- The music industry has changed drastically, with artists now having more control over their careers and revenue streams beyond deals with record labels.

- Artists today need to view themselves as enterprises with diverse income opportunities including live shows, merchandising, licensing deals, streaming royalties, content creation, and catalog sales.

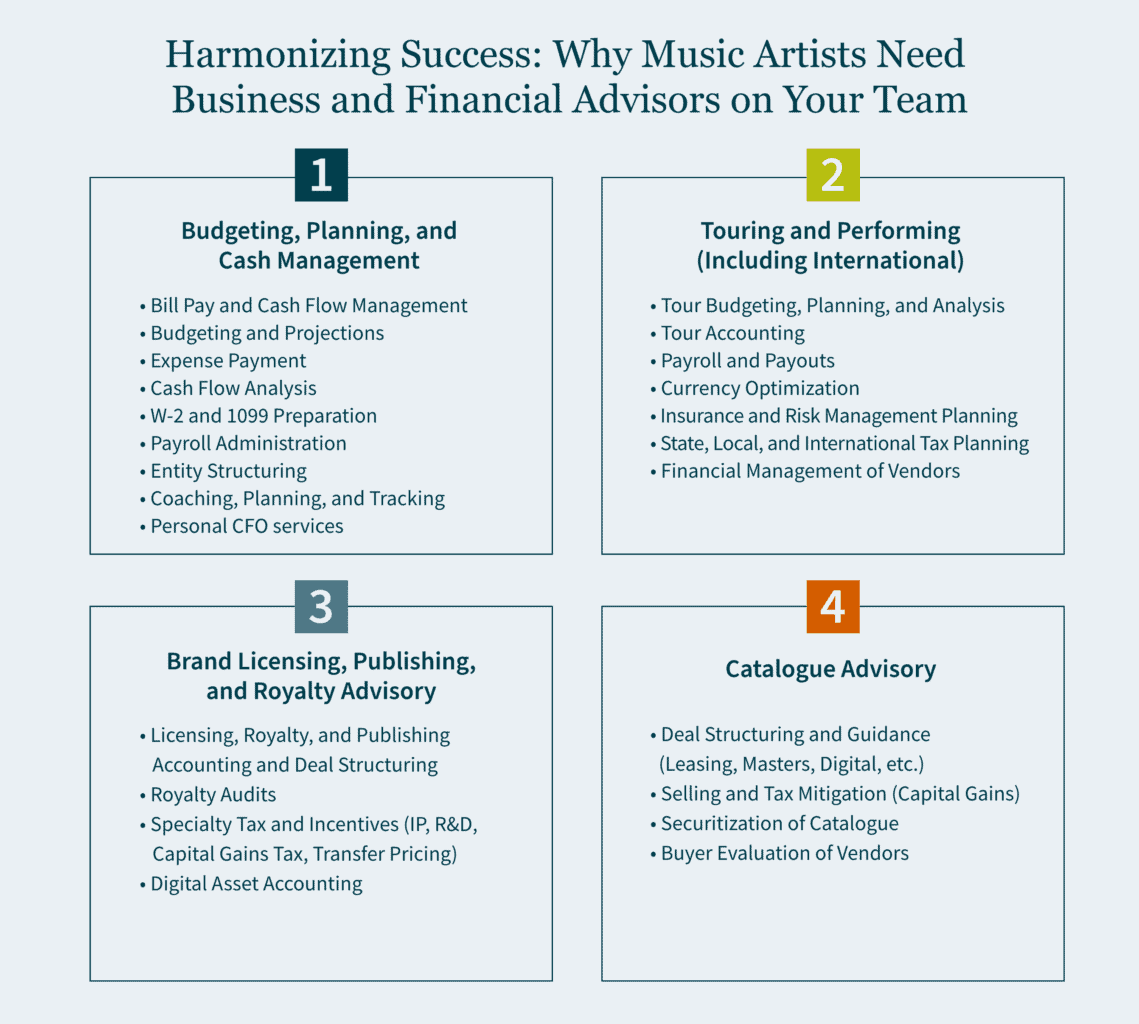

- To fully capitalize on these opportunities, artists must surround themselves with a team of expert advisors to help navigate all the financial, accounting, and business intricacies involved.

~

The journey to success in the music industry is no longer a straight line. While the path to earning substantial revenue previously only had one route — through a major label — those days are gone. The digital age has ushered in a new era, where artists have many direct pathways to their fans and an array of new revenue opportunities.

But with new opportunities comes new challenges. Today’s artists have to figure out how to navigate, manage, and optimize numerous complex revenue streams with little guidance. This is why having a trusted team of advisors is essential to ensure you are getting the most from your artistic output — both in terms of building your fan base and your financial future.

Here’s how working with a top advisor can help you transform from artist to enterprise, adept at building diverse income streams and overcoming any associated financial hurdles.

1. Live Performances: Looking Beyond the Spotlight

Live performances and touring remain pivotal for musicians to generate income. However, the financial success of a tour is not just about what you’re getting paid; it’s also about what you’re spending. That’s why meticulous planning is essential. From production costs to transportation, a trusted advisor ensures every dollar is accounted for before signing any contracts. Artists can also leverage performances for additional revenue through avenues like live streaming, behind-the-scenes access, or even concert films (i.e., Taylor Swift’s Eras Tour film). Advisors can help structure those deals to optimize the highest take-home payout.

2. Merchandising: Capitalizing on Brand Appeal

Merchandising offers a lucrative avenue to capitalize on an artist’s brand and deepen fan connections. Advisors can guide artists through various merchandising paths — from direct sales to brand collaborations to affiliations — to help them determine the best financial option. While direct sales may seem the most appealing on paper (where you might see numbers like “90% profit”), the associated responsibilities, such as sales tax management and warehousing, shipping, and staffing considerations, need careful evaluation. A seasoned advisor helps strike the right balance between profit and practicality.

3. Licensing and Sponsorships: Negotiating the Right Deal

Licensing and sponsorships have become integral to the music industry, with brands using music to sell everything from cars and sneakers to movies and fast food. Advisors play a crucial role in evaluating and negotiating these deals — ensuring you are getting fairly compensated for your name and image, and the opportunity aligns with your brand and goals. The evolving licensing landscape—with artists now able to self-publish and go through Spotify, Apple, and other platforms—has made getting licensing deals done easier. One independent artist we work with got a six-figure deal when a network went to TuneCore looking for music to use in a TV show.

