- In April, the U.S. Tax Court made news when it ruled in favor of businessman Alon Farhy, who challenged the Internal Revenue Service (IRS)’s authority to assess penalties for the failure to file IRS Form 5471.

- IRS Form 5471 is the Information Return of U.S. Persons With Respect to Certain Foreign Corporations.

- Taxpayers may be interested in filing protective refunds, and they should start the process sooner rather than later—there is a statute of limitations of two years for claiming refunds.

- This case’s ruling could have reverberating effects when it comes to the IRS collecting additional penalties, but only time will tell.

On April 3, 2023, the U.S. Tax Court came to a decision in the case Farhy v. Commissioner, ruling that the Internal Revenue Service (IRS) does not have the statutory authority to assess penalties for the failure to file IRS Form 5471, or the Information Return of U.S. Persons With Respect to Certain Foreign Corporations, against taxpayers. It also ruled that the IRS cannot administratively collect such penalties via levy.

Now that the IRS doesn’t have the authority to assess certain foreign information return penalties according to the court, affected taxpayers may want to file protective refund claims, even if the case goes to appeals — especially given the short statute of limitations of two years for claiming refunds.

Our Tax Controversy team breaks down the Farhy case, as well as what it may mean for your international filings — and the future of the IRS’s penalty collections.

The case

Alon Farhy owned 100% of a Belize corporation from 2003 until 2010, as well as 100% of another Belize corporation from 2005 until 2010. He admitted he participated in an illegal scheme to reduce his income tax and gained immunity from prosecution. However, throughout the time of his ownership of these two companies, he was required to file IRS Forms 5471 for both — but he didn’t.

The IRS then mailed him a notice in February 2016, alerting him of his failure to file. He still didn’t file, and in November 2018, he assessed $10,000 per failure to file, per year — plus a continuation penalty of $50,000 for each year he failed to file. The IRS determined his failures to file were deliberate, and so the penalties were met with the appropriate approval within the IRS.

Farhy didn’t dispute that he didn’t file. He also didn’t deny he failed to pay. Instead, he challenged the IRS’s legal authority to assess IRC section 6038 penalties.

The court’s ruling

The U.S. Tax Court then held that Congress authorized the assessment for a variety of penalties — namely, those found in subchapter B of chapter 68 of subtitle F — but not for those penalties under IRC sections 6038(b)(1) and (2), which apply to Form 5471. Because these penalties were not assessable, the court decided the IRS was prohibited from proceeding with collection, and the only way the IRS can pursue collection of the taxpayer’s penalties was by 28 U.S.C. Sec. 2461(a) — which allows recovery of any penalty by civil court action.

How this court decision affects your international penalty assessments

This case holds that the IRS may not assess penalties under IRC section 6038(b), or failure to file IRS Form 5471. The case’s ruling doesn’t mean you don’t have an obligation to file IRS Form 5471 — or any other required form.

Ultimately, this decision is expected to have a broad reach and will affect most IRS Form 5471 filers, namely category 1, 4, and 5 filers (but not category 2 and 3 filers, who are subject to penalties under IRC section 6679).

However, the case’s impact could permeate even deeper. For years, some practitioners have spoken out against the IRS’s systemic assessment of international information return (IIR) penalties after a return is filed late, making it impossible for taxpayers to avoid deficiency procedures. The court’s decision now reveals how a taxpayer can be protected by the judicial branch when something is deemed unfair. Farhy took a stand, challenged the system, and won — opening the door for potential challenges in the future.

It’s uncertain as to whether the IRS will appeal the court’s decision. But it seems as though the stakes are too high for the IRS not to appeal. While we don’t know what will happen, a former IRS official has stated he expects that, for cases currently pending review by IRS Appeals, Farhy will not be viewed as controlling law yet.

The impact of the ruling is clear and will most likely impact many taxpayers who are contesting — or who have already paid — IRC 6038 penalties. It may also affect other civil penalties where Congress has not prescribed the method of assessment in the future.

