What is the policy now? Well, the Tax Cuts and Jobs Act (TCJA) of 2017 changed the treatment of R&E costs so that taxpayers must capitalize all R&E costs incurred after December 31, 2021, and amortize them over either a five-year period (domestic costs) or a 15-year period (foreign costs). Previously, taxpayers could either (1) immediately deduct R&E expenditures, or (2) elect to amortize those costs over a period of five or more years, which gave the taxpayer the ability to choose the option that would be the most beneficial for them.

While it is still possible for the legislative process to postpone or repeal mandatory capitalization of Section 174 costs (including retroactively applying any changes to the 2022 tax year), such legislation would need to have bipartisan support due to the currently divided Congress.

In this article, we review what it would mean for your business if the much-anticipated revisions to Section 174 do not occur, and what kind of planning you should do to prepare on the front end. A number of these recommendations will be further refined once additional IRS guidance is provided.

Background on 174 R&E expenditures

R&E expenses for income tax purposes are defined under Section 174 and its regulations. In Treasury Regulation Section 1.174-2(a), R&E expenditures are described as expenditures incurred by the taxpayer in connection with the taxpayer’s trade or business in the experimental or laboratory sense. Section 174(c)(3) – added by the TCJA – also notes that any amount paid or incurred in connection with the development of any software shall also be an R&E expenditure subject to capitalization. Generally, when determining R&E expenses, not only are direct costs of R&E factored in, but also the indirect costs incident to the development or improvement of a product.

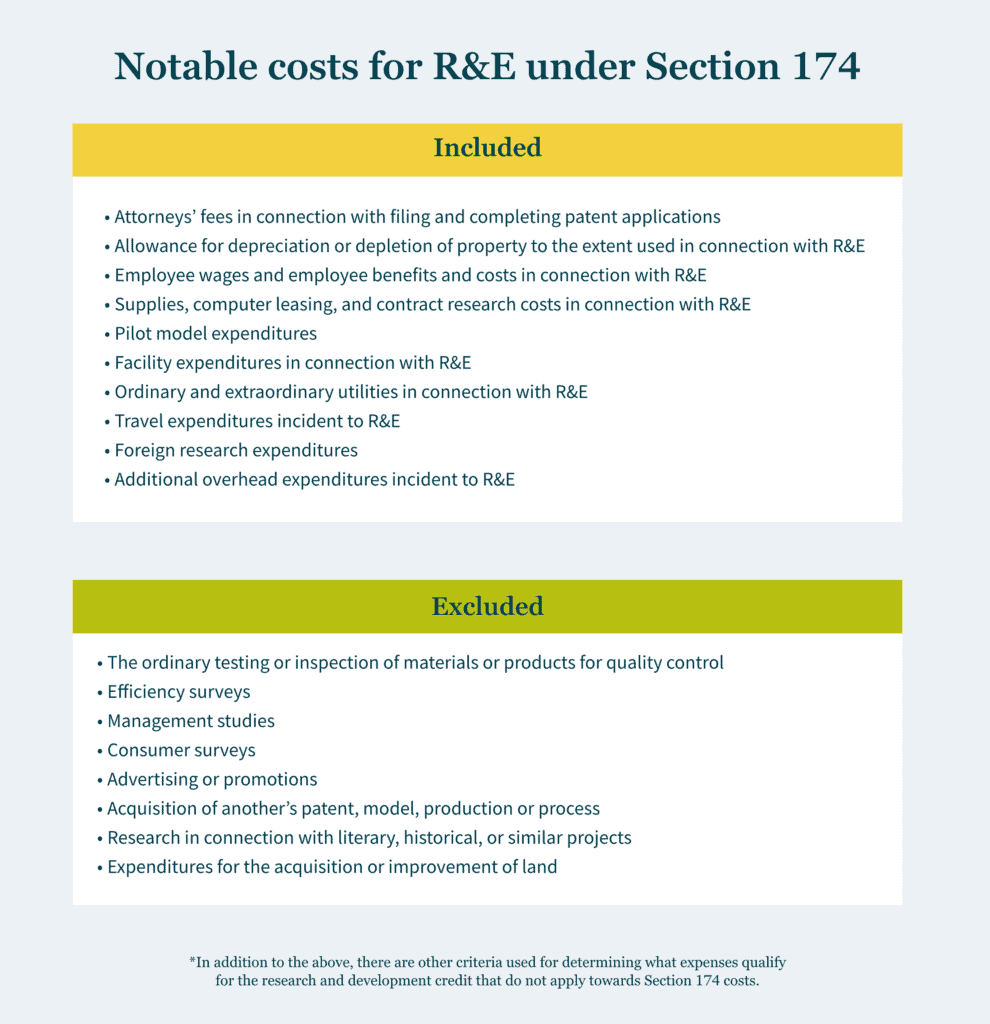

Common expenses included in R&E costs under Section 174 are the following. Many of these expenses are considered for Section 174 specifically and are not qualified research expenses for purposes of the R&D credit.

- Attorneys’ fees in connection with filing and completing patent applications.

- Allowance for depreciation or depletion of property to the extent used in connection with R&E.

- Employee wages and employee benefits and costs in connection with R&E.

- Supplies, computer leasing, and contract research costs in connection with R&E.

- Pilot model expenditures.

- Facility expenditures in connection with R&E.

- Ordinary and extraordinary utilities in connection with R&E.

- Travel expenditures incident to R&E.

- Foreign research expenditures.

- Additional overhead expenditures incident to R&E.

*In addition to the above, there are other criteria used for determining what expenses qualify for the R&D credit that do not apply towards determining Section 174 costs.

In contrast, the following are common expenses that are excluded from the expansive definition of R&E costs under Section 174:

- the ordinary testing or inspection of materials or products for quality control;

- efficiency surveys;

- management studies;

- consumer surveys;

- advertising or promotions;

- acquisition of another’s patent, model, production or process;

- research in connection with literary, historical, or similar projects; and

- expenditures for the acquisition or improvement of land.

