- California Governor Newsom strives to amend the personal income tax laws to prevent wealthy taxpayers from utilizing Incomplete Gift Non-Grantor trusts.

- California residents use this by transferring assets into trusts held by nonresident trustees in states without income tax.

- If this legislation passes, taxpayers will no longer be able to take advantage of the strategy.

If you reduce California income tax with an ING, Newsom is onto you

Californian legislators propose to amend the personal income tax laws to close a little-known-but-effective loophole for the wealthy by targeting Incomplete Gift Non-Grantor (ING) trusts set up in other states with more favorable income tax rules. To date, California residents have had the opportunity to transfer assets into these trusts held by nonresident trustees in states without income tax, utilizing the state’s sourcing rules to avoid the tax. If approved, this new legislation will put a stop to this tax planning strategy.

Taxing the rich in California

As it stands, the ING trust is not commonly used. There are about 1,500 California residents with this trust in states without income tax — and if implemented, California would see a minimal revenue increase (about $30 million in the first year and $15 million in the following years). However, this would put an end to a tax planning strategy the wealthy have been using to their benefit for about 20 years.

Because California is home to more billionaires than any other state at the same time as it also has the highest rate of poverty in the U.S., the concept of taxing the rich holds a certain appeal. In the past, Newsom has opposed proposals to raise taxes — but this proposal was included in the governor’s $223.6 billion budget plan for the next fiscal year, which begins in July. Whether the item survives the legislative process remains to be seen, but if New York’s passage of a similar law in 2014 is any indication, we are likely to see the end of this tax planning strategy for California’s ultra-rich.

Moreover, this proposal has a retroactive element, differentiating it from New York’s and opening it up to potential lawsuits (New York trust holders had a five-month period to move their accounts to a different type of trust without incurring the tax). Newsom is pushing for the measure to begin the calendar year after its implementation.

How the ING works (worked)

What is an ING, and why is Newsom trying to prevent its use? California taxpayers can transfer their assets into out-of-state, incomplete, non-grantor trusts (INGs), which constitute separate, taxable entities under state and federal tax law, and this move avoids California income tax on any appreciation or gains from those assets because it is “sourced” to another state based on the location of the trustee (i.e., the bank or whatever financial institution offers the trustee services in the other state). The non-grantor aspect comes into play when the taxpayer establishing the trust (the “grantor”) gives up control over managing investments or distributing assets to the trustee (contrast with a “grantor trust” in which the grantor continues to control how money is invested/distributed within the trust during their lifetime). For the trust to be deemed “incomplete,” the grantors specify how the money can be used.

Some of the states where these trusts are typically established include Florida, Wyoming, Delaware, Nevada, Tennessee, and South Dakota. For example, a California resident (TP) may decide to transfer stock in their business into an ING established in South Dakota. If TP held the stock directly, then as a resident, all the dividends (or if he sold it, the gain) would be taxable by California on their personal income tax return. But since TP doesn’t hold the asset – the ING does – the ING recognizes the income relating to the stock. California’s current rules provide that the income is sourced to (and thus taxable in) the state where the trustee is domiciled, and for this ING that location is South Dakota, which, incidentally, does not tax this sort of income.

Newsom is hoping that by eliminating this tax-free option, the state of California will be able to increase tax revenue in a way that will not alienate a large number of voters.

How MGO can help

If you are a California resident and currently use an ING as a tax strategy, there are steps to take now to avoid a negative impact. MGO’s experienced Private Client Services team can help you identify and implement an effective response.

]]>At a Glance…

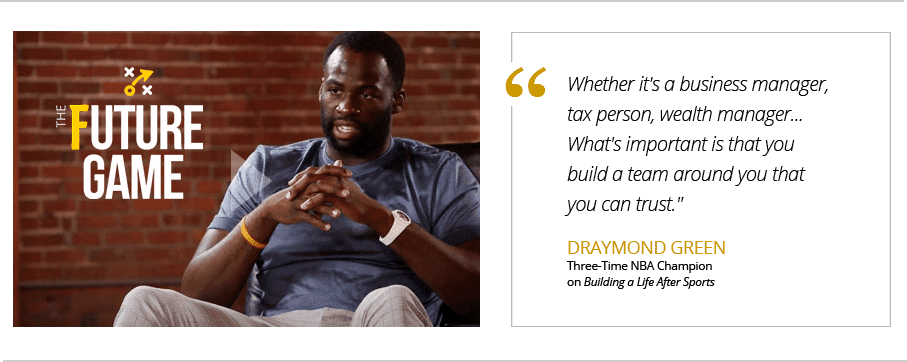

- A professional athlete is the CEO of the brand that bears his or her name. That’s why sports stars should turn to the strategies employed by the world’s most successful entrepreneurs and executives as a playbook for long-term success. In short, they need to think like a CEO.

