- The Internal Revenue Service (IRS) instituted a moratorium on the processing of new Employee Retention Tax Credit (ERTC) claims due to an influx of fraudulent and exaggerated claims — primarily stemming from unscrupulous ERTC mills.

- As of July 31, 2023, the IRS Criminal Investigation division had initiated 252 investigations involving more than $2.8 billion in potentially fraudulent ERTC claims. Fifteen investigations have resulted in federal charges, with six of those resulting in convictions with an average sentence of 21 months.

- Taxpayers who are not certain of their eligibility should consult with a trusted tax professional for a second review and may want to avail themselves of the IRS’s new settlement and/or withdrawal programs.

The IRS recently took a drastic step to impede a wave of ineligible ERTC claims by halting the processing of new refund requests through at least December 31, 2023.

Ineligible ERTC claims have plagued the IRS since Congress enacted the credit in 2020. In fact, the IRS opened its 2023 “Dirty Dozen” list with warnings about common ERTC scams that taxpayers should be wary of. This prominently placed notice — as well as subsequent announcements from the IRS — alerted taxpayers to unscrupulous actors who have been advising employers to claim credits in excess of what they could legitimately qualify for while charging those employers hefty upfront fees or fees contingent on ERTC refunds.

In the wake of a flurry of IRS investigations that identified more than $2.8 billion potentially fraudulent claims, the halt on processing ERTC claims will allow the IRS to further focus their efforts on investigating and ultimately prosecuting fraudulent claims. In the following we’ll detail the impact of the IRS moratorium and provide guidance if you suspect you’ve been exposed to inaccurate or fraudulent ERTC claims.

Background on the ERTC

First established in 2020 by the Coronavirus Aid, Relief, and Economic Security (CARES) Act, the employee retention tax credit was critical — along with Paycheck Protection Program (PPP) — in giving businesses that struggled to navigate the pandemic’s challenges much needed resources to pay employees while the businesses were shut down or facing declining sales.

For most taxpayers, the ERTC was claimed on quarterly payroll tax returns encompassing the period March 13, 2020, through September 30, 2021 (i.e., first quarter of 2020 through the third quarter of 2021). For a small subset of businesses classified as “recovery startup businesses” (as defined below), the ERTC could also be claimed for the fourth quarter of 2021.

Despite the halt in processing by the IRS, eligible taxpayers are still able to claim the credit by filing amended quarterly payroll tax returns. Amended payroll tax returns for 2020 quarters are able to be processed by the IRS as long as they are filed on or before April 15, 2024, while amended payroll tax returns for 2021 quarters are able to be processed as long as they are filed on or before April 15, 2025.

The credit is calculated based on the “qualified wages” of employees. The maximum amount of payroll tax credit that an employer can claim per employee is $26,000.

Qualification Tests

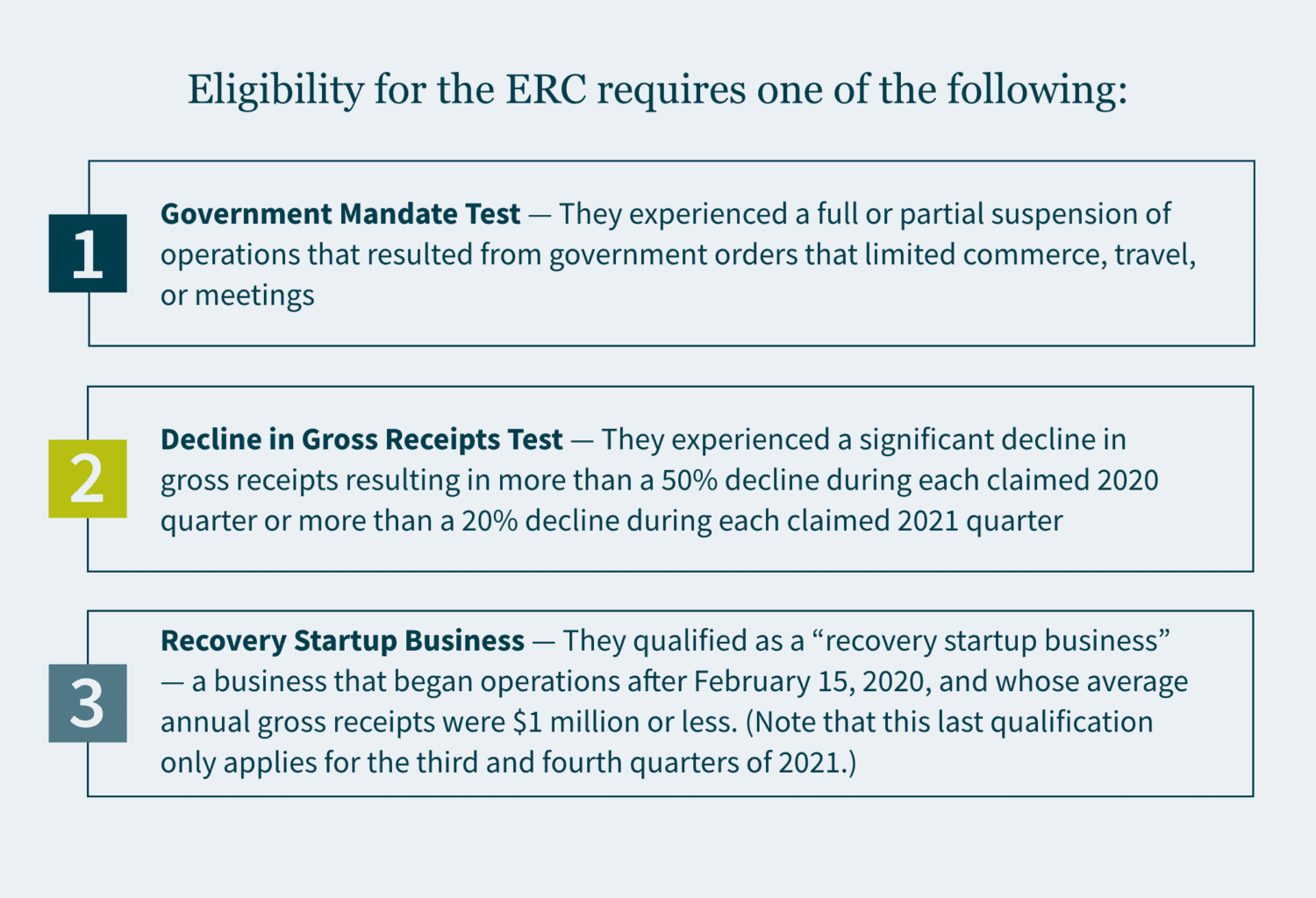

To be eligible for the ERTC, businesses must generally satisfy one of the following criteria for each of the quarters for which they are claiming the credit:

- Government Mandate Test — They experienced a full or partial suspension of operations that resulted from government orders that limited commerce, travel, or meetings.

- Decline in Gross Receipts Test — They experienced a significant decline in gross receipts resulting in more than a 50% decline during each claimed 2020 quarter or more than a 20% decline during each claimed 2021 quarter.

- Recovery Startup Business — They qualified as a “recovery startup business” — a business that began operations after February 15, 2020, and whose average annual gross receipts were $1 million or less. (Note that this last qualification only applies for the third and fourth quarters of 2021.)

The IRS Processing Moratorium

On September 14, 2023, the IRS announced that it would halt the processing of new ERTC claims through at least December 31, 2023. The IRS also stated that it plans to subject its queue of more than 600,000 existing ERTC claims to stricter compliance reviews, increasing the standard processing goal for those claims from 90 days to 180 days — with a potential for a much longer processing time for claims that require further review or audit.

