- Environmental, social, and governance (ESG) information helps investors, regulators, and the public-at-large understand and interpret a government entity’s risk profile and its ability to drive positive impact.

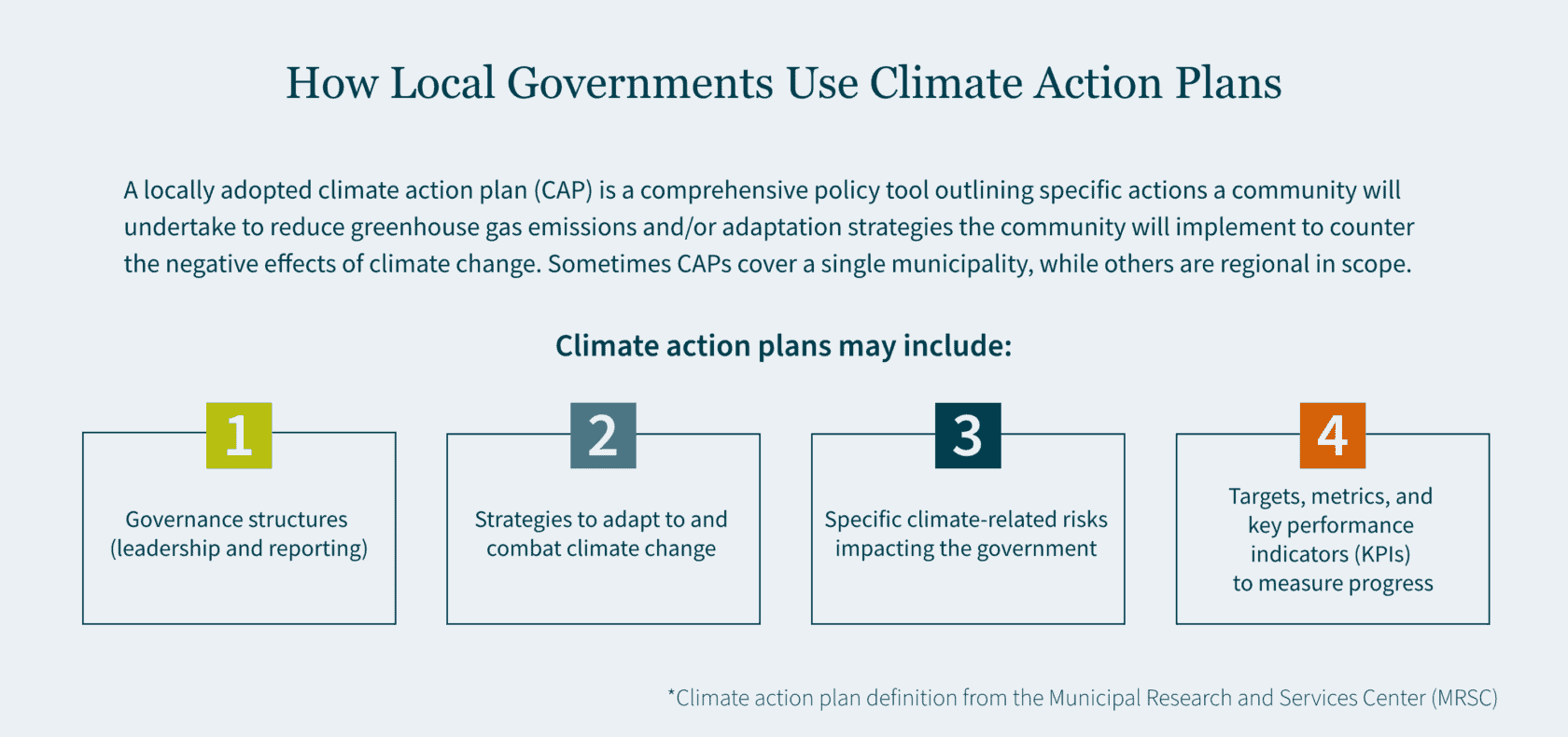

- To present this information publicly, government entities are developing robust “Climate Action Plans,” which are reviewed and refreshed on a periodic basis.

- As disclosing ESG-related information to the public becomes more common, government entities are also expanding ESG-related disclosures within annual financial reports.

Coined in a 2004 United Nations report, the term “environmental, social, and governance” (and its accompanying acronym “ESG”) is less than 20 years old. Yet, you would be hard-pressed to find a boardroom today where ESG is not top of mind. It is not just businesses either — ESG is also an increasingly important topic of discussion within government organizations.

State and local governments use ESG-related information as a mechanism to measure and track priorities, footprints, and targets. As governments have matured, ESG reporting and presented information more consistently with year-to-year comparability, investors*, regulators, and the public-at-large have sought out this reporting to help them understand risk and the government entity’s ability to drive positive impact.

*Note: The term “investors” refers to those who are exploring and/or holding investments in government-issued securities (e.g., hedge funds, institutions, individuals, etc.).

The Increasing Importance of “Climate Action Plans”

To present ESG-related information to the public, many government entities develop and communicate robust “Climate Action Plans”. These plans highlight a myriad of information, including (but not limited to):

- Governance structures (e.g., communication and reporting lines from environmental leadership into the mayor’s office)

- Strategies to adapt to and combat climate change

- Specific climate-related risks, which impact the government entity

- Targets, metrics, and key performance indicators (KPIs) used to measure progress

