- A growing organization is a positive, but along with it usually comes increasingly complex financial accounting.

- Outsourcing provides businesses of all sizes with an opportunity to manage an array of issues — from staffing shortages or a lack of specific expertise to disorganized or unsecure financial records.

- Benefits of outsourcing include significant cost savings, direct access to specific accounting knowledge, the minimization of turnover, the ability to scale, access to tools and processes, and flexibility.

Many CEOs and business leaders are experiencing challenges in the aftermath of the COVID-19 pandemic, including changing customer trends, aggressive competition, emerging digital technologies, and the new normal of employee expectations for workplace flexibility.

These uncertain economic forces and cultural shifts are putting increased pressure on staffing for organizations of all sizes – especially fast-growing ones. While these difficulties are difficult to overcome, they are also an opportunity to change the “status quo” and level-up back-office performance.

For leaders navigating the uncertain tailwinds of the pandemic and planning to enter a new era of growth, outsourcing represents a powerful opportunity to address any staffing issues or business challenges. It empowers you to access specialized insight on a temporary basis, create value ahead of a major transaction, manage overhead costs, and modernize and revitalize business processes.

A recent study showed that 59% of all businesses utilize outsourced resources and that accounting is the most commonly outsourced function. So, how do you know if outsourcing your accounting function is right for your organization?

In this article we’ll look at five indicators that this strategy might be right for you and detail the key benefits to outsourcing or augmenting your accounting function.

Five signs your business may benefit from outsourced accounting

Here are some questions you should ask yourself to determine if your organization would benefit from outsourced accounting services:

- Is your business growing rapidly?

If you’re experiencing a significant influx of revenue, first off, great work! Your business model is proving out and you’re on the fast-track to success. But what is happening to your expenses, profitability and working capital? Depending on your answer it could mean that your accounting needs are evolving, the risks of a breakdown are higher, and overall, there is simply more at stake. It may be time to confirm that your current in-house team is qualified and staffed appropriately to handle these new responsibilities.

- Are you struggling to keep up with your accounts receivable or payroll?

One way to get a firm answer to whether your team is understaffed is if you’re missing key deadlines or struggling to get timely collection of cash from your accounts receivable. The inability to collect and follow-up on AR is essential to funding current and future growth and is directly connected to meeting your payroll commitments – one of the largest expenses of any business. If anything falls behind, you can find yourself in a difficult position if you do not have the ability to access cash or financing.

- Are your financial records organized and producing usable data?

Your accounting function does more than compliance, it should help guide your organization’s financial hygiene. Organized financials tell a clear story of earnings, spending, and investment, so you can make informed decisions. An over-worked or inexperienced accounting team will be working furiously to keep up with compliance and may not have the capacity, or necessary experience, to provide guidance on your financial scorecard to accrete value to the organization.

- Do your accounting needs fluctuate significantly throughout the year?

If your business experiences big shifts in labor productivity based on the calendar year and your taxes filings are late with significant overages from the tax preparers, or your audits have a significant number of adjustments, that may mean your accounting team lacks capability. Striking the right balance between hiring quality talent and the speed of bringing new hires up to date with company procedures can be a challenge. Outsourcing your team can deliver the resources you need, when you need them, and limit costs during the slower periods.

- Are you concerned about financial security and checks and balances?

If your internal accounting team is one or two individuals, you may be open to hidden risks. An independent team can provide the checks-and-balances that help mitigate the risk of fraud and asset misappropriation.

If you answered yes to any of these questions, you should consider outsourcing part or all of your accounting function. With an outsourced accounting team, you gain immediate access to trained, knowledgeable staff with the knowledge you need in technical accounting. The right outsourced resources can help your business grow faster and run more smoothly — often at a lower price than building an internal accounting department.

