- Agents and managers can help globally earning clients like professional athletes, musical artists, and entertainers strategically manage finances and taxes across borders to maximize earnings.

- For U.S. citizens and residents earning money abroad, key areas for advisors to address include endorsement deals, royalties, foreign properties, foreign tax returns, and tax structuring that considers foreign investments.

- For foreign (non-resident) athletes, artists, and entertainers performing in the U.S., considerations include but are not limited to U.S. taxable income, withholding rules, tax status, Central Withholding Agreements (CWA), and tax treaties.

~

As an agent or manager for athletes, artists, and entertainers, many of your clients likely earn income across borders as they perform worldwide. Strategically managing their finances and taxes is crucial to maximize earnings. Proper planning can help reduce tax burdens and avoid double taxation across jurisdictions. This allows your clients to focus on their careers while you may finesse your assistance to them in optimizing their income with guidance from tax professionals.

Understanding key tax considerations can enable you to put frameworks in place to mitigate your clients’ liabilities. For clients who are citizens or residents of the United States earning money abroad, all worldwide income must be reported to the IRS. However, foreign countries also tax income earned by non-residents. Assessing relevant tax treaties and structuring contracts in an appropriate manner can lead to more advantageous tax treatment.

When your clients have income from various sources both from inside and outside the United States, proactive tax planning is key. Common international income types to consider include:

- Salaries from foreign leagues and tournaments

- Performance fees from concerts and festivals

- Royalties

- Endorsements and sponsorships

- Bonuses and prizes from international tournaments

- Merchandise sales

- Other income earned while playing or performing overseas

How these income types are classified and sourced impacts tax liabilities. Consulting tax professionals before your clients sign any deals allows for upfront planning that can keep more money in your clients’ pockets.

5 Key Considerations for U.S.-Based Athletes, Artists, and Entertainers Earning Income Abroad

If you are an advisor to musical artists, professional athletes, film actors, or other performers who are U.S. citizens, residents, or green card holders with foreign income sources, here are five important areas to address:

- Endorsement Deals – How will the construction of a contract impact tax treatment abroad? Will the income be considered U.S. or foreign sourced? What are some ways to proactively plan for potential tax savings?

- Royalties – Can royalties be classified differently if content is published while clients are abroad? How are royalties affected by collaborations with international artists? Is it considered U.S. income if royalties are received while playing or performing abroad?

- Foreign Properties – What are the tax rules surrounding your clients purchasing or renting homes abroad (rules may vary by country)? Did you know that foreign rental income may need to be disclosed on a U.S. tax return? How do investments in foreign countries get reported and taxed?

- Foreign Tax Returns – When is return filing required for extended stays abroad? Can foreign taxes be credited (and is the credit dollar-for-dollar)? What should be expected for payments received as a contractor versus as an employee? Which expenses are deductible in each country? For example, are agent fees, travel expenses, and entertainment deductible?

- Foreign Tax Structuring – Is it better to withhold taxes on gross revenues or after deductible expenses? How do local, state, and regional (provincial, cantonal, district, county) taxes factor in?

With these areas addressed upfront, you can maximize income and minimize overall tax burdens for your clients as opportunities arise.

5 Top Considerations for Foreign Domiciled Athletes, Artists, and Entertainers Performing or Playing in the U.S.

If you are an advisor to athlete, artist, and entertainer clients who are not residents or citizens of the U.S. but earn income in this country, areas that could have an impact on your clients’ taxes include (but are not limited to):

- U.S. Taxable Income – Is U.S.-sourced income taxable? What types of income may this include? Is there a requirement to file a U.S. federal income tax return? Is there an income threshold that must be met?

- Withholding Rules – What are the withholding rules surrounding payments to foreign athletes, artists, and entertainers?

- U.S. Tax Status – How is U.S. tax status determined — residency for income tax and domicile for transfer tax? How is taxation affected with or without a Social Security Number (SSN) or Individual Taxpayer Identification Number (ITIN)?

- Central Withholding Agreements (CWAs) – A CWA is a tool that can help entertainers and athletes who don’t live in the U.S. by having U.S. income tax withheld based on the non-resident’s income. Is a CWA beneficial for the individual’s situation?

- Tax Treaties – Does the individual’s home country have a tax treaty with the U.S.? How does it impact tax liabilities?

Evaluating options surrounding tax statuses, withholding approaches, and applicable treaties can mitigate liabilities and optimize tax treatment for your foreign clients.

Work with Tax Professionals to Help Your Clients Maximize Global Income

As an agent or manager navigating global income for your clients, working with experienced tax professionals is key. Advisors can assess your clients’ situations across jurisdictions to put frameworks in place reducing liabilities and avoiding double taxation. With the right global tax strategy tailored to each client, you can position them to pursue worldwide career opportunities with maximum income and minimum taxes.

Need help navigating the world of international tax for athletes, artists, and entertainers? We have experienced professionals dedicated to both international tax and entertainment, sports, and media (ESM) ready to answer all your questions. Reach out to our International Tax Team today.

]]>- In April, the U.S. Tax Court made news when it ruled in favor of businessman Alon Farhy, who challenged the Internal Revenue Service (IRS)’s authority to assess penalties for the failure to file IRS Form 5471.

- IRS Form 5471 is the Information Return of U.S. Persons With Respect to Certain Foreign Corporations.

- Taxpayers may be interested in filing protective refunds, and they should start the process sooner rather than later—there is a statute of limitations of two years for claiming refunds.

- This case’s ruling could have reverberating effects when it comes to the IRS collecting additional penalties, but only time will tell.

On April 3, 2023, the U.S. Tax Court came to a decision in the case Farhy v. Commissioner, ruling that the Internal Revenue Service (IRS) does not have the statutory authority to assess penalties for the failure to file IRS Form 5471, or the Information Return of U.S. Persons With Respect to Certain Foreign Corporations, against taxpayers. It also ruled that the IRS cannot administratively collect such penalties via levy.

Now that the IRS doesn’t have the authority to assess certain foreign information return penalties according to the court, affected taxpayers may want to file protective refund claims, even if the case goes to appeals — especially given the short statute of limitations of two years for claiming refunds.

Our Tax Controversy team breaks down the Farhy case, as well as what it may mean for your international filings — and the future of the IRS’s penalty collections.

The case

Alon Farhy owned 100% of a Belize corporation from 2003 until 2010, as well as 100% of another Belize corporation from 2005 until 2010. He admitted he participated in an illegal scheme to reduce his income tax and gained immunity from prosecution. However, throughout the time of his ownership of these two companies, he was required to file IRS Forms 5471 for both — but he didn’t.

The IRS then mailed him a notice in February 2016, alerting him of his failure to file. He still didn’t file, and in November 2018, he assessed $10,000 per failure to file, per year — plus a continuation penalty of $50,000 for each year he failed to file. The IRS determined his failures to file were deliberate, and so the penalties were met with the appropriate approval within the IRS.

Farhy didn’t dispute that he didn’t file. He also didn’t deny he failed to pay. Instead, he challenged the IRS’s legal authority to assess IRC section 6038 penalties.

The court’s ruling

The U.S. Tax Court then held that Congress authorized the assessment for a variety of penalties — namely, those found in subchapter B of chapter 68 of subtitle F — but not for those penalties under IRC sections 6038(b)(1) and (2), which apply to Form 5471. Because these penalties were not assessable, the court decided the IRS was prohibited from proceeding with collection, and the only way the IRS can pursue collection of the taxpayer’s penalties was by 28 U.S.C. Sec. 2461(a) — which allows recovery of any penalty by civil court action.

How this court decision affects your international penalty assessments

This case holds that the IRS may not assess penalties under IRC section 6038(b), or failure to file IRS Form 5471. The case’s ruling doesn’t mean you don’t have an obligation to file IRS Form 5471 — or any other required form.

Ultimately, this decision is expected to have a broad reach and will affect most IRS Form 5471 filers, namely category 1, 4, and 5 filers (but not category 2 and 3 filers, who are subject to penalties under IRC section 6679).

