- The Internal Revenue Service (IRS) instituted a moratorium on the processing of new Employee Retention Tax Credit (ERTC) claims due to an influx of fraudulent and exaggerated claims — primarily stemming from unscrupulous ERTC mills.

- As of July 31, 2023, the IRS Criminal Investigation division had initiated 252 investigations involving more than $2.8 billion in potentially fraudulent ERTC claims. Fifteen investigations have resulted in federal charges, with six of those resulting in convictions with an average sentence of 21 months.

- Taxpayers who are not certain of their eligibility should consult with a trusted tax professional for a second review and may want to avail themselves of the IRS’s new settlement and/or withdrawal programs.

The IRS recently took a drastic step to impede a wave of ineligible ERTC claims by halting the processing of new refund requests through at least December 31, 2023.

Ineligible ERTC claims have plagued the IRS since Congress enacted the credit in 2020. In fact, the IRS opened its 2023 “Dirty Dozen” list with warnings about common ERTC scams that taxpayers should be wary of. This prominently placed notice — as well as subsequent announcements from the IRS — alerted taxpayers to unscrupulous actors who have been advising employers to claim credits in excess of what they could legitimately qualify for while charging those employers hefty upfront fees or fees contingent on ERTC refunds.

In the wake of a flurry of IRS investigations that identified more than $2.8 billion potentially fraudulent claims, the halt on processing ERTC claims will allow the IRS to further focus their efforts on investigating and ultimately prosecuting fraudulent claims. In the following we’ll detail the impact of the IRS moratorium and provide guidance if you suspect you’ve been exposed to inaccurate or fraudulent ERTC claims.

Background on the ERTC

First established in 2020 by the Coronavirus Aid, Relief, and Economic Security (CARES) Act, the employee retention tax credit was critical — along with Paycheck Protection Program (PPP) — in giving businesses that struggled to navigate the pandemic’s challenges much needed resources to pay employees while the businesses were shut down or facing declining sales.

For most taxpayers, the ERTC was claimed on quarterly payroll tax returns encompassing the period March 13, 2020, through September 30, 2021 (i.e., first quarter of 2020 through the third quarter of 2021). For a small subset of businesses classified as “recovery startup businesses” (as defined below), the ERTC could also be claimed for the fourth quarter of 2021.

Despite the halt in processing by the IRS, eligible taxpayers are still able to claim the credit by filing amended quarterly payroll tax returns. Amended payroll tax returns for 2020 quarters are able to be processed by the IRS as long as they are filed on or before April 15, 2024, while amended payroll tax returns for 2021 quarters are able to be processed as long as they are filed on or before April 15, 2025.

The credit is calculated based on the “qualified wages” of employees. The maximum amount of payroll tax credit that an employer can claim per employee is $26,000.

Qualification Tests

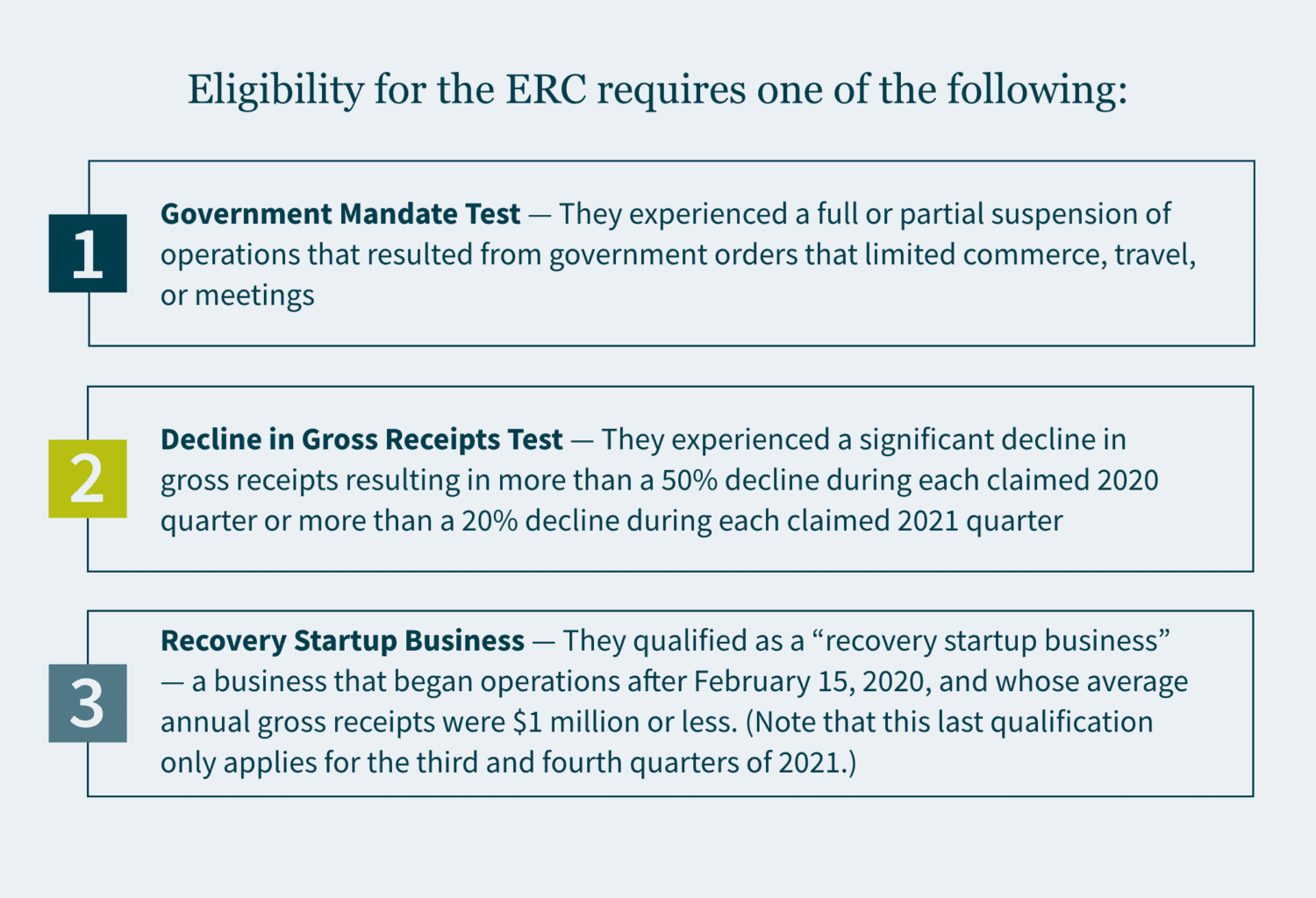

To be eligible for the ERTC, businesses must generally satisfy one of the following criteria for each of the quarters for which they are claiming the credit:

- Government Mandate Test — They experienced a full or partial suspension of operations that resulted from government orders that limited commerce, travel, or meetings.

