by the Inclusive Framework.

What is Amount B?

Amount B has two goals. First, it is intended to simplify transfer pricing rules for tax administrations and reduce compliance costs for taxpayers. Second, it is intended to reduce disputes between tax administrations and taxpayers.

Amount B attempts to set a standard baseline return for routine marketing and distribution activities. The transactional net margin method will be used to determine Amount B and the remuneration for the baseline activities. Amount B would be implemented through domestic law, and the Blueprint indicates that existing treaties can resolve disputes, but where there is no treaty in place, a new treaty-based dispute resolution mechanism may be required.

New rules establish a framework of minimum taxation for multinationals

Pillar Two Blueprint introduced several new rules to establish a global framework of minimum taxation, which only apply to MNE groups with a total consolidated revenue above €750 million.

• The income inclusion rule (IIR) operates as a top-up tax when income of controlled foreign entities is taxed below an effective minimum tax rate.

• The switch-over rule (SoR) complements the IIR by removing treaty obstacles in situations where a jurisdiction uses an exemption method that could frustrate the application of a top-up tax to branch structures.

• The undertaxed payments rule (UTPR) serves as a backstop to the IIR through application to certain constituent entities; the top-up tax computation is the same as under the IIR.

• The subject-to-tax rule (STTR) would help countries protect their tax base by denying treaty benefits for deductible payments made to jurisdictions with low or no taxation from related parties of the same consolidated group of businesses.

Biden international tax proposals

The Biden administration has responded to the OECD BEPS 2.0 and has also proposed changes for U.S. tax policy. Biden’s proposals were aimed at helping fund his $2.25 trillion infrastructure plan with a big focus on clean energy. Clearly, they were also an attempt to stabilize the international tax architecture. The proposals call for raising the current tax rate on global intangible low-tax income (GILT), to 21% from 10.5% and ending a tax break for companies exporting U.S.-manufactured goods, known as foreign derived intangible income (FDII).

The United States has proposed to OECD a simple profitability threshold to determine which companies are subject to Pillar One rules. The U.S. proposal would replace the complicated definitions the current OECD proposals use to determine which industries and business models are affected. It would affect fewer companies than the OECD proposals, without reducing how much corporate profit is reallocated. According to the U.S. proposal, it would apply to no more than 100 multinationals. For Pillar Two, the United States recently proposed a 15% global minimum tax which would put pressure on negotiators in the OECD discussion to move higher than the 12.5% they were expected to agree on.

Transfer pricing implications for MNEs

A lot of uncertainties remain. COVID-19 has had fundamental impacts on how we live, work, and do business. COVID-related spending and other economic challenges may prompt increased scrutiny from tax authorities. But some businesses may be able to turn these challenges into opportunities. Here are some strategies and practices that can make a difference:

• Plan for uncertainty. The economic and regulatory environments remain fluid, so it is critical for companies to review their business operations and transfer pricing policies more regularly and adjust along with these changes. The proposed tax rules may affect incentives regarding the location of profits and investments. MNEs should plan ahead by modeling the potential tax impacts of these new rules to quantify the effects. Reviewing financial results and making adjustments only for the year-end may trigger customs and corporate tax audits.

• Supply or value chain restructuring. Businesses need to consider both temporary and permanent impacts of COVID-19 and the new tax rules. This is critical time to review how to adapt business structure to the changing consumer behavior, supply chain dynamics, and tax policy updates. It’s also time to evaluate the digitalization of business and its tax implications.

• Add more rigor to compliance. Meeting the requirements for documentation is more critical. To minimize audit risks, it is extremely important for taxpayers to ensure consistency in intercompany agreements, transfer pricing policies, and documentation. Businesses should have intercompany agreements in place and keep them up-to-date. Appropriate transfer pricing policies and documentation should reflect the new economic and business environment.

• Talk to your tax advisors. Transfer pricing analysis can begin a healthy discussion that identifies business challenges and opportunities. Exploring your business and tax structures can help you plan for economic and regulatory uncertainties and minimize your risks.

MGO’s specialized transfer pricing team offers you the resources you need to develop a solution that is designed to meet the specific needs of your business. Contact us for more information about transfer pricing.

]]>With economic and tax policy a primary focus during the 2020 election, the

winning candidate/party will play a central role in pushing further economic

stimulus forward and determining long-term course for recovery following the

economic fall-out from the COVID-19 pandemic.

With the Biden campaign all but wrapping up the presidential election, businesses

and individuals with overseas concerns must pay close attention to how the

proposed policies of the candidate/party will affect their total tax liability and be prepared to make any changes or updates, in some cases, during the two months

ending the 2020 tax year.

2020 prospective results overview

Biden Victory | 50/50 Senate Split

In the case of a 50/50 split in the Senate, the tie-breaking vote goes to the Vice President, giving de facto Senate leadership to the party in the White House.

