- Environmental, social, and governance (ESG) information helps investors, regulators, and the public-at-large understand and interpret a government entity’s risk profile and its ability to drive positive impact.

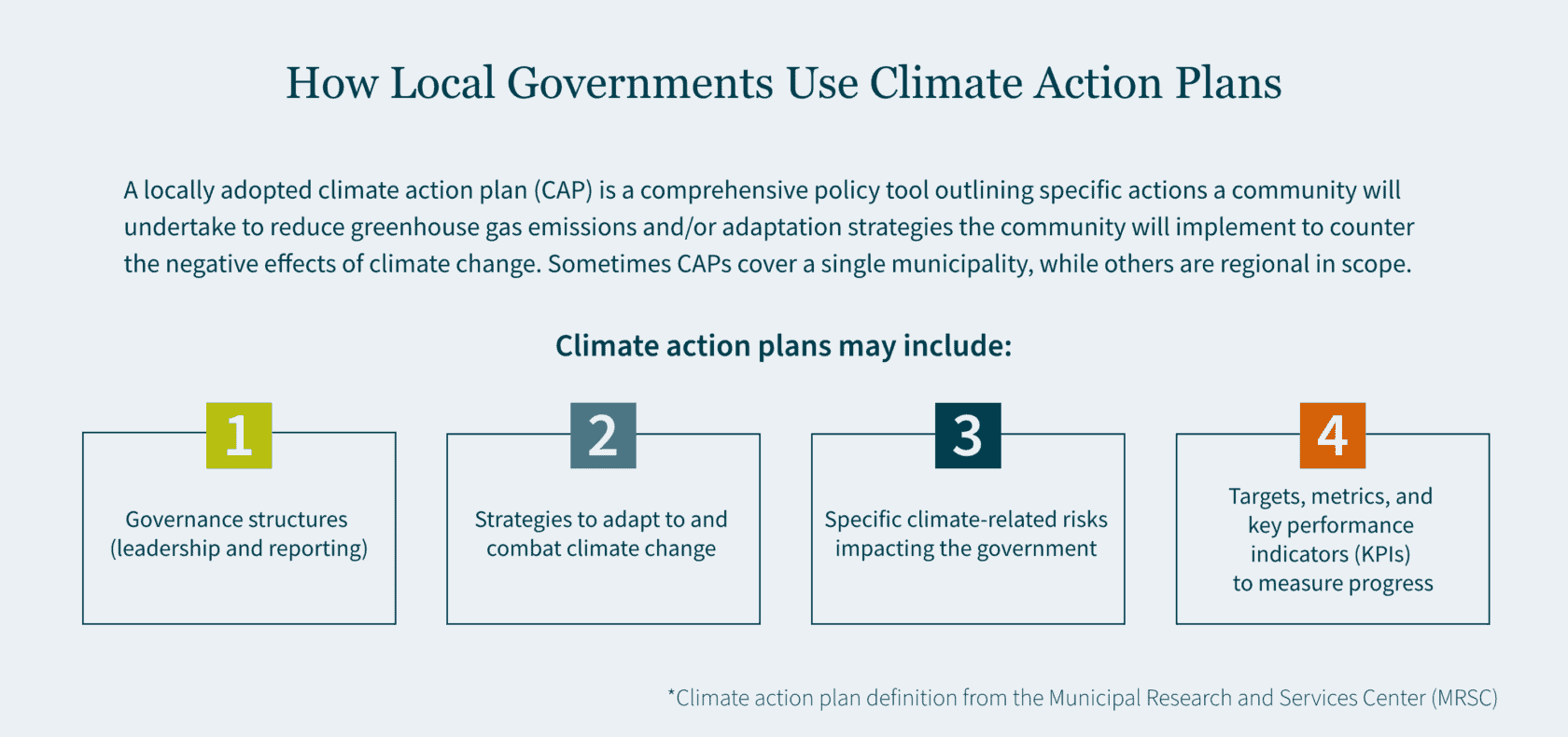

- To present this information publicly, government entities are developing robust “Climate Action Plans,” which are reviewed and refreshed on a periodic basis.

- As disclosing ESG-related information to the public becomes more common, government entities are also expanding ESG-related disclosures within annual financial reports.

Coined in a 2004 United Nations report, the term “environmental, social, and governance” (and its accompanying acronym “ESG”) is less than 20 years old. Yet, you would be hard-pressed to find a boardroom today where ESG is not top of mind. It is not just businesses either — ESG is also an increasingly important topic of discussion within government organizations.

State and local governments use ESG-related information as a mechanism to measure and track priorities, footprints, and targets. As governments have matured, ESG reporting and presented information more consistently with year-to-year comparability, investors*, regulators, and the public-at-large have sought out this reporting to help them understand risk and the government entity’s ability to drive positive impact.

*Note: The term “investors” refers to those who are exploring and/or holding investments in government-issued securities (e.g., hedge funds, institutions, individuals, etc.).

The Increasing Importance of “Climate Action Plans”

To present ESG-related information to the public, many government entities develop and communicate robust “Climate Action Plans”. These plans highlight a myriad of information, including (but not limited to):

- Governance structures (e.g., communication and reporting lines from environmental leadership into the mayor’s office)

- Strategies to adapt to and combat climate change

- Specific climate-related risks, which impact the government entity

- Targets, metrics, and key performance indicators (KPIs) used to measure progress

As Climate Action Plans continue to evolve, governments are commanding and allocating more financial resources to activate these plans. With the increased focus on climate-related initiatives presented in Climate Action Plans, we are seeing an expansion of ESG-related information disclosed within “Annual Comprehensive Financial Reports” across the country — a sign that financial disclosures are maturing to meet growing interests from investors, regulators, and the public-at-large.