How you should respond to the court’s decision

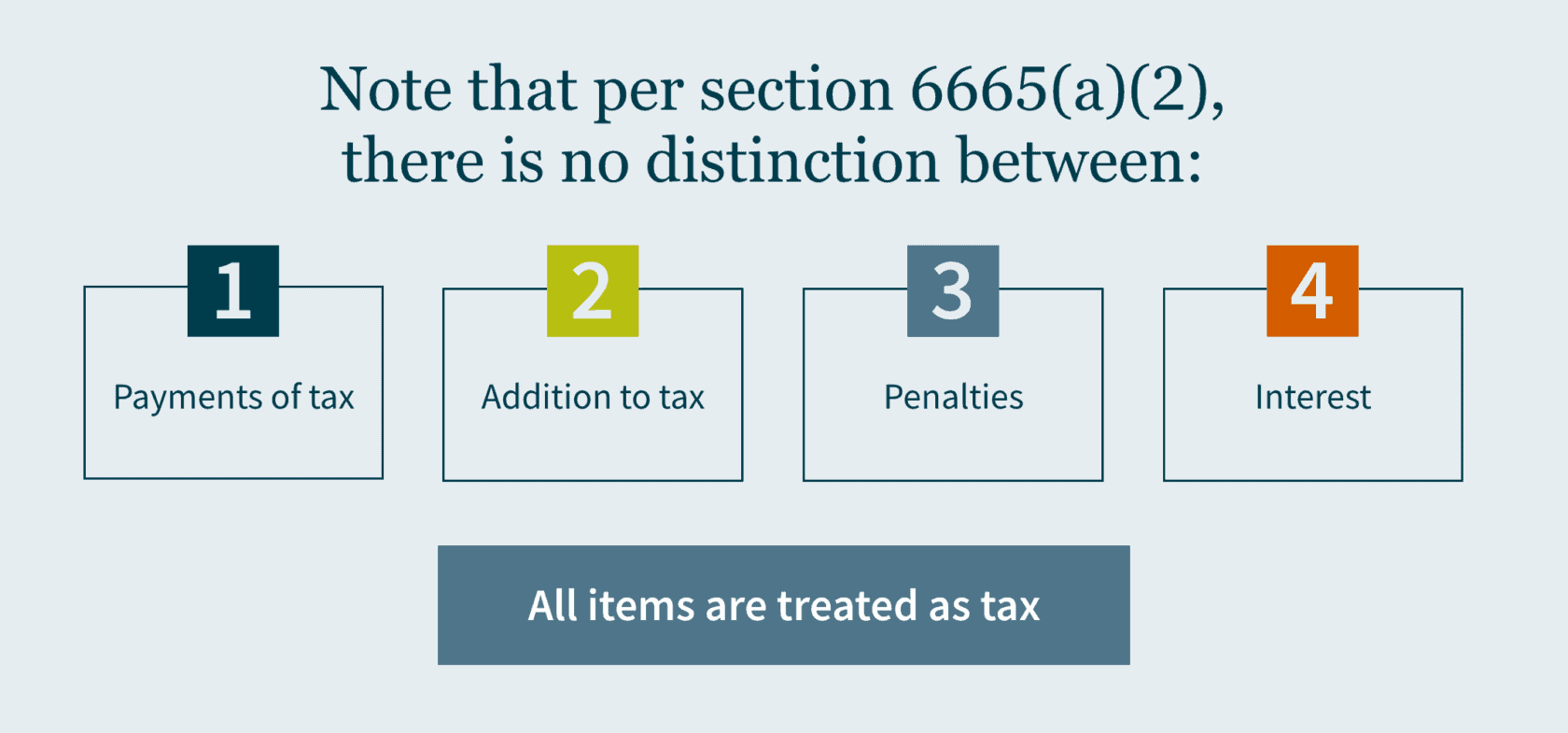

You should move quickly to take advantage of the court’s decision, as there is a two-year statute of limitations from the time a tax is paid to make a protective claim for a refund. It’s likely this legislation wouldn’t affect refund claims since that would be governed by the law that existed when the penalties were assessed. Note that per IRC section 6665(a)(2), there is no distinction between payments of tax, addition to tax, penalties, or interest — so all items are treated as tax.

