1. The corporate tax rate was permanently reduced from 35 percent to 21 percent.

The top corporate tax rate has been permanently reduced from 35 percent to a flat rate of 21 percent, beginning in 2018. Unlike all other provisions in the new law, including tax breaks for individuals, the new corporate tax rate provision does not expire.

2. There’s a tax break for owners of pass-through entities.

The new law provides owners of pass-through businesses — which include individuals, estates, and trusts — with a deduction of up to 20 percent of their domestic qualified business income, whether it is attributable to income earned through an S corporation, partnership, sole proprietorship, or disregarded entity. Without the new deduction, taxpayers would pay 2018 taxes on their share of qualified earnings at rates up to 37 percent. With the new 20 percent deduction, the tax rate on such income could be as low as 29.6 percent. It should again be noted that certain service industries are excluded from the preferential rate, unless taxable income is below $207,500 (for single filers) and $415,000 (for joint filers), under which the benefit of the deduction is phased out.

3. There might be huge tax benefits to changing your company’s current choice of entity.

Taxpayers should consider evaluating the choice of entity used to operate their businesses. The 21 percent reduced corporate tax rate may increase the popularity of corporations. However, factors such as the new 20 percent deduction for pass-through income, expected use of after-tax cash earnings, and potential exit values will significantly complicate these analyses. The potential after-tax cash benefits ultimately realized by owners could make choice-of-entity determinations one of the most important decisions taxpayers will now make.

4. There have been significant changes to the international tax system.

In connection with these changes, some U.S. shareholders who own stock in certain foreign corporations will have to pay a one-time “transition tax” on their share of accumulated overseas earnings. Other changes include a “participation exemption,” which is a 100 percent dividend-received deduction that permits certain domestic C corporations to receive dividends from their foreign subsidiaries without being taxed on such dividends when certain conditions are satisfied. There is also a new requirement that certain U.S. shareholders of controlled foreign corporations (CFCs) include in income their share of the “global intangible low-taxed income” of such CFCs. Finally, there are new measures to deter base erosion and promote U.S. production.

5. The corporate AMT and DPAD are dead, but Research Tax Credits live on.

The law repeals the Section 199 Domestic Production Activities Deduction (DPAD) and the corporate Alternative Minimum Tax (AMT) for tax years beginning after 2017. The Research Tax Credit was retained and is now more valuable given the reduction of the corporate tax rate from 35 percent to 21 percent.

6. They’ve scrapped NOL carrybacks and limited the use of carryforwards.

Previously, businesses were able to offset current taxable income by claiming net operating losses (NOLs), generally eligible for a two-year carryback and 20-year carryforward. Now NOLs for tax years ending after 2017 cannot be carried back, but can be indefinitely carried forward. In addition, NOLs for tax years beginning in 2018 will be subject to an 80 percent limitation. Companies will have to track their NOLs in different buckets and consider cost-recovery strategy on depreciable assets in applying the 80 percent limitation.

7. Tax reform’s impact on accounting methods may change when revenue is recognized, but new provisions could also lead to temporary and permanent tax benefits.

Under the new law, accrual basis taxpayers must now recognize income no later than the taxable year in which such income is taken into account as revenue in an applicable financial statement.

However, new provisions also provide favorable methods of accounting that were not previously available. That, coupled with the reduction in tax rates, creates a favorable and unique environment for filing accounting method changes.

There are many method changes still available for the 2017 tax year. Taxpayers should evaluate current accounting methods to identify any actionable opportunities to accelerate deductions and defer income for the 2017 tax year, which could result in significant tax savings.

8. There are new rules for bonus depreciation and full expensing on new and used property.

The new tax law allows a 100 percent first-year deduction — up from 50 percent — for the adjusted basis of qualifying assets placed in service after Sept. 27, 2017, and before Jan. 1, 2023, with a gradual phase down in subsequent years before sunsetting after 2026. The definition of qualifying property was also expanded to include used property purchased in an arm’s-length transaction. Businesses should pay close attention to any qualifying asset acquisitions made during the fourth quarter of 2017, as the full expensing can be taken on the 2017 return if the property was acquired and placed in service after Sept. 27, 2017.

Additionally, under new tax law, taxpayers may now deduct up to $1 million under Section 179 for properties placed in service beginning in 2018 — double the previous allowable amount. The phase-out threshold is increased to $2.5 million and will be indexed for inflation in future years and the types of qualifying property has been expanded.

9. The availability of the cash method of accounting expanded for small businesses.

Beginning in 2018, the average annual gross receipts threshold for businesses to use the cash method increases from $5 million to $25 million. Additionally, small businesses who meet the $25 million gross receipts threshold are not required to account for inventories and are exempt from the uniform capitalization rules. The $25 million is indexed for inflation for tax years beginning after 2018.

10. Now is the time to assess total rewards strategies.

Tax reform significantly impacts various components of an employer’s total compensation program — namely the expansion of the $1 million deduction cap on pay to covered employees; disallowed deductions for transportation fringe benefits provided to employees; income inclusion for employer-paid moving expenses; further deduction limitations on certain meal and entertainment expenses; and a two-year tax credit for employer-paid family and medical leave programs. As the IRS releases guidance, employers must immediately modify their payroll systems to reflect tax reform changes impacting individual taxpayers.

For more information about the impact of tax reform on the Government Contracting industry, please reach out to us.

]]>This Tax Alert provides an overview of some of the most significant modifications to the U.S. international tax provisions affecting businesses and individuals. We urge clients to evaluate the impact of tax reform and discuss relevant changes with their tax advisors since many of the new provisions may bring about unintended tax consequences with respect to properly implemented structures under the previous U.S. international tax regime. Overall, the changes expand the base of cross-border income to which current U.S. taxation applies.

Additional tax alerts for Individuals | Business

Details of international provisions

Introduction of Participation Exemption System for foreign income

The Act introduces a dividend exemption system that applies to distributions made after December 31, 2017, which generally provides for a 100% dividend received deduction (“DRD”) for the foreign-sourced portion of dividends received by a domestic C corporation from a specified 10%-owned foreign corporation (other than a Passive Foreign Investment Company – “PFIC”) of which it is a U.S. shareholder, provided certain conditions are satisfied. The DRD is available only to C corporations that are not regulated investment companies (“RICs”) or real estate investment trusts (“REITs”).

Note that dividends received from PFICs do not qualify for the DRD and domestic C corporations may not claim foreign tax credits or a deduction for foreign taxes paid or accrued with respect to any dividend allowed the DRD.

To the extent earnings of foreign corporations are neither subpart F income nor subject to the minimum tax rule discussed below, the new participation exemption system moves the U.S. away from a worldwide taxation system towards a territorial tax system for earnings of foreign corporations.

Sales or transfers involving specified 10%-owned foreign corporations

Certain deemed dividends under Code section 1248 – resulting from the sale or exchange of stock of a specified 10%-owned foreign corporation held for over one year – qualify for the 100% DRD under the new law.

The provision also allows a U.S. shareholder to claim a 100% DRD on deemed dividends under section 964(e) resulting from the gain on the sale of foreign stock by a controlled foreign corporation (“CFC”).

Two new loss limitation rules are included in the provision, which are applicable to transfers and distributions made after December 31, 2017:

- A domestic corporation that is allowed a DRD is required to reduce its basis in the stock of the foreign corporation by an amount equal to the DRD, solely for purposes of determining the domestic corporation’s loss on the sale of stock of the foreign corporation.