- Decline in Gross Receipts Test — They experienced a significant decline in gross receipts resulting in more than a 50% decline during each claimed 2020 quarter or more than a 20% decline during each claimed 2021 quarter.

- Recovery Startup Business — They qualified as a “recovery startup business” — a business that began operations after February 15, 2020, and whose average annual gross receipts were $1 million or less. (Note that this last qualification only applies for the third and fourth quarters of 2021.)

The IRS Processing Moratorium

On September 14, 2023, the IRS announced that it would halt the processing of new ERTC claims through at least December 31, 2023. The IRS also stated that it plans to subject its queue of more than 600,000 existing ERTC claims to stricter compliance reviews, increasing the standard processing goal for those claims from 90 days to 180 days — with a potential for a much longer processing time for claims that require further review or audit.

This processing moratorium comes on the heels of a significant influx of claims – many of which the IRS believes are ineligible. The IRS stated that it has received more than 3.6 million ERTC claims over the life of the ERTC program, with about 15% of those claims being received in the 90-day period preceding the processing freeze. This amounts to roughly 50,000 claims still being received a week. To put this in perspective: the IRS has paid out about triple the amount that Congress had originally estimated for the program.

Additionally, as of July 31, 2023, the IRS Criminal Investigation division had initiated 252 investigations involving more than $2.8 billion in potentially fraudulent ERTC claims. Fifteen of the 252 investigations had resulted in federal charges, with six of those resulting in convictions. Four of the six convictions had reached the sentencing phase with an average sentence being 21 months.

The IRS intends on utilizing the moratorium to add more safeguards to the processing of ERTC claims, to protect businesses by decreasing the momentum of the pop-up ERTC mill industry, and to provide several solutions for taxpayers who submitted invalid claims. Those solutions include:

- A claim withdrawal program will be rolled out in Fall 2023 allowing businesses to withdraw ERTC claims that have not been processed or paid, even if those claims are under audit or awaiting audit.

- A claim settlement program rolling out in Fall 2023 that will allow businesses to repay ERTC claims, while also avoiding penalties and future compliance actions. (Note that fraudulent claims may still be subject to criminal referral.)

How to respond to IRS scrutiny of ERTC claims

Given the expected extra scrutiny that businesses can expect to face on their claims, businesses should review ERTC claims that they have made and/or intend to make where there are any doubts regarding the eligibility of those claims:

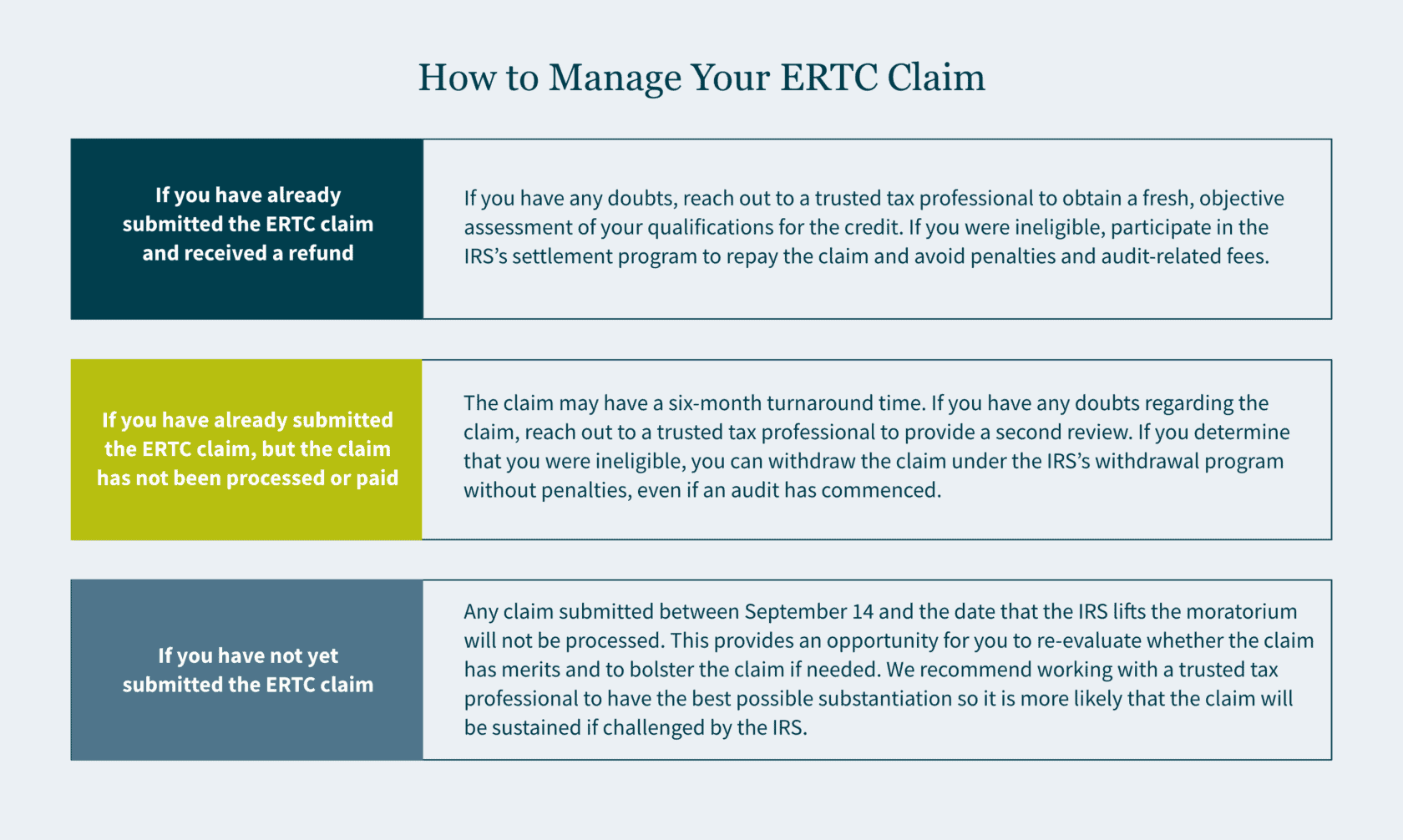

- If you have already submitted the ERTC claim and received a refund: If you have any doubts regarding your eligibility, we recommend reaching out to a trusted tax professional to obtain a fresh, objective assessment of your qualifications for the credit. If you determine that you were ineligible, you can participate in the IRS’s settlement program so that you can repay the claim, avoiding both penalties and audit-related fees.