Benefits of outsourced accounting services

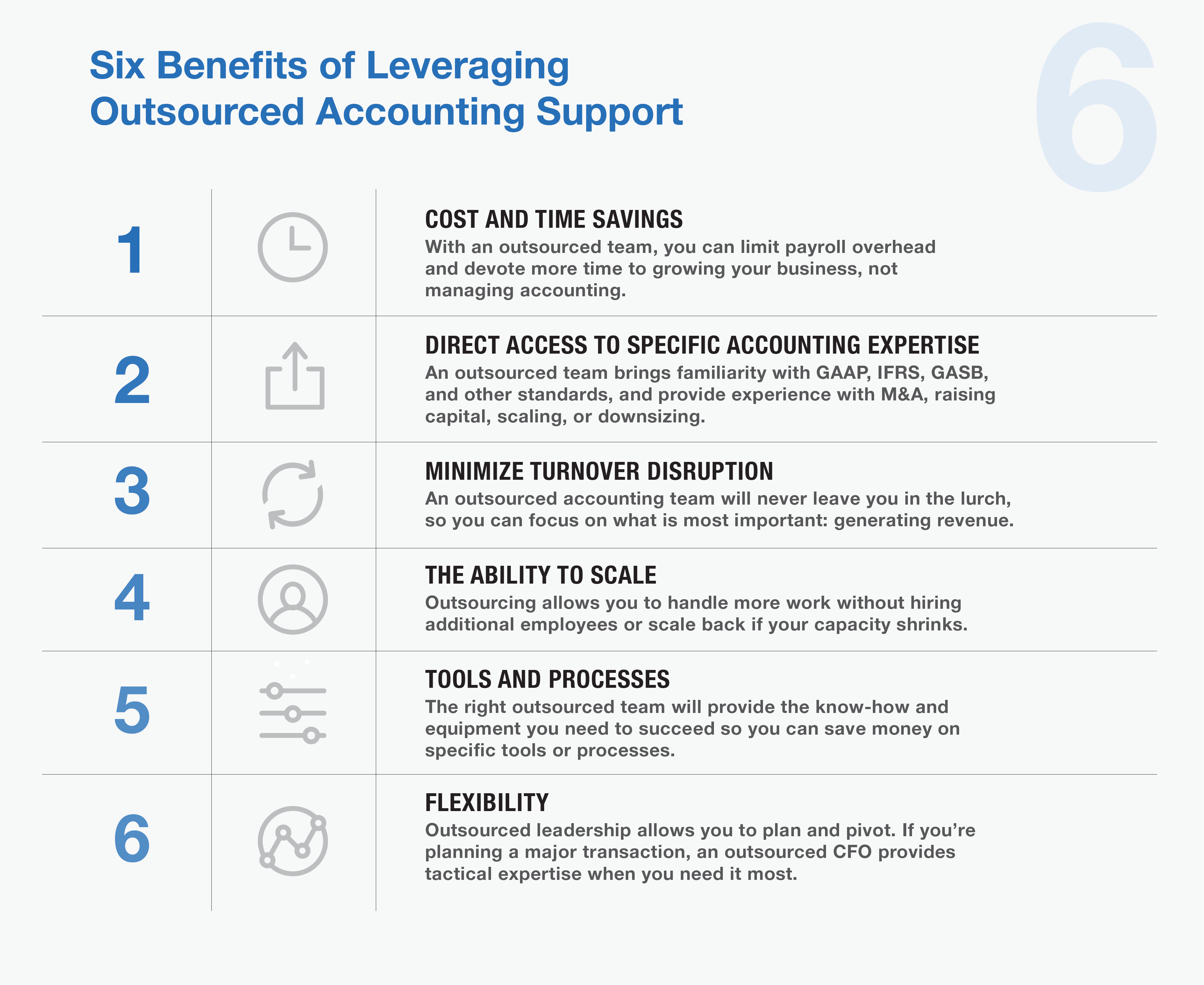

1.Cost and time savings

Maintaining full-time employees can be costly — and for most organizations, labor costs are some of the highest expenses. By relying on an outsourced team, you can devote your time to growing your business and spend less time managing accounting.

- Direct access to specific accounting expertise

Every company is different, which means every company’s needs are different. By outsourcing, you have access to the service you need when you need it. An outsourced team will bring familiarity with an array of accounting and reporting standards, including GAAP, IFRS, GASB, etc. Plus, they can provide specific experience with M&A transactions, raising capital, scaling, or downsizing operations.

- Minimize turnover disruption

In a smaller organization, each employee is vital to the business’s success. When you lose one, the disruption left in their wake can provide additional challenges. An outsourced accounting team will never leave you in the lurch, so you can focus on what is most important: generating revenue.

- The ability to scale

If your organization has grown quickly, you may experience growing pains when your fortunes suddenly shift. In boom times, you may need to hire more staff to meet demand. But that also means you may find yourself laying off employees in a downturn. Outsourcing allows you to handle more work without hiring additional employees or scale back if your capacity shrinks.