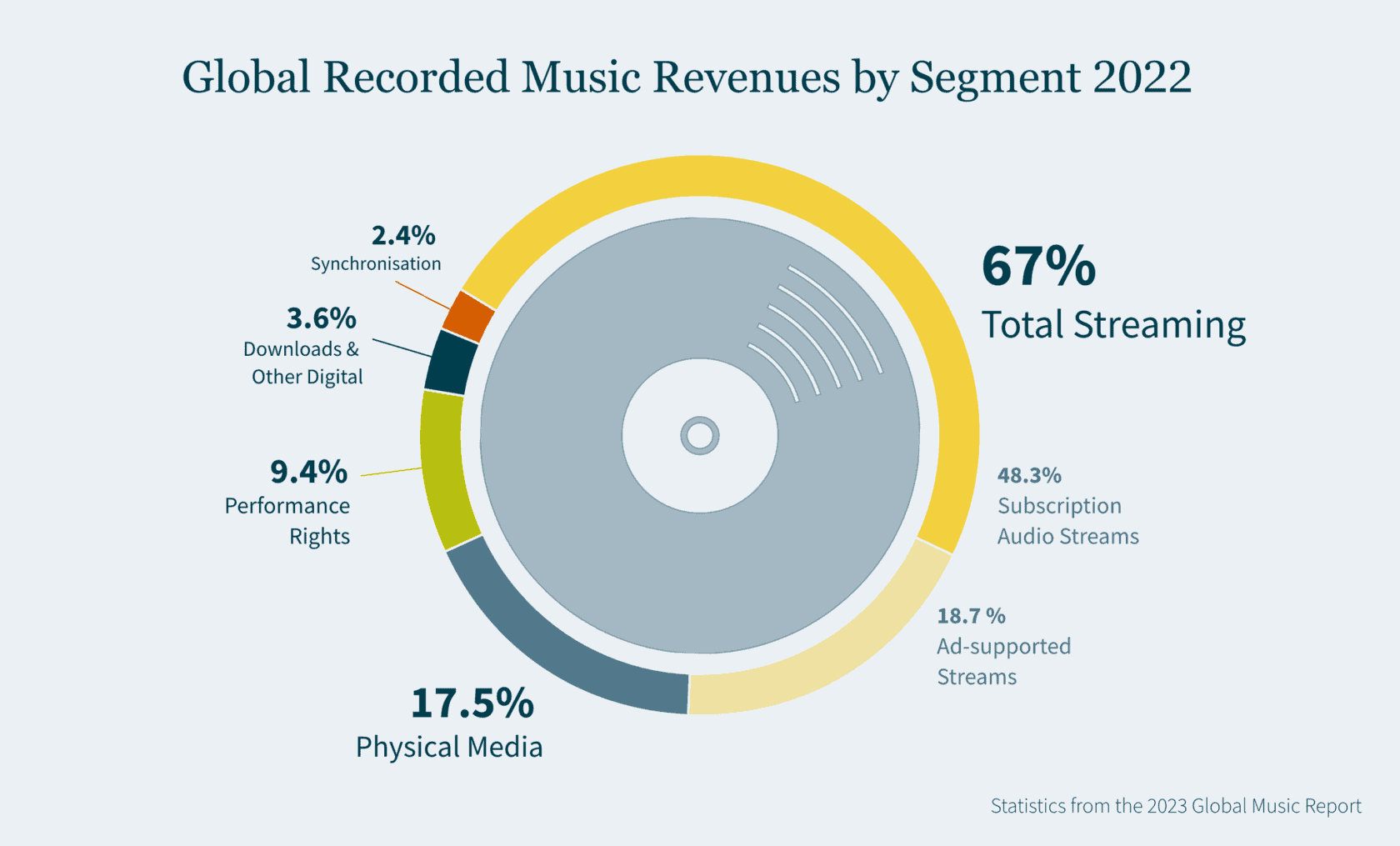

4. Streaming Revenue: Making the Most of Royalties

Music streaming platforms dominate the music consumption landscape today. While streaming royalties may be lower than what an artist receives from radio spins, terrestrial radio cannot touch the real-time data streaming provides (providing demographics of who is listening to your music, where they are listening, etc.). When it comes to managing streaming royalties, it pays to have a trusted advisor to track your royalties across all platforms — analyzing streaming data and royalty statements to ensure proper payment and identifying any discrepancies. Advisors also can strategize royalty planning, including estimated tax payments on royalties to avoid penalties, and help negotiate more favorable distribution deals with streaming platforms, exploring creative arrangements and exclusive partnerships.

5. Creator Content: Creating a Consistent Revenue Driver

In today’s creator economy, valued at over $100 billion, creating content is a powerful revenue stream. Many music artists are augmenting their income to the tune of six-to-nine figures a year by creating content for TikTok, YouTube, podcasts, NFTs, as well as a variety of other media and platforms. Advisors can guide you in navigating the challenges that arise from managing online content revenue — which often trickles, and then floods in, from multiple sources, and can quickly become unwieldy without a system in place to manage it. Proper financial management, including tax planning and budgeting, becomes crucial as content creation becomes a more prominent income source.

6. Catalogue Monetization: Structuring Your Ideal Sale

High-profile artists like Dr. Dre and Justin Bieber have recently sold their catalogue rights for large chunks of change. Catalogue monetization is the one time you are in complete control of your asset; you can carve out whatever deal you want (10-year, 20-year, 50%, 80%, etc.). Advisors guide artists in choosing the right partners, structuring deals, and determining the extent of the catalogue to sell. Your advisor will also help you weigh the tax considerations of collecting royalties versus selling all or some of your catalogue (royalties are taxed at 37%, while catalogue sales are taxed at 20%), and set up your sale in the most tax-efficient manner possible (for example, installment sale vs share sale). This one-time opportunity demands careful deliberation, and having the right team advising on nuances is paramount.

Building the Team Around Your Team

Moving from artist to enterprise means building a team to help you succeed. Your advisors are your team around your team. Much like a corporation brings in consultants, having seasoned business advisors available when you need them will help you make informed decisions to grow your brand and secure your financial future.

How We Can Help:

Our Entertainment, Sports, and Media (ESM) practice helps music artists at all stages, from rising stars to legends, offering financial, tax, and business management services to help you build your brand and maximize opportunities. Contact our ESM team today to learn how we can help take your music career to the next level.

- Whether you want to sell all or a portion of your music catalog, doing so can be very lucrative as you seek to achieve short- and long-term financial goals.

- Some factors to consider include your catalog decay, future album aspirations, and potential collaborations with other artists, as well as the fan-artist relationship.

- There is a four-step process to deciding to sell: determine the details, know your goals, be realistic, and reach out to the professionals for guidance.

Almost weekly, we’re hearing news of artists, songwriters, and producers selling all or part of the rights to their catalogs – and for big numbers:

- Justin Bieber: $200 million

- Dr. Dre: $200 million

- Stevie Nicks $100 million

- Future: $75 million

- Metro Boomin: $70 million

Some of these sales represent entire bodies of work. Others cover portions of work over a period of years and exclude high revenue-producing albums and tracks that will continue to generate wealth for years to come.

As a CPA, CGMA, and a veteran of the music industry, my Entertainment, Sports, and Media team and I can help you understand your options and determine the best way forward for you, right where you are in your career.

You may be thinking about selling all or a portion of your catalog for any number of reasons. We work with clients who have been motivated by the financial setbacks they experienced from tour cancellations due to COVID-19 restrictions, others who have new albums or tours they will be able to fund with lump sum payouts, and those who are ready to retire and enjoy the benefits of their life’s work.

The market is still good right now for investible music rights

Whether you act on it now or consider it as an option for the future, this is a good time to give it some thought and make a realistic assessment.

