While it appears that several of the more disadvantageous provisions targeting businesses won’t make it into the final bill, others may. In addition, some temporary provisions are coming to an end, requiring businesses to take action before year end to capitalize on them. As Congress continues to negotiate the final bill, here are some areas where you could act now to reduce your business’s 2021 tax bill.

Research and experimentation

Section 174 research and experimental (R&E) expenditures generally refer to research and development costs in the experimental or laboratory sense. They include costs related to activities intended to uncover information that would eliminate uncertainty about the development or improvement of a product.

Currently, businesses can deduct R&E expenditures in the year they’re incurred or paid. Alternatively, they can capitalize and amortize the costs over at least five years. Software development costs also can be immediately expensed, amortized over five years from the date of completion or amortized over three years from the date the software is placed in service.

However, under the Tax Cuts and Jobs Act (TCJA), that tax treatment is scheduled to expire after 2021. Beginning next year, you can’t deduct R&E costs in the year incurred. Instead, you must amortize such expenses incurred in the United States over five years and expenses incurred outside the country over 15 years. In addition, the TCJA requires that software development costs be treated as Sec. 174 expenses.

The BBBA may include a provision that delays the capitalization and amortization requirements to 2026, but it’s far from a sure thing. You might consider accelerating research expenses into 2021 to maximize your deductions and reduce the amount you may need to begin to capitalize starting next year.

Income and expense timing

Accelerating expenses into the current tax year and deferring income until the next year is a tried-and-true tax reduction strategy for businesses that use cash-basis accounting. These businesses might, for example, delay billing until later in December than they usually do, stock up on supplies and expedite bonus payments.

But the strategy is advised only for businesses that expect to be in the same or a lower tax bracket the following year — and you may expect greater profits in 2022, as the pandemic hopefully winds down. If that’s the case, your deductions could be worth more next year, so you’d want to delay expenses, while accelerating your collection of income. Moreover, under some proposed provisions in the BBBA, certain businesses may find themselves facing higher tax rates in 2022.

For example, the BBBA may expand the net investment income tax (NIIT) to include active business income from pass-through businesses. The owners of pass-through businesses — who report their business income on their individual income tax returns — also could be subject to a new 5% “surtax” on modified adjusted gross income (MAGI) that exceeds $10 million, with an additional 3% on income of more than $25 million.

Capital assets

The traditional approach of making capital purchases before year-end remains effective for reducing taxes in 2021, bearing in mind the timing issues discussed above. Businesses can deduct 100% of the cost of new and used (subject to certain conditions) qualified property in the year the property is placed in service.

You can take advantage of this bonus depreciation by purchasing computer systems, software, vehicles, machinery, equipment and office furniture, among other items. Bonus depreciation also is available for qualified improvement property (generally, interior improvements to nonresidential real property) placed in service this year. Special rules apply to property with a longer production period.

Of course, if you face higher tax rates going forward, depreciation deductions would be worth more in the future. The good news is that you can purchase qualifying property before year-end but wait until your tax filing deadline, including extensions, to determine the optimal approach.

You can also cut your taxes in 2021 with Sec. 179 expensing (deducting the entire cost). It’s available for several types of improvements to nonresidential real property, including roofs, HVAC, fire protection systems, alarm systems and security systems.

The maximum deduction for 2021 is $1.05 million (the maximum deduction also is limited to the amount of income from business activity). The deduction begins phasing out on a dollar-for-dollar basis when qualifying property placed in service this year exceeds $2.62 million. Again, you needn’t decide whether to take the immediate deduction until filing time.

Business meals

Not every tax-cutting tactic has to be dry and dull. One temporary tax provision gives you an incentive to enjoy a little fun.

For 2021 and 2022, businesses can generally deduct 100% (compared with the normal 50%) of qualifying business meals. In addition to meals incurred at and provided by restaurants, qualifying expenses include those for company events, such as holiday parties. As many employees and customers return to the workplace for the first time after extended pandemic-related absences, a company celebration could reap you both a tax break and a valuable chance to reconnect and re-engage.

Stay tuned

The TCJA was signed into law with little more than a week left in 2017. It’s possible the BBBA similarly could come down to the wire, so be prepared to take quick action in the waning days of 2021. Turn to us for the latest information.

]]>MGO’s panel of professionals provide an overview of ARPA, including allowable costs and revenue recognition, and the panel discuss their individual thoughts about the impact these will have on their organizations.

]]>Forgiveness basics

PPP loans generally are 100% forgivable if the borrower allocates at least 60% of the funds to payroll and eligible nonpayroll costs. Borrowers may apply for forgiveness at any time before their loans’ maturity date. Loans made before June 5, 2020, generally have a two-year maturity; loans made on or after that date have a five-year maturity.

However, if a borrower fails to apply for forgiveness within 10 months after the last day of the “covered period,” its PPP loan payments will no longer be deferred. (The covered period is eight to 24 weeks following disbursement during which the funds must be used.) Such loans will become standard loans, and borrowers will be responsible for repaying the full amount plus 1% interest before the maturity date — unless the loan is subsequently forgiven. The 10-month period soon will expire for many so-called “first-draw” borrowers.

SBA’s process improvements

The popularity of the PPP, as well as the requirement that lenders make forgiveness determinations within 60 days of receiving an application, has left many smaller lenders overwhelmed. Some are even limiting the time periods during which they’ll accept forgiveness applications. This, in turn, has created confusion and concern among borrowers.

In response, the SBA recently issued an Interim Final Rule (IFR). The rule streamlines the forgiveness process for smaller loans through two avenues:

1) Direct borrower forgiveness. The SBA is providing a direct borrower forgiveness process for lenders that choose to opt in. At the time the guidance was released, more than 600 banks had opted in, enabling more than 2.17 million borrowers to apply through a new online portal scheduled to launch on August 4, 2021.