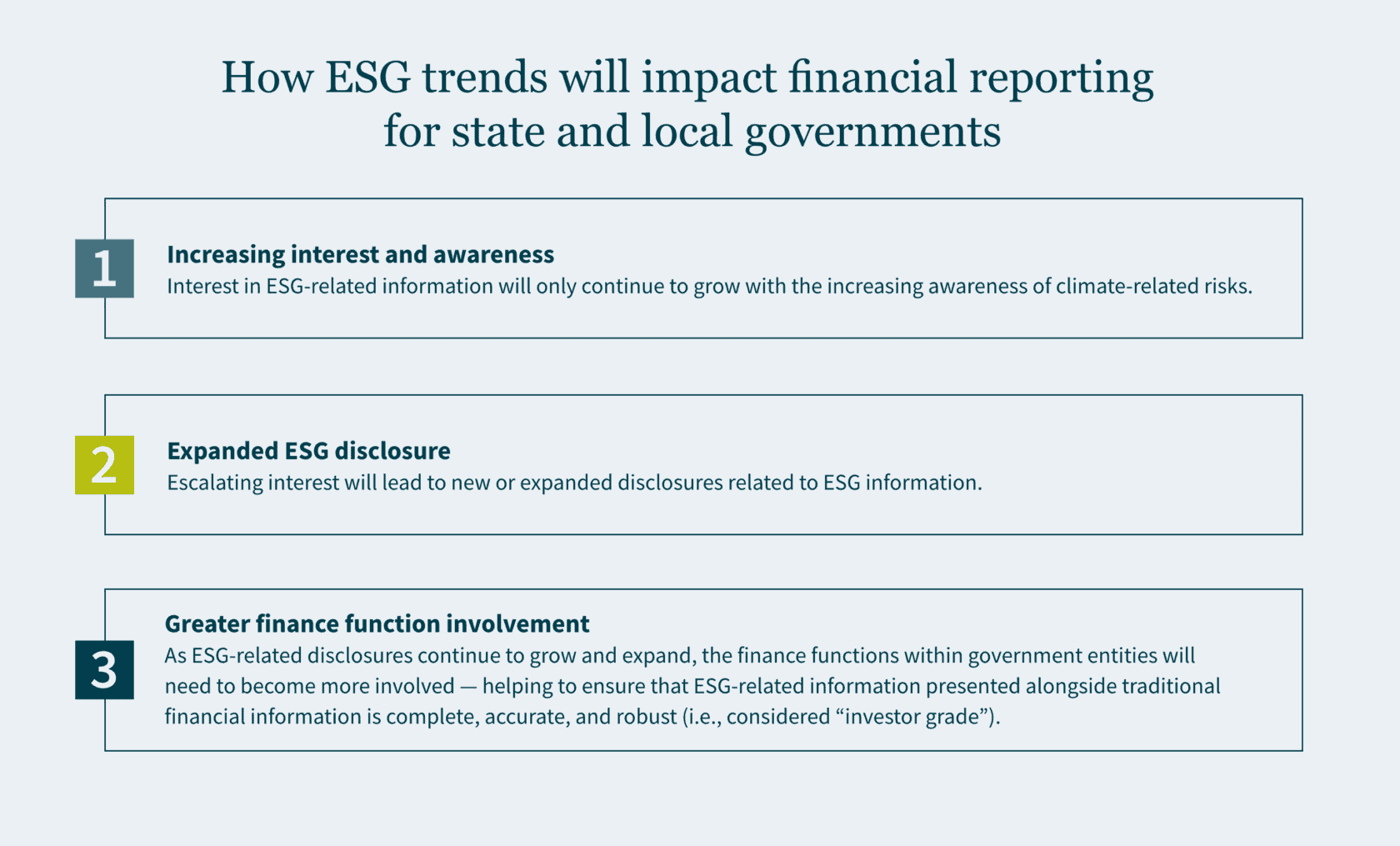

As Climate Action Plans continue to evolve, governments are commanding and allocating more financial resources to activate these plans. With the increased focus on climate-related initiatives presented in Climate Action Plans, we are seeing an expansion of ESG-related information disclosed within “Annual Comprehensive Financial Reports” across the country — a sign that financial disclosures are maturing to meet growing interests from investors, regulators, and the public-at-large.

A Growing Push from Investors and Regulators

The focus on non-financial risks (including, but not limited to, ESG-related risks) by investors and regulators continues to intensify. When we take a step back to analyze the trend, a few things become clear:

- Interest in ESG-related information will only continue to grow with the increasing awareness of climate-related risks.

- Escalating interest will lead to new or expanded disclosures related to ESG information.

- As ESG-related disclosures continue to grow and expand, the finance functions within government entities will need to become more involved — helping to ensure that ESG-related information presented alongside traditional financial information is complete, accurate, and robust (i.e., considered “investor grade”).

To dive deeper into that last point, where would a finance function start? The short answer is by increasing the integration and collaboration between a government entity’s environmental leaders and the finance functions. The longer answer is that government entities need to develop holistic approaches to collecting and reporting robust ESG-related information to meet the expectations of investors, regulators, and the public-at-large.

The bottom line: As the issuance of and investment in municipal securities continues to grow, the quality of ESG-related information disclosed to the public will need to be enhanced to meet the demands of investors.

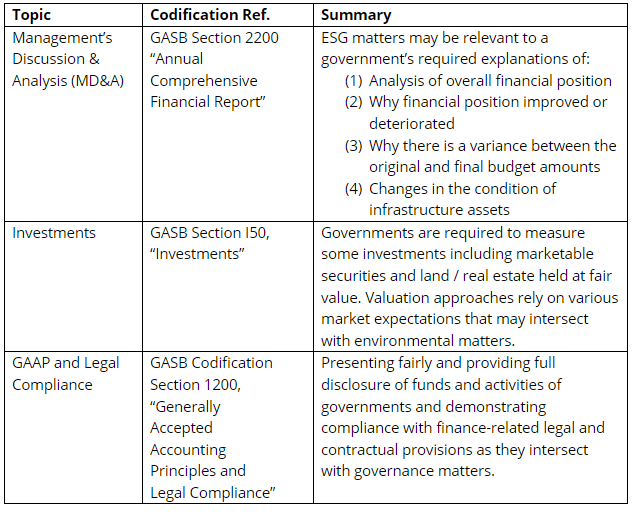

Transparency in Budgets and Financial Reporting

With an increase in ESG-related disclosures in annual financial reports by government entities, recent interpretive guidance from the Governmental Accounting Standards Board (GASB) indicates that government entities can expect further scrutiny and regulation as these types of disclosures become more commonplace.

Essentially, it is important for your government to have a robust, well-communicated ESG “story” within a Climate Action Plan — but you also must provide investor-grade transparency within audited financial statements. Government entities are already beginning to meet this challenge. Two examples of local governments with a growing presence of ESG-related information in their Annual Comprehensive Financial Reports are the City and County of San Francisco and the City of Fremont.

The City and County of San Francisco transparently discloses both environmental and social initiatives, capturing details related to its Environmental Protection Fund, as well as specific details related to revenues received from state, federal, and other sources for the preservation of the environment.

The City of Fremont — which is much smaller in terms of population (~230,000) and financial resources (roughly $1.5 billion in total primary government assets from “government activities”) — depicts ESG-related information throughout its annual report, including but not limited to qualitative information in the “management discussion and analysis” section, as well as quantitative information related to “community development and environmental services.”

The Path Forward: Enhancing Your ESG Reporting

With ESG-related information becoming more integrated into investor decision-making, your government needs to focus on enhancing its Climate Action Plans and developing “investor grade” disclosures related to ESG risks and opportunities for inclusion within your traditional financial reporting. These initiatives will require additional financial resources and human capital to create and maintain — and further collaboration between environmental, social, and financial leaders will be needed to drive the change.

How MGO Can Help

Incorporating ESG disclosures into financial reporting can pose challenges to states and local governments unfamiliar with ESG reporting standards. With experience providing ESG solutions, our State and Local Government Practice will work with your team to meet requirements and make information “investor-ready,” while also ensuring accountability and transparency.

]]>- President Biden has signed the Inflation Reduction Act of 2022 into law.

- This large package contains many new tax credits to incentivize taxpayers to “go green” with energy from renewable resources while simultaneously receiving financial relief.

- It also extends or adds to currently existing credits for additional tax-saving opportunities.

On August 16, President Joe Biden signed the Inflation Reduction Act (IRA) of 2022 into law. Within the large tax reform package are numerous “green” tax credits focused on providing financial relief to taxpayers while incentivizing them to make sustainable choices and combat climate change.

These new credits are aimed at motivating taxpayers to use energy from renewable sources, prioritizing options like wind and solar. The IRA also introduces new credits and strengthens or extends existing credits that provide tax relief for purchasing new and used clean-energy vehicles and installing energy efficient heating and cooling systems. Additionally, companies that cut their methane emissions can access certain credits, while those that do not could face penalties.

The rules and regulations around claiming these green credits can be complicated. In this article, our Tax Credits and Incentives team breaks down how individuals and organizations can capitalize on these tax saving opportunities.

Swap gas guzzlers for an electric vehicle

Taxpayers that purchase a new or used “clean car” can qualify for this consumer tax credit. Vehicles considered clean are those that use a battery partly or fully manufactured in North America and built with materials extracted or processed in one of the countries currently in a free-trade agreement with the U.S.

Your income is a factor in how much you can reap in tax credits. If a taxpayer makes less than $150,000 annually (or has a combined family income below $300,000), the taxpayer can get up to $7,500 for new electric vehicles that qualify. Note the money would be applied at the point of sale, so the taxpayer’s monthly payments would be lowered (as opposed to reducing the tax bill months down the line).