Radio airplay and sync licensing, as well as streaming on Spotify, Pandora, Apple Music, and other platforms, has the potential to drive significant revenue for artists. This is especially true for the top 1% who command about 90% of the revenue generated from the platforms. It is a long game for many artists who want to achieve wealth through these channels. Artist-fan relationships that can stand the test of time and drive ticket sales, merchandise sales, and album downloads have become even more critical to long-term success.

Should you sell?

At the right level, the kind of payout a catalog sale provides can be life-changing and even have a generational impact.

If you need liquidity fast, and without strings or ties to investors, selling your catalog can be a great way to get it. You can benefit from that money all at once, and from a tax standpoint, you’re going to pay a maximum tax rate of 20% on any proceeds (capital gains tax) you make from the sale. By contrast, if you keep your catalog in place and assume you’d earn revenue on all of it via streaming, you would have those assets taxed as income at a much higher rate. It can be as high as 37% based on your income level, year-after-year.

However, sync licensing, streaming popularity, and playlist rotations don’t last forever. Music and catalogs experience “catalog decay,” or the rate at which your music declines in consumption over time. Selling while the current value is up can be a wise choice. There are exceptions, as we saw last year with Kate Bush when her 80s hit “Running Up That Hill” became the most streamed song on Spotify globally, fueled by a sync licensing deal with the hot Netflix series Stranger Things. It is impossible to predict when one of those gems will hit, but in the event of a sale, the purchaser would have benefited from those royalties.

Honestly appraise where you are in your career and your album activity

Every artist is unique with a unique set of circumstances. Let’s look at the examples mentioned above:

- Dr. Dre is 58 and his sale worth $200MM+ gave him a huge influx of cash from royalties from two of his solo albums and his share of N.W.A. artist royalties, but he still has other revenue-producing assets and is currently on tour and has years of touring and album productivity ahead.

- Metro Boomin is 29 years old and has years of creative time ahead of him with $70MM from his catalog sale.

- Future is 39 years old, and with his $75MM in catalog sales of 612 songs from 2004-2020, this still leaves him with plenty of streaming revenue from smash hits and Grammy Award winners from 2021 and into the future.

- Stevie Nicks is 74 and is now $100MM wealthier from an 80% sale of her catalog in 2020. She is still actively touring, but she has wealth if she decides to slow down and still maintains 20% of her catalog for ongoing revenue.

- Justin Bieber is 29 years old but just cancelled the international leg of his tour due to his neurological health diagnosis; he now has $200MM he can count on for life and generational financial planning regardless of how he decides to, or is able to, proceed with his music career.

Evaluate how many albums and collab projects you are interested in pursuing as well as how many tours you think you have ahead of you. If you work with other artists, or crossover into different genres, you can cultivate larger audiences and grow your fanbase beyond its current limits.

If you’re considering selling your music rights, look at this four-step process:

Step 1: Determine the details.

What rights do you actually own? How much money have those rights made you in the last three years? Knowing this could help you determine how much they’d be worth if you sold them today and it will help you place a valuation on the catalog.

Who’s the potential buyer? Is this a buy and hold type of buyer? Is this a buyer who’s going to actively work your music catalog to increase its revenue, and your popularity? We know what questions to ask potential buyers to help you make the most informed decision.

Step 2: Know your personal and professional goals.

By doing this, you can balance them against the tax implications of selling by your catalog. It is your life, and you have your own personal and professional short- and long-term goals. Whether it’s sending your first-born to college or funding your next album or multi-media project independently, you have the power to use your assets in a meaningful way to enable you to attain your goals.

Step 3: Be realistic.

If you decide to sell, understand that not all catalog sales are going to yield the kind of sales that make Billboard magazine headlines. Level set your expectations with how successful you have been over the past few years, and how much you have been earning in publishing rights and streaming.

Step 4: Begin a conversation with us.

We know musicians. We know the industry. We know music. We know taxes. And we know there are options between selling versus leasing catalogs and choices between selling all or just portions of catalogs.

We’ve got you. MGO can be a steadfast partner through every step of this process to help you make the choice that is right for you and your family now, and for generations to come.

How we can help you reach your goals with catalog sales

Your music is your life — we get that. In the end, it’s one of the greatest legacies you’ll leave behind. Connect with our Entertainment, Sports, and Media practice to determine if monetizing your music catalog is the best move for you — and how it can help you reach both your professional and financial goals on a larger scale.

About the author

Tony Smalls is the leader of our Entertainment, Sports, and Media (ESM) practice and helps culture-defining entertainers, athletes, and other high-net-worth individuals build and protect their wealth while maximizing growth opportunities in today’s fast-evolving media marketplace. He specializes in accounting, finance, tax strategy, financial planning, and analysis, financial reporting, and contract/deal negotiations, working heavily on prospective investments like live music tours.

]]>Amid the uncertainty and concerns surrounding the COVID-19 outbreak, healthcare providers, public-health specialists, government officials and investors (and the general public) are looking to the biotech industry to create a “game-saving” vaccine against the novel coronavirus.

This optimism, and pressure, is particularly visible in the stock market where – even during the carnage of recent weeks – the biotech industry has held up better than others: the year-to-date decline of the Nasdaq Biotech Index, for instance, was only about half the selloff suffered by the broader market.

And while the industry arguably has performed well, it nevertheless has encountered difficulty on several critical fronts:

- Clinical trial delays and suspensions

- Supply chain failures

- Approval and application delays

“The COVID-19 pandemic represents a significant, ongoing public health threat and has created an unprecedented burden on healthcare systems across the globe,” says Jay Luly, Chief Executive Officer of Enanta Pharmaceuticals. “With the safety of our clinical trial participants in mind, coupled with a desire to alleviate many of the resource constraints at clinical trial sites, Enanta has proactively decided to make adjustments to some of our clinical programs.”

In the following, we take a deeper look at these three issues and the impact they are having on the industry, as well as an analysis of some the potential changes that could impact the biotech industry going forward.

Impact on clinical trials

There is unanimous agreement that COVID-19 already is causing significant delays and suspensions in clinical trials. Why this is important: Absent trial data, new drug filings likely will be delayed … meaning some important new medicines will take longer to reach the market.

BIO, the industry trade group, cites two additional issues that could affect trial schedules. They are:

- Missing or delayed data collection from ongoing clinical trials, particularly at hospital sites overwhelmed by COVID-19 cases

- Difficulties getting new clinical trials up and running because patients are reluctant to enroll or unable to visit hospitals

This is no small matter. Biotech and pharma, together, have some 120 Phase 3 clinical trials (with top-line data readouts) expected before the end of the year, according to BioMedTracker.

Eli Lilly, for instance, said it will delay the start of new clinical trials and suspend enrollment in “most” ongoing studies. Trials in which patient enrollment has already been completed will continue. Lilly is listed as the sponsor of 86 clinical trials currently enrolling patients, including 30 in Phase 3, according to ClinicalTrials.gov. Another 78 studies are active but no longer recruiting patients.

Others recently taking similar actions include Pfizer, Merck, Bristol Myers Squibb, Provention Bio and Galapagos. Each has paused the launch of some new studies, as well as enrollment in some ongoing studies.