- A domestic corporation is required to recapture certain foreign branch losses if it transfers substantially all of the assets of a foreign branch to a 10%-owned foreign corporation of which it is a United States shareholder after the transfer. The active trade or business exception of section 367(a)(3) is repealed for transfers made after December 31, 2017, which disfavors the use of foreign branches.

New mandatory repatriation

As a transition to the new participation exemption regime, a mandatory repatriation provision is included targeting previously untaxed earnings and increasing subpart F income by the shareholder’s pro rata share of each specified foreign corporation’s net untaxed post-’86 historical E&P, determined as of November 2 or December 31, 2017 (a measuring date). However, this mandatory inclusion is reduced (but not below zero) by an allocable portion of the taxpayer’s share of foreign E&P deficit of each specified foreign corporation and the taxpayer’s share of its affiliated group’s aggregate unused E&P deficit. Earnings attributable to the shareholder’s aggregate foreign cash position or liquid assets are subject to tax at a 15.5% rate, while earnings attributable to illiquid assets are subject to tax at an 8% rate.

The tax liability is payable over a period of up to eight years, at the election of the U.S. shareholder.

A special rule applies to S corporations under the mandatory repatriation provisions. S corporation shareholders may elect to continue to defer taxation of such foreign income until the S corporation changes its status, sells a substantial amount of its assets, ceases to conduct business, or the electing shareholder transfers their S corporation stock.

Non-corporate U.S. shareholders are exposed to the new mandatory repatriation rule if the specified foreign corporation is a CFC or any foreign corporation with at least one domestic corporate U.S. shareholder, even though the 100% dividend received deduction from foreign subsidiaries only applies to corporate U.S. shareholders under the Act.

Foreign tax credits and sourcing of income modifications

Foreign tax credits are allowed under the new law only with respect to foreign income taxes associated with the taxable portion of the U.S. shareholder’s net mandatory inclusion. Foreign tax credits are disallowed with respect to foreign income taxes attributable to the participation deduction. Taxpayers may not elect to take a deduction for foreign taxes that are disallowed as foreign tax credits.

The U.S. shareholder’s section 78 gross-up should also reflect the portion of foreign taxes attributable to the U.S. shareholder’s net mandatory inclusion.

The deemed paid foreign tax credit provisions under Code Section 902 are repealed while the deemed paid foreign tax credit provisions for subpart F inclusions under Code Section 960 are retained but modified, providing a credit on a current year basis. Foreign tax credits will be counted on an annual basis and will no longer be pooled.

Foreign taxes attributable to distributions of previously taxed income (“PTI”) are also regulated under the Act

The Act also revises the sourcing rules for income from inventory sales. Income from inventory sales is now sourced entirely based on the place of production and not allocated 50/50 to the place of production and the place of sale (based on title passage).

A separate foreign tax credit limitation basket is created under the new law for foreign branch income.

The Act repeals the fair market value method of interest expense apportionment. Taxpayers are now required to allocate and apportion interest expense of members of an affiliated group using the adjusted basis of assets.

New provisions regarding foreign passive and intangible income

The Act has new provisions that adopt a minimum tax on “global intangible low-taxed income” (“GILTI”) and a new special deduction for certain “foreign-derived intangible income” (“FDII”), subject to certain exceptions.

Regardless of whether distributions are actually made by a CFC during the tax year and similarly to the manner in which subpart F income inclusions operate, a U.S. shareholder of a CFC is now required to include in income its pro rata share of GILTI allocated to the CFC for the CFC’s tax year that ends with or within its own tax year.

GILTI provisions target a portion of the CFCs’ active (non-Subpart F) income and tax it at an effective tax rate of 10.5% prior to 2026 — generally speaking, the targeted portion is equal to the net income over a routine or ordinary return, defined as the excess of an implied 10% rate of return on the adjusted basis of the CFC’s tangible depreciable property used in generating the active income.

In conjunction with the new minimum GILTI tax regime, excess returns earned directly by a U.S. corporation from foreign sales (including licenses and leases) or services defined as FDII are now also subject to a 13.125% effective tax rate (increased to 16.406% starting in 2026). FDII is the amount of a U.S. corporation’s “deemed intangible income” that is attributable to sales of property (including licenses and leases) to foreign persons for use outside the U.S. or the performance of services for foreign persons or with respect to property outside the U.S.

Corporate shareholders are allowed a deduction equal to maximum 50% of GILTI (reduced to 37.5% starting in 2026) plus any corresponding Code section 78 gross-up plus maximum 37.5% of taxpayer’s FDII (reduced to 21.875% starting in 2026) – combined, these three components comprise the GILTI deduction. Not that the total GILTI deduction cannot exceed a corporation’s taxable income. S corporations or domestic corporations that are RICs or REITs are not allowed to claim this deduction. Transfers to foreign related persons generally do not qualify for FDII benefits.

U.S. shareholders can make a Code Section 962 election with respect to GILTI inclusions, which subjects the shareholder to tax on the GILTI inclusion based on corporate rates, and allows the electing shareholder to claim foreign tax credits on the inclusion as if the shareholder were a domestic corporation.

Modification to subpart F rules

The inclusion based on the withdrawal of previously excluded subpart F income from qualified investment is repealed.

The provision that provides for the inclusion of foreign base company oil-related income is repealed; hence, previously excluded foreign shipping income of a foreign subsidiary is no longer subject to current U.S. taxation under the subpart F rules if there is a net decrease in qualified shipping investments.

Stock attribution rules for determining status of a foreign corporation as a CFC are modified, which makes it more likely for a foreign corporation to be treated as a CFC as a result of the stock of certain related foreign persons being attributed downward to a U.S. citizen. As a result, for example, stock owned by a foreign corporation would be treated as constructively owned by its wholly-owned domestic subsidiary for purposes of determining the U.S. shareholder status of the subsidiary and the CFC status of the foreign corporation.

The new law eliminates the requirement that a corporation be a CFC for 30 days before subpart F inclusions apply.

Prevention of base erosion

The Act includes additional anti-base erosion measures, including a Base Erosion Anti- Abuse Tax (“BEAT”) for certain payments paid or accrued in tax years beginning after December 31, 2017. In general, the BEAT imposes a minimum tax on certain deductible payments made to foreign affiliates, including royalties and management fees, but excluding cost of goods sold.

Income shifting through intangible property transfers is further limited. This includes treating goodwill and going concern value and workforce in place as section 936(h)(3)(B) intangibles and, requiring the use of the aggregate basis valuation method in the case of transfers of multiple intangible properties in one or more related transactions. This applies if it is determined that an aggregate basis achieves a more reliable result than an asset-by-asset approach.

Deductions for certain related party interest or royalty payments paid or accrued in certain hybrid transactions or with certain hybrid entities are now disallowed under certain circumstances. The Act provides that the Secretary of State shall issue regulations or other guidance as may be necessary or appropriate to carry out the purposes of the provision for branches (domestic or foreign) and domestic entities, even if such branches or entities do not meet the statutory definition of a hybrid entity.

New rules were incorporated to limit the deductibility of interest within a corporate group.

Surrogate foreign corporations are not eligible for the reduced rate on dividends under the Act.