This processing moratorium comes on the heels of a significant influx of claims – many of which the IRS believes are ineligible. The IRS stated that it has received more than 3.6 million ERTC claims over the life of the ERTC program, with about 15% of those claims being received in the 90-day period preceding the processing freeze. This amounts to roughly 50,000 claims still being received a week. To put this in perspective: the IRS has paid out about triple the amount that Congress had originally estimated for the program.

Additionally, as of July 31, 2023, the IRS Criminal Investigation division had initiated 252 investigations involving more than $2.8 billion in potentially fraudulent ERTC claims. Fifteen of the 252 investigations had resulted in federal charges, with six of those resulting in convictions. Four of the six convictions had reached the sentencing phase with an average sentence being 21 months.

The IRS intends on utilizing the moratorium to add more safeguards to the processing of ERTC claims, to protect businesses by decreasing the momentum of the pop-up ERTC mill industry, and to provide several solutions for taxpayers who submitted invalid claims. Those solutions include:

- A claim withdrawal program will be rolled out in Fall 2023 allowing businesses to withdraw ERTC claims that have not been processed or paid, even if those claims are under audit or awaiting audit.

- A claim settlement program rolling out in Fall 2023 that will allow businesses to repay ERTC claims, while also avoiding penalties and future compliance actions. (Note that fraudulent claims may still be subject to criminal referral.)

How to respond to IRS scrutiny of ERTC claims

Given the expected extra scrutiny that businesses can expect to face on their claims, businesses should review ERTC claims that they have made and/or intend to make where there are any doubts regarding the eligibility of those claims:

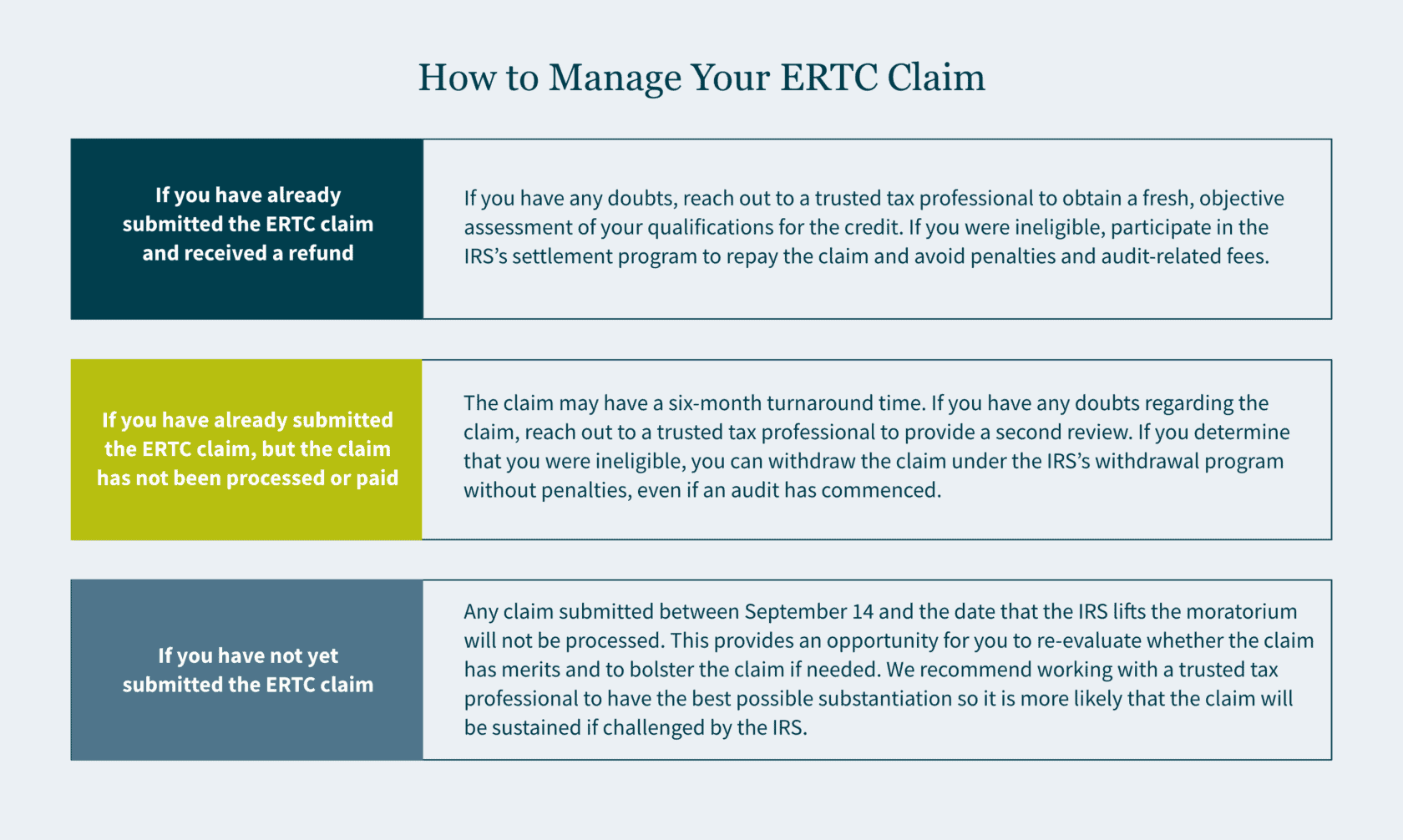

- If you have already submitted the ERTC claim and received a refund: If you have any doubts regarding your eligibility, we recommend reaching out to a trusted tax professional to obtain a fresh, objective assessment of your qualifications for the credit. If you determine that you were ineligible, you can participate in the IRS’s settlement program so that you can repay the claim, avoiding both penalties and audit-related fees.

- If you have already submitted the ERTC claim, but the claim has not been processed or paid: The claim will take longer to process than during the summer — increasing from a three-month turnaround time to a likely six-month turnaround time. If you have any doubts regarding the claim during this period, we recommend reaching out to a trusted tax professional to have a second review of the claim. If you determine that you were ineligible, you can withdraw the claim under the IRS’s withdrawal program without penalties, even if an audit has commenced.

- If you have not yet submitted the ERTC claim: Any claim submitted between September 14 and the date that the IRS lifts the moratorium – currently after December 31, 2023 – will not be processed. This should provide an opportunity for you to re-evaluate whether the claim has merits and to bolster the claim if needed. We recommend working with a trusted tax professional to have the best possible substantiation for your claim so that it is more likely that the claim will be sustained if challenged by the IRS.

How MGO can help

MGO’s ERTC Second Look program is geared towards the types of objective, trustworthy reviews that would benefit you during this time of heightened ERTC claim scrutiny. Our experienced Credits & Incentives team can identify audit red flags, areas that need more substantiation, miscalculations, and incomplete filings. In addition, our Tax Controversy team — in tandem with our Credits & Incentives team — can defend you if any of your ERTC claims are challenged by the IRS, with the ability to represent you during audit, appeals, and tax court. Contact us to learn more.

]]>- Contract negotiations during the planning phase are essential to securing appropriate financial outcomes

- Think carefully about production expenses, which can cut into potential profits

- Plan your travel route efficiently to cut down on transportation overhead

- Maximize the various opportunities to monetize content and merchandise

Our clients who are musical artists are excited to get back on the road now that COVID-19 event restrictions are largely lifted. Their passion for music, their connection with the fans, the irreplaceable energy of commanding a big stage in a packed arena are driving forces, but on the practical side, so is the revenue.