- Building a high-performing team is the number-one priority for growth-oriented businesses, and it’s no different for the Athlete/CEO. Drawing from the proven team-building models of the corporate world and the entertainment industry, we’ve developed the MGO Model, tailored to the unique needs of Athlete/CEOs.

- The Business Manager is the Financial Quarterback of an Athlete/CEO’s team. He or she is responsible for the daily oversight of a client’s financial affairs. That includes tax planning and compliance, establishing budgets, paying the bills, managing cash flow, and advising on major financial decisions. The Athlete/CEO should carefully vet the qualifications of anyone serving in this critical role.

Background

In the first installment of this series, we noted that the financial profile of a professional athlete more closely resembles a mid-sized, private company than a typical household. While the economics can be exceptional, an alarming number of players lack the support structure necessary to navigate the depth and complexity of their financial requirements.

A professional athlete is the CEO of the brand that bears his or her name. To ensure the long-term value of that brand, the Athlete/CEO needs to embrace that role and reimagine their future beyond the playing field. In this series, we examine the mindsets and practices of some of the world’s most effective business leaders as a model for navigating the unique challenges and opportunities facing professional athletes.

Building a Team

John Wooden said, “The main ingredient to stardom is the rest of the team.” This is just as true in the business world as it is in the world of professional sports. That’s why the world’s top CEOs make team-building their first priority. The way they approach that process serves as a valuable roadmap for Athlete/CEOs.

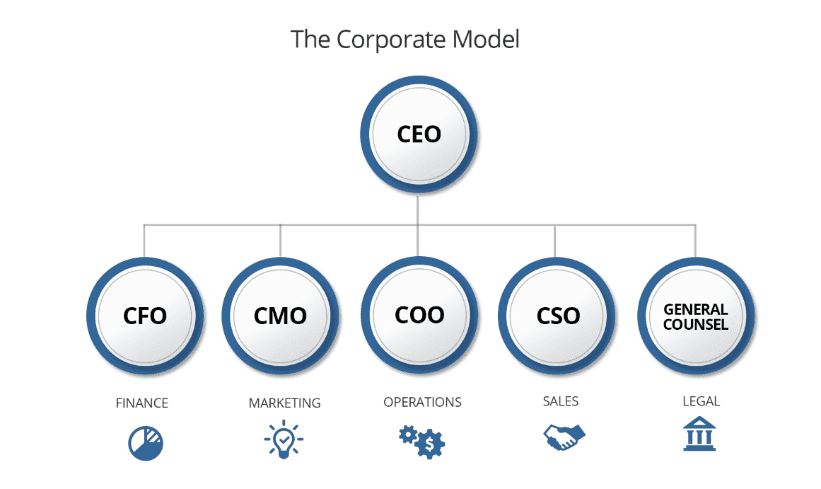

The Corporate Model

Most businesses share a common structural framework. While details may vary across different industries and global regions, the core elements of the Corporate Model (below) remain consistent. This framework identifies the primary business functions and areas of expertise critical to an organization’s success.

The Corporate Model has been successfully adapted to a wide variety of business categories, evolving as necessary to the unique needs of each organization’s operating environment. When working with athletes, perhaps the most relevant example is the entertainment industry.

The Hollywood Model

The Film & Television industry shares many of the traits of people working in professional sports. The quality of the product is determined largely by the quality of the talent in the spotlight – driving significant demand and high salaries for the best actors, directors, writers, etc. Over the years, Hollywood leaders recognized that many of the same principles of growth and financial governance in the corporate world apply to the financial lives of talent in Film & Television. This led to the evolution of what we call the Hollywood Model (shown below).

