At a Glance…

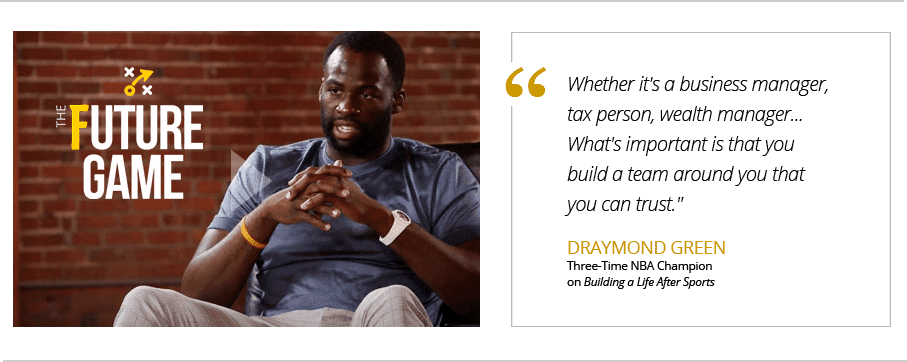

- A professional athlete is the CEO of the brand that bears his or her name. That’s why sports stars should turn to the strategies employed by the world’s most successful entrepreneurs and executives as a playbook for long-term success. In short, they need to think like a CEO.

- Building a high-performing team is the number-one priority for growth-oriented businesses, and it’s no different for the Athlete/CEO. Drawing from the proven team-building models of the corporate world and the entertainment industry, we’ve developed the MGO Model, tailored to the unique needs of Athlete/CEOs.

- The Business Manager is the Financial Quarterback of an Athlete/CEO’s team. He or she is responsible for the daily oversight of a client’s financial affairs. That includes tax planning and compliance, establishing budgets, paying the bills, managing cash flow, and advising on major financial decisions. The Athlete/CEO should carefully vet the qualifications of anyone serving in this critical role.

Background

In the first installment of this series, we noted that the financial profile of a professional athlete more closely resembles a mid-sized, private company than a typical household. While the economics can be exceptional, an alarming number of players lack the support structure necessary to navigate the depth and complexity of their financial requirements.

A professional athlete is the CEO of the brand that bears his or her name. To ensure the long-term value of that brand, the Athlete/CEO needs to embrace that role and reimagine their future beyond the playing field. In this series, we examine the mindsets and practices of some of the world’s most effective business leaders as a model for navigating the unique challenges and opportunities facing professional athletes.

Building a Team

John Wooden said, “The main ingredient to stardom is the rest of the team.” This is just as true in the business world as it is in the world of professional sports. That’s why the world’s top CEOs make team-building their first priority. The way they approach that process serves as a valuable roadmap for Athlete/CEOs.

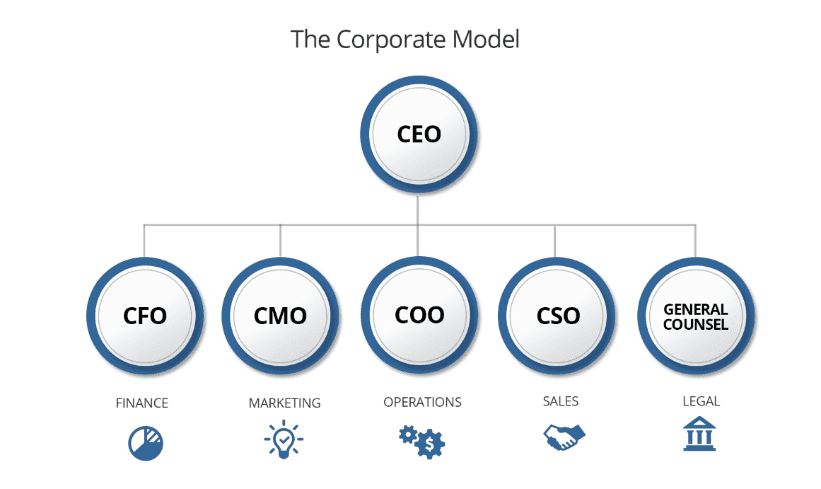

The Corporate Model

Most businesses share a common structural framework. While details may vary across different industries and global regions, the core elements of the Corporate Model (below) remain consistent. This framework identifies the primary business functions and areas of expertise critical to an organization’s success.