While music venues are open for business, the impact of COVID-19 can still be felt in conditions and requirements around events that can have a financial impact. In many instances, artists may be willing to jump at contract offers that could limit the financial benefits they could have otherwise realized.

As the Entertainment, Sports and Media Industry Leader, I have been on your side of the desk. I am not only a CPA, but for 15 years I was manager of a certified Diamond and 11-times Platinum, six-time Grammy Award winning hip-hop group. I have managed several other culture-defining artists, as well as partnered with artists, and their agents, managers, tour managers, lawyers, labels, crews, and families to help them secure favorable contracts for innumerable tours.

These are four things I most often advise our clients to keep in mind to maximize their profits when planning a tour.

#1 Be smart with your contract

Decide your rate per show ONLY after thinking through as many factors as you can. Without guidance, artists can get caught up in the excitement of tour planning, and get offered a certain amount per show that may not cover all of the overhead. We partner with artists and management, and layout typical hard costs and considerations, so you know what it will take to make the tour happen, and still get the kind of monetary return you are looking for. Factors such as set design, shipping and transportation, set construction, crew transportation, insurance, personnel, all of these elements need to be taken into account.

Knowledge is power in negotiations. Our process is to arm our clients with first-hand knowledge of the touring process and insights we have gained through the countless negotiations we’ve done on behalf of other artists.

#2 Think through your production expenses

The scope of the show and the set design has a direct impact on the profitability of your tour. The creative vision needs to be balanced with actual hard costs. The size of the set and the scale of the show will directly affect the equipment needed for set transport, the number of people needed to set up the stage, the number of dancers, tour managers, a band, audio engineers, lighting engineers, the required production staffing, security teams, the number of trucks, busses, etc. Additionally, for multi-city tours, budgets to transport and house the sets along the route also need to be allocated.

We work with our clients to provide an informed understanding of upfront planning so that you see all the factors and can identify areas to streamline. One of our best practice solutions is to hire multi-discipline specialists who can fulfill several jobs. This saves money on flights, hotels, per diems, and salaries.

Taxes and payroll are a factor to keep in mind, as are passports for all staff members if you are planning to include an international leg of your tour. There may additional fees that are crucial to budgeting, related to visas/passport fees and taxes and tariffs for each city, state, and country. We can provide Tour Accountant Services to manage the ins and outs of these details so you and your Tour Management Team can focus on what you do best.

#3 Map out your transportation

Managing tour transportation is critical for success and maximizing your profits. There are a lot of moving parts that require consideration. Before announcing tour dates and locations, focus on your tour route. For example, consider where you are located. If you’re on the east coast, it might make more sense to start there, work your way down, take a break, and then fly directly to the west coast, where it’ll be the most profitable. What about where your set is being built? If it is in Los Angeles, for instance, it will be far easier and cheaper to start there so you won’t have to pay to fly it all out initially. The size of your set and show will impact the number of trucks and busses, and/or air transportation elements that will need to be factored in.

Ultimately, you will need to determine the most cost-effective route for you. Start by locking in gig dates that you know are inflexible, like large music festivals, and work around them. Choosing an efficient route will not only ensure you’re seeing as many of your fans as you can, but you’ll also be doing so in a way that your tour will yield the best most profitable returns.

Transportation can have huge cost implications. Planned flights are much more efficient than last minute travel. Commercial flights are more affordable than private jets. Tour busses can be rented short term or leased long term and wrapped for marketing impact for a cohesive branding look. The more you plan ahead, the better you can manage your costs and the more profits you can retain from your tour.

#4 Your tour can have multiple lives

Every step of your tour: the struggles, the victories, the comic moments, the behind-the-scenes (BTS) life, your hopes, your thoughts on what it will mean to be back with your fans, and of course every on-stage performance … all of it is content with monetary value.

The life you will be living on tour is one your fans only dream of and you can bring them into that space. From potential specials that can be sold to streaming services like Netflix, to exclusive BTS content that can be on your website or packaged as part of marketing partnerships with companies who could potentially offer footage as video-on-demand, mobile content, and social media content.

Simultaneous streaming of concerts either in select cities on a certain date, in movie theaters, in the metaverse (i.e., Decentraland) or via Pay Per View, are areas that can be leveraged for profit.

All of the footage can also be used in long and short form to build out your own band’s social media presence as well.

Onsite and online Merchandise sales are another revenue channel to recognize for potential profits. At $60-70 per sweatshirt, $30 a tee shirt and $20 a water bottle sold onsite or online, profits from these items can quickly add up.

With guidance from our team, you gain access to our broad eco-system of partners to help you realize these additional revenue streams while you get to focus on performing.

How we can help plan and manage a profitable tour

You’re sharing your passion on a global stage — going on tour should be exciting. Not to mention, touring is now one of the best ways you can bring in significant income, given you know how to properly plan ahead. Our Entertainment, Sports and Media team has extensive experience planning large-scale tours, managing expenses, optimizing revenue, and delivering the financial results you expect. Before going on the road again, reach out to our team for a consultation to avoid common issues that can undermine profitability.

About the author

Tony Smalls is the leader of our Entertainment, Sports, and Media (ESM) practice and helps culture-defining entertainers, athletes, and other high-net-worth individuals build and protect their wealth while maximizing growth opportunities in today’s fast-evolving media marketplace. He specializes in accounting, finance, tax strategy, financial planning, and analysis, financial reporting, and contract/deal negotiations, working heavily on prospective investments like live music tours.

]]>- There is still uncertainty about how to account for the refundable Employee Retention Credit in your books, because you can’t account for it the same way you can account for the Paycheck Protection Program loan.

- The standards you can choose from are FASB ASC 958-605, International Accounting Standard (IAS) 20, FASB ASC 450-30, and FASB ASC 832.

- Depending on the standard you choose, you might have to consider the timing of recognition, the presentation of a grant income line, and financial ratios.

The Paycheck Protection Program (PPP) and the Employee Retention Credit (ERC) were powerful economic stimulus programs instituted during the COVID-19 pandemic to provide financial relief to struggling businesses. Both programs were the first initiatives of their kind, and as a result, there remains some uncertainty about what standards apply when accounting for them in your financial statements and records.

If you’re wondering how to distinguish the two, as well as determine the standard you should be utilizing, Angel Naval, a leader in our Client Accounting Solutions practice, breaks it down.

The PPP versus the ERC

Created to aid businesses facing financial challenges through the pandemic, there are several key differences between the PPP and the ERC.

The PPP is a loan and was created for small businesses with less than 500 employees in mind, giving them the funds needed to cover payroll and other eligible expenses. This includes hiring back employees who were laid off and covering applicable overhead. The loans are forgiven if the proper criteria are met (I.e., maintaining payroll and keeping consistent employee numbers).

A subset of the PPP loan, the ERC is a refundable tax credit that allows businesses to reduce their tax liability based on the qualified wages they’ve paid to their employees during the pandemic. It was created for businesses of all sizes to capitalize on in order to avoid layoffs. They can claim up to $5,000 per employee in 2020 and $7,000 per employee per quarter in 2021.

Determining the appropriate accounting standard for ERCs

If you took advantage of the ERC, currently, there is no straightforward way of accounting for it. Put simply, the ERC is a gray area because it’s so new, and there isn’t a straightforward way of accounting for it. Plus, ERCs are payroll credits, not income tax credits — and while FASB has extensive guidance for accounting for income taxes in ASC 740, it doesn’t for payroll taxes. Even the American Institute of Certified Public Accountants (AICPA) has suggested different standards, so it’s up to you to apply your best judgement based on the facts and circumstances of your business. Some things to consider:

- The timing of recognition,

- The financial ratios important to you, and

- Whether you want to present a grant income line.