Previously, the federal tax credit for electric vehicles did not include cars from manufacturers that already sold at least 200,000 models (GM, Toyota, and Tesla were excluded). This bill unravels that; instead, there is now a price threshold per vehicle. To qualify for the credit, bigger vehicles like SUVs, pickup trucks, and vans would have to cost less than $80,000 to qualify for the credits. Smaller vehicles are capped at $55,000. So, if you have your eye on a super sporty electric vehicle, you may be out of luck.

Taxpayers can also get $4,000 off a used electric vehicle if it is sold by a dealer for $25,000 or less — but only if they individually make up to $75,000 annually or $150,000 jointly. The addition of credits for used electric vehicle purchases is a win for the industry, and advocates of the bill are hopeful that this incentive will encourage an increase in electric vehicle adoption.

Modifying your home to be more energy efficient

To incentivize taxpayers to make their homes more energy efficient, the bill’s $4.28 billion High-Efficiency Electric Home Rebate Program provides rebates for low- and moderate-income households when they replace fossil-fuel boilers, furnaces, water heaters, and stoves with more efficient electric devices powered by renewable energy.

Some taxpayers will need to upgrade their electrical panels before they are able to install the new appliances. They can take advantage of up to $4,000 to do so. Furthermore, if they are interested in making their home generally more energy efficient, they can capitalize on a rebate of up to $1,600 given to seal and insulate their house, as well as up to $2,500 to improve their home’s wiring.

In terms of appliances, taxpayers can get up to $8,000 to install heat pumps that both heat and cool their home, plus as much as $1,750 for a heat-pump water heater. To offset the cost of a heat-pump dryer or electric stove, taxpayers can claim up to $840. It is estimated by making these changes, they can save significantly on their future energy bills.

There are several parameters for these rebates. First, the program runs through September 30, 2031 — so you do have time to implement these changes to your home. The maximum amount taxpayers can collect is $14,000, and to qualify, their household income cannot exceed $150% of the median income in the area they live. For those who do not qualify, there is a tax credit of up to $2,000 available to install heat pumps, plus up to $1,200 annually to install new windows, doors, or an induction stove.

Save when installing solar panels

Lastly, taxpayers can collect a 30% tax credit for installing residential solar panels through December 31, 2034. The credit decreases to 26% if you wait until after December 31, 2032. Taxpayers can also install solar battery systems to qualify for the tax credit.

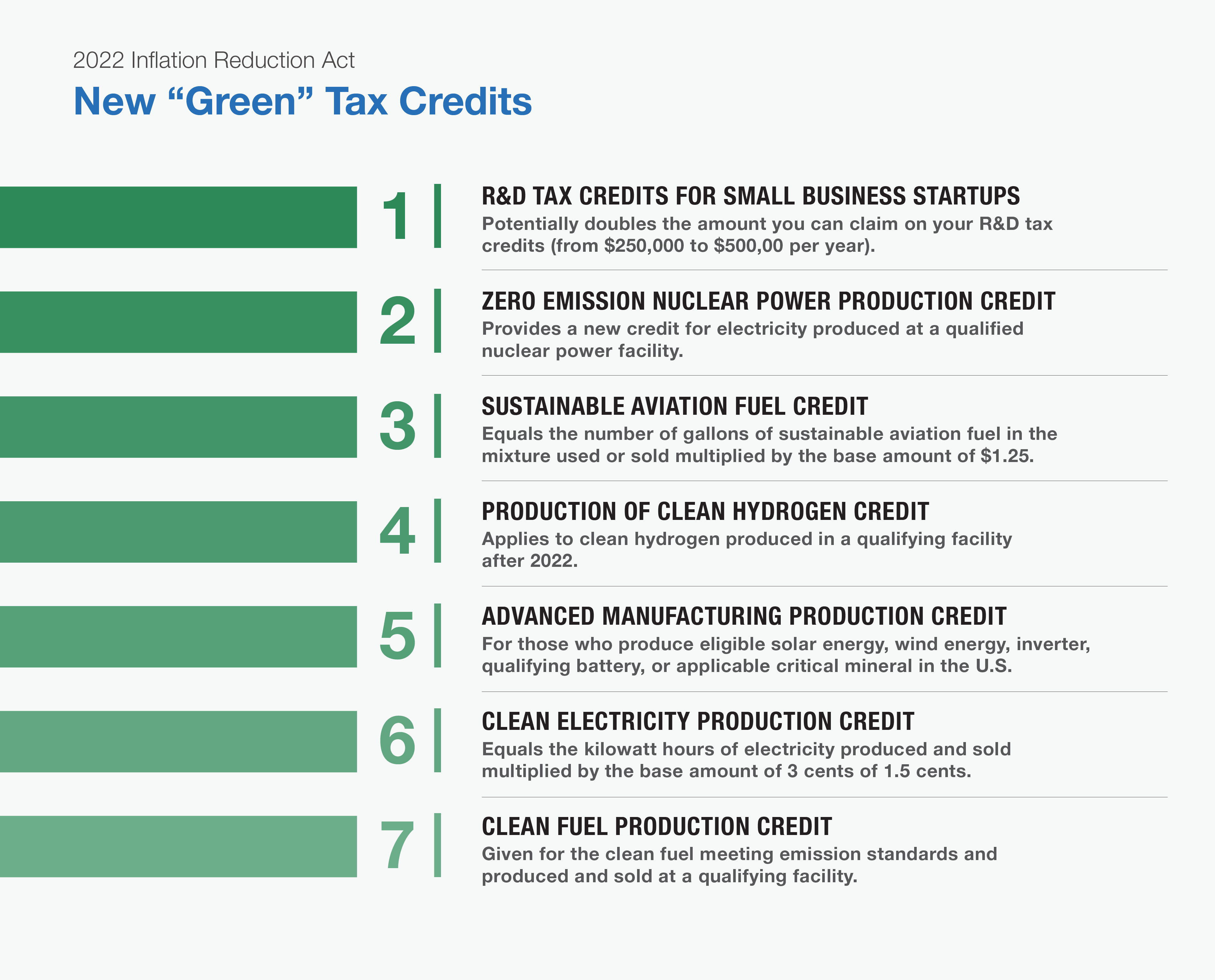

New “green” tax credits

There are other ways taxpayers can take advantage of going green. Here are some of the new tax credits to capitalize on.

Doubling of R&D Tax Credits for Small Business Startups — Would potentially allow recipients to double the amount they can claim on any R&D tax credits (from $250,000 to $500,000 per year against payroll taxes).

Zero Emission Nuclear Power Production Credit — Provides a new business credit for electricity produced by a taxpayer at a qualified nuclear power facility before the date of enactment.

Sustainable Aviation Fuel Credit – Creates a new business credit for each gallon of sustainable aviation fuel sold or used as part of a qualified fuel mixture. The credit equals the number of gallons of sustainable aviation fuel in the mixture multiplied by the base amount of $1.25. There are increases available if the taxpayer meets certain greenhouse gas emissions reductions, and it applies to fuel sold or used in 2023 and 2024.

Production of Clean Hydrogen Credit — Given to producers of clean hydrogen during the ten-year period beginning on the date a qualifying facility is originally placed in service. It applies to clean hydrogen produced after 2022.

Advanced Manufacturing Production Credit — Provides a new production credit for each eligible solar energy component, wind energy component, eligible inverter, qualifying battery component, and applicable critical mineral produced by a taxpayer in the U.S. (or in U.S. possession and sold to an unrelated person). It applies to components and minerals produced and sold after 2022.

Clean Electricity Production Credit — New business credit for clean electricity facilities placed in service after 2024 (where the greenhouse gas emissions rate is not greater than zero). The credit amount equals the kilowatt hours of electricity produced and sold multiplied by the base amount of 3 cents or 1.5 cents. The credit will phase out one year after the later of 2032 or the year when annual greenhouse gas emissions from U.S. production are equal to less than 25% of the 2022 emissions rate (whichever comes first).