The Corporate Model has been successfully adapted to a wide variety of business categories, evolving as necessary to the unique needs of each organization’s operating environment. When working with athletes, perhaps the most relevant example is the entertainment industry.

The Hollywood Model

The Film & Television industry shares many of the traits of people working in professional sports. The quality of the product is determined largely by the quality of the talent in the spotlight – driving significant demand and high salaries for the best actors, directors, writers, etc. Over the years, Hollywood leaders recognized that many of the same principles of growth and financial governance in the corporate world apply to the financial lives of talent in Film & Television. This led to the evolution of what we call the Hollywood Model (shown below).

This model identifies the importance of each individual role in the Corporate Model, albeit by different names. For example, the Business Manager takes on the role of the Chief Financial Officer (CFO), serving as the quarterback of the client’s financial affairs.

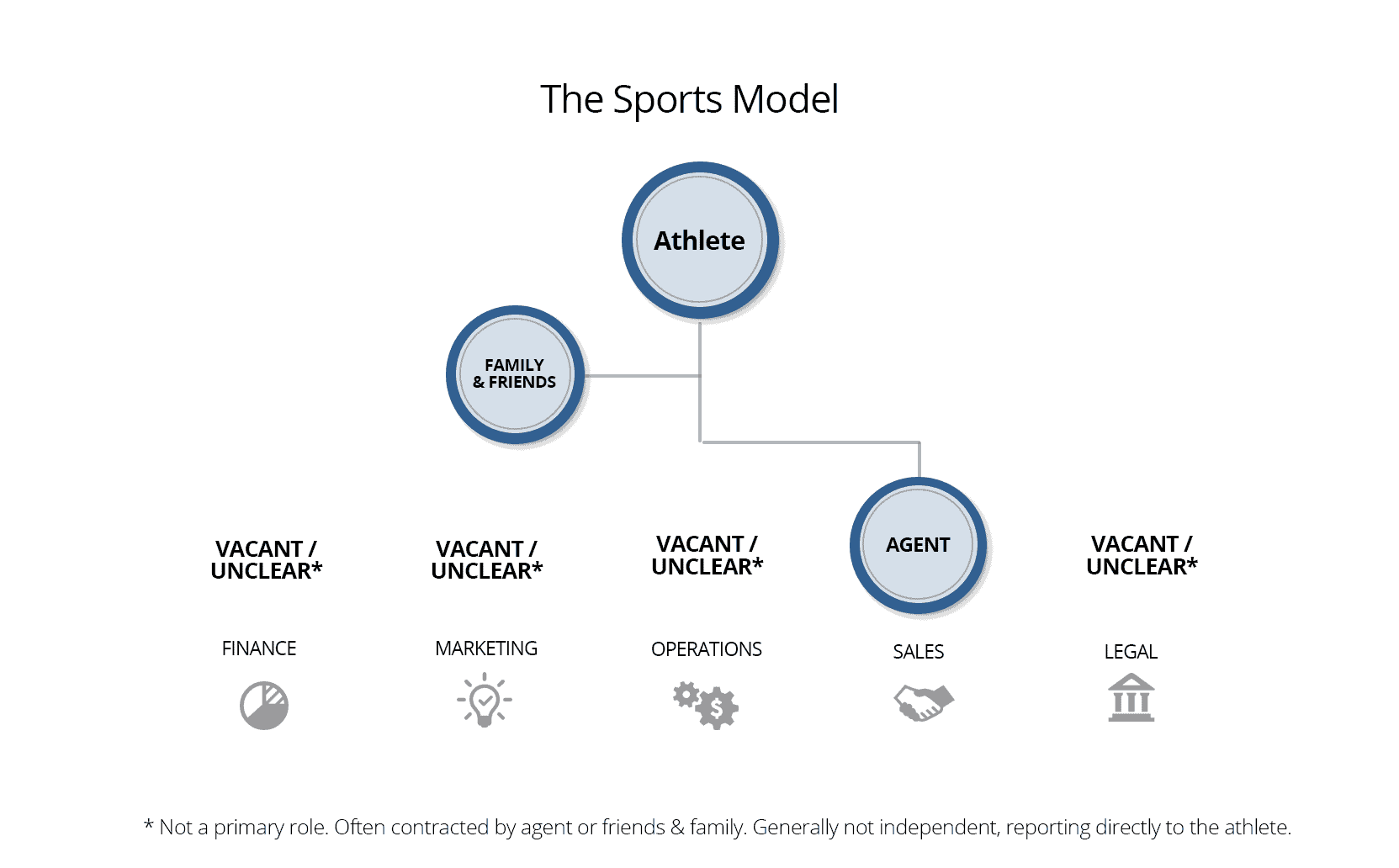

The Sports Model

Over the past several decades, the financial lives of professional athletes have grown increasingly complex. Salaries have grown significantly, as have endorsements, appearances, other sources of income, and the demands on each player’s time and attention. However, the average player’s support system has failed to evolve at the same pace. The model below shows how the support team of a typical athlete compares to Corporate Model.

While professional athletes understand the importance of experience, expertise, and teamwork, they often lack a clearly defined model for building their own teams off-the-field. The majority of highly publicized financial failures in professional sports stem from athletes who were either (a) missing key role players on their teams, or (b) trusting important roles to inexperienced or sometimes even unscrupulous acquaintances.