If you’ve previously paid the $10,000 penalty, it’s important to file your protective claim now, unless you’ve entered into an agreement with the IRS to extend the statute of limitations, which can occur during an examination. Requesting a refund won’t ever hurt, but some practitioners believe the IRS may try to keep any penalty money it collected, even if the assessment is invalid— because, in its eyes, the claim may not be. Just know, you can file your protective claim for a refund but may not get it, at least not any time soon.

The Farhy decision could likewise be applied to other US IRS forms, such as 5472, 8865, 8938, 926, 8858, 8854, and some argue the Farhy decision may also be applied to IRS Form 3520.

How MGO can help

Only time will tell if the court’s decision will open the government up to additional criticisms for other penalty assessments. If you have paid your penalties and are wondering what your current options are, MGO’s experienced International Tax team can help you determine if you’re eligible to file a refund claim.

Contact us to learn more.

]]>

To generate the revenue needed to fully fund the American Jobs Plan, the Made in America Tax Plan proposes reversing the corporate tax decrease that was the centerpiece of the Trump Administration’s Tax Cuts and Jobs Act of 2017. President Biden’s tax plan also proposes a number of other changes, mostly concerning international taxation, with the stated goal of incentivizing job creation and investment in the U.S.

In the following, we discuss practical tax considerations and potential planning points that corporations should consider to prepare for the proposed changes and provide the key provisions of the Made in America Tax Plan.

Planning considerations

With the announcement of the Made in America Tax Plan, major tax changes could be in the forecast. However, it is difficult to predict the ultimate changes or how seismic they will be. The fact sheet released by the White House is in many respects light on detail, and a comprehensive explanation of each proposal will not be available until the Treasury Department releases its “Green Book” this spring. Moreover, each proposal will likely face considerable pushback from Congressional Republicans, and the enactment of any proposal will minimally require the unanimous support of Senate Democrats and the support of the overwhelming majority of House Democrats.

Accordingly, the President’s more ambitious proposals could very well face Congressional gridlock, and may require considerable revision to amass the support necessary for enactment. Compounding this conundrum, several cabinet members, including Treasury Secretary Janet Yellen, have repeatedly indicated that proposed changes will be introduced iteratively, in separate legislation. That, combined with the lengthy congressional reconciliation process, makes it difficult to predict when any one proposal might be enacted, let alone become effective.

The difficulty forecasting the tax plan’s ultimate impact and the likelihood of a prolonged legislative process make interim tax planning exceptionally difficult, as tax professionals cannot reliably predict what is coming, or when. The Biden Administration has not provided any concrete details about timing, but in the fastest possible timeline, legislation could be introduced within the next six weeks, and voted into law within the next six months, with some changes potentially becoming effective for the 2022 tax year. However, the timetable could be considerably longer.

That said, there are financial, operational, and other remedial measures that companies can implement in 2021 to mitigate the eventual impact of Biden’s tax plan. First and foremost, companies should work with their tax advisors to model the potential impact of each of the proposals and, to the extent possible, include milder variants of each proposal (e.g., if the corporate income tax rate were raised to 25% rather than 28%). Using the results of these modeling efforts, companies should devise a strategic plan that accounts for the likeliest changes and identifies both interim and post-enactment measures that to mitigate the impact of potential changes.

Taxpayers and their advisors should also communicate with lawmakers about how each proposal would impact their bottom line, profitability, hiring practices, or other aspects of their business that could be negatively affected by these proposals.

Businesses should consider ceasing international expansion to the extent the tax plan’s proposals would undermine or negate the benefits. However, in some instances, it may well be advantageous to accelerate international expansion or the offshoring of certain operations. Modeling results can inform whether such measures would be beneficial or to a company’s detriment.