The current R&E amortization rule explained

The ability to deduct R&E costs changed for all tax years beginning after December 31, 2021. As previously mentioned, these costs can no longer be deducted in full and must be capitalized and then amortized over five years for domestic costs and over 15 years for foreign costs. This amortization starts at the midpoint of the first year that the expenses were incurred, which results in only 10% of domestic costs (1/2 of 20%) being able to be deducted in their first year.

Per IRS guidance, this mandatory change can be implemented as an automatic accounting method change through attaching a statement to a taxpayer’s first income tax return with a year beginning after 2021, in lieu of filing the much more intricate Form 3115. This change should not have an effect on prior tax years, since the automatic method change is implemented on a “cut-off basis.”

Macro effect of mandatory capitalization

As mentioned above, before the prior rule was changed, every R&E expense could be deducted in full in the year they were incurred. While it is expected that the Section 174 expensing rules will revert to this — to some extent — through pressure from persistent lobbyists, this change has not been incorporated into a bill yet.

Some believe the mandatory R&E capitalization and amortization will adversely affect U.S. innovation, potentially resulting in a detrimental impact on our global competitiveness and jobs. For more than 60 years, businesses were able to immediately deduct their R&D expenses in the year those expenses were incurred (or choose to defer based on what worked for them). Now, the amortization of new R&E costs could cost businesses billions in cash taxes.

Significant considerations

Estimated Tax Payments: For taxpayers making estimated tax payments utilizing current year taxable income, consideration should be given to R&E expenditures and how the capitalization of those expenditures may impact taxable income and timing of cash tax payments. A closer look at refining the various accounts in a taxpayer’s books may be needed for this.

Tax Accounting / ASC 740: Taxpayers should be mindful of whether a new deferred tax asset is created, if any adjustment of existing deferred taxes may be necessary, or if a full or partial valuation allowance may be needed.

Other Areas Affected: The amortization requirement also affects other areas of taxable income, including the following:

- increases the deductibility of business interest under Section 163(j),

- increases the deductibility of the QBI (Qualified Business Income) deduction,

- increases the amount of GILTI (global intangible low-taxed income) for controlled foreign corporations,

- potentially adjusts the amount of FDII (foreign derived intangible income) deduction that can be taken,

- changes the amount of R&E expenses allocable for purposes of the foreign tax credit, and

- impacts state taxable income for the few states that do not conform to the capitalization requirement (e.g., California).

R&D credit considerations

The Section 174 capitalization requirements should not directly impact the amount of expenses that can be used for the R&D Tax Credit under Section 41, since the research credit is calculated using a much smaller subset of R&E expenditures than Section 174 and is not limited by the capitalization requirement. As Section 174 is much broader in scope, it applies to expenditures both eligible and ineligible for the research credit.

Another consideration for tax planning is that the research credit will be even more important to assist with reducing the additional tax liability that will be generated by the R&E treatment change, since the credit can help offset some of the tax liability increase. Moreover, the analysis & processes used to determine the R&D credit can be leveraged to identify Section 174 R&E expenses, which helps create some efficiencies in quantifying the overall effect of the mandatory capitalization and amortization requirement.

Extend impacted returns where possible

Tax return extensions are highly recommended for tax returns that have their due dates coming up. Not only is there the pending IRS guidance that may significantly change R&E expense calculations, but also the act of extending tax returns should allow more time for tax returns to be superseded (rather than amended) and should allow for R&D credit claims to be made on originally filed returns.

This is echoed by a September 2021 Chief Counsel Memorandum issued by the IRS, which made the process for claiming a refund under the R&D credit far more stringent. The memorandum relayed that taxpayers must provide more information on business components, identify the research activities performed, and name the individuals who performed each research activity. Given the additional amount of detail needed, taxpayers making R&D credit claims on amended returns — especially small businesses — have a heavier burden than those who make the claim on an originally filed returns.

How will it affect you?

If the mandatory R&E capitalization requirement is not changed, you should consider how the 174 capitalization rules will affect your business and how claiming the R&D credit will help offset the increase in tax liability. If you currently have an R&D credit analysis and/or an ASC 730 financial statement analysis, those studies can be used as starting points to determine the overall effect of Section 174 — keeping in mind that neither analysis includes all the costs included in Section 174.

If the requirement is changed, there are several ways that the R&E expense landscape could turn out for taxpayers. Ideally, Congress will revert to the prior rule regarding R&D expenses. In that situation, you should be able to choose what is best for you — immediately deducting or deferring.

Our perspective

As experienced advisors, MGO can help model the best R&E position for you, through the 2022 tax year and beyond — potentially saving you significant amounts of money. Our holistic tax advisor and business advisor-first philosophy factors not only the direct effects of the R&E capitalization requirement, but also the impact on other areas of your tax returns (e.g., international, transfer pricing, state, and local tax) and what potential savings you can obtain by claiming the R&D credit. Please feel free to reach out to any of our R&E costing profesionals below to get the experienced insight that you deserve.

About the author

Danielle Bradley is a senior manager in MGO’s National Tax Credits and Incentives practice. She focuses on helping businesses identify, substantiate, and defend federal and state tax credits and incentives. She has helped hundreds of companies monetize and defend over $100 million in various tax credits and incentives, such as the Research and Development (R&D) Tax Credit, Orphan Drug Credit, Employee Retention Credit, meals and entertainment deduction, and the current Research and Experimental (R&E) amortization calculations. Danielle has extensive experience in various industries, including software and technology, life sciences, manufacturing, aerospace and defense, and food, beverage and agriculture businesses.

Contact Danielle to further discuss the R&E amortization or other credits and incentives at Danielle Bradley (Tax Credits and Incentives Director), Matthew Sapowith (Tax Partner), or Michael Silvio (Tax Partner).

]]>What is the policy now? Well, the Tax Cuts and Jobs Act (TCJA) of 2017 changed the treatment of R&E costs so that taxpayers must capitalize all R&E costs incurred after December 31, 2021, and amortize them over either a five-year period (domestic costs) or a 15-year period (foreign costs). Previously, taxpayers could either (1) immediately deduct R&E expenditures, or (2) elect to amortize those costs over a period of five or more years, which gave the taxpayer the ability to choose the option that would be the most beneficial for them.