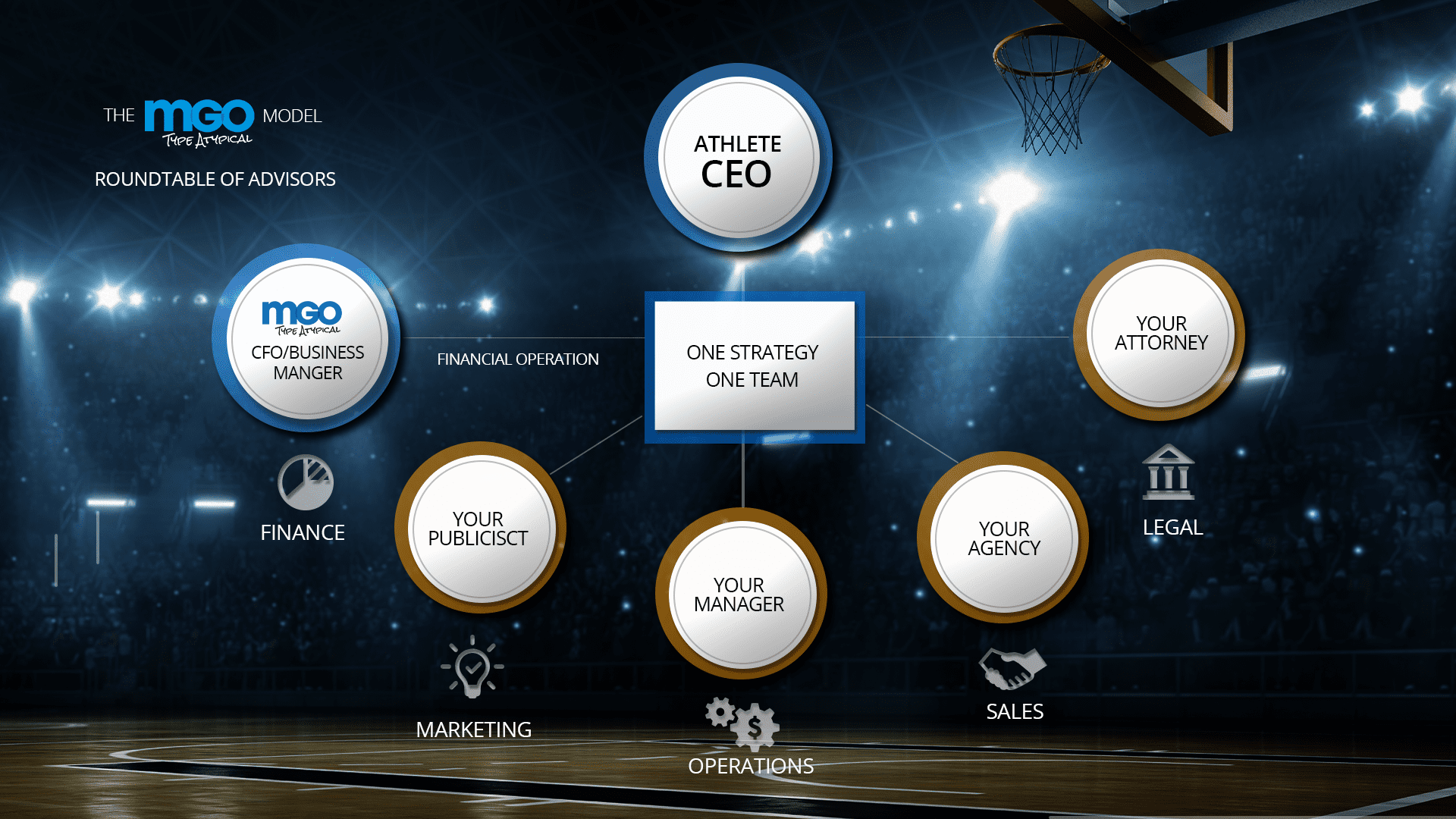

The MGO Model

At MGO, we’ve been fortunate to work with some of the most successful executives and entrepreneurs in the world – as well as many of the biggest names in Sports & Entertainment. As a result, we’ve come to know the traits and practices that drive success across industries.

The MGO Sports Model was developed to be a blueprint for Athlete/CEOs as they build their own teams. It identifies and defines the roles that are critical to success, while aligning the work of leading advisors under a common vision. While each role is important, we encourage clients to begin with the person who will serve as the quarterback of their daily financial lives; the CFO Business Manager.

The Financial Quarterback

In a recent article, Variety described the role of Business Managers in the Sports & Entertainment industry, stating, “Business Managers are the personal CFOs for celebrities, executives and athletes… They put their fortunes and their day-to-day lives in the hands of these trusted advisors.”

While each member of the Athlete/CEO’s team plays a vital role, the CFO/Business Manager is the person with the most tangible daily impact on a client’s financial life. He or she is the quarterback of the financial operation – responsible for hands-on, real-time execution of the financial plan. This includes establishing budgets paying the bills and monitoring the expenditures of anyone with access to the client’s accounts or credit cards.

Additionally, Business Managers serve as on-call financial advisors, working closely with clients on many of their most important financial decisions including family estates and trusts, tax planning, major purchases, potential investments, and charitable contributions.

