Now is a good time to evaluate and improve your financial reporting process for grants. While grants are subject to many reporting requirements, we will focus on revenue recognition under accounting principles generally accepted in the United States of America (GAAP) and the schedule of expenditures of federal awards, as required by Uniform Guidance.

Financial reporting in accordance with GAAP

In June 2020, the Governmental Accounting Standards Board (GASB) issued Technical Bulletin No. 2020-1, Accounting and Financial Reporting Issues Related to the Coronavirus Aid, Relief, and Economic Security Act (CARES Act) and Coronavirus Diseases (TB 2020-1). TB 2020-1 helps governments navigate the complexities of accounting for CARES Act funding. It addresses issues such as the type of financial assistance, characterization of loss of revenue, and effect of amendments. While ARPA funds have their own complexities, the principles established in TB 2020-1 for the CARES Act translate well to ARPA, and GASB has not published further guidance for ARPA.

In TB 2020-1, GASB provides guidance that the Coronavirus Relief Fund (CRF) resources are voluntary nonexchange transactions subject to eligibility requirements. The Local Fiscal Recovery Funds in ARPA are like the CRF resources in the CARES Act and should be treated consistently. This means the award should be recognized in the period when all applicable eligibility requirements are met.

When evaluating revenue recognition for voluntary nonexchange revenues, remember that the recipient cannot incur allowable costs until there is an executed grant agreement. For the ARPA funds, this means the recipient has signed all the required documents accepting grant terms and conditions, and that the recipient has received confirmation of the award before the end of its reporting period.

The presumed applicable period is the immediate provider’s fiscal year and begins on the first day of that year, based on the provider’s appropriation to disburse the resources. For the CARES Act, few cities met the threshold for directly awarded metropolitan cities, which subjected them to the state’s provisions rather than as a direct recipient of the federal government. For example, California cities and counties that received pass-through awards from the State of California were unable to recognize grant revenue in fiscal year ended June 30, 2020, because the State of California did not make the appropriations available to governments until July 1, 2020, through passage of its budget act.

The ARPA funds, which were directly distributed to a considerably greater number of recipients, were appropriated immediately by the federal government upon signing ARPA into law. That means the direct recipients of ARPA funds and the non-entitlement units of governments that received their allocations from states that executed the awards before the end of the reporting period, may recognize revenue immediately upon execution of the award, if they met the eligibility criteria.

For those governments that received cash before the end of the reporting period, a liability should be reported for the portion of financial assistance that was not recognized as revenue. For those governments that did not receive cash before the end of the reporting period, a receivable should be reported for the portion of financial assistance that was recognized as revenue.

The possibility of a single audit

While many governments require an annual single audit due to the amount of federal awards received each year, many others are below the threshold for requiring a single audit. Funding related to COVID-19 resources may push more governments over that $750,000 threshold.

For governments unfamiliar with single audits, it is important to prepare. Taking inventory and reading the guidance provided by the Office of Management and Budget (OMB) and awarding federal agencies will help you understand and equip yourself to submit (and pass) a single audit.

What is the SEFA?

The schedule of expenditures of federal awards (SEFA) acts as a supplemental schedule to the financial statements that an organization produces when it is subject to a single audit requirement. This requirement is triggered when the federal expenditures reported on the SEFA exceed $750,000 or more over the organization’s fiscal year

Preparing the SEFA is no small task. It must be completed in accordance with the Uniform Guidance and include all federal expenditures. In addition to determining the amount of federal expenditures, the Uniform Guidance specifies how the amounts are to be reported. Individual federal programs should be listed by federal agencies, and pass-through entities should be noted as well.

The single audit and ARPA

On March 19, 2021, the OMB released a memo that detailed single audit updates to be aware of in ARPA. The updates give awarding agencies the discretion and the authority to grant some exceptions to recipients who are affected by the pandemic if they are permissible by law. These entities do not necessarily have to be recipients of COVID-19 related financial assistance to receive these exceptions.