- If you have already submitted the ERTC claim, but the claim has not been processed or paid: The claim will take longer to process than during the summer — increasing from a three-month turnaround time to a likely six-month turnaround time. If you have any doubts regarding the claim during this period, we recommend reaching out to a trusted tax professional to have a second review of the claim. If you determine that you were ineligible, you can withdraw the claim under the IRS’s withdrawal program without penalties, even if an audit has commenced.

- If you have not yet submitted the ERTC claim: Any claim submitted between September 14 and the date that the IRS lifts the moratorium – currently after December 31, 2023 – will not be processed. This should provide an opportunity for you to re-evaluate whether the claim has merits and to bolster the claim if needed. We recommend working with a trusted tax professional to have the best possible substantiation for your claim so that it is more likely that the claim will be sustained if challenged by the IRS.

How MGO can help

MGO’s ERTC Second Look program is geared towards the types of objective, trustworthy reviews that would benefit you during this time of heightened ERTC claim scrutiny. Our experienced Credits & Incentives team can identify audit red flags, areas that need more substantiation, miscalculations, and incomplete filings. In addition, our Tax Controversy team — in tandem with our Credits & Incentives team — can defend you if any of your ERTC claims are challenged by the IRS, with the ability to represent you during audit, appeals, and tax court. Contact us to learn more.

]]>- There is still uncertainty about how to account for the refundable Employee Retention Credit in your books, because you can’t account for it the same way you can account for the Paycheck Protection Program loan.

- The standards you can choose from are FASB ASC 958-605, International Accounting Standard (IAS) 20, FASB ASC 450-30, and FASB ASC 832.

- Depending on the standard you choose, you might have to consider the timing of recognition, the presentation of a grant income line, and financial ratios.

The Paycheck Protection Program (PPP) and the Employee Retention Credit (ERC) were powerful economic stimulus programs instituted during the COVID-19 pandemic to provide financial relief to struggling businesses. Both programs were the first initiatives of their kind, and as a result, there remains some uncertainty about what standards apply when accounting for them in your financial statements and records.

If you’re wondering how to distinguish the two, as well as determine the standard you should be utilizing, Angel Naval, a leader in our Client Accounting Solutions practice, breaks it down.

The PPP versus the ERC

Created to aid businesses facing financial challenges through the pandemic, there are several key differences between the PPP and the ERC.

The PPP is a loan and was created for small businesses with less than 500 employees in mind, giving them the funds needed to cover payroll and other eligible expenses. This includes hiring back employees who were laid off and covering applicable overhead. The loans are forgiven if the proper criteria are met (I.e., maintaining payroll and keeping consistent employee numbers).

A subset of the PPP loan, the ERC is a refundable tax credit that allows businesses to reduce their tax liability based on the qualified wages they’ve paid to their employees during the pandemic. It was created for businesses of all sizes to capitalize on in order to avoid layoffs. They can claim up to $5,000 per employee in 2020 and $7,000 per employee per quarter in 2021.

Determining the appropriate accounting standard for ERCs

If you took advantage of the ERC, currently, there is no straightforward way of accounting for it. Put simply, the ERC is a gray area because it’s so new, and there isn’t a straightforward way of accounting for it. Plus, ERCs are payroll credits, not income tax credits — and while FASB has extensive guidance for accounting for income taxes in ASC 740, it doesn’t for payroll taxes. Even the American Institute of Certified Public Accountants (AICPA) has suggested different standards, so it’s up to you to apply your best judgement based on the facts and circumstances of your business. Some things to consider:

- The timing of recognition,

- The financial ratios important to you, and

- Whether you want to present a grant income line.

For income statement presentation, according to AICPA’s December 2022 report, more public entities are crediting the associated expense rather than recognizing the amounts on a separate line item.

For example, you may think you can account for the ERC the same way you can for the PPP, but you can’t. As we differentiated above, the PPP is a loan and the ERC is a payroll credit, therefore the PPP is subject to debt and liability standards and the ERC is not. While the PPP did come first, those companies that have paid payroll taxes but still qualified for the ERC are still able to retroactively claim the credit.

