At a Glance…

- A professional athlete is the CEO of the brand that bears his or her name. That’s why sports stars should turn to the strategies employed by the world’s most successful entrepreneurs and executives as a playbook for long-term success. In short, they need to think like a CEO.

- Building a high-performing team is the number-one priority for growth-oriented businesses, and it’s no different for the Athlete/CEO. Drawing from the proven team-building models of the corporate world and the entertainment industry, we’ve developed the MGO Model, tailored to the unique needs of Athlete/CEOs.

- The Business Manager is the Financial Quarterback of an Athlete/CEO’s team. He or she is responsible for the daily oversight of a client’s financial affairs. That includes tax planning and compliance, establishing budgets, paying the bills, managing cash flow, and advising on major financial decisions. The Athlete/CEO should carefully vet the qualifications of anyone serving in this critical role.

Background

In the first installment of this series, we noted that the financial profile of a professional athlete more closely resembles a mid-sized, private company than a typical household. While the economics can be exceptional, an alarming number of players lack the support structure necessary to navigate the depth and complexity of their financial requirements.

A professional athlete is the CEO of the brand that bears his or her name. To ensure the long-term value of that brand, the Athlete/CEO needs to embrace that role and reimagine their future beyond the playing field. In this series, we examine the mindsets and practices of some of the world’s most effective business leaders as a model for navigating the unique challenges and opportunities facing professional athletes.

Building a Team

John Wooden said, “The main ingredient to stardom is the rest of the team.” This is just as true in the business world as it is in the world of professional sports. That’s why the world’s top CEOs make team-building their first priority. The way they approach that process serves as a valuable roadmap for Athlete/CEOs.

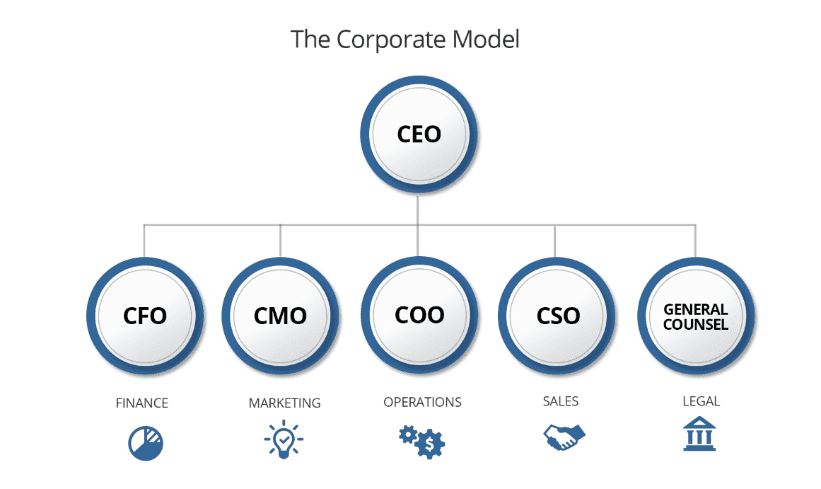

The Corporate Model

Most businesses share a common structural framework. While details may vary across different industries and global regions, the core elements of the Corporate Model (below) remain consistent. This framework identifies the primary business functions and areas of expertise critical to an organization’s success.

The Corporate Model has been successfully adapted to a wide variety of business categories, evolving as necessary to the unique needs of each organization’s operating environment. When working with athletes, perhaps the most relevant example is the entertainment industry.

The Hollywood Model

The Film & Television industry shares many of the traits of people working in professional sports. The quality of the product is determined largely by the quality of the talent in the spotlight – driving significant demand and high salaries for the best actors, directors, writers, etc. Over the years, Hollywood leaders recognized that many of the same principles of growth and financial governance in the corporate world apply to the financial lives of talent in Film & Television. This led to the evolution of what we call the Hollywood Model (shown below).

This model identifies the importance of each individual role in the Corporate Model, albeit by different names. For example, the Business Manager takes on the role of the Chief Financial Officer (CFO), serving as the quarterback of the client’s financial affairs.