High profile athletes are sometimes targets of investment scams and unwarranted requests for financial support. When these propositions come from friends, family and former acquaintances, a Business Manager can provide an important gatekeeper function. By establishing a recognized first point-of-contact for all financial requests, the majority of questionable requests can be filtered out before reaching the athlete.

Finally, the CFO/Business Manager works closely with the entire roundtable of advisors, ensuring that everyone is aligned and working together to implement a common strategy.

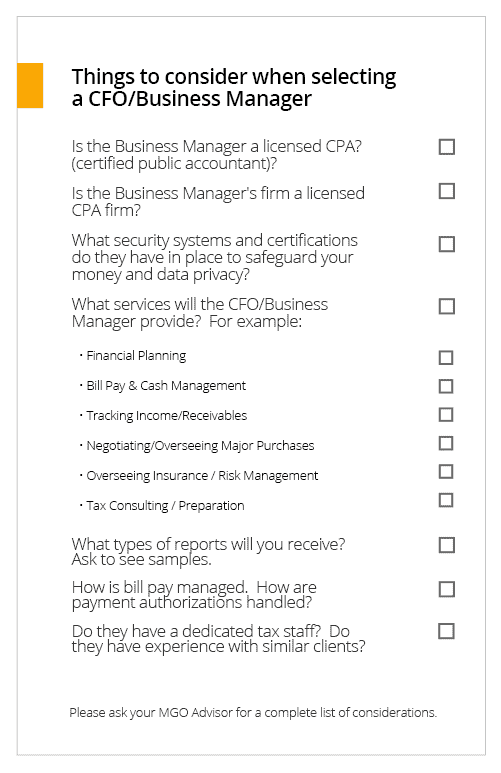

Selecting a CFO/Business Manager

Despite the critical role played by Business Managers in the financial lives of their clients, most states require no credentials to use the title Business Manager. As a result, there are people with little or no accounting experience using that title today.

Many of the highly publicized financial challenges in Sports & Entertainment have stemmed from unqualified and/or unethical advisors serving in the role of Business Manager for high profile clients. That’s why we suggest doing your own due diligence before hiring the quarterback of your financial team.

Questions? Let’s Talk.

]]>1. The corporate tax rate was permanently reduced from 35 percent to 21 percent.

The top corporate tax rate has been permanently reduced from 35 percent to a flat rate of 21 percent, beginning in 2018. Unlike all other provisions in the new law, including tax breaks for individuals, the new corporate tax rate provision does not expire.

