Executive summary The Paycheck Protection Program (PPP) and the Employee Retention Credit (ERC) were powerful economic stimulus programs instituted during the COVID-19 pandemic to provide financial relief to struggling businesses. Both programs were the first initiatives of their kind, and as a result, there remains some uncertainty about what standards apply when accounting for them in […]]]>

- There is still uncertainty about how to account for the refundable Employee Retention Credit in your books, because you can’t account for it the same way you can account for the Paycheck Protection Program loan.

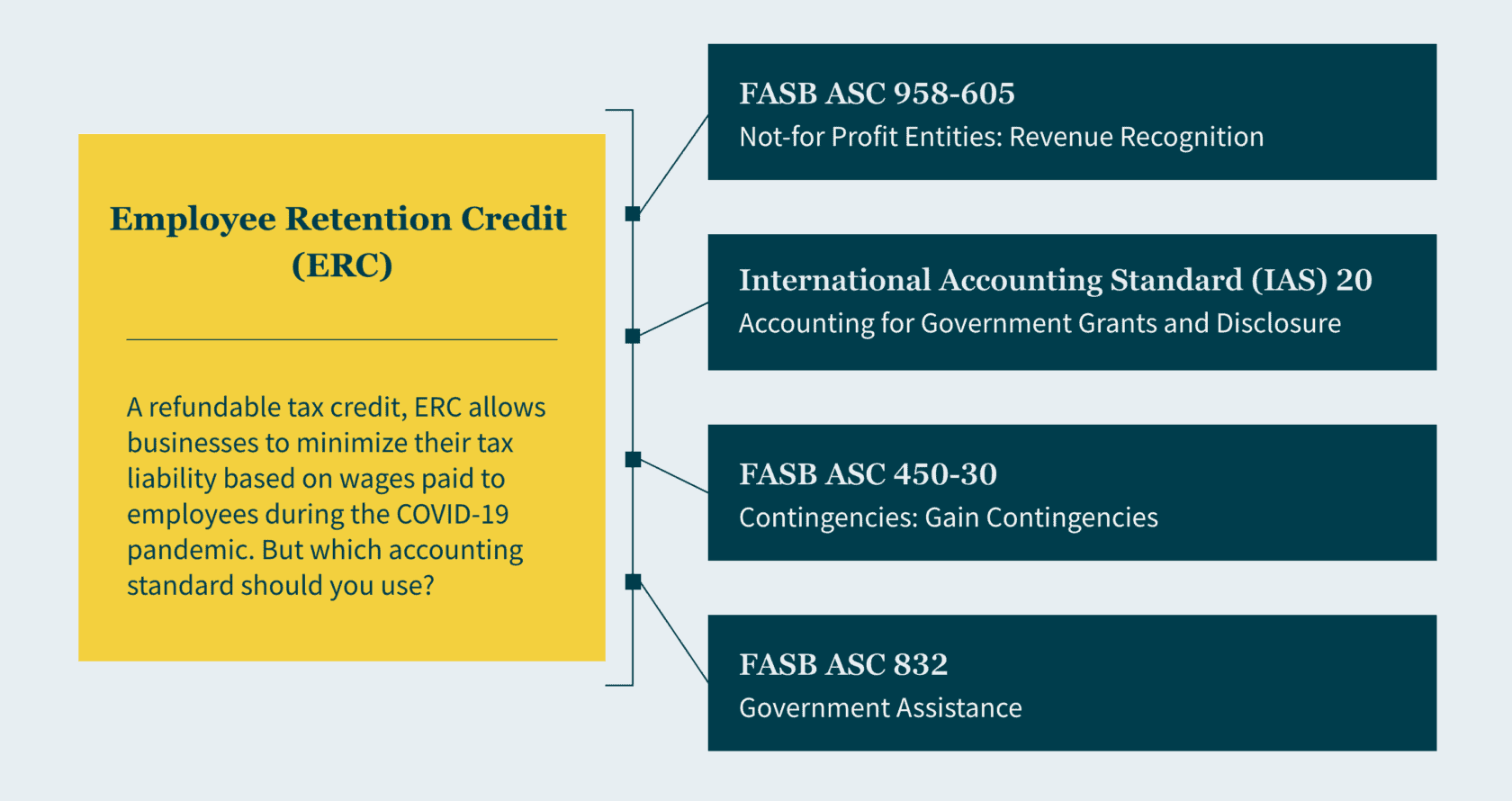

- The standards you can choose from are FASB ASC 958-605, International Accounting Standard (IAS) 20, FASB ASC 450-30, and FASB ASC 832.