MGO insights

The Tax Cuts and Jobs Act is the largest overhaul of the tax system in over three decades and will have a significant impact on U.S.-based multinational companies as well as inbound businesses. The bill fundamentally changes the landscape of U.S. international taxation. We recommend that companies, individuals, and flow through entities engaged in cross border business discuss their specific situation with MGO’s experienced international tax professionals and consultants – we are here to help you navigate the changes of this comprehensive tax reform.

]]>An unexpected consequence of economic downturn that started in 2008 was an increase of fraud across a wide variety of industries. As companies turned to layoffs as a way to lower overhead, many organizations unintentionally exposed themselves to potential fraud by laying-off employees who oversaw essential internal controls or served in a system of checks and balances that would have prevented fraud. According to the Association of Certified Fraud Examiners (“ACFE”), the combination of omnipresent economic pressure, and a lack of controls, resulted in historic levels of fraud following the recession. As a result, companies as large as Fortune 500 organizations, and as small as local businesses, have been forced to course correct and get a handle on fraud.

The first step toward preventing fraud is gaining a holistic view of the circumstances under which it occurs. The ACFE provided the following touchpoints to establish a baseline understanding of how fraud occurs:

- Organizations lose approximately 5% of revenue due to fraud

- Average fraud duration is 18 months

- 40% of fraud cases were detected via Tip /Hotline

- 75% of fraud cases were committed by employees working in seen departments:

– Accounting & Finance

– Purchasing

– Executive /Upper management

– Operations

– Customer Service

– Sales

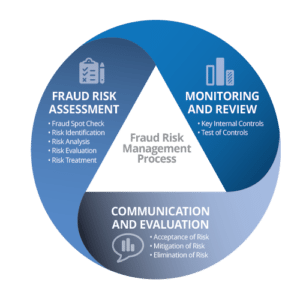

How do we fight fraud?

Fundamentally, business fraud prevention is a three-step process that combines reviews of operations and internal controls, the acceptance of certain conditions, and the systematic elimination of those risks.

Assessing fraud risk

The first step to preventing fraud is identifying opportunities for fraud and assessing the risk. Fraud can appear in unexpected ways. Therefore, a spot check of departments and operations is a necessary step. While following guidelines of where fraud is likely to occur (like those provided by the ACFE above) is a good way to prioritize activities, it should not limit the inquiry. The fraud assessment should be performed by employees independent of the operation or department, ideally by your in-house fraud investigation team, or internal audit department. Furthermore, collaborating with an outside subject matter expert, or Certified Fraud Examiner (“CFE”), can augment your team, providing a critical perspective for identifying fraud and developing internal procedures to eliminate fraud in the future.

Monitoring and review

An evergreen component of fraud prevention is the monitoring and review of internal controls. A sound internal control structure is the first line of defense against fraud (and a vast array of other operational hazards). Performing regularly scheduled testing, and updating controls based on the results of the testing, will create an operational structure actively working to limit opportunities for fraud.

Communication and evaluation

After the Assessment, and Monitoring stages, your organization can make final decisions based on the findings. The review function (whether performed by a CFE, internal auditor, or consultant) will present a final report on each stage of the operational review to the Internal Audit Committee, Board, or other decision-making body. The report should identify all gaps, assign risk levels, and propose solutions.

With this holistic view of operations, risks, and costs associated with fraud prevention in hand, the decision-making body can make informed decisions on the most efficient ways to shore up defenses and proactively prevent fraud.

Tips on developing internal controls

Internal Controls fall into two general categories: preventative controls and detective controls. The former are systems put in place to limit the possibility of fraud, whereas the latter can be enacted to identify and root out active, or historical, fraudulent activities. Each type of internal control requires specific knowledge of industry standards, business operations, and the culture of the organization.

Preventative controls can be the most effective, yet unheralded champions of fraud prevention, as they prevent fraud before it occurs. These can be difficult to “sell” to a governing body, as their upfront cost may not be easily balanced by definable losses saved.

Factors to consider when designing preventative controls:

- Business strategy and culture

- Utilization of IT systems

- Length of existing processes

- Consistent process outcomes

- Ability to circumvent internal controls

- Employee empowerment

Detective controls are an opportunity to identify and root out on-going or historical fraud. These controls tend to follow “after the fact” and are an attempt to “right a wrong,” when there has already been potentially significant loss. While it is always preferable to prevent fraud before the act, detective controls can produce valuable insights that can be used to prevent future fraudulent actions.

Factors to consider when designing detective controls:

- Average or expected outcomes

- Types of trends and patterns

- Unusual activity or outliers

- Review information from different directions

- Changes to defined time periods reviewed

- Utilization of IT systems

The limits of internal controls

While robust internal controls are the most effective solution to fighting fraud, there simply is no “fool-proof” system. A company must remain vigilant, responsive and adaptable to changing factors outside the limits of internal controls – factors like employee turnover and external economic pressures.

Understanding the limits of internal control structures is an important step toward developing a system that accounts for as many variable as possible. Common limits to internal controls include:

- Human judgment

- Management’s ability to override controls

- Maintaining sufficient resources to achieve adequate segregation of duties

- Breakdown of controls

- High management turnover

- Lack of employee training

- Poorly documented policies & procedures

- Internal audit plan not based on risk of operations

There is no “solution,” only steps to mitigate or uncover

Fraud is a major issue with which every organization – including public companies, growing small businesses, government institutions, or tribal entities – must actively contend. The economic downturn and the layoffs, downsizing and other negative economic outcomes that followed have created an environment where fraud is rampant, with no cessation in sight. Every organization must take a hard look at its operations, culture and internal controls to assess opportunities for fraudulent activity, and take the steps necessary to remove or limit those opportunities.

Stay tuned for future articles in this series where we will take a close look at what organizations can do to limit fraud.

]]>- Insufficient outreach to vendors

- Lowering of bonding requirements

- Burdensome administrative requirements

- Insufficient segregation of procurement approval and receiving duties

- Lack of cross-department evaluation of vendor proposals

- Inconsistent management and designated authority levels

- Organizations are unaware of procurement process times – from start of requisition until vendors are paid

- Procurement activities are not aligned with overall organizational activities

- Too many sign offs/approvals

If any of these issues sound familiar, or your organization has not reviewed its procurement function in a while, you run the risk that your procurement strategies are inconsistent with organizational needs, which can result in paying higher prices for the goods and services required to run your agency, insufficient number of competitive bids, or worse, violating your grant or service agreements.

IntelliBridge Partners has the expertise to improve the procure to pay cycle through business process reviews, risk assessments, and performance audits. If you would like help with your procurement department, please contact Greg Matayoshi at gmatayoshi@intellibridgepartners.com.

]]>Big earnings do not equal a lifetime of financial comfort

High tier individuals in entertainment can earn more money in a year than the average person makes in a lifetime. Yet, in a Forbes study of 165 talent agents and managers, more than nine out of ten interviewed claim a large percentage of their top tier clients have little or no understanding of wealth or how to handle that wealth for themselves.

As a result, a number of financial perils consistently trap, and occasionally ruin, a number of high-earning individuals. The media and the general public only care about the splashy, flashy tawdry spectacle of a former star down on their luck. That attention only addresses the symptoms of a disease, but never gets to the core cause that would enable a person to find a cure.

