Specific scams that mask as abusive or fraudulent tax avoidance strategies to be aware of include concealing assets in offshore accounts and improper reporting of digital assets, manipulation of high-income taxpayers to file their tax returns, abusive syndicated conservation easements, and abusive micro-captive insurance arrangements. Read more to round out the annual list for the 2022 filing season.

Tips for taxpayers on emerging scams

To avoid compromising yourself with these “too good to be true” schemes, taxpayers should stay wary, as these scams adopt a wide range of communication methods, including:

- Emails

- Phone calls

- Social media posts

- Targeted online advertisements

You must also consider each source before putting any of these arrangements on your tax returns — because ultimately, you are the one responsible for what is on the return, not the promoter who reached out to you and made a promise they failed to uphold. To mitigate risk, an anxious taxpayer should turn to trustworthy tax professionals to assist with their returns.

Read on to learn about these Dirty Dozen scams targeted primarily to high-net-worth individuals who may be trying to knowingly — or unknowingly — avoid filing.

Scam #9: Concealing Assets in Offshore Accounts and the Improper Reporting of Digital Assets

We hear Switzerland is beautiful this time of year … and so do some high-net-worth individuals looking to conceal their assets in offshore accounts (and yes, that does include cryptocurrency and other digital assets). As more taxpayers look to complex international tax avoidance schemes, the IRS is more determined than ever to “protect the integrity of the U.S. tax system” by enforcing tax responsibilities.

Whether it entails offshore banks, brokerage accounts, nominee entities, employee leasing schemes, foreign trusts, structured transactions, or private annuities, all are designed to hide the true owner of an account — which is illegal, considering U.S. taxpayers are taxed on all the income they make, not just what they keep in the country. But scammers know you may not want to give up some of your hard-earned assets to Uncle Sam. So, what do they do? They sell you a convincing story: you can easily evade the government and hide your assets through digital asset holdings; they claim these are “undetectable by tax authorities.” The catch? They are definitely detectable. By believing these fraudsters, you run the risk of being criminally charged or penalized, so in the end, it is better to report your assets — yes, all of them — when you file.

Scam #10: High-Income Individuals Who Don’t File Tax Returns

Believe it or not, there are some taxpayers who choose to just … not file a tax return. And believe it or not, there are scamming professionals out there aiming to convince you this is a good idea. The IRS takes this seriously. If you are considering this option, remember the Failure to File Penalty is higher than the Failure to Pay Penalty, meaning you are better off filing an accurate, timely return (and setting up a payment plan, if you are concerned about that) rather than not filing and hoping you get out of paying whatever taxes you owe.

Scam #11: Abusive Syndicated Conservation Easements

In this scam, dishonest promoters manipulate a part of the tax law that allows for conservation easements by inflating appraisals of underdeveloped land (i.e., the guise of a real estate investment) and engaging in bogus partnerships without a business purpose. These “deals” rarely help you out; instead, they benefit the promoters, who charge high fees, and clog the tax system with fraudulent tax deductions. (In the last five years, the IRS determined billions of dollars of deductions were wrongly claimed!) And if you are caught — which, you should expect to be, because the IRS takes a microscope to every single one of these “deals” — you can expect large fines and potential time in court.

Scam #12: Abusive Micro-Captive Insurance Arrangements

A high priority for the IRS, this scam sees professionals like accountants and wealth planners convince entity owners to pay for what they believe to be insurance coverage against unlikely events, events that are already being covered, or disingenuous business needs. Complete with sky-high premiums, the abusive structure does the opposite of protecting your organization’s tax safety — it opens you up to more risk as a ”micro-captive” to these “professionals” taking advantage of you. Be on the lookout for an offshore version of this too.

Consequences of falling for a Dirty Dozen scheme

It is important for taxpayers who have already taken part in transactions like these — or those who are thinking about doing so — to consult a tax professional before claiming any tax benefits they think they are owed.

Those taxpayers who have already claimed the purported tax benefits of one of these four “Dirty Dozen” arrangements on a tax return should file an amended return and go to an independent professional for guidance. If necessary, the IRS will examine the tax benefits from transactions like the ones depicted in the list and inflict penalties related to accuracy ranging from 20% to 40%, or a civil fraud penalty of 75% on any taxpayer who underpaid.

Our perspective on the latest batch of “Dirty Dozen” scams

This is not, of course, an exhaustive list of every scam the IRS has its eye on this year. But it does include some of the more common trends. The best advice we can give? If something looks too good to be true … it probably is. Consult your tax professional for guidance and know that it is in your best interest to stay aware of these nefarious arrangements, so you do not fall susceptible to additional penalties.