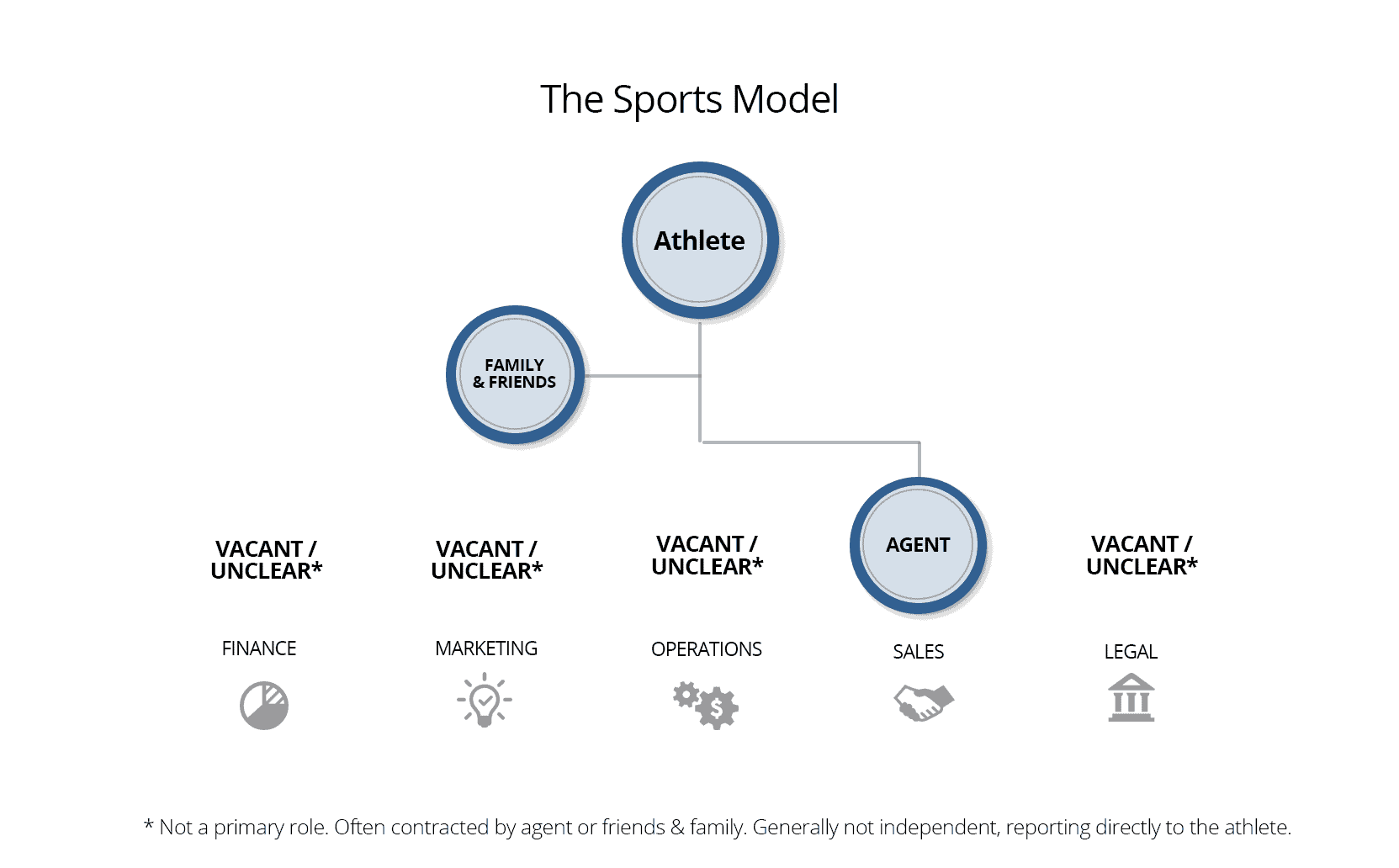

The Sports Model

Over the past several decades, the financial lives of professional athletes have grown increasingly complex. Salaries have grown significantly, as have endorsements, appearances, other sources of income, and the demands on each player’s time and attention. However, the average player’s support system has failed to evolve at the same pace. The model below shows how the support team of a typical athlete compares to Corporate Model.