While it is still possible for the legislative process to postpone or repeal mandatory capitalization of Section 174 costs (including retroactively applying any changes to the 2022 tax year), such legislation would need to have bipartisan support due to the currently divided Congress.

In this article, we review what it would mean for your business if the much-anticipated revisions to Section 174 do not occur, and what kind of planning you should do to prepare on the front end. A number of these recommendations will be further refined once additional IRS guidance is provided.

Background on 174 R&E expenditures

R&E expenses for income tax purposes are defined under Section 174 and its regulations. In Treasury Regulation Section 1.174-2(a), R&E expenditures are described as expenditures incurred by the taxpayer in connection with the taxpayer’s trade or business in the experimental or laboratory sense. Section 174(c)(3) – added by the TCJA – also notes that any amount paid or incurred in connection with the development of any software shall also be an R&E expenditure subject to capitalization. Generally, when determining R&E expenses, not only are direct costs of R&E factored in, but also the indirect costs incident to the development or improvement of a product.

Common expenses included in R&E costs under Section 174 are the following. Many of these expenses are considered for Section 174 specifically and are not qualified research expenses for purposes of the R&D credit.

- Attorneys’ fees in connection with filing and completing patent applications.

- Allowance for depreciation or depletion of property to the extent used in connection with R&E.

- Employee wages and employee benefits and costs in connection with R&E.

- Supplies, computer leasing, and contract research costs in connection with R&E.

- Pilot model expenditures.

- Facility expenditures in connection with R&E.

- Ordinary and extraordinary utilities in connection with R&E.

- Travel expenditures incident to R&E.

- Foreign research expenditures.

- Additional overhead expenditures incident to R&E.

*In addition to the above, there are other criteria used for determining what expenses qualify for the R&D credit that do not apply towards determining Section 174 costs.

In contrast, the following are common expenses that are excluded from the expansive definition of R&E costs under Section 174:

- the ordinary testing or inspection of materials or products for quality control;

- efficiency surveys;

- management studies;

- consumer surveys;

- advertising or promotions;

- acquisition of another’s patent, model, production or process;

- research in connection with literary, historical, or similar projects; and

- expenditures for the acquisition or improvement of land.

The current R&E amortization rule explained

The ability to deduct R&E costs changed for all tax years beginning after December 31, 2021. As previously mentioned, these costs can no longer be deducted in full and must be capitalized and then amortized over five years for domestic costs and over 15 years for foreign costs. This amortization starts at the midpoint of the first year that the expenses were incurred, which results in only 10% of domestic costs (1/2 of 20%) being able to be deducted in their first year.

Per IRS guidance, this mandatory change can be implemented as an automatic accounting method change through attaching a statement to a taxpayer’s first income tax return with a year beginning after 2021, in lieu of filing the much more intricate Form 3115. This change should not have an effect on prior tax years, since the automatic method change is implemented on a “cut-off basis.”

Macro effect of mandatory capitalization

As mentioned above, before the prior rule was changed, every R&E expense could be deducted in full in the year they were incurred. While it is expected that the Section 174 expensing rules will revert to this — to some extent — through pressure from persistent lobbyists, this change has not been incorporated into a bill yet.

Some believe the mandatory R&E capitalization and amortization will adversely affect U.S. innovation, potentially resulting in a detrimental impact on our global competitiveness and jobs. For more than 60 years, businesses were able to immediately deduct their R&D expenses in the year those expenses were incurred (or choose to defer based on what worked for them). Now, the amortization of new R&E costs could cost businesses billions in cash taxes.

Significant considerations

Estimated Tax Payments: For taxpayers making estimated tax payments utilizing current year taxable income, consideration should be given to R&E expenditures and how the capitalization of those expenditures may impact taxable income and timing of cash tax payments. A closer look at refining the various accounts in a taxpayer’s books may be needed for this.

Tax Accounting / ASC 740: Taxpayers should be mindful of whether a new deferred tax asset is created, if any adjustment of existing deferred taxes may be necessary, or if a full or partial valuation allowance may be needed.

Other Areas Affected: The amortization requirement also affects other areas of taxable income, including the following:

- increases the deductibility of business interest under Section 163(j),

- increases the deductibility of the QBI (Qualified Business Income) deduction,

- increases the amount of GILTI (global intangible low-taxed income) for controlled foreign corporations,

- potentially adjusts the amount of FDII (foreign derived intangible income) deduction that can be taken,

- changes the amount of R&E expenses allocable for purposes of the foreign tax credit, and

- impacts state taxable income for the few states that do not conform to the capitalization requirement (e.g., California).

R&D credit considerations

The Section 174 capitalization requirements should not directly impact the amount of expenses that can be used for the R&D Tax Credit under Section 41, since the research credit is calculated using a much smaller subset of R&E expenditures than Section 174 and is not limited by the capitalization requirement. As Section 174 is much broader in scope, it applies to expenditures both eligible and ineligible for the research credit.

Another consideration for tax planning is that the research credit will be even more important to assist with reducing the additional tax liability that will be generated by the R&E treatment change, since the credit can help offset some of the tax liability increase. Moreover, the analysis & processes used to determine the R&D credit can be leveraged to identify Section 174 R&E expenses, which helps create some efficiencies in quantifying the overall effect of the mandatory capitalization and amortization requirement.

Extend impacted returns where possible

Tax return extensions are highly recommended for tax returns that have their due dates coming up. Not only is there the pending IRS guidance that may significantly change R&E expense calculations, but also the act of extending tax returns should allow more time for tax returns to be superseded (rather than amended) and should allow for R&D credit claims to be made on originally filed returns.

This is echoed by a September 2021 Chief Counsel Memorandum issued by the IRS, which made the process for claiming a refund under the R&D credit far more stringent. The memorandum relayed that taxpayers must provide more information on business components, identify the research activities performed, and name the individuals who performed each research activity. Given the additional amount of detail needed, taxpayers making R&D credit claims on amended returns — especially small businesses — have a heavier burden than those who make the claim on an originally filed returns.

