- California now has a new tax credit called the High-Road Cannabis Tax Credit (HRCTC) available for eligible cannabis retailers and microbusinesses.

- The credit is available for tax years starting after January 1, 2023, through December 31, 2027, and can be applied against current year (and future) income taxes.

- To claim it, you must make a “tentative credit reservation.”

- Expenditures that qualify include wages for full-time employees; safety-related equipment, training, and services; and workforce development and safety.

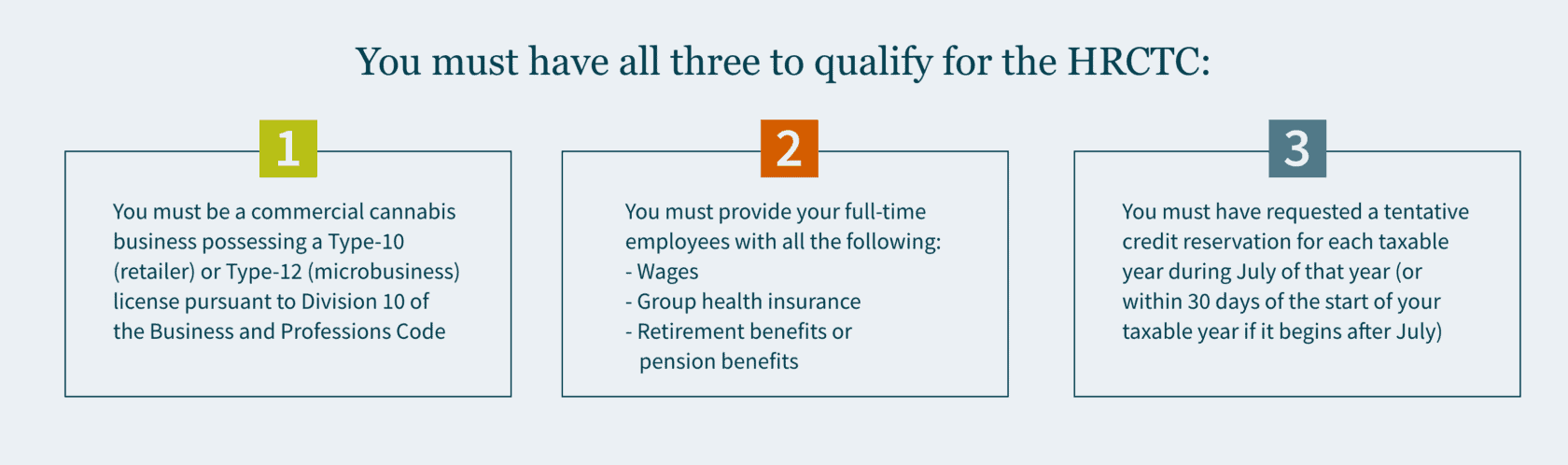

While the cannabis industry in California has been struggling on many levels, tax credit relief has come in the form of excise tax changes for distributors and has now arrived for retailers. The High-Road Cannabis Tax Credit is a new tax credit from the California Franchise Tax Board (FTB) available for cannabis retailers or microbusinesses for taxable years beginning January 1, 2023, through December 31, 2027. In order to capitalize on this opportunity, eligible calendar-year taxpayers must make a tentative credit reservation during the month of July to claim the credit on their 2023 CA income tax return.

Who qualifies for the HRCTC

To be eligible, you would need to meet three basic requirements.

Which expenditures qualify for the HRCTC

There are several types of expenditures eligible for the credit with specific parameters that you would need to meet to qualify for them. Qualified expenditures are amounts that you have paid or incurred for any of the following expenses.

Wages for full-time employees

Not every employee has to meet these requirements — but for those that do, their wages count as a qualified expenditure. First, full-time employees must be paid for no less than an average of 35 hours per week — or they must be a salaried employee paid compensation for full-time employment.

In addition, full-time employees must be paid no less than 150% ($23.25) but no more than 350% ($54.25) of the state minimum wage. To meet the 150% minimum wage requirement, you may include the following employee benefits in qualified wages: group health insurance, childcare support, employer contributions to employer-provided retirement plans, or contributions to employer-provided pension benefits. But if you pay employees wages that surpass more than 350% of the state minimum wage, those wages are not considered a qualified expenditure.

Safety-related equipment, training, and services

Expenditures related to safety, training, and providing services can also qualify if they meet the following criteria:

- Equipment primarily used by the employees of the cannabis licensee to ensure personal and occupational safety, or the safety of the business’s customers.

- Training for nonmanagement employees on workplace hazards. (This includes safety audits, security guards, security cameras, and fire risk mitigation.)

Workforce development and safety

Qualified training for your employees includes:

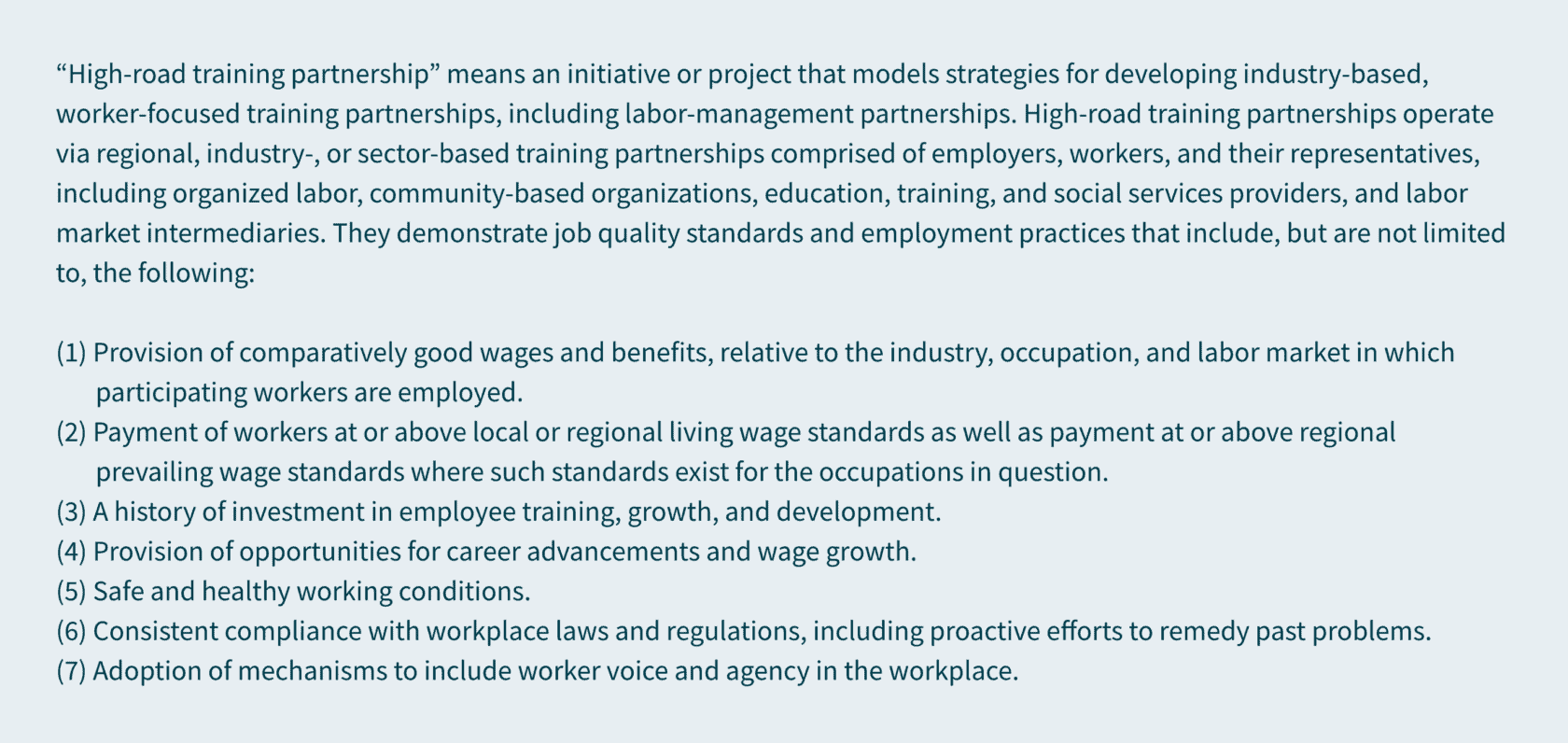

- Joint labor management training programs

- Membership in a joint apprenticeship training committee registered by the Division of Apprentice Standards, and a state-recognized “high-road training partnership” (as defined in Section 14005 of the Unemployment Insurance Code).

