Because of these newly tightened conditions, companies may face challenges when raising capital, forcing them to adopt a more thoughtful approach to seek funding. Likewise, investors will want to ensure their priorities are protected and their returns met. The combination of a given borrower’s need for capital and a financer’s desire to seek favorable returns may lead to the creation of agreements that have characteristics of both debt and equity. As such, it is crucial for all parties involved to understand the resulting tax classification and the treatment of these arrangements, so all expectations are met.

The taxation of debt and equity

For borrowers, the difference between debt and equity can be critical because interest payments are generally tax deductible and subject to certain limitations. Dividends or other payments related to equity would not be deductible for U.S. federal income tax purposes.

Enacted as part of the Tax Cuts and Job Act (TCJA) of 2017, one main limit on interest deductibility is the IRC 163(j) limit on the amount of business interest that can be deducted each year. This limit is calculated as 30 percent of adjusted taxable income, which prior to the 2022 tax year closely resembled earnings before interest, taxes, depreciation, and amortization (EBITDA). However, starting with the 2022 tax year adjusted taxable income excludes depreciation and amortization, becoming EBIT. This should result in a lower limit on the amount of interest expense that can be deducted each year. Any interest expense exceeding this annual limit can be carried forward to future years.

Determining if an arrangement is debt or equity for federal income tax purposes

Classifying an arrangement as debt or equity is made on a case-by-case basis depending on the facts and circumstances of a given agreement. While there is currently little guidance in this area beyond case law, the Internal Revenue Service (IRS) has issued a list of factors to consider when questioning whether something is debt or equity. (Keep in mind, however, that the IRS states not one factor is conclusive.) The factors include whether:

- An agreement contains an unconditional promise to pay a sum certain on demand or at maturity,

- A lender can enforce the payment of principal and interest by the borrower, and

- A borrower is thinly capitalized.

The courts have also established a broader — but similar — list of factors to consider when determining whether an instrument should be treated as debt or equity. Both the IRS and the courts have generally placed more weight on whether an instrument provides for the rights and remedies of a creditor, whether the parties intend to establish a debtor-creditor relationship, and if the intent is economically feasible. Some factors include:

- Participation in management (as a result of advances),

- Identity of interest between creditor and stockholder,

- Thinness of capital structure in relation to debt, and

- Ability of a corporation to obtain credit from outside sources.

For international companies, the characterization of debt or equity when considered in a cross-border funding arrangement is important, as withholding tax rates may apply to interest payments and may differ from tax rates applied to dividends. Further, withholding tax obligations occurs when a cash payment is made. If you have a cross-border arrangement, it is crucial to know if you have debt or equity on your hands.

Special rules related to payment-in-kind

Once it is determined that an agreement should be classified as debt for U.S. federal income tax purposes, some borrowers may prefer to set aside interest payments or pay interest with securities, which is often referred to as payment-in-kind (PIK). This is generally done to preserve cash flow for operations and growth of the business. When a borrower chooses this route, U.S. federal income tax rules will impute an interest payment to the lender.

While using a PIK mechanism will not automatically result in the debt being recharacterized as equity for federal income tax purposes, it can support viewing the instrument as equity.

Limits to deductible debt interest

There are limitations that can apply to interest deductibility. As noted above, IRC 163(j) limits deductibility of business interest; for a corporation, this is deemed to be all interest regardless of use. Another provision that can result in interest deductibility limitation is IRC 163(l), which applies to certain convertible notes and similar instruments held by corporations.

For cannabis operators, it is important to consider that IRC 280E disallows interest deductions. Hence, it is highly detrimental for cannabis operators to issue debt from entities that are cannabis plant-touching.

How we can help

Due to the nature of the debt versus equity analysis, companies thinking about fundraising should plan on how they intend to perform the raise and whether to have the raise treated as equity or debt. If debt classification is desired, a borrower should take the steps needed to strengthen the facts of the transaction to support the arrangement as a debt instrument.

MGO’s dedicated tax team has extensive experience advising companies across industries on capital-raising, debt refinancing and restructuring, recapitalizations, and other tax transactions. If you are planning to fundraise, or you are currently in the process of conducting a debt versus equity analysis, contact us today.

About the authors

Maryam Nicholes is a director and the national leader of MGO’s M&A Tax Advisory Services group. She has more than 13 years of experience advising on a wide range of clients, consulting on structuring and implementation of transactions including mergers, acquisitions and dispositions, global reorganizations, and new investment platforms. She also provides planning and related deal modeling regarding global cash tax exposures, repatriation planning, and related debt structuring and workout. Contact Maryam at MNicholes@mgocpa.com.