Despite the uncertainty, some tax planning measures may well be advisable in 2021. For example, the likelihood that the corporate income tax rate will be increasing could make it advisable to accelerate income recognition in 2021 under a preferable tax rate. Other timing measures could also prove beneficial, such as deferring losses and deductions to a later tax year, refraining from accelerating the deduction of prepaid expenses, capitalizing R&D expenses, or electing out of bonus depreciation. Businesses should work with their tax advisors to identify those measures which should be implemented in the interim period, before any tax law changes are implemented.

Key elements of the Made in America Tax Plan

Set the corporate tax rate at 28 percent

“The President’s tax plan will ensure that corporations pay their fair share of taxes by increasing the corporate tax rate to 28 percent. His plan will return corporate tax revenue as a share of the economy to around its 21st century average from before the 2017 tax law and well below where it stood before the 1980s. This will help fund critical investments in infrastructure, clean energy, R&D, and more to maintain the competitiveness of the United States and grow the economy.”

Discourage offshoring by strengthening the global minimum tax for U.S. multinational corporations

“Right now, the tax code rewards U.S. multinational corporations that shift profits and jobs overseas with a tax exemption for the first ten percent return on foreign assets, and the rest is taxed at half the domestic tax rate. Moreover, the 2017 tax law allows companies to use the taxes they pay in high-tax countries to shield profits in tax havens, encouraging offshoring of jobs. The President’s tax reform proposal will increase the minimum tax on U.S. corporations to 21 percent and calculate it on a country-by-country basis so it hits profits in tax havens. It will also eliminate the rule that allows U.S. companies to pay zero taxes on the first 10 percent of return when they locate investments in foreign countries. By creating incentives for investment here in the United States, we can reward companies that help to grow the U.S. economy and create a more level playing field between domestic companies and multinationals.”

End the race to the bottom around the world

“The United States can lead the world to end the race to the bottom on corporate tax rates. A minimum tax on U.S. corporations alone is insufficient. That can still allow foreign corporations to strip profits out of the United States, and U.S. corporations can potentially escape U.S. tax by inverting and switching their headquarters to foreign countries. This practice must end. President Biden is also proposing to encourage other countries to adopt strong minimum taxes on corporations, just like the United States, so that foreign corporations aren’t advantaged and foreign countries can’t try to get a competitive edge by serving as tax havens. This plan also denies deductions to foreign corporations on payments that could allow them to strip profits out of the United States if they are based in a country that does not adopt a strong minimum tax. It further replaces an ineffective provision in the 2017 tax law that tried to stop foreign corporations from stripping profits out of the United States. The United States is now seeking a global agreement on a strong minimum tax through multilateral negotiations. This provision makes our commitment to a global minimum tax clear. The time has come to level the playing field and no longer allow countries to gain a competitive edge by slashing corporate tax rates.”

Prevent U.S. corporations from inverting or claiming tax havens as their residence

“Under current law, U.S. corporations can acquire or merge with a foreign company to avoid U.S. taxes by claiming to be a foreign company, even though their place of management and operations are in the United States. President Biden is proposing to make it harder for U.S. corporations to invert. This will backstop the other reforms which should address the incentive to do so in the first place.”

Deny companies expense deductions for offshoring jobs and credit expenses for onshoring

“President Biden’s reform proposal will also make sure that companies can no longer write off expenses that come from offshoring jobs. This is a matter of fairness. U.S. taxpayers shouldn’t subsidize companies shipping jobs abroad. Instead, President Biden is also proposing to provide a tax credit to support onshoring jobs.”

Eliminate a loophole for intellectual property that encourages offshoring jobs and invest in effective R&D incentives

“The President’s ambitious reform of the tax code also includes reforming the way it promotes research and development. This starts with a complete elimination of the tax incentives in the Trump tax law for ‘Foreign Derived Intangible Income’ (FDII), which gave corporations a tax break for shifting assets abroad and is ineffective at encouraging corporations to invest in R&D. All of the revenue from repealing the FDII deduction will be used to expand more effective R&D investment incentives.”