While professional athletes understand the importance of experience, expertise, and teamwork, they often lack a clearly defined model for building their own teams off-the-field. The majority of highly publicized financial failures in professional sports stem from athletes who were either (a) missing key role players on their teams, or (b) trusting important roles to inexperienced or sometimes even unscrupulous acquaintances.

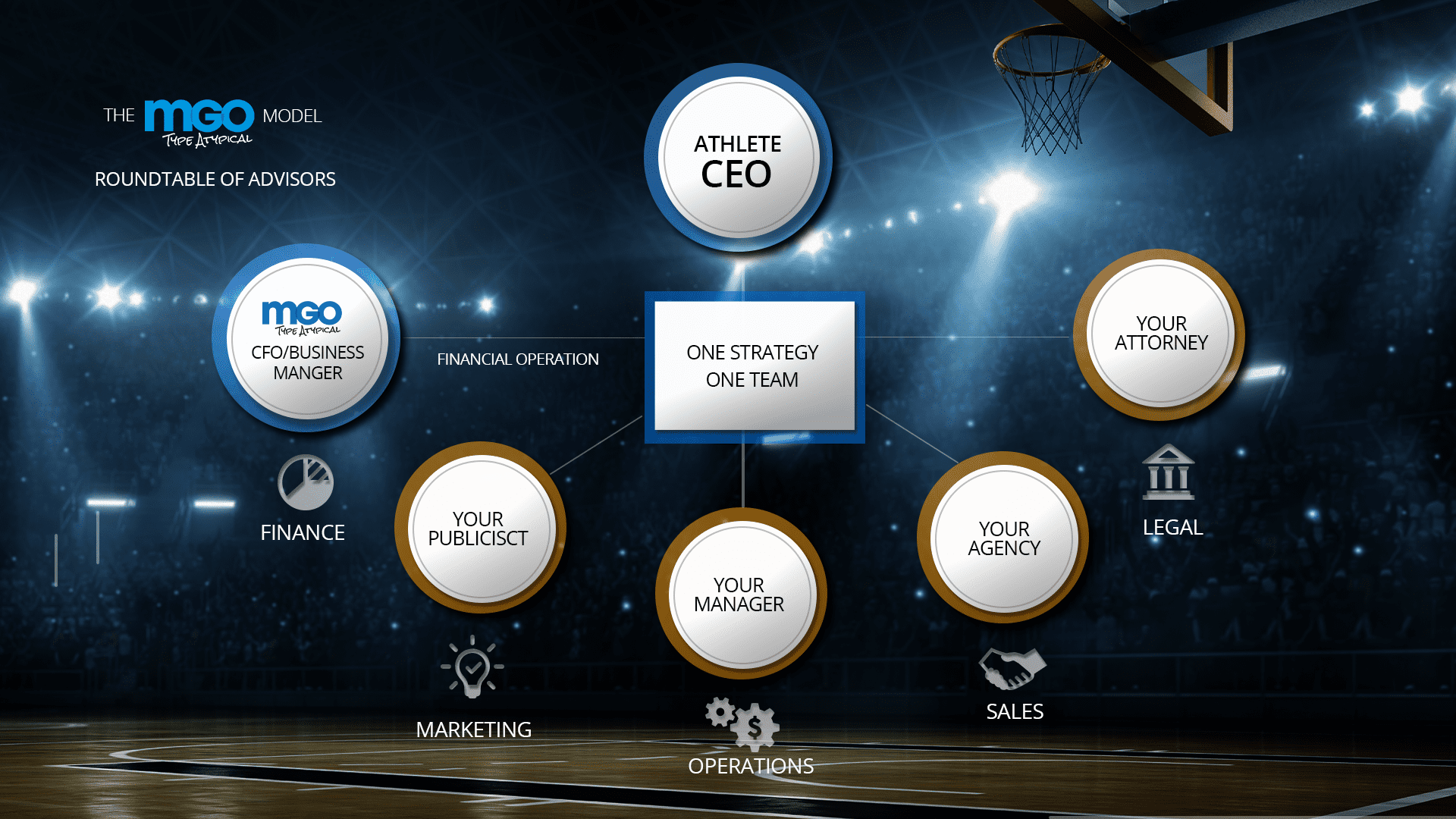

The MGO Model

At MGO, we’ve been fortunate to work with some of the most successful executives and entrepreneurs in the world – as well as many of the biggest names in Sports & Entertainment. As a result, we’ve come to know the traits and practices that drive success across industries.

The MGO Sports Model was developed to be a blueprint for Athlete/CEOs as they build their own teams. It identifies and defines the roles that are critical to success, while aligning the work of leading advisors under a common vision. While each role is important, we encourage clients to begin with the person who will serve as the quarterback of their daily financial lives; the CFO Business Manager.

The Financial Quarterback

In a recent article, Variety described the role of Business Managers in the Sports & Entertainment industry, stating, “Business Managers are the personal CFOs for celebrities, executives and athletes… They put their fortunes and their day-to-day lives in the hands of these trusted advisors.”

While each member of the Athlete/CEO’s team plays a vital role, the CFO/Business Manager is the person with the most tangible daily impact on a client’s financial life. He or she is the quarterback of the financial operation – responsible for hands-on, real-time execution of the financial plan. This includes establishing budgets paying the bills and monitoring the expenditures of anyone with access to the client’s accounts or credit cards.