Available credit

The amount of available credit is equal to 25% of qualified expenditures. The aggregate credit that can be claimed by each taxpayer (as determined on a combined reporting basis) is a maximum of $250,000 per year. Any unused credit can be carried over to the following eight taxable years. Availability is limited as the total cumulative amount of HRCTC available to all taxpayers is $20 million.

To claim the HRCTC on your California tax return, you must reduce any deduction or credit otherwise allowed for any qualified expenditure by the amount of the HRCTC allowed.

How do I make a tentative credit reservation — and when?

You must make a tentative credit reservation (TCR) with the FTB to claim the credit. This reservation must be made online and once you’ve done so, you’ll receive an immediate confirmation. FTB currently reports that the system will be up and running by July 1, 2023, but you can start preparing now.

How we can help

The HRCTC is a valuable tax credit opportunity for any commercial cannabis business operating in California. Determining if you qualify and calculating how much you can save could be complex. Our extensive experience in cannabis, cannabis tax, and state and local tax enables us to help you take advantage of this tax credit so you can stay focused on thriving in this ever-growing, culture-shaping industry.

Reach out to MGO’s State and Local Tax team to find out whether you qualify for this tax credit opportunity and determine how much you could potentially save.

]]>

To provide some clarity on this new fee for cannabis retailers located in Colorado, we answer some of your commonly asked questions.

What exactly is the new retail delivery fee charge? What kind of sale is it collected on?

As we stated, this new charge impacts tangible property, including cannabis products, that are delivered to a location within the state of Colorado by a vehicle. It is $0.27 per sale (regardless of the number or value of the items delivered).

And … cannabis counts as “tangible personal property?”

It does. CDOR defines tangible personal property as “all goods, wares, merchandise, products and commodities, and all tangible or corporeal things and substances that are dealt in and capable of being possessed and exchanged.” While several things are exempt from sales tax, cannabis products are not included — thus, this delivery fee applies to cannabis too.

What if I use a third-party vehicle to deliver my goods?

Whether you use a company-owned vehicle or a third-party organization, every seller must collect this 27-cent fee from its customers. The company facilitating the transport of cannabis products bears no responsibility for the fee.

Are there any sales that are exempt from this new charge? What about sales of cannabis otherwise exempt from the Colorado Delivery Fee?

Yes, wholesale transactions (or other tax-exempt purchases) don’t have to collect the retail delivery fee. This includes wholesale cannabis deliveries, making them exempt from the delivery fee. Sales of exempt tangible personal property (i.e., items for resale) will be exempt from the fee unless one item of tangible personal property subject to sales or use tax is included in the delivery. In that case, the delivery fee would apply.

Who is responsible for the fee?

Both the buyer and the seller, in a way — as the seller of the item(s) being delivered, you must collect the fee. But the customer is responsible for paying the fee once you have charged them — and it must be listed on your invoice as a separate item (shown on the receipt as “retail delivery fees”), so there is full transparency.

Do I have to register for this?

Businesses that have a sales tax collection obligation are required to also collect the delivery fee in addition to sales tax. If your business has already registered for sales and use tax, then you will automatically be registered for this additional retail delivery fee (with a Retail Delivery Fee Account). As mentioned above, third party delivery companies that would not otherwise charge sales tax, are not subject to this new fee.

Can I report this new fee on the same return as the Colorado sales and use tax? When is it due?

The fee must be reported on its own return called the Retail Delivery Fee Return (DR 1786), which is separate from the state-wide Colorado Sales and Use Tax System (SUTS) return or other local Colorado returns. However, both are due on the same date, or by the 20th day of the month after the reporting period. There are plans to incorporate the return into SUTS, but the feature will not be available until later this year.

July 1 has come and gone. Will I be penalized for failing to implement this quickly?

No. CDOR has generously decided to provide some leniency, as it received feedback that listing and collecting the fee by the July 1 start date would prove challenging. Informal guidance says if you fail to separately state the fee, you will not incur penalties or interest — given you do the best you can to implement the separate statement requirement.

The buyer will still be required to pay the fee whether you collect it from them or not, and you, the retailer, will still be responsible for remitting the fee for any transactions made on or before July 1, 2022, even if you did not charge it to the buyer.

Our perspective on the new delivery fee in Colorado

There is no question this fee, imposed while the country is experiencing record-setting inflation and sky-high fuel prices, has caught consumers and businesses alike by surprise. While you, the seller, do not have to pay the fee, your potential customers do — and this impacts everything they buy that gets delivered (including restaurant delivery). These add-ons will stack up, and with Colorado’s cost of living already rising, consumers may have to start budgeting, indicating this could affect your bottom line in the future.

Rely on cannabis and tax professionals

If you have any questions about the new fee, such as how to file this separate tax return or collect the tax from your customers, contact MGO’s team of Tax professionals.

MGO is positioned as a national leader in both tax advisory and cannabis accounting and financial best practices.

About the author

Ilias Savakis is a State & Local Tax Manager at MGO. He has over five years of experience in Sales and Use Tax compliance and consulting. Contact Ilias at ISavakis@mgocpa.com.

]]>Cannabis companies, like companies across every sector and industry, need to be focused on the double bottom line concept. Specifically, companies need to commit to both financial (first bottom line) and ESG-focused outcomes (second bottom line) to ensure long-term success.

The evolving definition of value

For companies across all industries, there is an enhanced sense of finding, committing, and tracking to a higher purpose. Whether it is prioritizing environmental risks and opportunities or committing to social initiatives, establishing a purpose beyond financial returns is paramount to long-term success in today’s world.

Cannabis in United States has a long history tied to criminalization which has had a disproportionate impact on minority and underprivileged populations. As such, there is significant opportunity for both federal and state governments and the industry itself to focus on social programs which drive positive impact and change (CNBC: Cannabis is projected to be a $70 billion market by 2028 — yet those hurt most by the war on drugs lack access).

Overall, ESG initiatives have become ubiquitous with business strategy and growth — and because the cannabis industry is inherently diverse, environmentally-focused, and values-driven, there is a unique opportunity make a real impact.

And how does a company develop a strategy on driving impact? It starts with inventorying your material, non-financial (i.e., ESG-specific) risks and opportunities.

A focus on materiality: the environmental pillar

When it comes to environmental issues, there are several material risks and opportunities that cannabis companies can prioritize, including but not limited to:

- energy management,

- greenhouse gas (GHG) emissions, and

- water and wastewater management.

For example, the western United States continues to experience historic droughts, which have forced local governments to restrict water usage (LA Times: Unprecedented water restrictions hit Southern California). As such, cannabis companies operating in the western U.S. are facing both a risk and an opportunity to re-think how they manage their water usage as part of the cultivation process.

A focus on materiality: the social pillar

As we previously mentioned, there are many social issues companies in the cannabis industry will find material to their businesses. These include:

- product quality and safety;

- access and affordability;

- customer welfare;

- human rights and community relations;

- selling practices and product labelling;

- employee engagement; and

- diversity, equity, and inclusion.

Leaders in the cannabis sector are using their businesses and platforms to push for tangible social progress — this includes investing in and prioritizing minority-led companies in their supply chains, establishing policy documents to hold business partners to strict operating standards, and adding new jobs with competitive pay and benefits in communities which need it the most.

A focus on materiality: the governance pillar

The cannabis industry’s complex relationship with the legal and regulatory environments is well documented. Since 2012, 19 states and Washington, DC have legalized recreational use of cannabis by adults; however, the product remains illegal at the federal level. Because of this, cannabis companies also have a unique relationship with the governance pillar of ESG.

From MGO’s perspective, until laws change at the federal level, businesses operating in the cannabis industry will need to prioritize each of the criteria in the governance pillar to navigate evolving risks and to ensure the long-term success of their companies.

The criteria in the governance pillar includes:

- management of the legal and regulatory environment,

- systemic risk management,

- competitive behavior,

- business ethics,

- critical incident risk management,

- tax transparency, and

- accounting policies and practices.

Opportunities in ESG

While many companies see ESG as a buzzword, integrating its concepts within the holistic business model is important to drive long-term value creation.

There are substantial competitive advantages — including employee acquisition and retention, reducing the cost and environmental impact of operations, and reducing the cost of capital (JP Morgan: ESG integration – building more resilient portfolios for the long term).

Like-minded companies can and are teaming up to build brand partnerships, adding to product lines with collaborations, and developing innovative ideas for the entire industry to benefit from.

Incorporating ESG into your cannabis company means taking a holistic look at where you currently stand — and then driving the necessary change across the entire organization and value chain.

Steps for developing an ESG strategy

Here are a few of the steps companies can take to get started with their ESG program:

- Perform an ESG program assessment for your business: determine what’s important (i.e., material) to your investors, employees, and communities, along with the gaps requiring your attention.