For income statement presentation, according to AICPA’s December 2022 report, more public entities are crediting the associated expense rather than recognizing the amounts on a separate line item.

For example, you may think you can account for the ERC the same way you can for the PPP, but you can’t. As we differentiated above, the PPP is a loan and the ERC is a payroll credit, therefore the PPP is subject to debt and liability standards and the ERC is not. While the PPP did come first, those companies that have paid payroll taxes but still qualified for the ERC are still able to retroactively claim the credit.

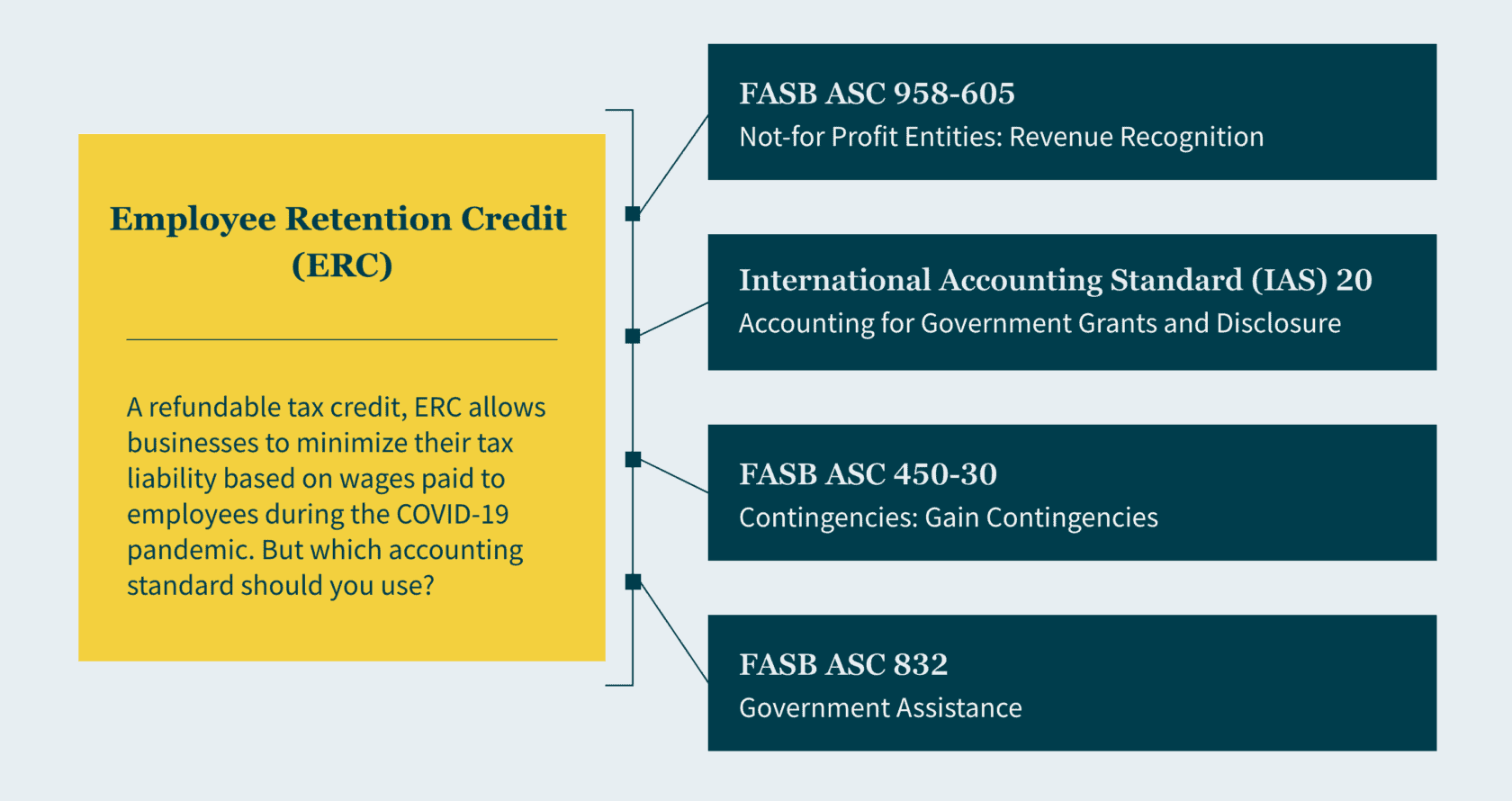

For prospective applications, for-profit entities can adhere to guidance in one of the following.

FASB ASC 958-605

If you’re applying the revenue recognition model under ASC 958-605, ERCs are treated as conditional contributions. In this case, companies must have met the program’s eligibility conditions to record revenue (and no amounts can be recorded until all criteria are evaluated and “substantially” met according to regulations). Given the conditions are met, a refund receivable and income should be recognized in the period the entity determines the conditions have been substantially met. This standard requires that gross revenue be recorded, and it doesn’t permit any netting of revenue against related expenses.

Some barriers to meeting ASC 958-605’s requirements include the eligibility requirements, like meeting the rules for a decline in gross receipts as well as incurring qualifying expenses (i.e., payroll costs). To file for the ERC, you’ll need to decide whether preparing the related ERC form and filing it with the government presents a barrier you’ll need to overcome. Note administrative and other small stipulations do not represent a barrier.

IAS 20

If you’re applying IAS 20, you can’t recognize the ERC until the “reasonable assurance” threshold is met in correlation with ERC’s conditions and receiving the credit. In this case, “reasonable assurance” translates to “probable” under GAAP standards and is easier to satisfy than “substantially met” in Subtopic 958-605. Once you’ve provided reasonable assurance that conditions will be met, the earnings impact of the government grants is recorded over the periods in which you recognize as expenses the related costs that the grants are intended to cover. So, you’ll need to estimate the amount of the credit you expect to keep.

IAS 20 allows you to record and present either the gross amount as other income or net the credit against other related payroll expenses. For every quarter that a company meets the recognition criteria, it records a receivable and either other income or net expense.

FASB ASC 450-30

If you’re interested in applying FASB ASC 450-30, please note amounts related to the ERC wouldn’t be recognized under this model until all uncertainties regarding the disposition of the credit are resolved — and there’s less detail on the disclosure, measurement, and recognition requirements as compared to the other standard models. For this reason, the AICPA doesn’t believe this model to be a preferred accounting policy for the ERC.

FASB ASC 832

If you’re applying this model, you must disclose several specifics about transactions with a government within its scope. These entail the nature of the transactions, which includes a description of the transactions as well as the form in which it has been received, whether it’s cash or other assets. You must also detail the accounting policies you used to account for the transactions. Any line items on the balance sheet and income statement that are affected by the transactions must be accounted for too — plus, the amounts applicable to each financial statement line item in the current reporting period.

How MGO can help

While there are clear accounting standards for the PPP, there is still some uncertainty surrounding the ERC. Depending on the standard you choose, you may have to consider the timing of recognition, financial ratios, and whether to present a grant income line. Therefore, businesses need to apply their best judgment based on the facts and circumstances of their business when accounting for ERCs. Our Client Accounting Solutions team has extensive experience helping clients navigate complex tax regulations post-pandemic. Contact us to learn more about which standard you should be using for federal relief programs.

About the author

Angel Naval oversees our West Coast Financial Advisory Services practice and provides value-added guidance for your corporate finance, financial planning, and business process needs.

]]>- A growing organization is a positive, but along with it usually comes increasingly complex financial accounting.

- Outsourcing provides businesses of all sizes with an opportunity to manage an array of issues — from staffing shortages or a lack of specific expertise to disorganized or unsecure financial records.