2. There’s a tax break for owners of pass-through entities.

The new law provides owners of pass-through businesses — which include individuals, estates, and trusts — with a deduction of up to 20 percent of their domestic qualified business income, whether it is attributable to income earned through an S corporation, partnership, sole proprietorship, or disregarded entity. Without the new deduction, taxpayers would pay 2018 taxes on their share of qualified earnings at rates up to 37 percent. With the new 20 percent deduction, the tax rate on such income could be as low as 29.6 percent. It should again be noted that certain service industries are excluded from the preferential rate, unless taxable income is below $207,500 (for single filers) and $415,000 (for joint filers), under which the benefit of the deduction is phased out.

3. There might be huge tax benefits to changing your company’s current choice of entity.

Taxpayers should consider evaluating the choice of entity used to operate their businesses. The 21 percent reduced corporate tax rate may increase the popularity of corporations. However, factors such as the new 20 percent deduction for pass-through income, expected use of after-tax cash earnings, and potential exit values will significantly complicate these analyses. The potential after-tax cash benefits ultimately realized by owners could make choice-of-entity determinations one of the most important decisions taxpayers will now make.

4. There have been significant changes to the international tax system.

In connection with these changes, some U.S. shareholders who own stock in certain foreign corporations will have to pay a one-time “transition tax” on their share of accumulated overseas earnings. Other changes include a “participation exemption,” which is a 100 percent dividend-received deduction that permits certain domestic C corporations to receive dividends from their foreign subsidiaries without being taxed on such dividends when certain conditions are satisfied. There is also a new requirement that certain U.S. shareholders of controlled foreign corporations (CFCs) include in income their share of the “global intangible low-taxed income” of such CFCs. Finally, there are new measures to deter base erosion and promote U.S. production.

5. The corporate AMT and DPAD are dead, but Research Tax Credits live on.

The law repeals the Section 199 Domestic Production Activities Deduction (DPAD) and the corporate Alternative Minimum Tax (AMT) for tax years beginning after 2017. The Research Tax Credit was retained and is now more valuable given the reduction of the corporate tax rate from 35 percent to 21 percent.

6. They’ve scrapped NOL carrybacks and limited the use of carryforwards.

Previously, businesses were able to offset current taxable income by claiming net operating losses (NOLs), generally eligible for a two-year carryback and 20-year carryforward. Now NOLs for tax years ending after 2017 cannot be carried back, but can be indefinitely carried forward. In addition, NOLs for tax years beginning in 2018 will be subject to an 80 percent limitation. Companies will have to track their NOLs in different buckets and consider cost-recovery strategy on depreciable assets in applying the 80 percent limitation.

7. Tax reform’s impact on accounting methods may change when revenue is recognized, but new provisions could also lead to temporary and permanent tax benefits.

Under the new law, accrual basis taxpayers must now recognize income no later than the taxable year in which such income is taken into account as revenue in an applicable financial statement.

However, new provisions also provide favorable methods of accounting that were not previously available. That, coupled with the reduction in tax rates, creates a favorable and unique environment for filing accounting method changes.

There are many method changes still available for the 2017 tax year. Taxpayers should evaluate current accounting methods to identify any actionable opportunities to accelerate deductions and defer income for the 2017 tax year, which could result in significant tax savings.

8. There are new rules for bonus depreciation and full expensing on new and used property.

The new tax law allows a 100 percent first-year deduction — up from 50 percent — for the adjusted basis of qualifying assets placed in service after Sept. 27, 2017, and before Jan. 1, 2023, with a gradual phase down in subsequent years before sunsetting after 2026. The definition of qualifying property was also expanded to include used property purchased in an arm’s-length transaction. Businesses should pay close attention to any qualifying asset acquisitions made during the fourth quarter of 2017, as the full expensing can be taken on the 2017 return if the property was acquired and placed in service after Sept. 27, 2017.

Additionally, under new tax law, taxpayers may now deduct up to $1 million under Section 179 for properties placed in service beginning in 2018 — double the previous allowable amount. The phase-out threshold is increased to $2.5 million and will be indexed for inflation in future years and the types of qualifying property has been expanded.

9. The availability of the cash method of accounting expanded for small businesses.

Beginning in 2018, the average annual gross receipts threshold for businesses to use the cash method increases from $5 million to $25 million. Additionally, small businesses who meet the $25 million gross receipts threshold are not required to account for inventories and are exempt from the uniform capitalization rules. The $25 million is indexed for inflation for tax years beginning after 2018.