- Prioritize your material topics grounded in risk and opportunity: recognize that with opportunity comes risk — and you need to be prepared for both when focusing on value creation.

- Establish a go-forward strategy focused on your gaps to drive the most impact: Is your company growing and in need of financial statement and/or tax preparation? Is there a specific way you can lobby for legislation, or partner with another company to help minority or women-owned businesses thrive as part of a social initiative? Create a program that invests in and bolsters the community?

- Reporting ESG metrics, KPIs, and progress against commitments to investors and/or the board of directors: Keep everyone in the loop, especially those who want to see you succeed;

- Leveraging leading ESG frameworks and standards: A robust ESG framework will lay out the necessary programs, capabilities, processes, policies, procedures, and essential initiatives to accompany your go forward ESG strategy.

Looking ahead

Whether you have an ESG program in place, or you are looking to get started, the definition of value is evolving and cannabis organizations that keep pace are primed for long-term success.

If you are interested in learning more, schedule a conversation with our ESG team today.

]]>In the cannabis and hemp industries, capturing the true value of real estate holdings in an M&A deal can be both elusive and central to the overall success of the transaction. Difficult-to-acquire licenses and permits are essential for operating, which often drives up the “ticket price” of property, ignoring operational and market realities that suppress value in the long run. On the flip side, real estate holdings are sometimes considered “throw-ins” during a large M&A deal. These properties can hold risks and exposures, or, in many cases, are under-utilized and present an opportunity to uncover hidden value.

Both Acquirers and Target companies must take specific steps toward understanding the varied layers of risk and opportunity presented by real estate holdings. In the following, we will address some common scenarios and provide guidance on the best way to ensure fair value throughout an M&A deal.

Real estate as a starting point for enterprise value

Leaders of cannabis and hemp enterprises must understand that real estate should be a focus of the M&A process from the very beginning. All too often, c-suite executives are well-acquainted with detailed financial analyses for other parts of the business, but have a limited or out-of-date idea of their enterprise’s square footage, details of lease agreements, or comparable values in shifting real estate markets. Oftentimes it takes a major business event, like an M&A deal, to spur leadership to reexamine and understand real estate holdings and strategy. Regrettably, and all too often, principals come to that realization post-closing and realize they may have left money on the table.

In an M&A deal, the party that takes a proactive approach to real estate considerations gains an upper-hand in negotiations and calculating value. Real estate holdings can provide immediate opportunities for liquidity, cost-reduction, or revenue generation. At the same time, detailed due diligence can reveal redundant properties, costly debt obligations, unbreakable leases, and other red flags that would undermine value post-closing.

For both sides of the M&A transaction, real estate strategy and valuation should be a core consideration of the overall goals and value drivers of the deal. A direct path to this mindset is to place real estate holdings on the same level of importance as other assets that drive value – human capital, technology, intellectual property, etc. Ensuring that real estate strategy aligns with business goals and objectives will save considerable headaches and potential liabilities in the later stages of negotiating and closing the deal.

Qualify and confirm all real estate data

One of the harmful side-effects of a laissez-faire attitude toward real estate in M&A is that the entire deal can be structured around data that is simply inaccurate or incomplete. This inconsistency is not necessarily the result of an overt deception, but too often it is simply an oversight. Valuations can also be based upon pride and ego, without supporting market data.

Let’s visit a very common M&A scenario: The Target company has real estate data on file from when they purchased or leased the property (which may have been years ago), and that data says headquarters is 20,000 sq. ft. of office space. Perhaps they invested heavily into improvements like custom interiors that did nothing to add value to the real estate. The Target includes that number in the valuation process and the Acquirer assumes it is accurate. Following the deal, the Acquirer moves in and, in the worst case, realizes there is actually only 15,000 sq. ft. of useable space. Or it is equally common that the Acquirer learns the space is actually 25,000 sq. ft. Either way, value has been misrepresented or underreported. M&A deals involve a multitude of figures and calculations, and sometimes things are simply missed. But those small things can have a major impact on value and performance in the long run.

The only solution to this problem is to dedicate resources to qualifying and quantifying data related to real estate holdings. When preparing to sell, Target companies should review all assumptions – square footage, usage percentage, useful life, etc. – and conduct field measurements and physical condition assessments (“PCA’s”). This will help your team understand the value of your holdings and set realistic expectations, and perhaps just as importantly, it saves you from the embarrassment of providing inaccurate numbers exposed during Acquirer’s due diligence—and getting re-traded on price and terms. That reputation will ripple through the marketplace.

From the Acquirer’s side, the details of real estate holdings should come under the same level of scrutiny as financials, control environment, etc. Your due diligence team should commission its own field measurements and PCA, and also seek out market comparables to confirm appraisals. It is simply unsafe and unwise to assume the accuracy of any of these details. Performing your own assessments could reveal a solid basis to re-negotiate the M&A, and will help shape post-merger integration planning.

Tax analysis will reveal risks and opportunities

The maze of tax regimes and regulatory requirements cannabis and hemp operators navigate naturally creates opportunities to maximize efficiencies. This is particularly the case when it comes to enterprise restructuring to navigate the tax burden of 280E.

For example, it may be possible to establish a real estate holding company that is a distinct entity from any “plant-touching” operations. By restructuring the real estate holdings and contributing those assets to this new entity it may be possible to take advantage of additional tax benefits not afforded to the group if owned directly by the “plant-touching” entity. This all assumes a fair market rent is charged between the entities.

Recently, operators have looked to sale/leaseback transactions to help with cash flow needs and thus these types of transactions have gained prominence for cannabis and hemp operators. It is important that these transactions be carefully reviewed prior to execution to ensure they can maintain their tax status as a true sale and subsequent lease, instead of being considered a deferred financing transaction. If a Target company has a sale/leaseback deal established but under audit the facts and circumstances do not hold up, this could open up major tax liabilities for the Acquirer.

When entering into an M&A transaction, it is important that the Acquirer look at the historical and future aspects of the Target’s assets, including the real estate, to maximize efficiencies of these potentially separate operations. It is also equally important to review pre-established agreements/transactions to ensure the appropriate tax classification has been made and that the appropriate facts and circumstances that gave rise to the agreements/transactions have been documented and followed to limit any potential negative exposure in the future.

Contract small print could make or break a deal

An area of particular focus during due diligence should be a review, and close read, of the Target company’s existing property leases and other contracts. There are any number of clauses and agreements that seem harmless and inconsequential on the surface, but can have disastrous effects in difficult situations. In many cases the lease/contract of a property is more important than the details of the property itself. For example, if the non-negotiable rent on a retail location is too high (and scheduled to go higher), there may be no way to ever turn a profit.

The financial distress resulting from the COVID-19 pandemic has brought these issues to the forefront in the real estate industry. Rent payment and occupancy issues are shifting the fundamental economics of many property deals and contracts. If, for example, you are acquiring a commercial location that is under-utilized because of market demand or governmental mandate, you must confirm whether sub-leases or assignments are allowed at below the contract price. If not, you could be stuck with a costly, underperforming asset amid quickly shifting commercial real estate demand.

In many leases and contracts there are Tenant Improvement Allowance conditions that require the landlord to fund certain property improvement projects. If utilizing these terms is part of the Acquirer’s plans, you may need to have frank and open conversations with landlords about whether the funds for these projects are still available, and if those contract obligations will be met. Details like these are often penned during times of financial comfort without consequences to the non-performing party, but a landlord struggling with cash flow may not have the capability to meet contract standards.

These are just a few examples from a multitude of potential real estate contract issues that can emerge. It is recommended to not only examine these contracts very closely, but have dedicated real estate industry experts perform independent assessments that account for broader social, economic, and market realities. That independent analysis will help your executive team formulate a real estate strategy that better aligns with core business objectives.

Dig deep to uncover real value

There are countless scenarios where issues related to real estate make or break an otherwise solid M&A transaction, whether before or after closing the deal. The only path forward is to treat real estate holdings with the same care and attention paid to the other asset classes driving the deal. The cannabis and hemp industries have recently endured micro-boom-and-bust cycles that have left many assets under-performing. As Target companies offload these assets, and Acquirers seek out good deals, both parties must undertake focused efforts to establish the fair value of complex real estate assets and obligations.

Catch up on previous articles in this series and see what’s coming next…

]]>Special Purpose Acquisition Companies, or SPACs, have been steadily rising in prominence over the last year, earning headlines with a number of eye-popping capital raises and making acquisitions that took high-profile companies public, including Virgin Galactic and electric carmaker Nikola. Previous, a relatively niche investment vehicle, many cannabis and hemp industry operators are still not clear as to how these investment companies operate, and what one should do if approached by a SPAC for an acquisition. In the following we will lay out the basics of SPACs and provide key considerations for cannabis operators and entrepreneurs approached by, or courting, investors.