Additionally, Business Managers serve as on-call financial advisors, working closely with clients on many of their most important financial decisions including family estates and trusts, tax planning, major purchases, potential investments, and charitable contributions.

High profile athletes are sometimes targets of investment scams and unwarranted requests for financial support. When these propositions come from friends, family and former acquaintances, a Business Manager can provide an important gatekeeper function. By establishing a recognized first point-of-contact for all financial requests, the majority of questionable requests can be filtered out before reaching the athlete.

Finally, the CFO/Business Manager works closely with the entire roundtable of advisors, ensuring that everyone is aligned and working together to implement a common strategy.

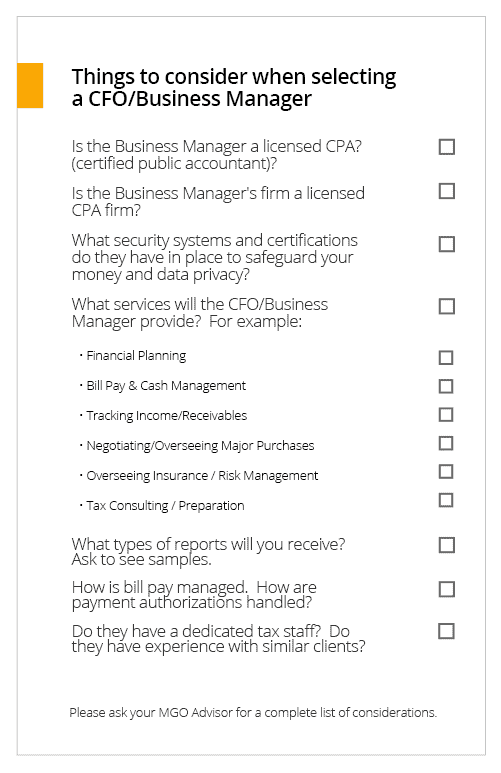

Selecting a CFO/Business Manager

Despite the critical role played by Business Managers in the financial lives of their clients, most states require no credentials to use the title Business Manager. As a result, there are people with little or no accounting experience using that title today.

Many of the highly publicized financial challenges in Sports & Entertainment have stemmed from unqualified and/or unethical advisors serving in the role of Business Manager for high profile clients. That’s why we suggest doing your own due diligence before hiring the quarterback of your financial team.

Questions? Let’s Talk.