How will it affect you?

If the mandatory R&E capitalization requirement is not changed, you should consider how the 174 capitalization rules will affect your business and how claiming the R&D credit will help offset the increase in tax liability. If you currently have an R&D credit analysis and/or an ASC 730 financial statement analysis, those studies can be used as starting points to determine the overall effect of Section 174 — keeping in mind that neither analysis includes all the costs included in Section 174.

If the requirement is changed, there are several ways that the R&E expense landscape could turn out for taxpayers. Ideally, Congress will revert to the prior rule regarding R&D expenses. In that situation, you should be able to choose what is best for you — immediately deducting or deferring.

Our perspective

As experienced advisors, MGO can help model the best R&E position for you, through the 2022 tax year and beyond — potentially saving you significant amounts of money. Our holistic tax advisor and business advisor-first philosophy factors not only the direct effects of the R&E capitalization requirement, but also the impact on other areas of your tax returns (e.g., international, transfer pricing, state, and local tax) and what potential savings you can obtain by claiming the R&D credit. Please feel free to reach out to any of our R&E costing profesionals below to get the experienced insight that you deserve.

About the author

Danielle Bradley is a senior manager in MGO’s National Tax Credits and Incentives practice. She focuses on helping businesses identify, substantiate, and defend federal and state tax credits and incentives. She has helped hundreds of companies monetize and defend over $100 million in various tax credits and incentives, such as the Research and Development (R&D) Tax Credit, Orphan Drug Credit, Employee Retention Credit, meals and entertainment deduction, and the current Research and Experimental (R&E) amortization calculations. Danielle has extensive experience in various industries, including software and technology, life sciences, manufacturing, aerospace and defense, and food, beverage and agriculture businesses.

Contact Danielle to further discuss the R&E amortization or other credits and incentives at Danielle Bradley, Matthew Sapowith (Tax Partner), or Michael Silvio (Tax Partner).

]]>While it appears that several of the more disadvantageous provisions targeting businesses won’t make it into the final bill, others may. In addition, some temporary provisions are coming to an end, requiring businesses to take action before year end to capitalize on them. As Congress continues to negotiate the final bill, here are some areas where you could act now to reduce your business’s 2021 tax bill.

Research and experimentation

Section 174 research and experimental (R&E) expenditures generally refer to research and development costs in the experimental or laboratory sense. They include costs related to activities intended to uncover information that would eliminate uncertainty about the development or improvement of a product.

Currently, businesses can deduct R&E expenditures in the year they’re incurred or paid. Alternatively, they can capitalize and amortize the costs over at least five years. Software development costs also can be immediately expensed, amortized over five years from the date of completion or amortized over three years from the date the software is placed in service.

However, under the Tax Cuts and Jobs Act (TCJA), that tax treatment is scheduled to expire after 2021. Beginning next year, you can’t deduct R&E costs in the year incurred. Instead, you must amortize such expenses incurred in the United States over five years and expenses incurred outside the country over 15 years. In addition, the TCJA requires that software development costs be treated as Sec. 174 expenses.

The BBBA may include a provision that delays the capitalization and amortization requirements to 2026, but it’s far from a sure thing. You might consider accelerating research expenses into 2021 to maximize your deductions and reduce the amount you may need to begin to capitalize starting next year.

Income and expense timing

Accelerating expenses into the current tax year and deferring income until the next year is a tried-and-true tax reduction strategy for businesses that use cash-basis accounting. These businesses might, for example, delay billing until later in December than they usually do, stock up on supplies and expedite bonus payments.

But the strategy is advised only for businesses that expect to be in the same or a lower tax bracket the following year — and you may expect greater profits in 2022, as the pandemic hopefully winds down. If that’s the case, your deductions could be worth more next year, so you’d want to delay expenses, while accelerating your collection of income. Moreover, under some proposed provisions in the BBBA, certain businesses may find themselves facing higher tax rates in 2022.

For example, the BBBA may expand the net investment income tax (NIIT) to include active business income from pass-through businesses. The owners of pass-through businesses — who report their business income on their individual income tax returns — also could be subject to a new 5% “surtax” on modified adjusted gross income (MAGI) that exceeds $10 million, with an additional 3% on income of more than $25 million.

Capital assets

The traditional approach of making capital purchases before year-end remains effective for reducing taxes in 2021, bearing in mind the timing issues discussed above. Businesses can deduct 100% of the cost of new and used (subject to certain conditions) qualified property in the year the property is placed in service.

You can take advantage of this bonus depreciation by purchasing computer systems, software, vehicles, machinery, equipment and office furniture, among other items. Bonus depreciation also is available for qualified improvement property (generally, interior improvements to nonresidential real property) placed in service this year. Special rules apply to property with a longer production period.

Of course, if you face higher tax rates going forward, depreciation deductions would be worth more in the future. The good news is that you can purchase qualifying property before year-end but wait until your tax filing deadline, including extensions, to determine the optimal approach.

You can also cut your taxes in 2021 with Sec. 179 expensing (deducting the entire cost). It’s available for several types of improvements to nonresidential real property, including roofs, HVAC, fire protection systems, alarm systems and security systems.

The maximum deduction for 2021 is $1.05 million (the maximum deduction also is limited to the amount of income from business activity). The deduction begins phasing out on a dollar-for-dollar basis when qualifying property placed in service this year exceeds $2.62 million. Again, you needn’t decide whether to take the immediate deduction until filing time.

Business meals

Not every tax-cutting tactic has to be dry and dull. One temporary tax provision gives you an incentive to enjoy a little fun.

For 2021 and 2022, businesses can generally deduct 100% (compared with the normal 50%) of qualifying business meals. In addition to meals incurred at and provided by restaurants, qualifying expenses include those for company events, such as holiday parties. As many employees and customers return to the workplace for the first time after extended pandemic-related absences, a company celebration could reap you both a tax break and a valuable chance to reconnect and re-engage.