- Depending on the standard you choose, you might have to consider the timing of recognition, the presentation of a grant income line, and financial ratios.

The Paycheck Protection Program (PPP) and the Employee Retention Credit (ERC) were powerful economic stimulus programs instituted during the COVID-19 pandemic to provide financial relief to struggling businesses. Both programs were the first initiatives of their kind, and as a result, there remains some uncertainty about what standards apply when accounting for them in your financial statements and records.

If you’re wondering how to distinguish the two, as well as determine the standard you should be utilizing, Angel Naval, a leader in our Client Accounting Solutions practice, breaks it down.

The PPP versus the ERC

Created to aid businesses facing financial challenges through the pandemic, there are several key differences between the PPP and the ERC.

The PPP is a loan and was created for small businesses with less than 500 employees in mind, giving them the funds needed to cover payroll and other eligible expenses. This includes hiring back employees who were laid off and covering applicable overhead. The loans are forgiven if the proper criteria are met (I.e., maintaining payroll and keeping consistent employee numbers).

A subset of the PPP loan, the ERC is a refundable tax credit that allows businesses to reduce their tax liability based on the qualified wages they’ve paid to their employees during the pandemic. It was created for businesses of all sizes to capitalize on in order to avoid layoffs. They can claim up to $5,000 per employee in 2020 and $7,000 per employee per quarter in 2021.

Determining the appropriate accounting standard for ERCs

If you took advantage of the ERC, currently, there is no straightforward way of accounting for it. Put simply, the ERC is a gray area because it’s so new, and there isn’t a straightforward way of accounting for it. Plus, ERCs are payroll credits, not income tax credits — and while FASB has extensive guidance for accounting for income taxes in ASC 740, it doesn’t for payroll taxes. Even the American Institute of Certified Public Accountants (AICPA) has suggested different standards, so it’s up to you to apply your best judgement based on the facts and circumstances of your business. Some things to consider:

- The timing of recognition,

- The financial ratios important to you, and

- Whether you want to present a grant income line.

For income statement presentation, according to AICPA’s December 2022 report, more public entities are crediting the associated expense rather than recognizing the amounts on a separate line item.

For example, you may think you can account for the ERC the same way you can for the PPP, but you can’t. As we differentiated above, the PPP is a loan and the ERC is a payroll credit, therefore the PPP is subject to debt and liability standards and the ERC is not. While the PPP did come first, those companies that have paid payroll taxes but still qualified for the ERC are still able to retroactively claim the credit.

For prospective applications, for-profit entities can adhere to guidance in one of the following.

FASB ASC 958-605

If you’re applying the revenue recognition model under ASC 958-605, ERCs are treated as conditional contributions. In this case, companies must have met the program’s eligibility conditions to record revenue (and no amounts can be recorded until all criteria are evaluated and “substantially” met according to regulations). Given the conditions are met, a refund receivable and income should be recognized in the period the entity determines the conditions have been substantially met. This standard requires that gross revenue be recorded, and it doesn’t permit any netting of revenue against related expenses.

Some barriers to meeting ASC 958-605’s requirements include the eligibility requirements, like meeting the rules for a decline in gross receipts as well as incurring qualifying expenses (i.e., payroll costs). To file for the ERC, you’ll need to decide whether preparing the related ERC form and filing it with the government presents a barrier you’ll need to overcome. Note administrative and other small stipulations do not represent a barrier.