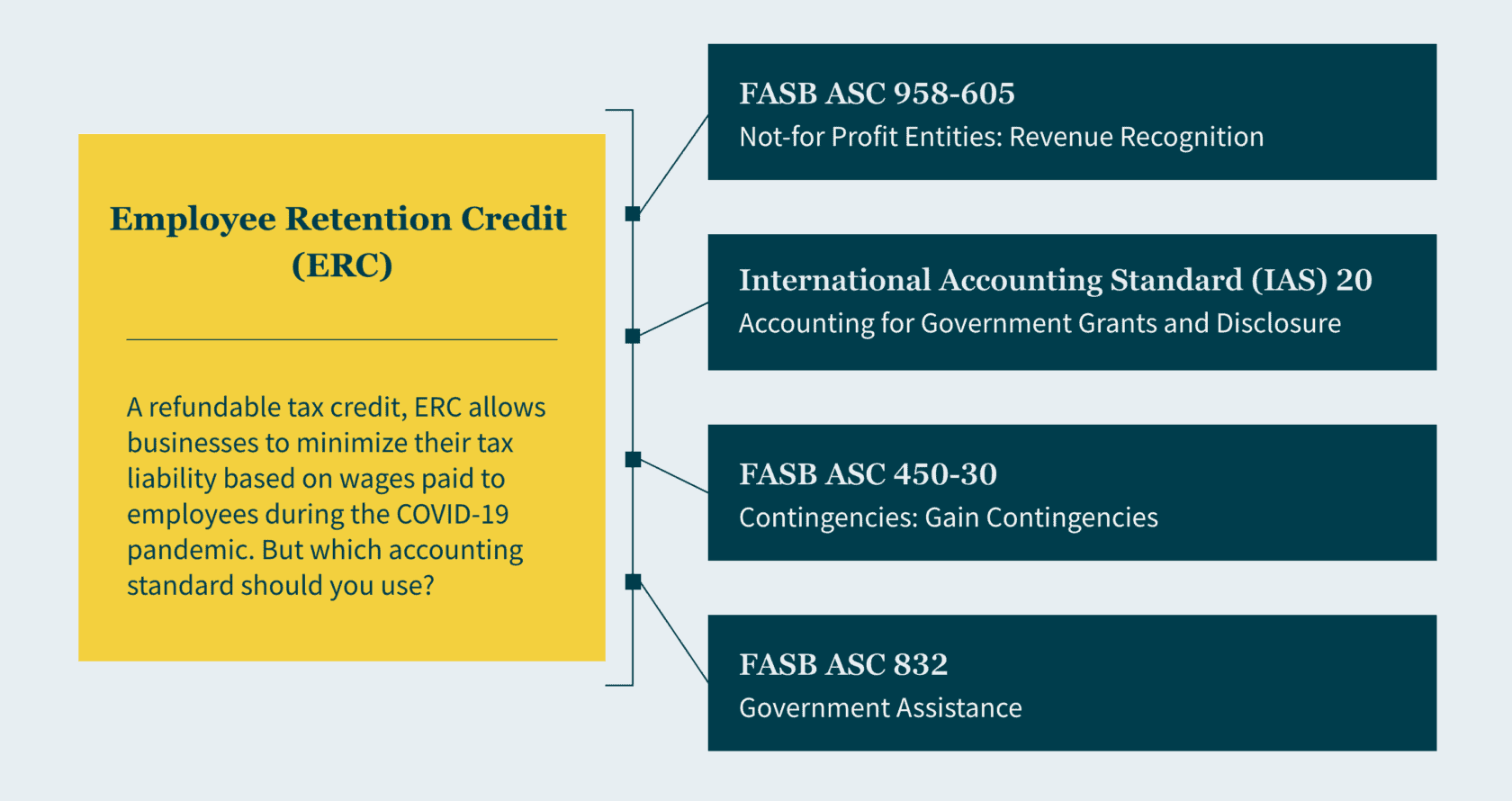

For prospective applications, for-profit entities can adhere to guidance in one of the following.

FASB ASC 958-605

If you’re applying the revenue recognition model under ASC 958-605, ERCs are treated as conditional contributions. In this case, companies must have met the program’s eligibility conditions to record revenue (and no amounts can be recorded until all criteria are evaluated and “substantially” met according to regulations). Given the conditions are met, a refund receivable and income should be recognized in the period the entity determines the conditions have been substantially met. This standard requires that gross revenue be recorded, and it doesn’t permit any netting of revenue against related expenses.

Some barriers to meeting ASC 958-605’s requirements include the eligibility requirements, like meeting the rules for a decline in gross receipts as well as incurring qualifying expenses (i.e., payroll costs). To file for the ERC, you’ll need to decide whether preparing the related ERC form and filing it with the government presents a barrier you’ll need to overcome. Note administrative and other small stipulations do not represent a barrier.

IAS 20

If you’re applying IAS 20, you can’t recognize the ERC until the “reasonable assurance” threshold is met in correlation with ERC’s conditions and receiving the credit. In this case, “reasonable assurance” translates to “probable” under GAAP standards and is easier to satisfy than “substantially met” in Subtopic 958-605. Once you’ve provided reasonable assurance that conditions will be met, the earnings impact of the government grants is recorded over the periods in which you recognize as expenses the related costs that the grants are intended to cover. So, you’ll need to estimate the amount of the credit you expect to keep.

IAS 20 allows you to record and present either the gross amount as other income or net the credit against other related payroll expenses. For every quarter that a company meets the recognition criteria, it records a receivable and either other income or net expense.

FASB ASC 450-30

If you’re interested in applying FASB ASC 450-30, please note amounts related to the ERC wouldn’t be recognized under this model until all uncertainties regarding the disposition of the credit are resolved — and there’s less detail on the disclosure, measurement, and recognition requirements as compared to the other standard models. For this reason, the AICPA doesn’t believe this model to be a preferred accounting policy for the ERC.

FASB ASC 832

If you’re applying this model, you must disclose several specifics about transactions with a government within its scope. These entail the nature of the transactions, which includes a description of the transactions as well as the form in which it has been received, whether it’s cash or other assets. You must also detail the accounting policies you used to account for the transactions. Any line items on the balance sheet and income statement that are affected by the transactions must be accounted for too — plus, the amounts applicable to each financial statement line item in the current reporting period.

How MGO can help

While there are clear accounting standards for the PPP, there is still some uncertainty surrounding the ERC. Depending on the standard you choose, you may have to consider the timing of recognition, financial ratios, and whether to present a grant income line. Therefore, businesses need to apply their best judgment based on the facts and circumstances of their business when accounting for ERCs. Our Client Accounting Solutions team has extensive experience helping clients navigate complex tax regulations post-pandemic. Contact us to learn more about which standard you should be using for federal relief programs.

About the author

Angel Naval oversees our West Coast Financial Advisory Services practice and provides value-added guidance for your corporate finance, financial planning, and business process needs.

]]>Now is a good time to evaluate and improve your financial reporting process for grants. While grants are subject to many reporting requirements, we will focus on revenue recognition under accounting principles generally accepted in the United States of America (GAAP) and the schedule of expenditures of federal awards, as required by Uniform Guidance.