Clean Electricity Investment Credit — New investment credit for clean electricity property investments in energy storage technology and qualified facilities placed in service after 2024 where the greenhouse gas emissions rate is not greater than zero. It phases out after the later of 2032 or when the annual greenhouse gas emissions from U.S. electricity production are equal to or less than 25% of the 2022 emission rate (whichever comes first).

Clean Fuel Production Credit — Creates a business credit for the clean fuel a taxpayer produces at a qualifying facility and sells for qualifying purposes. The fuel must meet certain emissions standards.

Extension and modification of “green” tax credits

Several tax credits already in existence were extended and modified in the Inflation Reduction Act. They include:

Renewable Electricity Production Tax Credit (PTC) — Extends the beginning of construction deadline for certain renewable electricity production facilities through the end of 2024, as well as reduces the base amount of credit with the potential to qualify for five times that amount. It applies to facilities placed in service after 2021, and increases the credit amounts for domestic content, energy communities, and hydropower.

Energy Investment Tax (ITC) — Extends the beginning of construction deadline for some types of energy property, including qualified fuel cell property, for one year through the end of 2024. It extends the beginning of construction deadline for geothermal equipment through the end of 2034 and permits the credit for new types of energy property like energy storage technology, microgrid controller property, and qualified biogas.

Carbon Oxide Sequestration Credit — Extends and enhances carbon oxide sequestration credits for qualified industrial facilities and direct air capture facilities IF construction begins before 2033. It also lowers the minimum carbon capture requirement, and generally applies to those facilities and equipment placed in service post-2022.

Tax Credits for Biodiesel, Renewable Diesel, and Alternative Fuels — Extends these tax credits through 2024 and apply to fuel sold or used after 2021.

Second Generation Biofuel Credit — Extends tax credits to second generation biofuel through 2024 and applies to second generation biofuel production after 2021.

Nonbusiness Energy Property Credit — Extends this credit through 2023, as well as changes the credit rate to 30% for both qualified energy efficiency improvements and residential energy property expenditures. It replaces the $500 lifetime limit with a $1200 annual limit, modifies the limits for specific types of property, and modifies standards for qualified energy efficiency improvements on property placed in service after 2022.

Residential Energy Efficient Property Credit — Extends the residential energy-efficient property credit through 2034 and replaces the credit for biomass fuel property expenditures with a new credit for battery storage technology expenditures on those made after 2022.

New Energy Efficient Home Credit — Extends the business credit for contractors who manufacture or construct energy efficient homes through 2032. It applies to dwellings acquired by the contractor after 2022.

Alternative Fuel Vehicle Refueling Property Credit — Extends the tax credit through 2032 and increases the credit limit to $100,000 per item of depreciable refueling property and $1,000 per item of non-depreciable refueling property.

Advanced Energy Project Credit — Extends the competitively awarded investment tax credit for clean energy and energy efficiency manufacturing projects. It provides as much as $10 billion of new credit allocations effective in early 2023.

Increase in Energy Credit for Solar and Wind Facilities — In order to qualify, one must have a maximum net output of less than five megawatts and must be in a low-income community, on American Indian land, or part of a low-income residential building project (or low-income economic benefit project), effective in early 2023.

Reinstatement of Superfund Hazardous Substance Financing Rate — Reinstates a financing rate on crude oil and imported petroleum products at a rate of 16.4 cents per gallon through 2032.

Our perspective on the Inflation Reduction Act’s tax credits

Looking ahead, it is imperative that you are ready to capitalize on these tax credits. Getting into the weeds with some of the qualifications, however, could prove challenging, and working with a professional services firm could make all the difference in ensuring you take advantage of the credits you qualify for.

At MGO, our dedicated Tax Credits and Incentives team brings more than 30 years of experience in helping you structure your expenses in a way that will help you acquire appropriate documentation, assist in calculating and claiming credits, and maximize the amount you can receive. Our full-service firm, led by experienced CPAs and attorneys, provides a holistic approach to examining your organization and determining how you can best reach your goals.

About the author

Michael Silvio is a partner at MGO. He has more than 25 years of experience in public accounting and tax and has served a variety of public and private businesses in the manufacturing, distribution, pharmaceutical, and biotechnology sectors.

]]>While the legislation is certainly complex, it will serve as a catalyst for the public and private sectors and allow the United States to align itself with the goals and interests of the largest global economies.

Or, as Bill Gates puts it, “(the Inflation Reduction Act) represents our best chance to build an energy future that is cleaner, cheaper and more secure.”

To date, the Inflation Reduction Act has been met with varying opinions (both positive and negative). However, there is no question that it will provide ample opportunities and incentives for existing businesses to capture new value.

Below, MGO’s Environmental, Social, and Governance (ESG) team breaks down a subset of the most important objectives you need to be aware of.

Objective #1: Supporting emerging climate technology

On its surface, carbon capture (or the process of removing carbon dioxide from the atmosphere and locking it away) offers opportunities to slow, limit, or even reverse climate change — especially if done at scale.

Carbon removal startups continue to research and innovate new technologies which will eventually remove many tons of CO2 from the atmosphere each year. These technologies are still relatively young and require additional financial investment in order to reduce costs and enhance impact.

With the passing of the act comes a new wave of funding, which carbon removal experts and startups are eager to take advantage of. Specifically, the bill will:

- Increase tax credits for permanent carbon removal from $50 to $180 per ton (using direct air capture)

- Significantly lower the amount of carbon companies must remove to qualify (100,000 tons to 1,000 tons)

While there are criticisms of this objective, effective policies and technologies are needed to explore climate change.

Objective #2: Individual tax credits

The Inflation Reduction Act also provides a host of environmental and clean energy tax rebates, credits, and incentives for taxpayers.

In a nutshell, the bill incentivizes taxpayers to seek out and use clean energy – prioritizing wind, solar, and other renewable sources. It also extends credits to taxpayers who purchase new or used clean-energy vehicles, as well as individuals who install energy efficient heating and cooling systems in their homes.

Keep in mind, both come with perimeters, including the amount of annual income you claim. A

Objective #3: Paying for the bill

Here are three ways Congress plans to fund the Inflation Reduction Act:

A minimum corporate tax rate on profits. The legislation will impose a tax rate of 15% on corporations that have at least $1 billion in profits. This will bring in approximately $222 billion in funding.

Increased IRS scrutiny. With strengthened, additional tax enforcement, the gap between what taxpayers owe and what the agency is collecting will shrink, allowing the agency to collect an approximate $124 billion.

Tax on stock buybacks. The Democrats added a 1% excise tax on stock buybacks when revising a draft of the Inflation Reduction Act. (Refresher: a stock buyback occurs when a publicly traded company buys its own stock back to raise the value of its shares). It is estimated that an additional $74 billion in funding will come from this portion of the bill.

Our perspective on how the Inflation Reduction Act will impact the ESG space

Many are calling the Inflation Reduction Act the biggest piece of climate legislation in American history. With $369 billion in subsidies and tax credits in electric vehicles, solar power, renewable energy, carbon capture and storage, the U.S. (which is the world’s second-biggest carbon emitter) is taking a leading position in the global energy transition.

]]>- The GASB has launched their first initiative to establish and introduce guidelines for ESG-related disclosures.

- The GASB has released an interpretation of its existing standards to help government entities further enhance ESG-related disclosures.

- We can expect that ESG-related disclosures will shift from voluntary guidance to mandatory reporting at some point.

Reporting and disclosure of environmental, social, and governance (ESG)-related information has long been a priority in the private sector and is now emerging as a key area of focus for state and local governments (or “government entities”).