Stay tuned

The TCJA was signed into law with little more than a week left in 2017. It’s possible the BBBA similarly could come down to the wire, so be prepared to take quick action in the waning days of 2021. Turn to us for the latest information.

]]>Here’s a summary of many of the proposals that could change the tax landscape soon.

Proposed tax provisions for businesses

The BBBA and BIB would also bring dramatic changes to the tax landscape for some businesses. Their tax bills could be influenced by proposals related to the following:

The corporate tax rate. The BBBA would replace the TCJA’s flat rate of 21% with a graduated rate structure. The first $400,000 of income would be subject to an 18% rate, with the 21% rate retained for income between $400,000 and $5 million. The graduated corporate rate would max out at 26.5% for income exceeding $5 million.

Personal service corporations and corporations with taxable income exceeding $10 million would be subject to a flat 26.5% rate. The pre-TCJA top corporate tax rate was 35%.

Excess business losses. The TCJA limits the amount of excess business losses that pass-through entities and sole proprietors can use to offset ordinary income to $250,000, or $500,000 for married taxpayers filing jointly, adjusted for inflation. The limit is set to expire at the end of 2025, but the BBBA would make it permanent.

The bill also would create a new carry forward for unused excess business losses, rather than carrying them forward as net operating losses.

The business interest deduction. Internal Revenue Code Section 163(j) limits the deduction for business interest incurred by both corporate and noncorporate taxpayers. Under the proposal, the limit wouldn’t apply to partnerships and S corporations at the entity level. It instead would apply to the partners and shareholders.

Research and experimentation expenses. Under the TCJA, research and experimentation expenditures incurred in 2022 and later years aren’t immediately deductible; rather, they generally must be amortized over five years. The BBBA would delay the effective date for the amortization requirement to 2026.

The employee retention credit. The BIB would terminate this credit earlier than originally planned. Instead of being available for all of 2021, it would no longer be available for the fourth quarter, except for recovery startup businesses.

Carried interest. Currently, carried interests are taxed as short-term capital gains unless the gains were on property held for at least three years. The BBBA would extend the holding period to qualify for long-term capital gain treatment to five years — except for real estate businesses and taxpayers with less than $400,000 of AGI. The carried interest rules also would be expanded to cover all property treated as generating capital gains.

International transactions. The BBBA includes numerous proposals that would change the taxation of cross-border transactions and trim some of the tax advantages enjoyed by multinational corporations. For example, it would reduce the deductions for global intangible low-taxed income (GILTI) and foreign-derived intangible income. It would determine GILTI and foreign tax credit limits on a country-by-country basis. It also would make changes to the base erosion and anti-abuse tax.

Interest Expense Deduction Limits. Proposed provisions would limit interest deduction if a U.S. parent and foreign subsidiaries are in the same International Financial Reporting Group for financial reporting purposes. This is defined as a group of 2 or more corporations, one of which is non-U.S. based, that prepares a GAAP or IFRS financial statement for non-tax purposes—the third-party debt is sent to foreign subsidiaries, and the group nets an interest expense of more than $12M for a 3-year period.

Foreign Tax Credit. One of the biggest changes is that credits will now be calculated on a country-by-country basis, which means there will be no more netting. Essentially, the FTC computation will assign income and loss to the taxable unit depending on which country the taxpayer is a tax resident in—or where it has a presence. It’s now time to look at Permanent Establishment. The degree to which excess credits can be used to offset tax liabilities in the present and the future has changed as well—the carry forward period of excess credits has been reduced from 10 years to 5 years, and there is no longer a one-year carryback allowance of FTCs.

Foreign-Derived Intangible Income (FDDII) Deduction. Any U.S. companies that export intangible goods like software outside the country and currently receive a reduced tax rate will be affected, as the new effective tax rate for FDII will increase to 20.7% under this reform. The BBA will also modify income eligible for treatment under the FDII, potentially impacting royalty income earned by foreign subsidiaries.

Estate tax provisions

The BBBA would be much less taxpayer-friendly than the TCJA when it comes to gift and estate taxes and strategies. Most notably:

The gift and estate tax exemption. The TCJA doubled the gift and estate tax exemption to $10 million through 2025. That amount is annually adjusted for inflation (for 2021, it’s $11.7 million). The BBBA would return the exemption to its pre-TCJA limit of $5 million in 2022. The amount would continue to be adjusted annually for inflation.

Grantor trusts. The assets in these trusts would no longer be excluded from a taxable estate if the deceased is deemed the owner of the trust. In addition, sales between individuals and their grantor trusts would be taxed as if they were transfers between the individual and a third party. And distributions from a grantor trust to an individual other than the grantor or the grantor’s spouse would be treated as a taxable gift from the grantor.

Valuation discounts. Taxpayers would no longer be able to claim discounts for gift and estate tax purposes on transfers of interests in entities that hold nonbusiness assets (that is, passive assets held for the production of income and not used for an active trade or business). For example, discounts couldn’t be used to reduce the value of transferred interests in family-owned entities that hold securities.

Note: An earlier proposal to end the stepped-up basis tax break on inherited assets is no longer in the current version of the BBBA.

Proposed tax provisions for individual tax payers

The current version of the BBBA includes several provisions that could affect the tax liability of individual taxpayers in ways both positive and negative, depending largely on their taxable income. Among other areas, the legislation addresses:

Individual tax rates. The top marginal tax rate would return to 39.6%, the rate that was in effect before the Tax Cuts and Jobs Act (TCJA) cut it to 37% beginning in 2018. This rate would apply to the taxable income of married couples that exceeds $450,000, single filers that exceeds $400,000 and married individuals filing separately that exceeds $225,000.

A surcharge on high-income taxpayers. The BBBA would establish a new 3% tax on modified adjusted gross income above $5 million for married taxpayers filing jointly and single filers and above $2.5 million for married individuals filing separately.

The capital gains and qualified dividends tax rate. The maximum rate would increase from 20% to 25% for taxpayers in the 39.6% tax bracket. The Biden administration earlier had proposed to raise it as high as 39.6%.