The Biden campaign’s proposed tax plan focuses on rolling back tax breaks and “loopholes” for corporations and high-net-worth individuals, specifically related to changes made in the 2017 Tax Cuts and Jobs Act (TCJA). Biden also proposed a number of significant tax breaks and stimulus efforts targeted at spurring growth in historically-disadvantaged communities and the renewable energy sector, while simultaneously rolling back fossil fuel industry subsidies.

Economic Stimulus

In the case of a Biden/Democratic win, it seems unlikely that an out-going President Trump will be motivated to support a new COVID-19 economic stimulus plan before leaving office. On the other hand, an incoming President Biden will likely immediately push for stimulus upon taking office, and will be successful with control over the Senate.

Biden Victory | Republican Senate Majority

Any outcome that has White House and Senate leadership at loggerheads will likely result in the blocking of any major economic and tax policy changes. With Senate Majority Leader Mitch McConnell’s re-election, there is little reason to suspect he’ll alter his long-standing obstructionist stance against Democrat-sponsored and supported bills.

Tax planning considerations

Increase in GILTI Tax Rate

- Accelerate income in 2020 under preferable tax rate.

- Defer deductions until after tax rate is raised.

Changes to Offshoring Tax Breaks and Penalties

- Accelerate overseas manufacturing and imports before tax plans change.

- Consider delaying launching U.S.-based manufacturing expansion until tax benefits are put into place.

Changes to Repatriation Tax Breaks and Penalties

Accelerate plans to move operations overseas before proposed tax penalties can be installed.

Final thoughts

It may be weeks before the full outcome of the election is determined and agreed-upon. This delay could create difficulties for corporations and individuals with overseas interests seeking to avoid tax penalties that could follow a Biden presidency. It is recommended to begin planning for all likely outcomes as soon as possible.

]]>Proactive tax planning during the M&A process is one of the key methods to drive value before, during, and after the transaction. In the cannabis and hemp industries, tax planning takes on a special importance due to the various regulatory concerns at the federal, state, and local levels and the overwhelming impact of IRC Section 280E.

In the simplest terms, the crux of tax discussions at the deal structure level are based on the competing interests of the Acquirer and the Target company’s owners – the former seeking to maximize future tax benefits, and the latter seeks to minimize or defer the tax liabilities relating to the gain from the transaction. In the following, we lay out the tax fundamentals guiding optimal value for both sides of an M&A transaction.

Target company tax classification

A key element to the discussion between the Acquirer and the Target’s owners is the tax classification of the Target company, since this affects a number of transaction structuring decisions. The most common tax classification types are the following:

C Corporation – This is the general form of a corporation. A C Corporation is taxed at the entity level. In addition, distributions to shareholders are typically subject to a second level of tax.

S Corporation – This is a corporation with an S Election. An S Corporation is generally treated as a passthrough entity for income tax purposes, although certain items may be subject to entity level taxation.

Partnership – A partnership is treated as a passthrough entity for income tax purposes. Taxation occurs at the partner level.

Disregarded (as separate from its tax owner) – All income is taxed to the tax owner of the disregarded entity. A common legal form for a disregarded entity is a single-member limited liability company (LLC).

Asset vs. stock acquisitions

This topic was addressed in our article focused on transaction structuring but represents such an essential touchstone that a more in-depth examination is warranted.

Broadly speaking there are two fundamental structures to an M&A transaction, each with its own tax implications: asset acquisition and stock acquisition.

Asset acquisition

The Acquirer purchases some or all of the Target’s assets. The Acquirer can also assume some, all, or none of the Target’s liabilities. (Note that certain successor liabilities can also transfer over.) Target may then either continue operations or liquidate following the transaction.

Tax Impact on Target/Target Owners:

C Corporation: Gain on the asset sale should be subject to tax at the entity level. In addition, any distributions of the proceeds from the transaction should generally be subject to a second level of taxation at the shareholder level.

S Corporation: Gain on the asset sale should typically be subject to tax at the shareholder level. However, certain built-in gains originating from a prior C Corporation conversion could be taxed at the entity level.

Partnership: Gain on the transaction should be subject to tax at the partner level.

Besides the general tax impact by entity type, there are also different classifications of the gain from the transaction:

- Capital Gain – This generally results from the sale of capital assets and assets used in a trade or business.

- Ordinary Gain – This can result from the sale of ordinary income assets (e.g., accounts receivable, inventory) and from depreciation recapture from previously depreciated assets. The amount of ordinary gain can have an effect on a number of tax attributes, as well as how much of a sale can be deferred through installment sale treatment. In addition, for Target Owners that are taxed on the gain as individuals, this gain can result in a higher effective tax rate than capital gain.

Tax Impact on Acquirer:

The Target’s assets that are acquired are typically stepped-up to fair market value, which may potentially generate additional depreciation and amortization deductions, subject to any Section 280E limitations.