The most notable update is the extension of the single audit submission due date. For those recipients who did not file their single audits with the Federal Audit Clearinghouse by March 19, 2021, and had fiscal year-ends through June 30, 2021, the submission of their reporting packages was extended to six months past the normal due date, and no action by the awarding agencies or recipients is necessary. However, the documentation showing the reason for the delay in filing must be retained.

Additional updates include:

- Awarding agencies may allow some necessary incurred pre-award costs.

- Awarding agencies may allow extensions of awards, which gives recipients more time to resume projects and expend the funds.

- Prior approval requirements may be waived.

- Awarding agencies can grant recipients up to a three-month extension beyond the normal due date to submit financial, performance, and other required reports.

- The award application deadlines can be flexible.

While it is clear the OMB is attempting to be reasonably flexible, maintaining clear documentation of your grants and expenditures will be helpful as new and changing guidance becomes available.

Understand the current requirements and look for changes

The pandemic threw many organizations into survival mode. However, with federal, state, and local support many have weathered the financial difficulties over the past 18 months as well as can be expected. As organizations move forward, they will have to account for how they survived, where the monetary support came from, and where the money went. The near future will require unprecedented diligence, flexibility, and perhaps most of all, patience.

MGO is here to help

Guidance over grant funding, especially as it relates to CARES Act and ARPA programs, are continuing to develop and evolve. It’s important to stay on top of the latest changes and updates, as utilization of these resources are critical to the financial recovery of your organization and the proper reporting of those resources to stakeholders and the federal agencies charged with oversight. If you need personalized guidance, don’t hesitate to reach out to your MGO contacts.

.

]]>Who is your grant administrator?

This seems like a simple question, but if an organization only has a few grants, grant administration may be one of many roles. Or, responsibility may be shared among several roles. That situation works until the size of the organization and the complexity of the grants make responsible grant management impossible.

When the responsibility and complexity of grant management becomes too demanding to include as one of many responsibilities, it’s time to identify one person to take the lead. Eventually, that person may build the team responsible for overseeing and coordinating grant administration.

It is easy to see the benefits of having one person develop the full knowledge of grant requirements and take responsibility for establishing policies and procedures for the organization. This person provides guidance for the organization and monitors compliance requirements. They also serve as the point person for grant related audits.

Do you have policies and procedures for grant administration?

A grant administrator’s first priority is to develop policies and procedures that outline each step in the lifecycle of the grant. Typically, this document will answer the following questions:

- Who approves grant applications?

- Who executes grant agreements?

- What systems will be used to track grant activities, such as qualifying expenses, reporting dates, performance metrics (both financial and programmatic)?

- What documentation is required for compliance?

- Who reviews and approves grant activities to ensure compliance?

- Who develops and manages a schedule and process for annual financial reporting (financial statements and grant reporting, e.g., single audit)?

- Who is responsible for training staff in grant requirements?

- Are subrecipient contracts standardized, and do they comply with your responsibilities as a grantor?

- Who is responsible for resolving audit findings?

Are you prepared for grant reporting?

One of the key responsibilities of a grant administrator is to manage deadlines (monthly, quarterly, biannually, annually, and grant close out). In addition to the initial application deadline, grants require consistent attention. You need to file updates and reports throughout the life of the grant, and they will often require specific documentation. The information in these reports must be complete, accurate, and filed promptly. If they are not, you can count on the grantor requiring you to follow-up and resolve the issues.

Do you have the resources to monitor activities?

It’s true, monitoring grants is a full-time job. Or it should be.

Being awarded a grant is the first chapter of a long story. The rest of the tale involves using the grant for its intended purposes and documenting that fact. Responsible monitoring and documentation require time, energy, systems, and personnel.

Someone should be assigned responsibility for the continuous monitoring and evaluation of grant administrative policies and procedures. This involves looking for changes in grant requirements communicated by the grantor.