And remember, you cannot hide income from the IRS!

MGO’s Tax team brings more than 30 years of experience and is well versed in reviewing your return for compliance. We also stay up to date on the risks, pitfalls, and warnings issued by the IRS so you don’t have to. If you think you have been involved in or are in the process of being involved in one of the Dirty Dozen scams, we can help. Contact us today.

]]>An unexpected consequence of economic downturn that started in 2008 was an increase of fraud across a wide variety of industries. As companies turned to layoffs as a way to lower overhead, many organizations unintentionally exposed themselves to potential fraud by laying-off employees who oversaw essential internal controls or served in a system of checks and balances that would have prevented fraud. According to the Association of Certified Fraud Examiners (“ACFE”), the combination of omnipresent economic pressure, and a lack of controls, resulted in historic levels of fraud following the recession. As a result, companies as large as Fortune 500 organizations, and as small as local businesses, have been forced to course correct and get a handle on fraud.

The first step toward preventing fraud is gaining a holistic view of the circumstances under which it occurs. The ACFE provided the following touchpoints to establish a baseline understanding of how fraud occurs:

- Organizations lose approximately 5% of revenue due to fraud

- Average fraud duration is 18 months

- 40% of fraud cases were detected via Tip /Hotline

- 75% of fraud cases were committed by employees working in seen departments:

– Accounting & Finance

– Purchasing

– Executive /Upper management

– Operations

– Customer Service

– Sales

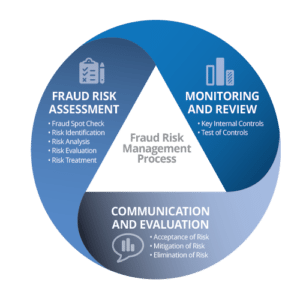

How do we fight fraud?

Fundamentally, business fraud prevention is a three-step process that combines reviews of operations and internal controls, the acceptance of certain conditions, and the systematic elimination of those risks.

Assessing fraud risk

The first step to preventing fraud is identifying opportunities for fraud and assessing the risk. Fraud can appear in unexpected ways. Therefore, a spot check of departments and operations is a necessary step. While following guidelines of where fraud is likely to occur (like those provided by the ACFE above) is a good way to prioritize activities, it should not limit the inquiry. The fraud assessment should be performed by employees independent of the operation or department, ideally by your in-house fraud investigation team, or internal audit department. Furthermore, collaborating with an outside subject matter expert, or Certified Fraud Examiner (“CFE”), can augment your team, providing a critical perspective for identifying fraud and developing internal procedures to eliminate fraud in the future.

Monitoring and review

An evergreen component of fraud prevention is the monitoring and review of internal controls. A sound internal control structure is the first line of defense against fraud (and a vast array of other operational hazards). Performing regularly scheduled testing, and updating controls based on the results of the testing, will create an operational structure actively working to limit opportunities for fraud.

Communication and evaluation

After the Assessment, and Monitoring stages, your organization can make final decisions based on the findings. The review function (whether performed by a CFE, internal auditor, or consultant) will present a final report on each stage of the operational review to the Internal Audit Committee, Board, or other decision-making body. The report should identify all gaps, assign risk levels, and propose solutions.

With this holistic view of operations, risks, and costs associated with fraud prevention in hand, the decision-making body can make informed decisions on the most efficient ways to shore up defenses and proactively prevent fraud.

Tips on developing internal controls

Internal Controls fall into two general categories: preventative controls and detective controls. The former are systems put in place to limit the possibility of fraud, whereas the latter can be enacted to identify and root out active, or historical, fraudulent activities. Each type of internal control requires specific knowledge of industry standards, business operations, and the culture of the organization.

Preventative controls can be the most effective, yet unheralded champions of fraud prevention, as they prevent fraud before it occurs. These can be difficult to “sell” to a governing body, as their upfront cost may not be easily balanced by definable losses saved.

Factors to consider when designing preventative controls:

- Business strategy and culture

- Utilization of IT systems

- Length of existing processes

- Consistent process outcomes

- Ability to circumvent internal controls

- Employee empowerment

Detective controls are an opportunity to identify and root out on-going or historical fraud. These controls tend to follow “after the fact” and are an attempt to “right a wrong,” when there has already been potentially significant loss. While it is always preferable to prevent fraud before the act, detective controls can produce valuable insights that can be used to prevent future fraudulent actions.