Financial reporting in accordance with GAAP

In June 2020, the Governmental Accounting Standards Board (GASB) issued Technical Bulletin No. 2020-1, Accounting and Financial Reporting Issues Related to the Coronavirus Aid, Relief, and Economic Security Act (CARES Act) and Coronavirus Diseases (TB 2020-1). TB 2020-1 helps governments navigate the complexities of accounting for CARES Act funding. It addresses issues such as the type of financial assistance, characterization of loss of revenue, and effect of amendments. While ARPA funds have their own complexities, the principles established in TB 2020-1 for the CARES Act translate well to ARPA, and GASB has not published further guidance for ARPA.

In TB 2020-1, GASB provides guidance that the Coronavirus Relief Fund (CRF) resources are voluntary nonexchange transactions subject to eligibility requirements. The Local Fiscal Recovery Funds in ARPA are like the CRF resources in the CARES Act and should be treated consistently. This means the award should be recognized in the period when all applicable eligibility requirements are met.

When evaluating revenue recognition for voluntary nonexchange revenues, remember that the recipient cannot incur allowable costs until there is an executed grant agreement. For the ARPA funds, this means the recipient has signed all the required documents accepting grant terms and conditions, and that the recipient has received confirmation of the award before the end of its reporting period.

The presumed applicable period is the immediate provider’s fiscal year and begins on the first day of that year, based on the provider’s appropriation to disburse the resources. For the CARES Act, few cities met the threshold for directly awarded metropolitan cities, which subjected them to the state’s provisions rather than as a direct recipient of the federal government. For example, California cities and counties that received pass-through awards from the State of California were unable to recognize grant revenue in fiscal year ended June 30, 2020, because the State of California did not make the appropriations available to governments until July 1, 2020, through passage of its budget act.

The ARPA funds, which were directly distributed to a considerably greater number of recipients, were appropriated immediately by the federal government upon signing ARPA into law. That means the direct recipients of ARPA funds and the non-entitlement units of governments that received their allocations from states that executed the awards before the end of the reporting period, may recognize revenue immediately upon execution of the award, if they met the eligibility criteria.

For those governments that received cash before the end of the reporting period, a liability should be reported for the portion of financial assistance that was not recognized as revenue. For those governments that did not receive cash before the end of the reporting period, a receivable should be reported for the portion of financial assistance that was recognized as revenue.

The possibility of a single audit

While many governments require an annual single audit due to the amount of federal awards received each year, many others are below the threshold for requiring a single audit. Funding related to COVID-19 resources may push more governments over that $750,000 threshold.

For governments unfamiliar with single audits, it is important to prepare. Taking inventory and reading the guidance provided by the Office of Management and Budget (OMB) and awarding federal agencies will help you understand and equip yourself to submit (and pass) a single audit.

What is the SEFA?

The schedule of expenditures of federal awards (SEFA) acts as a supplemental schedule to the financial statements that an organization produces when it is subject to a single audit requirement. This requirement is triggered when the federal expenditures reported on the SEFA exceed $750,000 or more over the organization’s fiscal year

Preparing the SEFA is no small task. It must be completed in accordance with the Uniform Guidance and include all federal expenditures. In addition to determining the amount of federal expenditures, the Uniform Guidance specifies how the amounts are to be reported. Individual federal programs should be listed by federal agencies, and pass-through entities should be noted as well.

The single audit and ARPA

On March 19, 2021, the OMB released a memo that detailed single audit updates to be aware of in ARPA. The updates give awarding agencies the discretion and the authority to grant some exceptions to recipients who are affected by the pandemic if they are permissible by law. These entities do not necessarily have to be recipients of COVID-19 related financial assistance to receive these exceptions.

The most notable update is the extension of the single audit submission due date. For those recipients who did not file their single audits with the Federal Audit Clearinghouse by March 19, 2021, and had fiscal year-ends through June 30, 2021, the submission of their reporting packages was extended to six months past the normal due date, and no action by the awarding agencies or recipients is necessary. However, the documentation showing the reason for the delay in filing must be retained.

Additional updates include:

- Awarding agencies may allow some necessary incurred pre-award costs.

- Awarding agencies may allow extensions of awards, which gives recipients more time to resume projects and expend the funds.

- Prior approval requirements may be waived.

- Awarding agencies can grant recipients up to a three-month extension beyond the normal due date to submit financial, performance, and other required reports.

- The award application deadlines can be flexible.

While it is clear the OMB is attempting to be reasonably flexible, maintaining clear documentation of your grants and expenditures will be helpful as new and changing guidance becomes available.

Understand the current requirements and look for changes

The pandemic threw many organizations into survival mode. However, with federal, state, and local support many have weathered the financial difficulties over the past 18 months as well as can be expected. As organizations move forward, they will have to account for how they survived, where the monetary support came from, and where the money went. The near future will require unprecedented diligence, flexibility, and perhaps most of all, patience.

MGO is here to help

Guidance over grant funding, especially as it relates to CARES Act and ARPA programs, are continuing to develop and evolve. It’s important to stay on top of the latest changes and updates, as utilization of these resources are critical to the financial recovery of your organization and the proper reporting of those resources to stakeholders and the federal agencies charged with oversight. If you need personalized guidance, don’t hesitate to reach out to your MGO contacts.

.

]]>The guidance comes as Congress weighs ending the ERTC early to help offset the costs of the pending infrastructure bill. As of now, the credit is worth as much as $28,000 per employee for 2021, or $7,000 per quarter.

ERTC essentials

The CARES Act generally made the ERTC available to employers whose:

- Operations were fully or partially suspended due to a COVID-19-related government shutdown order, or

- Gross receipts dropped more than 50% compared to the same quarter in 2019

The credit originally equaled 50% of “qualified wages” — including health care benefits — up to $10,000 per eligible employee from March 13, 2020, through December 31, 2020. As a result, the maximum benefit for 2020 was $5,000 per employee.

And initially, businesses couldn’t benefit from both the ERTC and the popular Paycheck Protection Program (PPP). Most opted for the PPP, which, among other advantages, put money into their pockets more quickly than the credit.

In December 2020, the Consolidated Appropriations Act (CAA) provided that employers that receive PPP loans still qualify for the ERTC for qualified wages not paid with forgiven PPP loans. It also extended the credit through June 30, 2021.

In addition, the CAA raised the amount of the credit to 70% of qualified wages, beginning January 1, 2021, and boosted the limit on per-employee qualified wages from $10,000 per year to $10,000 per quarter — so employers could obtain a credit as high as $7,000 per quarter per employee.