]]>In the following we will explain five “business hygiene” initiatives that can have a major impact on your bottom line and improve financial and operational efficiency now, and long after the crisis has passed:

- Cash flow calibration

- Operational cost assessment, optimization and reduction

- Flexibility in payables and receivables

- Revenue optimization

- Tax planning

Cash flow calibration: Understand your cash flow

Cash is king, and the core question businesses need to answer right now is: “how much cash do I need to survive?” The answer will decide how the company maneuvers through the next few months.

The first step to realizing better cash flows is undergoing a frank assessment of your operating targets, specifically a labor analysis to optimize operational performance ensuring that revenues flow straight into the bottom line. Businesses need to take a hard look at business plans in conjunction with financial data and current operations to assess short-term liquidity needs, which will be the best guide to navigating through this volatile environment.

Cost-Assessment, cost-optimization, cost-reduction

Reducing costs is the natural next step to addressing a cash flow shortage, and if done strategically, it doesn’t have to impact value or revenue generation either.

Answering “How are we identifying removable cost?” will be at the center of this step. If there is one silver lining to this pandemic, it is that the standard virus response is already cutting them naturally. Reducing unnecessary travel, hiring freezes, and limiting discretionary spending are all the first steps that most of the business world has already taken.

The next step is to execute a risk process of evaluating necessary costs in alignment with value drivers. This will highlight inadequate use of financial resources and possible under optimize cost resulting in preventable operating expenses affecting your income statement.

Flexibility in payables and receivables

Under normal circumstances, it is often advised to expedite payments to suppliers and, if needed, take a slow approach to receivables. Today, companies need to take the exact opposite approach. Delaying payment to suppliers is a common strategy to preserve capital but be aware that communication is key across the supply chain so to not disrupt future operations. Expediting receivables and assuring quick payments will optimize cash flow from accounts. Ensuring a customer-centric and detailed invoicing process is central to minimizing relationship disruptions while doing so.

Taking both steps will allow a company to build liquid reserves to work from until the crisis abates.

Revenue optimization

The best entrepreneurs are those that think outside of the box and support their innovation with financial data. Revenue optimization is about evaluating the ability to grow through product offerings and the company’s ability to capitalize on market demand. The first step is to evaluate all the costs associated with production and determine if the price is in alignment with market demand. A successful pricing strategy is backed by actual financial data, as more products do not necessarily equate to more revenue.

The next step of optimizing your revenue is understanding your products lines’ demand in order to respond quickly to market movements (inventory movement). Let the data guide you to evaluate what is selling quickly and has high margins. Also identify cross-selling and upselling opportunities, with tactics like bundling, which could be used to generate more profit from the same customer.

Tax planning considerations

In response to the COVID-19 pandemic, legislators at the state and federal levels, including the IRS, have issued a broad range of tax relief programs aimed at supporting businesses during this crisis. There have been major updates to everything from tax deadlines to deferrals and key calculations.

For example, a change to qualified improvement property (QIP) calculations has created the opportunity for businesses to file amended tax returns with bonus depreciation that includes monies spent on facility repair.

Careful tax planning at this stage, informed by a deep understanding of recent tax code changes, can have a major impact on immediate cash flow, and long-term tax burden.

How MGO can help

Many businesses are experiencing severe cash-flow issues that affect the likelihood of continued operation. No solution should be overlooked at this stage. Consulting with experienced professionals could help identify opportunities to boost cash flow through operational, accounting and financial changes. If you’d like to schedule a consultation to discuss available options, please reach out to us.

]]>What is the cannabis banking crisis?

Very simply put, the conflict between state and local cannabis laws that allow for adult- and medicinal-use of cannabis are in conflict with federal laws that categorize cannabis as a Schedule I controlled substance. As a result, major banking institutions are reluctant to provide traditional banking services to cannabis companies due to the risk of federal prosecution for money laundering or a variety of other offenses.

As a result, the cannabis industry is almost exclusively cash-based. Cannabis business operations – including payroll, rent/lease payments, vendor payments and taxes – are primarily conducted with cash. This results in hundreds of thousands of dollars in cash being moved between locations, simply to pay farms or manufacturers, or even to pay taxes. This inefficient system leads to a wide variety of issues, including significant operational difficulties, and growing risk threats from both untrustworthy employees and out right robbery.