The fundamentals of SPACS

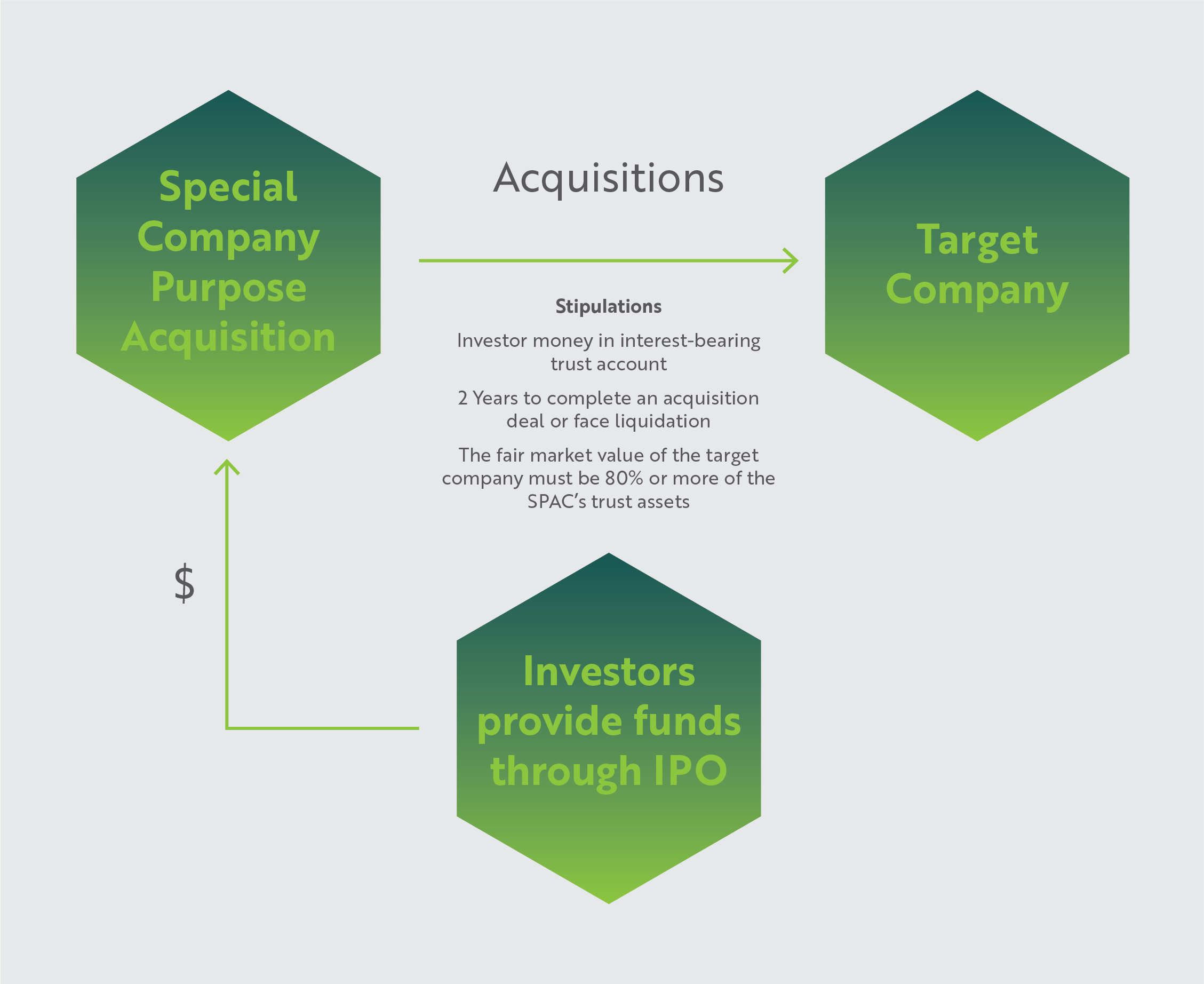

Simply defined, a SPAC is a shell company formed by founders/sponsors in order to raise investments through an IPO to acquire an existing company/companies. The key players involved are:

- Founders/Sponsors: Generally subject matter experts in their industry fields with credible market reputations.

- IPO Investors: Typically include institutional investors, equity funds, and the general public.

- Target company: A private company in the industry/sector stated as the SPAC’s focus during the IPO process.

As a regulatory stipulation, the Target company cannot be identified at the time of the IPO, and investors pour money into this instrument mainly on the basis of the founders’ reputation and the sector of investment – thus SPACs are also known as ‘blank check’ companies.

SPACs have many safety criteria for protecting investor interests. For example, investor money is generally kept in escrow in an interest-bearing trust account, and can be used only for acquisition purposes. The interest is used to cover certain operational SPAC costs until a transaction closes. Also, SPACs are time bound – a SPAC typically has two years to complete an acquisition or face liquidation, in which case the money is returned to the investors. (However, this period is extendable upon meeting certain conditions.) And finally, for the M&A transaction to be regulatory admissible, the fair market value of the target company must be 80% or more of the SPAC’s trust assets.

SPACs are generally beneficial to all parties concerned: sponsors/founders get liquidity to implement their ideas as well as ‘founder shares’ for their efforts; investors get an ‘expert’ backed investment platform to invest in; and the target company gets sound management expertise and liquidity. The IPO process is also faster for SPACs compared to traditional IPOs due to simplified documentation and listing procedures.

SPAC Structure

History and growing popularity of SPACs

SPACs have been in existence since the 1990s, but they became more popular in the early 2000s when entrepreneurs and mid-market public investors started seeking out private equity alternatives, more direct market options for raising funds, as well as suitable risk return options. Nowadays, SPACs are increasingly being used in various industries, to take companies public, and in situations where financing is scarce. At the moment, SPACs are having a major impact in technology and other high-growth sectors, exemplified by transactions involving DraftKings, Virgin Galactic, and Nikola. In the United States, the SPAC public offering structure, like many other financial instruments, is governed by the Securities and Exchange Commission (SEC).