However, the case’s impact could permeate even deeper. For years, some practitioners have spoken out against the IRS’s systemic assessment of international information return (IIR) penalties after a return is filed late, making it impossible for taxpayers to avoid deficiency procedures. The court’s decision now reveals how a taxpayer can be protected by the judicial branch when something is deemed unfair. Farhy took a stand, challenged the system, and won — opening the door for potential challenges in the future.

It’s uncertain as to whether the IRS will appeal the court’s decision. But it seems as though the stakes are too high for the IRS not to appeal. While we don’t know what will happen, a former IRS official has stated he expects that, for cases currently pending review by IRS Appeals, Farhy will not be viewed as controlling law yet.

The impact of the ruling is clear and will most likely impact many taxpayers who are contesting — or who have already paid — IRC 6038 penalties. It may also affect other civil penalties where Congress has not prescribed the method of assessment in the future.

How you should respond to the court’s decision

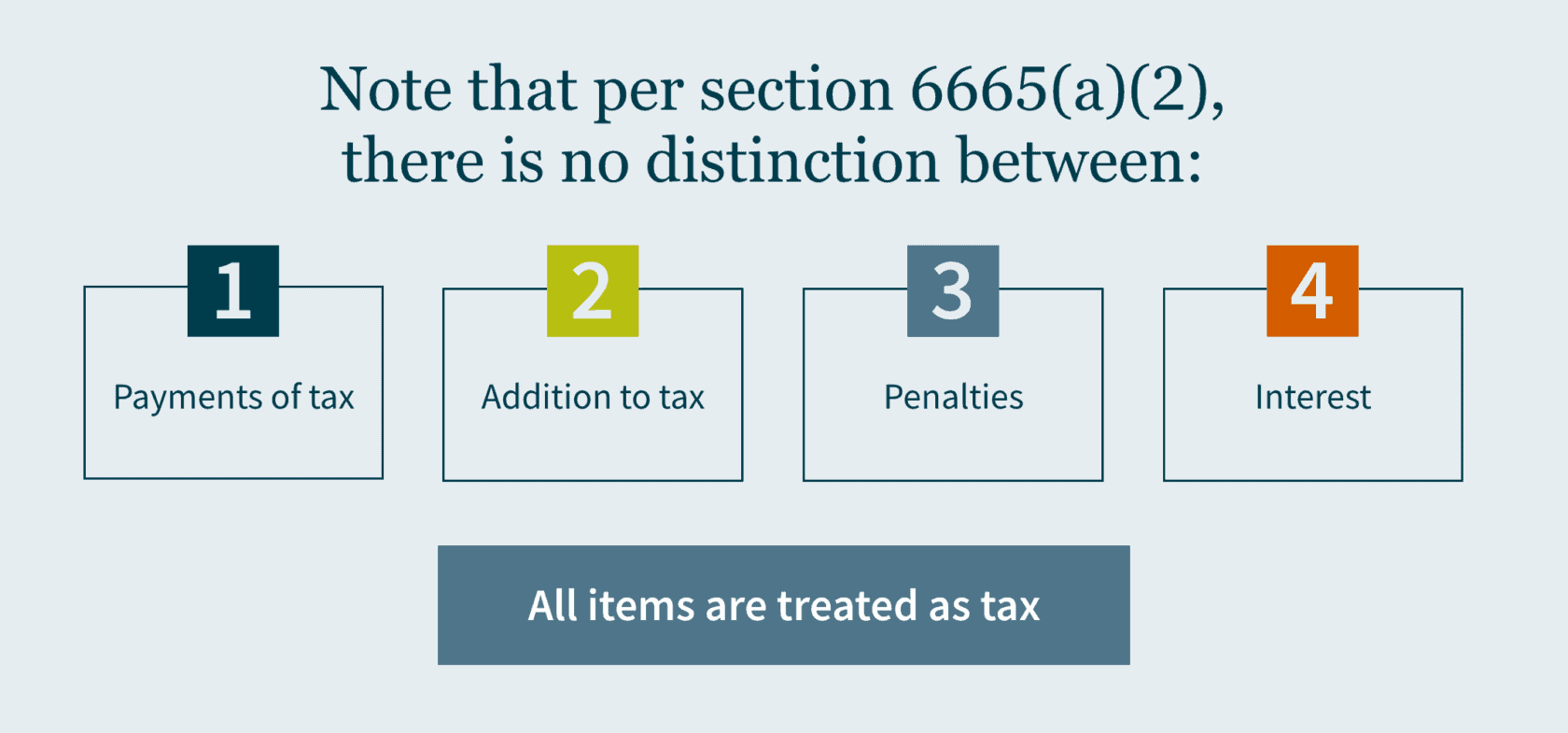

You should move quickly to take advantage of the court’s decision, as there is a two-year statute of limitations from the time a tax is paid to make a protective claim for a refund. It’s likely this legislation wouldn’t affect refund claims since that would be governed by the law that existed when the penalties were assessed. Note that per IRC section 6665(a)(2), there is no distinction between payments of tax, addition to tax, penalties, or interest — so all items are treated as tax.

If you’ve previously paid the $10,000 penalty, it’s important to file your protective claim now, unless you’ve entered into an agreement with the IRS to extend the statute of limitations, which can occur during an examination. Requesting a refund won’t ever hurt, but some practitioners believe the IRS may try to keep any penalty money it collected, even if the assessment is invalid— because, in its eyes, the claim may not be. Just know, you can file your protective claim for a refund but may not get it, at least not any time soon.

The Farhy decision could likewise be applied to other US IRS forms, such as 5472, 8865, 8938, 926, 8858, 8854, and some argue the Farhy decision may also be applied to IRS Form 3520.

How MGO can help

Only time will tell if the court’s decision will open the government up to additional criticisms for other penalty assessments. If you have paid your penalties and are wondering what your current options are, MGO’s experienced International Tax team can help you determine if you’re eligible to file a refund claim.

Contact us to learn more.

]]>

Here’s what you need to know to claim it:

- It’s a one-time abatement of any “timeliness” penalties incurred on individual income tax returns (Form 540, Form 540NR, Form 540 2EZ) for tax years beginning on or after January 1, 2022.

- It’s only available to individual taxpayers subject to personal income tax law (so estates, trusts, and fiduciaries aren’t eligible).

- It can be requested verbally or in writing starting on April 17, 2023.

- For California taxpayers who qualify for an extended 2022 income tax return due date because of the California Winter Storms (i.e., most California taxpayers), the “timeliness” penalties that would be abated through this program should not start being imposed until after the new extended due date for that tax year – October 16, 2023.

Which penalties are eligible?

Both the Failure to File Penalty (i.e., you did not file your tax return by the due date nor did you pay by the due date of your tax return) and the Failure to Pay Penalty (i.e., you did not pay the entire amount due by your payment due date) on California individual income tax returns for tax years beginning on or after January 1, 2022 are eligible for the one-time penalty abatement.