- Tools and processes

No matter what your organization’s size, you should always try to keep your overhead costs minimal. By outsourcing, you can save money on specific tools or processes you might otherwise need to function. The right outsourced team will provide the know-how and equipment you need to succeed.

- Flexibility

By outsourcing certain jobs, you can plan — and pivot, as needed — depending on your organization’s needs. This is especially relevant in the case of needing specialized guidance. If you’re planning a major transaction or other market move, an outsourced CFO can provide tactical expertise when and where you need it.

MGO can help

As your organization grows, your financial accounting needs become increasingly complex. Because your in-house accountants may be limited to handle the basics, outsourcing to professional teams with specialized knowledge and experience can provide precisely the kind of service you require — and give you the time you need to focus on the organization’s other needs.

MGO has a robust outsourced accounting team staffed by CPAs with diverse industry background and technical specialties. We’ll provide the right-size solution to your organization’s needs. Areas we support include day-to-day accounting tasks, complex financial systems projects, regulatory compliance demands, and support for M&A deals, raising capital, and other major transactions.

Whether you’re interested in simply augmenting your team with additional financial knowledge, or undertaking a complete accounting transformation, we can help you with the people, processes, and technology you need to move your business forward.

To explore your options and start along the path to organizational change, contact us.

]]>Under this Act, foreign companies traded on any U.S. exchanges are required to have their auditors submit to inspection by the Public Company Accounting Oversight Board (PCAOB) in an effort to establish that they’re neither owned nor controlled by a foreign government. With a wealth of Chinese companies trading in the U.S., the legislation is likely to have a significant impact on Chinese companies and their accounting firms, as well as U.S. investors and the capital market, for years to come.

How the HFCAA works

The Act will amend Section 104 the Sarbanes-Oxley Act of 2002, the comprehensive legislation passed by Congress aimed at overseeing the conduct of public companies. Pursuant to the HFCAA, there will be a number of sizable changes.

• First, the Securities and Exchange Commission (SEC) will now be required to identify companies that are utilizing registered public accounting firms located outside the United States that are preventing audits from the PCAOB.

• Additionally, the SEC must prohibit securities trading of these public companies within U.S. markets following three consecutive years of non-inspection. Under the language of the bill, these companies will be prohibited from trading on either a national securities exchange or “through any other method that is within the jurisdiction of the Commission to regulate, including through the method of trading that is commonly referred to as the ‘over-the-counter’ trading of securities.” It should be noted that in the event an issuer receives a trading prohibition, then the issuer is allowed to have the prohibition overturned as long as it is able to retain an accounting firm that can be fully inspected by the PCAOB.

• Also, as part of the Act, there are disclosure requirements for non-inspection years for foreign issuers of securities that utilize firms to prepare audit reports. For instance, they will need to disclose the percentage of shares owned by foreign government entities. They will also need to disclose whether or not foreign government entities have “controlling financial interest with respect to the issue.”

• Finally, there are also disclosure requirements that specifically involve China. According to the Act, the names of each official of the Chinese Communist Party of the board of directors of either the issuer or “the operating entity with respect to the issuer” must be disclosed in their Form 10-K, Form 20-F, and shell company reports. Additionally, it must be disclosed if the issuer’s articles of incorporation (or “equivalent organizing document”) has “any charter of the Chinese Communist Party, including the text of any such charter.”

Potential impact of the HFCAA

While the HFCAA applies to any U.S.-listed company incorporated outside the United States, including Mainland China, Hong Kong, France, and Belgium, it is generally understood as explicitly targeting Chinese companies under the restrictions imposed by the Chinese government.

This Act could lead to an increase in the number Chinese and Hong Kong-based issuers being delisted from U.S. exchanges in the coming years. In fact, according to the list of public companies affected by obstacles to PCAOB inspections, there are more than 200 Chinese companies currently audited by CPA firms in mainland China and Hong Kong that would be negatively impacted. These companies, including popular stocks such as Alibaba Group Holding Ltd – ADR, Baidu Inc, JD.com Inc, and Nio Inc – ADR, could feel the brunt of this new legislation.