Participating lenders will receive notice when a borrower applies through the SBA platform and will review applications and issue forgiveness decisions inside the platform. The SBA hopes this will reduce the wait time and uncertainly associated with applying through lenders.

2) COVID Revenue Reduction Score. The IFR also creates an alternative process for “second-draw” borrowers with loans of $150,000 or less to document their reduced revenue. To qualify for such loans, a borrower must have experienced a revenue reduction of at least 25% during one quarter of 2020 compared with the same quarter in 2019. If a borrower didn’t produce the necessary documentation when applying for the loan, it must do so on or before the date of application for forgiveness.

To make the revenue reduction confirmation process easier for such loans, an independent SBA contractor will assign every eligible second-draw loan a score based on several factors, including industry, geography, business size and current economic data. The score will be stored in the forgiveness platform and visible to lenders to document revenue reduction. If a borrower’s score doesn’t meet the value required to confirm the reduction, the borrower must provide documentation. If it does, no documentation is required.

Appeals and deferments

The IFR also extends the loan deferment period for borrowers who timely appeal a final SBA loan review decision. Under the previous rule, an appeal didn’t extend the period so borrowers had to begin making payments of principal and interest on the unforgiven amount.

The IFR amends that rule to extend the deferment period until the SBA’s Office of Hearings and Appeals issues a final decision. Appeals must be filed within 30 calendar days of receipt of the final SBA loan review decision, and borrowers should notify their lenders of appeals.

More to come

The SBA will release additional guidance regarding both the direct borrower forgiveness option and the COVID Revenue Reduction Score. We can help with your forgiveness application process and answer any questions you may have about your PPP loan.

]]>Also, keep in mind that, under the Tax Cuts and Jobs Act (TCJA), annual inflation adjustments are calculated using the chained consumer price index (also known as C-CPI-U). This increases tax bracket thresholds, the standard deduction, certain exemptions and other figures at a slower rate than was the case with the consumer price index previously used, potentially pushing taxpayers into higher tax brackets and making various breaks worth less over time. The TCJA adopts the C-CPI-U on a permanent basis.

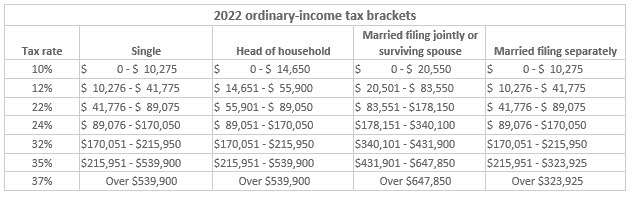

Individual income taxes

Tax-bracket thresholds increase for each filing status but, because they’re based on percentages, they increase more significantly for the higher brackets. For example, the top of the 10% bracket increases by $325 to $650, depending on filing status, but the top of the 35% bracket increases by $16,300 to $19,550, again depending on filing status.

The TCJA suspended personal exemptions through 2025. However, it nearly doubled the standard deduction, indexed annually for inflation through 2025. For 2022, the standard deduction is $25,900 (married couples filing jointly), $19,400 (heads of households), and $12,950 (singles and married couples filing separately). After 2025, standard deduction amounts are scheduled to drop back to the amounts under pre-TCJA law unless Congress extends the current rules or revises them.

Changes to the standard deduction could help some taxpayers make up for the loss of personal exemptions. But it might not help taxpayers who typically used to itemize deductions.

Alternative minimum tax

The alternative minimum tax (AMT) is a separate tax system that limits some deductions, doesn’t permit others and treats certain income items differently. If your AMT liability is greater than your regular tax liability, you must pay the AMT.

Like the regular tax brackets, the AMT brackets are annually indexed for inflation. For 2022, the threshold for the 28% bracket increased by $6,200 for all filing statuses except married filing separately, which increased by half that amount.

The AMT exemptions and exemption phaseouts are also indexed. The exemption amounts for 2022 are $75,900 for singles and heads of households and $118,100 for joint filers, increasing by $2,300 and $3,500, respectively, over 2021 amounts. The inflation-adjusted phaseout ranges for 2022 are $539,900–$843,500 (singles and heads of households) and $1,079,800–$1,552,200 (joint filers). Amounts for separate filers are half of those for joint filers.

Education and child-related breaks

The maximum benefits of certain education and child-related breaks generally remain the same for 2022. But most of these breaks are limited based on a taxpayer’s modified adjusted gross income (MAGI). Taxpayers whose MAGIs are within an applicable phaseout range are eligible for a partial break — and breaks are eliminated for those whose MAGIs exceed the top of the range.

The MAGI phaseout ranges generally remain the same or increase modestly for 2022, depending on the break. For example:

The American Opportunity credit. For tax years beginning after December 31, 2020, the MAGI amount used by joint filers to determine the reduction in the American Opportunity credit isn’t adjusted for inflation. The credit is phased out for taxpayers with MAGI in excess of $80,000 ($160,000 for joint returns). The maximum credit per eligible student is $2,500.

The Lifetime Learning credit. For tax years beginning after December 31, 2020, the MAGI amount used by joint filers to determine the reduction in the Lifetime Learning credit isn’t adjusted for inflation. The credit is phased out for taxpayers with MAGI in excess of $80,000 ($160,000 for joint returns). The maximum credit is $2,000 per tax return.

The adoption credit. The phaseout ranges for eligible taxpayers adopting a child will also increase for 2022 — by $6,750 to $223,410–$263,410 for joint, head-of-household and single filers. The maximum credit increases by $450, to $14,890 for 2022.