The net investment income tax (NIIT). The BBBA would expand the NIIT to apply to the trade or business income of high-income individuals, regardless of whether they’re actively involved in the business. The NIIT currently applies to certain investment income and business income only if it’s passive. As a result, active business income would go from being taxed at a maximum rate of 37% under the TCJA to a maximum rate of 46.4% (the 39.6% individual income tax rate plus the 3.8% NIIT plus the 3% high-income surcharge).

This change would apply when adjusted gross income (AGI) exceeds $500,000 for married couples filing jointly, $250,000 for married couples filing separately and $400,000 for other taxpayers. Business income subject to self-employment tax would be excluded.

The qualified business income (QBI) deduction. The Section 199A deduction for pass-through entities would be limited to $500,000 for married taxpayers filing jointly, $400,000 for single filers and $250,000 for married taxpayers filing separately.

The qualified small business stock (QSBS) exclusion. Capital gains from the sale of QSBS held more than five years currently are 100% excludable from gross income. The BBBA would limit the exclusion to 50% for taxpayers with an AGI over $400,000, regardless of filing status.

Retirement planning. The BBBA would prohibit IRA contributions by taxpayers whose 1) aggregate IRA and other account balances exceed $10 million and 2) taxable income exceeds $450,000 for married couples filing jointly or $400,000 for single filers or married taxpayers filing separately. These taxpayers also would have to take required minimum distributions equal to 50% of the value that exceeds $10 million and 100% of any amount over $20 million.

Roth IRA conversions. The BBBA would prohibit certain taxpayers from first making a nondeductible contribution to a traditional IRA and then converting it to a Roth IRA (to get around restrictions on who can contribute to a Roth IRA). The proposal would apply to taxpayers with taxable income exceeding $450,000 for married taxpayers filing jointly and $400,000 for single filers and married taxpayers filing separately.

Child and dependent care tax credits. The American Rescue Plan Act (ARPA), enacted earlier this year, temporarily expanded both the Child Tax Credit (CTC) and the Dependent Care Tax Credit (DCTC). The BBBA would extend the CTC through 2025 and make permanent the DCTC.

Premium tax credits (PTCs). The ARPA also expanded the availability of PTCs to subsidize the purchase of health insurance for 2021 and 2022. The BBBA would permanently expand the credits.

Banking activity reporting. The Biden administration has proposed requiring financial institutions to annually report the total amount of funds that go in and out of bank, loan and investment accounts (personal and business) that hold a value of at least $600. Reporting also would be required if the aggregate flow in and out of an account is at least $600 in a year.

As Democrats weigh including this proposal in one of the bills, it has received pushback from banks and privacy advocates. A revised version includes a $10,000 threshold, and exemptions for some common transactions, such as payments from payroll processors and mortgage payments, also are under consideration.

Stay tuned

It’s impossible to say which proposals will survive the ongoing negotiations intact. We’ll keep you up to date if and when the final legislation is enacted. In the meantime, contact us if you have concerns about how the proposed tax provisions may affect you personally or your business.

]]>The U.S. Small Business Administration (SBA) expanded eligibility in September 2021. While you may not have qualified or considered EIDL funding necessary previously, you might want to reconsider in light of yet another wave of COVID infections. But you’ll have to do so quickly, as the application deadline is December 31, 2021.

Shaky economic ground ahead?

Sen. Joe Manchin (D-WV) released a statement on December 19 announcing that he “cannot vote to move forward” on the BBBA. The $2.1 billion bill that passed in the U.S. House of Representatives includes numerous provisions related to healthcare, energy initiatives, immigration, education, social programs and taxes.

The Democrats lack the votes to pass the proposed legislation in the Senate without Manchin’s support. Yet Senate Majority Leader Chuck Schumer (D-NY) indicated on December 20 that he nonetheless intends to hold a vote on the bill in early 2022. Schumer’s announcement came hours after Goldman Sachs reduced its predictions for U.S. economic growth in 2022 based on Manchin’s statement.

Types of EIDL relief available

The COVID-19 EIDL program was created to make low-interest fixed-rate long-term loans to provide small businesses (including sole proprietorships and independent contractors) the working capital they need to withstand the effects of the pandemic. Three types of funding are available:

Loans. This funding type features a 30-year term and fixed interest rate of 3.75%. The proceeds can be used for any normal operating expense, including payroll, rent or mortgage, utilities, and other ordinary businesses expenses. Since the recent program expansion (see below), funds also can be used to pay or pre-pay business debt incurred at any time, including after submitting the application, and regularly scheduled payments of federal debt.

Targeted advances. Businesses located in low-income communities, have no more than 300 employees and have suffered more than a 30% reduction in revenue may qualify for a targeted advance up to $10,000. These advances don’t have to be repaid.

Supplemental targeted advances. Businesses in low-income communities that have no more than 10 employees and saw revenue declines of more than 50% may be eligible for an additional $5,000. Supplemental advances also don’t require repayment.

The recent expansion

The SBA has implemented several changes to make it easier for small businesses to access the COVID-19 EIDL loans. Among other things, the SBA:

- Expanded eligibility from organizations with no more than 500 employees (including affiliates) to encompass businesses in the hardest hit industries with no more than 500 employees per physical location, as long as the business (with affiliates) has no more than 20 locations,

- Increased the maximum loan amount from $500,000 to $2 million,

- Extended the payment deferment period to two years after the loan origination date for all loans (interest will accrue during that period, and principal and interest payments must be made over the remaining 28 years of the loan term), and

- Simplified the affiliation requirements.

The SBA has also limited entities that are part of a single corporate group to a combined total of no more than $10 million in COVID-19 EIDL loans.

Additional eligibility requirements

Applicants must be physically located in the United States or a designated territory and have suffered working capital losses due to the COVID-19 pandemic. In addition, the businesses must have been in operation on or before January 31, 2020.

Businesses (other than sole proprietorships) must have a valid tax identification number. Each owner, member, partner or shareholder of 20% or more must be a U.S. citizen, non-citizen national or qualified alien with a valid Social Security number.