Factors to consider when designing detective controls:

- Average or expected outcomes

- Types of trends and patterns

- Unusual activity or outliers

- Review information from different directions

- Changes to defined time periods reviewed

- Utilization of IT systems

The limits of internal controls

While robust internal controls are the most effective solution to fighting fraud, there simply is no “fool-proof” system. A company must remain vigilant, responsive and adaptable to changing factors outside the limits of internal controls – factors like employee turnover and external economic pressures.

Understanding the limits of internal control structures is an important step toward developing a system that accounts for as many variable as possible. Common limits to internal controls include:

- Human judgment

- Management’s ability to override controls

- Maintaining sufficient resources to achieve adequate segregation of duties

- Breakdown of controls

- High management turnover

- Lack of employee training

- Poorly documented policies & procedures

- Internal audit plan not based on risk of operations

There is no “solution,” only steps to mitigate or uncover

Fraud is a major issue with which every organization – including public companies, growing small businesses, government institutions, or tribal entities – must actively contend. The economic downturn and the layoffs, downsizing and other negative economic outcomes that followed have created an environment where fraud is rampant, with no cessation in sight. Every organization must take a hard look at its operations, culture and internal controls to assess opportunities for fraudulent activity, and take the steps necessary to remove or limit those opportunities.

Stay tuned for future articles in this series where we will take a close look at what organizations can do to limit fraud.

]]>By Scott P. Johnson, CPA, CGMA

Partner, State & Local Government, Advisory Services

As a public official for more than 24 years, I continuously strived to implement best practices, internal controls and policies and procedures to mitigate fraud, waste and abuse. Being a municipal finance officer responsible for literally billions of dollars, there were times when I would wake up in the middle of the night thinking about what could happen or what I may not know that could be occurring that could put the organization at risk. Fortunately throughout my municipal career the organizations I served did not experience headlines due to significant fraud. We had the appropriate “tone at the top” and practiced effective measures throughout the organization to mitigate potential fraud. However, from time-to-time, we would uncover the occasional lapse of an employee’s good judgement and detect inappropriate use of government funds, such as; improper procurement credit card use for personal purposes, time cards reporting that fraudulently claimed hours worked in excess of actual hours worked, and fictitious reimbursement claims for travel.

Employee fraud is a significant problem across industries and is faced by organizations of all types, sizes, locations, and industries. While employee fraud in private organizations rarely merits a mention in the local paper, the same fraud in a government agency will have editors competing to write the splashiest headlines and garner the highest reader traffic. It is critical for such organizations to maintain a positive reputation. Reputational risk can carry long-lasting damage in monetary losses, regulatory issues, and overall risk exposure. Frankly, all types of fraud are on the rise, and municipalities need an effective fraud mitigation strategy in place to protect against reputational and monetary harm.

Just a few recent examples of municipal fraud that have had significant press coverage and put the respective organizations in a challenging position: In 2014 officials in St. Louis County, IL, uncovered a $3.4 million embezzlement that escaped detection for more than six years. According to officials, a County Health Agency Division Manager overcharged for IT computer and technical services (unbeknownst to the County, the Division Manager owned the technology company). Unfortunately, the day after the suspected embezzlement was detected by County officials, the employee committed suicide, according to the County Medical Examiner.

The largest known municipal fraud in US history was uncovered in 2012 at the City of Dixon, IL. This embezzlement scheme of almost $54 million over a 22 year period was perpetrated by its Comptroller, Rita Crundwell, who used the proceeds to finance her quarter horse ranch business and lavish lifestyle. She was convicted and pleaded guilty to the crimes and is currently serving a 20 year sentence. Another recent case of an alleged fraud allegation is currently under trial in the Los Angeles Superior Court in which ex-Pasadena city employee, Danny Wooten and co-defendants are due back in court for arraignment on April 1, 2016, according to the Los Angeles County District Attorney’s Office. The criminal case involves allegations that more than $6 million in city money was embezzled over a decade in which Wooten is suspected of creating false invoices for the underground utility program between 2004 and March 2014.

Many factors can contribute to fraud, but the key factors are the improper segregation of duties, lack of management review, maintaining undocumented procedures, common exception processing, trust without verification and validation, and lack of accountability and monitoring. Employing proper risk assessments of events that could prevent, delay, or increase the costs of achieving organizational objectives and implementing a risk management plan not only ensure compliance, but strategically safeguard on organization against fraud. There are three important steps to earning a good night’s sleep.

1. Fraud Risk Assessment – understanding the organization as a whole and individual business units will lead to the most comprehensive risk management plan. Understand how resources flow as well as internal environments and processes. Conduct interviews, make observations and review all factors. Identify the possible and probable fraud schemes for all resource flows.