(Note: Married couples filing separately generally aren’t eligible for these credits.)

These are only some of the education and child-related breaks that may benefit you. Keep in mind that, if your MAGI is too high for you to qualify for a break for your child’s education, your child might be eligible to claim one on his or her tax return.

Gift and estate taxes

The unified gift and estate tax exemption and the generation-skipping transfer (GST) tax exemption are both adjusted annually for inflation. For 2022, the amount is $12.060 million (up from $11.70 million for 2021).

The annual gift tax exclusion increases by $1,000 to $16,000 for 2022.

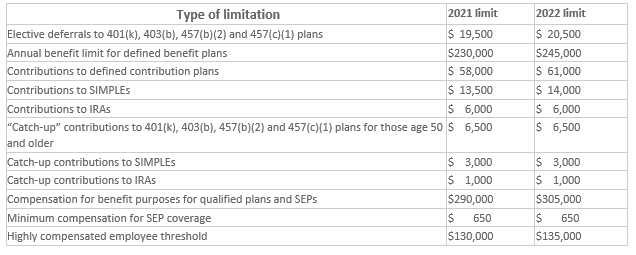

Retirement plans

Not all of the retirement-plan-related limits increase for 2022. Thus, depending on the type of plan you have, you may have limited opportunities to increase your retirement savings if you’ve already been contributing the maximum amount allowed.

Your MAGI may reduce or even eliminate your ability to take advantage of IRAs. Fortunately, IRA-related MAGI phaseout range limits all will increase for 2022:

Traditional IRAs. MAGI phaseout ranges apply to the deductibility of contributions if a taxpayer (or his or her spouse) participates in an employer-sponsored retirement plan:

- For married taxpayers filing jointly, the phaseout range is specific to each spouse based on whether he or she is a participant in an employer-sponsored plan:

- For a spouse who participates, the 2022 phaseout range limits increase by $4,000, to $109,000–$129,000.

- For a spouse who doesn’t participate, the 2022 phaseout range limits increase by $6,000, to $204,000–$214,000.

- For single and head-of-household taxpayers participating in an employer-sponsored plan, the 2022 phaseout range limits increase by $2,000, to $68,000–$78,000.

Taxpayers with MAGIs in the applicable range can deduct a partial contribution; those with MAGIs exceeding the applicable range can’t deduct any IRA contribution.

But a taxpayer whose deduction is reduced or eliminated can make nondeductible traditional IRA contributions. The $6,000 contribution limit (plus $1,000 catch-up if applicable and reduced by any Roth IRA contributions) still applies. Nondeductible traditional IRA contributions may be beneficial if your MAGI is also too high for you to contribute (or fully contribute) to a Roth IRA.

Roth IRAs. Whether you participate in an employer-sponsored plan doesn’t affect your ability to contribute to a Roth IRA, but MAGI limits may reduce or eliminate your ability to contribute:

- For married taxpayers filing jointly, the 2022 phaseout range limits increase by $6,000, to $204,000–$214,000.

- For single and head-of-household taxpayers, the 2022 phaseout range limits increase by $4,000, to $129,000–$144,000.

You can make a partial contribution if your MAGI falls within the applicable range, but no contribution if it exceeds the top of the range.

(Note: Married taxpayers filing separately are subject to much lower phaseout ranges for both traditional and Roth IRAs.)

2022 cost-of-living adjustments and tax planning

With many of the 2022 cost-of-living adjustment amounts trending higher, you have an opportunity to realize some tax relief next year. In addition, with certain retirement-plan-related limits also increasing, you have the chance to boost your retirement savings. If you have questions on the best tax-saving strategies to implement based on the 2022 numbers, please give us a call. We’d be happy to help.

]]>The U.S. Small Business Administration (SBA) expanded eligibility in September 2021. While you may not have qualified or considered EIDL funding necessary previously, you might want to reconsider in light of yet another wave of COVID infections. But you’ll have to do so quickly, as the application deadline is December 31, 2021.

Shaky economic ground ahead?

Sen. Joe Manchin (D-WV) released a statement on December 19 announcing that he “cannot vote to move forward” on the BBBA. The $2.1 billion bill that passed in the U.S. House of Representatives includes numerous provisions related to healthcare, energy initiatives, immigration, education, social programs and taxes.

The Democrats lack the votes to pass the proposed legislation in the Senate without Manchin’s support. Yet Senate Majority Leader Chuck Schumer (D-NY) indicated on December 20 that he nonetheless intends to hold a vote on the bill in early 2022. Schumer’s announcement came hours after Goldman Sachs reduced its predictions for U.S. economic growth in 2022 based on Manchin’s statement.

Types of EIDL relief available

The COVID-19 EIDL program was created to make low-interest fixed-rate long-term loans to provide small businesses (including sole proprietorships and independent contractors) the working capital they need to withstand the effects of the pandemic. Three types of funding are available:

Loans. This funding type features a 30-year term and fixed interest rate of 3.75%. The proceeds can be used for any normal operating expense, including payroll, rent or mortgage, utilities, and other ordinary businesses expenses. Since the recent program expansion (see below), funds also can be used to pay or pre-pay business debt incurred at any time, including after submitting the application, and regularly scheduled payments of federal debt.

Targeted advances. Businesses located in low-income communities, have no more than 300 employees and have suffered more than a 30% reduction in revenue may qualify for a targeted advance up to $10,000. These advances don’t have to be repaid.

Supplemental targeted advances. Businesses in low-income communities that have no more than 10 employees and saw revenue declines of more than 50% may be eligible for an additional $5,000. Supplemental advances also don’t require repayment.