The dangers of lavish spending

Many talented individuals make the mistake of buying into media depictions of how people with status in the entertainment industry “should” live and have little or no concept of how to keep themselves financially grounded. Often there is a perception that one should not only live their lives as if they are successful, but there is pressure to show that life to the world at large, most recently through the lens of social media.

Michael Jackson is just one of many celebrities who faced bankruptcy and financial ruin late in his career. The performer had zero self-control when it came to lavish spending. His Neverland Ranch and collection of oddities are a legendary lesson in the danger of excess and paved the road to his financial ruin.

Another behavior pattern that has led to lavish spending is a general negativity attached to money, referred to as “demonized wealth.” In this case, people from a lower income bracket are suddenly thrust into a position of high wealth, and feel that being wealthy is bad, dirty, or somehow embarrassing. This could be due to how they were raised, or gained from observing the behaviors of other wealthy individuals. Demonizing one’s wealth can lead to talent spending money as soon as they earn it, in an attempt to get rid of it, instead of letting it grow.

The risks of poor investments

Many celebrities try to make smart money choices by investing in real estate, emerging companies or other investment vehicles. For every stunning success, like 50 Cent’s famous investment in Vitamin Water, there are countless stories of failed investments. While risk is part of any investment strategy, far too many celebrities over-extend themselves in pursuit of greater wealth.

Kim Basinger and Burt Reynolds, A-List movie stars at the height of their fame, ran into financial distress due to poor investments. In Basinger’s case, the actress invested in a town outside Atlanta, Georgia, intending to turn it into a tourist destination. Just five years later, on the brink of financial ruin, Basinger and the other investors sold the property at a significant loss. For Reynolds the damage of a series of costly divorces was exacerbated by a major investment in a failed restaurant chain.

In both cases, the celebrities where trying to be proactive about securing and growing their personal wealth. But poor advice and over-extending their finances led them to ruin.

Lack of experienced financial guidance

New wealth in Hollywood comes with a wide variety of financial pitfalls and traps. Some celebrities do plan ahead and seek out financial advice early in their careers, but it can often fall severely short of the depth and breadth of options that are available to them. While many are wise enough to work with a “financial advisor” all too often that source of advice is not qualified for the role, or is downright criminally-minded.

R&B singer Toni Braxton placed her financial trust in her manager and his record label only to ultimately lose everything. It is a common story, where a celebrity places financial trust in someone who is either close to them (a friend or relative) or who is a scam artist disguised as a financial advisor. Those advisors then provide poor advice that seemingly enriches everyone else at the expense of the celebrities themselves.

How can talent avoid the financial pitfalls?

We’ll be discussing this in depth in the next installment of this series of articles, but the best thing high-earning talent can do is to find themselves a brilliant financial team to work with and for them. A top tier individual in entertainment should look at the management of their wealth the same way a mid-sized company would. The person earing the income is the CEO of their own business with their name as the brand. They then need a CFO and a team of experts that are the best in their specific fields of wealth management, diversified investing, and financial planning. Proper financial planning with a team can give someone a healthy, prosperous, and well-rounded financial lifestyle; while still enabling them to plan for the future and the security that comes with smart investment moves.

]]>Many cheered the passage of the 2018 Farm Bill, which descheduled industrial hemp and its derivatives (including CBD). But that was just the start of a much more complicated regulatory story that continues to have a major impact on entrepreneurs, investors, and advocates and patients who rely on CBD.

CBD and the 2018 Farm Bill

When President Trump signed the 2018 Farm Bill into law one of the key changes affecting the cannabis industry was the separation of “hemp” and “marijuana.” Before the Farm Bill, any incarnation of the cannabis plant and its byproducts were lumped into a single category and considered a Schedule 1 drug. Key language in Section 1103 of the Farm Bill defines hemp as:

“the plant Cannabis sativa L. and any part of that plant, including the seeds thereof and all derivatives, extracts, cannabinoids, isomers, acids, salts, and salts of isomers, whether growing or not with a delta-9 tetrahydrocannabinol concentration of not more than 0.3 percent on a dry weight basis.”

In short, the Farm Bill descheduled industrial hemp and its byproducts as long as it stayed under the threshold of less than 0.3 percent THC. CBD is derived from the cannabis plant, whether there are significant levels of THC or not. CBD industry advocates have interpreted the language “all derivatives, extracts, cannabinoids, isomers, acids, salts, and salts of isomers” as descheduling CBD when industrial hemp is the source. And they are “mostly” correct in this interpretation. Unfortunately, there are other federal agencies in play.

CBD and the FDA

United States Department of Agriculture (USDA) enacted the 2018 Farm Bill in their position overseeing laws related to the cultivation of industrial hemp. The United States Food and Drug Administration (FDA) oversees medicine and food additives. CBD has emerged as a “wonder drug” with a growing list of potential benefits and now appears as an additive in a wide range of consumer products. In addition, the FDA approved Epidiolex, the first CBD-derived drug, in 2018.

All of this has culminated in CBD being a priority of the FDA, so much so, that just a week after the Farm Bill was signed into law, the FDA issued a press release clarifying and asserting their regulatory control over all cannabis-derived compounds.

“We treat products containing cannabis or cannabis-derived compounds as we do any other FDA-regulated products — meaning they’re subject to the same authorities and requirements as FDA-regulated products containing any other substance. This is true regardless of the source of the substance, including whether the substance is derived from a plant that is classified as hemp under the Agriculture Improvement Act.”

Concurrent with the Farm Bill and the press release regarding CBD, the FDA also issued three Generally Regarded as Safe (GRAS) notices for hemp by-products: hulled hemp seeds, hemp protein powder, and hemp seed oil. Clearly demonstrating that (some) hemp products have been descheduled and cleared for use by the FDA.

The FDA’s policy is different toward CBD for two key reasons. Firstly, CBD products are largely marketed with a wide variety of therapeutic claims. In their press release the FDA notes:

“The FDA requires a cannabis product (hemp-derived or otherwise) that is marketed with a claim of therapeutic benefit, or with any other disease claim, to be approved by the FDA for its intended use before it may be introduced into interstate commerce.”

Secondly, the FDA’s approval of CBD-based drug Epidiolex, put CBD and THC into the category of “active ingredients in FDA-approved drugs.” Under the Federal Food, Drug, and Cosmetic Act (FD&C Act) it is “illegal to introduce drug ingredients like these into the food supply, or to market them as dietary supplements.”

In short, the FDA does not distinguish between CBD derived from hemp or “marijuana,” and until the agency approves CBD and establishes a regulatory framework, adding CBD to food and beverages is illegal.

Has the regulation of CBD slowed businesses?

While early CBD research has shown promise as a treatment for conditions like epilepsy and anxiety, as a consumer product it is unproven and has been largely unregulated until recently. In the absence of labeling standards and regulated dosage guidelines, consumers often have little understanding of what they are buying and its potential effects.

All of this uncertainty has earned greater regulatory attention for CBD. There have been reports of crackdowns on bakeries, restaurants and retailers selling CBD in California, New York, Maine and Ohio, just to name a few. This regulatory response has shocked and angered a number of hemp producers and CBD retailers who have invested millions into business ventures that they feel only supply the public with products that help manage health concerns.

Despite the confusing legality, the CBD industry appears to be moving full-steam ahead. In recent months, national retailers as diverse as Walgreens, DSW and Barney’s New York have announced plans (or have already begun) selling CBD products. Indicating the burgeoning CBD industry is well on the way to mainstream acceptance.