The FDA has issued new guidelines designed to help the companies maneuver through this challenging period. Among other things, it offers standards for ensuring the safety of trial participants and maintaining compliance with good clinical practice.

It’s impossible to know how many clinical trials will be affected adversely by the coronavirus outbreak, but the BioMedTracker database features 120 Phase 3 clinical trials being conducted by biotech and pharma companies with market values greater than $300 million. All of these clinical trials were expected to announce top-line results before the end of the year.

At stake are some closely followed drugs with blockbuster projections:

- Asthma medicine tezepelumab from Amgen and AstraZeneca

- Rare disease treatment mitapivat from Agios Pharma

- Heart failure drug omecamtiv mecarbil from Amgen and Cytokinetics

- Hemophilia therapy fitusiran from Sanofi and Alnylam Pharma

The database also includes mid-stage, or Phase 2, clinical trials, some of which could also serve as the basis for FDA submissions. Some 160 such studies have trial results scheduled for this year.

Another potential problem is the fact that the industry outsources much of the day-to-day operations of clinical trials to contract research organizations (CROs) like IQVIA Holdings (IQV), PRA Health Sciences (PRAH), Syneos Health (SYNH), and Medpace Holdings (MEDP). These CROs monitor clinical sites by assigning teams to the clinics to verify data in the trial database accurately reflects the patient’s medical records.

Some clinics, however, have stopped allowing clinical trial monitors on site. And that means companies are unable to “lock” the database (an essential step that precedes analyzing the data).

Patient behavior, too, is having an impact on trials.

A survey by Continuum Clinical, a consulting firm that works with drug makers and trial sites, found that:

- One-third of clinical trial sites expect COVID-19 to have a “big or extremely big” impact on their ability to recruit patients for new trials or keep enrolled patients in existing studies

- 39 percent of 170 clinical trial sites in the U.S. believe patients will be much less or somewhat less likely to enroll in new trials

- 25 percent of the sites expect patients currently enrolled in a trial to be much less or somewhat less willing to continue participating

COVID-19’s impact on supply chains

Expect supply disruptions or shortages of critical medical products in the U.S. So says Dr. Stephen Hahn, FDA Commissioner.

What’s affected:

- Manufacturing and importing active pharmaceutical ingredients (APIs) and excipients

- Manufacturing facilities will be stretched by employee absences

- Training of employees assuming new responsibilities will be critical

- Independent laboratory testing associated with manufacturing may be slowed due to demands for testing related to COVID-19

The agency has been active: It has contacted more than 180 drug companies to discuss the requirement to notify the FDA of supply disruptions and to ask them to evaluate their supply chain. The agency says its focus is on China, but that all supply chains will be impacted.

Application/approval delays

Application and approval timelines also could be at risk. Wall Street analysts worry the COVID-19 outbreak could result in regulatory employees having to work from home for an extended period, regulators becoming infected, or FDA bandwidth being overwhelmed by the virus itself.

Moreover, in instances where a sponsor has an new drug application (NDA), abbreviated new drug application (ANDA), biologic license application (BLA) or application supplement pending with the FDA, they could encounter delays and find the agency not in alignment with their timetables.

Industry press also has reported that the Center for Drug Evaluation and Research (CDER) has cancelled all non-essential travel for the next few weeks. Additionally, all CDER outside meetings, conferences and workshops will be postponed through April. FDA staff have further been encouraged to hold teleconferences rather than in-person meetings with external persons.

Biotech and lifesciences going forward

Predictions, of course, are somewhat chancy given the multiple unknowns at this point. However, there are some emerging developments that seem more likely than others to have enduring impact. Here are five to consider.

Virtual Trials

Given the concerns about interruptions and postponements to clinical trials, virtual trials are likely to become the rule, rather than the exception, in the not-too-distant future. What the FDA currently suggests: virtual visits, phone interviews, self-administration and remote monitoring. These adjustments already are being used during this period of quarantines, travel limitations and closings and the new procedures may get locked in over time.

Friendly FDA

Biotech companies should encounter a very friendly FDA. Over the past 10 years, the agency’s annual approval rate of novel drugs has more than doubled, reaching 48 last year. There’s no reason to believe that trend is going to change. And that should be good news for biotech companies and their pipelines.

Scrutiny of Imports

Imported drug products are facing increased scrutiny at U.S. ports of entry and it’s hard to see the U.S. backing off from that standard in the future. The FDA warns it may deny entry of unsafe products, conduct physical examinations and/or product samplings, review a company’s previous compliance history, and request records in advance/instead of on-site drug inspections.

Restructured Supply Chains

China-based companies are critical components of the international supply chains of multiple industries. Biotech is one of them. Pricing, subcontracting and other factors have contributed to the growth and entrenchment of this structure. Now, however, the chaos caused by COVID-19 has underscored the unprecedented country risk that has been created in the process. Expect efforts aimed at regionalizing supply chains, developing second sources and creating proprietary stockpiles.

More Private/Public Partnerships

Look for greater cooperation between public and private organizations. Real-time example: Governor JB Pritzker’s recent announcement of a new partnership between the state of Illinois and the Illinois Manufacturers’ Association (IMA) and the Illinois Biotechnology Innovation Organization (iBIO) to increase in-state production of essential supplies.

Living Your Vision, Part 2: How to Create an Honest Brand for Your Present & Future >

]]>Everything changes, except when it doesn’t

Time and time again we’ve seen reactions to various accounting scandals, after which new policies, procedures, and legislation are created and implemented. An example of this is the Sarbanes-Oxley Act (SOX) of 2002, which was a direct result of the accounting scandals at Enron, WorldCom, Global Crossing, Tyco, and Arthur Andersen.

SOX was established to provide additional auditing and financial regulations for publicly held companies to address the failures in corporate governance. Primarily it sets forth a requirement that the governing board, through the use of an audit committee, fulfill its corporate governance and oversight responsibilities for financial reporting by implementing a system that includes internal controls, risk management, and internal and external audit functions.

Governments experience challenges and oversight responsibility similar to those encountered by corporate America. Governance risks can be mitigated by applying the provisions of SOX to the public sector.

Some states and local governments have adopted similar requirements to SOX but, unfortunately, in many cases only after cataclysmic events have already taken place. In California, we only need to look back at the bankruptcy of Orange County and the securities fraud investigation surrounding the City of San Diego as examples of audit committees that were established in response to a breakdown in governance.