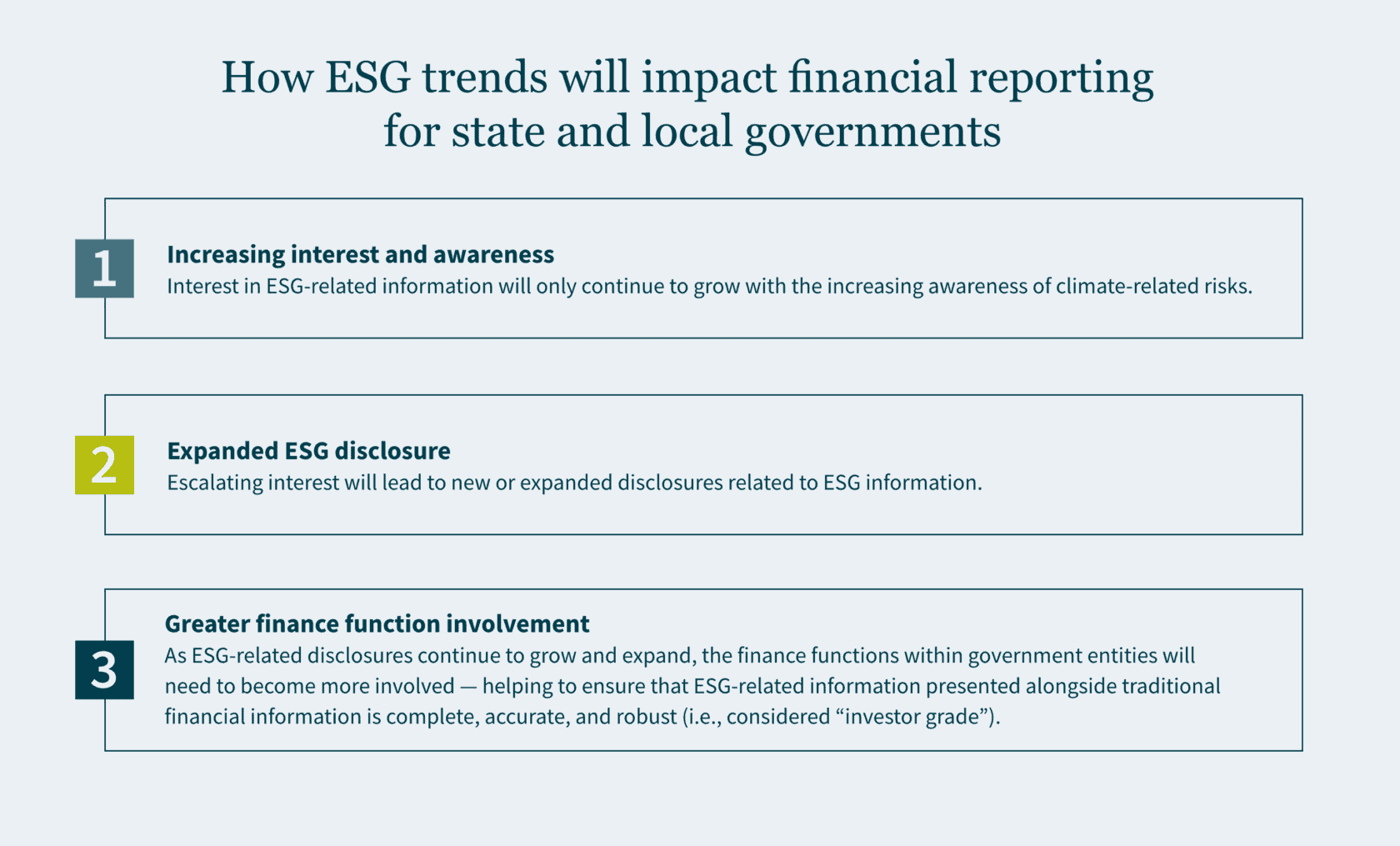

A Growing Push from Investors and Regulators

The focus on non-financial risks (including, but not limited to, ESG-related risks) by investors and regulators continues to intensify. When we take a step back to analyze the trend, a few things become clear:

- Interest in ESG-related information will only continue to grow with the increasing awareness of climate-related risks.

- Escalating interest will lead to new or expanded disclosures related to ESG information.

- As ESG-related disclosures continue to grow and expand, the finance functions within government entities will need to become more involved — helping to ensure that ESG-related information presented alongside traditional financial information is complete, accurate, and robust (i.e., considered “investor grade”).

To dive deeper into that last point, where would a finance function start? The short answer is by increasing the integration and collaboration between a government entity’s environmental leaders and the finance functions. The longer answer is that government entities need to develop holistic approaches to collecting and reporting robust ESG-related information to meet the expectations of investors, regulators, and the public-at-large.

The bottom line: As the issuance of and investment in municipal securities continues to grow, the quality of ESG-related information disclosed to the public will need to be enhanced to meet the demands of investors.

Transparency in Budgets and Financial Reporting

With an increase in ESG-related disclosures in annual financial reports by government entities, recent interpretive guidance from the Governmental Accounting Standards Board (GASB) indicates that government entities can expect further scrutiny and regulation as these types of disclosures become more commonplace.

Essentially, it is important for your government to have a robust, well-communicated ESG “story” within a Climate Action Plan — but you also must provide investor-grade transparency within audited financial statements. Government entities are already beginning to meet this challenge. Two examples of local governments with a growing presence of ESG-related information in their Annual Comprehensive Financial Reports are the City and County of San Francisco and the City of Fremont.

The City and County of San Francisco transparently discloses both environmental and social initiatives, capturing details related to its Environmental Protection Fund, as well as specific details related to revenues received from state, federal, and other sources for the preservation of the environment.

The City of Fremont — which is much smaller in terms of population (~230,000) and financial resources (roughly $1.5 billion in total primary government assets from “government activities”) — depicts ESG-related information throughout its annual report, including but not limited to qualitative information in the “management discussion and analysis” section, as well as quantitative information related to “community development and environmental services.”

The Path Forward: Enhancing Your ESG Reporting

With ESG-related information becoming more integrated into investor decision-making, your government needs to focus on enhancing its Climate Action Plans and developing “investor grade” disclosures related to ESG risks and opportunities for inclusion within your traditional financial reporting. These initiatives will require additional financial resources and human capital to create and maintain — and further collaboration between environmental, social, and financial leaders will be needed to drive the change.

How MGO Can Help

Incorporating ESG disclosures into financial reporting can pose challenges to states and local governments unfamiliar with ESG reporting standards. With experience providing ESG solutions, our State and Local Government Practice will work with your team to meet requirements and make information “investor-ready,” while also ensuring accountability and transparency.

]]>- States and local governments are receiving billions in funding from opioid settlements over the next two decades to fight the opioid epidemic through approved abatement strategies.

- To avoid misuse, settlements mandate 85% of funds must go toward addressing the opioid crisis, and governments must report annually on expenditures.

- Understanding state reporting rules, deadlines, and processes is critical for local governments to comply with settlement agreements.

~

States and local governments are starting to receive the first round of funding from recent settlements with opioid manufacturers, distributors, and retailers. These funds present an important opportunity to make progress against the ongoing opioid crisis through expanded treatment and prevention efforts.

To ensure states and local governments seize the opportunity to combat the opioid epidemic, settlement creators established acceptable uses for how the money can be spent. These requirements were put in place to avoid a repeat of the tobacco settlement of the 1990s, where states reportedly only spent a small portion of funding on tobacco prevention and cessation programs.

The National Opioids Settlement includes specific language to prevent similar misuse, mandating that “at least 85% of the funds going directly to participating states and subdivisions must be used for abatement of the opioid epidemic.” Most states also require local governments to report annual settlement fund expenditures.

As your agency begins to receive, access, and report on funding from opioid settlements, here is an overview of allowable uses, as well as a detailed look at potential reporting requirements.

Spreading Billions of Dollars Across States and Subdivisions to Battle the Opioid Epidemic

The opioid crisis has grown exponentially throughout the 2000s, ravaging communities and depleting resources. In response to this, more than 3,000 states and local governments filed lawsuits against opioid makers and distributors to recover tax dollars spent addressing the epidemic. The suits allege that these companies marketed opioids in misleading ways — downplaying risks, exaggerating benefits, and engaging in reckless distribution practices.

As a result of these lawsuits, several opioid manufacturers, distributors, and retailers agreed to pay settlements totaling more than $50 billion to states, counties, and municipalities. The payouts for these settlements will be made incrementally over periods ranging from 6-18 years. Each state’s share of the total settlements is calculated based on factors such as overall population, opioid shipment volumes, opioid use disorder rates, and overdose deaths. Distribution metrics vary from state to state as determined by state legislatures.