Matt Sapowith is a tax partner at MGO. He has more than 14 years of tax planning and compliance experience in areas including corporate and partnership taxation, international tax, M&A transaction advisory, transfer pricing, state and local tax, R&D credit, and compensation planning. He assists companies with structuring for multiple business lines, excise tax and sales tax planning and compliance in a variety of industries including technology, financial services, manufacturing and distribution, professional services, retail and consumer goods, cannabis, and cryptocurrency. Contact Matt at MSapowith@mgocpa.com.

]]>In the following, we explain the updated PPP loan terms and conditions and how to fast-track potential loan forgiveness.

Third wave of Paycheck Protection Program relief

After the second wave of PPP loans ran dry in August of 2020, Congress moved to fund the popular relief program for a third, and potentially final, time. Within the larger CAA bill, the Economic Aid to Hard-Hit Small Businesses, Nonprofits, and Venues Act (the “Act”) earmarked up to $284 billion for PPP loans available through March 31, 2021. Several categories of loans were created to provide:

- A second PPP loan for small businesses that already used their first PPP loan (“Second Draw Loan”)

- A first PPP loan for small businesses that did not receive a 2020 loan (“First Draw Loan”)

- An increase to the amount of 2020 PPP loans to account for expanded qualifying expenses and conditions (“increased Draw of 2020 PPP Loans”)

Taking a look a Second Draw PP Loans

Perhaps the most anticipated change to the PPP loan system is the newly implemented option of attaining a second loan after having secured a first PPP loan.

To qualify for a Second Draw PPP Loan, an eligible entity is defined as any small business that has 300 or fewer employees and can demonstrate a 25% or greater decline in gross receipts for any one quarter in 2020 – compared to the corresponding quarter in 2019. The Act also requires that small business applicants have used, or will use, all of their 2020 PPP loan funds by the loan funding date.

To receive a loan that exceeds $150,000, the applicant must submit documentation that substantiates the 25% revenue reduction. For loans that do not exceed $150,000, documentation is not required for the application, however the borrower must submit documentation to receive forgiveness of the loan.

Second Draw PPP Loan Eligible Entities: In addition to those included in the 2020 PPP loans, eligible entities have been expanded to include housing cooperatives; certain nonprofit 501(c)(6) business organizations; certain news and broadcasting organizations; and destination marketing organizations. The Act also specifically excludes publicly traded entities and their affiliates; debtors in bankruptcy proceedings; entities engaged in political or lobbying activities; companies organized in China or that have a director that is a resident of China; any participant in the Shuttered Venue Operator Grant Program; and any business that was not in operation on February 15, 2020.

Second Draw PPP Maximum Loan: The maximum amount of the Second Draw PPP Loan is the lesser of a) $2 million ($4 million for an affiliated group) or b) 250% of the average payroll costs incurred or paid for either calendar 2019 or the one-year period before the date on which the Second Draw PPP loan is made. For NAICS 72 businesses, including restaurants, hotels, bars and other hospitality businesses, the percentage of average monthly payroll costs is increased to 350%.

Use of Second Draw PPP Loan Proceeds: In addition to the permitted uses outlined in the 2020 PPP program, the Act expands the types of expenditures that qualify for the loan and for loan forgiveness. Additionally, the percentage of proceeds that apply to non-payroll expenditures is increased from 30 to 40%. The covered expenses include:

• Operating Expenditures – Payment for any business software or cloud computing service that facilitates business operations; product or service delivery; processing of payments or tracking of payroll expenses, human resources, sales and billing functions; or accounting or tracking of supplies, inventory, records and expenses.

• Property Damage Costs – Property damage costs that are related to property damage and vandalism or looting due to pubic disturbances that occurred in 2020 and was not covered by insurance or other compensation.

• Supplier Costs – Covered supplier costs are expenditures for the supply of goods that (a) are essential to the operations of the PPP borrower at the time at which the expenditure is made and (b) are made pursuant to a contract, order or purchase order:

o (i) in effect at any time before the covered period with respect to the applicable covered loan or;

o (ii) with respect to perishable goods, in effect before or at any time during the covered period with respect to the applicable covered loan.

• Worker Protection Expenditures – Covered worker protection expenditures are any operating or capital expenditures to facilitate the adaptation of the business activities of a PPP borrower to comply with federal, state or local requirements established or guidance issued during the period beginning on March 1, 2020, and ending the date on which the national emergency declared by the President expires. This includes costs related to the maintenance of standards for sanitation, social distancing, or any other worker or customer safety requirement related to COVID-19.

• Additional included Payroll Costs – In addition to the allowable payroll costs in the 2020 PPP, the definition of includable payroll costs was expanded to include payments for group life, disability, vision and dental insurance benefits.