Cannabis businesses have found a number of creative ways to navigate the banking issue. Some business restructure so a professional services firm, not directly touching the cannabis, provides payroll and other financial services. Shops and dispensaries have adopted a variety of debit or gift card payment systems. And finally, a handful of cannabis operators have established relationships with local credit unions willing to work with the industry. But the vast majority of cannabis operators must navigate daily risks related to the collection and remittance of large cash sums.

The banking crisis hearing

“We’re trying to examine how outdated banking regulations on the federal level are hindering reform on the state level when it comes to marijuana,” said Democratic Congressman Gregory Meeks, chairman of the Consumer Protection and Financial Institutions subcommittee, in advance of Wednesday’s hearing. The event brought together a wide range of affected parties, including representatives of credit unions and banks, cannabis industry advocates, and finally government officials advocating for responsible cannabis laws.

The hearing was called to discuss the Secure and Fair Enforcement Banking Act of 2019 (SAFE act). The bill was introduced by a bipartisan coalition that includes Colorado Democratic Rep. Ed Perlmutter, Washington Democratic Rep. Denny Heck and Ohio Republicans, Rep. Steve Stivers and Rep. Warren Davidson. The SAFE act seeks: “To create protections for depository institutions that provide financial services to cannabis-related legitimate businesses, and for other purposes.”

Cannabis banking advocates emerge

Prior to the hearing, the American Bankers Association offered public support for the SAFE act, stating in part: “Simply excluding legal state cannabis activity from the banking sector has not prevented the growth and spread of this industry, but providing access to the banking system could help facilitate public safety, streamline tax payments, and enable effective oversight in the states where voters have chosen to embrace cannabis legalization.”

Fiona Ma, Treasurer for the State of California, offered her support for the bill in a written testimony that reads in part: “an effective safe harbor mechanism in federal law promotes the safety of the public, improves the efficiency of collecting the taxes and fees we use to regulate the industry, and does not allow the banks and credit unions to totally abdicate their responsibilities to know their customers and avoid illicit money laundering.”

“(Current laws) encourage tax fraud, add expensive monitoring and bookkeeping expenses and—most importantly—leave legitimate businesses vulnerable to theft, robbery and the violence that accompany those crimes,” said Maj. Neill Franklin, Executive Director of the Law Enforcement Action Partnership (LEAP). He closed his passionate testimony by stating that the “safety of thousands of employees, business owners, security personnel, police officers and community members is in your hands.”

What can cannabis businesses do until laws change?

The primary purpose of the hearing was to create public momentum for a change in cannabis banking laws. The House Financial Services subcommittee heard hours of public testimony, largely in support of changing federal laws to support the cannabis industry. While nothing concrete emerged from the hearing, allowing so many influential advocates and politicians to publicly support the cannabis industry represents a major step-forward.

It will be a long process before any laws change, but in the meantime there are a number of legal actions a cannabis business can take to alleviate the stress of being denied traditional banking relationships. Most of these, including restructuring a business or implementing alternative payment systems, are complex activities that require professional guidance to execute successfully.

Additionally, there are a number of cash management solutions and internal controls all cannabis businesses should implement to limit opportunities for fraud and criminal abuse, both internally and externally. The MGO | ELLO Cannabis Alliance has long been an advocate for responsible practices regarding cash management in the cannabis industry. The Alliance provides a comprehensive suite of risk management solutions designed to promote operational best practices in the cannabis industry.

For more information or to arrange a consultation, please contact us.

About the author:

Linda Hurley is the leader of the MGO | ELLO Alliance Governance, Risk, and Compliance practice. She has over 20 years of experience providing risk advisory, compliance, accounting, internal audit, and auditing services to a wide variety of public and private companies. She is primarily focused on providing cannabis enterprises with a holistic view of their risk and compliance needs. She designs and implements internal controls, risk management procedures, and governance practices that support every level of a cannabis organization.

]]>