10. Now is the time to assess total rewards strategies.

Tax reform significantly impacts various components of an employer’s total compensation program — namely the expansion of the $1 million deduction cap on pay to covered employees; disallowed deductions for transportation fringe benefits provided to employees; income inclusion for employer-paid moving expenses; further deduction limitations on certain meal and entertainment expenses; and a two-year tax credit for employer-paid family and medical leave programs. As the IRS releases guidance, employers must immediately modify their payroll systems to reflect tax reform changes impacting individual taxpayers.

For more information about the impact of tax reform on the Government Contracting industry, please reach out to us.

]]>The deadline for implementation is Jan. 1, 2018, for calendar year publicly-held companies, and Jan. 1, 2019, for calendar year privately-held companies. Although the implementation date for non-public companies is over one year away, our dedicated Government Contractor practice specialists encourage clients to start evaluating the changes now to understand the impact on their financial statements.

In this article, we will provide an overview of the revenue standard’s main provisions, provide best practices for implementation methods, and identify key issues that may impact government contractors during implementation. This guidance will be especially beneficial to entities following the AICPA’s Industry Revenue Recognition Task Force for Aerospace & Defense.

Main provisions of the new standard

The new standard is more principle-based than current revenue recognition guidance and will require government contractors to exercise more judgement. The principle is based on a five-step model from the AICPA Revenue Recognition Guide:

Step 1: Identify the Contract with a Customer

The standard includes characteristics that need to be met for a contract to permit revenue recognition. In general, a contract exists if there is an agreement between a buyer and seller that creates enforceable rights and obligations for the two parties. Only when there is such an agreement is there any revenue to recognize under Topic 606. This step sets the base to which the rest of the steps in the model are applied.

Also included in this step is guidance on when to combine multiple contracts into a single contract for revenue recognition purposes, and what to do if a contract is modified, thereby changing the identified contract with a customer.

Step 2: Identify the Performance Obligations in the Contract

Among the rights and obligations that will be set forth in the contract (either explicitly or implicitly), are:

- 1. The right of the buyer to receive goods or services from the seller, and;

- 2. The obligation of the seller to provide those goods or services to the buyer.

Once the contract has been identified, the seller identifies what goods or services it has promised to provide to the buyer. The standard includes guidance on evaluating provisions of a contract to determine whether they should be regarded as creating promised goods or services.

If multiple goods or services are promised, the seller must determine whether each good or service is distinct from other goods or services in the arrangement, or must instead be combined with other goods or services to form a bundle that is distinct from other goods or services in the contract.

Each good or service that is distinct, or each bundle of goods or services that is distinct, is called a performance obligation under the standard. Performance obligations are then used as units that are evaluated for revenue recognition purposes in the rest of the model.

Step 3: Determine the Transaction Price

In addition to rights and obligations over goods or services to be provided, a contract will include:

- 1. The obligation of the buyer to pay the seller for the goods or services, and;

- 2. The right of the seller to collect that payment from the buyer.

Those provisions provide a starting point for determining the transaction price. Often, the payment terms are fixed and payment is due when goods or services are delivered. In that case, it is simple to determine the transaction price to be used in recognizing revenue.

However, the vendor needs to determine whether all amounts to be collected are appropriately reported as revenue. In addition, the contract may include terms that make the transaction price variable. For example, the transaction price could vary due to usage-based payments, award and incentive fees, rights of return or refund, or economic price adjustment.

Topic 606 explains when, and how much, variable consideration is to be included as part of the transaction price. This will generally require variable consideration to be included in the transaction price to the extent it is probable such consideration will become due under the contract.

Step 4: Allocate the Transaction Price to the Performance Obligations in the Contract

In this step, the transaction price determined in Step 3 is allocated, or assigned, to the performance obligations identified in Step 2. Obviously, if there is only one performance obligation, this allocation is easy, as the entire transaction price is allocated to the single performance obligation. However, if there are multiple performance obligations, the transaction price must be allocated to those performance obligations.

Generally, this is done based on the stand-alone selling prices of the performance obligations in the contract. The stand-alone selling price of a performance obligation may be objectively determinable if the performance obligation is regularly sold on a stand-alone basis. If it is not, its stand-alone selling price must be estimated through a reasonable technique.