Second Draw PPP Loan Forgiveness. A borrower is eligible for forgiveness of a Second Draw PPP Loan in an amount equal to the sum of the following listed costs incurred and payments made during the covered period. The covered period is an 8- to 24-week period selected by the PPP borrower at the beginning of the loan period. Forgivable expenditures include:

a. payroll costs,

b. payments of interest on any covered mortgage obligation (but not any prepayment of or payment of principal on a covered mortgage obligation),

c. payments on any covered rent obligation,

d. covered utility payments,

e. covered operations expenditures,

f. covered property damage costs,

g. covered supplier costs, and

h. covered worker protection expenditures.

For loan forgiveness, payroll costs must comprise at least 60% of the forgiveness amount requested. This is a reduction from the 70% required for the original Cares Act.

Revised conditions for First Draw PPP Loans

First Draw PPP Loans are available to any small business that did not apply for or receive a 2020 PPP loan in the first round. Entities are eligible for a First Draw PPP loan if the business:

• Has less than 500 employees, and

• Is either a business concern, veterans’ organization, nonprofit, sole proprietor, self-employed individual, or independent contractor, and

• The SBA is still requiring businesses applying for loans over $2 million to meet the “necessity test.” That requirement means borrowers have to certify that the PPP loan is necessary to support their business’s ongoing operations. It can be a tricky requirement to meet, so make sure to talk to your financial and legal advisors.

Certain modifications in the Act apply retroactively to the 2020 PPP loans. This should be taken into consideration for a Second Draw PPP Loan, the 2020 PPP loan forgiveness application, and potentially 2020 tax returns. These items include retroactive application of:

• The covered costs as expanded in the Act and noted in the Second Draw PPP Loan, above.

• The requirement for the payroll component is reduced to 60% of the forgiveness amount, reduced from 70%.

Increased draw of 2020 PPP Loans

Since many of the provisions of the Act pertaining to PPP Loans were given retroactive to March 27, 2020, the date on which the PPP was established by the CARES Act. 2020 PPP loan recipients may be able to request an increase to their 2020 PPP Loan amount in certain circumstances if and, only if, the SBA did not issue a loan forgiveness determination on or before December 26, 2020. These circumstances include (a) partnerships and limited liability companies taxed as partnerships that did not include any amount for partner compensation, and (b) seasonal employers whose calculation of their maximum loan amount increased based on the changes made by the Economic Aid Act.

In addition:

(a) a 2020 PPP Loan recipient that returned all of its 2020 PPP Loan may apply for a First Draw PPP Loan;

(b) a 2020 PPP Loan recipient that returned part of its loan may reapply for a loan amount equal to the difference between the loan amount retained and the loan amount previously approved; and;

(c) a 2020 PPP Loan recipient that did not accept the full amount of the loan for which it was approved may request an increase in the 2020 PPP Loan amount up to the amount previously approved.

PPP Loan forgiveness

The process of applying for forgiveness for a loan over $150,000 remains the same. However, a shortcut to forgiveness for businesses that receive a loan equal or less than $150,000 has been implemented. The loan will be forgiven if its representative signs and submits to its lender a certification that is less than one page in length that lists:

(a) the number of employees the recipient was able to retain because of the covered loan;

(b) the estimated amount of the covered loan amount spent on payroll; and

(c) the total loan value.

Final thoughts

The PPP loan system has been a much-needed source of financial relief for organizations hit hard by the COVID-19 pandemic. With the third round of PPP loans now live, there are no guarantees that there will be any more rounds funded in the future. In addition, Employee Retention Credits (ERC) may be available to companies that meet the eligibility requirements, retroactive to March 13, 2020.

To make sure you get the loan amounts you are due, maximize the potential for forgiveness, and consider whether you qualify for ERC, it is recommended you consult with MGO’s dedicated accounting specialists.

]]>Everything changes, except when it doesn’t

Time and time again we’ve seen reactions to various accounting scandals, after which new policies, procedures, and legislation are created and implemented. An example of this is the Sarbanes-Oxley Act (SOX) of 2002, which was a direct result of the accounting scandals at Enron, WorldCom, Global Crossing, Tyco, and Arthur Andersen.

SOX was established to provide additional auditing and financial regulations for publicly held companies to address the failures in corporate governance. Primarily it sets forth a requirement that the governing board, through the use of an audit committee, fulfill its corporate governance and oversight responsibilities for financial reporting by implementing a system that includes internal controls, risk management, and internal and external audit functions.

Governments experience challenges and oversight responsibility similar to those encountered by corporate America. Governance risks can be mitigated by applying the provisions of SOX to the public sector.