In response to interested parties seeking more ESG-related information (e.g., investors, credit rating agencies, preparers and auditors of financial statements, citizens, policymakers, etc.) from government entities, the Governmental Accounting Standards Board (GASB) has released a publication to clarify how ESG-related information intersects with their existing standards.

The bottom line: GASB’s stakeholders and interested parties are seeking to understand the impacts of ESG-related matters on a government entity’s cash flows, financial position, and overall responsibility for fiscal accountability — and the publication can be seen as a form of interpretive guidance to bridge the gap.

What’s inside the publication?

GASB’s “Intersection of Environmental, Social, and Governance Matters with Governmental Accounting Standards” document was released on May 31, 2022, and it provides clear examples for government entities to make new, or enhance existing, ESG-related disclosures by leveraging their current standards and principles.

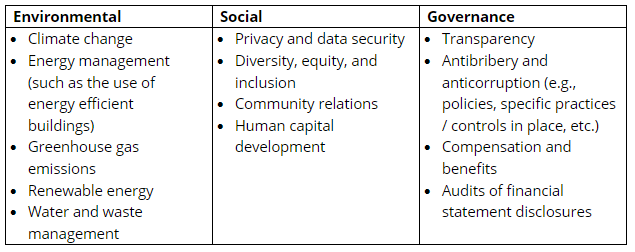

Up front, the publication acknowledges that “a single consistent definition of ESG is not prevalent in practice today.” However, broad examples are included in the publication for each pillar (note, the below list has been shortened for purposes of this article):

The interpretive portion of the publication goes on to assist government entities with detailed examples of how ESG-related information coincides with the current GASB standards (note, the below are 3 of 25 total examples from the publication):

Why this GASB release matters

In publishing this document, GASB is taking a traditional first step to introduce concepts and guidelines that set a foundation ahead for new reporting and disclosure rules in the future (also referred to as “interpretive guidance”).

This is not the first time a regulator or standard setter has issued interpretive guidance specific to ESG. In 2010, the Securities and Exchange Commission (SEC) released their own interpretive guidance to provide clarity to the private sector on how to leverage existing financial reports to make disclosures related to climate change. While it was uncertain how many companies would incorporate climate-related information in their financial reports, many chose to do so (at last count by the SEC in 2020, 33% of the 6,644 filings submitted to the regulator contained some form of climate-related disclosure). The interpretive guidance, therefore, laid the groundwork for a new climate-related proposal issued by the SEC in March 2022.

Essentially, interpretive guidance has historically preceded the release of new, formal guidance and the creation of new standards. If this proves true in the public sector, then we will first see an increase from state and local governments enhancing their existing financial reports and disclosures by incorporating ESG-related information. Subsequently, and after further analysis by GASB of those enhanced disclosures, we will likely see the release of a new ESG-specific standard from GASB.

Increasing the pressure

As demand for ESG-related disclosures increases, pressure will also increase on governments to begin providing or enhancing the disclosures in their financial reports. Further, if your entity issues securities (e.g., municipal bonds), you may encounter pressure from credit rating agencies depending on your approach (or lack thereof) to disclose and address ESG-related risks.

At present, ESG-related disclosures are contingent on a variety of factors (including but not limited to the government entity’s location, the historical or anticipated impacts of climate change, the level of ambition to become a leader in ESG-related reporting, etc.), but at some point these disclosures will shift from voluntary to mandatory.

How MGO can help

Many state and local governments have proactively disclosed ESG-related information on their websites or in standalone ESG / sustainability reports; however, GASB’s interpretive guidance demonstrates that ESG-information also needs to be considered when preparing your annual financial reports.

To stay ahead, MGO is helping the public sector as well as the private sector, develop and enhance their ESG disclosure strategies.

If you are interested in learning more, schedule a conversation with our ESG team today.

]]>Cannabis companies, like companies across every sector and industry, need to be focused on the double bottom line concept. Specifically, companies need to commit to both financial (first bottom line) and ESG-focused outcomes (second bottom line) to ensure long-term success.

The evolving definition of value

For companies across all industries, there is an enhanced sense of finding, committing, and tracking to a higher purpose. Whether it is prioritizing environmental risks and opportunities or committing to social initiatives, establishing a purpose beyond financial returns is paramount to long-term success in today’s world.

Cannabis in United States has a long history tied to criminalization which has had a disproportionate impact on minority and underprivileged populations. As such, there is significant opportunity for both federal and state governments and the industry itself to focus on social programs which drive positive impact and change (CNBC: Cannabis is projected to be a $70 billion market by 2028 — yet those hurt most by the war on drugs lack access).

Overall, ESG initiatives have become ubiquitous with business strategy and growth — and because the cannabis industry is inherently diverse, environmentally-focused, and values-driven, there is a unique opportunity make a real impact.

And how does a company develop a strategy on driving impact? It starts with inventorying your material, non-financial (i.e., ESG-specific) risks and opportunities.

A focus on materiality: the environmental pillar

When it comes to environmental issues, there are several material risks and opportunities that cannabis companies can prioritize, including but not limited to:

- energy management,

- greenhouse gas (GHG) emissions, and

- water and wastewater management.

For example, the western United States continues to experience historic droughts, which have forced local governments to restrict water usage (LA Times: Unprecedented water restrictions hit Southern California). As such, cannabis companies operating in the western U.S. are facing both a risk and an opportunity to re-think how they manage their water usage as part of the cultivation process.

A focus on materiality: the social pillar

As we previously mentioned, there are many social issues companies in the cannabis industry will find material to their businesses. These include:

- product quality and safety;

- access and affordability;

- customer welfare;

- human rights and community relations;

- selling practices and product labelling;

- employee engagement; and

- diversity, equity, and inclusion.

Leaders in the cannabis sector are using their businesses and platforms to push for tangible social progress — this includes investing in and prioritizing minority-led companies in their supply chains, establishing policy documents to hold business partners to strict operating standards, and adding new jobs with competitive pay and benefits in communities which need it the most.

A focus on materiality: the governance pillar

The cannabis industry’s complex relationship with the legal and regulatory environments is well documented. Since 2012, 19 states and Washington, DC have legalized recreational use of cannabis by adults; however, the product remains illegal at the federal level. Because of this, cannabis companies also have a unique relationship with the governance pillar of ESG.

From MGO’s perspective, until laws change at the federal level, businesses operating in the cannabis industry will need to prioritize each of the criteria in the governance pillar to navigate evolving risks and to ensure the long-term success of their companies.

The criteria in the governance pillar includes:

- management of the legal and regulatory environment,

- systemic risk management,

- competitive behavior,

- business ethics,

- critical incident risk management,

- tax transparency, and

- accounting policies and practices.

Opportunities in ESG

While many companies see ESG as a buzzword, integrating its concepts within the holistic business model is important to drive long-term value creation.

There are substantial competitive advantages — including employee acquisition and retention, reducing the cost and environmental impact of operations, and reducing the cost of capital (JP Morgan: ESG integration – building more resilient portfolios for the long term).

Like-minded companies can and are teaming up to build brand partnerships, adding to product lines with collaborations, and developing innovative ideas for the entire industry to benefit from.

Incorporating ESG into your cannabis company means taking a holistic look at where you currently stand — and then driving the necessary change across the entire organization and value chain.

Steps for developing an ESG strategy

Here are a few of the steps companies can take to get started with their ESG program:

- Perform an ESG program assessment for your business: determine what’s important (i.e., material) to your investors, employees, and communities, along with the gaps requiring your attention.

- Prioritize your material topics grounded in risk and opportunity: recognize that with opportunity comes risk — and you need to be prepared for both when focusing on value creation.