Taking your audit committee on the right mission

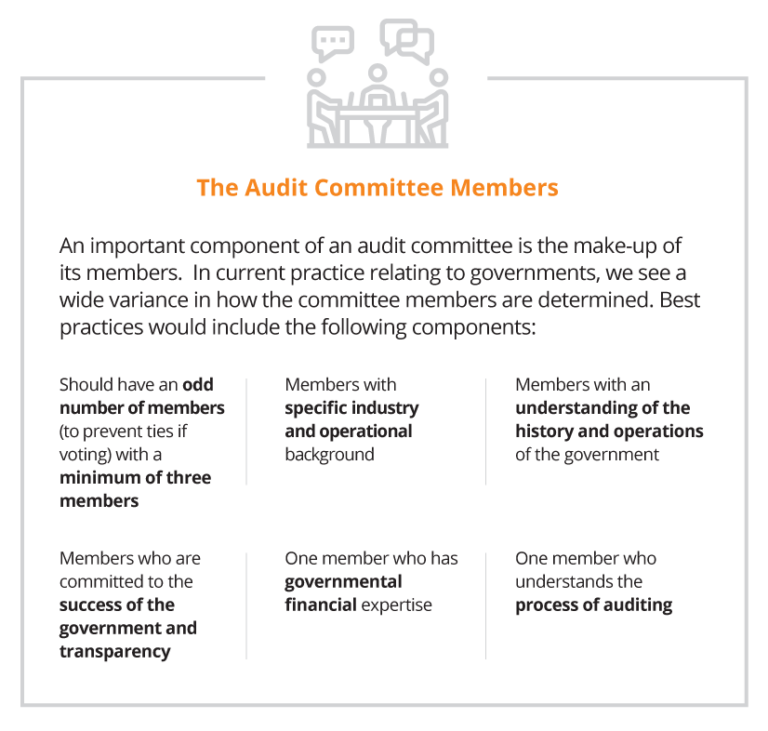

Governments typically establish audit committees for a number of reasons, which include addressing the risk of fraud, improving audit capabilities, strengthening internal controls, and using it as a tool that increases accountability and transparency. As a result, the mission of the audit committee often includes responsibility for:

- Oversight of the external audit.

- Oversight of the internal audit function.

- Oversight for internal controls and risk management.

Chart(er) your course

Most successful audit committees are created by a formal mandate by the governing board and, in some cases, a voter-approved charter. Mandates establish the mission of the committee and define the responsibilities and activities that the audit committee is expected to accomplish. A wide variety of items can be included in the mandate.

Creating the governing board’s resolution is the first step on the road to your audit committee’s success.

Follow the leader(ship)

In practice we see a combination of these attributes, ranging from the full board acting as the audit committee, committees with one or more independent outsiders appointed by the board, and/or members from management and combinations of all of the above. While there are advantages and disadvantages for all of these approaches, each government needs to evaluate how to work within their own governance structure to best arrive at the most workable solution.

Strike the right balance between cost and risk

The overriding responsibility of the audit committee is to perform its oversight responsibilities related to the significant risks associated with the financial reporting and operational results of the government. This is followed closely by the need to work with management, internal auditors and the external auditors in identifying and implementing the appropriate internal controls that will reduce those risks to an acceptable level. While the cost of establishing and enforcing a level of zero risk tolerance is cost prohibitive, the audit committee should be looking for the proper balance of cost and a reduced level of risk.

Engage your audit committee with regular meetings

Depending on the complexity and activity levels of the government, the audit committee should meet at least three times a year. In larger governments, with robust systems and reporting, it’s a good practice to call for monthly meetings with the ability to add special purpose meetings as needed. These meetings should address the following:

External Auditors

- Confirmation of the annual financial statement and compliance audit, including scope and timing.

- Ad hoc reporting on issues where potential fraud or abuse have been identified.

- Receipt and review of the final financial statements and auditor’s reports

- Opinion on the financial statements and compliance audit;

- Internal controls over financial reporting and grants; and

- Violations of laws and regulations.

Internal Auditors

- Review of updated risk assessments over identified areas of risk.

- Review of annual audit plan, including status of the prior year’s efforts.

- Status reports of ongoing and completed audits.

- Reporting of the status of corrective action plans, including conditions noted, management’s response, steps taken to correct the conditions, expected time-line for full implementation of the corrective action and planned timing to verify the corrective action plan has been implemented.

Establish resources that are at the ready

Audit committees should be given the resources and authority to acquire additional expertise as and when required. These resources may include, but are not limited to, technical experts in accounting, auditing, operations, debt offerings, securities lending, cybersecurity, and legal services.

Taking extra steps now will save time later

While no system can guarantee breakdowns will not occur, a properly established audit committee will demonstrate for both elected officials and executive management that on behalf of their constituents they have taken the proper steps to reduce these risks to an acceptable tolerance level. History has shown over and over again that breakdowns in governance lead to fraud, waste and abuse. Don’t be deluded into thinking that it will never happen to your organization. Make sure it doesn’t happen on your watch.

]]>Some have questioned the value of creating a brand for yourself. Does it really need to be done? Is it something that anyone actually looks at? Is it simply a social construct for media purposes that has no genuine bearing on the real world, and your life?

There is a simple answer. While your brand may be a “social construct” it can have an indelible impact on your life and career. When planned and utilized correctly, your brand is an essential part of the early journey in defining your vision for yourself and your continued financial success and security. The first step when approaching yourself as a brand is to decide what that brand and you will stand for. It should serve as a reflection of your current values and also what you aspire to achieve your dreams.

Develop your brand by watching and listening

Conceiving your brand starts with basic tenants you learned in elementary school: watch and listen. Take a look at people in your world and your chosen field. Look beyond any pre-conceived notions you may have and really look and listen to who they are, and the message they are projecting to the world. Examine them in person as well as via any kind of digital or social media and decide for yourself whether that person is succeeding or failing to represent what they are putting into the world. Look at any kind of context they put out in terms, of public goals, mission statements, and information for their personal journey and vision.

Doing your homework ahead of time and developing an understanding of what works and what doesn’t, helps you determine the trajectory of your brand and how it will propel you forward in living your vision. Remember, you are your own mid-sized Fortune 500 Company, and you need to run your business affairs as such. No one invests personally or financially in a company that has unfocused goals, trajectory, or has a brand that seems off the mark or undefinable.

Be honest and truthful when creating your brand

The most important element in creating a brand for yourself is to be honest in what you are doing. There’s no lasting value in creating a brand and financial path that is no more than smoke and mirrors. Social media and the impression that you give people through your brand will appear hollow if you are not being truthful in what you are creating. Make sure that your brand represents your personal voice and views. Truth and hard work will always reap you a tangible benefit in the end. You can’t build a vision of the future on lies and public opinion. It’s much easier and more effective to maintain a brand that is honest and true. Sustaining falsehoods and superficial façades requires ten times the work and creates unnecessary risk and complexity.

Package your brand and create goals

Once you’ve decided how you are going to brand yourself, and what path you are taking; start working out a step by step financial plan with your advisors. There should be a series of definable goals and markers along the journey into living your vision. Working with your team of financial advisors, decide the duration of time you would like to spend on each element or part of your goals, and where exactly you see these goals fitting into the much larger picture of your present and future life.

Create your plan so that it is a package deal. It has to meet your needs, the needs of your financial vision, and all elements need to align correctly. All elements of your vision and financial scope need to feed into and allow your brand to exist on multiple planes and levels. Again, your finances should be run like a company’s, and there will always be elements that exist on separate levels but need to work in harmony for everything to move forward.