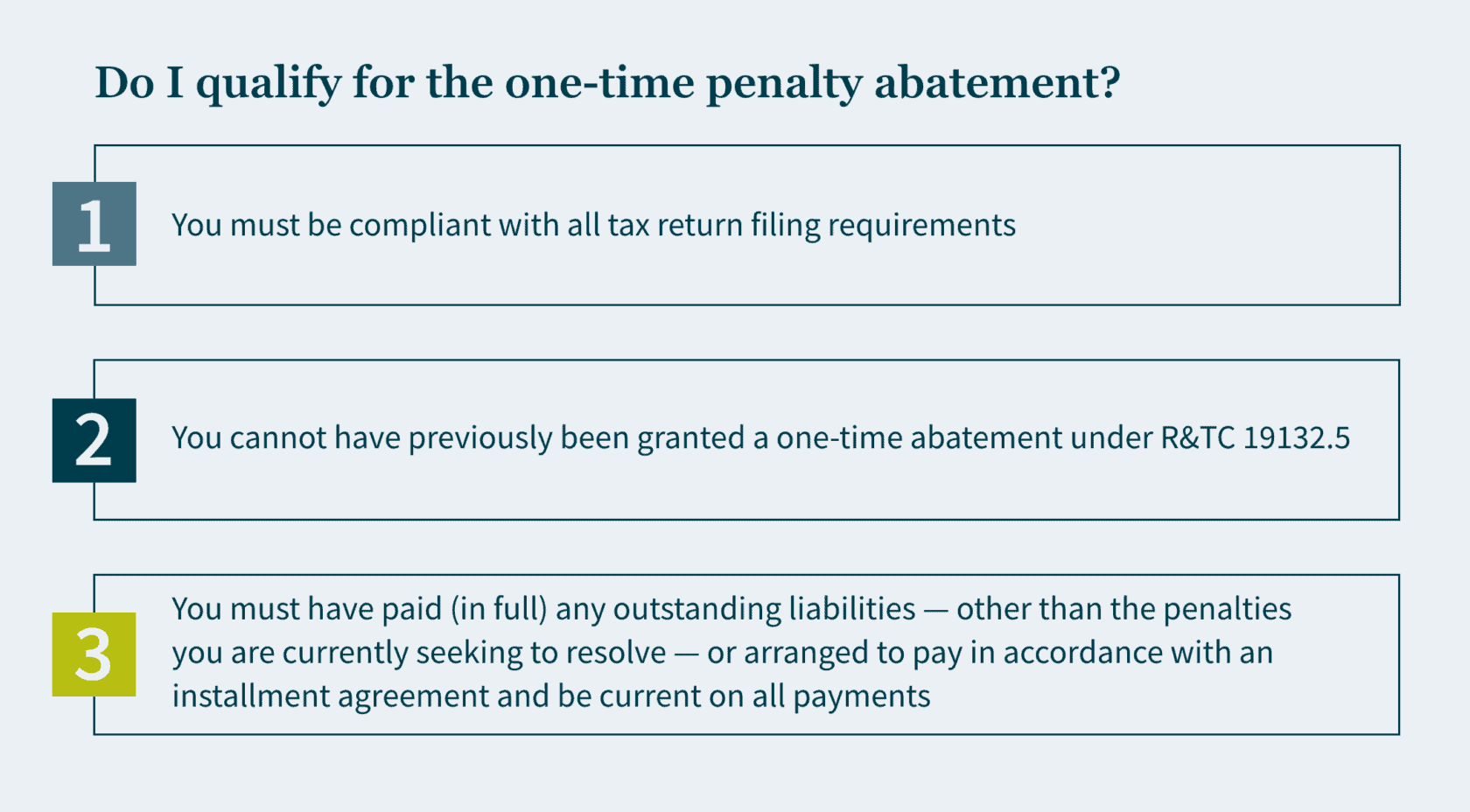

How do I qualify?

How do I request a one-time penalty abatement?

You can mail in a completed Form FTB 2918 or call the FTB at +1 (800) 689-4776 to request penalty abatement.

What if I can provide that I had reasonable cause for late filing or late payment?

If you can demonstrate that you exercised ordinary care and prudence and were nevertheless unable to file your return or pay your taxes on time, then you may qualify for penalty relief due to reasonable cause. Reasonable cause is determined on a case-by-case basis and considers all the facts of your situation.

You may request penalty abatement based on reasonable cause by mailing in a completed Form FTB 2917 or by filling out a reasonable cause request on your MyFTB online account. Penalty abatement based on reasonable cause may – depending on the circumstances – be preferable to using up your one-time penalty abatement request.

How we can help

If you need help with relief for your “timeliness” penalties or if you need help with any other state and local tax matters, please reach out to our experienced State and Local Tax team.

]]>- The Supreme Court of Washington State issued a landmark ruling maintaining the constitutionality of the state’s capital gains tax (CGT) by determining that it’s an excise tax, or a tax on a good or service (and not a property tax).

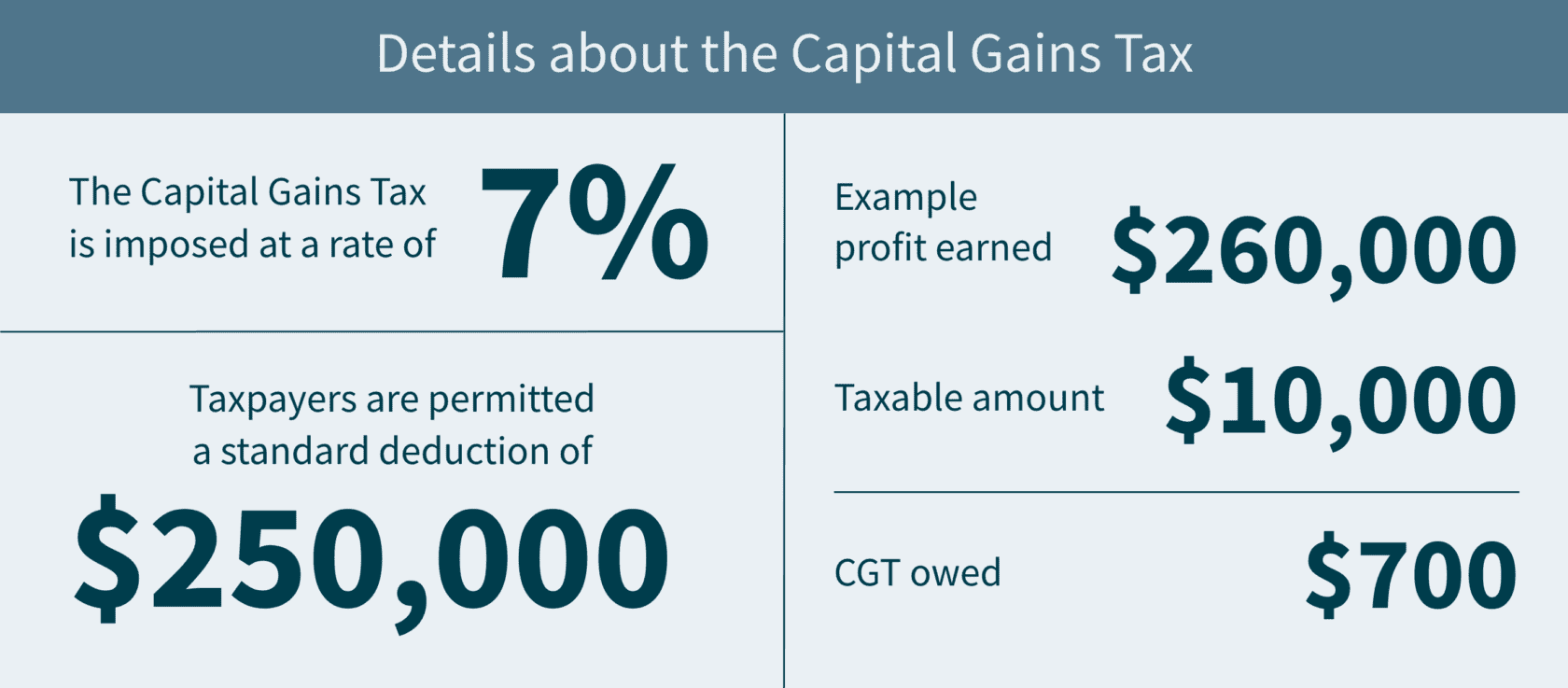

- It’s imposed at a rate of 7% and taxpayers can claim a standard deduction of $250,000.

- There are other deductions, like long-term gains from the sales of qualified family-owned small businesses and charitable contributions of more than $250,000.

- You may be able to apply a tax credit.

On March 24, 2023, the Supreme Court of Washington State (SCOWA) ruled 7-2 to uphold the constitutionality of the state’s controversial capital gains tax. Thus, by the April 18, 2023, deadline, Washington residents recognizing capital gains income (and nonresidents engaged in transactions occurring within the state) in 2022 will have to calculate this new tax and pay accordingly.