Once stand-alone selling prices for all performance obligations are estimated, the transaction price is generally allocated based on the relative values of the performance obligations, effectively allocating any discount in the contract to the performance obligations on a pro rata basis.

Step 5: Recognize Revenue When (or as) the Entity Satisfies a Performance Obligation

Once the transaction price has been allocated to the performance obligations in the contract, the amount of revenue allocated to each performance obligation is recognized when, or as, the entity performs the obligation as required by transferring the promised goods or services that make up the performance obligation to the customer.

A good or service is deemed to be transferred to the customer when the customer gains control over the good or service. A customer sometimes gains control of promised goods or services as performance occurs over time. In other instances, the customer gains control of a promised good or service at a single point in time, often when something is physically delivered to the customer.

When a performance obligation is satisfied over time, the seller must determine an appropriate measure of its progress toward satisfying the performance obligation, and then recognize revenue based on that progress measurement applied to the amount of the transaction price allocated to the performance obligation.

When a performance obligation is satisfied at a point in time, the seller must determine the appropriate point in time at which to recognize as revenue the amount of the transaction price allocated to the performance obligation.

Implementation methods

Full retrospective application: Recast of prior period financial statements (with an adjustment to opening retained earnings for the first year presented). For example, for a public company, 2016 and 2017 would be recast to reflect the adoption of the new standard presented in the 2018 financial statements. The cumulative adjustment would be reflected as of Jan. 1, 2016.

Modified retrospective application: Cumulative effect of initially applying the standard is recorded as an adjustment to opening retained earnings of the period of initial application. Under the same example, 2016 and 2017 would not be recast in the 2018 financial statements. The cumulative adjustment would be reflective as of Jan. 1, 2018.

Implementation issues and guidance

For government contracts, the type of contract will determine if there will be a change from current revenue recognition practices. For time and materials and cost-plus-fixed-fee contracts, as well as services-based firm-fixed-price contracts, there will be minimal change to the total revenue and timing of revenue recognized under the new revenue standard. Under more complex contracts (i.e., award fees under cost-plus contracts, or firm-fixed-price contracts where the entity performs manufacturing, design, development, integration, and/or production), applying the new standard will require careful analysis and consideration, and could impact the timing of revenue recognition.

The AICPA’s Industry Revenue Recognition Task Force for Aerospace & Defense has identified various revenue recognition implementation issues and continually updates the list of issues as discussions continue.

The following are some of the key areas to consider when implementing the new guidance as noted in the AICPA’s Industry Revenue Recognition Task Force for Aerospace & Defense.

Acceptable Measure of Progress – what to consider when measuring progress towards completion of performance obligations satisfied over time.

Accounting for Contract Costs – considerations for applying the guidance in Financial Accounting Standards Board (“FASB”) Accounting Standards Codification (“ASC”) 340 for incremental costs of obtaining a contract, costs to fulfill a contract and amortization and impairment, to costs typically incurred in aerospace and defense contracts, including pre-contract costs and learning or start-up costs.

Variable Consideration – considerations for estimating the amount of variable consideration (incentive fees, award fees, economic price adjustments) in aerospace and defense contracts, the impact of subsequent modifications, and how to determine the amount of estimated variable consideration to include in the transaction price.

Significant Financing Component – considerations needed to assess whether a significant financing component exists in determining the transaction price for various types of aerospace and defense contracts.

Allocating the Transaction Price – considerations for determining how to allocate the transaction price to multiple performance obligations in aerospace and defense contracts.

Implementation plan for government contractors

The AICPA Financial Report Center developed an implementation plan that may be helpful as a starting point for developing your own implementation plan. Below are the high-level steps included in that plan.

- Designate the individual(s) responsible for overseeing implementation.

- Evaluate how the changes will impact how your company accounts for different types of revenue streams/contracts. Consider how the new standard will impact current performance metrics and compensation plans. Work with your auditor to discuss the completeness and accuracy of your analysis.

- Determine an implementation method (full or modified retrospective approach).

- Determine changes that may be needed within systems and/or software applications to facilitate revenue recognition under the new standard.

- Determine what interim disclosures may be required prior to the effective date.

- Develop a plan for implementation to incorporate the above steps, as well as train your staff.

- Educate the company’s management on the new standards and the impact you expect the changes to have on the company’s financial statements.