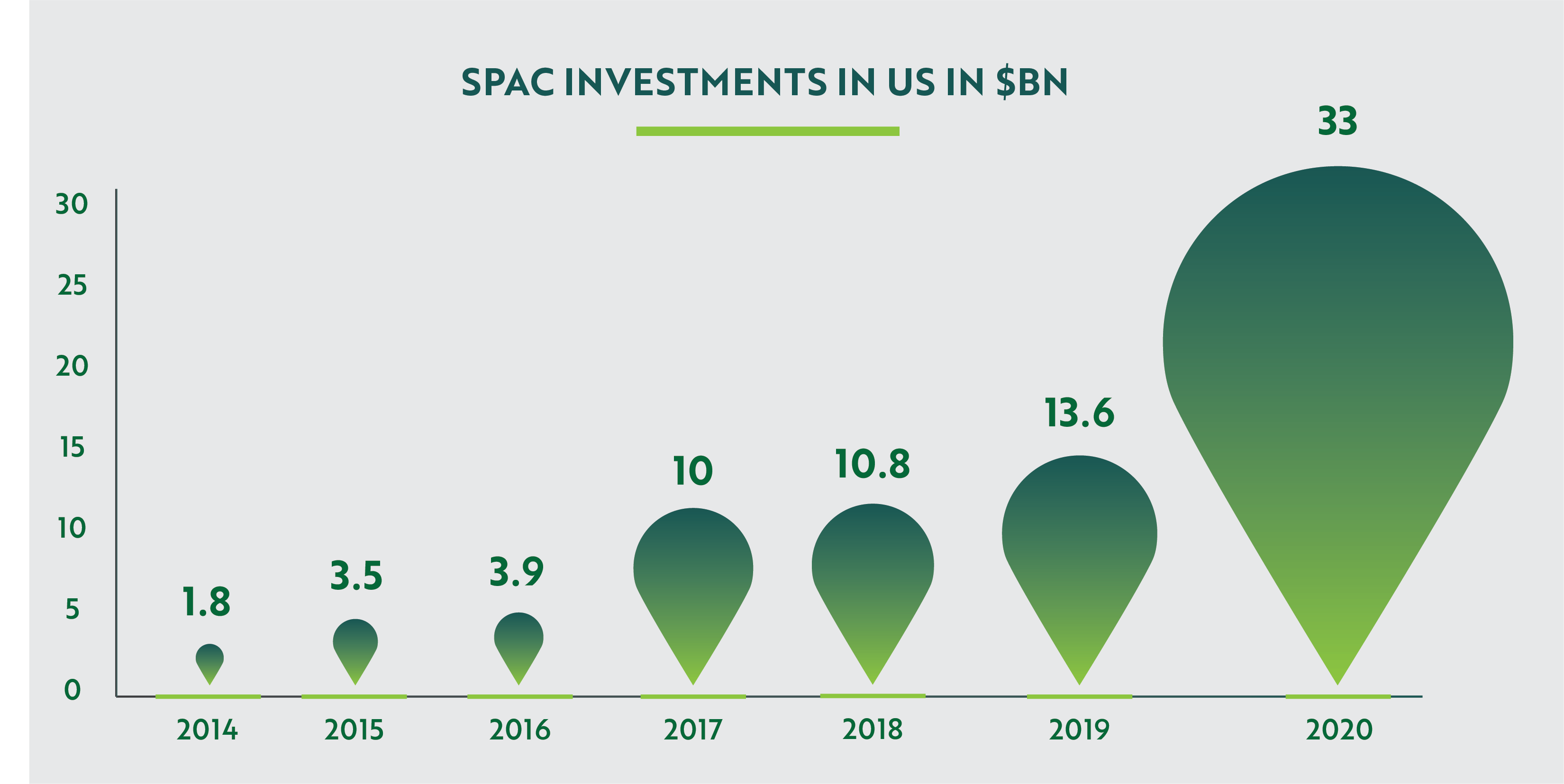

Source: SPAC Research

SPACs as a force in cannabis and hemp

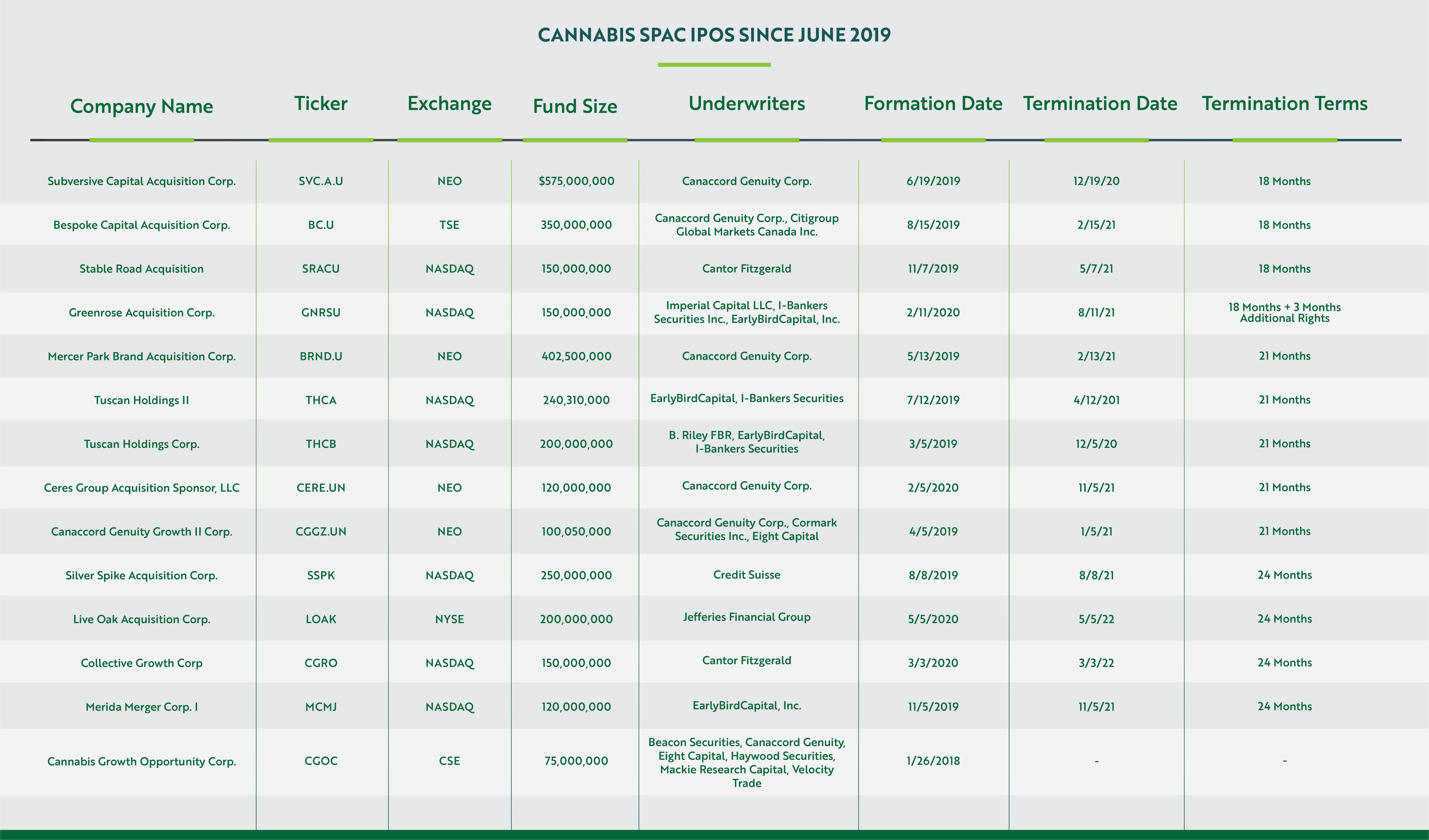

On May 1, 2020, founder and former CEO of Canopy Growth, Bruce Linton, rang the Nasdaq’s opening bell on the day he took his new venture public – a SPAC called Collective Growth Corp. – raising $150 million. While not the first SPAC to enter the cannabis space, Linton’s high-profile in the cannabis and hemp industries introduced the idea of SPACs to many industry operators and investors.

According to analysis provided by ELLO Capital, cannabis SPACs raised over $3 billion between June, 2019 and July, 2020. Not all of the funds have been utilized to date, so the clock is ticking on the ~two year window following the initial capital raise.

Considering the proliferation of distressed assets and companies struggling with the cash crunch, general economic turndown, and other complexities inherent to today’s cannabis industry, SPACs are likely to offer lifelines to a significant number operators – building new market leaders and reshaping the cannabis industry in the process.

Source: ELLO Capital

Guidance for cannabis industry companies

When a SPAC makes an acquisition, it can follow any of the standard transaction structures – asset acquisition, stock/share purchase, or merger – and the resultant entity combines the SPAC and the Target company into a publicly traded operating company.

So, what should cannabis and hemp operators and entrepreneurs do if approached by a SPAC for an acquisition? Of course, it’s a personal decision whether to go public or not, but for companies in need of liquidity or seeking an exit, merging with/selling to a SPAC can be quite advantageous, especially in the present market context. For one, a SPAC acquisition can help to raise the Target company’s sale price, due to increased competition as private equity and SPACs compete for the same targets. Furthermore, SPAC founders’ reputation and their choice of your company can also bring increased attractiveness/investor interest and richer valuations.

Since SPACs are traditionally led by experienced founders, the IPO process often runs smoothly and efficiently. Because there is typically no roadshow or series of investor presentations, the timeline and resources are more optimal than an IPO. And finally, for companies without experienced management, SPAC control can help provide the requisite expertise and talent.

It is important to note that SPACs listed on US exchanges, including Linton’s Collective Growth Corp, are necessarily focused on the legal hemp sector, since SEC regulatory guidelines prohibit adult-use and medical cannabis companies from going public in the US. However, several SPACs are listed on Canadian exchanges, which creates the potential for investments in US-based cannabis businesses.

Final thoughts

In the last year, broad market conditions have elevated the importance of SPACs across all industries. The cannabis and hemp industries are no different and SPACs represent a welcome investment source in these tough times. SPACs are bringing investment back into the industry, importantly from ‘so far on the bench’ institutional investors, which is particularly important for companies who want liquidity at a time when other avenues are drying up.

Catch up on previous articles in this series and see what’s coming next…

]]>According to the CBCC press release, the emergency regulations are meant to address the vaping crisis: “The emergency regulations are designed to help consumers identify licensed cannabis retail stores, assist law enforcement, and support the legal cannabis market, where products such as vape cartridges are routinely tested to protect public health and safety.”

The code certificate needs to be posted within three feet of any public entrance to a cannabis dispensary or “in a locked display case mounted on the outside wall of the premises.” In addition to paper, the QR code certificate can be printed on glass, metal, or other material. It needs to be 8 ½ inches by 11 inches, the size of a standard sheet of paper. The code itself needs to be 3.75 inches by 3.75 inches.

The regulatory change was pursued by the CBCC to allow consumers and law enforcement officials to be able to quickly discern the origin of a product and ensure its safety after the code is scanned. QR codes will help consumers know they are purchasing a product from a vendor in the legal market.

The cartridges that caused the illnesses that led to the vaping crisis last year originated in the underground market. As of February 18th, 2020, the CDC reported 2,807 cases of illness associated with e-cigarettes across the U.S. and 68 cases resulted in deaths, with four of those in California.