Our State and Local Tax team breaks down what you need to know about this divisive tax with an impending deadline.

The details about CGT

The CGT was created when Washington enacted Senate Bill 5096 in April 2021 with the intention of having the excise tax proceeds — projected to be nearly $415 million — fund the state’s early education and childcare programs. Charged on long-term Washington-allocated capital gains, the CGT is imposed at a rate of 7% of an individual’s federal capital gain from a sale or exchange of long-term investments that exceed $250,000. This includes stocks, bonds, businesses, and other assets.

The controversy of CGT

This bill has generated controversy since its inception — mostly because it is categorized as an excise tax and not an income tax (Washington is one of nine states that doesn’t have income tax due to limitations in the state constitution on the state government assessing a tax on “property”). As a reminder, an excise tax is a legislated tax on the sale of specific services, activities, or goods.

In March 2022, the Douglas County Superior Court in Washington deemed the CGT unconstitutional as an impermissible income tax that is only masquerading as an excise tax. The Court defined gains as income, and therefore property under the Washington Constitution, that the state impermissibly taxed at a non-uniform rate (i.e., the tax doesn’t apply to every resident equally, but only those whose profits exceed the $250,000 threshold). In the past, Washington’s Supreme Court has considered income as property — and property must be taxed at a flat rate.

Since state revenue relies on sales and business taxes, taxpayers who earn the least will end up paying a higher share of their income in tax. This notion has split public opinion. Community groups and labor unions believe the tax is not just legal, it’s necessary because of its capability to create a more equitable tax system. But organizations with business interests in mind find it to be bad public policy in addition to violating the constitution.

However, the Washington Supreme Court ruled to uphold the tax, agreeing it is constitutional as an excise tax — “levied on the sale or exchange of capital assets, not on capital assets or gains themselves.” In other words, the Court reasoned that the tax is tied not to the person’s ownership interest in the property (which would be unconstitutional), but on the transaction itself.

Calculating your tax base

Adjusted capital gains

As mentioned, the new tax is imposed on your adjusted capital gains allocated to Washington, minus allowable deductions and exemptions. First, it starts with your federal net long-term capital gain for the tax year. It’s then adjusted by adding back long-term capital losses from sales or exchanges that are exempt or not allocated to the state. Finally, you subtract your long-term capital gains from sales or exchanges that are exempt or not allocated to the state.

Deductions

There are several deductions allowed against adjusted capital gains. Individual taxpayers are permitted a $250,000 standard deduction in calculating the CGT. But married or state-registered domestic partners that file a single federal tax return collectively have only a single $250,000 deduction. For example, if you earned $260,000 in profit from selling bonds in the past year, only $10,000 would be taxed, and the CGT owed would be $700. And if you and your husband together earned $260,000 from selling bonds, you wouldn’t get to “double” the standard deduction – you’d have the same tax bill.

Additional deductions include long-term gains from the sales of qualified family-owned small businesses, and charitable contributions. Associated regulations do treat the sale or transfer of an interest in a “qualified family-owned small business” as a separate deduction from the charitable deduction. (Note that the “qualified family-owned small business” is not the same as the federal Qualified Small Business Stock (QSBS) tax exclusion — there are separate requirements). To receive the charitable deduction, you would need to contribute over $250,000, not exceeding a deduction of $100,000 in total. Consequently, if you donate $350,000, you’ll receive the maximum deduction.

Exemptions

Certain long-term capital gains and losses from sales of capital assets are not subject to the tax. These exempt items include sales or exchanges of the following types of assets:

- Livestock;

- Timber;

- Real estate, and land structures; and

- Capital assets held in IRAs, 401(k) plans, and other qualified retirement plans

Allocating your capital gains and losses

If you were living in Washington at the time of a sale or exchange of intangibles (e.g., stocks, bonds, etc.), related long-term capital gains and losses are allocated to Washington.

In addition, gains or losses from the sale or exchange of other (tangible) personal property is allocated to Washington if:

- The property was in Washington at any time during the tax year when the sale/exchange occurred,

- You were a Washington resident at the time of the sale/exchange, and

- You were “not subject to the payment of an income tax or excise tax legally imposed” by another jurisdiction* on that long-term capital gain or loss.

* Jurisdiction is defined to include not only U.S. states, political subdivisions, territories, and possessions, but also foreign countries and political subdivisions of foreign countries.

Good news: a tax credit is available

If you’re interested in applying a tax credit against this new tax, you might be able to. Any Washington capital gains tax can qualify as a credit against the Washington business and occupation (B&O) tax — given that the B&O tax includes the gain from a transaction subject to capital gains tax (because it applies to ALL gross receipts regardless of character).

In addition, a credit can be applied for an income or excise tax legally imposed by another jurisdiction on capital gains “derived from capital assets within the other taxing jurisdiction to the extent such capital gains are included in the taxpayer’s Washington capital gains.”

Filing your returns

Remember, a Washington capital gains tax return is required only if tax is owed — and it must be filed on or before the due date of your federal income tax return, including extensions. But the payment of the tax is required BY the original due date of your federal income tax return, NOT including extensions. Any filing and payments must be done online using the MyDOR portal by April 18, 2023, for most taxpayers.

How MGO can help

Keep in mind that while this tax will more than likely impact Washington residents the most, if you are a nonresident whose capital gains from the sales and exchanges of your tangible personal property is allocated to Washington, you could be affected too. Accordingly, anyone with a large gain event (other than the sale of real property) during 2022 or later years, should consider whether this tax may affect them.

MGO’s State and Local Tax team can help you prepare and file this return and manage any of the other surprises that can occur in state and local tax. Contact us if you have additional questions about how the capital gains tax impacts your finances, or if you’re interested in additional strategies to boost your tax efficiency.

]]>- When planning your estate, you must now consider the future of your digital assets.

- Digital assets can include cryptocurrency, nonfungible tokens, intellectual property rights, domain names and websites, and more.

- To make sure your digital assets can be accessed and transferred without incident, proactive planning is key.

- There are risks and challenges associated with each storage and transfer method, so you must choose the best one for you and your beneficiaries.

Estate planning is an ever-evolving process that should be continually revisited as one moves through the various phases of life. There are many facets to consider when it comes to protecting and planning for your assets. Who will get the house and other tangible assets? What about choosing beneficiaries for retirement accounts and life insurance policies?

These are questions surrounding more traditional assets, which certainly play an important role in estate planning, but in today’s technologically advanced age, these are not the only types of assets that should be considered. Digital assets play a larger role in our lives with each passing year, bringing their own unique complications and potential pitfalls to your estate plan.

It can be akin to the Wild West when it comes to the laws governing access to digital assets after one has passed, which can vary in different states or countries, as well as company to company. Read on to learn more about the proactive planning they require to be confident your estate will be administered smoothly.

What are digital assets?

Digital assets are anything created and stored digitally (i.e., on a cell phone, a server, computer, or other electronic device) that has or provides value. This can be sentimental value, as well as the more direct financial value. They can include data, videos, images, written content, and more — and, like tangible assets, they have ownership rights.

Some of the more common examples when it comes to estate planning are:

- Cryptocurrency, such as bitcoin

- Nonfungible tokens (NFTs)

- Intellectual property rights

- Domain names and websites

Accessing your digital assets

Issues can arise with digital assets if they aren’t given proper consideration in your estate plan. Without adequate planning, the executor of one’s estate may have issues locating and accessing the assets, meaning they could go untouched, never reaching the intended beneficiary or providing value to anyone.