This model identifies the importance of each individual role in the Corporate Model, albeit by different names. For example, the Business Manager takes on the role of the Chief Financial Officer (CFO), serving as the quarterback of the client’s financial affairs.

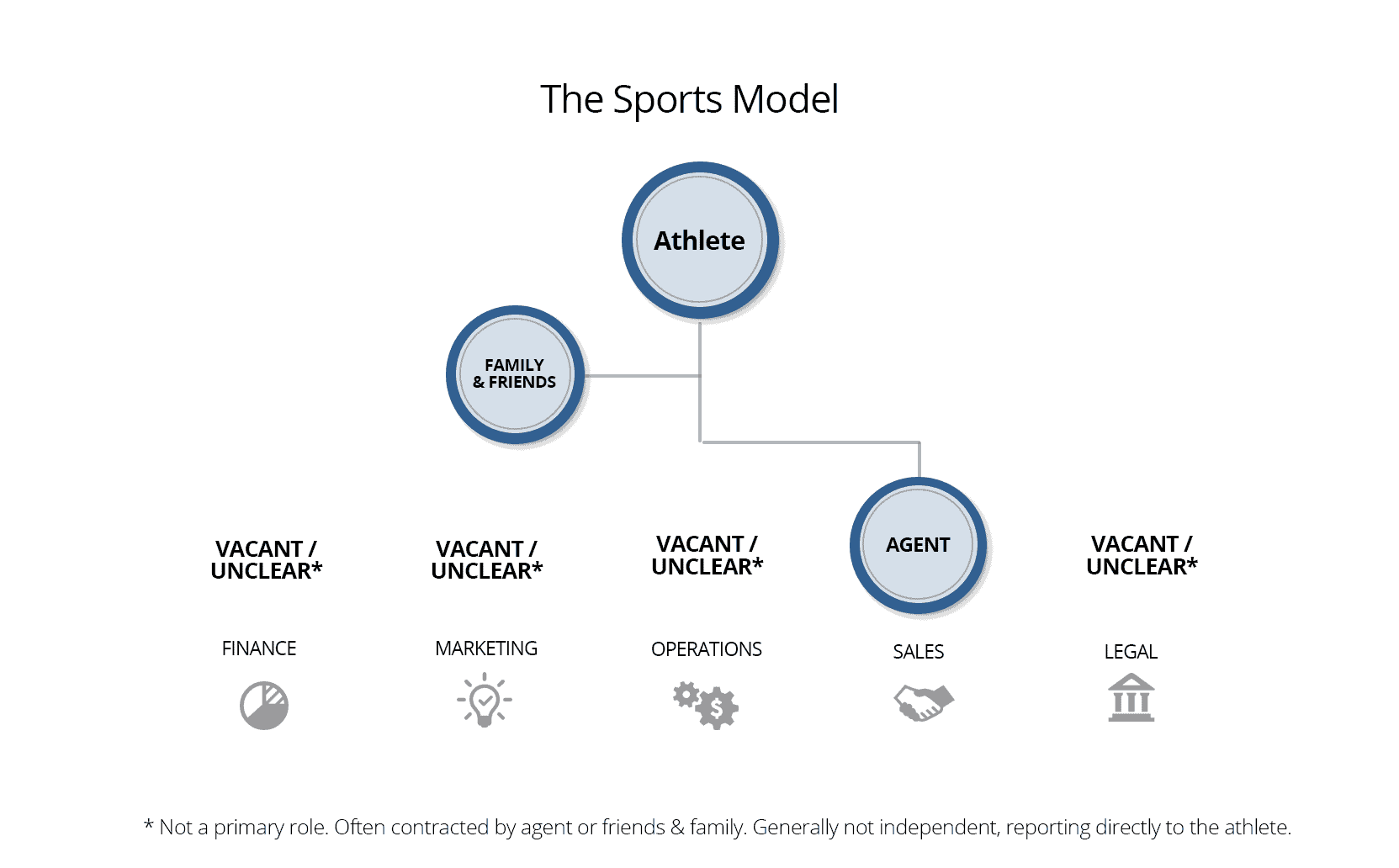

The Sports Model

Over the past several decades, the financial lives of professional athletes have grown increasingly complex. Salaries have grown significantly, as have endorsements, appearances, other sources of income, and the demands on each player’s time and attention. However, the average player’s support system has failed to evolve at the same pace. The model below shows how the support team of a typical athlete compares to Corporate Model.