- Establish a go-forward strategy focused on your gaps to drive the most impact: Is your company growing and in need of financial statement and/or tax preparation? Is there a specific way you can lobby for legislation, or partner with another company to help minority or women-owned businesses thrive as part of a social initiative? Create a program that invests in and bolsters the community?

- Reporting ESG metrics, KPIs, and progress against commitments to investors and/or the board of directors: Keep everyone in the loop, especially those who want to see you succeed;

- Leveraging leading ESG frameworks and standards: A robust ESG framework will lay out the necessary programs, capabilities, processes, policies, procedures, and essential initiatives to accompany your go forward ESG strategy.

Looking ahead

Whether you have an ESG program in place, or you are looking to get started, the definition of value is evolving and cannabis organizations that keep pace are primed for long-term success.

If you are interested in learning more, schedule a conversation with our ESG team today.

]]>- The SEC has proposed new regulations regarding climate-related disclosures, which impact reporting for public registrants.

- The proposed rules will involve calculating and reporting Scope 1,2, and 3 greenhouse gas emissions.

- If these proposed SEC guidelines are enacted, privately held companies that are contracted suppliers or vendors to public companies will have to report GHG data as part of their Scope 3 calculations.

In March 2022, the U.S. Securities and Exchange Commission (SEC) proposed new regulations specific to climate-related disclosures which would impact reporting obligations for public registrants. A key component of the proposed rules (refer to pages 41-45 of the 506 page proposal for the analysis) involves calculating and reporting Scope 1, 2, and 3 greenhouse gas (GHG) emissions.

For anyone unfamiliar with the concept of Scope 1, 2, and 3 GHG emissions, our Environmental, Social and Governance (ESG) practice breaks down what they are, why they are important, and what you can do to start inventorying, measuring, and ultimately reducing your company’s emissions impact.

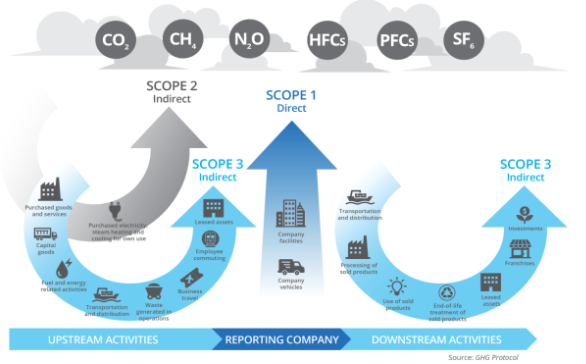

Understanding the difference between Scope 1, 2 and 3 GHGs

In order to define Scope 1, 2, and 3 emissions, companies must first look to the most common standards and frameworks.

For example, while the International Organization for Standardization (ISO) has provided a general set of standards (through ISO 14064); however, the Greenhouse Gas Protocol (GHG Protocol) has emerged to provide “accounting and reporting standards, sector guidance, calculation tools and trainings for businesses and local and national governments” and has “created a comprehensive, global, standardized framework for measuring and managing emissions from private and public sector operations, value chains, products, cities and policies to enable greenhouse gas reductions across the board.”

Further, the SEC notes on page 34 of their proposed rule, that the GHG Protocol “has become a leading accounting and reporting standard for greenhouse gas [GHG] emissions” with “concepts and a vocabulary that are commonly used by companies when providing climate-related disclosures.”

As such, the SEC has grounded the proposed rules in line with the following definitions established by the GHG Protocol:

Scope 1 GHG Emissions:

Direct emissions that occur from sources owned or controlled by the company – such as fuel combustion from buildings, vehicles, machinery, and other equipment.

Scope 2 GHG Emissions:

Indirect emissions resulting from the generation of electricity purchased and used by the company (derived from the activities of the power provider). This includes purchased electricity, heat, steam, and cooling.

Scope 3 GHG Emissions:

All other indirect emissions which are not captured in the Scope 2 category. Scope 3 emissions are generated as a result of a company’s value chain but are not directly owned or managed by the company. For example:

- Upstream emissions include but are not limited to goods and services purchased from vendors and suppliers; upstream transportation and distribution; business travel; and employee commuting.

- Downstream emissions include but are not limited to transportation and distribution to customers; the processing of sold products; the use of sold products; sold products’ the end-of-life treatment; and investments.

Given the scope and scale, Scope 3 emissions are significantly more complex and time consuming to inventory, calculate, track, and manage compared to both Scope 1 and Scope 2 emissions.

Why measuring greenhouse gas emissions is important

The SEC’s proposed rule has its most immediate impact on public companies; however, private companies that operate in the value chain for public companies impacted by the proposal need to consider their own GHG emissions calculations.

For example, if the SEC guidelines are put in place and include Scope 3 reporting requirements as currently written (i.e., based on materiality or linkage to commitments), privately held companies that are contracted suppliers or vendors to public companies impacted by the proposed rule are likely to receive recurring requests (i.e., at least annually) for complete, accurate, and timely GHG data, which the public company will include as part of their upstream Scope 3 calculation.

As such, an inability to furnish complete, accurate, and timely GHG data may become a barrier for entry to becoming a supplier or vendor to certain public registrants.

Attestation of GHG reporting

With the SEC’s proposed climate-related disclosure rules, GHG emission information will need to be validated through third-party attestation.

Per the proposed rule, the attestation requirements for GHG emissions metrics would:

- Pertain to Scope 1 and Scope 2 only (i.e., any Scope 3 disclosures would not be subject to the attestation requirement and would be protected through a safe harbor provision)

- Impact large accelerated and accelerated filers only (i.e., non-accelerated and/or smaller reporting companies [SRCs] would not be required to comply with the attestation requirements)

- Define a set of minimum attestation report requirements, including acceptable attestation frameworks

- Include a phase-in period with a compliance date dependent on the registrant’s filing status

It should be noted that the proposed rule also allows impacted registrants to transition into the reasonable assurance attestation requirement by initially subjecting the new GHG emissions disclosures to a limited assurance review. Both reasonable and limited assurance engagement and reporting requirements are defined at length by various organizations (including the AICPA); however, impacted registrants need to understand that a limited assurance review is considered “substantially less in scope” than an examination performed under reasonable assurance (i.e., impacted registrants need to ensure they are taking appropriate steps to ensure that their GHG emissions disclosures are robust, in all material respects).

Greenhouse Gas strategy for state and local governments

Measuring Scope 1, 2, and 3 GHG emissions is not only applicable for businesses — leaders of state and local government institutions are also under growing pressure to inventory, measure, and disclose ESG-related metrics and key performance indicators (KPIs), including GHG emissions disclosures.

As a result, the GHG Protocol has also developed an accounting and reporting standard for cities.

MGO’s perspective

Regardless of your ESG program’s maturity, the definition of value is evolving, and organizations that keep pace are primed for long-term success. If you are interested in inventorying, measuring, and reporting Scope 1, 2, and 3 GHG emissions, contact us to get started.

For insights tailored to your company and industry, schedule a conversation with our ESG team today.

]]>- The SEC has issued a proposal requiring companies to disclose information about corporations’ climate change risks within their filings.

- This proposal includes new requirements for qualitative and quantitative disclosures, attestations, and audit reporting requirements for Scope 1 and 2 Greenhouse Gas emissions.

- The SEC’s goal in creating this new proposal is to drive greater transparency from registrants to protect investors and solidify climate-related disclosures as required reporting.

On March 21, 2022, the U.S. Securities and Exchange Commission (SEC) issued a proposed rule that would require registrants to include climate-related disclosures within registration statements and annual reports (including Form 10-K). According to SEC Chair Gary Gensler, the rule is intended to promote transparency and protect investors, providing them with “consistent, comparable, and useful information for making their investment decisions.”