Allowable Uses of Opioid Settlement Funds

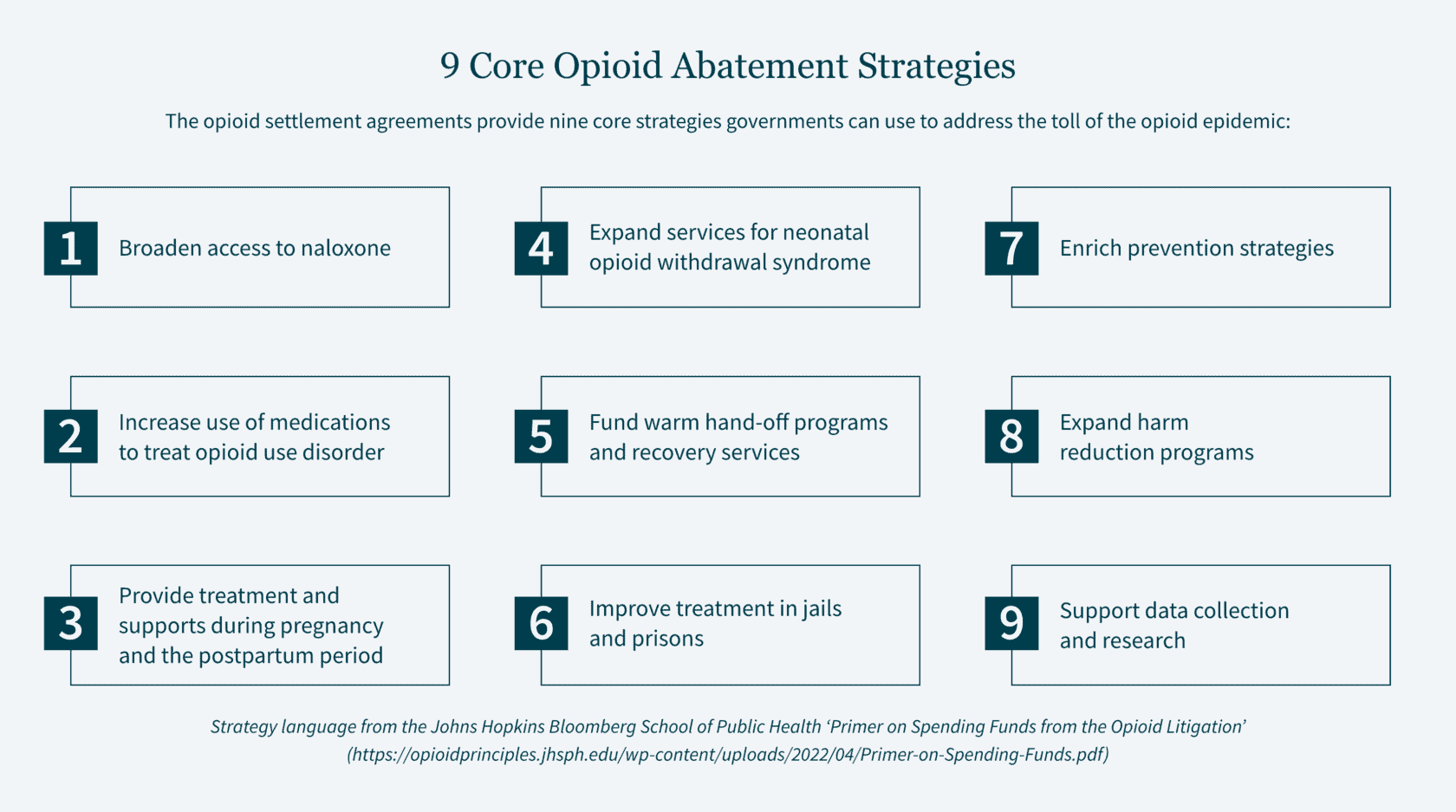

The settlements require that funds are to be used for “opioid remediation” activities. To paint a clearer picture of what constitutes a remediation activity, the National Settlement Agreements provide Exhibit E, which outlines allowed uses. Exhibit E has two sections: Schedule A lists high-priority, evidence-based Core Strategies; and Schedule B lists an additional set of broader Approved Uses.

Here are examples of allowable uses for opioid settlement funds from both Schedule A and Schedule B:

Schedule A (Core Strategies)

- Expand access to naloxone and medications for opioid use disorder (MOUD)

- Support treatment programs, particularly for pregnant/postpartum women and incarcerated populations

- Fund recovery services and connections (“warm hand-off” programs)

- Broaden evidence-based addiction prevention efforts

Schedule B (Approved Uses)

- Treat opioid use disorder (OUD)

- Connect people who need help to the help they need

- Prevent overdose deaths and other harms

- Educate law enforcement or other first responders

State Limitations on How Funds Are Used

Many states add further limitations on how these funds can be used. For example, California created its own High Impact Abatement Activities (HIAAs) list, and the state requires participating subdivisions to spend no less than 50% of their funds on HIAAs.

HIAA strategies (applicable to California only) include:

- Creating new or expanding substance use disorder (SUD) treatment infrastructure

- Addressing the needs of communities of color and vulnerable populations

- Diversion of people with SUD from the justice system into treatment

- Interventions to prevent drug addiction in vulnerable youth

- Purchase of naloxone for distribution and efforts to expand access to naloxone

Prohibited Uses of Opioid Settlement Funds

The idea is to ensure settlement fund expenditures are connected to addressing opioid misuse, treating opioid disorders, and mitigating the epidemic’s effects.

For example, the State of California Department of Health Care Services (DHCS) prohibits spending settlement funds on the following:

- Salaries for staff not involved in abatement activities

- General government administrative costs more than 10% of the total allocation

- Law enforcement not related to treatment

- Unapproved medications or treatments

- Infrastructure unrelated to prevention, treatment, or recovery

- Any costs not tied to approved abatement strategies

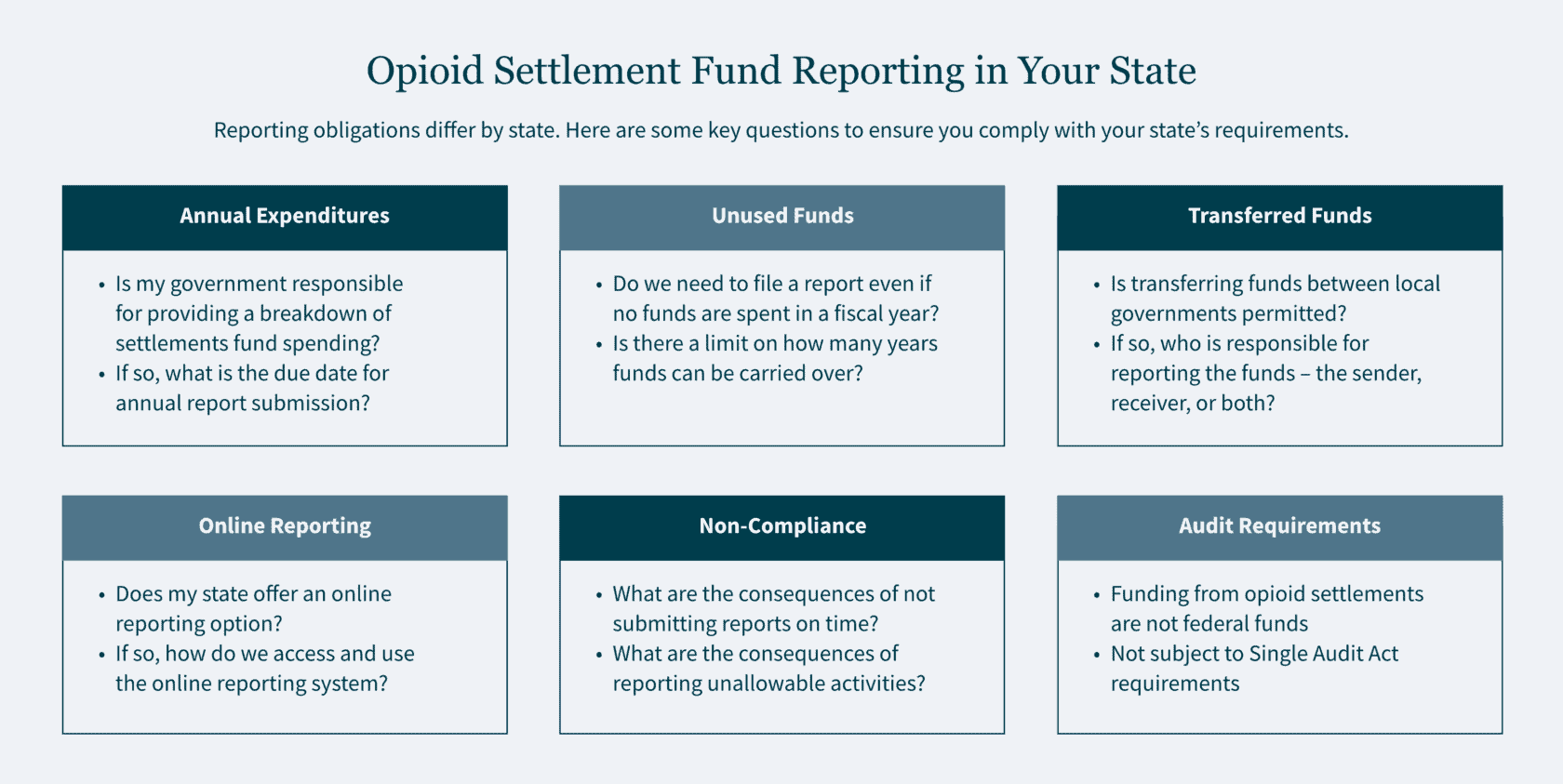

Understanding Your State’s Opioid Fund Reporting Requirements

Local governments receiving settlement funds must prioritize effective reporting as they move forward. The specific reporting criteria you need to meet will depend on your state. Texas subdivisions currently have no reporting obligations, whereas California subdivisions will need to report expenditures annually.