What is next for CBD?

In February, former FDA Commissioner Scott Pruitt testified before the House Appropriations Committee and said that the FDA is initiating a rule making procedure with the goal of creating “an appropriately efficient and predictable regulatory framework for regulating CBD products.” The FDA will launch the process with a public hearing on CBD scheduled for May 31, 2019.

Further complexity struck when Pruitt unexpectedly announced his resignation, which took effect in early April. Pruitt has been replaced by Dr. Ned Sharpless, the former director of the National Cancer Institute. To date, it is unknown whether Sharpless intends to take a progressive stance toward CBD.

While delays occur at the federal level, states are shifting into action. Maine recently passed an emergency law governing CBD. The bill aligns the definition of hemp in Maine’s laws with the definition used in the Farm Bill. Meaning, as long as CBD is derived from hemp sources it is to be considered a food product, rather than medicine, and is cleared for use in Maine.

Ultimately, until the FDA creates a regulatory framework for CBD, it will remain illegal to add it to any food or drink products.

Learn more about the FDA Public Hearing on CBD here

Provide a public comment for the FDA on CBD here

]]>The financial perils celebrities face in Hollywood

A professional athlete or a top tier individual in entertainment should look at their expanded wealth and the management of that wealth the same way a mid-sized company would. The person earning the income is the CEO of the business and their name is the brand. They need a CFO to manage finances who is supported by a team of experts who are the best in their fields of wealth management, diversified investing, and financial planning. This team then enables the talent to get the best use out of their wealth while still making provisions for a comfortable future.

A good partnership between a high earning professional and a financial team can yield endless results and allow earners to live comfortably now and long into the future when considering retirement. Trust is the key to a successful working relationship between a high-income client and their financial team. With that trust established; the future of an individual and their family will be assured with strategy, planning, and more than just a bit of market savvy.

The first step in working with a professional financial team is to take ownership of financial awareness and education. It’s important that the earner takes time whether over the phone, remotely through video conference, or when possible in person; to sit and talk to their financial professionals. This will help them understand how and why their money is being managed the way it is.

A financial team needs to be allowed to act as guardians of wealth

High-earning talent must allow their financial team to act as guardians and keepers of their money. In the worlds of sports and entertainment celebrity, very few things are ever denied top-earning talent, and quite often they are not acquainted with the word “no.”

This is where financial teams step in to not only shield talent from financial predators and bad investments, but to also protect the earner’s money from themselves by helping curb extravagant spending and off-the-wall purchases. A good financial professional team is the best line of defense against money disappearing with no return.

Establish current and future goals for the life you want

A series of goals must be set by the earner and their financial professionals to properly plan for the future. Where do you want to be when you retire? What kind of life do you want to have? With the money you have coming in, what sort of plans can you make for yourself and your family? It’s important that individuals set realistic goals that are guided by their financial team, and that they maintain solid credit through their more lucrative years so they have an excellent history to build from.

Work to establish a series of sound and profitable investments

Talent can work with their financial team to establish investments that will earn returns and dividends that they can draw upon once they are no longer working. Municipal Bonds and ETFs in efficient markets are examples of smart investments. There are a multitude of options available, and if your financial team is savvy; they can advise you in the world of alternative investments like casinos, restaurants, hotels, and newer

markets like cannabis.

Get the right insurance for your career and risk profile

The financial team must work to ensure that talent has adequate insurance. Athletes take risks with their bodies all the time, so it is important that a player maintains the correct type of insurance that will cover them if they are injured and are unable to return to playing for a season. Or in a worst case scenario, they are forced into early retirement by an injury. The same can is true for actors, directors, and professionals in the world of entertainment. On-set accidents do happen, and if a person is unable to work in their chosen field; their earnings drop to next to nothing.

There is an energy and synergy to money

There is a synergy and energy to the exchange of money. Money is like an electrical current and a flow must be maintained at all times for wealth to increase in size. There needs to be a give and receive in place when balancing an individuals’ investments and wealth, and there is always the value of giving vs. receiving to consider. This journey to finding a balance with a financial team and a true vision of what a person wants to achieve with their wealth and their life is a much broader topic; which we’ll be discussing soon enough. So, just keep your eyes open for further editorials in this ongoing series!

]]>Currently, cannabis is one of the fastest-growing industries in the world, on the way to generating an estimated $146.4 billion by 2025 (according to Grand View Research). The industry is currently in its early-stages, which can mean that even modest investments now could greatly increase in value 5, 10 or 20 years down the road. As the industry finds its footing on a global scale new investment opportunities emerge every day.

Cannabis does carry lingering social stigmas that may keep investors away. Yet the plant itself is only one facet of a diverse industry that includes everything from “plant-touching” companies to “ancillary” businesses that support the cannabis industry. The following are some of the opportunities tribes and other private investor groups are exploring.

Creating Native-owned cultivation, manufacturing and/or retail operations

As the wave of legalization has slowly but steadily swept across the U.S., the unique sovereignty of Tribal nations has created potential for cannabis business opportunities in communities located in states where recreational-use and/or medicinal cannabis has been legalized.

Investments of this type can take many forms, whether focusing on cultivation, manufacturing, or retail, or the development of a vertically-integrated cannabis operation. This path gives the Tribe complete control over the business.

Leasing Tribal land to cannabis cultivators

In many areas of the country, there are far more aspiring cultivators than there are locations where they can grow. As a result, an emerging trend is the rise of cultivation facilities established by real estate groups or private businesses, which are then leased to cannabis cultivators.

A Tribe looking to invest in cannabis could identify open land or create a greenhouse/indoor cultivation facility that can then be leased to cultivators looking for space. This is an ideal option for Tribal leadership that may not want to take on the operational and legal complexities of cultivating cannabis, but can still benefit from an investment supporting the industry.

Private investment opportunities in cannabis

In recent years a number of leading cannabis companies have gone public, primarily on stock exchanges in Canada, and with a select handful of listed on the NYSE and NASDAQ. The best-in-class producers and retailers represent an intriguing option for private investors. Standard due diligence for purchasing shares of a public company apply equally to the cannabis industry.

Additionally, a number of ancillary companies, those serving the cannabis industry through technology, real estate, or other services, have also gone public and represent a potential investment option. A diverse portfolio that includes a balanced mix of “plant-touching” and “ancillary” businesses could be a low-risk entry into the cannabis industry.

Institutional investment opportunities

As a fast-growing global industry, many cannabis companies are actively searching for capital infusions to expand operations, fund research, launch new products, or enter new markets. There is heated competition for both private venture capital investments, and for institutional investments in newly public cannabis and cannabis-related companies.

Tribal leadership can consider establishing, or investing in, a private equity or venture capital firm and act as an incubator for emerging cannabis businesses. Establishing a fund in conjunction with the other options listed previously could produce a robust cannabis portfolio.

Considering hemp and CBD

While cannabis legalization gets headlines, related products like hemp and CBD are quietly establishing themselves as intriguing industries on their own. The path for growing industrial hemp has recently been opened by federal legislation and the uses of the product are endless. Similarly, CBD has launched a holistic medicine craze, is in great demand for a wide variety of products, and can be derived from non-cannabis sources.