Earn your reputation for your brand

Reputations are earned, not just freely given. They take work, time, and patience. Creating and building your brand for yourself and your finances is no different. Stay true to what you and your financial advisory team have worked to create for you. This brand is a way to represent yourself in the world, and as such is as much a part of you as your body of work. In having others help you establish your brand, make sure you are doubling back to check on others and let everyone know that you are invested in them, just as much as you are in making this brand a reality and a success. Treat others well as you forge ahead to give your brand a life and longevity and keep it rooted in a reputation that you are working hard to maintain.

]]>This Tax Alert provides an overview of some of the most significant modifications to the U.S. international tax provisions affecting businesses and individuals. We urge clients to evaluate the impact of tax reform and discuss relevant changes with their tax advisors since many of the new provisions may bring about unintended tax consequences with respect to properly implemented structures under the previous U.S. international tax regime. Overall, the changes expand the base of cross-border income to which current U.S. taxation applies.

Additional tax alerts for Individuals | Business

Details of international provisions

Introduction of Participation Exemption System for foreign income

The Act introduces a dividend exemption system that applies to distributions made after December 31, 2017, which generally provides for a 100% dividend received deduction (“DRD”) for the foreign-sourced portion of dividends received by a domestic C corporation from a specified 10%-owned foreign corporation (other than a Passive Foreign Investment Company – “PFIC”) of which it is a U.S. shareholder, provided certain conditions are satisfied. The DRD is available only to C corporations that are not regulated investment companies (“RICs”) or real estate investment trusts (“REITs”).

Note that dividends received from PFICs do not qualify for the DRD and domestic C corporations may not claim foreign tax credits or a deduction for foreign taxes paid or accrued with respect to any dividend allowed the DRD.

To the extent earnings of foreign corporations are neither subpart F income nor subject to the minimum tax rule discussed below, the new participation exemption system moves the U.S. away from a worldwide taxation system towards a territorial tax system for earnings of foreign corporations.

Sales or transfers involving specified 10%-owned foreign corporations

Certain deemed dividends under Code section 1248 – resulting from the sale or exchange of stock of a specified 10%-owned foreign corporation held for over one year – qualify for the 100% DRD under the new law.

The provision also allows a U.S. shareholder to claim a 100% DRD on deemed dividends under section 964(e) resulting from the gain on the sale of foreign stock by a controlled foreign corporation (“CFC”).

Two new loss limitation rules are included in the provision, which are applicable to transfers and distributions made after December 31, 2017:

- A domestic corporation that is allowed a DRD is required to reduce its basis in the stock of the foreign corporation by an amount equal to the DRD, solely for purposes of determining the domestic corporation’s loss on the sale of stock of the foreign corporation.

- A domestic corporation is required to recapture certain foreign branch losses if it transfers substantially all of the assets of a foreign branch to a 10%-owned foreign corporation of which it is a United States shareholder after the transfer. The active trade or business exception of section 367(a)(3) is repealed for transfers made after December 31, 2017, which disfavors the use of foreign branches.

New mandatory repatriation

As a transition to the new participation exemption regime, a mandatory repatriation provision is included targeting previously untaxed earnings and increasing subpart F income by the shareholder’s pro rata share of each specified foreign corporation’s net untaxed post-’86 historical E&P, determined as of November 2 or December 31, 2017 (a measuring date). However, this mandatory inclusion is reduced (but not below zero) by an allocable portion of the taxpayer’s share of foreign E&P deficit of each specified foreign corporation and the taxpayer’s share of its affiliated group’s aggregate unused E&P deficit. Earnings attributable to the shareholder’s aggregate foreign cash position or liquid assets are subject to tax at a 15.5% rate, while earnings attributable to illiquid assets are subject to tax at an 8% rate.

The tax liability is payable over a period of up to eight years, at the election of the U.S. shareholder.

A special rule applies to S corporations under the mandatory repatriation provisions. S corporation shareholders may elect to continue to defer taxation of such foreign income until the S corporation changes its status, sells a substantial amount of its assets, ceases to conduct business, or the electing shareholder transfers their S corporation stock.

Non-corporate U.S. shareholders are exposed to the new mandatory repatriation rule if the specified foreign corporation is a CFC or any foreign corporation with at least one domestic corporate U.S. shareholder, even though the 100% dividend received deduction from foreign subsidiaries only applies to corporate U.S. shareholders under the Act.

Foreign tax credits and sourcing of income modifications

Foreign tax credits are allowed under the new law only with respect to foreign income taxes associated with the taxable portion of the U.S. shareholder’s net mandatory inclusion. Foreign tax credits are disallowed with respect to foreign income taxes attributable to the participation deduction. Taxpayers may not elect to take a deduction for foreign taxes that are disallowed as foreign tax credits.

The U.S. shareholder’s section 78 gross-up should also reflect the portion of foreign taxes attributable to the U.S. shareholder’s net mandatory inclusion.

The deemed paid foreign tax credit provisions under Code Section 902 are repealed while the deemed paid foreign tax credit provisions for subpart F inclusions under Code Section 960 are retained but modified, providing a credit on a current year basis. Foreign tax credits will be counted on an annual basis and will no longer be pooled.

Foreign taxes attributable to distributions of previously taxed income (“PTI”) are also regulated under the Act

The Act also revises the sourcing rules for income from inventory sales. Income from inventory sales is now sourced entirely based on the place of production and not allocated 50/50 to the place of production and the place of sale (based on title passage).

A separate foreign tax credit limitation basket is created under the new law for foreign branch income.

The Act repeals the fair market value method of interest expense apportionment. Taxpayers are now required to allocate and apportion interest expense of members of an affiliated group using the adjusted basis of assets.

New provisions regarding foreign passive and intangible income

The Act has new provisions that adopt a minimum tax on “global intangible low-taxed income” (“GILTI”) and a new special deduction for certain “foreign-derived intangible income” (“FDII”), subject to certain exceptions.

Regardless of whether distributions are actually made by a CFC during the tax year and similarly to the manner in which subpart F income inclusions operate, a U.S. shareholder of a CFC is now required to include in income its pro rata share of GILTI allocated to the CFC for the CFC’s tax year that ends with or within its own tax year.

GILTI provisions target a portion of the CFCs’ active (non-Subpart F) income and tax it at an effective tax rate of 10.5% prior to 2026 — generally speaking, the targeted portion is equal to the net income over a routine or ordinary return, defined as the excess of an implied 10% rate of return on the adjusted basis of the CFC’s tangible depreciable property used in generating the active income.

In conjunction with the new minimum GILTI tax regime, excess returns earned directly by a U.S. corporation from foreign sales (including licenses and leases) or services defined as FDII are now also subject to a 13.125% effective tax rate (increased to 16.406% starting in 2026). FDII is the amount of a U.S. corporation’s “deemed intangible income” that is attributable to sales of property (including licenses and leases) to foreign persons for use outside the U.S. or the performance of services for foreign persons or with respect to property outside the U.S.

Corporate shareholders are allowed a deduction equal to maximum 50% of GILTI (reduced to 37.5% starting in 2026) plus any corresponding Code section 78 gross-up plus maximum 37.5% of taxpayer’s FDII (reduced to 21.875% starting in 2026) – combined, these three components comprise the GILTI deduction. Not that the total GILTI deduction cannot exceed a corporation’s taxable income. S corporations or domestic corporations that are RICs or REITs are not allowed to claim this deduction. Transfers to foreign related persons generally do not qualify for FDII benefits.