IAS 20

If you’re applying IAS 20, you can’t recognize the ERC until the “reasonable assurance” threshold is met in correlation with ERC’s conditions and receiving the credit. In this case, “reasonable assurance” translates to “probable” under GAAP standards and is easier to satisfy than “substantially met” in Subtopic 958-605. Once you’ve provided reasonable assurance that conditions will be met, the earnings impact of the government grants is recorded over the periods in which you recognize as expenses the related costs that the grants are intended to cover. So, you’ll need to estimate the amount of the credit you expect to keep.

IAS 20 allows you to record and present either the gross amount as other income or net the credit against other related payroll expenses. For every quarter that a company meets the recognition criteria, it records a receivable and either other income or net expense.

FASB ASC 450-30

If you’re interested in applying FASB ASC 450-30, please note amounts related to the ERC wouldn’t be recognized under this model until all uncertainties regarding the disposition of the credit are resolved — and there’s less detail on the disclosure, measurement, and recognition requirements as compared to the other standard models. For this reason, the AICPA doesn’t believe this model to be a preferred accounting policy for the ERC.

FASB ASC 832

If you’re applying this model, you must disclose several specifics about transactions with a government within its scope. These entail the nature of the transactions, which includes a description of the transactions as well as the form in which it has been received, whether it’s cash or other assets. You must also detail the accounting policies you used to account for the transactions. Any line items on the balance sheet and income statement that are affected by the transactions must be accounted for too — plus, the amounts applicable to each financial statement line item in the current reporting period.

How MGO can help

While there are clear accounting standards for the PPP, there is still some uncertainty surrounding the ERC. Depending on the standard you choose, you may have to consider the timing of recognition, financial ratios, and whether to present a grant income line. Therefore, businesses need to apply their best judgment based on the facts and circumstances of their business when accounting for ERCs. Our Client Accounting Solutions team has extensive experience helping clients navigate complex tax regulations post-pandemic. Contact us to learn more about which standard you should be using for federal relief programs.

About the author

Angel Naval oversees our West Coast Financial Advisory Services practice and provides value-added guidance for your corporate finance, financial planning, and business process needs.

]]>Now is a good time to evaluate and improve your financial reporting process for grants. While grants are subject to many reporting requirements, we will focus on revenue recognition under accounting principles generally accepted in the United States of America (GAAP) and the schedule of expenditures of federal awards, as required by Uniform Guidance.

Financial reporting in accordance with GAAP

In June 2020, the Governmental Accounting Standards Board (GASB) issued Technical Bulletin No. 2020-1, Accounting and Financial Reporting Issues Related to the Coronavirus Aid, Relief, and Economic Security Act (CARES Act) and Coronavirus Diseases (TB 2020-1). TB 2020-1 helps governments navigate the complexities of accounting for CARES Act funding. It addresses issues such as the type of financial assistance, characterization of loss of revenue, and effect of amendments. While ARPA funds have their own complexities, the principles established in TB 2020-1 for the CARES Act translate well to ARPA, and GASB has not published further guidance for ARPA.

In TB 2020-1, GASB provides guidance that the Coronavirus Relief Fund (CRF) resources are voluntary nonexchange transactions subject to eligibility requirements. The Local Fiscal Recovery Funds in ARPA are like the CRF resources in the CARES Act and should be treated consistently. This means the award should be recognized in the period when all applicable eligibility requirements are met.

When evaluating revenue recognition for voluntary nonexchange revenues, remember that the recipient cannot incur allowable costs until there is an executed grant agreement. For the ARPA funds, this means the recipient has signed all the required documents accepting grant terms and conditions, and that the recipient has received confirmation of the award before the end of its reporting period.

The presumed applicable period is the immediate provider’s fiscal year and begins on the first day of that year, based on the provider’s appropriation to disburse the resources. For the CARES Act, few cities met the threshold for directly awarded metropolitan cities, which subjected them to the state’s provisions rather than as a direct recipient of the federal government. For example, California cities and counties that received pass-through awards from the State of California were unable to recognize grant revenue in fiscal year ended June 30, 2020, because the State of California did not make the appropriations available to governments until July 1, 2020, through passage of its budget act.