The recent expansion

The SBA has implemented several changes to make it easier for small businesses to access the COVID-19 EIDL loans. Among other things, the SBA:

- Expanded eligibility from organizations with no more than 500 employees (including affiliates) to encompass businesses in the hardest hit industries with no more than 500 employees per physical location, as long as the business (with affiliates) has no more than 20 locations,

- Increased the maximum loan amount from $500,000 to $2 million,

- Extended the payment deferment period to two years after the loan origination date for all loans (interest will accrue during that period, and principal and interest payments must be made over the remaining 28 years of the loan term), and

- Simplified the affiliation requirements.

The SBA has also limited entities that are part of a single corporate group to a combined total of no more than $10 million in COVID-19 EIDL loans.

Additional eligibility requirements

Applicants must be physically located in the United States or a designated territory and have suffered working capital losses due to the COVID-19 pandemic. In addition, the businesses must have been in operation on or before January 31, 2020.

Businesses (other than sole proprietorships) must have a valid tax identification number. Each owner, member, partner or shareholder of 20% or more must be a U.S. citizen, non-citizen national or qualified alien with a valid Social Security number.

For loans of $500,000 or less, you must have a credit score of at least 570. For larger loans, the credit score must be at least 625. Personal guaranty and collateral requirements may apply, too, depending on the amount of the loan.

The looming deadline

The SBA will accept applications for loans and targeted advances until December 31, 2021. It will continue to process applications after that date, until the funds are exhausted. While the SBA earlier advised businesses seeking supplemental targeted advances to submit applications by December 10, 2021, it later announced it will accept applications until year end. It can’t process applications after the deadline, though, so applications submitted near the deadline might not be processed.

Note that borrowers can request increases, up to their maximum loan eligibility amount, for up to two years after loan origination or until the program funds are exhausted. In addition, the SBA will accept reconsideration and appeal requests received before December 31, 2021, if received on a timely basis. For reconsiderations, that means within six months from the date the application was declined. Appeals must be received within 30 days from the date the reconsideration was declined.

Don’t dawdle

You can apply online for COVID-19 EIDL relief, but the clock is ticking. We can help you determine if you should go this route and help you collect the necessary documentation.

]]>Early termination of the Employee Retention Credit

The IIJA terminates the Employee Retention Credit (ERC) created by the CARES Act earlier than originally planned. The American Rescue Plan Act (ARPA) had extended the credit to eligible employers for the third and fourth quarters of 2021. Under the new law, the ERC — which for 2021 is worth up to $7,000 per qualifying employee per quarter — is no longer available for wages paid after September 30, 2021 (rather than December 31, 2021), except for so-called “recovery startup businesses.”

The ARPA generally defines recovery startup businesses as those that began operating after February 15, 2020, and have annual gross receipts for the three previous tax years of less than or equal to $1 million. These employers can claim the ERC for up to $50,000 total per quarter for the third and fourth quarters of 2021, without showing suspended operations or reduced receipts.

However, clients can still file retractive amendments to claim credits missed (seek refunds) for Q1 – Q4 2020 and Q1 – Q3 2021.

New information reporting on digital assets

The IIJA requires brokers to report to the IRS the cost basis of digital assets transferred by their clients to nonbrokers, similar to how securities brokers report stock and bond trades. “Digital assets” are defined as “any digital representation of value which is recorded on a cryptographically secured distributed ledger or any similar technology.” This definition could ensnare not only cryptocurrencies like Bitcoin and Ethereum, but also certain nonfungible tokens (NFTs). The IIJA expands the definition of the term “broker” to include those who operate trading platforms for digital assets, such as cryptocurrency exchanges.

In addition, the IIJA modifies existing tax law to redefine “cash” subject to reporting to include “any digital representation of value”. As a result, individuals engaged in a trade or business must submit IRS Form 8300, “Report of Cash Payments Over $10,000 Received in a Trade or Business,” when they receive such amounts in one transaction or multiple related transactions.

The digital assets provisions take effect for returns required to be filed, and statements required to be furnished, after December 31, 2023. The IRS is expected to provide guidance before that time, but some businesses may find that accepting cryptocurrencies for payment isn’t worth the reporting burden.

Miscellaneous tax provisions

The IIJA extends several excise taxes used to fund highway spending, extends and modifies certain Superfund excise taxes, and allows private activity bonds for qualified broadband projects and carbon dioxide capture facilities. It extends pension funding relief and expands certain IRS administrative relief for taxpayers affected by federally declared disasters and “significant fires.”

More to come

The majority of the Democrats’ proposed tax law changes, to the extent they survive ongoing negotiations, will be included in the Build Back Better Act (BBBA). The BBBA could, for example, have significant provisions regarding the child tax credit, the cap on the state and local tax deduction, and limits on the business interest expense deduction. We’ll keep you current on the developments that could affect both your personal and business’s bottom lines.

]]>Prepare for grant reporting

The total distribution of government grants for Native American Tribes is estimated to be more than $31 billion. Being awarded a grant is a welcomed relief, however organizations must ensure that the proper grant accounting and compliance guidance are followed. This requires time, energy, systems, and often an increase in internal efforts. Furthermore, for some organizations initial grant awards may trigger new audit requirements and reengineering of existing accounting procedures.

Grant requirements can be complicated, so it is crucial to develop a systematic grant management program. Identify (or hire) a grant administrator to take responsibility for meeting compliance guidelines. Develop policies and procedures that outline each step in the lifecycle of a grant (application, interim reporting, and final results). Grant reporting involves many deadlines and needs consistent attention and clear communication with the granting agency. Close attention to the reporting and compliance details of the grant will make final reporting or an audit of the grant much easier. But it’s not just ease that is important, solid grant compliance and grant management is about good fiscal management, transparency, and mitigating risk. Because the consequences of noncompliance can be fines, costs to reputation, and a loss of confidence from funders.