MGO has a dedicated Government Contractor practice with CPAs and industry specialists who are well-versed in the new standard and can assist in evaluating the impact of the changes on government contracts revenue recognition and financial reporting. We also assist our clients in implementing the new standard.

To learn more about how we can help, let’s talk.

]]>- Insufficient outreach to vendors

- Lowering of bonding requirements

- Burdensome administrative requirements

- Insufficient segregation of procurement approval and receiving duties

- Lack of cross-department evaluation of vendor proposals

- Inconsistent management and designated authority levels

- Organizations are unaware of procurement process times – from start of requisition until vendors are paid

- Procurement activities are not aligned with overall organizational activities

- Too many sign offs/approvals

If any of these issues sound familiar, or your organization has not reviewed its procurement function in a while, you run the risk that your procurement strategies are inconsistent with organizational needs, which can result in paying higher prices for the goods and services required to run your agency, insufficient number of competitive bids, or worse, violating your grant or service agreements.

IntelliBridge Partners has the expertise to improve the procure to pay cycle through business process reviews, risk assessments, and performance audits. If you would like help with your procurement department, please contact Greg Matayoshi at gmatayoshi@intellibridgepartners.com.

]]>The financial perils celebrities face in Hollywood

A professional athlete or a top tier individual in entertainment should look at their expanded wealth and the management of that wealth the same way a mid-sized company would. The person earning the income is the CEO of the business and their name is the brand. They need a CFO to manage finances who is supported by a team of experts who are the best in their fields of wealth management, diversified investing, and financial planning. This team then enables the talent to get the best use out of their wealth while still making provisions for a comfortable future.

A good partnership between a high earning professional and a financial team can yield endless results and allow earners to live comfortably now and long into the future when considering retirement. Trust is the key to a successful working relationship between a high-income client and their financial team. With that trust established; the future of an individual and their family will be assured with strategy, planning, and more than just a bit of market savvy.

The first step in working with a professional financial team is to take ownership of financial awareness and education. It’s important that the earner takes time whether over the phone, remotely through video conference, or when possible in person; to sit and talk to their financial professionals. This will help them understand how and why their money is being managed the way it is.

A financial team needs to be allowed to act as guardians of wealth

High-earning talent must allow their financial team to act as guardians and keepers of their money. In the worlds of sports and entertainment celebrity, very few things are ever denied top-earning talent, and quite often they are not acquainted with the word “no.”

This is where financial teams step in to not only shield talent from financial predators and bad investments, but to also protect the earner’s money from themselves by helping curb extravagant spending and off-the-wall purchases. A good financial professional team is the best line of defense against money disappearing with no return.

Establish current and future goals for the life you want

A series of goals must be set by the earner and their financial professionals to properly plan for the future. Where do you want to be when you retire? What kind of life do you want to have? With the money you have coming in, what sort of plans can you make for yourself and your family? It’s important that individuals set realistic goals that are guided by their financial team, and that they maintain solid credit through their more lucrative years so they have an excellent history to build from.

Work to establish a series of sound and profitable investments

Talent can work with their financial team to establish investments that will earn returns and dividends that they can draw upon once they are no longer working. Municipal Bonds and ETFs in efficient markets are examples of smart investments. There are a multitude of options available, and if your financial team is savvy; they can advise you in the world of alternative investments like casinos, restaurants, hotels, and newer

markets like cannabis.

Get the right insurance for your career and risk profile

The financial team must work to ensure that talent has adequate insurance. Athletes take risks with their bodies all the time, so it is important that a player maintains the correct type of insurance that will cover them if they are injured and are unable to return to playing for a season. Or in a worst case scenario, they are forced into early retirement by an injury. The same can is true for actors, directors, and professionals in the world of entertainment. On-set accidents do happen, and if a person is unable to work in their chosen field; their earnings drop to next to nothing.

There is an energy and synergy to money

There is a synergy and energy to the exchange of money. Money is like an electrical current and a flow must be maintained at all times for wealth to increase in size. There needs to be a give and receive in place when balancing an individuals’ investments and wealth, and there is always the value of giving vs. receiving to consider. This journey to finding a balance with a financial team and a true vision of what a person wants to achieve with their wealth and their life is a much broader topic; which we’ll be discussing soon enough. So, just keep your eyes open for further editorials in this ongoing series!

]]>