What and how you report about your fund expenditures will also vary by state. For example, here are six aspects of settlement fund reporting specific to California that may or may not apply to your state (but nonetheless should be on your radar):

- Annual Expenditures – Most local governments will file annual reports. These reports typically break down dollars spent on approved abatement strategies over the past year. States may also ask for planned expenditures for the coming year as well. Make sure you add your report submission due dates to the calendar. These dates will vary from state to state, but are expected to be the same each year moving forward.

- Unused Funds – In California, local governments must still complete annual reporting even if no settlement funds were spent or committed during a given fiscal year. The reports should show any dollars being carried over or reserved for future abatement activities. Unused funds can be retained year to year, but must be fully expended within five to seven years (depending on the type of expenditure).

- Transferred Funds – In California, if settlement funds are transferred from one participating government to another, both must report the transaction. The sender reports the transfer amount while the recipient reports the funds as money received from another subdivision.

- Online Reporting – Many states, like California, are creating online reporting systems to track opioid settlement expenditures. Governments will need to familiarize themselves with these reporting tools as they come online.

- Non-Compliance – Meeting your reporting obligations is essential to maintaining access to this funding. Failure to submit timely reports or spending on unallowable activities may result in an audit of fund usage or legal action. Accurate reporting also demonstrates good stewardship to the mission of the National Opioids Settlement.

- Audit Requirements – The Single Audit Act requires an annual audit of non-federal entities that spend $750,000 or more of federal funds in a fiscal year. Opioid settlement funds are not federal funds and therefore not subject to Single Audit Act requirements.

Maximizing the Impact of Your Government’s Opioid Settlement Funds

The opioid epidemic’s staggering cost defies calculation, with an estimated $1.5 trillion in damages in 2020 alone. Beyond the numbers lie lives lost, families shattered, and communities ravaged. While the National Opioids Settlement can never truly compensate for this immeasurable loss, it does offer states and local governments a chance to reshape the future.

With billions in abatement funding flowing to local communities over the next two decades, ensuring compliance with opioid settlement guidelines will enable you to maximize the impact of every dollar while avoiding the risks of non-compliance. Our experienced state and local government advisors can assist you in tracking allowable spending and meeting reporting requirements so that you can get the most out of these vital funds. Contact our practice today to learn more about how we can help your government achieve its goals.

]]>The Governmental Audit Quality Center (GAQC) promotes the importance of quality governmental audits and the value of such audits to purchasers of governmental audit services. GAQC is a voluntary membership center for CPA firms and state audit organizations that perform governmental audits. The GASB Matters section of the GAQC site highlights key interest areas, key resources, and advocacy efforts related to state and local government engagements.

Pension-related matters

GASB Pensions: Issues & Resources page of the GAQC Web site consolidates the various resources available to practitioners to assist with understanding the new standards and developing appropriate audit strategies. This page also includes links to various whitepapers and related auditing interpretations addressing cost-sharing and agent multiple-employer plans.

Comment Letters

- September 16, 2019 comment letter on GASB’s Exposure Draft, Public-Private and Public-Public Partnerships and Availability Payment Arrangements

- September 16, 2019 comment letter on GASB’s Exposure Draft, Omnibus 20XX

- April 30, 2019 comment letter on GASB’s Exposure Draft, Leases Implementation Guide

- March 8, 2019 comment letter on GASB’s Exposure Draft, Fiduciary Activities Implementation Guide

- February 14, 2019 comment letter on GASB’s Financial Reporting Model Improvements & Recognition of Elements of Financial Statements

Giving state and local governments the resources to protect against hackers

The SLCIA updates the Homeland Security Act of 2002 to give the DHS leeway to utilize centers like the Cybersecurity and Infrastructure Security Agency (CISA) and Multi-State Information Sharing and Analysis Center (MS-ISAC). This will allow them to work with state, local, tribal, and territorial governments as needed, upon request.

This collaboration will encourage conducting cybersecurity exercises and hosting trainings meant to address current or future cyber risks or incidents. It will also provide operational and technical assistance to state and local governments to implement security resources, tools, and procedures to improve overall protection against attacks. The goal is to provide state and local governments with the support they need to defend themselves from hackers.

Resources to bolster government security capabilities

The SLCIA establishes a $500 million DHS grant program that will empower government institutions to increase their focus on cybersecurity. The bill also:

- Requires CISA to develop a strategy to improve cybersecurity of state, local, tribal, and territorial governments, enabling them to identify federal resources to capitalize on as well as set baseline objectives for their efforts;

- Indicates state, local, tribal, and territorial governments must develop a comprehensive cybersecurity plan to guide their usage of any grant money they receive;

- Establishes a state and local cybersecurity resiliency committee made up of representatives from state, local, tribal, and territorial governments to provide awareness of cybersecurity needs; and

- Enjoins CISA to assess the feasibility of a rotational program for the detail of approved government employees holding cyber positions.

The bill gives state and local governments the push they need to begin defending their networks. This can include the development of new strategies to boost their cybersecurity capabilities and acquisition of the funding needed to ensure their implementation. By investing in cybersecurity ahead of an attack, an entity is more likely to save money and protect its data.

Assessing eligibility for cybersecurity grants

Cybersecurity grants are available to municipalities of all sizes — but it’s important to start strategizing now by considering your IT infrastructure and cybersecurity frameworks. By applying for the grants, you indicate that you are taking your entity’s security seriously and taking the proper steps to qualify.

The State and Local Cybersecurity Improvement Act will provide up to $1 billion in grants for state, local, tribal, and territorial governments, allowing them to directly address their cybersecurity threats and risks. The program’s funding starts at $2 million for 2022, $400 million for 2023, $300 million for 2024, and $100 million for 2025.

To be eligible, an entity must:

- Maintain responsibility for monitoring, managing, and tracking its information systems, applications, and those user accounts owned and operated by the government;

- Show it has a process of continuously prioritizing the assessment of its cybersecurity vulnerabilities and threat mitigation practices; and

- Have a tangible plan that outlines:

- How to manage and audit network traffic.

- How the government plans to use the information to improve its systems’ resiliency and strength.

Our perspective

While the bill is still waiting on the Committee on Homeland Security and Governmental Affairs there are some things you can do to make sure you are ready. State and local governments should focus on building teams that can handle the grant application process — and be prepared to implement once awarded. This bill indicates that governments are past the point of merely updating a firewall or running a generic virus program — things like multifactor authentication and zero-trust architecture are viewed as the next steps (which was required for federal agencies in a 2021 executive order).

How we can help

Prior to starting the grant application process, your IT leaders should start thinking about how to handle security gaps with various procedures and consistent tests. MGO can help. Our Technology and Cybersecurity team can provide guidance as you prepare for the future.

About the authors

Francisco Colon is a Partner at MGO with extensive experience in external audit, fraud examinations, litigation support, operational and internal controls reviews, and buyer/seller due diligence. He specifically focuses on assisting organizations with evaluating and updating their internal controls with a focus on strategic alignment and fraud litigation deterrence management in a variety of industries, including tribal government, gaming, technology, cannabis, hospitality, government contracting, distribution, manufacturing, and private equity. Contact Francisco at FColon@mgocpa.com.