The ARPA funds, which were directly distributed to a considerably greater number of recipients, were appropriated immediately by the federal government upon signing ARPA into law. That means the direct recipients of ARPA funds and the non-entitlement units of governments that received their allocations from states that executed the awards before the end of the reporting period, may recognize revenue immediately upon execution of the award, if they met the eligibility criteria.

For those governments that received cash before the end of the reporting period, a liability should be reported for the portion of financial assistance that was not recognized as revenue. For those governments that did not receive cash before the end of the reporting period, a receivable should be reported for the portion of financial assistance that was recognized as revenue.

The possibility of a single audit

While many governments require an annual single audit due to the amount of federal awards received each year, many others are below the threshold for requiring a single audit. Funding related to COVID-19 resources may push more governments over that $750,000 threshold.

For governments unfamiliar with single audits, it is important to prepare. Taking inventory and reading the guidance provided by the Office of Management and Budget (OMB) and awarding federal agencies will help you understand and equip yourself to submit (and pass) a single audit.

What is the SEFA?

The schedule of expenditures of federal awards (SEFA) acts as a supplemental schedule to the financial statements that an organization produces when it is subject to a single audit requirement. This requirement is triggered when the federal expenditures reported on the SEFA exceed $750,000 or more over the organization’s fiscal year

Preparing the SEFA is no small task. It must be completed in accordance with the Uniform Guidance and include all federal expenditures. In addition to determining the amount of federal expenditures, the Uniform Guidance specifies how the amounts are to be reported. Individual federal programs should be listed by federal agencies, and pass-through entities should be noted as well.

The single audit and ARPA

On March 19, 2021, the OMB released a memo that detailed single audit updates to be aware of in ARPA. The updates give awarding agencies the discretion and the authority to grant some exceptions to recipients who are affected by the pandemic if they are permissible by law. These entities do not necessarily have to be recipients of COVID-19 related financial assistance to receive these exceptions.

The most notable update is the extension of the single audit submission due date. For those recipients who did not file their single audits with the Federal Audit Clearinghouse by March 19, 2021, and had fiscal year-ends through June 30, 2021, the submission of their reporting packages was extended to six months past the normal due date, and no action by the awarding agencies or recipients is necessary. However, the documentation showing the reason for the delay in filing must be retained.

Additional updates include:

- Awarding agencies may allow some necessary incurred pre-award costs.

- Awarding agencies may allow extensions of awards, which gives recipients more time to resume projects and expend the funds.

- Prior approval requirements may be waived.

- Awarding agencies can grant recipients up to a three-month extension beyond the normal due date to submit financial, performance, and other required reports.

- The award application deadlines can be flexible.

While it is clear the OMB is attempting to be reasonably flexible, maintaining clear documentation of your grants and expenditures will be helpful as new and changing guidance becomes available.

Understand the current requirements and look for changes

The pandemic threw many organizations into survival mode. However, with federal, state, and local support many have weathered the financial difficulties over the past 18 months as well as can be expected. As organizations move forward, they will have to account for how they survived, where the monetary support came from, and where the money went. The near future will require unprecedented diligence, flexibility, and perhaps most of all, patience.

MGO is here to help

Guidance over grant funding, especially as it relates to CARES Act and ARPA programs, are continuing to develop and evolve. It’s important to stay on top of the latest changes and updates, as utilization of these resources are critical to the financial recovery of your organization and the proper reporting of those resources to stakeholders and the federal agencies charged with oversight. If you need personalized guidance, don’t hesitate to reach out to your MGO contacts.

.

]]>The deadline for implementation is Jan. 1, 2018, for calendar year publicly-held companies, and Jan. 1, 2019, for calendar year privately-held companies. Although the implementation date for non-public companies is over one year away, our dedicated Government Contractor practice specialists encourage clients to start evaluating the changes now to understand the impact on their financial statements.