U.S. shareholders can make a Code Section 962 election with respect to GILTI inclusions, which subjects the shareholder to tax on the GILTI inclusion based on corporate rates, and allows the electing shareholder to claim foreign tax credits on the inclusion as if the shareholder were a domestic corporation.

Modification to subpart F rules

The inclusion based on the withdrawal of previously excluded subpart F income from qualified investment is repealed.

The provision that provides for the inclusion of foreign base company oil-related income is repealed; hence, previously excluded foreign shipping income of a foreign subsidiary is no longer subject to current U.S. taxation under the subpart F rules if there is a net decrease in qualified shipping investments.

Stock attribution rules for determining status of a foreign corporation as a CFC are modified, which makes it more likely for a foreign corporation to be treated as a CFC as a result of the stock of certain related foreign persons being attributed downward to a U.S. citizen. As a result, for example, stock owned by a foreign corporation would be treated as constructively owned by its wholly-owned domestic subsidiary for purposes of determining the U.S. shareholder status of the subsidiary and the CFC status of the foreign corporation.

The new law eliminates the requirement that a corporation be a CFC for 30 days before subpart F inclusions apply.

Prevention of base erosion

The Act includes additional anti-base erosion measures, including a Base Erosion Anti- Abuse Tax (“BEAT”) for certain payments paid or accrued in tax years beginning after December 31, 2017. In general, the BEAT imposes a minimum tax on certain deductible payments made to foreign affiliates, including royalties and management fees, but excluding cost of goods sold.

Income shifting through intangible property transfers is further limited. This includes treating goodwill and going concern value and workforce in place as section 936(h)(3)(B) intangibles and, requiring the use of the aggregate basis valuation method in the case of transfers of multiple intangible properties in one or more related transactions. This applies if it is determined that an aggregate basis achieves a more reliable result than an asset-by-asset approach.

Deductions for certain related party interest or royalty payments paid or accrued in certain hybrid transactions or with certain hybrid entities are now disallowed under certain circumstances. The Act provides that the Secretary of State shall issue regulations or other guidance as may be necessary or appropriate to carry out the purposes of the provision for branches (domestic or foreign) and domestic entities, even if such branches or entities do not meet the statutory definition of a hybrid entity.

New rules were incorporated to limit the deductibility of interest within a corporate group.

Surrogate foreign corporations are not eligible for the reduced rate on dividends under the Act.

MGO insights

The Tax Cuts and Jobs Act is the largest overhaul of the tax system in over three decades and will have a significant impact on U.S.-based multinational companies as well as inbound businesses. The bill fundamentally changes the landscape of U.S. international taxation. We recommend that companies, individuals, and flow through entities engaged in cross border business discuss their specific situation with MGO’s experienced international tax professionals and consultants – we are here to help you navigate the changes of this comprehensive tax reform.

]]>The deadline for implementation is Jan. 1, 2018, for calendar year publicly-held companies, and Jan. 1, 2019, for calendar year privately-held companies. Although the implementation date for non-public companies is over one year away, our dedicated Government Contractor practice specialists encourage clients to start evaluating the changes now to understand the impact on their financial statements.

In this article, we will provide an overview of the revenue standard’s main provisions, provide best practices for implementation methods, and identify key issues that may impact government contractors during implementation. This guidance will be especially beneficial to entities following the AICPA’s Industry Revenue Recognition Task Force for Aerospace & Defense.

Main provisions of the new standard

The new standard is more principle-based than current revenue recognition guidance and will require government contractors to exercise more judgement. The principle is based on a five-step model from the AICPA Revenue Recognition Guide:

Step 1: Identify the Contract with a Customer

The standard includes characteristics that need to be met for a contract to permit revenue recognition. In general, a contract exists if there is an agreement between a buyer and seller that creates enforceable rights and obligations for the two parties. Only when there is such an agreement is there any revenue to recognize under Topic 606. This step sets the base to which the rest of the steps in the model are applied.

Also included in this step is guidance on when to combine multiple contracts into a single contract for revenue recognition purposes, and what to do if a contract is modified, thereby changing the identified contract with a customer.

Step 2: Identify the Performance Obligations in the Contract

Among the rights and obligations that will be set forth in the contract (either explicitly or implicitly), are:

- 1. The right of the buyer to receive goods or services from the seller, and;

- 2. The obligation of the seller to provide those goods or services to the buyer.

Once the contract has been identified, the seller identifies what goods or services it has promised to provide to the buyer. The standard includes guidance on evaluating provisions of a contract to determine whether they should be regarded as creating promised goods or services.

If multiple goods or services are promised, the seller must determine whether each good or service is distinct from other goods or services in the arrangement, or must instead be combined with other goods or services to form a bundle that is distinct from other goods or services in the contract.

Each good or service that is distinct, or each bundle of goods or services that is distinct, is called a performance obligation under the standard. Performance obligations are then used as units that are evaluated for revenue recognition purposes in the rest of the model.

Step 3: Determine the Transaction Price

In addition to rights and obligations over goods or services to be provided, a contract will include:

- 1. The obligation of the buyer to pay the seller for the goods or services, and;

- 2. The right of the seller to collect that payment from the buyer.

Those provisions provide a starting point for determining the transaction price. Often, the payment terms are fixed and payment is due when goods or services are delivered. In that case, it is simple to determine the transaction price to be used in recognizing revenue.

However, the vendor needs to determine whether all amounts to be collected are appropriately reported as revenue. In addition, the contract may include terms that make the transaction price variable. For example, the transaction price could vary due to usage-based payments, award and incentive fees, rights of return or refund, or economic price adjustment.

Topic 606 explains when, and how much, variable consideration is to be included as part of the transaction price. This will generally require variable consideration to be included in the transaction price to the extent it is probable such consideration will become due under the contract.

Step 4: Allocate the Transaction Price to the Performance Obligations in the Contract

In this step, the transaction price determined in Step 3 is allocated, or assigned, to the performance obligations identified in Step 2. Obviously, if there is only one performance obligation, this allocation is easy, as the entire transaction price is allocated to the single performance obligation. However, if there are multiple performance obligations, the transaction price must be allocated to those performance obligations.

Generally, this is done based on the stand-alone selling prices of the performance obligations in the contract. The stand-alone selling price of a performance obligation may be objectively determinable if the performance obligation is regularly sold on a stand-alone basis. If it is not, its stand-alone selling price must be estimated through a reasonable technique.

Once stand-alone selling prices for all performance obligations are estimated, the transaction price is generally allocated based on the relative values of the performance obligations, effectively allocating any discount in the contract to the performance obligations on a pro rata basis.

Step 5: Recognize Revenue When (or as) the Entity Satisfies a Performance Obligation

Once the transaction price has been allocated to the performance obligations in the contract, the amount of revenue allocated to each performance obligation is recognized when, or as, the entity performs the obligation as required by transferring the promised goods or services that make up the performance obligation to the customer.