]]>California’s workaround is in effect for the 2021 tax year and will continue to be available through the 2025 tax year (although it could expire earlier if the federal $10,000 limitation is repealed by Congress prior to its current sunset date of January 1, 2026).

The state tax credit, which is nonrefundable, can be carried over for five years. Nonresidents and part-year residents do not have to prorate the credit to account for their non-California income.

How to elect

California’s workaround is available for partnerships (including those structured as LLCs) and S corporations that only have individuals, trusts, estates, and/or corporations as owners. Publicly traded partnerships, partnerships owned by other partnerships, members of a combined reporting group, and disregarded entities do not qualify. (Disregarded Single-Member LLCs are not eligible to make the election, but will not make the entity ineligible if they are an owner of an otherwise eligible PTE).

Not all the owners of the pass-through entity need to consent to the election. Those that do not consent are not included in the calculation of the PTE Tax. To take advantage of the workaround, the pass-through entity needs to make the election annually on its state tax return. In addition, payments towards the PTE Tax need to be made by specified due dates.

• For the 2021 tax year, 100% of the PTE Tax needs to be paid by the due date for the pass-through entity’s state tax return without extensions – March 15, 2022.

• In later years, the PTE tax needs to be paid in two installments: the first installment is due by June 15 of the tax year for which the election is being made, and the second installment is due by the due date for the pass-through entity’s state tax return for that tax year without extensions (i.e., the following March 15). The minimum amount for the first installment is $1,000.

What to consider

The biggest benefit to the owners of a pass-through entity is the ability to claim a federal tax deduction for their share of the pass-through entity’s state income tax paid to California, but there is another potential benefit. In future years (starting with the 2022 tax year) PTE Tax payments may create some “float” for the owners in terms of the timing and amount of their individual estimated tax payments:

- Individuals in California need to pay 70% of their estimated tax liability through quarterly payments on April 15 and June 15, while the PTE Tax only requires that one installment of 50% of the total tax be paid in by June 15.

- Individuals in California need to pay the remaining 30% of their estimated tax liability by January 15 of the following year (i.e., the 4th quarter payment), while the PTE Tax only requires the remaining 50% be paid in by March 15.

However, despite these benefits, other factors should be considered before making the election:

- If the pass-through entity provides most of the income for an owner and that owner’s top California tax rate is less than or equal to 9.3%, the state tax credit cannot be used in full before it expires. On the other hand, since the election is made annually, you could avoid accruing too much carryover by opting not to elect in a following year.

- It’s unclear how California’s workaround will interact with pass-through entity tax regimes enacted by other states, especially their associated state tax credits. California provides credits against most other states’ taxes, but guidance has not been provided to indicate that it will afford the same treatment to other state PTE Taxes paid. Multi-state operators may not be able to reduce California taxable income by the amounts of other states’ similar taxes.

- The 9.3% flat rate may not be sufficient to cover the full tax liability for higher income owners.

- The PTE tax credit does not reduce the amount of tax due below California’s Tentative Minimum Tax (TMT), and thus may not be as beneficial for taxpayers subject to the TMT.

- There are considerations pertaining to cash management, since the pass-through entity would be paying the PTE Tax, not the owners.

- Non-resident withholding (7% for individuals) is not offset by the withholding requirements for the PTE Election. Non-resident taxpayers making the election would therefore be required to pay in tax at 16.3% among the quarterly and bi-annual installments, then claim a refund up to the amount of the 7% withholding. But because the 9.3% PTE Tax is non-refundable, to the extent that withholding exceeds tax due, it would need to be claimed in a later year.

How we can help

This PTE Election is a little complicated, but it is worth the effort to explore. MGO’s state and local tax professionals can advise you on the numerous pass-through entity tax regimes being passed by states to counter the federal limitation on deducting state taxes. Our cumulative experience as SALT specialists can help you determine if you are able to benefit from pass-through entity taxes and how to appropriately use them. Reach out to our team of experienced practitioners for your state and local tax needs.

]]>That all changed on March 11, when President Biden signed the American Rescue Plan Act of 2021 into law. The bill allocates $432 billion in direct financial support to U.S. territories, states, and local and tribal governments. In the following, we highlight how the bill affects state, local, and Tribal governments, and breakdown the details of key provisions.

American Rescue Plan of 2021: Impact on State, Local and Tribal Governments

The American Rescue Plan of 2021 contains wide-ranging programs designed to support state, local, and Tribal governments through the financial crises resulting from the COVID-19 pandemic. These include active support for COVID-19 response and planning, funds for in-state capital improvement projects, emergency housing support, and much more.

Much of the relief funding is allocated and disbursed automatically using metrics that include population, economic conditions, and unemployment rates. While each program has different disbursement details, broadly speaking, payments are delivered in two or more installments, the first coming within a 60-day window following the bill becoming law, and future installments through 2022 and beyond.

Other programs will require state and local authorities to apply for grants based on specific needs.

One of the highlights of the revised funding and plan is looser restrictions on how funds from the Coronavirus State Fiscal Recovery Fund can be utilized. The accepted uses include:

• Funding government services that have been curtailed due to decreases in tax revenue caused by the pandemic.

• Aid to households, small businesses and nonprofits, and impacted industries like tourism, hospitality and travel.

• Making “necessary investments” in water, sewer, or broadband infrastructure.

While potential uses have been broadened, all programs require stringent rules for intended use, tracking and reporting.

Highlights of the American Rescue Plan of 2021

Coronavirus State Fiscal Recovery Fund

50 States and the District of Columbia receive $195.3 billion in aid:

- $25.5 billion will be split evenly among each state and the District of Columbia, with each state and the District of Columbia receiving $500 million in aid.

- $168.55 billion distributed based on each state’s share of total unemployed workers over the period of October 2020 to December 2020.

- District of Columbia receives additional $1.25 billion.

- Tribal governments receive $20 billion (further discussion to come).

- U.S. territories receive $4.5 billion.

- U.S. Treasury receives $50 million to cover costs of administration of the fund.

Coronavirus Local Fiscal Recovery Fund

Local governments to receive $130.2 billion in aid to be split among counties, metropolitan cities, and non-entitlement units of local government:

- Counties receive $65.1 billion in population-adjusted payments, with additional adjustments for Community Development Block Grant (CDBG) recipients.

- Metropolitan cities receive $45.57 billion.

- Non-entitlement units of local government receive $19.53 billion, distributed by individual states and funded by the U.S. Treasury. Each jurisdiction receives population-adjusted payments based on such jurisdiction’s share of the state population.

Coronavirus Capital Projects Fund

$10 billion available for states, territories, and Tribal governments to support critical capital projects directly enabling work, education and health monitoring in response to COVID-19:

- Each state receives $100 million.

- U.S. territories receive $100 million to be split among them.

- Tribal governments and the state of Hawaii receive $100 million to be split among them.

- Remainder of funds to be allocated to states based on population.

NOTE: The Treasury Department will establish an application process for grants from the fund within 60 days of enactment of the law.

Local Assistance and Tribal Consistency Fund

$2 billion for eligible revenue-sharing counties and tribal governments:

- Eligible revenue-sharing counties will receive $750 million allocated based on economic conditions for each FY 2022 and FY 2023.

- Eligible tribal governments will receive $250 million allocated based on economic conditions for each FY 2022 and FY 2023.

NOTE: Payments from this fund may be used for any governmental purpose other than a lobbying activity and will remain available until September 30, 2023.

Other State, Local, and Government Funding Sources

Additional federal government programs have received funding earmarked to support recovery efforts in states, Tribes, and territories. These funds can be applied for via grant applications depending on each government agency’s circumstances.

Homeowner Assistance Fund

$10 billion allocated to states, territories, and tribes through grants to prevent homeowner mortgage defaults, foreclosures, and displacements.

Funds may be used to reduce mortgage principal amounts, assist homeowners with housing payments and other aid needed to prevent eviction, mortgage default, foreclosure, or the loss of utility services.