For subrecipients, the grant administrator must convey the expectations about their activities and then monitor the progress toward the stated goals. On-site visits will sometimes be necessary and require time. Verifying the status of periodic reporting responsibilities can also take up resources that may already be scarce.

The final chapter of monitoring activities is to develop a clearly defined plan for responding to audit findings. Depending on the complexity of the findings, resolving these issues can require rewriting procedures, documenting changes, and verifying the implementation.

Are you ready for an audit?

While this may seem obvious, knowing your requirements should be the first step in preparing for the possibility of an audit.

In addition to reviewing grant requirements, look back at your prior year findings to confirm that they were fully resolved. If they were not, they need to be addressed immediately.

The next step in being prepared for an audit is to ensure all necessary documentation is complete and accurate. Your documentation should demonstrate compliance with the grant requirements. Usually, your materials will need to include evidence of internal controls that supports the process of reviews and approvals. Internal policies and procedures should be easily accessible. (Thankfully, once this document is complete, it only needs to be updated going forward.) When these items are assembled, make sure all reconciliations connected to the grant are complete.

Once the preparations are made, the hardest part of an audit is done. You will still need to meet with auditors and discuss expectations, timelines, and requests for information, but these are more scheduling and time management issues. If your paperwork and systems are in good order, your work will consist mainly of providing evidentiary support, and possibly providing explanations on details that may not appear obvious to an outsider.

Continuously improving your grant compliance processes

With a lot of subjectivity in the process of managing grants, along with requirements changing on a regular basis, it is important to continuously evaluate the adequacy of your grant administration policies and procedures. So, no matter what your situation is, your processes can always improve, and any deficiencies can be remediated. But it takes commitment as an organization to devote the resources to do the ongoing work of grant compliance.

Many state and local governments have compliance questions about the federal grants that were distributed during the pandemic. The reporting rules of these programs are complex, and requirements continue to evolve.

MGO’s state and local government professionals can help answer questions about these federal grants and help organizations document their systems of internal controls, improve their audit preparation, and address audit findings. Contact Linda Hurley at +1 (949) 296-4340 or lhurley@mgocpa.com for more information on how to improve your grant compliance processes.

]]>Prepare for grant reporting

The total distribution of government grants for Native American Tribes is estimated to be more than $31 billion. Being awarded a grant is a welcomed relief, however organizations must ensure that the proper grant accounting and compliance guidance are followed. This requires time, energy, systems, and often an increase in internal efforts. Furthermore, for some organizations initial grant awards may trigger new audit requirements and reengineering of existing accounting procedures.

Grant requirements can be complicated, so it is crucial to develop a systematic grant management program. Identify (or hire) a grant administrator to take responsibility for meeting compliance guidelines. Develop policies and procedures that outline each step in the lifecycle of a grant (application, interim reporting, and final results). Grant reporting involves many deadlines and needs consistent attention and clear communication with the granting agency. Close attention to the reporting and compliance details of the grant will make final reporting or an audit of the grant much easier. But it’s not just ease that is important, solid grant compliance and grant management is about good fiscal management, transparency, and mitigating risk. Because the consequences of noncompliance can be fines, costs to reputation, and a loss of confidence from funders.

Secure your assets against cybercrime

Cybersecurity should be another priority for tribal communities. Casinos and gaming organizations are high-value targets for cyber criminals because of the large quantity of Personal Identifiable Information (PII) obtained and stored on a daily basis. Casinos also have many physical and digital entry points, a variety of technology, a large workforce, multiple third- party vendors, and high frequency of high cash and payment card transactions. These components entice cyber criminals to launch large scale attacks and potentially cause expensive data breaches.

How do you protect yourself in an industry that is so ripe for cybercrime? A formal risk assessment can gather disparate pieces of information and evaluate your entire environment including the mix of digital computing platforms. This will help you prioritize the issues you need to address to build a more secure structure in which to do business. A comprehensive risk assessment will also help assess your compliance and controls and identify your full range of risk exposure.