Stock acquisition

An equity transaction involves the sale of equity by the Target company’s owners to the Acquirer. Generally, all assets and liabilities of the Target company are transferred in the process. This often includes the Target’s tax liabilities and uncertain tax positions (although there are certain exceptions for partnerships).

As such, the Acquirer may find itself liable for tax audit adjustments.

This is especially relevant in the cannabis industry, where Section 280E audits can result in significant tax liabilities. As part of the diligence process, Section 280E exposure should be identified and quantified. In addition, indemnifications, representation & warranties, and tax representation responsibilities should consider the impact of Section 280E.

Tax Impact on Target/Target Owners:

C Corporation: Gain on the equity sale should be subject to tax at the Target owner level, resulting in a single level of taxation. If the stock meets the qualifications for Qualified Small Business Stock and the requisite 5 year holding period is met (i.e., the Section 1202 exclusion), up to $10 million of the gain can be excluded by Target owners that are not corporations.

S Corporation: Gain on the equity sale should be subject to tax at the shareholder level. S Corporation shareholders do not qualify for the Section 1202 exclusion.

Partnership: Gain on the equity sale should be subject to tax at the partner level.

Usually, gain on the sale of an ownership interest is characterized as capital gain. This is especially important for individuals who have held the equity for more than a year, since they may qualify for preferential tax rates. However, note that partnerships with “hot assets” will have a portion of this gain recharacterized as ordinary gain.

Tax Impact on Acquirer:

An Acquirer purchasing a corporate Target’s stock does not obtain a step-up in the basis of Target, resulting in the Acquirer typically not being able to take the additional tax deductions described above for an asset purchase. However, depending on the circumstances, an IRC 338 election ((g) or (h)(10)) or an IRC 336(e) election may be available to treat the stock acquisition as an asset acquisition for US tax purposes. Tax modelling is often recommended to determine whether making such an election is advisable, especially considering that the election may result in adjustments to purchase price to reflect any additional tax costs or to reflect a premium for allowing the election.

An Acquirer purchasing a partnership Target’s equity also generally does not obtain a step-up in the basis in assets, unless a Section 754 election is in place or the Acquirer is acquiring 100% of the Target’s equity. As a result, a Section 754 election is often made in order to step-up the inside basis of the partnership’s assets to match the outside basis of the ownership interests held by the partners.

Tax attributes (e.g., net operating losses, credits) of the Target company transfer over in an equity transaction. However, they may be subject to limitations due to the ownership change (e.g., Section 382). As a result, a review of the availability of tax attributes post-transaction is often factored into the transaction structuring considerations.

Cash vs. stock vs. debt: the perfect storm of tax-free acquisitions

The other major determinant of the tax implications of an M&A equity deal is the form of consideration paid by the Acquirer. Consideration typically comes in some combination of cash, stock, or debt.

In the notably cash-poor cannabis and hemp industries, equity consideration is commonly used to lower the cash flow needs in M&A. However, the proliferation of distressed assets and over-extended operations have made debt assumptions an emerging and increasingly common form of consideration as well. Consequently, an Acquirer willing to pay in cash is relatively unique and brings significant advantage to the M&A negotiation table.

As the percentage of equity consideration in the transaction increases, the opportunity to have at least a portion of the transaction be tax-free also increases:

Corporations – The transaction may be able to be structured as a reorganization (and sometimes a contribution) if the equity consideration is at least 40%. This usually results in no gain recognition for the equity portion of the consideration. The cash/debt portion would still be taxable.

Partnership – The transaction may be able to be structured as a part-sale/part-contribution. This would result in the contribution portion being nontaxable (subject to certain exceptions).

Navigating tax credits

A thorough review of the potential tax benefits and credits available to a Target can influence the structure of an M&A deal and increase the appeal for the Acquirer. Tax credits and incentives in particular can result in significant tax savings. Even cannabis operators subject to Section 280E can qualify for significant credits and incentives at the state & local levels. For instance, cannabis operators have been able to qualify for job creation credits, social equity incentives, and reduced local tax rates.

International transactions

One final consideration to take into account with M&A is the potential for an international transaction. This can occur in a foreign “go public” transaction or an expansion into international operations. These types of deals add an additional (and possibly unfamiliar) layer of tax considerations to a deal structure. Often, US tax planners familiar with the US tax intricacies of the transaction coordinate with their foreign counterparts to iron out the details of the transaction to ensure that the transaction is tax efficient in all of the respective jurisdictions.

As part of an international transaction, some form of Acquirer structuring usually occurs in order to take advantage of various tax incentives (e.g., treaty benefits) while mitigating exposures such as Subpart F. This can be as simple as forming a new holding company and as complicated as a detailed international structure that considers IP placement, supply chain, and transfer pricing.

Final thoughts

Ultimately, any M&A deal will require careful tax planning to minimize tax burdens and maximize the value of the deal. As an important aspect of the M&A process, tax planning is one of the best ways to ensure that both sides of the transaction get the best deal possible.

Catch up on previous articles in this series and see what’s coming next…

]]>