“The proposed regulations will help consumers avoid purchasing cannabis goods from unlicensed businesses by providing a simple way to confirm licensure immediately before entering the premises or receiving a delivery,” said CBCC Chief Lori Ajax.

Unfortunately, illegal cartridges with a lethal amount of Vitamin E look nearly identical to those from legal retailers, as do underground sellers who maintain brick and mortar stores. And because they are underground, they do not comply with regulations. Recent estimates have shown that in California, the underground black market is more than twice the size of the legal market.

Those with smartphones will be able to scan the QR codes to ensure the product comes from a licensed retailer. When they scan the code, it will send them to the BCC’s License Search database where they will be able to see the business license number, license type, its official name, contact information, business structure, premise address, license status, issue date, expiration date, and activities.

In addition, you can see whether the business holds a license for adult use, medical, or both. The database also includes phone numbers and email addresses for all the businesses. In addition, you can see if they hold multiple licenses. Many of the businesses also have links to their respective websites. Active licenses are listed along with those who are suspended, canceled, revoked, inactive, or expired.

While the emergency regulations present another regulatory hurdle for compliant California cannabis businesses, the silver lining is that legal market operators can now advertise their compliance with safety standards – an additional edge in the battle to win market share from black market operators.

]]>The immense demand for hemp-derived CBD has motivated farmers to embrace the crop. According to the advocacy group Vote Hemp, 9,770 acres of hemp were grown in 2016 under a limited USDA pilot program. In 2018 the number was 78,176 acres. This year, the first planting since the Hemp Farming Act was signed into law, farmers have received licenses to plant 511,442 acres. By giving farmers a defined, though many think unduly onerous, testing process to certify their crop is within the THC limit, the rule is likely to encourage more hemp planting until supply and demand reach equilibrium. There has been a wide range of where that may be given the many uses of the crop, and only time will tell where research will lead us to or consumer demand will pull us towards.

Certified legal hemp

The Hemp Farming Act of 2018 removed hemp containing .03 percent or less THC from Schedule 1. In theory, this immediately made hemp (and presumably CBD derived from it) as legal as a bushel of corn. Legal hemp is indistinguishable from illegal cannabis without lab testing, which has resulted in police mistaking hemp for cannabis.

The hemp farming rule establishes a national laboratory protocol for certifying hemp is within THC limits, a crucial step for allowing routine transport of hemp from field to processor to market.

Putting the USDA hemp certification process into effect will take some time. The labs will have to be DEA certified. The samples of hemp flower must be collected no more than 15 days before harvest by a USDA-approved agent, who could be law enforcement officers. The testing protocol allows for a margin of error, or “measurement of uncertainty” as USDA terms it, to allow for crops marginally above the THC limit. Beyond that, however, crops with excessive THC will be destroyed. It is likely the hemp industry will advocate for more lenient testing and certification protocols, so the final rule could be different. Given the nature of the plant and benign effects of remediating the crop to reduce THC levels, there’s little reason why more leniency wouldn’t be employed other than to create significant waste and loss (hardship for farmers) for no other discernible reason than continued demonization of a useful cannabinoid.

The draft hemp rule marks the end of hemp’s regulatory stigma but USDA has work to do before the crop is fully normalized. A freak hail storm in eastern Oregon late this summer severely damaged 500 acres of hemp worth $25 million. That’s a total loss for the farmers because the USDA crop insurance program doesn’t yet cover hemp. USDA still must specify standard measures and units for hemp, as it has for all other crops. There can’t be a hemp commodity market until there is a measure, like the bushel, for a standard unit of hemp.

CBD as a commodity

Consumer demand for CBD is the economic engine that has driven a 50-fold increase in the amount of hemp planted in the US since the first pilot programs authorized in the Farm Bill of 2013. High prices for CBD-rich hemp encouraged a rapid increase in the number of acres planted and a frantic scaling of the supply chain to process raw biomass into consumer products.

Prices for hemp biomass and the wholesale CBD products derived from it have been dropping recently, a response to the bumper harvest anticipated this year and continued acreage expansion expected as a result of the USDA rule. Consumer demand for CBD is expected to grow. BDS Analytics estimates that US sales of cannabis- and hemp-derived CBD products were $1.9 billion in 2018 to $20 billion by 2024, a compound annual growth rate of 49 percent.

A growing consumer market for CBD products and an abundant hemp supply will require a buildout of the hemp supply chain and is likely to create significant opportunities, such as specialized farm equipment and building the DEA-certified labs required for testing and certification.

The USDA hemp farming rule will allow farmers to grow as much hemp as required for CBD (if not more) but how soon the market for CBD consumer products grows is subject to other rulemaking. CBD is unlikely to reach its full market potential as a food ingredient before the FDA, or Congress, makes a regulatory distinction between the amount of CBD in a single serving snack or beverage and the therapeutic amounts in prescription medications (Epidiolex, the first FDA approved drug containing a cannabinoid, came on the market in 2018).

Currently, most of the companies adding CBD to food and beverages are relatively small but risk-tolerant regional players. Every global CPG brand is formulating a CBD strategy and some are considering or entering the US market with their own products or through acquisition of incumbent companies even prior to FDA guidance. Similarly, the CBD market is unlikely to reach its full potential until the Treasury Department, or Congress, normalizes CBD sales. Though CBD is legal, companies still have difficulty obtaining routine banking services, such as payment processing.

The exuberance about the prospects for CBD over the next few years is entirely rational, but CBD is just one of the 113 known cannabinoids. One of the others, THC, is the basis of the multi-billion dollar legal cannabis industry. Another, CBG (cannabigerol) is a strong contender to be the next cannabinoid on the market. What little is known of the other cannabinoids points to promising therapeutic applications. The global pharmaceutical industry, like the global CPG industry, is ready to invest in hemp and cannabinoids as soon as the regulatory picture becomes clear and some have begun R&D to get ahead of that timing.

USDA takes the long view

What USDA repeatedly makes clear in the rule is that hemp, outside of the strict requirements for lab certification, is just another legal crop free to find markets and cross borders.

There are no restrictions on hemp seed import/export, which means US farmers can purchase seed on the international market and US cannabis biotech companies are free to export seeds. The rule explicitly states “there’s no need for additional regulation on biomass, fiber, seed, hemp seed oil or hemp seed for consumption.”

The rule sets the stage for US farmers to participate in a global hemp trade. The labs that certify hemp for THC content will also be able to certify it for export, so long as they are DEA certified. USDA, which actively promotes American crops on global markets, will do the same for hemp. “Should there be sufficient interest in exporting hemp in the future, USDA will work with industry and other Federal agencies to help facilitate this process.”

The regulation in many ways clears regulatory barriers to import/export of hemp-derived products. It is reasonable to see this as good for free trade in CBD. The first export of US CBD products was shipped to Mexico at the end of last July.

What about the rest of the plant?

The 90 percent of the hemp plant that yields no CBD (or other cannabinoids) may someday be at least as valuable as the 10 percent that does. In 1938, Popular Mechanics extolled hemp as The New Billion Dollar Crop (which is about $18 billion now) based solely on its value as fiber. Though farmers in 1938 could have used a valuable new crop, the Marihuana (sic) Tax Act was making the crop economically worthless. The farm economy hemp might have sustained was not allowed to take root.

The hemp farming rule begins to reverse that historic mistake. The potential for hemp as a source of food, fiber and plant-based industrial products is substantial. The Congressional Research Service found “The global market for hemp consists of more than 25,000 products in nine submarkets: agriculture, textiles, recycling, automotive, furniture, food and beverages, paper, construction materials, and personal care.” The relatively small existing markets for hemp fiber and hemp seed as food are more profitable per acre than the depressed prices for corn and soybeans.

There is reason to think future policies to address global climate change through “carbon farming” could benefit hemp agriculture. An Australian study concluded a hemp crop is “the ideal carbon sink” because hemp absorbs more atmospheric carbon per acre than any forest or commercial crop.

Products derived from hemp could have advantages in a future carbon-constrained economy. For example, concrete manufacturing is one of the largest industrial sources of C02 emissions globally but hempcrete, a product few people have heard about, is a carbon-negative substitute.

It will be a while, perhaps a long while, before hemp is as common as cotton or hempcrete is standard in new construction. Hemp has a tiny market presence outside of CBD and hemp seed as a food, and its lobbying presence is no larger. The future of hemp as a large and growing market is nonetheless very promising. As more and more hemp is harvested each year it is all but inevitable that entrepreneurs and investors will take on the challenge of bringing entirely new product categories to market.

]]>Meanwhile, the steady march toward legalization has fueled remarkable growth in the cannabis sector over the last several years. While the outlook on cannabis remains bullish, many wonder how this emerging sector will respond to a major economic downturn.