Enact A minimum tax on large corporations’ book income

“The President’s tax reform will also ensure that large, profitable corporations cannot exploit loopholes in the tax code to get by without paying U.S. corporate taxes. A 15 percent minimum tax on the income corporations use to report their profits to investors—known as ‘book income’—will backstop the tax plan’s other ambitious reforms and apply only to the very largest corporations.”

Eliminate tax preferences for fossil fuels and make sure polluting industries pay for environmental clean up

“The current tax code includes billions of dollars in subsidies, loopholes, and special foreign tax credits for the fossil fuel industry. As part of the President’s commitment to put the country on a path to net-zero emissions by 2050, his tax reform proposal will eliminate all these special preferences. The President is also proposing to restore payments from polluters into the Superfund Trust Fund so that polluting industries help fairly cover the cost of cleanups.”

Ramping up enforcement against corporations

“All of these measures will make it much harder for the largest corporations to avoid or evade taxes by eliminating parts of the tax code that are too easily abused. This will be paired with an investment in enforcement to make sure corporations pay their fair share. Typical workers’ wages are reported to the IRS and their employer withholds, so they pay all the taxes they owe. By contrast, large corporations have at their disposal loopholes they exploit to avoid or evade tax liabilities, and an army of high-paid tax advisors and accountants who help them get away with this. At the same time, an under-funded IRS lacks the capacity to scrutinize these suspect tax maneuvers: A decade ago, essentially all large corporations were audited annually by the IRS; today, audit rates are less than 50 percent. This plan will reverse these trends, and make sure that the Internal Revenue Service has the resources it needs to effectively enforce the tax laws against corporations. This will be paired with a broader enforcement initiative to be announced in the coming weeks that will address tax evasion among corporations and high-income Americans.”

Final thoughts

The stated goals of Biden’s Made in America Tax Plan is to “raise over $2 trillion over the next 15 years and more than pay for the mostly one-time investments in the American Jobs Plan and then reduce deficits on a permanent basis.” Whether these changes will ultimately be implemented or have the desired effect remains to be seen. In the meantime, US-based corporations, especially those with international operations, must prepare for significant changes to their tax reporting and obligations, despite the difficulty they will face in accurately predicting what those change will be.

]]>Under this Act, foreign companies traded on any U.S. exchanges are required to have their auditors submit to inspection by the Public Company Accounting Oversight Board (PCAOB) in an effort to establish that they’re neither owned nor controlled by a foreign government. With a wealth of Chinese companies trading in the U.S., the legislation is likely to have a significant impact on Chinese companies and their accounting firms, as well as U.S. investors and the capital market, for years to come.

How the HFCAA works

The Act will amend Section 104 the Sarbanes-Oxley Act of 2002, the comprehensive legislation passed by Congress aimed at overseeing the conduct of public companies. Pursuant to the HFCAA, there will be a number of sizable changes.

• First, the Securities and Exchange Commission (SEC) will now be required to identify companies that are utilizing registered public accounting firms located outside the United States that are preventing audits from the PCAOB.

• Additionally, the SEC must prohibit securities trading of these public companies within U.S. markets following three consecutive years of non-inspection. Under the language of the bill, these companies will be prohibited from trading on either a national securities exchange or “through any other method that is within the jurisdiction of the Commission to regulate, including through the method of trading that is commonly referred to as the ‘over-the-counter’ trading of securities.” It should be noted that in the event an issuer receives a trading prohibition, then the issuer is allowed to have the prohibition overturned as long as it is able to retain an accounting firm that can be fully inspected by the PCAOB.

• Also, as part of the Act, there are disclosure requirements for non-inspection years for foreign issuers of securities that utilize firms to prepare audit reports. For instance, they will need to disclose the percentage of shares owned by foreign government entities. They will also need to disclose whether or not foreign government entities have “controlling financial interest with respect to the issue.”

• Finally, there are also disclosure requirements that specifically involve China. According to the Act, the names of each official of the Chinese Communist Party of the board of directors of either the issuer or “the operating entity with respect to the issuer” must be disclosed in their Form 10-K, Form 20-F, and shell company reports. Additionally, it must be disclosed if the issuer’s articles of incorporation (or “equivalent organizing document”) has “any charter of the Chinese Communist Party, including the text of any such charter.”