Funds may also reimburse state and local governments that have provided similar assistance since January 2020.

Each state, along with the District of Columbia and Puerto Rico, will receive at least $50 million. Additional amounts will be set aside for other U.S. territories and tribes.

States, territories, and Tribes receiving funding will have to set aside at least 60% of their allocation to assist homeowners who make less than 100% of the local or national median income.

Homelessness Assistance and Supportive Services Program

$5 billion allocated to state and local governments to provide supportive services for homeless and at-risk individuals. Permitted fund uses include tenant-based rental assistance, housing counseling and homeless prevention services, and acquiring non-congregate shelter units.

Low-Income Home Energy Assistance Program (LIHEAP) and Water Assistance Program

$4.5 billion allocated to fund the LIHEAP program, and $500 million provided in state grants to assist low-income households with drinking water and wastewater services.

FEMA Disaster Relief Fund

$50 billion to reimburse state and local governments for the costs of ongoing COVID-19 response and recovery activities, and other emergencies.

Funding to remain available through FY 2025.

Final thoughts

With billions of dollars in aid becoming available to state, local and tribal government agencies, the use of these funds is going to be tracked very closely by federal regulators. If you have any questions about how funds can be utilized, and how to track and report this use, MGO’s dedicated State and Local Government team can help. Contact Us.

]]>Everything changes, except when it doesn’t

Time and time again we’ve seen reactions to various accounting scandals, after which new policies, procedures, and legislation are created and implemented. An example of this is the Sarbanes-Oxley Act (SOX) of 2002, which was a direct result of the accounting scandals at Enron, WorldCom, Global Crossing, Tyco, and Arthur Andersen.

SOX was established to provide additional auditing and financial regulations for publicly held companies to address the failures in corporate governance. Primarily it sets forth a requirement that the governing board, through the use of an audit committee, fulfill its corporate governance and oversight responsibilities for financial reporting by implementing a system that includes internal controls, risk management, and internal and external audit functions.

Governments experience challenges and oversight responsibility similar to those encountered by corporate America. Governance risks can be mitigated by applying the provisions of SOX to the public sector.

Some states and local governments have adopted similar requirements to SOX but, unfortunately, in many cases only after cataclysmic events have already taken place. In California, we only need to look back at the bankruptcy of Orange County and the securities fraud investigation surrounding the City of San Diego as examples of audit committees that were established in response to a breakdown in governance.

Taking your audit committee on the right mission

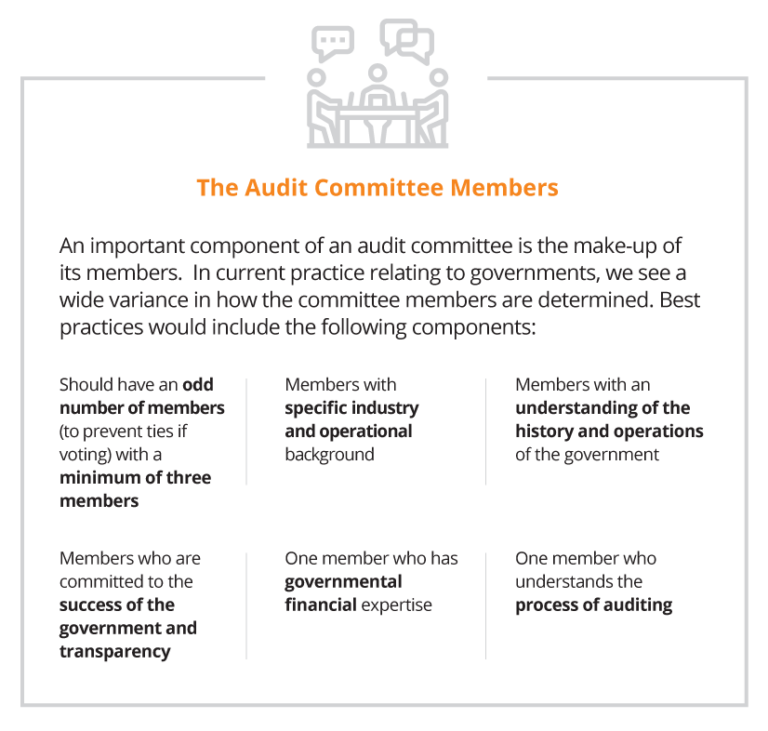

Governments typically establish audit committees for a number of reasons, which include addressing the risk of fraud, improving audit capabilities, strengthening internal controls, and using it as a tool that increases accountability and transparency. As a result, the mission of the audit committee often includes responsibility for:

- Oversight of the external audit.

- Oversight of the internal audit function.

- Oversight for internal controls and risk management.

Chart(er) your course

Most successful audit committees are created by a formal mandate by the governing board and, in some cases, a voter-approved charter. Mandates establish the mission of the committee and define the responsibilities and activities that the audit committee is expected to accomplish. A wide variety of items can be included in the mandate.

Creating the governing board’s resolution is the first step on the road to your audit committee’s success.

Follow the leader(ship)

In practice we see a combination of these attributes, ranging from the full board acting as the audit committee, committees with one or more independent outsiders appointed by the board, and/or members from management and combinations of all of the above. While there are advantages and disadvantages for all of these approaches, each government needs to evaluate how to work within their own governance structure to best arrive at the most workable solution.

Strike the right balance between cost and risk

The overriding responsibility of the audit committee is to perform its oversight responsibilities related to the significant risks associated with the financial reporting and operational results of the government. This is followed closely by the need to work with management, internal auditors and the external auditors in identifying and implementing the appropriate internal controls that will reduce those risks to an acceptable level. While the cost of establishing and enforcing a level of zero risk tolerance is cost prohibitive, the audit committee should be looking for the proper balance of cost and a reduced level of risk.

Engage your audit committee with regular meetings

Depending on the complexity and activity levels of the government, the audit committee should meet at least three times a year. In larger governments, with robust systems and reporting, it’s a good practice to call for monthly meetings with the ability to add special purpose meetings as needed. These meetings should address the following:

External Auditors

- Confirmation of the annual financial statement and compliance audit, including scope and timing.

- Ad hoc reporting on issues where potential fraud or abuse have been identified.

- Receipt and review of the final financial statements and auditor’s reports

- Opinion on the financial statements and compliance audit;

- Internal controls over financial reporting and grants; and

- Violations of laws and regulations.

Internal Auditors

- Review of updated risk assessments over identified areas of risk.

- Review of annual audit plan, including status of the prior year’s efforts.

- Status reports of ongoing and completed audits.

- Reporting of the status of corrective action plans, including conditions noted, management’s response, steps taken to correct the conditions, expected time-line for full implementation of the corrective action and planned timing to verify the corrective action plan has been implemented.

Establish resources that are at the ready

Audit committees should be given the resources and authority to acquire additional expertise as and when required. These resources may include, but are not limited to, technical experts in accounting, auditing, operations, debt offerings, securities lending, cybersecurity, and legal services.

Taking extra steps now will save time later

While no system can guarantee breakdowns will not occur, a properly established audit committee will demonstrate for both elected officials and executive management that on behalf of their constituents they have taken the proper steps to reduce these risks to an acceptable tolerance level. History has shown over and over again that breakdowns in governance lead to fraud, waste and abuse. Don’t be deluded into thinking that it will never happen to your organization. Make sure it doesn’t happen on your watch.

]]>The deadline for implementation is Jan. 1, 2018, for calendar year publicly-held companies, and Jan. 1, 2019, for calendar year privately-held companies. Although the implementation date for non-public companies is over one year away, our dedicated Government Contractor practice specialists encourage clients to start evaluating the changes now to understand the impact on their financial statements.

In this article, we will provide an overview of the revenue standard’s main provisions, provide best practices for implementation methods, and identify key issues that may impact government contractors during implementation. This guidance will be especially beneficial to entities following the AICPA’s Industry Revenue Recognition Task Force for Aerospace & Defense.