Will the steady stream of retail capital, venture capital and private equity funds spurring cannabis industry growth dry up and bring expansion to a shuddering halt? Or will the cannabis industry – and individual cannabis private and public companies – demonstrate the historical counter-cyclical behavior we’ve come to expect from ”vice” industries, such as alcohol and tobacco?

Likelihood of a recession

The experts can argue about the severity and the timing, but – on the heels of an extraordinary 10-plus years of economic growth and stability – most agree that it is at least wise to prepare for a significant slowdown. Portfolio adjustments are probably in order, as prepared investors will start considering bonds, dividends, stability and commingled accounts.

It is also time to start thinking about defensive stocks – and add cannabis and cannabis-related equities to those considerations. If you have an option to invest through private markets, those opportunities may hold a key to more value, albeit with slightly less transparency to the public market.

Alcohol and tobacco’s recession track record

Clearly, the cannabis industry has never encountered a recession and as such, we can’t revisit history and cite earlier performance, milestones to watch or other informative data.

We can, however, note that the industry would enter a recession with what arguably appears to be very strong fundamentals. According to one report:

- Global consumer cannabis spending is expected to surge 38% in 2019 to $16.9 billion, up from an estimated $12.2 billion in 2018, $9.5 billion in 2017, and $6.9 billion in 2016.

- Compound annual sales growth between 2017 and 2022 is expected to average 26.7%, with $31.3 billion in global marijuana sales expected in 2022.

Additionally, the industry got an important kicker in 2018, when passage of the U.S. Farm Bill made hemp legal nationwide.

It can also be insightful to go back and review the performance of comparable industries, in this case we will examine “vice” industries, specifically alcohol and tobacco. All have track records that provide at least some degree of visibility of what we might expect from cannabis.

The alcohol/tobacco example that followed the recent Great Recession is particularly informative. Consider (information compiled by financial information company Sageworks):

- In 2008, the first full year of the Great Recession, alcohol sales increased 9% and the average unemployment rate was 5.8%.

- In the 12-month period June 1, 2010-May 31, 2011, alcoholic beverage sales grew 10% in the U.S. and the unemployment rate hit 9.6%.

Takeaway: Consumers cut back on a great number of things when the economy turned, but drinking was not one of them.

Lessons (and non-lessons) learned from individual stocks

Are there lessons to be learned by the performances of some of the individual stocks during and immediately following the Great Recession?

Yes and no.

Anheuser-Busch Inbev (NYSE: BUD) delivered a 39.4% return in 2008, which was nearly 80% better than the S&P 500. Revenue, however, climbed just 5%. The strong performance was not based on financial performance but, rather Anheuser-Busch’s acquisition by Inbev.

Lesson: Undervalued companies with market share will get noticed.

Shares of Altria (NYSE:MO) the parent company of Marlboro among other brands, gained 28% between December 2007 and December 2010. In the middle of that period (2009), the National Institutes of Health (NIH) put out a paper stating that smokers actually increased their cigarette intake during a period of economic difficulty.

Lesson: Price increases can offset weak sales. Brand power has value. Dividends are important in downturns.

Molson Coors (NYSE:TAP) is an interesting example, as the company’s “average-Joe” brand was overwhelmed by craft beers in the Great Recession. Example: the share price of The Boston Beer Co. Inc. (NYSE:SAM) advanced 80%. The issue has since been rectified, with numerous acquisitions, including Blue Moon, Leinenkugel, Hop Valley and Revolver. (Sidebar: Molson Coors, like Constellation (NYSE:STZ) before it with its acquisition of Canopy Growth (NYSE:CGC), also has a deal with cannabis company Hexo (NYSE:HEXO) to develop non-alcoholic cannabis-infused drinks in Canada.

Lesson: Consumers seek out “stress relievers” during stressful times. People with a little extra disposable income will consume products at the higher end of the pecking order.

Diageo (NYSE:DEO) is a global juggernaut, with a huge portfolio of brands, including Johnnie Walker, Smirnoff, Captain Morgan, Ketel One, and Guinness beer. The company continued to be highly profitable during the Great Recession, dropped a bit the next year and then more than recovered in 2011. Their dividend payout ratio is just over 50%.

Lesson: Brand power stays strong during a downturn.

Other factors to consider

There are a number of intangible differences across the cannabis industry that also need to be considered in any analysis:

- Illicit Market, Red Ink? – One major difference between cannabis and alcohol/tobacco is that in a recession the cannabis industry would still have to deal with the competitive pressures and potential price cutting of the illicit market. As an economic downturn puts pressure on consumers’ wallets, we could see a resurgence in illicit market offerings, cutting into legal profits.

- Strong Medical Tailwind – The cannabis industry really is two distinct sectors: adult-use and medical, and the differences are profound. As stated in the Cannabis Private Investment Review, the adult-use market is broader and has long-term growth potential, but the medical market has a number of strong characteristics. For example, U.S. public opinion is overwhelmingly in favor of medical cannabis; ample models of successful regulatory programs; the progress of medical cannabis at the pharmacological level, and the FDA’s 2018 approval of the first CBD-based medicine, are clearing the path for further de-scheduling of cannabis compounds.

- Mature Support Sectors In Place – The opportunity for cannabis investors extends beyond the well-known cultivation, manufacturing and distribution brands. Companies focused on research and development, accessory products, services, publishing and software all have carved out positions as well. In a recession, certain sectors may decline, but the diverse array of companies representing the cannabis industry could produce a mixed bag of winners and losers, evening out the industry’s performance as a whole, or even floating poor-performing sectors.

- Lawyers. Bankers. Politicians – Right now, the future of cannabis as a legal and regulated industry appears more promising than at any previous point as industry growth is being stimulated on several fronts. Doctors are beginning to embrace the medicinal value of cannabis and they are incorporating it into their practices. This is also supported by new efforts to enhance research and development throughout the US and internationally. Lawyers are pushing for legalization in jurisdiction after jurisdiction. Investment bankers and Venture Capital and Private Equity firms are stimulating a flow of needed capital. And even politicians are seeing that legalization is in their best interests.

One more consideration

Finally, there are some market watchers who believe the bull case for cannabis in a recession has almost nothing to do with the burgeoning industry being counter-cyclical, recession-proof or recession-resistant. Instead, they assert, the strong performance will be driven by economics, politics, balancing budgets and generating tax revenues.

Scenario: The prohibition remains at the federal level once the next recession hits. The economic downturn acts as a major catalyst for cannabis legalization at the state and federal levels in the U.S. and abroad. Legislatures will feel pressured to take action – and no jurisdiction will want to be left at the starting line as the others race toward to finish line, creating a possible “domino-effect” scenario.

Bottom line

“Recession-proof” is language that doesn’t belong in investment analysis. However, there is ample reason – based upon fundamentals, the track record of similar sectors and other investment considerations – to conclude that selective cannabis companies and public company stocks could, in fact, be “counter-cyclical” or “recession-resistant.” Accordingly, they should be seriously evaluated as investors consider adjusting their portfolio for a possible economic slowdown.

]]>Hemp has been an agricultural product for millennia, and it was once an important crop central to the founding of the U.S. Yet for decades, the cultivation of hemp was banned and a once flourishing industry died with it. That all changed with the passage of the 2018 Farm Bill, which made hemp cultivation legal again.

Suddenly a timeless plant with countless industrial and medical uses is back in a big way. As individual states work to create regulatory programs, many established and emerging businesses are leaping at the opportunity to cultivate hemp or use it as an ingredient in a wide variety of uses.

What exactly is industrial hemp?

Industrial hemp is a variety of the plant Cannabis sativa L, a genetic cousin of cannabis. The major difference between them is that hemp has 0.3 percent or less of THC, the psychoactive ingredient in cannabis. The Farm Bill effectively descheduled hemp as a controlled substance, so that hemp and all of the useful products derived from it, are no longer regulated in the same way as cannabis (although CBD, remains in a regulatory gray area).

A brief history of industrial hemp

The cultivation of hemp is as old as farming itself. Anthropologists have found evidence of human cultivation dating back to the advent of agriculture, roughly 10,000 years ago. Hemp was also one of the first plants to be spun into fiber. An 8,000-year-old piece of ancient Mesopotamian cloth, the oldest ever found, was made of hemp. Evidence has shown China has grown hemp for about 6,000 years, while cultivation in Europe and the rest of the ancient world began around 1,200 BCE. By the sixteenth century, hemp’s fiber and seeds made it an important cash crop in Europe, and soon after it became the dominant crop in the British Isles and Russia’s number one export.