While professional athletes understand the importance of experience, expertise, and teamwork, they often lack a clearly defined model for building their own teams off-the-field. The majority of highly publicized financial failures in professional sports stem from athletes who were either (a) missing key role players on their teams, or (b) trusting important roles to inexperienced or sometimes even unscrupulous acquaintances.

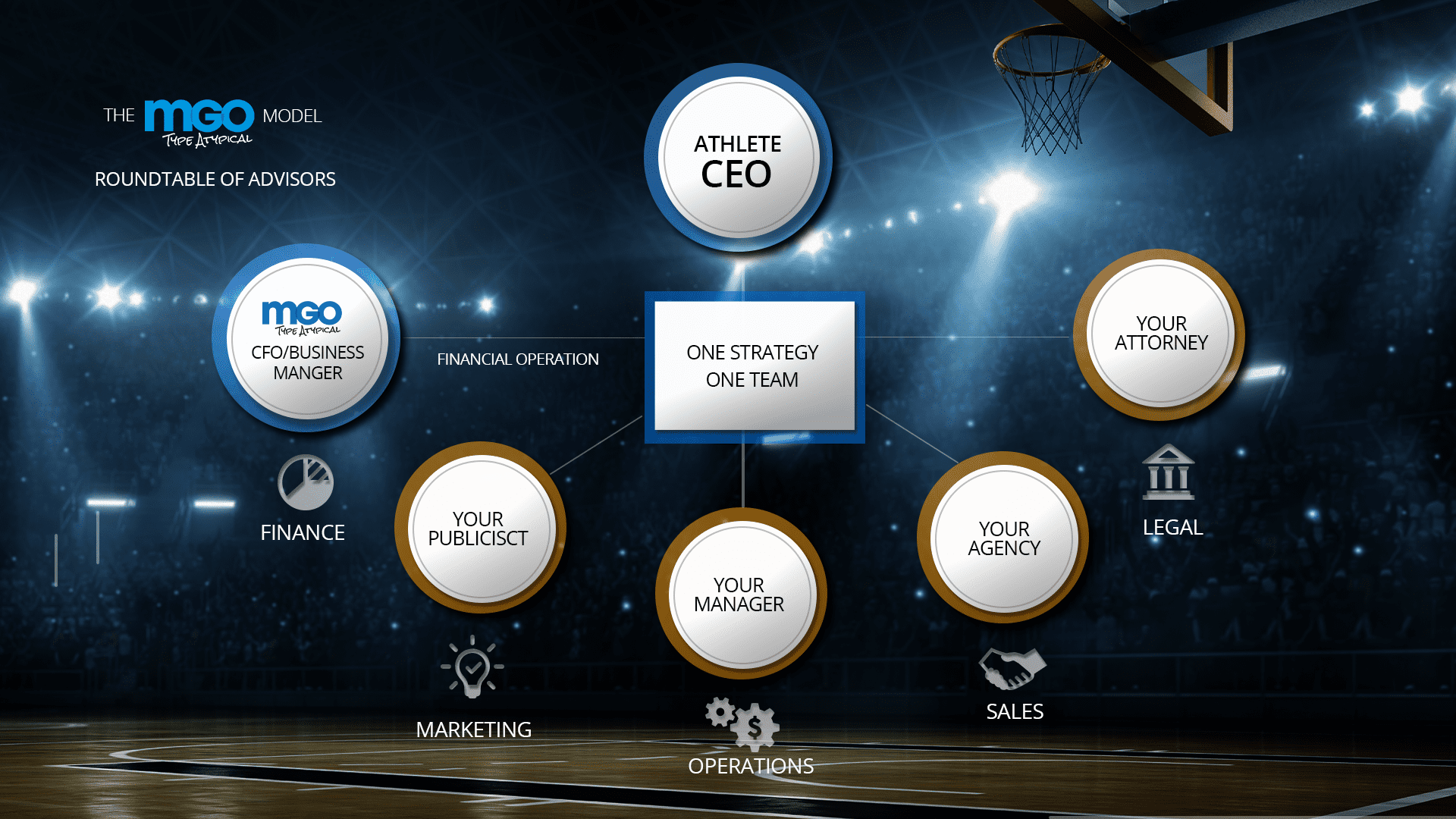

The MGO Model

At MGO, we’ve been fortunate to work with some of the most successful executives and entrepreneurs in the world – as well as many of the biggest names in Sports & Entertainment. As a result, we’ve come to know the traits and practices that drive success across industries.