For loans of $500,000 or less, you must have a credit score of at least 570. For larger loans, the credit score must be at least 625. Personal guaranty and collateral requirements may apply, too, depending on the amount of the loan.

The looming deadline

The SBA will accept applications for loans and targeted advances until December 31, 2021. It will continue to process applications after that date, until the funds are exhausted. While the SBA earlier advised businesses seeking supplemental targeted advances to submit applications by December 10, 2021, it later announced it will accept applications until year end. It can’t process applications after the deadline, though, so applications submitted near the deadline might not be processed.

Note that borrowers can request increases, up to their maximum loan eligibility amount, for up to two years after loan origination or until the program funds are exhausted. In addition, the SBA will accept reconsideration and appeal requests received before December 31, 2021, if received on a timely basis. For reconsiderations, that means within six months from the date the application was declined. Appeals must be received within 30 days from the date the reconsideration was declined.

Don’t dawdle

You can apply online for COVID-19 EIDL relief, but the clock is ticking. We can help you determine if you should go this route and help you collect the necessary documentation.

]]>Impact on the deficit

The House vote came after the Congressional Budget Office (CBO) released its score on the legislation on Nov. 18. The CBO estimates that the legislation will increase the deficit by $367 billion over a 10-year period.

However, the CBO score doesn’t take into account any additional revenues generated by improved compliance with federal tax laws. The BBBA allocates $80 billion for the IRS to heighten enforcement (which the CBO did include in its calculation), likely to target primarily high-wealth individuals, businesses and overseas transactions. The U.S. Treasury Department “conservatively” estimates increased IRS enforcement will lead to $400 billion in additional revenues over the 10-year period.

Significant tax proposals

Funding for the sweeping package largely comes from tax increases on high-income individuals and businesses, but the law also includes tax breaks for eligible taxpayers. Some of the most notable tax-related provisions include:

State and local taxes (SALT) deduction. The BBBA would amend the Tax Cuts and Jobs Act (TCJA) to raise the cap on the so-called SALT deduction from $10,000 to $80,000 ($40,000 for married taxpayers filing separately) for tax years 2021 through 2031. The limit would return to $10,000 in 2032.

Child tax credit (CTC). The American Rescue Plan Act (ARPA) expanded the CTC from $2,000 per child to $3,000 per child ages six through 17 and $3,600 per child under age six. The BBBA would extend the expansion through 2022.

Premium tax credits (PTCs). The ARPA expanded the availability of PTCs for health insurance purchased through Affordable Care Act exchanges (for example, Healthcare.gov) for 2021 and 2022. The BBBA would extend the expansion through 2025.

High-income surtax. The BBBA would create a 5% surtax on individuals with a modified adjusted gross income (MAGI) that exceeds $10 million ($5 million for married taxpayers filing separately). It adds another 3% surtax on MAGI exceeding $25 million ($12.5 million for married taxpayers filing separately). The surtax would take effect for 2022.

Net investment income tax (NIIT). The BBBA would expand the 3.8% NIIT to apply to the trade or business income of high-income individuals, regardless of whether they’re actively involved in the business. The income thresholds are over $500,000 for joint filers, over $400,000 for single filers and over $250,000 for married couples filing separately. The NIIT currently applies to business income only if the income is passive.

Retirement savings. The BBBA includes several limitations on the ability of high-income taxpayers with large retirement account balances to take advantage of certain tax breaks. For example, beginning in 2029, it would prohibit additional contributions to a Roth IRA or traditional IRA for a tax year if a taxpayer’s income exceeds a certain amount and the contributions would cause the total value of an individual’s IRA and defined contribution accounts as of the end of the prior tax year to exceed $10 million. The bill also would impose new mandatory distribution requirements on such taxpayers. But some retirement-related provisions would go into effect as soon as 2022, such as ones that would restrict and, in some circumstances, eliminate Roth conversions.

Minimum corporate tax rate. The BBBA would impose a 15% minimum tax on the profits of corporations that report more than $1 billion in profits to shareholders (book income vs. tax income), for tax years beginning after 2022.

Excess business losses. The BBBA would make permanent the Tax Cuts and Jobs Act’s limit on the amount of excess business losses that pass-through entities and sole proprietors can use to offset ordinary income. It also would create a new carryforward for unused excess business losses, rather than carrying them forward as net operating losses.

Excise tax on stock buybacks. The BBBA includes a 1% excise tax on the fair market value of stock buybacks by publicly traded U.S. corporations, which would be effective for repurchases after 2021.

Business interest deduction. The BBBA would add a new limit on the amount of net interest expense that certain corporations that are part of an international financial reporting group can deduct, for tax years beginning after 2022.

Moving on to the Senate

Now that the bill has been passed by the House, it still must fight its way through the Senate, where it faces additional debate. A Senate vote isn’t expected to take place until late December. Most likely the Senate will make some changes to the bill, which could include changes to some of the tax provisions. We’ll keep you apprised of the important developments.

]]>Early termination of the Employee Retention Credit

The IIJA terminates the Employee Retention Credit (ERC) created by the CARES Act earlier than originally planned. The American Rescue Plan Act (ARPA) had extended the credit to eligible employers for the third and fourth quarters of 2021. Under the new law, the ERC — which for 2021 is worth up to $7,000 per qualifying employee per quarter — is no longer available for wages paid after September 30, 2021 (rather than December 31, 2021), except for so-called “recovery startup businesses.”

The ARPA generally defines recovery startup businesses as those that began operating after February 15, 2020, and have annual gross receipts for the three previous tax years of less than or equal to $1 million. These employers can claim the ERC for up to $50,000 total per quarter for the third and fourth quarters of 2021, without showing suspended operations or reduced receipts.

However, clients can still file retractive amendments to claim credits missed (seek refunds) for Q1 – Q4 2020 and Q1 – Q3 2021.