With a 3-1 passing vote, the SEC’s formal proposal has now opened a public comment period which seeks responses from the impacted companies, accounting firms, and the public at large (note the comment period will end on May 20, 2022, or 30 days following the publication in the Federal Register, whichever is later).

While updates to the proposed regulations are likely to follow the closure of the comment period, it is already evident that mandatory climate-related disclosures are close. Further, given the complexity of the proposal, it is apparent that registrants will experience increased costs driven by new governance and reporting requirements – and these costs could extend through the registrant’s entire value chain (including upstream suppliers and downstream customers).

MGO’s Environmental, Social and Governance (ESG) practice has inspected the proposed rules and provides a summary and contextual overview in the following paragraphs.

Note: The complete, 506-page SEC proposal is viewable here, while a 3-page summary fact sheet is viewable here.

SEC proposed climate disclosure requirements

Through its independent research of 6,644 annual filings, the SEC found that many companies were already disclosing both qualitative and quantitative metrics related to climate change (i.e., on a voluntary basis). Additionally, the SEC found that a subset of those companies was doing so in line with two of the most common frameworks and standards:

- Task Force on Climate-Related Financial Disclosures (TCFD) – The framework primarily used by companies that make qualitative, climate-related disclosures around governance, strategy, and risk management as well as certain quantitative disclosures (i.e., the metrics and targets used by a company to measure and assess climate risks, opportunities, and targets)

- Greenhouse Gas Protocol – The standardized framework used by most organizations to inventory, calculate, and manage greenhouse gas (GHG) emissions (i.e., the quantitative disclosures commonly referred to as Scope 1, Scope 2, and Scope 3 GHG emissions)

At the highest level, the proposal’s new disclosure requirements include:

- New qualitative disclosures (under Regulation S-K) in a separate, captioned section of the annual filing, including but not limited to descriptions of:

- The governance of climate-related risks (e.g., board and management oversight)

- Material climate-related impacts on strategy, business model, and outlook

- Approaches to climate-related risk management

- GHG emissions metrics (e.g., Scope 1, Scope 2, and potentially Scope 3 emissions)

- Climate-related targets and goals, if any (e.g., net-zero commitments)

- Usage of an internal carbon price and how this price was determined

- New quantitative disclosures (under Regulation S-X) included as a note within the audited financial statements, including:

- Disaggregated information about the climate-related impacts, events, and transition activities to existing financial statement line items (FSLIs) above a certain threshold (e.g., increases to reserves, impairment charges, expenditures specific to transition activities, etc.)

- Incremental attestation and audit requirements

- Scope 1 and Scope 2 GHG emissions disclosures (under Regulation S-K) would be subject to an attestation requirement; however, the disclosures would initially be subject to an audit under the limited assurance standard and followed by an audit under the reasonable assurance standard two years later

- Climate-related impacts, events, transition activities, etc. to existing FSLIs would be subject to existing audit requirements (i.e., consistent with procedures performed over historical financial statement footnotes, including internal controls over financial reporting [or ICFR])

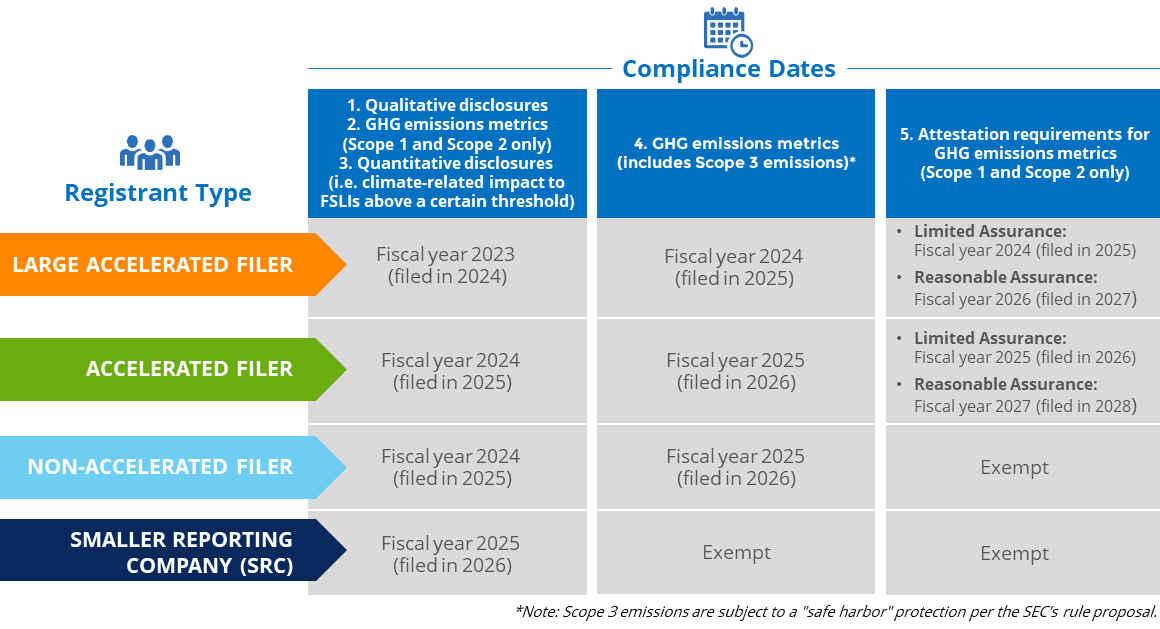

When would the proposed climate-disclosure updates go into effect?

Under the proposed rule (which is subject to change after the comment period), domestic and foreign registrants would be required to adhere to the following phase-in timelines:

MGO’s perspective

Through our experience to date, and corroborated through the review of the SEC’s analysis of 6,644 annual filings (refer to pages 311-320 of the 506 page proposal for the analysis), many registrants across all industries are already voluntarily disclosing climate-related information. However, for the companies that have not yet moved to establish climate-related governance, evaluate their existing business strategies, analyze the emerging risks, or inventory the data required for climate-related metrics, the compliance effort is expected to be considerable.

In the end, the SEC’s goal with the proposed rule appears to be two-fold:

- The first is to drive transparency from registrants to protect investors. As many issuers already disclose climate-related information voluntarily, standardizing the requirements will provide more comparable information while reducing compliance costs in the long run

- The second is a recognition that climate-related disclosures are not only here to stay but set to grow in importance in the coming decades. Given that anticipated growth, the SEC’s proposal will ensure the US regulatory environment is able to keep pace — especially with its international counterparts

Regardless of your company’s current maturity as it relates to climate governance, strategy, risk assessment, and disclosure, the time to act is now. Rule proposals of this scale and complexity from the SEC are infrequent, and with international regulators looking to adopt their own sustainability disclosure requirements (see the IFRS Foundation’s Sustainability Disclosure Standards draft released on March 31, 2022), we expect the path to compliance will be long and ambiguous for many.

Lastly, while the proposal is intended for public registrants, we believe that private companies also need to begin to mobilize. As an example, if a private company operates as a vendor or supplier for a Large Accelerated filer with Scope 3 emission reporting ambitions, the privately held vendor or supplier can expect that Large Accelerated filer to request timely and quality Scope 1 and/or Scope 2 GHG data to serve as an input into the filer’s Scope 3 calculation (inclusive of questions around the completeness and accuracy of data).

Questions to consider about the SEC’s proposed ESG ruling

- Who is responsible for governance and oversight (at both the board and management level) of climate-related risks and opportunities?

- Which climate-related frameworks and/or standards has the company considered adopting or are already following for existing disclosures?

- Are existing qualitative and quantitative climate-related disclosures robust (i.e., considered investor-grade)?