Potential impact of the HFCAA

While the HFCAA applies to any U.S.-listed company incorporated outside the United States, including Mainland China, Hong Kong, France, and Belgium, it is generally understood as explicitly targeting Chinese companies under the restrictions imposed by the Chinese government.

This Act could lead to an increase in the number Chinese and Hong Kong-based issuers being delisted from U.S. exchanges in the coming years. In fact, according to the list of public companies affected by obstacles to PCAOB inspections, there are more than 200 Chinese companies currently audited by CPA firms in mainland China and Hong Kong that would be negatively impacted. These companies, including popular stocks such as Alibaba Group Holding Ltd – ADR, Baidu Inc, JD.com Inc, and Nio Inc – ADR, could feel the brunt of this new legislation.

Note that the Big Four accounting firms in China are independent from the Big Four in the U.S. and do not meet the audit requirements of the PCAOB since they are under the China’s national security laws and the Chinese Securities Law, which prohibit Chinese companies from providing records “relating to securities business activities” overseas without approval by the Chinese securities regulator. Besides, the imminent enactment would certainly discourage new listing of Chinese companies in the U.S. as it could result in a discount on the trading prices as investors may factor in the potential de-listing risk.

However, it remains to be seen how the SEC implementation will roll out within 90 days of the HFCAA’s enactment, which could be greatly influenced by the new leadership of the SEC. According to Bloomberg, President-elect Joe Biden is expected to pick Gary Gensler to head the SEC.

Additionally, because of the three-year compliance timeline in the Act, Chinese companies may consider several options to mitigate the impending risks. The most likely one is to engage a reputable U.S.-based CPA firm, preferably one that has an established China Group, who understands both the Chinese business climate and the U.S. accounting rules, and most importantly obtain a clean compliance record with PCAOB. Yet, it’s also critical that companies consider other factors such as the investor and make sustainable long-term plan to maintain a legitimate and confident position in US capital markets.

If you have any questions

MGO’s SEC practice has a dedicated China Group experienced with Chinese IPOs, RTOs, M&A deals and the unique characteristics of SPAC acquisitions. To understand your options, and the path ahead, please feel free to reach out to us for a consultation.

This Tax Alert provides an overview of some of the most significant modifications to the U.S. international tax provisions affecting businesses and individuals. We urge clients to evaluate the impact of tax reform and discuss relevant changes with their tax advisors since many of the new provisions may bring about unintended tax consequences with respect to properly implemented structures under the previous U.S. international tax regime. Overall, the changes expand the base of cross-border income to which current U.S. taxation applies.

Additional tax alerts for Individuals | Business

Details of international provisions

Introduction of Participation Exemption System for foreign income

The Act introduces a dividend exemption system that applies to distributions made after December 31, 2017, which generally provides for a 100% dividend received deduction (“DRD”) for the foreign-sourced portion of dividends received by a domestic C corporation from a specified 10%-owned foreign corporation (other than a Passive Foreign Investment Company – “PFIC”) of which it is a U.S. shareholder, provided certain conditions are satisfied. The DRD is available only to C corporations that are not regulated investment companies (“RICs”) or real estate investment trusts (“REITs”).

Note that dividends received from PFICs do not qualify for the DRD and domestic C corporations may not claim foreign tax credits or a deduction for foreign taxes paid or accrued with respect to any dividend allowed the DRD.

To the extent earnings of foreign corporations are neither subpart F income nor subject to the minimum tax rule discussed below, the new participation exemption system moves the U.S. away from a worldwide taxation system towards a territorial tax system for earnings of foreign corporations.

Sales or transfers involving specified 10%-owned foreign corporations

Certain deemed dividends under Code section 1248 – resulting from the sale or exchange of stock of a specified 10%-owned foreign corporation held for over one year – qualify for the 100% DRD under the new law.

The provision also allows a U.S. shareholder to claim a 100% DRD on deemed dividends under section 964(e) resulting from the gain on the sale of foreign stock by a controlled foreign corporation (“CFC”).