- Benefits of outsourcing include significant cost savings, direct access to specific accounting knowledge, the minimization of turnover, the ability to scale, access to tools and processes, and flexibility.

Many CEOs and business leaders are experiencing challenges in the aftermath of the COVID-19 pandemic, including changing customer trends, aggressive competition, emerging digital technologies, and the new normal of employee expectations for workplace flexibility.

These uncertain economic forces and cultural shifts are putting increased pressure on staffing for organizations of all sizes – especially fast-growing ones. While these difficulties are difficult to overcome, they are also an opportunity to change the “status quo” and level-up back-office performance.

For leaders navigating the uncertain tailwinds of the pandemic and planning to enter a new era of growth, outsourcing represents a powerful opportunity to address any staffing issues or business challenges. It empowers you to access specialized insight on a temporary basis, create value ahead of a major transaction, manage overhead costs, and modernize and revitalize business processes.

A recent study showed that 59% of all businesses utilize outsourced resources and that accounting is the most commonly outsourced function. So, how do you know if outsourcing your accounting function is right for your organization?

In this article we’ll look at five indicators that this strategy might be right for you and detail the key benefits to outsourcing or augmenting your accounting function.

Five signs your business may benefit from outsourced accounting

Here are some questions you should ask yourself to determine if your organization would benefit from outsourced accounting services:

- Is your business growing rapidly?

If you’re experiencing a significant influx of revenue, first off, great work! Your business model is proving out and you’re on the fast-track to success. But what is happening to your expenses, profitability and working capital? Depending on your answer it could mean that your accounting needs are evolving, the risks of a breakdown are higher, and overall, there is simply more at stake. It may be time to confirm that your current in-house team is qualified and staffed appropriately to handle these new responsibilities.

- Are you struggling to keep up with your accounts receivable or payroll?

One way to get a firm answer to whether your team is understaffed is if you’re missing key deadlines or struggling to get timely collection of cash from your accounts receivable. The inability to collect and follow-up on AR is essential to funding current and future growth and is directly connected to meeting your payroll commitments – one of the largest expenses of any business. If anything falls behind, you can find yourself in a difficult position if you do not have the ability to access cash or financing.

- Are your financial records organized and producing usable data?

Your accounting function does more than compliance, it should help guide your organization’s financial hygiene. Organized financials tell a clear story of earnings, spending, and investment, so you can make informed decisions. An over-worked or inexperienced accounting team will be working furiously to keep up with compliance and may not have the capacity, or necessary experience, to provide guidance on your financial scorecard to accrete value to the organization.

- Do your accounting needs fluctuate significantly throughout the year?

If your business experiences big shifts in labor productivity based on the calendar year and your taxes filings are late with significant overages from the tax preparers, or your audits have a significant number of adjustments, that may mean your accounting team lacks capability. Striking the right balance between hiring quality talent and the speed of bringing new hires up to date with company procedures can be a challenge. Outsourcing your team can deliver the resources you need, when you need them, and limit costs during the slower periods.

- Are you concerned about financial security and checks and balances?

If your internal accounting team is one or two individuals, you may be open to hidden risks. An independent team can provide the checks-and-balances that help mitigate the risk of fraud and asset misappropriation.

If you answered yes to any of these questions, you should consider outsourcing part or all of your accounting function. With an outsourced accounting team, you gain immediate access to trained, knowledgeable staff with the knowledge you need in technical accounting. The right outsourced resources can help your business grow faster and run more smoothly — often at a lower price than building an internal accounting department.

Benefits of outsourced accounting services

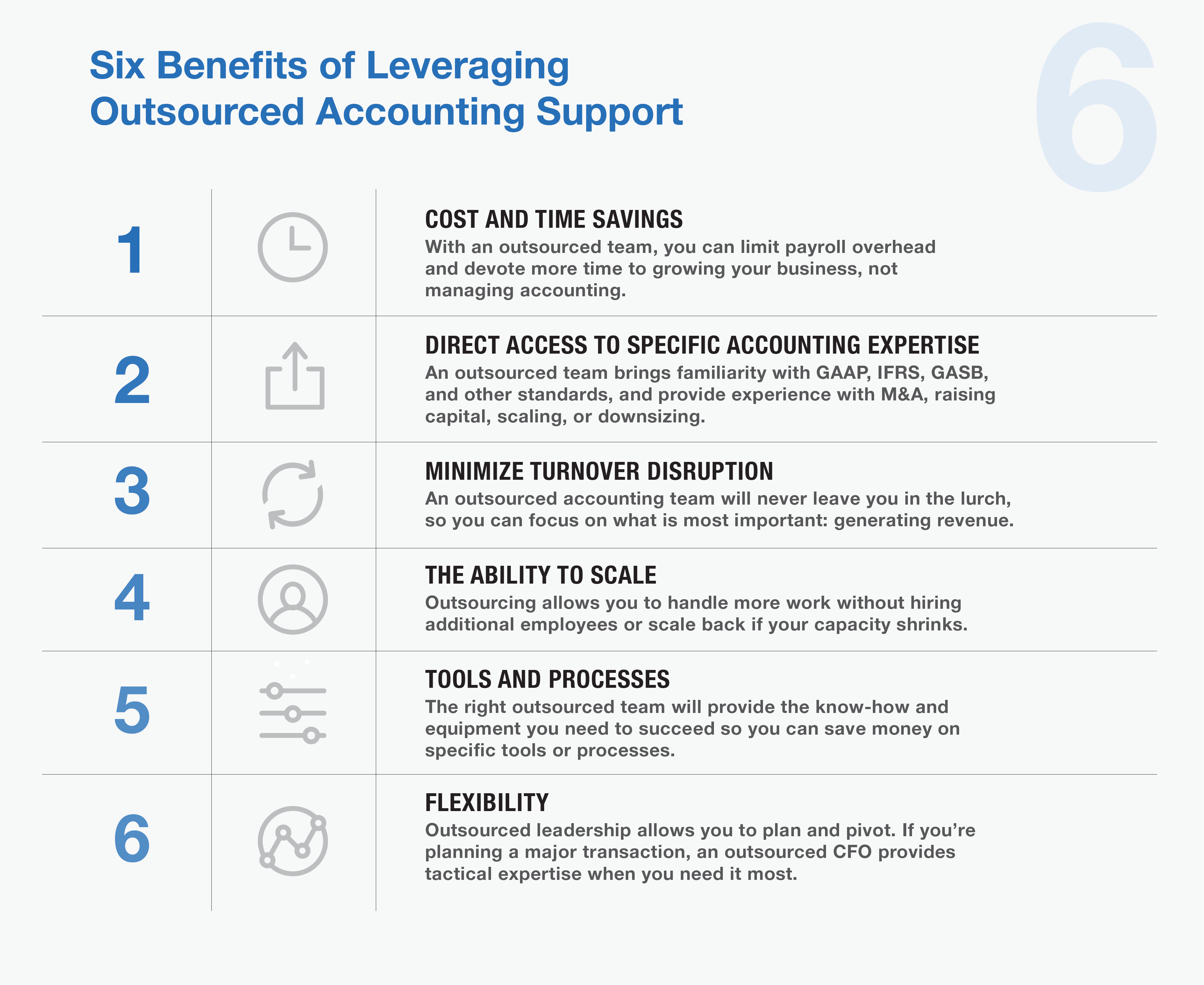

1.Cost and time savings

Maintaining full-time employees can be costly — and for most organizations, labor costs are some of the highest expenses. By relying on an outsourced team, you can devote your time to growing your business and spend less time managing accounting.