The MGO Sports Model was developed to be a blueprint for Athlete/CEOs as they build their own teams. It identifies and defines the roles that are critical to success, while aligning the work of leading advisors under a common vision. While each role is important, we encourage clients to begin with the person who will serve as the quarterback of their daily financial lives; the CFO Business Manager.

The Financial Quarterback

In a recent article, Variety described the role of Business Managers in the Sports & Entertainment industry, stating, “Business Managers are the personal CFOs for celebrities, executives and athletes… They put their fortunes and their day-to-day lives in the hands of these trusted advisors.”

While each member of the Athlete/CEO’s team plays a vital role, the CFO/Business Manager is the person with the most tangible daily impact on a client’s financial life. He or she is the quarterback of the financial operation – responsible for hands-on, real-time execution of the financial plan. This includes establishing budgets paying the bills and monitoring the expenditures of anyone with access to the client’s accounts or credit cards.

Additionally, Business Managers serve as on-call financial advisors, working closely with clients on many of their most important financial decisions including family estates and trusts, tax planning, major purchases, potential investments, and charitable contributions.

High profile athletes are sometimes targets of investment scams and unwarranted requests for financial support. When these propositions come from friends, family and former acquaintances, a Business Manager can provide an important gatekeeper function. By establishing a recognized first point-of-contact for all financial requests, the majority of questionable requests can be filtered out before reaching the athlete.

Finally, the CFO/Business Manager works closely with the entire roundtable of advisors, ensuring that everyone is aligned and working together to implement a common strategy.

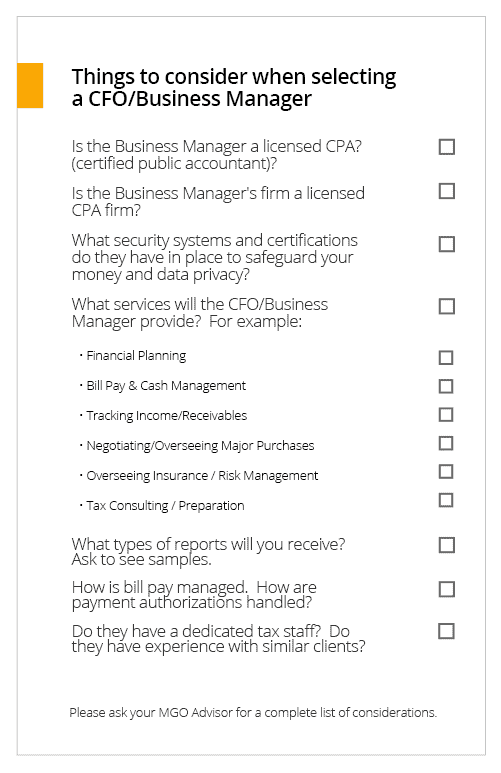

Selecting a CFO/Business Manager

Despite the critical role played by Business Managers in the financial lives of their clients, most states require no credentials to use the title Business Manager. As a result, there are people with little or no accounting experience using that title today.

Many of the highly publicized financial challenges in Sports & Entertainment have stemmed from unqualified and/or unethical advisors serving in the role of Business Manager for high profile clients. That’s why we suggest doing your own due diligence before hiring the quarterback of your financial team.

Questions? Let’s Talk.

]]>Everything changes, except when it doesn’t

Time and time again we’ve seen reactions to various accounting scandals, after which new policies, procedures, and legislation are created and implemented. An example of this is the Sarbanes-Oxley Act (SOX) of 2002, which was a direct result of the accounting scandals at Enron, WorldCom, Global Crossing, Tyco, and Arthur Andersen.