Some states and local governments have adopted similar requirements to SOX but, unfortunately, in many cases only after cataclysmic events have already taken place. In California, we only need to look back at the bankruptcy of Orange County and the securities fraud investigation surrounding the City of San Diego as examples of audit committees that were established in response to a breakdown in governance.

Taking your audit committee on the right mission

Governments typically establish audit committees for a number of reasons, which include addressing the risk of fraud, improving audit capabilities, strengthening internal controls, and using it as a tool that increases accountability and transparency. As a result, the mission of the audit committee often includes responsibility for:

- Oversight of the external audit.

- Oversight of the internal audit function.

- Oversight for internal controls and risk management.

Chart(er) your course

Most successful audit committees are created by a formal mandate by the governing board and, in some cases, a voter-approved charter. Mandates establish the mission of the committee and define the responsibilities and activities that the audit committee is expected to accomplish. A wide variety of items can be included in the mandate.

Creating the governing board’s resolution is the first step on the road to your audit committee’s success.

Follow the leader(ship)

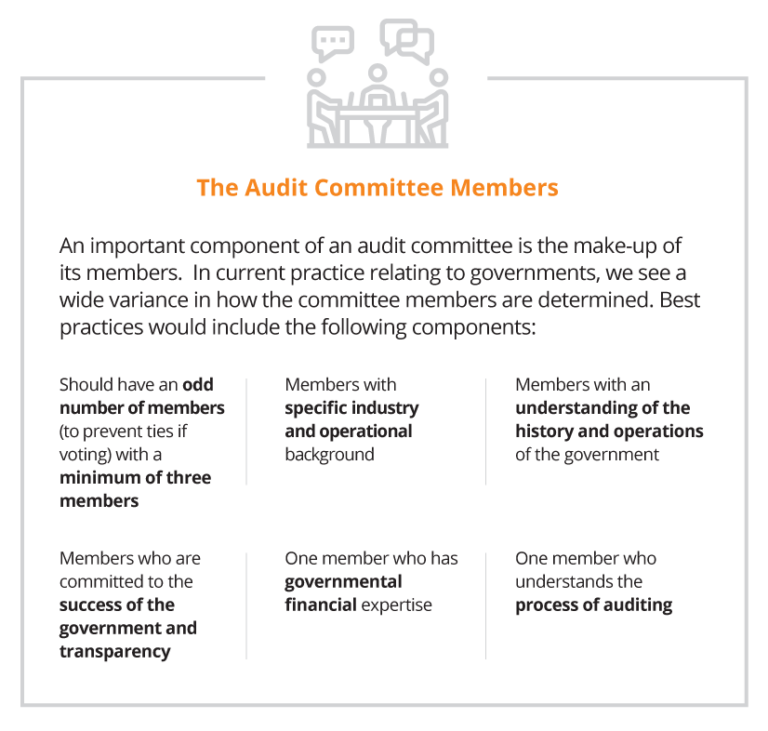

In practice we see a combination of these attributes, ranging from the full board acting as the audit committee, committees with one or more independent outsiders appointed by the board, and/or members from management and combinations of all of the above. While there are advantages and disadvantages for all of these approaches, each government needs to evaluate how to work within their own governance structure to best arrive at the most workable solution.

Strike the right balance between cost and risk

The overriding responsibility of the audit committee is to perform its oversight responsibilities related to the significant risks associated with the financial reporting and operational results of the government. This is followed closely by the need to work with management, internal auditors and the external auditors in identifying and implementing the appropriate internal controls that will reduce those risks to an acceptable level. While the cost of establishing and enforcing a level of zero risk tolerance is cost prohibitive, the audit committee should be looking for the proper balance of cost and a reduced level of risk.

Engage your audit committee with regular meetings

Depending on the complexity and activity levels of the government, the audit committee should meet at least three times a year. In larger governments, with robust systems and reporting, it’s a good practice to call for monthly meetings with the ability to add special purpose meetings as needed. These meetings should address the following:

External Auditors

- Confirmation of the annual financial statement and compliance audit, including scope and timing.

- Ad hoc reporting on issues where potential fraud or abuse have been identified.

- Receipt and review of the final financial statements and auditor’s reports

- Opinion on the financial statements and compliance audit;

- Internal controls over financial reporting and grants; and

- Violations of laws and regulations.

Internal Auditors

- Review of updated risk assessments over identified areas of risk.

- Review of annual audit plan, including status of the prior year’s efforts.

- Status reports of ongoing and completed audits.

- Reporting of the status of corrective action plans, including conditions noted, management’s response, steps taken to correct the conditions, expected time-line for full implementation of the corrective action and planned timing to verify the corrective action plan has been implemented.