2. Prevention – “Tone at the Top” is critical. Inspiring employees to follow ethical standards starts with the tone at the executive level and must trickle down through the management level and ultimately throughout the entire organization. The organization needs to know that unethical practices will not be tolerated and when detected, will be dealt with in a timely and effective manner. One measure to communicate the “tone” is writing a fraud policy in concert with the employee conduct handbook will ensure the message is designed into the orientation, onboarding, and training process. Conduct management reviews, provide whistleblower channels, and communicate often with key business unit leaders, who in turn should communicate with their staff regarding fraud prevention, detection, and correction.

3. Detection – while assessment and prevention will create a strong defense against fraud, it is still important to seek out other measures to detect fraud that may not have been included in the fraud risk assessment plan. Only three percent (3%) of all fraud is discovered by accident or the good luck of the right person in the right place. Only six percent (6%) of fraud is discovered through account reconciliation. Clearly we cannot simply rely on these detection methods. In addition to account reconciliation and keeping your ears open, creating channels for detection are of the utmost importance. Eleven percent (11%) of fraud discoveries are due to an internal audit. Return to step one by assessing and re-assessing fraud risk regularly. Conduct meaningful management reviews on-time. Twelve percent (12%) of fraud detection were the result of properly conducted management reviews. Finally, be sure to enforce an open door policy and a culture of interest in detection and reporting. Fifty-four percent (54%) of all fraud detection comes through insider tips. Ensuring there are proper procedures in place to accept these tips is paramount when designing and especially, implementing the fraud management and detection plan.

Deceitful misconduct among employees significantly damages reputations, negatively affects resources, and limits the ability of any organization to effectively serve the consumer and their community. Following this roadmap on how to respond to and prevent employee fraud will not only protect the organization and its key objectives but will lead to an easier night’s sleep – even in the face of increasing fraud across all industries.

This article is only a small representation of the material presented during MGO’s “Case in Point” presentation at the 2016 CSMFO Conference. Special recognition to Ruthe Holden, Internal Audit Manager at the City of Pasadena for her contribution to the “Case in Point” presentation. Contact Scott Johnson at sjohnson@mgocpa.com if you have any questions or comments. Comments and opinions expressed in this article are those of the authors and may not reflect the positions, opinions, or beliefs of the CSFMO or MGO and should not be construed or interpreted as such.

]]>Big earnings do not equal a lifetime of financial comfort

High tier individuals in entertainment can earn more money in a year than the average person makes in a lifetime. Yet, in a Forbes study of 165 talent agents and managers, more than nine out of ten interviewed claim a large percentage of their top tier clients have little or no understanding of wealth or how to handle that wealth for themselves.

As a result, a number of financial perils consistently trap, and occasionally ruin, a number of high-earning individuals. The media and the general public only care about the splashy, flashy tawdry spectacle of a former star down on their luck. That attention only addresses the symptoms of a disease, but never gets to the core cause that would enable a person to find a cure.

The dangers of lavish spending

Many talented individuals make the mistake of buying into media depictions of how people with status in the entertainment industry “should” live and have little or no concept of how to keep themselves financially grounded. Often there is a perception that one should not only live their lives as if they are successful, but there is pressure to show that life to the world at large, most recently through the lens of social media.

Michael Jackson is just one of many celebrities who faced bankruptcy and financial ruin late in his career. The performer had zero self-control when it came to lavish spending. His Neverland Ranch and collection of oddities are a legendary lesson in the danger of excess and paved the road to his financial ruin.

Another behavior pattern that has led to lavish spending is a general negativity attached to money, referred to as “demonized wealth.” In this case, people from a lower income bracket are suddenly thrust into a position of high wealth, and feel that being wealthy is bad, dirty, or somehow embarrassing. This could be due to how they were raised, or gained from observing the behaviors of other wealthy individuals. Demonizing one’s wealth can lead to talent spending money as soon as they earn it, in an attempt to get rid of it, instead of letting it grow.

The risks of poor investments

Many celebrities try to make smart money choices by investing in real estate, emerging companies or other investment vehicles. For every stunning success, like 50 Cent’s famous investment in Vitamin Water, there are countless stories of failed investments. While risk is part of any investment strategy, far too many celebrities over-extend themselves in pursuit of greater wealth.

Kim Basinger and Burt Reynolds, A-List movie stars at the height of their fame, ran into financial distress due to poor investments. In Basinger’s case, the actress invested in a town outside Atlanta, Georgia, intending to turn it into a tourist destination. Just five years later, on the brink of financial ruin, Basinger and the other investors sold the property at a significant loss. For Reynolds the damage of a series of costly divorces was exacerbated by a major investment in a failed restaurant chain.