In this article, we will provide an overview of the revenue standard’s main provisions, provide best practices for implementation methods, and identify key issues that may impact government contractors during implementation. This guidance will be especially beneficial to entities following the AICPA’s Industry Revenue Recognition Task Force for Aerospace & Defense.

Main provisions of the new standard

The new standard is more principle-based than current revenue recognition guidance and will require government contractors to exercise more judgement. The principle is based on a five-step model from the AICPA Revenue Recognition Guide:

Step 1: Identify the Contract with a Customer

The standard includes characteristics that need to be met for a contract to permit revenue recognition. In general, a contract exists if there is an agreement between a buyer and seller that creates enforceable rights and obligations for the two parties. Only when there is such an agreement is there any revenue to recognize under Topic 606. This step sets the base to which the rest of the steps in the model are applied.

Also included in this step is guidance on when to combine multiple contracts into a single contract for revenue recognition purposes, and what to do if a contract is modified, thereby changing the identified contract with a customer.

Step 2: Identify the Performance Obligations in the Contract

Among the rights and obligations that will be set forth in the contract (either explicitly or implicitly), are:

- 1. The right of the buyer to receive goods or services from the seller, and;

- 2. The obligation of the seller to provide those goods or services to the buyer.

Once the contract has been identified, the seller identifies what goods or services it has promised to provide to the buyer. The standard includes guidance on evaluating provisions of a contract to determine whether they should be regarded as creating promised goods or services.

If multiple goods or services are promised, the seller must determine whether each good or service is distinct from other goods or services in the arrangement, or must instead be combined with other goods or services to form a bundle that is distinct from other goods or services in the contract.

Each good or service that is distinct, or each bundle of goods or services that is distinct, is called a performance obligation under the standard. Performance obligations are then used as units that are evaluated for revenue recognition purposes in the rest of the model.

Step 3: Determine the Transaction Price

In addition to rights and obligations over goods or services to be provided, a contract will include:

- 1. The obligation of the buyer to pay the seller for the goods or services, and;

- 2. The right of the seller to collect that payment from the buyer.

Those provisions provide a starting point for determining the transaction price. Often, the payment terms are fixed and payment is due when goods or services are delivered. In that case, it is simple to determine the transaction price to be used in recognizing revenue.

However, the vendor needs to determine whether all amounts to be collected are appropriately reported as revenue. In addition, the contract may include terms that make the transaction price variable. For example, the transaction price could vary due to usage-based payments, award and incentive fees, rights of return or refund, or economic price adjustment.

Topic 606 explains when, and how much, variable consideration is to be included as part of the transaction price. This will generally require variable consideration to be included in the transaction price to the extent it is probable such consideration will become due under the contract.

Step 4: Allocate the Transaction Price to the Performance Obligations in the Contract

In this step, the transaction price determined in Step 3 is allocated, or assigned, to the performance obligations identified in Step 2. Obviously, if there is only one performance obligation, this allocation is easy, as the entire transaction price is allocated to the single performance obligation. However, if there are multiple performance obligations, the transaction price must be allocated to those performance obligations.

Generally, this is done based on the stand-alone selling prices of the performance obligations in the contract. The stand-alone selling price of a performance obligation may be objectively determinable if the performance obligation is regularly sold on a stand-alone basis. If it is not, its stand-alone selling price must be estimated through a reasonable technique.

Once stand-alone selling prices for all performance obligations are estimated, the transaction price is generally allocated based on the relative values of the performance obligations, effectively allocating any discount in the contract to the performance obligations on a pro rata basis.

Step 5: Recognize Revenue When (or as) the Entity Satisfies a Performance Obligation

Once the transaction price has been allocated to the performance obligations in the contract, the amount of revenue allocated to each performance obligation is recognized when, or as, the entity performs the obligation as required by transferring the promised goods or services that make up the performance obligation to the customer.