Hemp was also an important agricultural product and commodity in the U.S., where in the 1700s it gave rise to cordage and canvas businesses across the nation. It remained a core crop for a century until other industries, along with anti-cannabis legislation, contributed to its being banned. But, with thousands of uses, from paints to textiles to paper (the original Levi’s jeans and the paper the U.S. Constitution was written on were made of hemp), industrial hemp has always been a vital agricultural crop worldwide.

Some of industrial hemp’s innumerable uses

- Hemp as Food — Hemp seeds are about 30 percent oil by weight, and the U.S. Department of Agriculture has shown hemp seed oil to be highly nutritious, with 20 percent high-quality digestible proteins. Meal made from the seeds is also used in food products, from nutrition bars and tortilla chips to beer, as well as in animal feed.

- Hemp as Fiber — Hemp fibers were once widely used to make, among other things, canvas for sailing ships. The word “canvas” comes from “cannabis.” Today hemp is used to make rope, paper, and plastic and composite materials for everything from car parts to bathroom fixtures. It’s also used to make consumer goods, including clothing, shoes, and accessories.

- Hemp as Medicine — Cannabidiol (CBD), which can be derived from industrial hemp or from any cannabis plant, has surged in popularity in recent years for its potential health benefits, which are growing in number as more research is done. The Food and Drug Administration has approved the first drug with cannabidiol as an active ingredient, and more drugs are likely on the way. With CBD already an additive in a wide variety of food and beverage products, cosmetics, skincare, and health products, the market is set for significant growth.

- Hemp as … — Hemp can be used in bio-diesel fuel, lubricants, paints and varnishes, inks, plastics, a wide variety of body care products, animal bedding, garden mulch, and building materials.

First Steps of the Industrial Hemp Market

With so many uses both new and old, industrial hemp is quickly becoming a market to be reckoned with. U.S. farmers quadrupled the acres of land planted with industrial hemp to more than 511,000 between August of 2018 and August of 2019, according to the USDA. That represents a 368 percent growth, larger than any other cash crop in the same time period.

As of September, 16,877 new licenses to grow hemp were issued in 34 states in 2019, four times more than the previous year, according to one report. And, the number of licenses issued to process hemp jumped 483 percent.

Who is building the industry?

Cannabis production in maturing markets like Colorado and California are seeing price erosion because they’re doing what markets are supposed to do, competing with one another and achieving efficiencies that ultimately benefit the consumer. But with industrial hemp production now legal, major cannabis producers have been aggressively entering the suddenly enormous domestic market. Companies like Canopy Growth and Tilray are among many Canadian cannabis producers that have invested heavily in industrial hemp-fueled markets in the U.S. in 2019.

Producers of other crops are moving into the hemp market, too, switching from crops like corn, cotton, and wheat. Hemp requires far less water and has thousands of uses that utilize the entire plant, and as experienced large-scale farmers, they’re already set up to cultivate hemp. The Farm Bill also created a path for hemp cultivators to access to privileges conventional farmers have always enjoyed, including crop insurance, legal interstate travel, and basic banking services.

A bright future

Industrial hemp’s 2018 revenues were $1.1 billion, and are expected to reach $2.6 billion by 2022. New Frontier Data, a research company focused on the cannabis industry, predicts that with the signing of the Farm Bill, hemp-based industrial products will see stronger growth than any other cannabis sector over the next five to 10 years.

With that growth will come new jobs, as well, in nearly every sector and at every income level. In addition to roles on farms, the industrial hemp industry will create opportunities for specialized law experts, state and local regulators, financial and insurance experts, marketers, C-Suite executives, and distributors, just to name a few.

The hemp industry has a long way to go before we can accurately assess the crop’s market value, but in less than a year, legal industrial hemp is already a clear disruptor.

]]>60 speakers were given three minute slots, during which they could make a public statement regarding the treatment of hemp in the Farm Bill. The speakers (selected via a submission process) represented a wide variety of related parties and included: representatives from state-level agriculture, regulatory and law enforcement agencies; private sector business owners and entrepreneurs; Native American tribal leaders; and a variety of other industry advocates and stakeholders.

The diversity of speakers helped represent a broad view of issues and concerns related to the expansion of hemp cultivation. Due to the fact that it was a listening session, the USDA did not respond to any concerns raised. In the following article, we examine a number of recurrent themes raised by speakers, which illustrate concerns regarding the future of industrial hemp production in the US.

Difficulty distinguishing between hemp and cannabis

Hemp and “consumable cannabis” (adult-use or medicinal cannabis) are the same plant, and are only distinguished by the level of THC. Per the Farm Bill’s definition, industrial hemp contains less than 0.3% THC, in contrast to “cannabis,” which can contain up to 20% THC. To sight and smell, the two are indistinguishable, which places a great amount of importance on testing measures for THC.

A recurring issue, raised by both regulatory and law enforcement officials and hemp cultivators and advocates, is the lack of universal testing measures. Officials expressed concern that it was incredibly difficult to test THC content via roadside stops or in customs examinations. This results in delays to traffic and other processes and can lead to unlawful detainment and seizures. On the commercial side, hemp producers don’t want to see their legal shipments delayed or seized.

Speakers from all sides of the issue agreed that for the hemp industry to move forward, the USDA will need to define consistent testing measures and help provide training to officials tasked with regulating the cultivation and transportation of hemp.

Treating hemp as a viable agricultural commodity

The Farm Bill removed industrial hemp (as defined previously) from the Federal Controlled Substances Act, in effect decriminalizing hemp production. And yet, many advocates brought up concerns related to provisions in the Farm Bill that they felt continued to treat hemp as a scheduled drug.

For example, the Farm Bill requires license applications prior to cultivating hemp, which leads to background checks for the licensees. No other commercial crop requires diligent background checks, and subsequent application and processing fees.

Similarly, the Farm Bill did not eliminate the requirement under the Controlled Substances Import and Export Act wherein the importation of hemp seeds requires registration with the DEA. Industrial hemp has a strong history of cultivation in other parts of the world, including Canada and Europe, and the agricultural science and genomics of hemp in these regions are far ahead of the US. Access to advanced genetics in hemp crops is essential to commercial production and the DEA requirement presents a major roadblock to free trade.

These are just two examples of ways in which the specter of hemp’s past as a controlled substance continues to linger. Asking the USDA and other federal agencies to go all the way with decriminalizing every aspect of hemp motivated commentary across a number of regulatory and operational concerns.

Access to financial institutions for hemp growers

Like any other agribusiness, hemp businesses need access to lines of credit, insurance, and other traditional banking relationships. And yet, like the cannabis banking crisis, a number of hemp cultivators expressed concern related to the reluctance of financial institutions to work with them.

Representatives of financial institutions, including banks and credit unions, also made their voice heard, asking for clear protection against liability so they would feel able to serve hemp producers. Both parties concurred in requesting that the USDA make a clear pronunciation regarding access to banking for hemp producers.

While the SAFE Act has made progress in recent months, there are no guarantees about access to banking for all cannabis businesses. In the meantime, the industrial hemp industry seeks clear and strong direction at the federal level to ease the path to traditional banking.

Lack of clarity for Tribal Lands and sovereign nations

A number of Native American communities and leaders were given an opportunity to speak during the listening session and all shared enthusiasm about the potential economic benefits of hemp cultivation on tribal land. And yet, many pointed to a lack of clarity regarding regulation and self-governance for tribal communities in the 2018 Farm Bill.

For example, the management of much tribal land is a complex web of oversight from federal agencies combined with the autonomous control of tribal governments. A number of Native American leaders asked for further guidance regarding hemp production from the USDA so tribal nations can participate in upcoming planting seasons.

The balance of federal and state oversight

The 2014 Farm Bill carried provisions allowing for the creation of hemp-growing pilot programs at the state level. The successful inclusion of hemp production in the 2018 bill owes much to the success of these pilot programs. During the listening session a number of representatives from state agricultural agencies raised their voices to speak to the success of their programs and to support a continued balance between federal and state oversight.

Kentucky, Wisconsin, and Colorado all provided details on the growth of hemp in their respective states and made the case that future USDA laws should not interfere with state’s rights in the matter of hemp. At the same time, they acknowledged the essential role in federal oversight protecting and ensuring factors that include: intra-state commerce, managing import/export laws and enforcement, and the implementation of standardized testing protocols.

What is next for industrial hemp in the US?

The above topics were a sample of the diverse range of issues and concerns that remain undefined under the current wording of the 2018 Farm Bill. In coming months, each state and tribal nation will have the opportunity to submit a regulatory system governing hemp production in their respective jurisdictions. Those proposals will then be reviewed and approved by the USDA.

The USDA also seeks to implement a regulatory system that addresses these concerns, and more, which is scheduled for release in fall of 2019. If all goes well, hemp producers across the nation will have clear guidance to move forward as early as 2020.

]]>