- Are there sufficient processes and controls in place to ensure climate-related disclosures are complete, accurate, and timely?

- Is a communication plan in place to make employees aware of climate-related risks, opportunities, commitments, and progress?

- Does the board understand why ESG-related information (which is broader than the information in the climate-disclosure proposal) is important to investors and other stakeholders?

Regardless of your ESG program’s maturity, the definition of value is evolving, and organizations that evolve with it are primed for long-term success.

For insights tailored to your company and industry, schedule a conversation with our ESG team today.

]]>- Expectations around sustainability and corporate social responsibility are becoming increasingly ubiquitous in the lives of customers, employees, and investors.

- Traditional private equity (PE) houses are increasingly considering ESG risks and incorporating opportunities for value creation across the due diligence and investment cycles.

- While the focus on specific ESG activities varies, there is a growing consensus that a structured approach to risk assessment and reporting is necessary to both create new value and protect existing value.

Private equity sees value in ESG

The private equity industry continues to push through the ambiguity surrounding ESG criteria to navigate risks and discover opportunities to increase investment returns. While many traditional PE houses are taking the “wait and see” approach, those that are proactive about integrating ESG considerations into their due diligence and investment cycles are being rewarded.

Regardless of the approach, the confluence of risk mitigation, opportunities for growth, expected regulation, and customer demand make it clear that ESG will be playing a critical role in short- and long-term value creation.

ESG: The shift from “nice” to “need.”

Private and public companies alike have been taking stock of their ESG risks and ramping up their ESG strategies for some time. What was once considered a “nice to have” has become table stakes for companies of all shapes and sizes looking to meet shifting stakeholder demands. Therefore, the most progressive private equity firms have incorporated ESG considerations (i.e., risks and opportunities) throughout all aspects of the investment lifecycle (i.e., due diligence, investment, exit). As “The Expanding Case for ESG in Private Equity” report from Bain & Company highlights:

“Firms recognize that consumers, regulators, employees, and sources of capital are energized by the notion that investors can and should use their economic clout to address the many existential crises we face as a society. Each of these groups is ramping up demands for change and, in many cases, rewarding it.”

While it’s clear that stakeholder demand is embedding ESG criteria into the investment lifecycle, there is still uncertainty surrounding how to measure and monitor ESG risk exposure and opportunities for growth.

Navigating ESG risks and developing new opportunities

A company’s ability to “tell its ESG story” has become synonymous with measuring ESG program maturity. Furthermore, the ability to take traditional business models and drive them towards sustainability-focused principles has been seen to unlock new business opportunities and create long-term value (i.e., loyalty) from consumers. This is especially true for the youngest consumers entering the period of their lives where they will have the most spending power.

To measure risk and develop new opportunities, PE firms are driving portfolio companies to:

- Identify or reassess priority ESG criteria (i.e., those which carry the highest impact for their industry); and

- Establish goals that can be measured and reported to internal and external stakeholders.

To accomplish this, an organization should adopt a structured approach that follows the most common frameworks and standards. Specifically, companies can increase the quality of their ESG program by adopting the most common standards and frameworks (e.g., Sustainability Accounting Standards Board (SASB) or Task Force on Climate-Related Financial Disclosures (TCFD)).

With a structured approach and quality reporting mechanisms, PE firms can continue to integrate ESG elements into portfolio companies throughout the investment lifecycle. By adhering to the most common standards, portfolio companies will be well positioned to comply with expected global regulatory changes.

Building and strengthening your ESG story

Whether you’re an acquisition target company or an established private equity house, a clear ESG strategy is needed to address shifting stakeholder demands. PE firms that have embraced the development of ESG strategies for themselves as well as their portfolio companies are poised to benefit from the changes on the horizon being driven by both stakeholders, customers, and regulation.

ESG’s value proposition may be clear, but a few questions remain as firms embrace ESG principles and build out their programs:

- Are your ESG strategy and expectations clear for your firm, portfolio companies, and investment targets?

- How have you integrated ESG into your value transformation processes for your portfolio companies?

- Does your ESG story convey a mature ESG program?

- By understanding where you are today in the ESG realm, you may be able to embrace the opportunities that are quickly developing.

If you are interested in learning more, schedule a conversation with our ESG team today.

]]>Bottom line:

- Expect more net zero commitments and specific strategies to achieve the goals

- Scrutiny of the data supporting for ESG commitments and metrics will increase

- Regulatory guidance will be released to chart a path forward for non-financial reporting

The evolution of ESG

In 2020 we saw the concept of ESG go mainstream — specifically it was the year where the value of having a strong ESG-centric strategy became clear in the minds of leadership teams, investors and the public at large. In response, companies of all shapes and sizes strengthened their existing sustainability and corporate responsibility programs to consider more aspects of the value chain.

In January 2021, when the United States rejoined the Paris climate agreement, the number of companies and local governments committing to net zero emission targets by 2050 began to skyrocket. Further, regulatory bodies in the United States began to signal that non-financial disclosure requirements would be coming — likely starting with public issuers and focused on greenhouse gas emissions, diversity, equity and inclusion, and cybersecurity.

So as we enter 2022, what’s in store?

Continued focus on ESG reporting

Most of the world’s largest companies now set ESG-related targets and issue a report with ESG metrics, targets and disclosures. The expectation among consumers and investors is that small and medium-sized companies will continue to build out their ESG strategies and reporting capabilities to meet stakeholder demands.

ESG reporting also continues to evolve. Companies use two primary approaches: standalone reporting (i.e., creating a standalone ESG or impact report) and integrated reporting (i.e., leveraging existing mechanisms, such as a 10K, to disclose non-financial information).

Regardless of which reporting option you choose, one thing is clear: the qualitative and quantitative data needs to be complete, accurate and timely. Companies and governments need to begin upgrading their reporting. They must update existing policies, build out a robust process and control framework and begin to engage internal and external audit functions to assure the integrity of the non-financial information disclosed.

Net zero commitments influence strategies

When the United States rejoined the Paris climate agreement, it signaled a shift in the country’s approach to climate change (as detailed in the November 2021 release of The Long-Term Strategy of the United States, Pathways to Net-Zero Greenhouse Gas Emissions by 2050). The strategy is ambitious and concrete, and it will drive many companies to change how they do business. It will also require state and local governments to implement new approaches and incentives to get communities onboard.

To meet these net zero commitments, we expect the purchase of alternative energy options (i.e., solar) to increase. Further, there will be an increase in carbon offset investments — driven by companies and governments entering the market to buy and sell carbon credits.

Scrutiny moving to regulation

Currently businesses aren’t required to report metrics on greenhouse gas emissions, workforce diversity or governance – but stakeholders continue to seek this type of non-financial information. In response, the SEC has signaled that regulation is coming in 2022 (WSJ: SEC Under Pressure to Implement Agenda in 2022).

Specifically, public issuers can expect clear guidance to enhance their non-financial disclosures related to:

- Climate risks (e.g., consideration of physical and transition risks as well as greenhouse gas emissions and targets)

- Human capital (e.g., board and executive committee diversity)

- Cybersecurity risks

Be proactive

A lot has changed in a short time, and as with any period of rapid change, there are more questions than answers. How do companies proactively prepare for the expectations connected to their ESG programs? What types of regulation and compliance requirements are coming first? How do companies make net-zero commitments if they don’t have an established ESG program?

It’s productive to ask hard questions, because ESG is here to stay. Investors are ready to use these new tools to help direct their capital. Stakeholders are especially attuned to environmental and social issues when making their strategic decisions. And reporting and compliance is coming fast.

Perhaps the first question to answer is: Where do we start?

If you are interested in learning more, schedule a conversation with our ESG team today.

]]>