If a Tribe chose to explore hemp and CBD as investment opportunity, they could follow any of the paths illustrated previously and swap out cannabis for hemp or CBD.

Finding the investment mix for your Tribe

The options provided above are just a sample of the opportunities available to investors. There are risks involved with any investment, and cannabis’ complex legal status creates further complications. As result, many traditional investors have been slow to move into the space. But for proactive investor groups, now is the time to get an early foothold in what will soon be a multi-billion dollar global industry.

]]>To help cannabis entrepreneurs and investors keep up with the fast pace of change in the cannabis industry we will be providing monthly summaries of the latest regulatory and legislative news to provide a snapshot of latest happenings while also highlighting matters of interest looking forward.

This month the focus is on prominent federal legislative activity (e.g. the SAFE Act and the STATES Act), state legalization measures (e.g. NJ, NY, IL, and others), and two bills in Colorado that have the potential to attract out-of-state investment to that market.

Changes in federal cannabis legislation

With control of the House of Representatives being transferred to the Democratic party, several bills that have the potential to profoundly impact the cannabis landscape have advanced in Congress. For example, the last week of March saw the House Financial Services Committee move forward the Secure And Fair Enforcement (SAFE) Banking Act to a full House vote, reportedly “within weeks.” Following the momentum of the House bill, U.S. Sens. Jeff Merkley (D-OR) and Cory Gardner (R-CO) have introduced the companion bill in the Senate.

The latest SAFE iteration addresses the cannabis banking crisis and includes amendments that offer protection to insurance companies and other financial services companies.

The banking issue is long-standing and predates even the implementation of recreational cannabis in the US. The lack of straight forward access to fundamental banking services for the cannabis industry creates a multitude of challenges, most notably the operational and financial difficulties of a multi-billion-dollar industry operating almost entirely in cash. This has obvious implications for public safety and potential diversion to the black market, among other concerns.

The inability to access banking services is often identified as a major hindrance to market entry for large and well-resourced corporations and removal of this barrier could herald a seismic shift in investment into the cannabis industry. At time of writing the House Bill had 152 cosponsors, including 12 Republicans, whereas the Senate bill has 20 co-sponsors.

Adding further momentum to the SAFE bill, last week Last week, Secretary Steve Mnuchin offered his support for a legislative fix for the banking issues facing the cannabis industry. “There is not a Treasury solution to this. There is not a regulator solution to this,” he said. “If this is something that Congress wants to look at on a bipartisan basis, I’d encourage you to do this.”

Another potentially substantial piece of legislation is the Strengthening the Tenth Amendment Through Entrusting States Act (STATES Act), which aims to reduce conflict between federal and state laws as they relate to cannabis. The STATES Act is a potential gamechanger for the cannabis industry, allowing legal certainty for companies seeking to operate in dozens of jurisdictions across the US.

Although this legislation stalled in December, it was reintroduced on April 4th, alongside other measures, which include:

- the Ending Federal Marijuana Prohibition Act that would effectively legalize marijuana at the federal level by removing it from the Controlled Substances Act.

- The Marijuana Justice Act of 2019

The extent to which these bills have bipartisan support may be crucial if they are move beyond the House.

Four steps forward and two steps back in state legalization efforts

It has been a mixed month in terms of advancing cannabis legalization measures at the state level. On the one hand, there has been progress in multiple states, such as Connecticut, Illinois, and New Hampshire. While on the other hand there was a couple of snags holding up the implementation of recreational markets in New Jersey and New York.

Recent adult-use cannabis legalization headlines include:

- The New Jersey cannabis legalization bill was pulled due to lack of support although Gov. Murphey (D) reportedly stated he remained committed to getting the bill passed.

- New York dropped cannabis legalization from its budget bill where it was viewed as more likely to pass, however, regulators remain optimistic of progress later in the year. The New York City Council also voted to ban cannabis testing for job applicants.

- A General Law Committee in the Connecticut Legislature approved a bill that would legalize an adult-use cannabis market in the state.

- In New Hampshire, the House Ways and Means Committee approved a vote on the floor on legislation that would legalize an adult-use cannabis market.

- A bill to legalize retail cannabis in Illinois was introduced and passed to a subcommittee for further consideration.

- Governor of Guam signed a bill legalizing cannabis, becoming the first US territory to do so.

Despite the hiccups outlined above, there is a clear trend towards legal cannabis across the US. Moreover, several states took steps towards expansion or liberalization of their medical cannabis markets. Certainly in the long term, the outlook is optimistic for the cannabis industry on a number of fronts.

Back to the future as Colorado looks to position itself as an investment hub for cannabis

When Colorado became the first state to implement an adult-us cannabis framework in 2014, out of state investment was restricted. This allowed the state to build upon its existing medical cannabis market.

The understandable caution has since been questioned, however, and a Bill offering more flexibility in investment passed both the Colorado House and Senate in 2018, only for then Gov. Hickenlooper to veto it. In 2019, a replacement Bill was introduced and has recently passed its third reading in the House unamended.

As an established market with mature regulations and market stability, Colorado has low-risk potential when compared to emerging markets in other states – although competition is likely to be strong, with ever-thinning margins as prices continue to drop in the state.

Out-of-state investors exploring options in Colorado may be interested in acquiring social consumption licenses in Denver, or seek opportunities for market expansion in the delivery segment of the market. If passed, HB19-1234 would allow licensed dispensaries to offer these services for the first time.

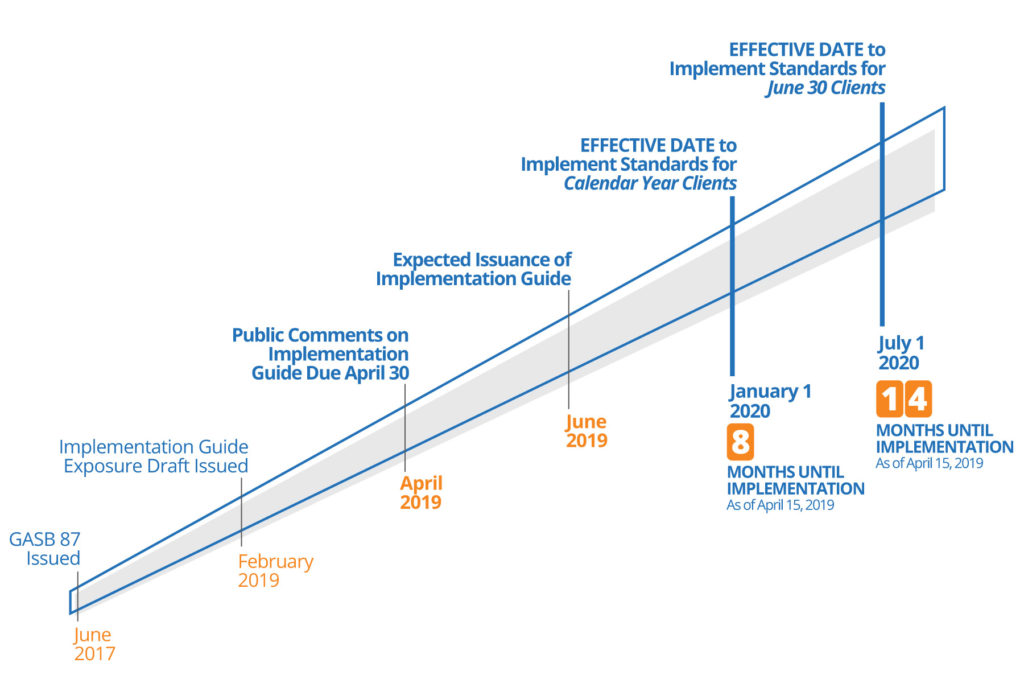

]]>GASB 87 readiness

With an effective date within the next year for some governments (i.e., as soon as January 1, 2020, for governments with a calendar year ending December 31, 2020) – the countdown has begun for planning for the impending changes to accounting and reporting for leases.