Secure your assets against cybercrime

Cybersecurity should be another priority for tribal communities. Casinos and gaming organizations are high-value targets for cyber criminals because of the large quantity of Personal Identifiable Information (PII) obtained and stored on a daily basis. Casinos also have many physical and digital entry points, a variety of technology, a large workforce, multiple third- party vendors, and high frequency of high cash and payment card transactions. These components entice cyber criminals to launch large scale attacks and potentially cause expensive data breaches.

How do you protect yourself in an industry that is so ripe for cybercrime? A formal risk assessment can gather disparate pieces of information and evaluate your entire environment including the mix of digital computing platforms. This will help you prioritize the issues you need to address to build a more secure structure in which to do business. A comprehensive risk assessment will also help assess your compliance and controls and identify your full range of risk exposure.

It’s also crucial to understand what assets you have so you know what must be protected. These include more than just laptops or servers. Your cloud, web applications, and mobile devices are also at risk. Gap analysis and a penetration test can reveal the vulnerabilities in your IT environment.

Once you’ve fully identified your vulnerabilities, you can take actions to strengthen your defenses and protect your business. Ultimately, you will need to identify the leaders responsible for managing cybersecurity risks, suggesting methods and resources for mitigation, providing training, and developing an executable cyber security roadmap in order to move forward.

A diversified portfolio reduces risk

Both individuals and organizations need a diverse group of investments to spread out risk. This is not news, but frequently, the awareness of risk does not result in actions that mitigate it.

Finding the right investments takes time. A financial advisor can help you, but ultimately the decisions are yours. Do you look for high returns? Not if you are looking to balance your risk. Do you seek out the predictability of bonds? There are actually risks in that approach, too. There is no single way to mitigate risk, but examining your current investments is a good place to start before evaluating new ones.