Main provisions of the new standard

The new standard is more principle-based than current revenue recognition guidance and will require government contractors to exercise more judgement. The principle is based on a five-step model from the AICPA Revenue Recognition Guide:

Step 1: Identify the Contract with a Customer

The standard includes characteristics that need to be met for a contract to permit revenue recognition. In general, a contract exists if there is an agreement between a buyer and seller that creates enforceable rights and obligations for the two parties. Only when there is such an agreement is there any revenue to recognize under Topic 606. This step sets the base to which the rest of the steps in the model are applied.

Also included in this step is guidance on when to combine multiple contracts into a single contract for revenue recognition purposes, and what to do if a contract is modified, thereby changing the identified contract with a customer.

Step 2: Identify the Performance Obligations in the Contract

Among the rights and obligations that will be set forth in the contract (either explicitly or implicitly), are:

- 1. The right of the buyer to receive goods or services from the seller, and;

- 2. The obligation of the seller to provide those goods or services to the buyer.

Once the contract has been identified, the seller identifies what goods or services it has promised to provide to the buyer. The standard includes guidance on evaluating provisions of a contract to determine whether they should be regarded as creating promised goods or services.

If multiple goods or services are promised, the seller must determine whether each good or service is distinct from other goods or services in the arrangement, or must instead be combined with other goods or services to form a bundle that is distinct from other goods or services in the contract.

Each good or service that is distinct, or each bundle of goods or services that is distinct, is called a performance obligation under the standard. Performance obligations are then used as units that are evaluated for revenue recognition purposes in the rest of the model.

Step 3: Determine the Transaction Price

In addition to rights and obligations over goods or services to be provided, a contract will include:

- 1. The obligation of the buyer to pay the seller for the goods or services, and;

- 2. The right of the seller to collect that payment from the buyer.

Those provisions provide a starting point for determining the transaction price. Often, the payment terms are fixed and payment is due when goods or services are delivered. In that case, it is simple to determine the transaction price to be used in recognizing revenue.

However, the vendor needs to determine whether all amounts to be collected are appropriately reported as revenue. In addition, the contract may include terms that make the transaction price variable. For example, the transaction price could vary due to usage-based payments, award and incentive fees, rights of return or refund, or economic price adjustment.

Topic 606 explains when, and how much, variable consideration is to be included as part of the transaction price. This will generally require variable consideration to be included in the transaction price to the extent it is probable such consideration will become due under the contract.

Step 4: Allocate the Transaction Price to the Performance Obligations in the Contract

In this step, the transaction price determined in Step 3 is allocated, or assigned, to the performance obligations identified in Step 2. Obviously, if there is only one performance obligation, this allocation is easy, as the entire transaction price is allocated to the single performance obligation. However, if there are multiple performance obligations, the transaction price must be allocated to those performance obligations.

Generally, this is done based on the stand-alone selling prices of the performance obligations in the contract. The stand-alone selling price of a performance obligation may be objectively determinable if the performance obligation is regularly sold on a stand-alone basis. If it is not, its stand-alone selling price must be estimated through a reasonable technique.

Once stand-alone selling prices for all performance obligations are estimated, the transaction price is generally allocated based on the relative values of the performance obligations, effectively allocating any discount in the contract to the performance obligations on a pro rata basis.

Step 5: Recognize Revenue When (or as) the Entity Satisfies a Performance Obligation

Once the transaction price has been allocated to the performance obligations in the contract, the amount of revenue allocated to each performance obligation is recognized when, or as, the entity performs the obligation as required by transferring the promised goods or services that make up the performance obligation to the customer.

A good or service is deemed to be transferred to the customer when the customer gains control over the good or service. A customer sometimes gains control of promised goods or services as performance occurs over time. In other instances, the customer gains control of a promised good or service at a single point in time, often when something is physically delivered to the customer.

When a performance obligation is satisfied over time, the seller must determine an appropriate measure of its progress toward satisfying the performance obligation, and then recognize revenue based on that progress measurement applied to the amount of the transaction price allocated to the performance obligation.

When a performance obligation is satisfied at a point in time, the seller must determine the appropriate point in time at which to recognize as revenue the amount of the transaction price allocated to the performance obligation.

Implementation methods

Full retrospective application: Recast of prior period financial statements (with an adjustment to opening retained earnings for the first year presented). For example, for a public company, 2016 and 2017 would be recast to reflect the adoption of the new standard presented in the 2018 financial statements. The cumulative adjustment would be reflected as of Jan. 1, 2016.

Modified retrospective application: Cumulative effect of initially applying the standard is recorded as an adjustment to opening retained earnings of the period of initial application. Under the same example, 2016 and 2017 would not be recast in the 2018 financial statements. The cumulative adjustment would be reflective as of Jan. 1, 2018.

Implementation issues and guidance

For government contracts, the type of contract will determine if there will be a change from current revenue recognition practices. For time and materials and cost-plus-fixed-fee contracts, as well as services-based firm-fixed-price contracts, there will be minimal change to the total revenue and timing of revenue recognized under the new revenue standard. Under more complex contracts (i.e., award fees under cost-plus contracts, or firm-fixed-price contracts where the entity performs manufacturing, design, development, integration, and/or production), applying the new standard will require careful analysis and consideration, and could impact the timing of revenue recognition.

The AICPA’s Industry Revenue Recognition Task Force for Aerospace & Defense has identified various revenue recognition implementation issues and continually updates the list of issues as discussions continue.

The following are some of the key areas to consider when implementing the new guidance as noted in the AICPA’s Industry Revenue Recognition Task Force for Aerospace & Defense.

Acceptable Measure of Progress – what to consider when measuring progress towards completion of performance obligations satisfied over time.

Accounting for Contract Costs – considerations for applying the guidance in Financial Accounting Standards Board (“FASB”) Accounting Standards Codification (“ASC”) 340 for incremental costs of obtaining a contract, costs to fulfill a contract and amortization and impairment, to costs typically incurred in aerospace and defense contracts, including pre-contract costs and learning or start-up costs.

Variable Consideration – considerations for estimating the amount of variable consideration (incentive fees, award fees, economic price adjustments) in aerospace and defense contracts, the impact of subsequent modifications, and how to determine the amount of estimated variable consideration to include in the transaction price.

Significant Financing Component – considerations needed to assess whether a significant financing component exists in determining the transaction price for various types of aerospace and defense contracts.

Allocating the Transaction Price – considerations for determining how to allocate the transaction price to multiple performance obligations in aerospace and defense contracts.

Implementation plan for government contractors

The AICPA Financial Report Center developed an implementation plan that may be helpful as a starting point for developing your own implementation plan. Below are the high-level steps included in that plan.

- Designate the individual(s) responsible for overseeing implementation.

- Evaluate how the changes will impact how your company accounts for different types of revenue streams/contracts. Consider how the new standard will impact current performance metrics and compensation plans. Work with your auditor to discuss the completeness and accuracy of your analysis.

- Determine an implementation method (full or modified retrospective approach).

- Determine changes that may be needed within systems and/or software applications to facilitate revenue recognition under the new standard.

- Determine what interim disclosures may be required prior to the effective date.

- Develop a plan for implementation to incorporate the above steps, as well as train your staff.

- Educate the company’s management on the new standards and the impact you expect the changes to have on the company’s financial statements.

MGO has a dedicated Government Contractor practice with CPAs and industry specialists who are well-versed in the new standard and can assist in evaluating the impact of the changes on government contracts revenue recognition and financial reporting. We also assist our clients in implementing the new standard.

To learn more about how we can help, let’s talk.

]]>On August 3rd, new tax legislation — 26 USC 7345: Revocation or denial of passport in case of certain tax delinquencies — went into effect, taking aim at expats and international travelers. This represents the latest attempt by the Internal Revenue Service (IRS) to limit the amount in taxes lost each year from U.S. citizens living and/or working abroad and not reporting income, filing tax returns, or paying overdue taxes.