Note that the Big Four accounting firms in China are independent from the Big Four in the U.S. and do not meet the audit requirements of the PCAOB since they are under the China’s national security laws and the Chinese Securities Law, which prohibit Chinese companies from providing records “relating to securities business activities” overseas without approval by the Chinese securities regulator. Besides, the imminent enactment would certainly discourage new listing of Chinese companies in the U.S. as it could result in a discount on the trading prices as investors may factor in the potential de-listing risk.

However, it remains to be seen how the SEC implementation will roll out within 90 days of the HFCAA’s enactment, which could be greatly influenced by the new leadership of the SEC. According to Bloomberg, President-elect Joe Biden is expected to pick Gary Gensler to head the SEC.

Additionally, because of the three-year compliance timeline in the Act, Chinese companies may consider several options to mitigate the impending risks. The most likely one is to engage a reputable U.S.-based CPA firm, preferably one that has an established China Group, who understands both the Chinese business climate and the U.S. accounting rules, and most importantly obtain a clean compliance record with PCAOB. Yet, it’s also critical that companies consider other factors such as the investor and make sustainable long-term plan to maintain a legitimate and confident position in US capital markets.

If you have any questions

MGO’s SEC practice has a dedicated China Group experienced with Chinese IPOs, RTOs, M&A deals and the unique characteristics of SPAC acquisitions. To understand your options, and the path ahead, please feel free to reach out to us for a consultation.

Private organizations, while not always smaller, often have limited resources in specialty areas, including accounting for income tax. This resource constraint —the work being done outside the core accounting team — combined with the complexity of the issues, means private companies are ideal candidates for, and can achieve significant benefit from, internal controls enhancements. Thinking beyond the present, the following are five reasons private companies may want to adopt public-company-level controls:

1. Future Initial Public Offering (IPO) – Walk before you run! If the company believes an IPO may be in its future, it’s better to “practice” before the company is required to be SOX compliant. A phased approach to implementation can drive important changes in company culture as it prepares to become a public organization. Recently published reports analyzing IPO activity reveal that material weaknesses reported by public companies were disproportionately attributable to recent IPO companies. Making a rapid change to SOX compliance can place a heavy burden on a newly public company.

2. Merger and Acquisition Deals – If the possibility of the company being sold to an M&A deal exists, enhanced financial reporting controls can provide the potential buyer with an added layer of security or comfort regarding the financial position of the company. Further, if the acquiring firm has an exit strategy that involves an IPO, the requirement for strong internal controls may be on the horizon.

3. Rapid Growth – Private companies that are growing rapidly, either organically or through acquisition, are susceptible to errors and fraud. The sophistication of these organizations often outpaces the skills and capacity of their support functions, including accounting, finance, and tax. Standard processes with preventive and detective controls can mitigate the risk that comes with rapid growth.

4. Assurance for Private Investors and Banks – Many users other than public shareholders may rely on financial information. The added security and accountability of having controls in place is a benefit to these users, as the enhanced credibility may impact the cost of borrowing for the organization.

5. Peer-Focused Industries – While not all industries are peer-focused, some place significant weight on the leading practices of their peers. Further, some industries require enhanced levels of security and control. For example, cannabis companies with a heavy regulatory burden, industries with sensitive customer data like lifesciences, and tech companies that handle customer data, often look to their peer group for leading practices, including their control environment. When the peer group is a mix of public and private companies, the private company can benefit from keeping pace with the leading practices of their public peers.

Private companies are not immune from the intense scrutiny of numerous stakeholders over accountability and risk. Companies with a clear understanding of the inherent risks that come from negligible accounting practices demonstrate their ability to think beyond the present, and to be better prepared for future growth or change in ownership.

]]>Last year’s Tax Cuts and Jobs Act, H.R. 1 (“the Act”) created a federal capital gains tax deferral program through the opportunity zone statute, which is designed to attract private, long-term investments in low-income and economically distressed communities. Over 8,700 communities designated as Qualified Opportunity Zones (QOZ), located across all 50 states, territories and Washington D.C, were nominated by local governments and confirmed by the Department of Treasury (DoT) in Notice 2018-48 issued in June 2018.

The statutory language of the Act introduced the tax incentive deferring taxable gains but it did not provide important details, including the types of gains eligible for deferral, the timing and specific requirements of qualified investments, and how investors report deferred gains. On October 19, 2018, the Treasury Department released proposed regulations, a revenue ruling, and tax forms to provide additional guidance on the opportunity zone tax incentive.