Establish resources that are at the ready

Audit committees should be given the resources and authority to acquire additional expertise as and when required. These resources may include, but are not limited to, technical experts in accounting, auditing, operations, debt offerings, securities lending, cybersecurity, and legal services.

Taking extra steps now will save time later

While no system can guarantee breakdowns will not occur, a properly established audit committee will demonstrate for both elected officials and executive management that on behalf of their constituents they have taken the proper steps to reduce these risks to an acceptable tolerance level. History has shown over and over again that breakdowns in governance lead to fraud, waste and abuse. Don’t be deluded into thinking that it will never happen to your organization. Make sure it doesn’t happen on your watch.

]]>By Scott P. Johnson, CPA, CGMA

Partner, State & Local Government, Advisory Services

As a public official for more than 24 years, I continuously strived to implement best practices, internal controls and policies and procedures to mitigate fraud, waste and abuse. Being a municipal finance officer responsible for literally billions of dollars, there were times when I would wake up in the middle of the night thinking about what could happen or what I may not know that could be occurring that could put the organization at risk. Fortunately throughout my municipal career the organizations I served did not experience headlines due to significant fraud. We had the appropriate “tone at the top” and practiced effective measures throughout the organization to mitigate potential fraud. However, from time-to-time, we would uncover the occasional lapse of an employee’s good judgement and detect inappropriate use of government funds, such as; improper procurement credit card use for personal purposes, time cards reporting that fraudulently claimed hours worked in excess of actual hours worked, and fictitious reimbursement claims for travel.

Employee fraud is a significant problem across industries and is faced by organizations of all types, sizes, locations, and industries. While employee fraud in private organizations rarely merits a mention in the local paper, the same fraud in a government agency will have editors competing to write the splashiest headlines and garner the highest reader traffic. It is critical for such organizations to maintain a positive reputation. Reputational risk can carry long-lasting damage in monetary losses, regulatory issues, and overall risk exposure. Frankly, all types of fraud are on the rise, and municipalities need an effective fraud mitigation strategy in place to protect against reputational and monetary harm.

Just a few recent examples of municipal fraud that have had significant press coverage and put the respective organizations in a challenging position: In 2014 officials in St. Louis County, IL, uncovered a $3.4 million embezzlement that escaped detection for more than six years. According to officials, a County Health Agency Division Manager overcharged for IT computer and technical services (unbeknownst to the County, the Division Manager owned the technology company). Unfortunately, the day after the suspected embezzlement was detected by County officials, the employee committed suicide, according to the County Medical Examiner.

The largest known municipal fraud in US history was uncovered in 2012 at the City of Dixon, IL. This embezzlement scheme of almost $54 million over a 22 year period was perpetrated by its Comptroller, Rita Crundwell, who used the proceeds to finance her quarter horse ranch business and lavish lifestyle. She was convicted and pleaded guilty to the crimes and is currently serving a 20 year sentence. Another recent case of an alleged fraud allegation is currently under trial in the Los Angeles Superior Court in which ex-Pasadena city employee, Danny Wooten and co-defendants are due back in court for arraignment on April 1, 2016, according to the Los Angeles County District Attorney’s Office. The criminal case involves allegations that more than $6 million in city money was embezzled over a decade in which Wooten is suspected of creating false invoices for the underground utility program between 2004 and March 2014.

Many factors can contribute to fraud, but the key factors are the improper segregation of duties, lack of management review, maintaining undocumented procedures, common exception processing, trust without verification and validation, and lack of accountability and monitoring. Employing proper risk assessments of events that could prevent, delay, or increase the costs of achieving organizational objectives and implementing a risk management plan not only ensure compliance, but strategically safeguard on organization against fraud. There are three important steps to earning a good night’s sleep.

1. Fraud Risk Assessment – understanding the organization as a whole and individual business units will lead to the most comprehensive risk management plan. Understand how resources flow as well as internal environments and processes. Conduct interviews, make observations and review all factors. Identify the possible and probable fraud schemes for all resource flows.

2. Prevention – “Tone at the Top” is critical. Inspiring employees to follow ethical standards starts with the tone at the executive level and must trickle down through the management level and ultimately throughout the entire organization. The organization needs to know that unethical practices will not be tolerated and when detected, will be dealt with in a timely and effective manner. One measure to communicate the “tone” is writing a fraud policy in concert with the employee conduct handbook will ensure the message is designed into the orientation, onboarding, and training process. Conduct management reviews, provide whistleblower channels, and communicate often with key business unit leaders, who in turn should communicate with their staff regarding fraud prevention, detection, and correction.