A good or service is deemed to be transferred to the customer when the customer gains control over the good or service. A customer sometimes gains control of promised goods or services as performance occurs over time. In other instances, the customer gains control of a promised good or service at a single point in time, often when something is physically delivered to the customer.

When a performance obligation is satisfied over time, the seller must determine an appropriate measure of its progress toward satisfying the performance obligation, and then recognize revenue based on that progress measurement applied to the amount of the transaction price allocated to the performance obligation.

When a performance obligation is satisfied at a point in time, the seller must determine the appropriate point in time at which to recognize as revenue the amount of the transaction price allocated to the performance obligation.

Implementation methods

Full retrospective application: Recast of prior period financial statements (with an adjustment to opening retained earnings for the first year presented). For example, for a public company, 2016 and 2017 would be recast to reflect the adoption of the new standard presented in the 2018 financial statements. The cumulative adjustment would be reflected as of Jan. 1, 2016.

Modified retrospective application: Cumulative effect of initially applying the standard is recorded as an adjustment to opening retained earnings of the period of initial application. Under the same example, 2016 and 2017 would not be recast in the 2018 financial statements. The cumulative adjustment would be reflective as of Jan. 1, 2018.

Implementation issues and guidance

For government contracts, the type of contract will determine if there will be a change from current revenue recognition practices. For time and materials and cost-plus-fixed-fee contracts, as well as services-based firm-fixed-price contracts, there will be minimal change to the total revenue and timing of revenue recognized under the new revenue standard. Under more complex contracts (i.e., award fees under cost-plus contracts, or firm-fixed-price contracts where the entity performs manufacturing, design, development, integration, and/or production), applying the new standard will require careful analysis and consideration, and could impact the timing of revenue recognition.

The AICPA’s Industry Revenue Recognition Task Force for Aerospace & Defense has identified various revenue recognition implementation issues and continually updates the list of issues as discussions continue.

The following are some of the key areas to consider when implementing the new guidance as noted in the AICPA’s Industry Revenue Recognition Task Force for Aerospace & Defense.

Acceptable Measure of Progress – what to consider when measuring progress towards completion of performance obligations satisfied over time.

Accounting for Contract Costs – considerations for applying the guidance in Financial Accounting Standards Board (“FASB”) Accounting Standards Codification (“ASC”) 340 for incremental costs of obtaining a contract, costs to fulfill a contract and amortization and impairment, to costs typically incurred in aerospace and defense contracts, including pre-contract costs and learning or start-up costs.

Variable Consideration – considerations for estimating the amount of variable consideration (incentive fees, award fees, economic price adjustments) in aerospace and defense contracts, the impact of subsequent modifications, and how to determine the amount of estimated variable consideration to include in the transaction price.

Significant Financing Component – considerations needed to assess whether a significant financing component exists in determining the transaction price for various types of aerospace and defense contracts.

Allocating the Transaction Price – considerations for determining how to allocate the transaction price to multiple performance obligations in aerospace and defense contracts.

Implementation plan for government contractors

The AICPA Financial Report Center developed an implementation plan that may be helpful as a starting point for developing your own implementation plan. Below are the high-level steps included in that plan.

- Designate the individual(s) responsible for overseeing implementation.

- Evaluate how the changes will impact how your company accounts for different types of revenue streams/contracts. Consider how the new standard will impact current performance metrics and compensation plans. Work with your auditor to discuss the completeness and accuracy of your analysis.

- Determine an implementation method (full or modified retrospective approach).

- Determine changes that may be needed within systems and/or software applications to facilitate revenue recognition under the new standard.

- Determine what interim disclosures may be required prior to the effective date.

- Develop a plan for implementation to incorporate the above steps, as well as train your staff.

- Educate the company’s management on the new standards and the impact you expect the changes to have on the company’s financial statements.

MGO has a dedicated Government Contractor practice with CPAs and industry specialists who are well-versed in the new standard and can assist in evaluating the impact of the changes on government contracts revenue recognition and financial reporting. We also assist our clients in implementing the new standard.

To learn more about how we can help, let’s talk.

]]>MGO Technology Group has leveraged contacts from the dark web, conversations with federal authorities, and other proprietary research and insight to provide an overview of the leading cyber threats cannabis enterprises face.

Who is targeting cannabis and where are they attacking?

Information gathered by MGO Technology Group from underground assets and federal investigations indicates that, to date, there is no specific group actively targeting the cannabis industry. But there are hackers focusing on three areas within the seed-to-sale lifecycle:

- Research and extraction

- Cultivation

- Consumption and retail operations.

Investigations revealed two incidents where intellectual property was stolen by a former employee due to partial or ineffective security practices. In addition to potential malicious insiders, external threat actors are expected to attack the research portion of the industry in order to steal intellectual property. Potential targets of hackers include strains being developed, marketing strategies, and technology practices related to cultivation.

Potential impact on hacked cultivators

The loss or modification of proprietary information, such as strain development and cultivation methodology, could severely impact the production of future products, result in a tampered or inferior product, or the loss of competitive advantage within the industry. While an increased timeline for a future product or loss of IP to a competitor would result in a negative financial impact, the release of a tampered product could also cause a negative reputational impact as well.

Risks presented by cannabis payment systems

The search for payment solutions in the notoriously cash-heavy cannabis industry has led to the emergence of a number of payment systems. While they may be convenient, they are a high-risk target for hackers. Mobile applications that are not securely developed or have appropriate oversight are at risk and provide an attack vector for malicious actors. The success breaching of an application could provide access to customer financial information, leading to mistrust of the application author and discontinued usage.

Protecting medical and customer information

As the legalization of medical and adult-use cannabis spreads across North America, the customer base will continue to expand making retailers increasingly high-priority targets of malicious actors. Medical information and Protected Health Information (PHI) are already highly valued assets for cyber-criminals.

Similar to other small businesses and early stages of a new industry, the protection and security of computers and networks involved with customer information is minimal or inefficient. Specifically, this involves the Point-of-Sale system and supporting infrastructure, two of the most targeted assets, a breach of which would result in the theft of customer information. Once again, a breach of customer information, especially PHI, will not only have a negative impact to the reputation of the retailer and industry overall, but could result in HIPAA violations resulting in millions of dollars’ worth of fines.

]]>The MGO | ELLO Cannabis Investment Review is the first publication of its kind for the cannabis industry. Developed in cooperation with PitchBook, the premier data provider for the private and public equity markets, the report offers a wide range of marketplace insights to an industry that is increasingly hungry for data.

The Review examines this generation’s most dynamic industry from a private market perspective, investigating venture capital and private equity trends, and the consolidating M&A deals reshaping the cannabis landscape.

The report finds that venture capital investment in cannabis has soared to new heights, far surpassing last year’s impressive rally, despite federal restrictions on banking and financing. Plus, investment in cannabis reached nearly $1.3 billion before the first half of 2019, exceeding last year’s tally of nearly $1 billion for all of 2018. The report goes on to examine a number key factors influencing cannabis industry growth, including:

- The growing cannabis ecosystem

- Location: The impact of federal, state and local laws on cannabis investments

- How to value cannabis startups

- What’s next in the cannabis industry?