Two new loss limitation rules are included in the provision, which are applicable to transfers and distributions made after December 31, 2017:

- A domestic corporation that is allowed a DRD is required to reduce its basis in the stock of the foreign corporation by an amount equal to the DRD, solely for purposes of determining the domestic corporation’s loss on the sale of stock of the foreign corporation.

- A domestic corporation is required to recapture certain foreign branch losses if it transfers substantially all of the assets of a foreign branch to a 10%-owned foreign corporation of which it is a United States shareholder after the transfer. The active trade or business exception of section 367(a)(3) is repealed for transfers made after December 31, 2017, which disfavors the use of foreign branches.

New mandatory repatriation

As a transition to the new participation exemption regime, a mandatory repatriation provision is included targeting previously untaxed earnings and increasing subpart F income by the shareholder’s pro rata share of each specified foreign corporation’s net untaxed post-’86 historical E&P, determined as of November 2 or December 31, 2017 (a measuring date). However, this mandatory inclusion is reduced (but not below zero) by an allocable portion of the taxpayer’s share of foreign E&P deficit of each specified foreign corporation and the taxpayer’s share of its affiliated group’s aggregate unused E&P deficit. Earnings attributable to the shareholder’s aggregate foreign cash position or liquid assets are subject to tax at a 15.5% rate, while earnings attributable to illiquid assets are subject to tax at an 8% rate.

The tax liability is payable over a period of up to eight years, at the election of the U.S. shareholder.

A special rule applies to S corporations under the mandatory repatriation provisions. S corporation shareholders may elect to continue to defer taxation of such foreign income until the S corporation changes its status, sells a substantial amount of its assets, ceases to conduct business, or the electing shareholder transfers their S corporation stock.

Non-corporate U.S. shareholders are exposed to the new mandatory repatriation rule if the specified foreign corporation is a CFC or any foreign corporation with at least one domestic corporate U.S. shareholder, even though the 100% dividend received deduction from foreign subsidiaries only applies to corporate U.S. shareholders under the Act.

Foreign tax credits and sourcing of income modifications

Foreign tax credits are allowed under the new law only with respect to foreign income taxes associated with the taxable portion of the U.S. shareholder’s net mandatory inclusion. Foreign tax credits are disallowed with respect to foreign income taxes attributable to the participation deduction. Taxpayers may not elect to take a deduction for foreign taxes that are disallowed as foreign tax credits.

The U.S. shareholder’s section 78 gross-up should also reflect the portion of foreign taxes attributable to the U.S. shareholder’s net mandatory inclusion.

The deemed paid foreign tax credit provisions under Code Section 902 are repealed while the deemed paid foreign tax credit provisions for subpart F inclusions under Code Section 960 are retained but modified, providing a credit on a current year basis. Foreign tax credits will be counted on an annual basis and will no longer be pooled.

Foreign taxes attributable to distributions of previously taxed income (“PTI”) are also regulated under the Act

The Act also revises the sourcing rules for income from inventory sales. Income from inventory sales is now sourced entirely based on the place of production and not allocated 50/50 to the place of production and the place of sale (based on title passage).

A separate foreign tax credit limitation basket is created under the new law for foreign branch income.

The Act repeals the fair market value method of interest expense apportionment. Taxpayers are now required to allocate and apportion interest expense of members of an affiliated group using the adjusted basis of assets.

New provisions regarding foreign passive and intangible income

The Act has new provisions that adopt a minimum tax on “global intangible low-taxed income” (“GILTI”) and a new special deduction for certain “foreign-derived intangible income” (“FDII”), subject to certain exceptions.

Regardless of whether distributions are actually made by a CFC during the tax year and similarly to the manner in which subpart F income inclusions operate, a U.S. shareholder of a CFC is now required to include in income its pro rata share of GILTI allocated to the CFC for the CFC’s tax year that ends with or within its own tax year.