SOX was established to provide additional auditing and financial regulations for publicly held companies to address the failures in corporate governance. Primarily it sets forth a requirement that the governing board, through the use of an audit committee, fulfill its corporate governance and oversight responsibilities for financial reporting by implementing a system that includes internal controls, risk management, and internal and external audit functions.

Governments experience challenges and oversight responsibility similar to those encountered by corporate America. Governance risks can be mitigated by applying the provisions of SOX to the public sector.

Some states and local governments have adopted similar requirements to SOX but, unfortunately, in many cases only after cataclysmic events have already taken place. In California, we only need to look back at the bankruptcy of Orange County and the securities fraud investigation surrounding the City of San Diego as examples of audit committees that were established in response to a breakdown in governance.

Taking your audit committee on the right mission

Governments typically establish audit committees for a number of reasons, which include addressing the risk of fraud, improving audit capabilities, strengthening internal controls, and using it as a tool that increases accountability and transparency. As a result, the mission of the audit committee often includes responsibility for:

- Oversight of the external audit.

- Oversight of the internal audit function.

- Oversight for internal controls and risk management.

Chart(er) your course

Most successful audit committees are created by a formal mandate by the governing board and, in some cases, a voter-approved charter. Mandates establish the mission of the committee and define the responsibilities and activities that the audit committee is expected to accomplish. A wide variety of items can be included in the mandate.

Creating the governing board’s resolution is the first step on the road to your audit committee’s success.

Follow the leader(ship)

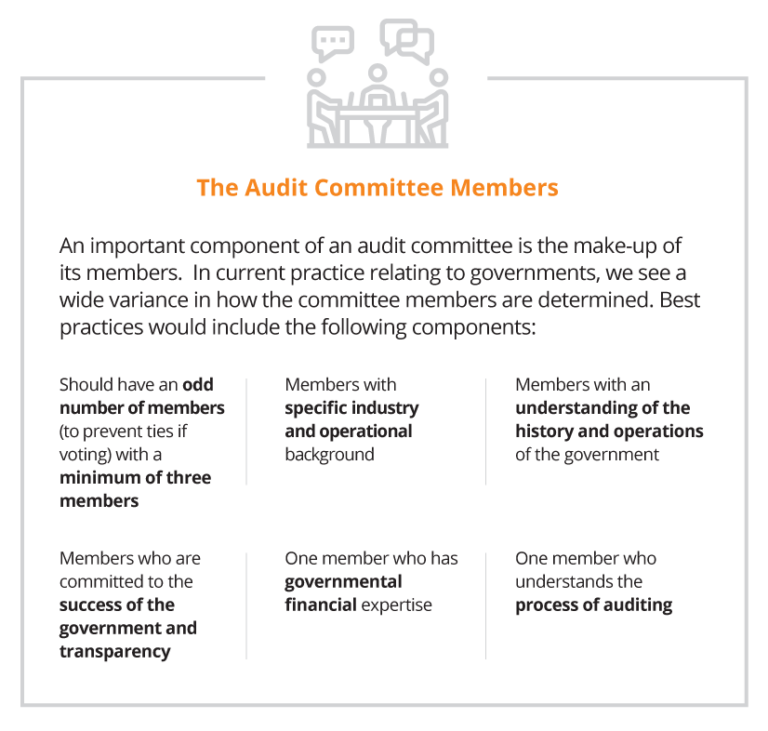

In practice we see a combination of these attributes, ranging from the full board acting as the audit committee, committees with one or more independent outsiders appointed by the board, and/or members from management and combinations of all of the above. While there are advantages and disadvantages for all of these approaches, each government needs to evaluate how to work within their own governance structure to best arrive at the most workable solution.

Strike the right balance between cost and risk

The overriding responsibility of the audit committee is to perform its oversight responsibilities related to the significant risks associated with the financial reporting and operational results of the government. This is followed closely by the need to work with management, internal auditors and the external auditors in identifying and implementing the appropriate internal controls that will reduce those risks to an acceptable level. While the cost of establishing and enforcing a level of zero risk tolerance is cost prohibitive, the audit committee should be looking for the proper balance of cost and a reduced level of risk.