- Direct access to specific accounting expertise

Every company is different, which means every company’s needs are different. By outsourcing, you have access to the service you need when you need it. An outsourced team will bring familiarity with an array of accounting and reporting standards, including GAAP, IFRS, GASB, etc. Plus, they can provide specific experience with M&A transactions, raising capital, scaling, or downsizing operations.

- Minimize turnover disruption

In a smaller organization, each employee is vital to the business’s success. When you lose one, the disruption left in their wake can provide additional challenges. An outsourced accounting team will never leave you in the lurch, so you can focus on what is most important: generating revenue.

- The ability to scale

If your organization has grown quickly, you may experience growing pains when your fortunes suddenly shift. In boom times, you may need to hire more staff to meet demand. But that also means you may find yourself laying off employees in a downturn. Outsourcing allows you to handle more work without hiring additional employees or scale back if your capacity shrinks.

- Tools and processes

No matter what your organization’s size, you should always try to keep your overhead costs minimal. By outsourcing, you can save money on specific tools or processes you might otherwise need to function. The right outsourced team will provide the know-how and equipment you need to succeed.

- Flexibility

By outsourcing certain jobs, you can plan — and pivot, as needed — depending on your organization’s needs. This is especially relevant in the case of needing specialized guidance. If you’re planning a major transaction or other market move, an outsourced CFO can provide tactical expertise when and where you need it.

MGO can help

As your organization grows, your financial accounting needs become increasingly complex. Because your in-house accountants may be limited to handle the basics, outsourcing to professional teams with specialized knowledge and experience can provide precisely the kind of service you require — and give you the time you need to focus on the organization’s other needs.

MGO has a robust outsourced accounting team staffed by CPAs with diverse industry background and technical specialties. We’ll provide the right-size solution to your organization’s needs. Areas we support include day-to-day accounting tasks, complex financial systems projects, regulatory compliance demands, and support for M&A deals, raising capital, and other major transactions.

Whether you’re interested in simply augmenting your team with additional financial knowledge, or undertaking a complete accounting transformation, we can help you with the people, processes, and technology you need to move your business forward.

To explore your options and start along the path to organizational change, contact us.

]]>While it appears that several of the more disadvantageous provisions targeting businesses won’t make it into the final bill, others may. In addition, some temporary provisions are coming to an end, requiring businesses to take action before year end to capitalize on them. As Congress continues to negotiate the final bill, here are some areas where you could act now to reduce your business’s 2021 tax bill.

Research and experimentation

Section 174 research and experimental (R&E) expenditures generally refer to research and development costs in the experimental or laboratory sense. They include costs related to activities intended to uncover information that would eliminate uncertainty about the development or improvement of a product.

Currently, businesses can deduct R&E expenditures in the year they’re incurred or paid. Alternatively, they can capitalize and amortize the costs over at least five years. Software development costs also can be immediately expensed, amortized over five years from the date of completion or amortized over three years from the date the software is placed in service.

However, under the Tax Cuts and Jobs Act (TCJA), that tax treatment is scheduled to expire after 2021. Beginning next year, you can’t deduct R&E costs in the year incurred. Instead, you must amortize such expenses incurred in the United States over five years and expenses incurred outside the country over 15 years. In addition, the TCJA requires that software development costs be treated as Sec. 174 expenses.

The BBBA may include a provision that delays the capitalization and amortization requirements to 2026, but it’s far from a sure thing. You might consider accelerating research expenses into 2021 to maximize your deductions and reduce the amount you may need to begin to capitalize starting next year.

Income and expense timing

Accelerating expenses into the current tax year and deferring income until the next year is a tried-and-true tax reduction strategy for businesses that use cash-basis accounting. These businesses might, for example, delay billing until later in December than they usually do, stock up on supplies and expedite bonus payments.

But the strategy is advised only for businesses that expect to be in the same or a lower tax bracket the following year — and you may expect greater profits in 2022, as the pandemic hopefully winds down. If that’s the case, your deductions could be worth more next year, so you’d want to delay expenses, while accelerating your collection of income. Moreover, under some proposed provisions in the BBBA, certain businesses may find themselves facing higher tax rates in 2022.

For example, the BBBA may expand the net investment income tax (NIIT) to include active business income from pass-through businesses. The owners of pass-through businesses — who report their business income on their individual income tax returns — also could be subject to a new 5% “surtax” on modified adjusted gross income (MAGI) that exceeds $10 million, with an additional 3% on income of more than $25 million.

Capital assets

The traditional approach of making capital purchases before year-end remains effective for reducing taxes in 2021, bearing in mind the timing issues discussed above. Businesses can deduct 100% of the cost of new and used (subject to certain conditions) qualified property in the year the property is placed in service.

You can take advantage of this bonus depreciation by purchasing computer systems, software, vehicles, machinery, equipment and office furniture, among other items. Bonus depreciation also is available for qualified improvement property (generally, interior improvements to nonresidential real property) placed in service this year. Special rules apply to property with a longer production period.

Of course, if you face higher tax rates going forward, depreciation deductions would be worth more in the future. The good news is that you can purchase qualifying property before year-end but wait until your tax filing deadline, including extensions, to determine the optimal approach.

You can also cut your taxes in 2021 with Sec. 179 expensing (deducting the entire cost). It’s available for several types of improvements to nonresidential real property, including roofs, HVAC, fire protection systems, alarm systems and security systems.

The maximum deduction for 2021 is $1.05 million (the maximum deduction also is limited to the amount of income from business activity). The deduction begins phasing out on a dollar-for-dollar basis when qualifying property placed in service this year exceeds $2.62 million. Again, you needn’t decide whether to take the immediate deduction until filing time.

Business meals

Not every tax-cutting tactic has to be dry and dull. One temporary tax provision gives you an incentive to enjoy a little fun.

For 2021 and 2022, businesses can generally deduct 100% (compared with the normal 50%) of qualifying business meals. In addition to meals incurred at and provided by restaurants, qualifying expenses include those for company events, such as holiday parties. As many employees and customers return to the workplace for the first time after extended pandemic-related absences, a company celebration could reap you both a tax break and a valuable chance to reconnect and re-engage.

Stay tuned

The TCJA was signed into law with little more than a week left in 2017. It’s possible the BBBA similarly could come down to the wire, so be prepared to take quick action in the waning days of 2021. Turn to us for the latest information.

]]>Playing on the fear and uncertainty many taxpayers have felt over the past few years in the wake of the pandemic, scammers are working aim to steal sensitive personal information from taxpayers like you. In the following we’ll discuss specific scams to be aware of, including false stimulus payments, fraudulent unemployment claims, fake offers of employment via social media, and bogus charitable donations.

Tips for taxpayers on emerging scams

To avoid compromising yourself with these “too good to be true” schemes, taxpayers should stay wary, as these scams adopt a wide range of communication methods, including:

- Emails

- Phone calls

- Social media posts

- Targeted online advertisements

You must also consider each source before putting any of these arrangements on your tax returns — because ultimately, you are the one responsible for what is on the return, not the promoter who reached out to you and made a promise they failed to uphold. To mitigate risk, an anxious taxpayer should turn to trustworthy tax professionals to assist with their returns.

Read on to learn which scams fall under this Dirty Dozen category.

Scam #5: Pandemic-Related Scams

Economic Impact Payment and Tax Refund Scams

This scam involves identity thieves who use text messages, phone calls, or emails to ask individuals to click a link, verify a date, or provide bank account information to access Economic Impact Payments (EIPs), or stimulus payments.

Reminiscent of tax refund scams, you should act defensively by ignoring these calls and deleting suspicious emails or texts without opening them — the IRS will never contact an individual by phone, email, text, or social media to acquire sensitive information.