New information reporting on digital assets

The IIJA requires brokers to report to the IRS the cost basis of digital assets transferred by their clients to nonbrokers, similar to how securities brokers report stock and bond trades. “Digital assets” are defined as “any digital representation of value which is recorded on a cryptographically secured distributed ledger or any similar technology.” This definition could ensnare not only cryptocurrencies like Bitcoin and Ethereum, but also certain nonfungible tokens (NFTs). The IIJA expands the definition of the term “broker” to include those who operate trading platforms for digital assets, such as cryptocurrency exchanges.

In addition, the IIJA modifies existing tax law to redefine “cash” subject to reporting to include “any digital representation of value”. As a result, individuals engaged in a trade or business must submit IRS Form 8300, “Report of Cash Payments Over $10,000 Received in a Trade or Business,” when they receive such amounts in one transaction or multiple related transactions.

The digital assets provisions take effect for returns required to be filed, and statements required to be furnished, after December 31, 2023. The IRS is expected to provide guidance before that time, but some businesses may find that accepting cryptocurrencies for payment isn’t worth the reporting burden.

Miscellaneous tax provisions

The IIJA extends several excise taxes used to fund highway spending, extends and modifies certain Superfund excise taxes, and allows private activity bonds for qualified broadband projects and carbon dioxide capture facilities. It extends pension funding relief and expands certain IRS administrative relief for taxpayers affected by federally declared disasters and “significant fires.”

More to come

The majority of the Democrats’ proposed tax law changes, to the extent they survive ongoing negotiations, will be included in the Build Back Better Act (BBBA). The BBBA could, for example, have significant provisions regarding the child tax credit, the cap on the state and local tax deduction, and limits on the business interest expense deduction. We’ll keep you current on the developments that could affect both your personal and business’s bottom lines.

]]>Accelerate and defer with care

One of the most reliable year-end tactics for reducing taxes has long been to accelerate your deductible expenses and defer your income. For example, self-employed individuals who use cash-basis accounting can delay invoices until late December and move up the planned purchase of equipment or the payment of estimated state income taxes from early next year to this year.

This technique has always carried the caveat that you generally shouldn’t pursue it if you expect to be in a higher tax bracket the following year. Potential provisions in the BBBA also may make it advisable for certain taxpayers to reverse the strategy for 2021 — that is, accelerate income and defer deductible expenses.

The current version of the BBBA would impose a new “surtax” of 5% on modified adjusted gross income (MAGI) that exceeds $10 million, with an additional 3% on income of more than $25 million. As a result, the highest earners could pay a 45% federal marginal income tax on wages and business income (the current 37% income tax rate plus 8%). It could be even higher when combined with the net investment income tax, which might be expanded to include active business income for pass-through entities.

In addition, there’s a proposal to temporarily increase the $10,000 cap on the state and local tax deduction to $80,000. Individuals in high-tax states should consider whether there may be an advantage to accelerating a 2022 property or estimated state income tax payment into 2021, or whether the deduction might be more valuable next year, particularly if they’ll face a higher effective tax rate.

Leverage your losses

Taxpayers with substantial capital gains in 2021 could benefit from “harvesting” their losses before year-end. Capital losses can be used to offset capital gains, and up to $3,000 ($1,500 for married persons filing separately) of excess losses (those that exceed the amount of gains for the year) can be applied against ordinary income. Any remaining losses can be carried forward indefinitely.

Beware, however, of the wash-sale rule. Generally, the rule prohibits the deduction of a loss if you acquire “substantially identical” investments within 30 days, before or after, of the date of the sale.

Taxpayers who itemize their deductions could compound their tax benefits by donating the proceeds from the sale of a depreciated investment to a charity. They can both offset realized gains and claim a charitable contribution deduction for the donation.

Satisfy your charitable inclinations

For 2021, charitable contributions can reduce taxes for both itemizers and non-itemizers. Taxpayers who take the standard deduction can claim an above-the-line deduction of $300 ($600 for married couples filing jointly) for cash contributions to qualified charitable organizations.

The adjusted gross income limit for cash donations is 100% for 2021; it’s scheduled to return to 60% for 2022. That means you could offset all of your taxable income with charitable contributions this year. (Donations to donor advised funds and private foundations don’t qualify, though.)

Taxpayers who don’t generally itemize can benefit by “bunching” their charitable contributions. In other words, delaying or accelerating contributions into a tax year to exceed the standard deduction and claim itemized deductions. For example, if you usually make your donations at the end of the year, you could bunch donations in alternative years — say, donate in January and December of 2022 and January and December of 2024.

Retired taxpayers who are age 70½ and older can reduce their taxable income by making qualified charitable contributions of up to $100,000 from their non-Roth IRAs. Retired or not, individuals age 72 and older can use such contributions to satisfy their annual required minimum distributions (RMDs). Note that RMDs were suspended for 2020 but are effective for 2021.

So long as the assets would be considered long-term if they were sold, donations of appreciated assets offer a double-barreled tax benefit. You avoid the capital gains tax on the appreciation and can deduct the asset’s fair market value as of the date of the gift.

Convert traditional IRAs to Roth IRAs

As in 2020, when many taxpayers saw lower than typical income, 2021 could be a smart time to convert funds in traditional pre-tax IRAs to an after-tax Roth IRA. Roth IRAs have no RMDs, and distributions are tax-free.

You’ll have to pay income tax on the converted funds, but it’s better to do so while subject to lower tax rates. Similarly, if you convert securities that have dropped in value, your tax may well be lower now than down the road — and any subsequent appreciation while in the Roth IRA will be tax-free.

It’s worth noting that President Biden had proposed including a provision in the BBBA that would limit the ability of wealthy individuals to engage in Roth conversions. There was a lot of back-and-forth with respect to these provisions, and the latest version of the House bill includes certain restrictions. Whether these provisions will make it past any Senate amendments remains to be seen, but the proposal could be a harbinger of future proposed restrictions.

Proceed with caution

The strategies outlined above always come with pros and cons, but perhaps never more so than now, when potentially significant tax legislation that would take effect next year is under negotiation. We can help you chart the best course in light of any developments.

]]>