Engage your audit committee with regular meetings

Depending on the complexity and activity levels of the government, the audit committee should meet at least three times a year. In larger governments, with robust systems and reporting, it’s a good practice to call for monthly meetings with the ability to add special purpose meetings as needed. These meetings should address the following:

External Auditors

- Confirmation of the annual financial statement and compliance audit, including scope and timing.

- Ad hoc reporting on issues where potential fraud or abuse have been identified.

- Receipt and review of the final financial statements and auditor’s reports

- Opinion on the financial statements and compliance audit;

- Internal controls over financial reporting and grants; and

- Violations of laws and regulations.

Internal Auditors

- Review of updated risk assessments over identified areas of risk.

- Review of annual audit plan, including status of the prior year’s efforts.

- Status reports of ongoing and completed audits.

- Reporting of the status of corrective action plans, including conditions noted, management’s response, steps taken to correct the conditions, expected time-line for full implementation of the corrective action and planned timing to verify the corrective action plan has been implemented.

Establish resources that are at the ready

Audit committees should be given the resources and authority to acquire additional expertise as and when required. These resources may include, but are not limited to, technical experts in accounting, auditing, operations, debt offerings, securities lending, cybersecurity, and legal services.

Taking extra steps now will save time later

While no system can guarantee breakdowns will not occur, a properly established audit committee will demonstrate for both elected officials and executive management that on behalf of their constituents they have taken the proper steps to reduce these risks to an acceptable tolerance level. History has shown over and over again that breakdowns in governance lead to fraud, waste and abuse. Don’t be deluded into thinking that it will never happen to your organization. Make sure it doesn’t happen on your watch.

]]>Big earnings do not equal a lifetime of financial comfort

High tier individuals in entertainment can earn more money in a year than the average person makes in a lifetime. Yet, in a Forbes study of 165 talent agents and managers, more than nine out of ten interviewed claim a large percentage of their top tier clients have little or no understanding of wealth or how to handle that wealth for themselves.

As a result, a number of financial perils consistently trap, and occasionally ruin, a number of high-earning individuals. The media and the general public only care about the splashy, flashy tawdry spectacle of a former star down on their luck. That attention only addresses the symptoms of a disease, but never gets to the core cause that would enable a person to find a cure.

The dangers of lavish spending

Many talented individuals make the mistake of buying into media depictions of how people with status in the entertainment industry “should” live and have little or no concept of how to keep themselves financially grounded. Often there is a perception that one should not only live their lives as if they are successful, but there is pressure to show that life to the world at large, most recently through the lens of social media.

Michael Jackson is just one of many celebrities who faced bankruptcy and financial ruin late in his career. The performer had zero self-control when it came to lavish spending. His Neverland Ranch and collection of oddities are a legendary lesson in the danger of excess and paved the road to his financial ruin.

Another behavior pattern that has led to lavish spending is a general negativity attached to money, referred to as “demonized wealth.” In this case, people from a lower income bracket are suddenly thrust into a position of high wealth, and feel that being wealthy is bad, dirty, or somehow embarrassing. This could be due to how they were raised, or gained from observing the behaviors of other wealthy individuals. Demonizing one’s wealth can lead to talent spending money as soon as they earn it, in an attempt to get rid of it, instead of letting it grow.

The risks of poor investments

Many celebrities try to make smart money choices by investing in real estate, emerging companies or other investment vehicles. For every stunning success, like 50 Cent’s famous investment in Vitamin Water, there are countless stories of failed investments. While risk is part of any investment strategy, far too many celebrities over-extend themselves in pursuit of greater wealth.

Kim Basinger and Burt Reynolds, A-List movie stars at the height of their fame, ran into financial distress due to poor investments. In Basinger’s case, the actress invested in a town outside Atlanta, Georgia, intending to turn it into a tourist destination. Just five years later, on the brink of financial ruin, Basinger and the other investors sold the property at a significant loss. For Reynolds the damage of a series of costly divorces was exacerbated by a major investment in a failed restaurant chain.

In both cases, the celebrities where trying to be proactive about securing and growing their personal wealth. But poor advice and over-extending their finances led them to ruin.

Lack of experienced financial guidance

New wealth in Hollywood comes with a wide variety of financial pitfalls and traps. Some celebrities do plan ahead and seek out financial advice early in their careers, but it can often fall severely short of the depth and breadth of options that are available to them. While many are wise enough to work with a “financial advisor” all too often that source of advice is not qualified for the role, or is downright criminally-minded.