The CAA also expanded eligibility by reducing the requisite gross receipt reduction from 50% to only 20%. And it increased the threshold for determining whether a business is a “large employer,” and therefore subject to a more stringent standard when computing the qualified wage base, from 100 to 500 employees.

The ARPA extended the ERTC through the end of 2021. It also made some changes that apply solely to the third and fourth quarters of 2021.

Guidance on ARPA changes

The majority of the IRS guidance deals with issues raised by the ARPA’s ERTC-related provisions, including:

Applicable employment taxes. Under the CARES Act, employers could claim the ERTC only against Social Security taxes. The guidance states that, for the third and fourth quarters of 2021, employers are entitled to claim the credit against their share of Medicare taxes, with the excess refundable.

Maximum amount. The maximum credit of $7,000 per employee per quarter for the first and second quarters of 2021 continues to apply to the third and fourth quarters. A separate limit applies to so-called “recovery startup businesses,” though.

Recovery startup businesses. The ARPA expanded the pool of ERTC-eligible employers to include those that:

- Began operating after February 15, 2020, and

- Have average annual gross receipts for the three previous tax years of less than or equal to $1 million.

These employers can claim the credit without suspended operations or reduced receipts, up to $50,000 total per quarter for the third and fourth quarters of 2021.

The guidance clarifies that a taxpayer hasn’t begun operating until it has begun functioning as a going concern and performing those activities for which it was organized. It also provides that the determination of whether a taxpayer is a recovery startup business is made separately for each quarter.

Qualified wages. The ARPA directs extra relief to “severely financially distressed employers” with less than 10% of gross receipts for 2021 when compared to the same calendar quarter in 2019. These businesses may count as qualified wages any wages paid to an employee during any calendar quarter — regardless of employer size.

Note that the ARPA prohibits “double dipping.” Wages taken into account for several business tax credits (for example, the research, empowerment zone and work opportunity tax credits, as well as credits for COVID-related paid sick and family leave) can’t also be taken into account for purposes of the ERTC.

Interplay with shuttered venue and restaurant revitalization grants. According to the guidance, recipients of a Shuttered Venue Operator Grant or a Restaurant Revitalization Fund grant may not treat any amounts reported or otherwise taken into account as payroll costs for those programs as qualified wages for ERTC purposes. Such employers must retain documentation that supports the ERTCs they claim.

Miscellaneous issues

The guidance addresses several other lingering issues related to the ERTC for 2020 and 2021. For example, it clarifies the definition of a “full-time employee.”

The notice explains that employers needn’t include full-time equivalents when calculating the average number of full-time employees for purposes of determining whether an employer is a large or small eligible employer. But, for purposes of identifying qualifying wages, an employee’s status is irrelevant, so wages paid to non-full-time workers may be treated as qualified wages (assuming all other applicable requirements are met).

The guidance also sheds further light on the:

- Treatment of tips and the Section 45B credit,

- Timing of qualified wage deduction disallowance,

- Alternative quarter election for 2021,

- Requirements to file amended federal income tax returns.

- Gross receipts safe harbor, and

- Exclusion of wages paid to the majority owners of corporations.

The rules regarding the last item above, which attribute ownership to owners’ family members, could significantly reduce the amount of the ERTC for family-owned corporations. A footnote in the guidance indicates that even the wages paid to minority owners might end up excluded from the ERTC computation.

ERTC’s future is uncertain

The U.S. Senate has passed infrastructure legislation that would eliminate the ERTC for the fourth quarter of 2021. However, the House of Representatives is on recess until the fall, so the fate of the credit remains uncertain. Contact us for additional information regarding the latest ERTC guidance.

]]>Employee Retention Tax Credit

The Employee Retention Tax Credit (ERTC) is a refundable tax credit created by the Coronavirus Aid, Relief and Economic Security (CARES) Act, to encourage businesses to keep employees on their payroll. For 2020, the credit is 70% of up to $10,000 in wages paid by an employer whose business was fully or partially suspended because of COVID-19 or whose gross receipts declined by more than 50%

For 2021, an employer can receive 70 percent of the first $10,000 of qualified wages paid per employee in each qualifying quarter. The credit applies to wages paid from March 13, 2020, through December 31, 2021. And the cost of employer-paid health benefits can be considered part of employees’ qualified wages.

It’s an attractive credit if you qualify.

Eligible businesses

The credit applies to all employers regardless of size, including tax exempt organizations that had a full or partial shutdown because of a government order limiting commerce due to COVID-19 during 2020 or 2021. With the exceptions of state and local governments or small businesses that take Small Business Administration loans, this credit is available to almost everyone.

Of course, there is some fine print:

• To qualify, gross receipts must have declined more than 50 percent during a 2020 or 2021 calendar quarter, when compared to the same quarter in the prior year.

• For employers with 100 or fewer full-time employees, all employee wages qualify for the credit, whether the employer is open for business or shutdown.

• For employers with more than 100 full-time employees, qualified wages are wages paid to employees when they are not providing services due to COVID-19-related circumstances.

One bright point about the ERTC is that employers can be immediately reimbursed for the credit by reducing the amount of payroll taxes they would usually have withheld from employees’ wages. That was a nice touch by the IRS.

Retroactive claims for the ERTC

Although it appears the IRS tried to make this as easy as possible, you may still need a tax professional to sort it out. For instance, if your business had a substantial decline in gross receipts but has now recovered, you can still claim the credit for the difficult period

Retroactive claims for refunds will probably be delayed because currently everything is delayed at the IRS. The credit can be claimed on amended payroll tax returns as long as the statute of limitations remains open, which is three years from the date of filing. So you have some time to claim the credit, but why wait?

Keep December 2021 in mind

The economy is in a state of change, and it is fair to say that we are once again in uncharted territory. On the positive side, there seems to be significant resources and support for businesses from both government and consumers. You and your tax professional should keep your eyes open for credits and benefits to make sure you don’t miss any opportunitie

The ERTC expires in December 2021. Though it may be difficult to think about year-end in the middle of the summer, you’ll want to figure out your position on this credit before December. A tax professional can help you understand the ERTC and help you decide on your next step.