Mailbox theft is another worry associated with this scam, so we encourage you to exercise vigilance and the report suspected mail loss to postal inspectors.

Unemployment Fraud (and, subsequently, inaccurate taxpayer 1099-Gs)

As many people lost their jobs and unemployment rates rose during the pandemic, many taxpayers applied for and received unemployment compensation to stay afloat. But they were not the only ones who applied; defrauders went to work stealing the personal information of those who had not applied and proceeded to file unemployment compensation claims for themselves to ultimately steal the payments.

If this happened, you may receive Form 1099-G to report unreceived unemployment compensation. Then request a corrected form to file compliantly, stating only the unemployment compensation and income you did receive.

Fake Employment Offers Via Social Media

In a similar vein, scams continue to capitalize on those who faced unemployment throughout the pandemic by littering social media with fake job postings to entice out-of-work job seekers to provide their personal information. This can then be used to steal your identify or file a fraudulent tax return, so the scammer ends up with your tax refund.

Fake Charities Created to Steal Your Money

While fake charities aren’t exactly new to the scammer scene, the threat has grown throughout the pandemic. Because taxpayers can claim a deduction on their federal tax returns by donating money or goods to a qualified charity, giving back can be enticing. But taxpayers should always verify the charity in which they are donating to — note the exact name, web address, and mailing address, and confirm it is a legitimate organization and not a knock-off meant to confuse.

The IRS also recommends using this search tool to ensure a charity’s validity. Remember, a charity should never pressure an individual to donate right away, and do not donate using a gift card or money wire — only credit card or check, and only after you have performed your due diligence in verifying the charity’s legitimacy.

Consequences of falling for a Dirty Dozen scheme

It is important for taxpayers who have already taken part in transactions like these — or those who are thinking about doing so — to consult tax professionals before claiming any tax benefits they think they are owed.

Those taxpayers who have already claimed the purported tax benefits of one of these four “Dirty Dozen” arrangements on a tax return should file an amended return and go to an independent professional for guidance. If necessary, the IRS will examine the tax benefits from transactions like the ones depicted in the list and inflict penalties related to accuracy ranging from 20% to 40%, or a civil fraud penalty of 75% on any taxpayer who underpaid.

Our perspective on the latest batch of “Dirty Dozen” scams

This is not, of course, an exhaustive list of every scam the IRS has its eye on this year. But it does include some of the more common trends. The best advice we can give? If something looks too good to be true… it probably is. Consult your tax professional for guidance and know that it is in your best interest to stay aware of these nefarious arrangements, so you do not fall susceptible to additional penalties.

Stay tuned for more deep dives into the IRS’s Dirty Dozen list.

MGO’s Tax team brings more than 30 years of experience and is well versed in ensuring your tax returns are compliant. We also stay up to date on the risks, pitfalls, and warnings issued by the IRS so you don’t have to. If you think you have been involved in or are in the process of being involved in one of the Dirty Dozen scams, we can help. Contact us today.

]]>Since Section 280E does not apply to employment payroll taxes because the provision is found in the income tax section of the code, qualifying cannabis companies may be able to capitalize on the credit that rewards employers for keeping their employees on payroll through the pandemic.

What is the ERTC?

Issued as a refund of an employer’s Form 941, the ERTC provides an incentive for those employers who suffered from pandemic-related disruptions and decreased revenues. If a cannabis company continued to pay employees through these challenges, they may be eligible to qualify for ERTC refunds retroactively. The refundable credit can be claimed on qualified wages, including certain health costs paid to employees.

Why was cannabis excluded?

Cannabis companies were unable to qualify for a Paycheck Protection Program (PPP) loan under IRS Section 280E, which prohibits them from deducting ordinary business expenses from gross income for the purpose of income tax. This is because while many states are now proposing and passing legislation to legalize cannabis, the substance is still federally classified as illegal under the Controlled Substances Act (and thus subject to IRS Section 280E).

How do cannabis businesses claim relief?

MGO’s approach to 280E mitigation is based on the idea that the rule only applies to income tax — not payroll tax. And because the ERTC is a payroll tax credit and issued as a refund, cannabis companies previously thought to be ineligible for relief can now claim it if they meet the qualifications:

(1) prove they had a decrease in percentage of gross receipts in calendar quarters during the COVID-19 pandemic when compared to prior quarters, or

(2) that they underwent a full or partial government suspension due to COVID-19 restrictions, like forced closure or quarantine.

The IRS has not yet weighed in on the cannabis issue, so for now, we consider it safe for cannabis companies to act on the opportunity. To determine qualification, a cannabis company will need to provide information like quarterly revenues, payroll tax returns, employee wages, and lines of business on Form 941, the Employer’s Quarterly Federal Tax Return.

Rely on cannabis tax and accounting specialists

All things cannabis tax and finance are complicated and make a major impact on an operator’s bottom line. On top of that, the IRS’ penchant for focusing additional attention on the cannabis industry is well-documented. As a result, cannabis operators should always utilize a cannabis-focused accounting provider that is well-versed in the ins-and-outs of cannabis tax compliance and planning.

MGO is uniquely positioned as a national leader in both tax credit advisory and cannabis accounting and financial best practices. We can help you identify tax credits, file claims, prepare documentation, and ultimately successfully defend your claim.

About the author

Michael Silvio is a partner at MGO. He has more than 25 years of experience in public accounting and tax and has served a variety of public and private businesses in the manufacturing, distribution, pharmaceutical, and biotechnology sectors.

]]>Forgiveness basics

PPP loans generally are 100% forgivable if the borrower allocates at least 60% of the funds to payroll and eligible nonpayroll costs. Borrowers may apply for forgiveness at any time before their loans’ maturity date. Loans made before June 5, 2020, generally have a two-year maturity; loans made on or after that date have a five-year maturity.

However, if a borrower fails to apply for forgiveness within 10 months after the last day of the “covered period,” its PPP loan payments will no longer be deferred. (The covered period is eight to 24 weeks following disbursement during which the funds must be used.) Such loans will become standard loans, and borrowers will be responsible for repaying the full amount plus 1% interest before the maturity date — unless the loan is subsequently forgiven. The 10-month period soon will expire for many so-called “first-draw” borrowers.

SBA’s process improvements

The popularity of the PPP, as well as the requirement that lenders make forgiveness determinations within 60 days of receiving an application, has left many smaller lenders overwhelmed. Some are even limiting the time periods during which they’ll accept forgiveness applications. This, in turn, has created confusion and concern among borrowers.

In response, the SBA recently issued an Interim Final Rule (IFR). The rule streamlines the forgiveness process for smaller loans through two avenues:

1) Direct borrower forgiveness. The SBA is providing a direct borrower forgiveness process for lenders that choose to opt in. At the time the guidance was released, more than 600 banks had opted in, enabling more than 2.17 million borrowers to apply through a new online portal scheduled to launch on August 4, 2021.

Participating lenders will receive notice when a borrower applies through the SBA platform and will review applications and issue forgiveness decisions inside the platform. The SBA hopes this will reduce the wait time and uncertainly associated with applying through lenders.

2) COVID Revenue Reduction Score. The IFR also creates an alternative process for “second-draw” borrowers with loans of $150,000 or less to document their reduced revenue. To qualify for such loans, a borrower must have experienced a revenue reduction of at least 25% during one quarter of 2020 compared with the same quarter in 2019. If a borrower didn’t produce the necessary documentation when applying for the loan, it must do so on or before the date of application for forgiveness.