A good or service is deemed to be transferred to the customer when the customer gains control over the good or service. A customer sometimes gains control of promised goods or services as performance occurs over time. In other instances, the customer gains control of a promised good or service at a single point in time, often when something is physically delivered to the customer.

When a performance obligation is satisfied over time, the seller must determine an appropriate measure of its progress toward satisfying the performance obligation, and then recognize revenue based on that progress measurement applied to the amount of the transaction price allocated to the performance obligation.

When a performance obligation is satisfied at a point in time, the seller must determine the appropriate point in time at which to recognize as revenue the amount of the transaction price allocated to the performance obligation.

Implementation methods

Full retrospective application: Recast of prior period financial statements (with an adjustment to opening retained earnings for the first year presented). For example, for a public company, 2016 and 2017 would be recast to reflect the adoption of the new standard presented in the 2018 financial statements. The cumulative adjustment would be reflected as of Jan. 1, 2016.

Modified retrospective application: Cumulative effect of initially applying the standard is recorded as an adjustment to opening retained earnings of the period of initial application. Under the same example, 2016 and 2017 would not be recast in the 2018 financial statements. The cumulative adjustment would be reflective as of Jan. 1, 2018.

Implementation issues and guidance

For government contracts, the type of contract will determine if there will be a change from current revenue recognition practices. For time and materials and cost-plus-fixed-fee contracts, as well as services-based firm-fixed-price contracts, there will be minimal change to the total revenue and timing of revenue recognized under the new revenue standard. Under more complex contracts (i.e., award fees under cost-plus contracts, or firm-fixed-price contracts where the entity performs manufacturing, design, development, integration, and/or production), applying the new standard will require careful analysis and consideration, and could impact the timing of revenue recognition.

The AICPA’s Industry Revenue Recognition Task Force for Aerospace & Defense has identified various revenue recognition implementation issues and continually updates the list of issues as discussions continue.

The following are some of the key areas to consider when implementing the new guidance as noted in the AICPA’s Industry Revenue Recognition Task Force for Aerospace & Defense.

Acceptable Measure of Progress – what to consider when measuring progress towards completion of performance obligations satisfied over time.

Accounting for Contract Costs – considerations for applying the guidance in Financial Accounting Standards Board (“FASB”) Accounting Standards Codification (“ASC”) 340 for incremental costs of obtaining a contract, costs to fulfill a contract and amortization and impairment, to costs typically incurred in aerospace and defense contracts, including pre-contract costs and learning or start-up costs.

Variable Consideration – considerations for estimating the amount of variable consideration (incentive fees, award fees, economic price adjustments) in aerospace and defense contracts, the impact of subsequent modifications, and how to determine the amount of estimated variable consideration to include in the transaction price.

Significant Financing Component – considerations needed to assess whether a significant financing component exists in determining the transaction price for various types of aerospace and defense contracts.

Allocating the Transaction Price – considerations for determining how to allocate the transaction price to multiple performance obligations in aerospace and defense contracts.

Implementation plan for government contractors

The AICPA Financial Report Center developed an implementation plan that may be helpful as a starting point for developing your own implementation plan. Below are the high-level steps included in that plan.

- Designate the individual(s) responsible for overseeing implementation.

- Evaluate how the changes will impact how your company accounts for different types of revenue streams/contracts. Consider how the new standard will impact current performance metrics and compensation plans. Work with your auditor to discuss the completeness and accuracy of your analysis.

- Determine an implementation method (full or modified retrospective approach).

- Determine changes that may be needed within systems and/or software applications to facilitate revenue recognition under the new standard.

- Determine what interim disclosures may be required prior to the effective date.

- Develop a plan for implementation to incorporate the above steps, as well as train your staff.

- Educate the company’s management on the new standards and the impact you expect the changes to have on the company’s financial statements.

MGO has a dedicated Government Contractor practice with CPAs and industry specialists who are well-versed in the new standard and can assist in evaluating the impact of the changes on government contracts revenue recognition and financial reporting. We also assist our clients in implementing the new standard.

To learn more about how we can help, let’s talk.

]]>