The process for enforcement begins with the IRS sending letters to persons with “seriously delinquent tax debt.” If the issue does not reach a timely resolution, the IRS will proceed by sending “certification” of the debt to the Secretary of State, who will then have the power to deny, revoke, or limit a passport.

How to know if you’re affected

This is may be an alarming surprise for expatriates living and working overseas, or U.S. citizens who travel internationally (for work or otherwise) but also have significant tax debt. Before panic sets in, it is important to note that the law lays out several key requirements before enforcement. In this case, “seriously delinquent tax debt” refers to an individual with an assessed tax debt of $50,000 or more, for which a tax lien has been filed and/or a levy has been issued.

While $50,000 (or more) in tax debt certainly seems like a lot, limiting the law’s impact. But as pointed out by Journal of Accountancy, 1.4 million U.S. citizens owe between $25,000 and $100,000 in tax debt, and 453,470 U.S. citizens individuals owed more than $100,000, per 2015 IRS data.

For those the law does affect, the impact could be disastrous. It would certainly be a rude surprise to arrange travel and accommodations, only to have your entry or exit from the U.S. denied. This could limit or undermine business opportunities for persons who rely on international travel. And expatriates living overseas may be barred from returning to the U.S. until the certification is removed.

Expats are at the highest risk

According to a 2014 study by the Treasury Inspector General for Tax Administration (TIGTA), 7.5 million Americans earn a living working abroad and are required to file and pay U.S. taxes. Complex filing and reporting rules, and simply not knowing they are required to pay U.S. taxes, are likely reasons why that same TIGTA study noted that the IRS sent 855,000 notices and letters to U.S. citizens overseas in 2014.

Further complicating the issue many expats may not know about their tax debt. International mail is notoriously unreliable in many regions, plus in some circumstances, the IRS is not required to send international mail.

How to get back on track

Expats and international travelers who are unsure whether they owe unpaid taxes should confirm their status with the IRS by calling 855-519-4965 or 267-941-1004, for international calls.

Persons who have been certified and a passport has been affected, or those who fear certification is imminent, should strongly consider consulting with a CPA who can help identify the best path back to good standing.

The good news is that once an individual has reconciled with the IRS, they will remove the certification within 30 days. The fastest way is to set-up an installment agreement with automatic deductions. Other options, including hardship situations and other agreement types, require submitting detailed financial information to the IRS, which could take months to confirm.

]]>By Scott P. Johnson, CPA, CGMA

Partner, State & Local Government, Advisory Services

As a public official for more than 24 years, I continuously strived to implement best practices, internal controls and policies and procedures to mitigate fraud, waste and abuse. Being a municipal finance officer responsible for literally billions of dollars, there were times when I would wake up in the middle of the night thinking about what could happen or what I may not know that could be occurring that could put the organization at risk. Fortunately throughout my municipal career the organizations I served did not experience headlines due to significant fraud. We had the appropriate “tone at the top” and practiced effective measures throughout the organization to mitigate potential fraud. However, from time-to-time, we would uncover the occasional lapse of an employee’s good judgement and detect inappropriate use of government funds, such as; improper procurement credit card use for personal purposes, time cards reporting that fraudulently claimed hours worked in excess of actual hours worked, and fictitious reimbursement claims for travel.

Employee fraud is a significant problem across industries and is faced by organizations of all types, sizes, locations, and industries. While employee fraud in private organizations rarely merits a mention in the local paper, the same fraud in a government agency will have editors competing to write the splashiest headlines and garner the highest reader traffic. It is critical for such organizations to maintain a positive reputation. Reputational risk can carry long-lasting damage in monetary losses, regulatory issues, and overall risk exposure. Frankly, all types of fraud are on the rise, and municipalities need an effective fraud mitigation strategy in place to protect against reputational and monetary harm.

Just a few recent examples of municipal fraud that have had significant press coverage and put the respective organizations in a challenging position: In 2014 officials in St. Louis County, IL, uncovered a $3.4 million embezzlement that escaped detection for more than six years. According to officials, a County Health Agency Division Manager overcharged for IT computer and technical services (unbeknownst to the County, the Division Manager owned the technology company). Unfortunately, the day after the suspected embezzlement was detected by County officials, the employee committed suicide, according to the County Medical Examiner.

The largest known municipal fraud in US history was uncovered in 2012 at the City of Dixon, IL. This embezzlement scheme of almost $54 million over a 22 year period was perpetrated by its Comptroller, Rita Crundwell, who used the proceeds to finance her quarter horse ranch business and lavish lifestyle. She was convicted and pleaded guilty to the crimes and is currently serving a 20 year sentence. Another recent case of an alleged fraud allegation is currently under trial in the Los Angeles Superior Court in which ex-Pasadena city employee, Danny Wooten and co-defendants are due back in court for arraignment on April 1, 2016, according to the Los Angeles County District Attorney’s Office. The criminal case involves allegations that more than $6 million in city money was embezzled over a decade in which Wooten is suspected of creating false invoices for the underground utility program between 2004 and March 2014.

Many factors can contribute to fraud, but the key factors are the improper segregation of duties, lack of management review, maintaining undocumented procedures, common exception processing, trust without verification and validation, and lack of accountability and monitoring. Employing proper risk assessments of events that could prevent, delay, or increase the costs of achieving organizational objectives and implementing a risk management plan not only ensure compliance, but strategically safeguard on organization against fraud. There are three important steps to earning a good night’s sleep.

1. Fraud Risk Assessment – understanding the organization as a whole and individual business units will lead to the most comprehensive risk management plan. Understand how resources flow as well as internal environments and processes. Conduct interviews, make observations and review all factors. Identify the possible and probable fraud schemes for all resource flows.

2. Prevention – “Tone at the Top” is critical. Inspiring employees to follow ethical standards starts with the tone at the executive level and must trickle down through the management level and ultimately throughout the entire organization. The organization needs to know that unethical practices will not be tolerated and when detected, will be dealt with in a timely and effective manner. One measure to communicate the “tone” is writing a fraud policy in concert with the employee conduct handbook will ensure the message is designed into the orientation, onboarding, and training process. Conduct management reviews, provide whistleblower channels, and communicate often with key business unit leaders, who in turn should communicate with their staff regarding fraud prevention, detection, and correction.

3. Detection – while assessment and prevention will create a strong defense against fraud, it is still important to seek out other measures to detect fraud that may not have been included in the fraud risk assessment plan. Only three percent (3%) of all fraud is discovered by accident or the good luck of the right person in the right place. Only six percent (6%) of fraud is discovered through account reconciliation. Clearly we cannot simply rely on these detection methods. In addition to account reconciliation and keeping your ears open, creating channels for detection are of the utmost importance. Eleven percent (11%) of fraud discoveries are due to an internal audit. Return to step one by assessing and re-assessing fraud risk regularly. Conduct meaningful management reviews on-time. Twelve percent (12%) of fraud detection were the result of properly conducted management reviews. Finally, be sure to enforce an open door policy and a culture of interest in detection and reporting. Fifty-four percent (54%) of all fraud detection comes through insider tips. Ensuring there are proper procedures in place to accept these tips is paramount when designing and especially, implementing the fraud management and detection plan.

Deceitful misconduct among employees significantly damages reputations, negatively affects resources, and limits the ability of any organization to effectively serve the consumer and their community. Following this roadmap on how to respond to and prevent employee fraud will not only protect the organization and its key objectives but will lead to an easier night’s sleep – even in the face of increasing fraud across all industries.

This article is only a small representation of the material presented during MGO’s “Case in Point” presentation at the 2016 CSMFO Conference. Special recognition to Ruthe Holden, Internal Audit Manager at the City of Pasadena for her contribution to the “Case in Point” presentation. Contact Scott Johnson at sjohnson@mgocpa.com if you have any questions or comments. Comments and opinions expressed in this article are those of the authors and may not reflect the positions, opinions, or beliefs of the CSFMO or MGO and should not be construed or interpreted as such.

]]>