It’s also crucial to understand what assets you have so you know what must be protected. These include more than just laptops or servers. Your cloud, web applications, and mobile devices are also at risk. Gap analysis and a penetration test can reveal the vulnerabilities in your IT environment.

Once you’ve fully identified your vulnerabilities, you can take actions to strengthen your defenses and protect your business. Ultimately, you will need to identify the leaders responsible for managing cybersecurity risks, suggesting methods and resources for mitigation, providing training, and developing an executable cyber security roadmap in order to move forward.

A diversified portfolio reduces risk

Both individuals and organizations need a diverse group of investments to spread out risk. This is not news, but frequently, the awareness of risk does not result in actions that mitigate it.

Finding the right investments takes time. A financial advisor can help you, but ultimately the decisions are yours. Do you look for high returns? Not if you are looking to balance your risk. Do you seek out the predictability of bonds? There are actually risks in that approach, too. There is no single way to mitigate risk, but examining your current investments is a good place to start before evaluating new ones.

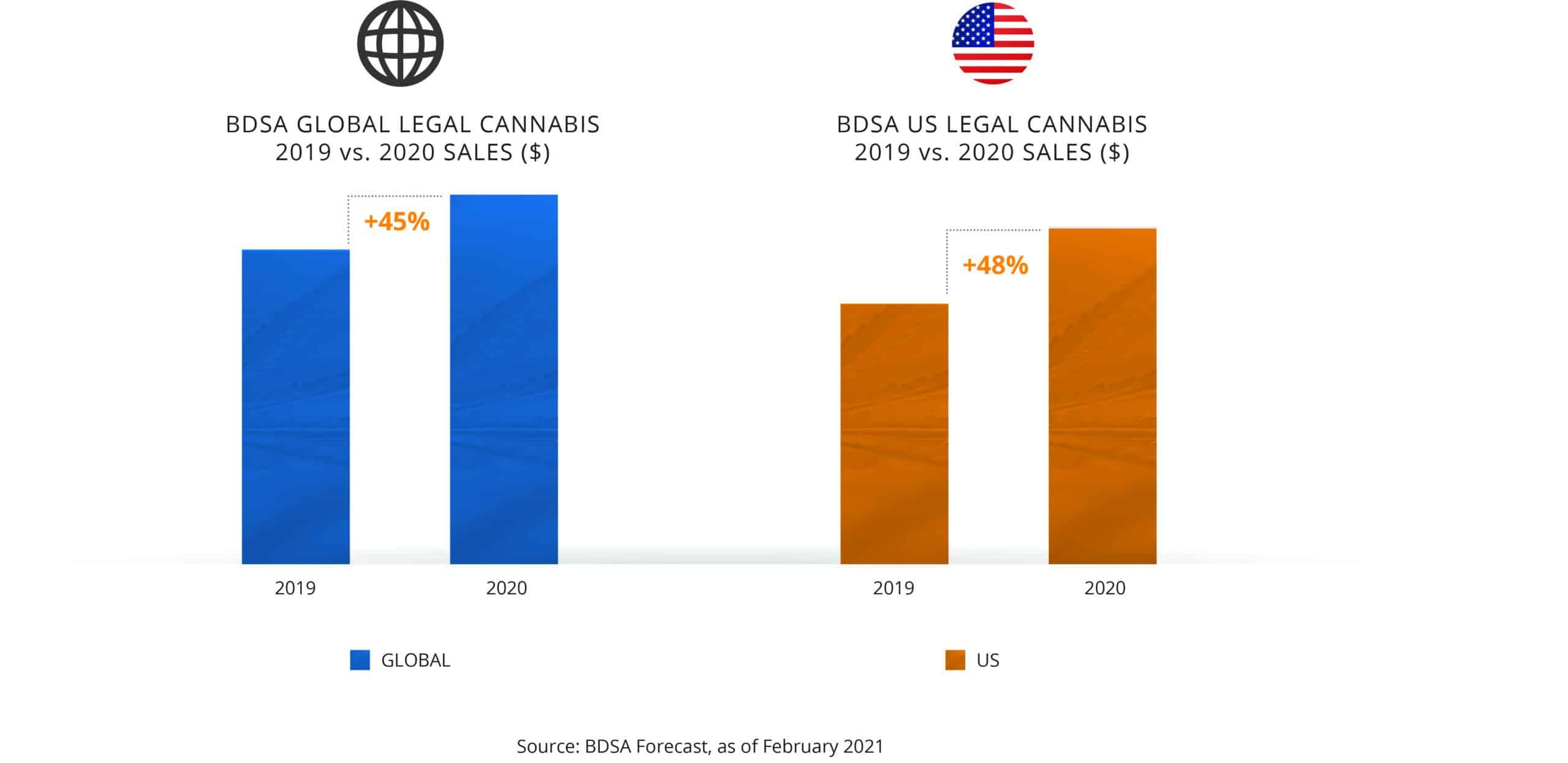

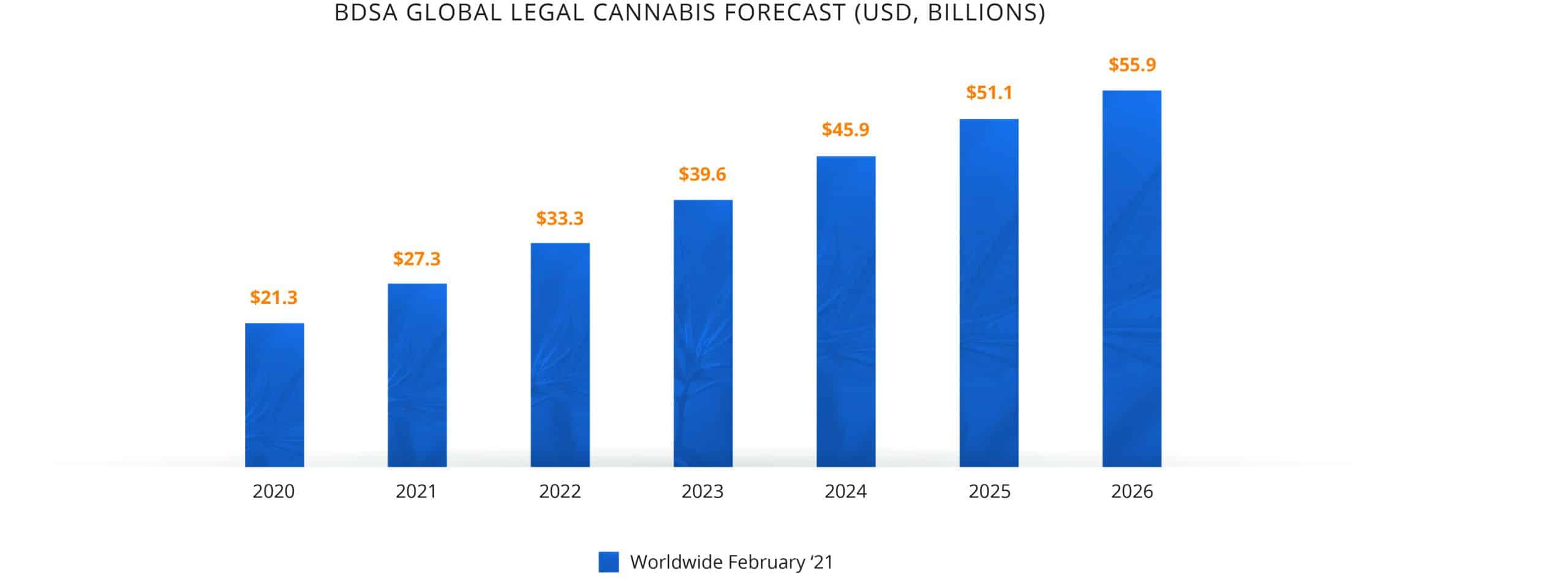

When it comes to diversifying your portfolio, take your time to do the due diligence. For instance, the cannabis industry is one of the fastest-growing industries in the world. It will generate an estimated $146.4 billion by 2025, according to Grand View Research. Does that make it the right opportunity for you? To find the answer, you need to dig deeper.