About the author

Michael Silvio is a partner at MGO. He has more than 25 years of experience in public accounting and tax and has served a variety of public and private businesses in the manufacturing, distribution, pharmaceutical, and biotechnology sectors.

]]>PPP basics

Generally, PPP loans are 100% forgivable given the borrower allocates the funds on a 60/40 basis between payroll and eligible nonpayroll costs. Nonpayroll costs originally solely included mortgage interest, rent, utilities, and interest on any other existing debt. However, the Consolidated Appropriations Act (CAA), which was enacted in late 2020, significantly expanded the eligible nonpayroll costs to include other costs the funds can be applied to, such as certain operating expenses and worker protection expenses.

The CAA also withdrew the original requirement that mandated borrowers deduct the amount of any Small Business Administration (SBA) Economic Injury Disaster Loan (EIDL) advance from the forgiveness amount they received from the PPP. A borrower doesn’t need to include any forgiven amounts in its gross income and can deduct otherwise deductible expenses paid for with forgiven PPP proceeds.

Forgiveness filings

Those who borrowed PPP loans can apply for forgiveness at any time before their loans’ maturity date, and loans made before June 5, 2020, generally have a two-year maturity while loans made on or after that date have a five-year maturity. However, if a borrower does not apply for forgiveness within 10 months after the last day of the “covered period” (the eight-to-24 weeks following disbursement during which the funds must be used), the PPP loan payments will no longer be deferred, and payments must begin to be made to the lender.

This 10-month period is ending for many “first-draw” borrowers. If a business applied early in the program, it might have a covered period that ended on October 30, 2020, meaning it would need to apply for forgiveness by August 30, 2021, to avoid loan repayment responsibilities.

To apply for forgiveness, borrowers file forms with their lenders, who will then submit the forms to the SBA. The type of form that must be filed is dependent on both the amount of the loan and whether a business is a sole proprietor, independent contractor, or self-employed individual with no employees.

The borrower will be notified by the lender if the SBA does not forgive a loan or only partially forgives it. Interest accrues during the time from disbursement of the loan proceeds to SBA remittance to the lender of the forgiven amount, and the borrower must pay any interest that has accrued on any amount not forgiven.

To maximize their employee retention tax credits, some businesses may have delayed filing their forgiveness applications. The reason for this stems from the fact that qualified wages paid after March 12, 2020, through December 31, 2021—that are considered for purposes of calculating the credit amount—cannot be included when calculating eligible payroll costs for PPP loan forgiveness. These businesses should pay careful attention to the date their 10-month period expires as to avoid triggering loan repayment.

Audit action

There is the possibility that borrowers will be audited by the SBA’s Office of Inspector General with support from the IRS and other federal agencies. The SBA automatically audits every loan in excess of $2 million after the borrower applies for forgiveness, but it’s possible that smaller loans could be subject to scrutiny too.

Despite the audit safe harbor for loans of $2 million or less established by the SBA, this carveout solely applies to the examination of the borrower’s good faith certification on the loan application that states “the current economic uncertainty makes the loan request necessary to support the ongoing operations” of the business. Those borrowers will also no longer need to complete a burdensome, time-consuming Loan Necessity Questionnaire, as the SBA recently notified lenders that this loan necessity requirement for loans more than $2 million has been eliminated.

However, all borrowers still have the potential to be audited on matters like eligibility (like the number of employees), calculation of the loan amount, how the funds were used, and entitlement to forgiveness. Borrowers that receive poor audit findings may be required to repay their loans and, depending on what kinds of missteps were recovered, could face civil penalties and persecution under the federal False Claims Act.

Those businesses that received loans of more than $2 million should not wait to prepare for their audits. By beginning to work with their CPAs now, they can gather and organize the documents and information auditors are likely to request, including:

• Financial statements,

• Income and employment tax returns,

• Payroll records for all pay periods within the applicable covered period,

• Calculation of full-time equivalent employees, and

• Bank and other records related to how the funds were used (for example, canceled checks, utility bills, leases, and mortgage statements).

It is important to note that some of this documentation will overlap with what is required when filing the application for loan forgiveness.

Act now

Businesses always have their plates full, so it isn’t surprising that many may not have been focused on the various dates that matter to their PPP loans. Now is the time to ensure that you file your forgiveness application promptly with the necessary documentation already gathered to survive any SBA audit that may follow. Contact us for assistance.

]]>In the following we will describe many of the key changes and what they mean for PPP loan borrowers.

Key points from the Paycheck Protection Flexibility Act (PPFA)

PPP loan use “covered period” extended to 24 weeks

The “covered period” during which PPP loans can be used has been extended from eight weeks to 24 weeks, from date of loan origination. Loan recipients may choose to maintain the eight week timeline. There is a hard cap of December 31, 2020.

What it means: The original eight-week period PPP loans were to be used in has proven insufficient as the economic fallout from the COVID-19 pandemic has continued for many businesses. The extended deadline is meant to help businesses maximize the forgiveness potential of the loans. The ability to adhere to the original eight-week deadline is also notable, as businesses that have recovered will be able to seek forgiveness when they are ready.

Payroll expenditure requirement lowered to 60%

Borrowers now need to use 60% of funds to support payroll to meet forgiveness requirements. The prior level was 75%. However, the 60% limit now becomes a cliff, meaning at least 60% of funds MUST be used on payroll or there is no loan forgiveness.

What it means: One of the biggest criticisms of the original PPP loan terms was the 75% usage requirement for maintaining payroll, as many businesses had other pressing needs (rent/lease payments, supplier payments, utilities, etc.) superseding or directly connected to the need to maintain payroll levels. Lowering the payroll threshold to 60% is useful, while also reemphasizing the purpose of the loans being for maintaining payroll through implementing the “cliff” dynamic.

Deadline for restoring full workforce extended to 24 weeks

Borrowers now have 24 weeks, or a hard deadline of December 31, 2020, to meet the forgiveness condition of restoring workforce levels to pre-pandemic levels. Previous deadline was June 30, 2020.

What it means: As the economic fallout from the COVID-19 pandemic continues, this is a very welcome change, as many borrowers are not yet near former operational levels. This makes returning workforce to pre-pandemic levels nearly impossible for many borrowers.