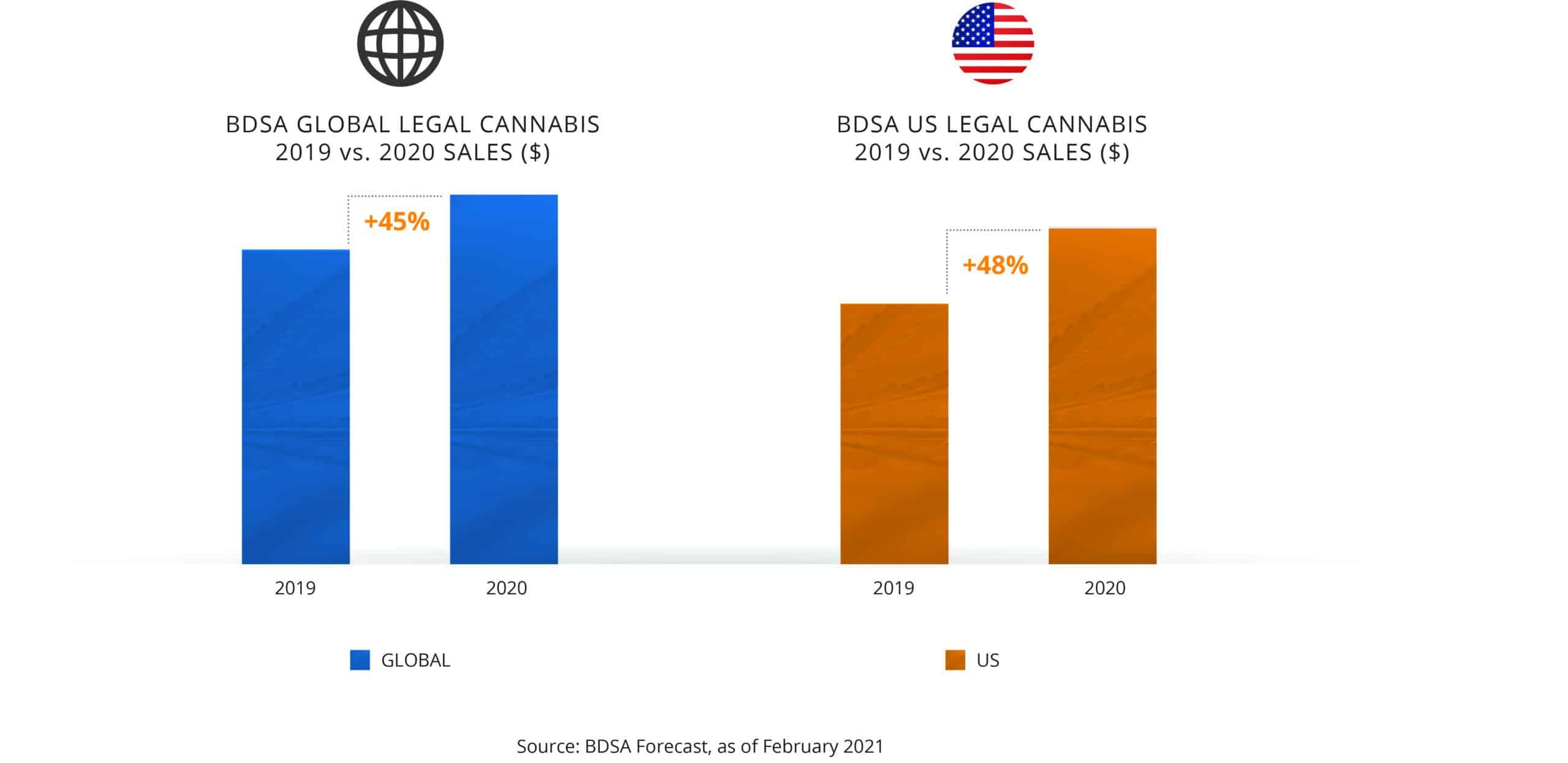

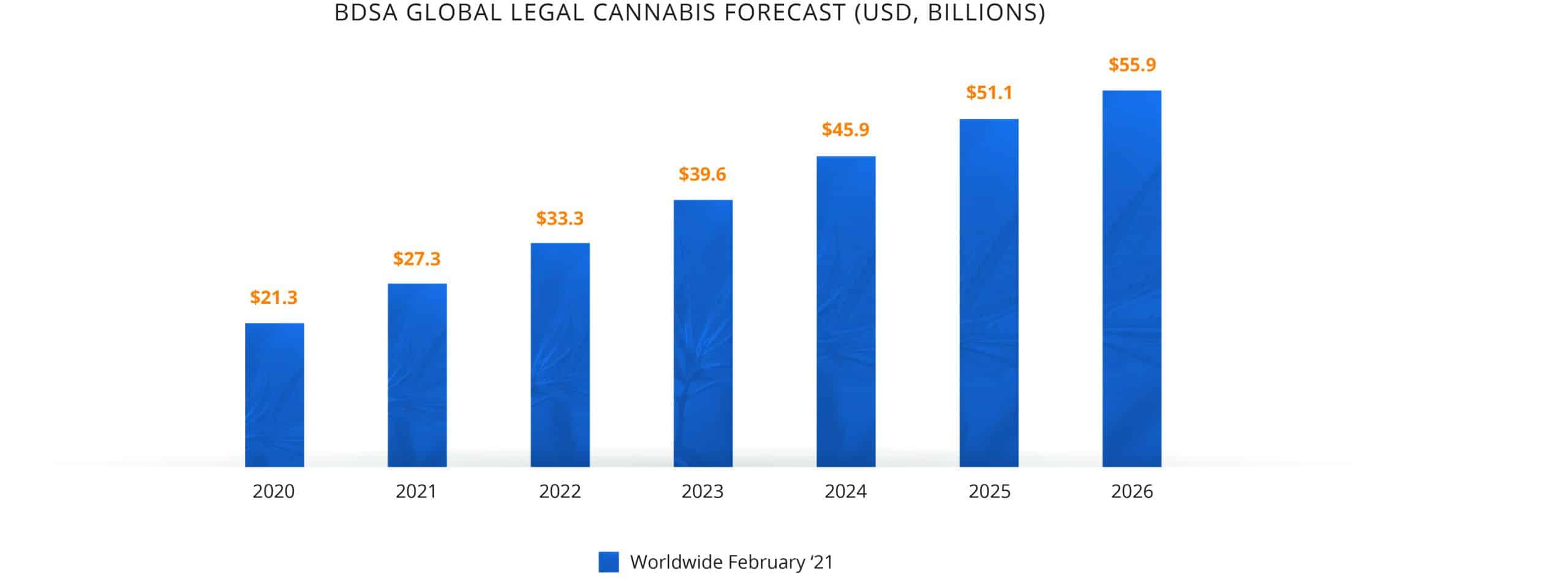

When it comes to diversifying your portfolio, take your time to do the due diligence. For instance, the cannabis industry is one of the fastest-growing industries in the world. It will generate an estimated $146.4 billion by 2025, according to Grand View Research. Does that make it the right opportunity for you? To find the answer, you need to dig deeper.

The industry is still in its early stages of growth, and this can work in your favor. Your investment could grow quickly, but regulations and licensing can be complicated for an emerging industry. Cannabis may be an exciting and profitable business to get involved in, but that doesn’t mean it is it the right investment for your particular portfolio. If you are trying to mitigate risk, does this investment really accomplish that? Do you already have a high-growth investment? Are there stigmas associated with cannabis that you might want to avoid? Are there compliance issues that could be more of a headache than investing in a more mature industry?

An investment in cannabis may not be a simple decision. Like many industries, you can also decide how deeply you want to invest — and there are risks at each level. An investor could focus on cultivation, manufacturing, retail, or the development of a vertically integrated cannabis operation. The unique sovereignty of Tribal nations even creates potential for leasing Tribal land to cannabis cultivators or aspiring cultivators without land to grow.

Like any investment, due diligence is key to risk mitigation. If you understand the industry you are investing in, you will understand your investment’s impact on your portfolio. And remember, when considering risk, your focus should be on your overall portfolio, rather than the intriguing possibilities of the industry or the certainty of returns.

How we can help

Tribal leadership is facing unique challenges. More than ever, sound due diligence and risk mitigating practices must be an integral part of decision making. MGO’s professionals have helped Tribes develop frameworks for grant management, cybersecurity, and economic diversification that facilitate the decision-making process for council members.

]]>PPP basics

Generally, PPP loans are 100% forgivable given the borrower allocates the funds on a 60/40 basis between payroll and eligible nonpayroll costs. Nonpayroll costs originally solely included mortgage interest, rent, utilities, and interest on any other existing debt. However, the Consolidated Appropriations Act (CAA), which was enacted in late 2020, significantly expanded the eligible nonpayroll costs to include other costs the funds can be applied to, such as certain operating expenses and worker protection expenses.

The CAA also withdrew the original requirement that mandated borrowers deduct the amount of any Small Business Administration (SBA) Economic Injury Disaster Loan (EIDL) advance from the forgiveness amount they received from the PPP. A borrower doesn’t need to include any forgiven amounts in its gross income and can deduct otherwise deductible expenses paid for with forgiven PPP proceeds.