R&B singer Toni Braxton placed her financial trust in her manager and his record label only to ultimately lose everything. It is a common story, where a celebrity places financial trust in someone who is either close to them (a friend or relative) or who is a scam artist disguised as a financial advisor. Those advisors then provide poor advice that seemingly enriches everyone else at the expense of the celebrities themselves.

How can talent avoid the financial pitfalls?

We’ll be discussing this in depth in the next installment of this series of articles, but the best thing high-earning talent can do is to find themselves a brilliant financial team to work with and for them. A top tier individual in entertainment should look at the management of their wealth the same way a mid-sized company would. The person earing the income is the CEO of their own business with their name as the brand. They then need a CFO and a team of experts that are the best in their specific fields of wealth management, diversified investing, and financial planning. Proper financial planning with a team can give someone a healthy, prosperous, and well-rounded financial lifestyle; while still enabling them to plan for the future and the security that comes with smart investment moves.

]]>The financial perils celebrities face in Hollywood

A professional athlete or a top tier individual in entertainment should look at their expanded wealth and the management of that wealth the same way a mid-sized company would. The person earning the income is the CEO of the business and their name is the brand. They need a CFO to manage finances who is supported by a team of experts who are the best in their fields of wealth management, diversified investing, and financial planning. This team then enables the talent to get the best use out of their wealth while still making provisions for a comfortable future.

A good partnership between a high earning professional and a financial team can yield endless results and allow earners to live comfortably now and long into the future when considering retirement. Trust is the key to a successful working relationship between a high-income client and their financial team. With that trust established; the future of an individual and their family will be assured with strategy, planning, and more than just a bit of market savvy.

The first step in working with a professional financial team is to take ownership of financial awareness and education. It’s important that the earner takes time whether over the phone, remotely through video conference, or when possible in person; to sit and talk to their financial professionals. This will help them understand how and why their money is being managed the way it is.

A financial team needs to be allowed to act as guardians of wealth

High-earning talent must allow their financial team to act as guardians and keepers of their money. In the worlds of sports and entertainment celebrity, very few things are ever denied top-earning talent, and quite often they are not acquainted with the word “no.”

This is where financial teams step in to not only shield talent from financial predators and bad investments, but to also protect the earner’s money from themselves by helping curb extravagant spending and off-the-wall purchases. A good financial professional team is the best line of defense against money disappearing with no return.

Establish current and future goals for the life you want

A series of goals must be set by the earner and their financial professionals to properly plan for the future. Where do you want to be when you retire? What kind of life do you want to have? With the money you have coming in, what sort of plans can you make for yourself and your family? It’s important that individuals set realistic goals that are guided by their financial team, and that they maintain solid credit through their more lucrative years so they have an excellent history to build from.

Work to establish a series of sound and profitable investments

Talent can work with their financial team to establish investments that will earn returns and dividends that they can draw upon once they are no longer working. Municipal Bonds and ETFs in efficient markets are examples of smart investments. There are a multitude of options available, and if your financial team is savvy; they can advise you in the world of alternative investments like casinos, restaurants, hotels, and newer

markets like cannabis.

Get the right insurance for your career and risk profile

The financial team must work to ensure that talent has adequate insurance. Athletes take risks with their bodies all the time, so it is important that a player maintains the correct type of insurance that will cover them if they are injured and are unable to return to playing for a season. Or in a worst case scenario, they are forced into early retirement by an injury. The same can is true for actors, directors, and professionals in the world of entertainment. On-set accidents do happen, and if a person is unable to work in their chosen field; their earnings drop to next to nothing.

There is an energy and synergy to money

There is a synergy and energy to the exchange of money. Money is like an electrical current and a flow must be maintained at all times for wealth to increase in size. There needs to be a give and receive in place when balancing an individuals’ investments and wealth, and there is always the value of giving vs. receiving to consider. This journey to finding a balance with a financial team and a true vision of what a person wants to achieve with their wealth and their life is a much broader topic; which we’ll be discussing soon enough. So, just keep your eyes open for further editorials in this ongoing series!

]]>