The industry is still in its early stages of growth, and this can work in your favor. Your investment could grow quickly, but regulations and licensing can be complicated for an emerging industry. Cannabis may be an exciting and profitable business to get involved in, but that doesn’t mean it is it the right investment for your particular portfolio. If you are trying to mitigate risk, does this investment really accomplish that? Do you already have a high-growth investment? Are there stigmas associated with cannabis that you might want to avoid? Are there compliance issues that could be more of a headache than investing in a more mature industry?

An investment in cannabis may not be a simple decision. Like many industries, you can also decide how deeply you want to invest — and there are risks at each level. An investor could focus on cultivation, manufacturing, retail, or the development of a vertically integrated cannabis operation. The unique sovereignty of Tribal nations even creates potential for leasing Tribal land to cannabis cultivators or aspiring cultivators without land to grow.

Like any investment, due diligence is key to risk mitigation. If you understand the industry you are investing in, you will understand your investment’s impact on your portfolio. And remember, when considering risk, your focus should be on your overall portfolio, rather than the intriguing possibilities of the industry or the certainty of returns.

How we can help

Tribal leadership is facing unique challenges. More than ever, sound due diligence and risk mitigating practices must be an integral part of decision making. MGO’s professionals have helped Tribes develop frameworks for grant management, cybersecurity, and economic diversification that facilitate the decision-making process for council members.

]]>Start a grant application here: https://careliefgrant.com/partners/county/

Basics of the COVID-19 relief grant program

The program, which allocates $500 million in financial relief to small businesses and nonprofits that have been impacted by the COVID-19 pandemic, was first announced by Gov. Newsom and the California state legislature on November 30th, 2020.

All California-based small businesses (including sole proprietors, home-based businesses, and independent contractors) and not-for-profits with a yearly gross revenue of $2.5 million or less, and have been in operation since at least June 1, 2019, may be eligible for the grant. It is worth noting that applicants with multiple business entities/franchises/locations, etc. are not eligible for multiple grants and are only allowed to apply once using their eligible small business with the highest revenue.

Grant awards by entity revenue

The grant award ranges from $5,000 to $25,000 based on your operation’s annual gross revenue as reported in the most recent federal tax return.

Gross Annual Revenue – Grant Award

$1,000 to $100,000 – $5,000

Greater than $100,000 up to $1,000,000 – $15,000

Greater than $1,000,000 up to $2,500,000 – $25,000

The award is a true grant, not a loan that has to be forgiven. The funds are intended to be used as working capital for your business’s operating expenses – payroll, rent, loan payments, COVID-protective measures, etc.

Award selection process

The grants are not issued on a “first-come, first-served” basis; rather all applications will be assessed following the close of each application round. The program prioritizes distribution based on key factors, including:

- Geographic distribution based on COVID-19 health and safety restrictions;

- County status and regional stay-at-home orders;

- Industry sectors most impacted by the pandemic;

- Underserved small business groups:

- e.g., majority-owned and run by women, persons of color, or veterans, or located in low-to-moderate income and rural communities.

The Small Business COVID-19 Relief Grant Program will be offered in two “Rounds” – with the first Round running from December 30, 2020 to January 13, 2021 at 11:59pm. Everyone who applies during a Round will be given equal consideration. Awards will be announced after each Round closes. The timing of the second and final Round is to be determined.

If you apply in the Round 1 and are not successful, your application will be carried over for consideration in Round 2 without the need to reapply. Businesses can only receive one grant even though there will be two Rounds.

For more information, visit careliefgrant.com

]]>