To make the revenue reduction confirmation process easier for such loans, an independent SBA contractor will assign every eligible second-draw loan a score based on several factors, including industry, geography, business size and current economic data. The score will be stored in the forgiveness platform and visible to lenders to document revenue reduction. If a borrower’s score doesn’t meet the value required to confirm the reduction, the borrower must provide documentation. If it does, no documentation is required.

Appeals and deferments

The IFR also extends the loan deferment period for borrowers who timely appeal a final SBA loan review decision. Under the previous rule, an appeal didn’t extend the period so borrowers had to begin making payments of principal and interest on the unforgiven amount.

The IFR amends that rule to extend the deferment period until the SBA’s Office of Hearings and Appeals issues a final decision. Appeals must be filed within 30 calendar days of receipt of the final SBA loan review decision, and borrowers should notify their lenders of appeals.

More to come

The SBA will release additional guidance regarding both the direct borrower forgiveness option and the COVID Revenue Reduction Score. We can help with your forgiveness application process and answer any questions you may have about your PPP loan.

]]>The U.S. Small Business Administration (SBA) expanded eligibility in September 2021. While you may not have qualified or considered EIDL funding necessary previously, you might want to reconsider in light of yet another wave of COVID infections. But you’ll have to do so quickly, as the application deadline is December 31, 2021.

Shaky economic ground ahead?

Sen. Joe Manchin (D-WV) released a statement on December 19 announcing that he “cannot vote to move forward” on the BBBA. The $2.1 billion bill that passed in the U.S. House of Representatives includes numerous provisions related to healthcare, energy initiatives, immigration, education, social programs and taxes.

The Democrats lack the votes to pass the proposed legislation in the Senate without Manchin’s support. Yet Senate Majority Leader Chuck Schumer (D-NY) indicated on December 20 that he nonetheless intends to hold a vote on the bill in early 2022. Schumer’s announcement came hours after Goldman Sachs reduced its predictions for U.S. economic growth in 2022 based on Manchin’s statement.

Types of EIDL relief available

The COVID-19 EIDL program was created to make low-interest fixed-rate long-term loans to provide small businesses (including sole proprietorships and independent contractors) the working capital they need to withstand the effects of the pandemic. Three types of funding are available:

Loans. This funding type features a 30-year term and fixed interest rate of 3.75%. The proceeds can be used for any normal operating expense, including payroll, rent or mortgage, utilities, and other ordinary businesses expenses. Since the recent program expansion (see below), funds also can be used to pay or pre-pay business debt incurred at any time, including after submitting the application, and regularly scheduled payments of federal debt.

Targeted advances. Businesses located in low-income communities, have no more than 300 employees and have suffered more than a 30% reduction in revenue may qualify for a targeted advance up to $10,000. These advances don’t have to be repaid.

Supplemental targeted advances. Businesses in low-income communities that have no more than 10 employees and saw revenue declines of more than 50% may be eligible for an additional $5,000. Supplemental advances also don’t require repayment.

The recent expansion

The SBA has implemented several changes to make it easier for small businesses to access the COVID-19 EIDL loans. Among other things, the SBA:

- Expanded eligibility from organizations with no more than 500 employees (including affiliates) to encompass businesses in the hardest hit industries with no more than 500 employees per physical location, as long as the business (with affiliates) has no more than 20 locations,

- Increased the maximum loan amount from $500,000 to $2 million,

- Extended the payment deferment period to two years after the loan origination date for all loans (interest will accrue during that period, and principal and interest payments must be made over the remaining 28 years of the loan term), and

- Simplified the affiliation requirements.

The SBA has also limited entities that are part of a single corporate group to a combined total of no more than $10 million in COVID-19 EIDL loans.

Additional eligibility requirements

Applicants must be physically located in the United States or a designated territory and have suffered working capital losses due to the COVID-19 pandemic. In addition, the businesses must have been in operation on or before January 31, 2020.

Businesses (other than sole proprietorships) must have a valid tax identification number. Each owner, member, partner or shareholder of 20% or more must be a U.S. citizen, non-citizen national or qualified alien with a valid Social Security number.

For loans of $500,000 or less, you must have a credit score of at least 570. For larger loans, the credit score must be at least 625. Personal guaranty and collateral requirements may apply, too, depending on the amount of the loan.

The looming deadline

The SBA will accept applications for loans and targeted advances until December 31, 2021. It will continue to process applications after that date, until the funds are exhausted. While the SBA earlier advised businesses seeking supplemental targeted advances to submit applications by December 10, 2021, it later announced it will accept applications until year end. It can’t process applications after the deadline, though, so applications submitted near the deadline might not be processed.

Note that borrowers can request increases, up to their maximum loan eligibility amount, for up to two years after loan origination or until the program funds are exhausted. In addition, the SBA will accept reconsideration and appeal requests received before December 31, 2021, if received on a timely basis. For reconsiderations, that means within six months from the date the application was declined. Appeals must be received within 30 days from the date the reconsideration was declined.

Don’t dawdle

You can apply online for COVID-19 EIDL relief, but the clock is ticking. We can help you determine if you should go this route and help you collect the necessary documentation.

]]>Early termination of the Employee Retention Credit

The IIJA terminates the Employee Retention Credit (ERC) created by the CARES Act earlier than originally planned. The American Rescue Plan Act (ARPA) had extended the credit to eligible employers for the third and fourth quarters of 2021. Under the new law, the ERC — which for 2021 is worth up to $7,000 per qualifying employee per quarter — is no longer available for wages paid after September 30, 2021 (rather than December 31, 2021), except for so-called “recovery startup businesses.”

The ARPA generally defines recovery startup businesses as those that began operating after February 15, 2020, and have annual gross receipts for the three previous tax years of less than or equal to $1 million. These employers can claim the ERC for up to $50,000 total per quarter for the third and fourth quarters of 2021, without showing suspended operations or reduced receipts.

However, clients can still file retractive amendments to claim credits missed (seek refunds) for Q1 – Q4 2020 and Q1 – Q3 2021.

New information reporting on digital assets

The IIJA requires brokers to report to the IRS the cost basis of digital assets transferred by their clients to nonbrokers, similar to how securities brokers report stock and bond trades. “Digital assets” are defined as “any digital representation of value which is recorded on a cryptographically secured distributed ledger or any similar technology.” This definition could ensnare not only cryptocurrencies like Bitcoin and Ethereum, but also certain nonfungible tokens (NFTs). The IIJA expands the definition of the term “broker” to include those who operate trading platforms for digital assets, such as cryptocurrency exchanges.

In addition, the IIJA modifies existing tax law to redefine “cash” subject to reporting to include “any digital representation of value”. As a result, individuals engaged in a trade or business must submit IRS Form 8300, “Report of Cash Payments Over $10,000 Received in a Trade or Business,” when they receive such amounts in one transaction or multiple related transactions.

The digital assets provisions take effect for returns required to be filed, and statements required to be furnished, after December 31, 2023. The IRS is expected to provide guidance before that time, but some businesses may find that accepting cryptocurrencies for payment isn’t worth the reporting burden.

Miscellaneous tax provisions

The IIJA extends several excise taxes used to fund highway spending, extends and modifies certain Superfund excise taxes, and allows private activity bonds for qualified broadband projects and carbon dioxide capture facilities. It extends pension funding relief and expands certain IRS administrative relief for taxpayers affected by federally declared disasters and “significant fires.”

More to come

The majority of the Democrats’ proposed tax law changes, to the extent they survive ongoing negotiations, will be included in the Build Back Better Act (BBBA). The BBBA could, for example, have significant provisions regarding the child tax credit, the cap on the state and local tax deduction, and limits on the business interest expense deduction. We’ll keep you current on the developments that could affect both your personal and business’s bottom lines.

]]>