3. Detection – while assessment and prevention will create a strong defense against fraud, it is still important to seek out other measures to detect fraud that may not have been included in the fraud risk assessment plan. Only three percent (3%) of all fraud is discovered by accident or the good luck of the right person in the right place. Only six percent (6%) of fraud is discovered through account reconciliation. Clearly we cannot simply rely on these detection methods. In addition to account reconciliation and keeping your ears open, creating channels for detection are of the utmost importance. Eleven percent (11%) of fraud discoveries are due to an internal audit. Return to step one by assessing and re-assessing fraud risk regularly. Conduct meaningful management reviews on-time. Twelve percent (12%) of fraud detection were the result of properly conducted management reviews. Finally, be sure to enforce an open door policy and a culture of interest in detection and reporting. Fifty-four percent (54%) of all fraud detection comes through insider tips. Ensuring there are proper procedures in place to accept these tips is paramount when designing and especially, implementing the fraud management and detection plan.

Deceitful misconduct among employees significantly damages reputations, negatively affects resources, and limits the ability of any organization to effectively serve the consumer and their community. Following this roadmap on how to respond to and prevent employee fraud will not only protect the organization and its key objectives but will lead to an easier night’s sleep – even in the face of increasing fraud across all industries.

This article is only a small representation of the material presented during MGO’s “Case in Point” presentation at the 2016 CSMFO Conference. Special recognition to Ruthe Holden, Internal Audit Manager at the City of Pasadena for her contribution to the “Case in Point” presentation. Contact Scott Johnson at sjohnson@mgocpa.com if you have any questions or comments. Comments and opinions expressed in this article are those of the authors and may not reflect the positions, opinions, or beliefs of the CSFMO or MGO and should not be construed or interpreted as such.

]]>- Insufficient outreach to vendors

- Lowering of bonding requirements

- Burdensome administrative requirements

- Insufficient segregation of procurement approval and receiving duties

- Lack of cross-department evaluation of vendor proposals

- Inconsistent management and designated authority levels

- Organizations are unaware of procurement process times – from start of requisition until vendors are paid

- Procurement activities are not aligned with overall organizational activities

- Too many sign offs/approvals

If any of these issues sound familiar, or your organization has not reviewed its procurement function in a while, you run the risk that your procurement strategies are inconsistent with organizational needs, which can result in paying higher prices for the goods and services required to run your agency, insufficient number of competitive bids, or worse, violating your grant or service agreements.

IntelliBridge Partners has the expertise to improve the procure to pay cycle through business process reviews, risk assessments, and performance audits. If you would like help with your procurement department, please contact Greg Matayoshi at gmatayoshi@intellibridgepartners.com.

]]>What is the cannabis banking crisis?

Very simply put, the conflict between state and local cannabis laws that allow for adult- and medicinal-use of cannabis are in conflict with federal laws that categorize cannabis as a Schedule I controlled substance. As a result, major banking institutions are reluctant to provide traditional banking services to cannabis companies due to the risk of federal prosecution for money laundering or a variety of other offenses.

As a result, the cannabis industry is almost exclusively cash-based. Cannabis business operations – including payroll, rent/lease payments, vendor payments and taxes – are primarily conducted with cash. This results in hundreds of thousands of dollars in cash being moved between locations, simply to pay farms or manufacturers, or even to pay taxes. This inefficient system leads to a wide variety of issues, including significant operational difficulties, and growing risk threats from both untrustworthy employees and out right robbery.

Cannabis businesses have found a number of creative ways to navigate the banking issue. Some business restructure so a professional services firm, not directly touching the cannabis, provides payroll and other financial services. Shops and dispensaries have adopted a variety of debit or gift card payment systems. And finally, a handful of cannabis operators have established relationships with local credit unions willing to work with the industry. But the vast majority of cannabis operators must navigate daily risks related to the collection and remittance of large cash sums.

The banking crisis hearing

“We’re trying to examine how outdated banking regulations on the federal level are hindering reform on the state level when it comes to marijuana,” said Democratic Congressman Gregory Meeks, chairman of the Consumer Protection and Financial Institutions subcommittee, in advance of Wednesday’s hearing. The event brought together a wide range of affected parties, including representatives of credit unions and banks, cannabis industry advocates, and finally government officials advocating for responsible cannabis laws.

The hearing was called to discuss the Secure and Fair Enforcement Banking Act of 2019 (SAFE act). The bill was introduced by a bipartisan coalition that includes Colorado Democratic Rep. Ed Perlmutter, Washington Democratic Rep. Denny Heck and Ohio Republicans, Rep. Steve Stivers and Rep. Warren Davidson. The SAFE act seeks: “To create protections for depository institutions that provide financial services to cannabis-related legitimate businesses, and for other purposes.”