In both cases, the celebrities where trying to be proactive about securing and growing their personal wealth. But poor advice and over-extending their finances led them to ruin.

Lack of experienced financial guidance

New wealth in Hollywood comes with a wide variety of financial pitfalls and traps. Some celebrities do plan ahead and seek out financial advice early in their careers, but it can often fall severely short of the depth and breadth of options that are available to them. While many are wise enough to work with a “financial advisor” all too often that source of advice is not qualified for the role, or is downright criminally-minded.

R&B singer Toni Braxton placed her financial trust in her manager and his record label only to ultimately lose everything. It is a common story, where a celebrity places financial trust in someone who is either close to them (a friend or relative) or who is a scam artist disguised as a financial advisor. Those advisors then provide poor advice that seemingly enriches everyone else at the expense of the celebrities themselves.

How can talent avoid the financial pitfalls?

We’ll be discussing this in depth in the next installment of this series of articles, but the best thing high-earning talent can do is to find themselves a brilliant financial team to work with and for them. A top tier individual in entertainment should look at the management of their wealth the same way a mid-sized company would. The person earing the income is the CEO of their own business with their name as the brand. They then need a CFO and a team of experts that are the best in their specific fields of wealth management, diversified investing, and financial planning. Proper financial planning with a team can give someone a healthy, prosperous, and well-rounded financial lifestyle; while still enabling them to plan for the future and the security that comes with smart investment moves.

]]>The financial perils celebrities face in Hollywood

A professional athlete or a top tier individual in entertainment should look at their expanded wealth and the management of that wealth the same way a mid-sized company would. The person earning the income is the CEO of the business and their name is the brand. They need a CFO to manage finances who is supported by a team of experts who are the best in their fields of wealth management, diversified investing, and financial planning. This team then enables the talent to get the best use out of their wealth while still making provisions for a comfortable future.

A good partnership between a high earning professional and a financial team can yield endless results and allow earners to live comfortably now and long into the future when considering retirement. Trust is the key to a successful working relationship between a high-income client and their financial team. With that trust established; the future of an individual and their family will be assured with strategy, planning, and more than just a bit of market savvy.

The first step in working with a professional financial team is to take ownership of financial awareness and education. It’s important that the earner takes time whether over the phone, remotely through video conference, or when possible in person; to sit and talk to their financial professionals. This will help them understand how and why their money is being managed the way it is.

A financial team needs to be allowed to act as guardians of wealth

High-earning talent must allow their financial team to act as guardians and keepers of their money. In the worlds of sports and entertainment celebrity, very few things are ever denied top-earning talent, and quite often they are not acquainted with the word “no.”

This is where financial teams step in to not only shield talent from financial predators and bad investments, but to also protect the earner’s money from themselves by helping curb extravagant spending and off-the-wall purchases. A good financial professional team is the best line of defense against money disappearing with no return.

Establish current and future goals for the life you want

A series of goals must be set by the earner and their financial professionals to properly plan for the future. Where do you want to be when you retire? What kind of life do you want to have? With the money you have coming in, what sort of plans can you make for yourself and your family? It’s important that individuals set realistic goals that are guided by their financial team, and that they maintain solid credit through their more lucrative years so they have an excellent history to build from.

Work to establish a series of sound and profitable investments

Talent can work with their financial team to establish investments that will earn returns and dividends that they can draw upon once they are no longer working. Municipal Bonds and ETFs in efficient markets are examples of smart investments. There are a multitude of options available, and if your financial team is savvy; they can advise you in the world of alternative investments like casinos, restaurants, hotels, and newer

markets like cannabis.

Get the right insurance for your career and risk profile

The financial team must work to ensure that talent has adequate insurance. Athletes take risks with their bodies all the time, so it is important that a player maintains the correct type of insurance that will cover them if they are injured and are unable to return to playing for a season. Or in a worst case scenario, they are forced into early retirement by an injury. The same can is true for actors, directors, and professionals in the world of entertainment. On-set accidents do happen, and if a person is unable to work in their chosen field; their earnings drop to next to nothing.

There is an energy and synergy to money

There is a synergy and energy to the exchange of money. Money is like an electrical current and a flow must be maintained at all times for wealth to increase in size. There needs to be a give and receive in place when balancing an individuals’ investments and wealth, and there is always the value of giving vs. receiving to consider. This journey to finding a balance with a financial team and a true vision of what a person wants to achieve with their wealth and their life is a much broader topic; which we’ll be discussing soon enough. So, just keep your eyes open for further editorials in this ongoing series!

]]>