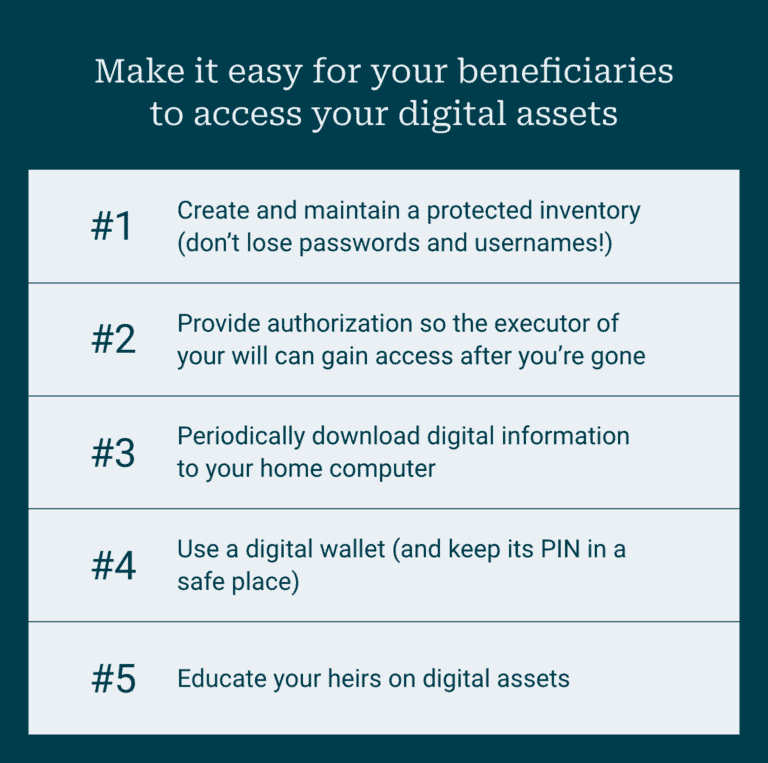

Typically, digital assets are password-protected. To ensure the fiduciary will have access after one passes, it is important to create and maintain a secure inventory of your digital assets and online accounts with their respective login information (such as passwords and usernames). If access requires a biometric reading, such as face or iris recognition or fingerprint scanning, be sure you communicate this to the service provider or administrator, so authority is not challenged, risking permanent loss of access.

However, due to federal privacy laws such as the Computer Fraud and Abuse Act and the Stored Communications Act, as well as online user agreements, it can be difficult to gain access to online accounts from service providers. To mitigate this, as part of one’s estate plan, it is advisable to prepare a statement to permit these companies to disclose the account information to whoever is executing the will and handling the estate proceedings. Unfortunately, some companies don’t always comply with intended authorization, depending on the terms and conditions of their agreement.

To best avoid control and access issues, periodically download digital information to a home computer so, with the assistance of online afterlife companies, the information can be easily restored.

Digital storage of digital assets

There is also an option to store certain digital assets in a way that is not reliant on the internet: using a digital wallet. This is also referred to as “cold storage” or a “cold wallet,” and they are not accessible via the internet. Thus, they are what most consider to be the safer approach to storing digital assets because they can’t be easily hacked or broken into. In fact, in some cases, it’s impossible to do so.

This type of storage, however, does come with its own set of risks. Because it is accessed by a password and private key (which is like a secret PIN used to confirm transactions and prove ownership of a blockchain address), if those are lost or destroyed, it could mean losing the assets forever. There is no “forgot password” option or customer service department to call for help. We advise storing the password and key in a way that is also not accessible through the internet (i.e., on a phone or computer). Storing the access information at home could also prove risky due to the chance of a break-in, house fire, or natural disaster. Securing them in a safe deposit box or making multiple copies to store in various places are recommended approaches.

Transferring your digital assets

Physically transferring digital assets to heirs can also be challenging. It is important that clear instructions are left detailing the intent for the content and ensure heirs have access to the assets as needed.

For example, if digital assets are stored on a computer, those may be transferred with the computer without proper planning. If the same person isn’t to inherit the computer and the digital assets housed there, this needs to be specified.

When working with cryptocurrency, it can be especially challenging to transfer to heirs because most exchanges do not allow a beneficiary to be named directly within the account — transferring ownership must be done via a will or legal document. Be sure to leave account information and/or private keys with a trusted source — or, as noted above, secure it in a safe place (and tell someone where it is). It is challenging enough when a family loses a loved one; difficulties in executing their estate plan will further the burden.

Another measure that can be taken to ensure estate executors and heirs know how to work with digital assets is for all parties to have familiarity with the transfer process. This can be more complicated than a basic bank transaction — each recipient will need his or her own personal digital address for each type of digital currency. Some range in excess of 100 characters and can be confusing or overwhelming to maneuver and work with.

We advise some training or practice while the original owner of the assets is still living to help alleviate these concerns. When needing to transfer larger asset values, we suggest first initiating a transfer of a very small portion of the total asset value to ensure the process is working as intended, then proceeding to repeat the process with the remainder. If a mistake is made and asset value is sent to the wrong digital address, it may be lost permanently.

MGO’s perspective on digital assets and estate planning

A proper estate plan should ensure your assets — all of them — fall into good hands after one passes. Without proper planning in this new and ever-changing arena of digital assets, the value of these assets may be lost. Maintaining an inventory of assets, accounts, and their associated passwords; backing up data; and meeting with a professional who can assist with these steps goes a long way towards ensuring your digital assets are not lost into the digital abyss.

MGO’s Private Client Services team is equipped to help you with this unique form of family wealth management. Contact us to learn more about how you can ensure your digital assets endure the test of time.

]]>We just have one question: have you hired a Certified Divorce Financial Analyst (CDFA®) yet?

The truth of the matter is, your attorney can do a lot, but they can’t provide all the guidance you need. Read on to learn the five things you don’t know about the tax implications of a divorce — and why you should hire a CDFA for your own financial security and peace of mind.

1: Be prepared for the long haul

It’s great that you and your former spouse are on good terms now, but you want to make sure you understand the divorce’s full scope of financial impact. Splitting everything down the middle sounds easy, but things are rarely simple, and the process could take longer than anticipated — especially if you want to make sure your interests are being looked after. As soon as you’ve decided on a divorce, equip yourself with financial knowledge by hiring a CDFA. If you know your interests, you have control over how they are handled, giving you the upper hand, preventing you from being blindsided later — no matter how long the “long haul” ends up being.

2: Know your long-term tax liabilities for the assets you’re divvying up pre-divorce

Whether it is interest-free bonds, the house you raised your kids in, your retirement fund, or a timeshare to Walt Disney World, there will be tax consequences and implications for the assets you divide between the two of you.

Often, people look at the fair market value of jointly owned property instead of a property’s tax basis, assuming that this is enough to go on when divvying up. But let’s say you have two different assets you’re splitting “fairly”: stock options and undeveloped land (you never did get around to building that second home together … ). Both assets are valued at the same amount. So, naturally, it makes sense for you to get one, and your spouse to get the other. That is, until one of you sells your asset, and you get a hefty tax bill. This is considered a tax carryforward, and you should understand them before the divorce is finalized.

Tax carryforwards are important to consider when dividing assets because of the tax consequences — and planning opportunities — that could exist in the future. They include carryovers like:

- net operating loss carryovers,

- business tax credit carryovers,

- capital loss carryovers,

- excess business loss carryovers,

- investment interest expense carryovers, and

- suspended passive activity loss carryovers.

Tax regulations give you a great framework, but unfortunately, they do not tell you how these carryovers should be allocated between you and your spouse; instead, you must decide. A CPA should be leveraged to identify the tax considerations, as well as any potential impact they could have on each spouse.

3: Rely on a seasoned professional to gain the full financial picture

You don’t want to think this way, but you need to be prepared for the fact your spouse may have been getting away with unsavory tax practices you were not aware of when you were married. And if so, you need someone on your side. A CDFA can help you gain the clarity and understanding you will need to strategize so you are satisfied with the choices you make during a divorce long after the marriage is dissolved.

For example, imagine your spouse purchased a Mercedes-Benz G-Wagon SUV during the marriage. At the time, you thought everything was above board. But your analyst uncovers that the G-Wagon’s full value was written off because of the weight, thus showing a lower annual income — negatively impacting you and your likelihood of a fair division of property and income.