How QOZ tax incentives work

Simply stated, the opportunity zone statute allows for the deferral of capital gains if some or all of the amount of the capital gain recognized is invested in a Qualified Opportunity Fund (QOF) by an eligible taxpayer. A QOF is any entity that invests in qualified opportunity zone property and is taxed as a partnership or corporation organized in any of the 50 states, US territories, or D.C. The QOF is required to hold at least 90 percent of its assets in qualified opportunity zone property.

To defer a capital gain, a taxpayer has 180 days from the date of sale or exchange of the appreciated property to invest the recognized gain in a QOF. The potential tax benefits of opportunity zone statute include:

- Deferral of tax on capital gains invested in a QOF through 2019: Any recognized capital gain invested in a QOF through December 31, 2019 may be deferred until December 31, 2026 or eliminated when an investment in a QOF is disposed. There is an opportunity for taxpayers to make multiple investments in QOFs through the statute expiration date.

- Potential to eliminate 15% to 100% of taxes for capital gains invested: Capital gains invested in a QOF are deemed to have an initial tax basis of zero. The taxpayer receives a 10% increase in tax basis if the investment is held five years and an additional 5% increase in tax basis after seven years. If an investment in a QOF is held for ten years, the taxpayer can elect to increase their tax basis in the QOF to fair market value upon disposition, which provides for a tax-free investment in the QOF. Tax is realized on the excess of the deferred gain over the basis in the QOF at the time of disposal.

- Ability to rollover gains on disposal of investments in QOF: In general, the original deferred gain must be recognized by the taxpayer upon disposition of the investment in the QOF. If a taxpayer disposes of all of an investment in a QOF, triggering tax on the deferred gain and the qualified opportunity zone property, a taxpayer can make an investment in a new QOF and rollover the deferred gain. The rollover investment must be made before December 31, 2026.

Qualified Opportunity Zone Property

The purpose of the opportunity zone statute is to incentivize investment in low-income areas of the country in need of community development and improvement. IRC Sec. 1400Z-2(d)(2) provides guidance regarding the types of assets that will be considered qualified opportunity zone property if held by a QOF. In general, qualified opportunity zone property includes the following:

- Newly issued stock held in a domestic corporation if such corporation is a qualified opportunity zone business,

- Newly issued partnership interests in a domestic partnership if such partnership is a qualified opportunity zone business, or

- Qualified opportunity zone business property.

Qualified opportunity zone business property is further defined in IRC Sec. 1400Z-2(d)(2)(D) as tangible property used in a business in a qualified opportunity zone that is either:

- Land in a qualified opportunity zone,

- A building in a qualified opportunity zone that is first used by the QOF or the qualified opportunity business,

- A building in a qualified opportunity zone that was previously used but is “substantially improved” by the QOF or qualified opportunity business,

- Equipment that was never previously used in a qualified opportunity zone, or

- Equipment that was previously used in a qualified opportunity zone but it “substantially improved” by the QOF or the qualified opportunity business.

The opportunity zone statute defines “substantial improvement,” as an amount of investment in existing tangible property by a QOF, during any 30-month period, that exceeds the adjusted basis in the property at the beginning of the 30-month period. The Revenue Ruling issued clarifies that improvements made to land are not included in the total improvements for purposes of the “substantial improvement test” and the value of land is excluded from the adjusted basis calculations.

More details on qualifying as a QOF

The new guidance also provides details on what qualifies an investment vehicle as a QOF. And a draft of Form 8996, Qualified Opportunity Fund was released alongside the guidance to demonstrate how corporations and partnerships can self-identify as a QOF by including the form with the filing of their tax return. Additional information provided includes guidelines for determining when a QOF begins, how a QOF can meet the requirements to be recognized as a qualified opportunity zone business, and what pre-existing entities may qualify as a QOF. And finally, guidance details the test required of QOFs to determine whether the entity holds the minimum threshold of assets in qualified opportunity zone property.

Considering a QOZ investment?

While the new guidance helps fill in many details, many questions are left unanswered and the Department of Treasury plans to release further guidance before the end of the year. If you’re planning on creating or investing in a QOF, we recommend consulting with an experienced tax advisor first.

The tax team at MGO is ready to assist you in navigating QOZs, QOFs, and other income tax concerns. For further guidance or to schedule a consultation, please contact us.

]]>