Forgiveness filings

Those who borrowed PPP loans can apply for forgiveness at any time before their loans’ maturity date, and loans made before June 5, 2020, generally have a two-year maturity while loans made on or after that date have a five-year maturity. However, if a borrower does not apply for forgiveness within 10 months after the last day of the “covered period” (the eight-to-24 weeks following disbursement during which the funds must be used), the PPP loan payments will no longer be deferred, and payments must begin to be made to the lender.

This 10-month period is ending for many “first-draw” borrowers. If a business applied early in the program, it might have a covered period that ended on October 30, 2020, meaning it would need to apply for forgiveness by August 30, 2021, to avoid loan repayment responsibilities.

To apply for forgiveness, borrowers file forms with their lenders, who will then submit the forms to the SBA. The type of form that must be filed is dependent on both the amount of the loan and whether a business is a sole proprietor, independent contractor, or self-employed individual with no employees.

The borrower will be notified by the lender if the SBA does not forgive a loan or only partially forgives it. Interest accrues during the time from disbursement of the loan proceeds to SBA remittance to the lender of the forgiven amount, and the borrower must pay any interest that has accrued on any amount not forgiven.

To maximize their employee retention tax credits, some businesses may have delayed filing their forgiveness applications. The reason for this stems from the fact that qualified wages paid after March 12, 2020, through December 31, 2021—that are considered for purposes of calculating the credit amount—cannot be included when calculating eligible payroll costs for PPP loan forgiveness. These businesses should pay careful attention to the date their 10-month period expires as to avoid triggering loan repayment.

Audit action

There is the possibility that borrowers will be audited by the SBA’s Office of Inspector General with support from the IRS and other federal agencies. The SBA automatically audits every loan in excess of $2 million after the borrower applies for forgiveness, but it’s possible that smaller loans could be subject to scrutiny too.

Despite the audit safe harbor for loans of $2 million or less established by the SBA, this carveout solely applies to the examination of the borrower’s good faith certification on the loan application that states “the current economic uncertainty makes the loan request necessary to support the ongoing operations” of the business. Those borrowers will also no longer need to complete a burdensome, time-consuming Loan Necessity Questionnaire, as the SBA recently notified lenders that this loan necessity requirement for loans more than $2 million has been eliminated.

However, all borrowers still have the potential to be audited on matters like eligibility (like the number of employees), calculation of the loan amount, how the funds were used, and entitlement to forgiveness. Borrowers that receive poor audit findings may be required to repay their loans and, depending on what kinds of missteps were recovered, could face civil penalties and persecution under the federal False Claims Act.

Those businesses that received loans of more than $2 million should not wait to prepare for their audits. By beginning to work with their CPAs now, they can gather and organize the documents and information auditors are likely to request, including:

• Financial statements,

• Income and employment tax returns,

• Payroll records for all pay periods within the applicable covered period,

• Calculation of full-time equivalent employees, and

• Bank and other records related to how the funds were used (for example, canceled checks, utility bills, leases, and mortgage statements).

It is important to note that some of this documentation will overlap with what is required when filing the application for loan forgiveness.

Act now

Businesses always have their plates full, so it isn’t surprising that many may not have been focused on the various dates that matter to their PPP loans. Now is the time to ensure that you file your forgiveness application promptly with the necessary documentation already gathered to survive any SBA audit that may follow. Contact us for assistance.

]]>Tax incentives for telemedicine tools

Health care professionals are incorporating tablets, chat capabilities, and other mobile solutions to diagnose more patients in a shorter amount of time and across geographical boundaries. This demand for innovation presents opportunities for software companies, and the development of these technologies is being encouraged by Federal and state Research and Development (R&D) Tax Credits.

About the R&D tax credit

Enacted in 1981, the Federal R&D Tax Credit allows a credit of up to 14 percent of eligible spending for new and improved software products.

To qualify as an R&D activity, one must meet each of the following criteria:

• Technological in nature. Activities must be based on hard science.

• Qualified purpose. Activities must be intended to develop a new or improved product or process.

• Technological uncertainty. Activities must be aimed at eliminating uncertainty with respect to the development of a product or process.

• Process of experimentation. Activities must involve a systemic or iterative approach of evaluating different alternatives to eliminate ambiguity.

Eligible costs include:

• Employee wages

• Supplies

• Contract research expenses

Software companies developing platforms to enable and improve remote health care may be able to take advantage of the R&D Tax Credit as a dollar-for-dollar tax saving for the work that they are already doing.

Software activities that may qualify for a tax credit

If your company is investing in developing telemedicine platforms, you may be able a claim an R&D Tax Credit. Though each situation is unique, development activities for the following products may qualify:

- Tools that allow physicians to view medical images and other data on mobile devices such as smartphones, tablets, and other electronic devices

- Application programming interfaces and capabilities to transfer information electronically and view electronic medical files

- Cloud-based platforms to enable health care providers to directly engage patients in an easy-to-use virtual care environment that is HIPAA compliant

- Platforms with the capabilities of linking physicians and pharmacies to allow physicians to submit a prescription electronically

- Wearable devices with sensors to provide continuous monitoring of patients and automated treatment for health conditions

- Virtual therapy platforms for online counseling

- Medical data cloud storage solutions and data security

How we can help

The pandemic put our current telemedicine capabilities to the test, and patients gave these innovations a passing grade. But we have yet to experience the true power of telemedicine. As the innovation continues and popularity grows, we can be certain of even more widespread acceptance of telemedicine. And as the need continues to increase, it appears that the various tax credits for research and development will be available to help support the work of those who develop technology in the health care sector.