To combat this, your CDFA would provide a lifestyle analysis. This entails scrutinizing everything from tax returns to credit card transactions, which could uncover hidden trails of unreported income or assets in the uncovered discrepancies. The party’s liquid assets may not support their current standard of living with business class flights abroad and stays at the newest Dorchester Collection hotel. An analysis would show the warning signs.

The examinations and reports gathered by an analyst can show both you and your attorneys a clear picture of the financial matters you’re dealing with on both sides, which can contribute to an equitable resolution between parties. This applies whether you settle or go to court. If it’s the latter, your CDFA can be an invaluable witness on your “team.”

4: Conduct a financial analysis early in the divorce process

As we mentioned, projecting financial impacts for both the short- and long-term is critical to understanding how you will be affected by the divorce. Have your CDFA prepare an independent analysis of the tax consequences under different scenarios, so you know possible outcomes. This will not only create a framework for you moving forward, but it will prevent your partner from successfully sneaking around and attempting to pull the wool over your eyes. These financial analyses can also include a review of the last income tax return filed by your spouse.

5: Remember, this service pays for itself

You may be tempted to forgo a CDFA in the throes of your divorce, thinking it’s just another bill to pay. But the truth is, the service they provide does pay for itself. If fraud or misuse is identified at any point in the divorce process, you will save yourself money in the long run having prepared for these tax liability scenarios, and when it comes to figuring out your assets, you will be able to see beyond the current fair market value, so you won’t be blindsided later on.

Our perspective on hiring a CDFA for your divorce

At the end of the day, think of the financial side of your divorce like a puzzle: you need each and every piece in order to complete the picture. While you may be on good terms with your spouse now, things are rarely simple when money is involved. It is far better to see the puzzle in its entirety now instead of picking up a piece that got edged under the sofa later and discovering you’ve been misled or treated unfairly.

Hiring a CDFA purges the emotion from the situation, which is exactly what you must do to ensure your financial security.

At MGO, we can help. Our Private Client Services practice puts you and your story first.

]]>Specific scams that mask as abusive or fraudulent tax avoidance strategies to be aware of include concealing assets in offshore accounts and improper reporting of digital assets, manipulation of high-income taxpayers to file their tax returns, abusive syndicated conservation easements, and abusive micro-captive insurance arrangements. Read more to round out the annual list for the 2022 filing season.

Tips for taxpayers on emerging scams

To avoid compromising yourself with these “too good to be true” schemes, taxpayers should stay wary, as these scams adopt a wide range of communication methods, including:

- Emails

- Phone calls

- Social media posts

- Targeted online advertisements

You must also consider each source before putting any of these arrangements on your tax returns — because ultimately, you are the one responsible for what is on the return, not the promoter who reached out to you and made a promise they failed to uphold. To mitigate risk, an anxious taxpayer should turn to trustworthy tax professionals to assist with their returns.

Read on to learn about these Dirty Dozen scams targeted primarily to high-net-worth individuals who may be trying to knowingly — or unknowingly — avoid filing.

Scam #9: Concealing Assets in Offshore Accounts and the Improper Reporting of Digital Assets

We hear Switzerland is beautiful this time of year … and so do some high-net-worth individuals looking to conceal their assets in offshore accounts (and yes, that does include cryptocurrency and other digital assets). As more taxpayers look to complex international tax avoidance schemes, the IRS is more determined than ever to “protect the integrity of the U.S. tax system” by enforcing tax responsibilities.

Whether it entails offshore banks, brokerage accounts, nominee entities, employee leasing schemes, foreign trusts, structured transactions, or private annuities, all are designed to hide the true owner of an account — which is illegal, considering U.S. taxpayers are taxed on all the income they make, not just what they keep in the country. But scammers know you may not want to give up some of your hard-earned assets to Uncle Sam. So, what do they do? They sell you a convincing story: you can easily evade the government and hide your assets through digital asset holdings; they claim these are “undetectable by tax authorities.” The catch? They are definitely detectable. By believing these fraudsters, you run the risk of being criminally charged or penalized, so in the end, it is better to report your assets — yes, all of them — when you file.

Scam #10: High-Income Individuals Who Don’t File Tax Returns

Believe it or not, there are some taxpayers who choose to just … not file a tax return. And believe it or not, there are scamming professionals out there aiming to convince you this is a good idea. The IRS takes this seriously. If you are considering this option, remember the Failure to File Penalty is higher than the Failure to Pay Penalty, meaning you are better off filing an accurate, timely return (and setting up a payment plan, if you are concerned about that) rather than not filing and hoping you get out of paying whatever taxes you owe.

Scam #11: Abusive Syndicated Conservation Easements

In this scam, dishonest promoters manipulate a part of the tax law that allows for conservation easements by inflating appraisals of underdeveloped land (i.e., the guise of a real estate investment) and engaging in bogus partnerships without a business purpose. These “deals” rarely help you out; instead, they benefit the promoters, who charge high fees, and clog the tax system with fraudulent tax deductions. (In the last five years, the IRS determined billions of dollars of deductions were wrongly claimed!) And if you are caught — which, you should expect to be, because the IRS takes a microscope to every single one of these “deals” — you can expect large fines and potential time in court.

Scam #12: Abusive Micro-Captive Insurance Arrangements

A high priority for the IRS, this scam sees professionals like accountants and wealth planners convince entity owners to pay for what they believe to be insurance coverage against unlikely events, events that are already being covered, or disingenuous business needs. Complete with sky-high premiums, the abusive structure does the opposite of protecting your organization’s tax safety — it opens you up to more risk as a ”micro-captive” to these “professionals” taking advantage of you. Be on the lookout for an offshore version of this too.

Consequences of falling for a Dirty Dozen scheme

It is important for taxpayers who have already taken part in transactions like these — or those who are thinking about doing so — to consult a tax professional before claiming any tax benefits they think they are owed.

Those taxpayers who have already claimed the purported tax benefits of one of these four “Dirty Dozen” arrangements on a tax return should file an amended return and go to an independent professional for guidance. If necessary, the IRS will examine the tax benefits from transactions like the ones depicted in the list and inflict penalties related to accuracy ranging from 20% to 40%, or a civil fraud penalty of 75% on any taxpayer who underpaid.

Our perspective on the latest batch of “Dirty Dozen” scams

This is not, of course, an exhaustive list of every scam the IRS has its eye on this year. But it does include some of the more common trends. The best advice we can give? If something looks too good to be true … it probably is. Consult your tax professional for guidance and know that it is in your best interest to stay aware of these nefarious arrangements, so you do not fall susceptible to additional penalties.

And remember, you cannot hide income from the IRS!

MGO’s Tax team brings more than 30 years of experience and is well versed in reviewing your return for compliance. We also stay up to date on the risks, pitfalls, and warnings issued by the IRS so you don’t have to. If you think you have been involved in or are in the process of being involved in one of the Dirty Dozen scams, we can help. Contact us today.

]]>Tips for taxpayers on emerging scams

To avoid compromising yourself with these “too good to be true” schemes, taxpayers should stay wary, as these scams adopt a wide range of communication methods, including:

- Emails

- Phone calls

- Social media posts

- Targeted online advertisements

You must also consider each source before putting any of these arrangements on your tax returns — because ultimately, you are the one responsible for what is on the return, not the promoter who reached out to you and made a promise they failed to uphold. To mitigate risk, an anxious taxpayer should turn to trustworthy tax professionals to assist with their returns.

Read on to learn which scams are next on the Dirty Dozen list.

Scam #6: Offer in Compromise “Mills”

This scam, known as an Offer in Consequence (OIC) mill, targets taxpayers who struggle to pay their taxes and may face debt as a consequence for their delinquency or noncompliance. It is commonly seen right after the filing season concludes as these taxpayers stress about what they might owe. What is the OIC? It is an agreement between you and the IRS that resolves your tax debt, and these mills claim to be able to settle your tax debt on the cheap. But the reality is, only the IRS has the authority to settle or compromise your federal tax liabilities, and it is based on certain circumstances. Utilizing local advertising, the mills boast they can get you a great deal, even if they know you do not actually qualify — and if they do get you a “deal,” it is the same deal you would have received if you had worked directly with the IRS (and if you had gone to the IRS first, you would not have paid potentially thousands in fees to these fraudsters).