More exceptions for restoring workforce forgiveness condition

If a PPP borrower cannot restore prior workforce levels due to the inability to find qualified help, or have not restored prior business operations to pre-pandemic levels, their loans remain eligible for forgiveness.

What it means: Previous guidance allowed borrowers to exclude from payroll calculations employees who turned down ‘good faith’ offers to be rehired at pre-pandemic hours and wages. Creating two further exceptions makes sense as many businesses may not be able to return to previous workforce levels, possibly for years to come. Businesses seeking these exclusion will need to be able definitively document these conditions when seeking forgiveness terms through their lender.

PPP borrowers have five years to pay back loans

PPP loans can be extended to five years if borrower and lender agree. The previous timeline was two years. Loans extended to five years will maintain the 1% interest rate.

What it means: Additional flexibility in repayment terms is another welcome change as economic conditions remain difficult for many businesses.

PPP borrowers can delay payroll taxes

PPP loan recipients are now eligible for the payroll tax deferral created by the CARES Act. Previously, receiving PPP loans disqualified businesses from the payroll tax break.

What it means: In the CARES Act legislation that created the PPP program, there were tax credits and incentives designed to help struggling businesses. One essential option was the ability to defer the deposit and payment of the employer’s portion of social security taxes that otherwise would be due between March 27, 2020, and Dec. 31, 2020. Employers could instead to deposit half of deferred payments by the end of 2021 and the other half by the end of 2022.

Support for maximizing PPP loan forgiveness

The Payroll Protection Program Flexibility Act provides much needed flexibility to businesses that have taken loans out in the face of unprecedented economic disruption. These changes to terms represent a moving target for businesses seeking to use funds as directed, in many cases increasing complexity. But overall these changes are welcome and ultimately create expanded opportunities for maximizing PPP loan forgiveness.

If you have any questions about PPP loans, forgiveness terms, or related issues, our dedicated team is ready to provide guidance. Please do not hesitate to reach out to us with any questions: contact us.

]]>To assist our state and local government clients during these unprecedented times, MGO is offering support designed to help you understand and access funding options, manage regulatory complexity, and institute financial best practices.

Support accessing CARES Act funding

- Assistance with identification of eligible funding provisions within the CARES Act.

- Training of applicable personnel regarding CARES Act provisions and requirements.

- General Advisory Services related to CARES Act provisions and requirements.

- Assistance with preparation of initial appropriation requirements, if applicable.

- Process and procedure development for CARES Act funding provision requirements by source, including:

- Governance

- Document Retention

- Procurement

- Timelines & Scope

- Reporting and Other

- Assistance with preparation of ongoing reporting requirements by funding provision.

- Preparation of cash flow and revenue projections resulting from the impact of COVID-19.

- Identification of methods to address budget gaps resulting from the impact of COVID-19.

For more information, please contact your MGO advisor directly, or email our team at response@mgocpa.com

]]>Of the long list of relief efforts, one of the most significant changes for businesses small and large was not something new, but rather a correction to the Tax Cuts and Jobs Act (TCJA) of 2018 regarding qualified improvement property (QIP). Here’s why that minor fix could have a major impact by providing much-needed liquidity in the midst of a pandemic.

Understanding the “Retail Glitch”

As the TCJA came together, Congress added language that renewed 100% bonus depreciation for QIP that was acquired after September 23, 2018, and began being used by January 1, 2023. This is depreciation that included properties that had a life of up to 20 years. During the whirlwind drafting sessions that took place before the bill was finalized, drafters failed to include an amendment that included a 15-year recovery period for QIP, even though it was clear they had intended to do so. The omission, known as the “Retail Glitch,” meant that QIP was subject to a 39-year recovery period rather than the intended 15, and that businesses would not be able to write it off.

Fixing the glitch

The CARES Act addressed the error in the TCJA by including QIP as a 15-year MACRS asset and 20-year ADS asset, allowing businesses in hard-hit industries like hospitality, retail, and restaurants, to retroactively write-off any investments they have made into their spaces dating back to the enactment of the TCJA on December 22, 2017. The impact of this is significant, as fixing the error allows leaseholders and building owners to immediately retrieve the costs of improvement-related investments they have made in their property since December 2017, which are now classified as bonus depreciation under the CARES Act.

Why QIP changes are critical

This provision of the CARES Act is so important because it is an immediate injection of cash to thousands of businesses who are likely experiencing severe cash flow issues. The QIP classification includes any renovation to the interior of a non-domicile property that was made after the building began business use and applies mostly to industries that often revamp their facilities. Additionally, because the bill is retroactive, it is likely that many businesses will be able to access liquidity from several past projects, allowing them to potentially further ease financial burdens.

Getting the cash

As with any major piece of legislation, specifics on how to access the depreciation that the CARES Act entitles business owners to is scarce. However, industry professionals have found several methods to file for the money, the simplest of which is to work with your tax services provider to file amended returns for tax years 2018 and 2019. Other options exist as well, including filing superseding returns or filing a Form 3115, which is an application for change in accounting method. Because the QIP change will have widespread effects, it is anticipated that when the IRS issues formal guidance they will automatically allow the change to be made.

Small businesses and corporate America alike are struggling at this moment, and the future is uncertain. Taking advantage of the QIP amendment to the tax code is strategically imperative for any business that needs a boost in financial health in the short and long term.

For guidance applying the new QIP changes or filing amended tax returns, please reach out to schedule a consultation.

]]>The bill is the third phase of Congress’ COVID-19 response and provides substantial federal government support aimed to address the economic fallout associated with the COVID-19 pandemic in the United States.

For state and local governments the Act provides substantial appropriations to assist with the financial impacts of COVID-19. There are various funding provisions that state and local governments will be able to participate in, each of which has differing eligibility and reporting requirements.

MGO understands the complexities of this historic Act and in an effort to provide support and clarity to our state and local government clients we have summarized some of the significant funding sources by type, total monies allotted, general purpose, and eligible parties.

As state and local governments, you will be facing significant fiscal and personnel restraints not only due to new costs incurred directly related to the COVID-19 pandemic, but also due to decreased revenue resulting from the reduction in overall economic activity. As leaders in serving state and local governments for more than 30 years, we are here to help you navigate through this time.

For more information, please contact your MGO advisor directly, or email our team at response@mgocpa.com.

]]>