GILTI provisions target a portion of the CFCs’ active (non-Subpart F) income and tax it at an effective tax rate of 10.5% prior to 2026 — generally speaking, the targeted portion is equal to the net income over a routine or ordinary return, defined as the excess of an implied 10% rate of return on the adjusted basis of the CFC’s tangible depreciable property used in generating the active income.

In conjunction with the new minimum GILTI tax regime, excess returns earned directly by a U.S. corporation from foreign sales (including licenses and leases) or services defined as FDII are now also subject to a 13.125% effective tax rate (increased to 16.406% starting in 2026). FDII is the amount of a U.S. corporation’s “deemed intangible income” that is attributable to sales of property (including licenses and leases) to foreign persons for use outside the U.S. or the performance of services for foreign persons or with respect to property outside the U.S.

Corporate shareholders are allowed a deduction equal to maximum 50% of GILTI (reduced to 37.5% starting in 2026) plus any corresponding Code section 78 gross-up plus maximum 37.5% of taxpayer’s FDII (reduced to 21.875% starting in 2026) – combined, these three components comprise the GILTI deduction. Not that the total GILTI deduction cannot exceed a corporation’s taxable income. S corporations or domestic corporations that are RICs or REITs are not allowed to claim this deduction. Transfers to foreign related persons generally do not qualify for FDII benefits.

U.S. shareholders can make a Code Section 962 election with respect to GILTI inclusions, which subjects the shareholder to tax on the GILTI inclusion based on corporate rates, and allows the electing shareholder to claim foreign tax credits on the inclusion as if the shareholder were a domestic corporation.

Modification to subpart F rules

The inclusion based on the withdrawal of previously excluded subpart F income from qualified investment is repealed.

The provision that provides for the inclusion of foreign base company oil-related income is repealed; hence, previously excluded foreign shipping income of a foreign subsidiary is no longer subject to current U.S. taxation under the subpart F rules if there is a net decrease in qualified shipping investments.

Stock attribution rules for determining status of a foreign corporation as a CFC are modified, which makes it more likely for a foreign corporation to be treated as a CFC as a result of the stock of certain related foreign persons being attributed downward to a U.S. citizen. As a result, for example, stock owned by a foreign corporation would be treated as constructively owned by its wholly-owned domestic subsidiary for purposes of determining the U.S. shareholder status of the subsidiary and the CFC status of the foreign corporation.

The new law eliminates the requirement that a corporation be a CFC for 30 days before subpart F inclusions apply.

Prevention of base erosion

The Act includes additional anti-base erosion measures, including a Base Erosion Anti- Abuse Tax (“BEAT”) for certain payments paid or accrued in tax years beginning after December 31, 2017. In general, the BEAT imposes a minimum tax on certain deductible payments made to foreign affiliates, including royalties and management fees, but excluding cost of goods sold.

Income shifting through intangible property transfers is further limited. This includes treating goodwill and going concern value and workforce in place as section 936(h)(3)(B) intangibles and, requiring the use of the aggregate basis valuation method in the case of transfers of multiple intangible properties in one or more related transactions. This applies if it is determined that an aggregate basis achieves a more reliable result than an asset-by-asset approach.

Deductions for certain related party interest or royalty payments paid or accrued in certain hybrid transactions or with certain hybrid entities are now disallowed under certain circumstances. The Act provides that the Secretary of State shall issue regulations or other guidance as may be necessary or appropriate to carry out the purposes of the provision for branches (domestic or foreign) and domestic entities, even if such branches or entities do not meet the statutory definition of a hybrid entity.

New rules were incorporated to limit the deductibility of interest within a corporate group.

Surrogate foreign corporations are not eligible for the reduced rate on dividends under the Act.

MGO insights

The Tax Cuts and Jobs Act is the largest overhaul of the tax system in over three decades and will have a significant impact on U.S.-based multinational companies as well as inbound businesses. The bill fundamentally changes the landscape of U.S. international taxation. We recommend that companies, individuals, and flow through entities engaged in cross border business discuss their specific situation with MGO’s experienced international tax professionals and consultants – we are here to help you navigate the changes of this comprehensive tax reform.

]]>