Cannabis banking advocates emerge

Prior to the hearing, the American Bankers Association offered public support for the SAFE act, stating in part: “Simply excluding legal state cannabis activity from the banking sector has not prevented the growth and spread of this industry, but providing access to the banking system could help facilitate public safety, streamline tax payments, and enable effective oversight in the states where voters have chosen to embrace cannabis legalization.”

Fiona Ma, Treasurer for the State of California, offered her support for the bill in a written testimony that reads in part: “an effective safe harbor mechanism in federal law promotes the safety of the public, improves the efficiency of collecting the taxes and fees we use to regulate the industry, and does not allow the banks and credit unions to totally abdicate their responsibilities to know their customers and avoid illicit money laundering.”

“(Current laws) encourage tax fraud, add expensive monitoring and bookkeeping expenses and—most importantly—leave legitimate businesses vulnerable to theft, robbery and the violence that accompany those crimes,” said Maj. Neill Franklin, Executive Director of the Law Enforcement Action Partnership (LEAP). He closed his passionate testimony by stating that the “safety of thousands of employees, business owners, security personnel, police officers and community members is in your hands.”

What can cannabis businesses do until laws change?

The primary purpose of the hearing was to create public momentum for a change in cannabis banking laws. The House Financial Services subcommittee heard hours of public testimony, largely in support of changing federal laws to support the cannabis industry. While nothing concrete emerged from the hearing, allowing so many influential advocates and politicians to publicly support the cannabis industry represents a major step-forward.

It will be a long process before any laws change, but in the meantime there are a number of legal actions a cannabis business can take to alleviate the stress of being denied traditional banking relationships. Most of these, including restructuring a business or implementing alternative payment systems, are complex activities that require professional guidance to execute successfully.

Additionally, there are a number of cash management solutions and internal controls all cannabis businesses should implement to limit opportunities for fraud and criminal abuse, both internally and externally. The MGO | ELLO Cannabis Alliance has long been an advocate for responsible practices regarding cash management in the cannabis industry. The Alliance provides a comprehensive suite of risk management solutions designed to promote operational best practices in the cannabis industry.

For more information or to arrange a consultation, please contact us.

About the author:

Linda Hurley is the leader of the MGO | ELLO Alliance Governance, Risk, and Compliance practice. She has over 20 years of experience providing risk advisory, compliance, accounting, internal audit, and auditing services to a wide variety of public and private companies. She is primarily focused on providing cannabis enterprises with a holistic view of their risk and compliance needs. She designs and implements internal controls, risk management procedures, and governance practices that support every level of a cannabis organization.

]]>60 speakers were given three minute slots, during which they could make a public statement regarding the treatment of hemp in the Farm Bill. The speakers (selected via a submission process) represented a wide variety of related parties and included: representatives from state-level agriculture, regulatory and law enforcement agencies; private sector business owners and entrepreneurs; Native American tribal leaders; and a variety of other industry advocates and stakeholders.

The diversity of speakers helped represent a broad view of issues and concerns related to the expansion of hemp cultivation. Due to the fact that it was a listening session, the USDA did not respond to any concerns raised. In the following article, we examine a number of recurrent themes raised by speakers, which illustrate concerns regarding the future of industrial hemp production in the US.

Difficulty distinguishing between hemp and cannabis

Hemp and “consumable cannabis” (adult-use or medicinal cannabis) are the same plant, and are only distinguished by the level of THC. Per the Farm Bill’s definition, industrial hemp contains less than 0.3% THC, in contrast to “cannabis,” which can contain up to 20% THC. To sight and smell, the two are indistinguishable, which places a great amount of importance on testing measures for THC.

A recurring issue, raised by both regulatory and law enforcement officials and hemp cultivators and advocates, is the lack of universal testing measures. Officials expressed concern that it was incredibly difficult to test THC content via roadside stops or in customs examinations. This results in delays to traffic and other processes and can lead to unlawful detainment and seizures. On the commercial side, hemp producers don’t want to see their legal shipments delayed or seized.

Speakers from all sides of the issue agreed that for the hemp industry to move forward, the USDA will need to define consistent testing measures and help provide training to officials tasked with regulating the cultivation and transportation of hemp.

Treating hemp as a viable agricultural commodity

The Farm Bill removed industrial hemp (as defined previously) from the Federal Controlled Substances Act, in effect decriminalizing hemp production. And yet, many advocates brought up concerns related to provisions in the Farm Bill that they felt continued to treat hemp as a scheduled drug.

For example, the Farm Bill requires license applications prior to cultivating hemp, which leads to background checks for the licensees. No other commercial crop requires diligent background checks, and subsequent application and processing fees.