Under these new rules, the recording of leases, including assumptions, will significantly impact financial statement amounts and disclosures. Because governments use a variety of leasing arrangements to stabilize cash flows and reduce risk and uncertainty, the new requirements have strong accounting and financial reporting implications requiring a readiness plan. But first, why are these changes occurring?

The backstory on GASB 87

It is important to have some context for the impending changes. The new statement was created because leasing guidance for state and local governments, as we know it, predates GASB’s existence. Because of this fact, the GASB’s conceptual framework was not taken into consideration, which includes definitions of assets, deferred outflows of resources, liabilities, and deferred inflows of resources. The updated guidance for lease accounting has rectified the situation, which is currently underreporting the economics of a lease transaction.

The new lease accounting standards will replace the current operating and capital lease categories with a single model for lease accounting, based on the concept that leases are a means to finance the right to use an asset.

Lease assessment timeline

With the effective date approaching quickly, the time to prepare is NOW!

Taking the lead

The MGO GASB 87 Implementation Team has created a readiness assessment tool providing 10 preliminary implementation questions for consideration in your planning. These will not only prepare you for the new lease accounting standards, but may uncover matters that were not previously considered or identified.

This 10-step Implementation Plan is more of a general guide designed to assist you in identifying issues and help you organize your implementation process, rather than being an all-inclusive plan with specific technical guidance. As you evaluate the leases that are unique to your organization, you will most likely find that further research and analysis is necessary to ensure proper accounting considerations. For example, if you operate an airport and have aviation leases with air carriers regulated by the U.S. Department of Transportation and the Federal Aviation Administration, it will be necessary to understand how the regulated lease provisions affect your contracts, especially in situations where there are multiple lease components.

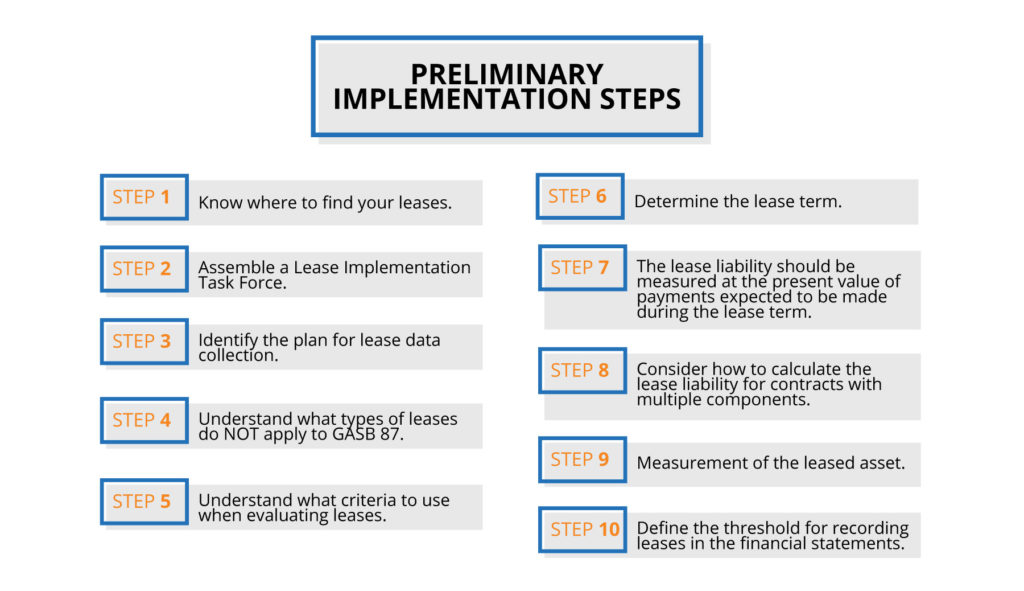

Preliminary implementation steps

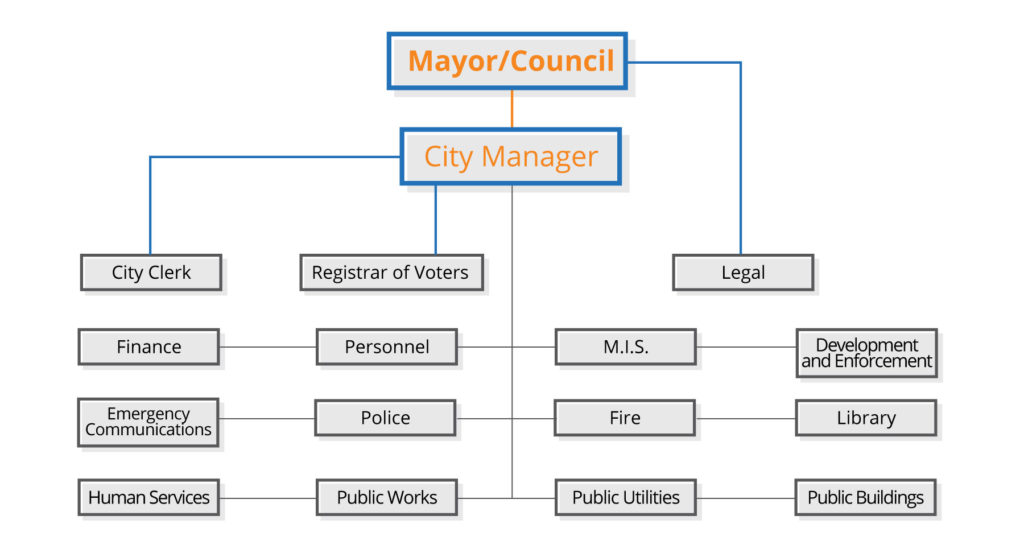

Step 1. Know where to find your leases.

It may seem obvious, but the first step in managing your leases is knowing where they are and, specifically, who is responsible for maintaining them. A good place to begin is with organizational charts. This is an example for a municipal government.

Depending on how your government contracts services, leases may be held centrally within the Finance Department or they may be decentralized in a multitude of departments, and possibly even managed by various entities.

Keep in mind that most leases that were previously expensed as operating leases will need to be accounted for as a lease obligation under the new standards, including option years if you are reasonably certain they will be exercised.

After the “where” has been established you can move into the “what” by identifying the universe of leases for your organization. This can be accomplished by evaluating the general ledger, reviewing contract files and surveying purchasing and operating departments, which leads to assembling a task force and formulating a plan for data collection.

Step 2. Assemble a Lease Implementation Task Force.

Identify people who are critical to a successful implementation. Consider including operational and legal staff who are already familiar with existing lease terms and conditions. The Lease Implementation Task Force should remain in place until the action plan for lease implementation is finalized. The benefits are many, including a collective think tank to evaluate and apply appropriate accounting treatment to each class of leases.