Before you trust an OIC mill or invest your time in submitting an offer yourself, check out the IRS’s Offer in Compromise Pre-Qualifier Tool to determine your eligibility. The site also has a host of resources to utilize when it comes to tackling these offers — the right way.

Other dishonest tax preparation tactics include:

- Ghost preparers who do not sign the tax returns they prepare for you,

- Inflated refund promises, and

- Preparers who:

- Only take cash,

- Do not provide you with a receipt,

- Fabricate income so you qualify for certain tax credits,

- Direct your refunds into their accounts, or

- Claim fake deductions so the refund is bigger (which they, in turn, get a cut of).

Scam #7: Suspicious communications in all forms, including text, email, and by phone

These scams strive to make you feel fearful or surprised so scammers can trick you into divulging your personal information, which they can then steal to file fake tax returns and access financial accounts. Whether it entails a phone call, a text message, or an email, these methods have been around for years, and it is no question why they are still in circulation today: they work. And while they evolve and change depending on what is going on in the country (many currently reference stimulus checks or the COVID-19 pandemic), these are the basic methods.

Text message scams:

sent to smartphones and sometimes include website links that can seem reputable — but they are not. Remember, the IRS will not send you text messages regarding personal tax issues, and they definitely do not reach out via social media. If you receive a text that claims to be from the IRS, you can report it by taking a screenshot of the message and emailing it to phishing@irs.gov along with the date, time, and time zone you received it and your phone number. And, it may go without saying, but we are going to say it anyway: do not open the attachments or links in these messages!

Email scams:

work similarly to text message scams, but they appear in your inbox instead of your messages. Just like texts, the IRS will not contact you by email to request personal information — they use regular mail. You can report suspicious emails to the IRS at the email address above.

Phone scams:

have several different pre-recorded voicemail scripts, but nearly all are threatening and include language meant to scare you into answering with your personal information. Threats include issuing a warrant for your arrest if you ignore them, getting deported, or revoking your license. Be wary of any and all phone numbers you do not recognize; these scammers can fake caller ID numbers, so you are unable to check who is calling.

Here are some things the IRS will not do over the phone:

- Ask for your credit or debit card information,

- Make “right now” demands for you to pay what you owe,

- Threaten to call the authorities if you do not pay, and

- Demand you pay immediately using methods like a gift card or wire transfer.

Scam #8: Spear phishing attacks to steal identities

Spear phishing deploys an email scam aimed at stealing a professional firm’s software credentials so the scammers can steal data and identities to file tax returns for refunds, which they will then pocket. The most recent phishing email convincingly utilizes the IRS logo with a subject line telling you action is required because your account has been put on hold. If you click on the link within the body of the email, malware could be downloaded to your computer, or you will be directed to a site with popular tax software preparation providers’ logos. Once you select a logo, you will be asked to input your credentials (which will be stolen and most likely used to file fraudulent tax returns).

The IRS labels spear phishing as a very serious problem because it can be “tailored to attack and steal the computer system credentials of any small business with a client data base,” including tax professionals’ firms. Their suggestion? Never let your guard down when it comes to your cybersecurity. Any client-based enterprise can be targeted.

Consequences of falling for a Dirty Dozen scheme

It is important for taxpayers who have already taken part in transactions like these — or those who are thinking about doing so — to consult tax professionals before claiming any tax benefits they think they are owed.

Taxpayers who have already claimed the purported tax benefits of one of these four “Dirty Dozen” arrangements on a tax return should file an amended return and go to an independent professional for guidance. If necessary, the IRS will examine the tax benefits from transactions like the ones depicted in the list and inflict penalties related to accuracy ranging from 20% to 40%, or a civil fraud penalty of 75% on any taxpayer who underpaid.

Our perspective on the latest batch of “Dirty Dozen” scams

This is not, of course, an exhaustive list of every scam the IRS has its eye on this year. But it does include some of the more common trends. The best advice we can give? If something looks too good to be true … it probably is. Consult your tax professional for guidance and know that it is in your best interest to stay aware of these nefarious arrangements, so you do not fall susceptible to additional penalties.

Stay tuned for more deep dives into the IRS’s Dirty Dozen list.

And remember: if you owe taxes, the IRS will almost always mail you a bill first!

MGO’s Tax team brings more than 30 years of experience and is well versed in reviewing your return for compliance. We also stay up to date on the risks, pitfalls, and warnings issued by the IRS so you don’t have to. If you think you have been involved in or are in the process of being involved in one of the Dirty Dozen scams, we can help. Contact us today.

As listed in the IRS’s news release, the first scams announced involve charitable remainder annuity trusts, Maltese individual retirement arrangements, foreign captive insurance, and monetized installment sales. Soon, the IRS will release information about eight more scams, including some that target the average taxpayer and some that pertain to high-net-worth individuals.

Tips for taxpayers on emerging scams

To avoid compromising themselves with these “too good to be true” tax-saving schemes, taxpayers should stay wary, as these scams adopt a wide range of communication methods ranging from seemingly harmless emails to direct phone calls to alluring targeted online advertisements. They should also consider each source before putting any of these arrangements on their tax returns — because ultimately, they are the ones who are responsible for what is on the return, not the promoter who reached out to them and made a promise they did not uphold. To mitigate risks, it is crucial that anxious taxpayers should turn to trustworthy tax professionals to assist with their returns.

Read on to learn about each of the four now-public Dirty Dozen scams.

Scam #1: Use of Charitable Remainder Annuity Trust (CRAT) to Eliminate Taxable Gain

In this transaction, taxpayers wrongly claim the transfer of appreciated property assets to a CRAT, giving the assets a bump in fair market value, as though they had been sold to a trust. Then, after actually selling the property (and not netting a gain because of the claimed “step-up”), the CRAT uses the proceeds to buy a single premium immediate annuity (SPIA). The beneficiary then reports a small amount of the annuity received from the SPIA as income and mistreats the remaining payment as an excluded portion representing a return on investment — with no associated tax due, which is a misapplication of the rules under sections 72 and 664.

Scam #2: Maltese (or other Foreign) Pension Arrangements Misusing Treaty

These transactions see U.S. citizens or residents try to avoid paying taxes by contributing to certain foreign individual retirement arrangements in Malta (but it is possible this pertains to other foreign countries too). A warning sign here is the individual’s lack of a “local” connection because local law allows contributions in a form other than cash, or just does not limit the amount of contributions at all by reference to income earned through employment or self-employment. The foreign arrangement is then named as a “pension fund” for U.S. tax treaty purposes, and the thus the taxpayer wrongly claims an exemption from their income tax on earnings in and distributions from the foreign arrangement.

Scam #3: Puerto Rican and Other Foreign Captive Insurance

Here, the owners of U.S. closely held entities engage in an insurance arrangement with someone from Puerto Rico (or another foreign corporation) who has segregated asset plans or cell arrangements. Typically, the U.S. owner has a vested financial interest in these plans and claims deductions for the insurance coverage provided by a fronting carrier, reinstating the “coverage” with the foreign corporation. There are several things to look for here: non-arm’s length pricing, no actual business purpose for entering the arrangement, and implausible risks covered.

Scam #4: Monetized Installment Sales

These transactions violate the installment sale rules under section 453 by a seller who receives the proceeds from a sale (in the same year of the sale) through purported loans. This happens when the seller enters in a contract to sell appreciated property to a buyer for cash, and then intends to sell that same property to an intermediary in return for in installment note. The intermediary then plans to sell the property to a buyer and receives the cash purchase price. The seller ends up receiving an amount equal to the sales price minus the transactional fees in the form of a purported loan that is unsecured.

Consequences of falling for a Dirty Dozen scheme

It is important for taxpayers who have already taken part in transactions like these — or those who are thinking about doing so — to consult tax professionals before claiming any tax benefits they think they are owed.