MGO professionals bring over 25 years of R&D Tax Credit experience to help you identify, analyze, file, and defend your claim. We provide a no-cost eligibility analysis to determine if these tax incentives are appropriate to your situation.

About the author

Michael Silvio is a partner at MGO. He has more than 25 years of experience in public accounting and tax and has served a variety of public and private businesses in the manufacturing, distribution, pharmaceutical, and biotechnology sectors.

That all changed on March 11, when President Biden signed the American Rescue Plan Act of 2021 into law. The bill allocates $432 billion in direct financial support to U.S. territories, states, and local and tribal governments. In the following, we highlight how the bill affects state, local, and Tribal governments, and breakdown the details of key provisions.

American Rescue Plan of 2021: Impact on State, Local and Tribal Governments

The American Rescue Plan of 2021 contains wide-ranging programs designed to support state, local, and Tribal governments through the financial crises resulting from the COVID-19 pandemic. These include active support for COVID-19 response and planning, funds for in-state capital improvement projects, emergency housing support, and much more.

Much of the relief funding is allocated and disbursed automatically using metrics that include population, economic conditions, and unemployment rates. While each program has different disbursement details, broadly speaking, payments are delivered in two or more installments, the first coming within a 60-day window following the bill becoming law, and future installments through 2022 and beyond.

Other programs will require state and local authorities to apply for grants based on specific needs.

One of the highlights of the revised funding and plan is looser restrictions on how funds from the Coronavirus State Fiscal Recovery Fund can be utilized. The accepted uses include:

• Funding government services that have been curtailed due to decreases in tax revenue caused by the pandemic.

• Aid to households, small businesses and nonprofits, and impacted industries like tourism, hospitality and travel.

• Making “necessary investments” in water, sewer, or broadband infrastructure.

While potential uses have been broadened, all programs require stringent rules for intended use, tracking and reporting.

Highlights of the American Rescue Plan of 2021

Coronavirus State Fiscal Recovery Fund

50 States and the District of Columbia receive $195.3 billion in aid:

- $25.5 billion will be split evenly among each state and the District of Columbia, with each state and the District of Columbia receiving $500 million in aid.

- $168.55 billion distributed based on each state’s share of total unemployed workers over the period of October 2020 to December 2020.

- District of Columbia receives additional $1.25 billion.

- Tribal governments receive $20 billion (further discussion to come).

- U.S. territories receive $4.5 billion.

- U.S. Treasury receives $50 million to cover costs of administration of the fund.

Coronavirus Local Fiscal Recovery Fund

Local governments to receive $130.2 billion in aid to be split among counties, metropolitan cities, and non-entitlement units of local government:

- Counties receive $65.1 billion in population-adjusted payments, with additional adjustments for Community Development Block Grant (CDBG) recipients.

- Metropolitan cities receive $45.57 billion.

- Non-entitlement units of local government receive $19.53 billion, distributed by individual states and funded by the U.S. Treasury. Each jurisdiction receives population-adjusted payments based on such jurisdiction’s share of the state population.

Coronavirus Capital Projects Fund

$10 billion available for states, territories, and Tribal governments to support critical capital projects directly enabling work, education and health monitoring in response to COVID-19:

- Each state receives $100 million.

- U.S. territories receive $100 million to be split among them.

- Tribal governments and the state of Hawaii receive $100 million to be split among them.

- Remainder of funds to be allocated to states based on population.

NOTE: The Treasury Department will establish an application process for grants from the fund within 60 days of enactment of the law.

Local Assistance and Tribal Consistency Fund

$2 billion for eligible revenue-sharing counties and tribal governments:

- Eligible revenue-sharing counties will receive $750 million allocated based on economic conditions for each FY 2022 and FY 2023.

- Eligible tribal governments will receive $250 million allocated based on economic conditions for each FY 2022 and FY 2023.

NOTE: Payments from this fund may be used for any governmental purpose other than a lobbying activity and will remain available until September 30, 2023.

Other State, Local, and Government Funding Sources

Additional federal government programs have received funding earmarked to support recovery efforts in states, Tribes, and territories. These funds can be applied for via grant applications depending on each government agency’s circumstances.

Homeowner Assistance Fund

$10 billion allocated to states, territories, and tribes through grants to prevent homeowner mortgage defaults, foreclosures, and displacements.

Funds may be used to reduce mortgage principal amounts, assist homeowners with housing payments and other aid needed to prevent eviction, mortgage default, foreclosure, or the loss of utility services.

Funds may also reimburse state and local governments that have provided similar assistance since January 2020.

Each state, along with the District of Columbia and Puerto Rico, will receive at least $50 million. Additional amounts will be set aside for other U.S. territories and tribes.

States, territories, and Tribes receiving funding will have to set aside at least 60% of their allocation to assist homeowners who make less than 100% of the local or national median income.

Homelessness Assistance and Supportive Services Program

$5 billion allocated to state and local governments to provide supportive services for homeless and at-risk individuals. Permitted fund uses include tenant-based rental assistance, housing counseling and homeless prevention services, and acquiring non-congregate shelter units.

Low-Income Home Energy Assistance Program (LIHEAP) and Water Assistance Program

$4.5 billion allocated to fund the LIHEAP program, and $500 million provided in state grants to assist low-income households with drinking water and wastewater services.

FEMA Disaster Relief Fund

$50 billion to reimburse state and local governments for the costs of ongoing COVID-19 response and recovery activities, and other emergencies.

Funding to remain available through FY 2025.

Final thoughts

With billions of dollars in aid becoming available to state, local and tribal government agencies, the use of these funds is going to be tracked very closely by federal regulators. If you have any questions about how funds can be utilized, and how to track and report this use, MGO’s dedicated State and Local Government team can help. Contact Us.

]]>