This task force may also be important to developing internal policies and procedures, such as whether or not a materiality threshold is appropriate, and whether or not lease accounting software should be utilized to manage the lease database. Furthermore, the implementation of the lease accounting standards is only a start, proper accounting treatment, including the remeasurement of the initial lease liability when certain lease changes have occurred and the evaluation of new leases subsequent to implementation, will be an on-going requirement.

Step 3. Identify the plan for lease data collection.

Converting your lease data into an organized structure is not without its challenges. You may encounter incomplete lease files, “hard copy versions only” of certain lease agreements, voluminous amendments, and the need to translate data from lease agreements into databases. This is all part of the process leading to a successful implementation of the new standards. Once you complete the database, you’ll then need to properly classify the leases.

Step 4. Understand what types of leases do NOT apply to GASB 87.

While a multitude of leases will be impacted by the new GASB 87 standards, there are several classifications that are not subject to GASB 87, including: intangible assets (such as computer software licenses); biological assets, including timber, plants and animals; inventories; service concession arrangement contracts; leases in which the underlying asset is financed with outstanding conduit debt; and supply contracts, such as power purchase contracts. Additionally, nonexchange agreements are exempt: for example, in the case of leasing property to a school district for a reduced price of $1/year for 30 years.

In the end, it is all about evaluating the leases subject to GASB 87.

Step 5. Understand what criteria to use when evaluating leases.

After eliminating leases that are not subject to GASB 87, as identified in Step 4, further classification of leases is necessary to ensure that the appropriate accounting treatment is applied. Short-term leases, contracts that transfer ownership, leases of assets that are investments (lessors only), and certain regulated leases (lessors only) all qualify as leases, but have differing accounting treatments than the typical long-term, noncancellable leases.

Step 6. Determine the lease term.

A lease term is defined as the period during which a lessee has a noncancellable right to use an underlying asset, plus any extension periods and options that are reasonably certain to be exercised. The GASB wants organizations to consider extension periods and options, so there is no incentive to structure initial lease terms to avoid meeting the definition of a lease. Since month-to-month leases that continue into a holdover period until a new lease is signed are not part of the noncancellable period or a formal extension, there is no basis in the standard for currently including them. Let’s discuss the calculation of the lease liability.

Step 7. The lease liability should be measured at the present value of payments expected to be made during the lease term.

The lessee should initially measure the lease liability at the present value of payments expected to be made during the lease term, which includes the following elements:

- Fixed payments

- Variable payments that depend on an index or a rate, initially measured using the index or rate as of the commencement of the lease term

- Variable payments that are fixed in substance

- Amounts that are reasonably certain of being required to be paid by the lessee under residual value guarantees

- The exercise price of a purchase option if it is reasonably certain that a lessee will exercise that option

- Payments for penalties for terminating the lease, if the lease term reflects the lessee exercising (1) an option to terminate the lease or (2) a fiscal funding or cancellation clause

- Any lease incentives receivable from the lessor

- Any other payments that are reasonably certain of being required based on an assessment of all relevant factors

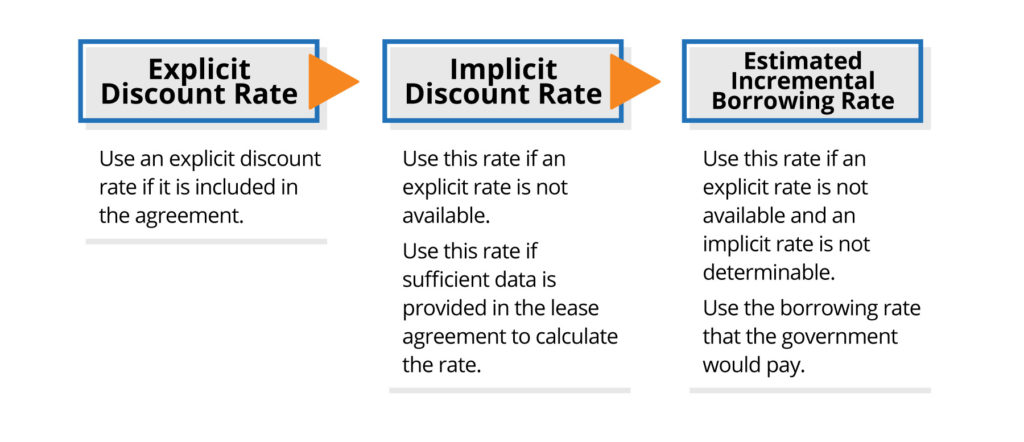

For additional guidance and context to these bulleted items, refer to GASB 87 paragraph 21. In order to determine the present value, you may need to develop the discount rate.

Step 8. Consider how to calculate the lease liability for contracts with multiple components.

Proper classification of leases is not always straightforward when both lease and nonlease components are included in the same contract. What if a building lease has utilities and common area maintenance costs? The answer can be found in guidance covering contracts with multiple components, which identifies maintenance services as a nonlease component. What if a lease involves multiple assets and those assets have different lease terms? The answer can also be found in guidance covering contracts with multiple components, which provides that each asset should be accounted for as a separate lease component. Many rental leases embed the cost of utilities and common area maintenance into the lease payment. Contract components should be separated using the best estimate available based on observable information. If it is not practicable to estimate these separate costs, then account for the contract as a single lease unit (see GASB 87 paragraph 67).

Step 9. Measurement of the leased asset.

The initial measurement of the leased asset should be based on the measurement of the associated lease liability. In the case of contracts with multiple components, the value of the underlying leased asset is not always clearly stated in the agreements, and many lease agreements will not cover the life of the leased asset. Some leased assets may involve proprietary information that lessors are not willing to share. Therefore, determining the value of the underlying asset is not always straightforward in these cases. Whenever possible, identifying comparable assets that are sold in a market transaction is an important part of the process. You can then utilize the knowledge of internal or external experts who can provide a basis for an estimate.

You are now ready for the final step.

Step 10. Define the threshold for recording leases in the financial statements.

Unfortunately, while GASB provides explicit guidance on capitalization thresholds for capital assets, it does not specify any such consideration for lease obligations. Using a threshold may help you avoid recording leases that are immaterial and avoid a mismatch with leased assets that are too small to capitalize. A good starting point may be to use the capitalization thresholds that are already established for your organization. Once you determine your initial criteria for establishing leases, verify that it does not exclude significant leases from application of the new standard. You can revise these thresholds as needed.

Now that we have provided you with our 10-step GASB 87 readiness plan, you should have a fairly good idea what your next steps will be.

So you can plan for compliance, this is an excellent time for the MGO GASB 87 Implementation Team to review your leases. This will ensure that you are ready to take the most important step: Implementation. In addition, we have put together an online readiness assessment that helps you evaluate where you stand in the implementation process.

About the Author:

David Bullock is a thought leader in MGO’s State and Local Government practice. An Assurance and Government Advisory Services Partner with 25 years of professional experience, he currently oversees numerous audits and other services to governmental organizations throughout California. In 2018, David was appointed to the AICPA State and Local Government Expert Panel. He is also on the Governmental Accounting Standards Board’s (GASB) Financial Reporting Model Reexamination Task Force. In 2018, he was appointed to the California Society of CPAs’ Governmental Accounting and Auditing Committee. His numerous presentations cover topics related to generally accepted accounting principles promulgated by the GASB, and auditing standards, promulgated by the AICPA and the GAO.

]]>