Those taxpayers who have already claimed the purported tax benefits of one of these four “Dirty Dozen” arrangements on a tax return should take the proper steps to amend their actions. These include filing an amended return and going to an independent professional for guidance. If necessary, the IRS will examine the tax benefits from transactions like the ones depicted in the list and inflict penalties related to accuracy ranging from 20% to 40%, or a civil fraud penalty of 75% on any taxpayer who underpaid.

Our perspective on the “Dirty Dozen”

This is not, of course, an exhaustive list of every scam the IRS has its eye on this year. But it does include some of the more common trends that appear like they will peak this year as returns are filed. The best advice we can give? If something looks too good to be true…it probably is. Consult your tax professional for guidance and know that it is in your best interest to stay aware of these nefarious arrangements, so you do not fall susceptible to additional penalties.

MGO’s Tax team brings more than 30 years of experience and is well versed in ensuring your tax returns are compliant. We also stay up to date on the risks, pitfalls, and warnings issued by the IRS so you don’t have to. If you think you have been involved in or are in the process of being involved in one of the Dirty Dozen scams, we can help. Contact us today.

]]>How is interest calculated on unpaid taxes?

Interest accrues on any unpaid tax from the due date of the return until the date of payment in full. The interest rate is determined quarterly. Interest compounds daily and is charged on the sum of all outstanding taxes and penalties.

Understanding overpayment and underpayment rates

The overpayment rate is the sum of the federal short-term rate plus 3 percentage points. For corporations, it is the federal short-term rate plus 2 percentage points. For the portion of a corporate overpayment of tax exceeding $10,000, it is the federal short-term rate plus 0.5%.

The underpayment rate is the sum of the federal short-term rate plus 3 percentage points, except underpayments for large corporations is the sum of the federal short-term rate plus 5 percentage points.

Starting July 1, the new increased rates will be:

- 5% for overpayments (4% for corporations),

- 2.5% for the portion of corporate overpayment exceeding $10,000,

- 5% for underpayments, and

- 7% for large corporate underpayments.

What are the most common penalties?

Failure to Pay Penalty: If a return is filed but the tax owed was not paid on time, a late payment penalty will be imposed at .5% of the unpaid taxes for each month, or the part of the month the taxes remained unpaid. The penalty will not exceed 25% of the unpaid tax amount. Full monthly charges are applied even if taxes are paid in full before the end of the month.

Failure to File Penalty: Based on how late the tax return is filed and the amount of unpaid tax as of the original payment due date, this penalty is 5% of the unpaid taxes for each month, or the part of the month that a tax return is late. The penalty will not exceed 25% of the unpaid tax amount.

Combined Failure to Pay and Failure to File Penalty: If both penalties are applied in the same month, the Failure to File Penalty will be reduced by the amount of the Failure to Pay Penalty applied in that month. Based on the current penalty percentages, the late payment penalty would remain at .5%, and the late filing penalty would be reduced to 4.5%.

Substantial Underpayment Penalty: This penalty applies to (1) individuals if the tax liability is understated by 10% of the tax required to be shown on the return or $5,000, whichever is greater or (2) to corporations, if the tax liability is understated by 10% (or, if greater, $10,000) or $10,000,000. The penalty is 20% of the portion of the underpayment of tax that was understated on the return.

Negligence or Disregard of Rules or Regulations Penalty: At 20% of the portion of the underpayment of tax, this occurs due to negligence (lack of a reasonable attempt to follow the tax laws) or a disregard for the tax rules, meaning the taxpayer carelessly, recklessly, or intentionally ignores the tax laws.

Underpayment of Estimated Tax Penalty: This penalty applies to corporations or individuals that do not make enough estimated tax payments or are late in paying them when required. The penalty is based on (1) the amount of the underpayment, (2) the period when the underpayment was due and underpaid, and (3) the interest rate for underpayments published quarterly by the IRS. To avoid it, corporations can make quarterly estimated tax payments if they expect to owe $500 or more in estimated tax when they file their return. Individual taxpayers can avoid it if they owe less than $1,000 in tax after subtracting withholding and refundable credits, or if they paid withholding and estimated tax of the lesser of at least 90% of the tax for the current year or 100% of tax shown on the prior year’s return.

Can a penalty or interest be removed (abated)?

The IRS can remove or reduce some penalties if the taxpayer acted in good faith and can show reasonable cause for the failure to meet their tax obligations. However, by law, the IRS cannot reduce or remove interest unless the penalty is removed or reduced.

Reasonable cause is based on all the facts and circumstances of each situation, and the IRS will consider any reason establishing that a taxpayer used all ordinary business care and prudence to meet their federal tax obligations but were unable to do so. It is important to note that lack of funds is not a reasonable cause for failing to file or pay on time — but it could be considered reasonable cause for the failure-to-pay penalty.

The IRS’s First Time Penalty Abatement Policy (FTA) can provide relief from a penalty if a taxpayer has not incurred penalties previously. To qualify under this policy, the taxpayer (1) did not previously need to file a return or had no penalties for the last 3 years prior to the tax year in which the penalty was received, (2) is current on all required returns or extensions of time to file, and (3) has paid or arranged to pay any tax due.

What options are available if a taxpayer cannot pay the taxes due?

Short Term Payment Plan: This plan is not available for businesses unless it is a sole proprietor or an independent contractor. There is no setup fee, and the balance must be paid within 180 days. A short-term payment plan is available for individuals if less than $100,00 in combined tax, penalties and interest is due. Penalties and interest accrue until the balance is paid in full. T

Long Term Payment Plan (Installment Agreements): An installment agreement is available for individuals if less than $50,000 is owed or for a business if less than $25,000 is due in combined tax, penalties and interest and all required returns are filed. Penalties and interest accrue until the balance is paid in full. The maximum term for most installment plans is 72 months.

If a taxpayer pays less than the full amount due, how is the partial payment applied?

If a taxpayer makes a partial payment accepted by the IRS, and the taxpayer provides specific written directions as to the application of the payment, then the IRS will apply the payment as instructed by the taxpayer. If the taxpayer does not provide instructions with the partial payment, then the partial payment is applied to periods in order of priority that the IRS determines is in its best interest. The payment will be applied to satisfy the liability in successive periods in descending order of priority until the payment is absorbed. If the partial payment applied to a period is less than the liability for the period then the payment will be applied to the tax, then penalty and finally interest, until the amount is exhausted (Rev. Proc. 2002-26).

Example: The taxpayer incurs the following tax deficiency, penalties and interest:

Year 1: Tax: 6,000, Penalty: $1,800, Interest: $1,200

Year 2: Tax: 7,000, Penalty: $ 0, Interest: $ 1,500

The IRS agrees that the taxpayer can satisfy the total liability of $17,500 for a payment of $15,000. There is no agreement as to the allocation of the payment and the taxpayer does not provide any directions for application of the partial payment. The payment is first applied to the Year 1 tax, penalty, and interest (a total of $9,000), leaving $6,000 to be applied to Year 2. The remaining amount is completely absorbed by the tax due for Year 2, which results in the payment of interest in Year 1, but not for Year 2.

However, if the partial payment accepted by the IRS is less than the total of tax and penalties due in both years and there is no agreement regarding the application of the partial payment, then nothing is allocated to the interest in either year. For example: following the amounts listed above, if the partial payment was $12,000 instead, then the entire amount is applied to the tax and penalty in Year 1 (a total of $7,800) and the remaining amount of $4,200 is applied to the Year 2 tax due. None of the partial payment would be applied to the interest in either year.

Final thoughts

Delaying paying (or paying down) any outstanding balances with the IRS will cost you more than in prior years. If you are filing for an extension and planning on simply paying with the return in the fall, remember that, in addition to penalties, you will owe interest on any unpaid tax from the return’s due date until the day you actually make the payment — and interest will be compounded daily.

If you have questions and want to ensure you avoid being hit with tax penalties and interest, please reach out to MGO’s Tax team for assistance. You can rely on us to help you mitigate the impact of the interest rate increase.

]]>