Similarly, the Farm Bill did not eliminate the requirement under the Controlled Substances Import and Export Act wherein the importation of hemp seeds requires registration with the DEA. Industrial hemp has a strong history of cultivation in other parts of the world, including Canada and Europe, and the agricultural science and genomics of hemp in these regions are far ahead of the US. Access to advanced genetics in hemp crops is essential to commercial production and the DEA requirement presents a major roadblock to free trade.

These are just two examples of ways in which the specter of hemp’s past as a controlled substance continues to linger. Asking the USDA and other federal agencies to go all the way with decriminalizing every aspect of hemp motivated commentary across a number of regulatory and operational concerns.

Access to financial institutions for hemp growers

Like any other agribusiness, hemp businesses need access to lines of credit, insurance, and other traditional banking relationships. And yet, like the cannabis banking crisis, a number of hemp cultivators expressed concern related to the reluctance of financial institutions to work with them.

Representatives of financial institutions, including banks and credit unions, also made their voice heard, asking for clear protection against liability so they would feel able to serve hemp producers. Both parties concurred in requesting that the USDA make a clear pronunciation regarding access to banking for hemp producers.

While the SAFE Act has made progress in recent months, there are no guarantees about access to banking for all cannabis businesses. In the meantime, the industrial hemp industry seeks clear and strong direction at the federal level to ease the path to traditional banking.

Lack of clarity for Tribal Lands and sovereign nations

A number of Native American communities and leaders were given an opportunity to speak during the listening session and all shared enthusiasm about the potential economic benefits of hemp cultivation on tribal land. And yet, many pointed to a lack of clarity regarding regulation and self-governance for tribal communities in the 2018 Farm Bill.

For example, the management of much tribal land is a complex web of oversight from federal agencies combined with the autonomous control of tribal governments. A number of Native American leaders asked for further guidance regarding hemp production from the USDA so tribal nations can participate in upcoming planting seasons.

The balance of federal and state oversight

The 2014 Farm Bill carried provisions allowing for the creation of hemp-growing pilot programs at the state level. The successful inclusion of hemp production in the 2018 bill owes much to the success of these pilot programs. During the listening session a number of representatives from state agricultural agencies raised their voices to speak to the success of their programs and to support a continued balance between federal and state oversight.

Kentucky, Wisconsin, and Colorado all provided details on the growth of hemp in their respective states and made the case that future USDA laws should not interfere with state’s rights in the matter of hemp. At the same time, they acknowledged the essential role in federal oversight protecting and ensuring factors that include: intra-state commerce, managing import/export laws and enforcement, and the implementation of standardized testing protocols.

What is next for industrial hemp in the US?

The above topics were a sample of the diverse range of issues and concerns that remain undefined under the current wording of the 2018 Farm Bill. In coming months, each state and tribal nation will have the opportunity to submit a regulatory system governing hemp production in their respective jurisdictions. Those proposals will then be reviewed and approved by the USDA.

The USDA also seeks to implement a regulatory system that addresses these concerns, and more, which is scheduled for release in fall of 2019. If all goes well, hemp producers across the nation will have clear guidance to move forward as early as 2020.

]]>Many cheered the passage of the 2018 Farm Bill, which descheduled industrial hemp and its derivatives (including CBD). But that was just the start of a much more complicated regulatory story that continues to have a major impact on entrepreneurs, investors, and advocates and patients who rely on CBD.

CBD and the 2018 Farm Bill

When President Trump signed the 2018 Farm Bill into law one of the key changes affecting the cannabis industry was the separation of “hemp” and “marijuana.” Before the Farm Bill, any incarnation of the cannabis plant and its byproducts were lumped into a single category and considered a Schedule 1 drug. Key language in Section 1103 of the Farm Bill defines hemp as:

“the plant Cannabis sativa L. and any part of that plant, including the seeds thereof and all derivatives, extracts, cannabinoids, isomers, acids, salts, and salts of isomers, whether growing or not with a delta-9 tetrahydrocannabinol concentration of not more than 0.3 percent on a dry weight basis.”

In short, the Farm Bill descheduled industrial hemp and its byproducts as long as it stayed under the threshold of less than 0.3 percent THC. CBD is derived from the cannabis plant, whether there are significant levels of THC or not. CBD industry advocates have interpreted the language “all derivatives, extracts, cannabinoids, isomers, acids, salts, and salts of isomers” as descheduling CBD when industrial hemp is the source. And they are “mostly” correct in this interpretation. Unfortunately, there are other federal agencies in play.

CBD and the FDA

United States Department of Agriculture (USDA) enacted the 2018 Farm Bill in their position overseeing laws related to the cultivation of industrial hemp. The United States Food and Drug Administration (FDA) oversees medicine and food additives. CBD has emerged as a “wonder drug” with a growing list of potential benefits and now appears as an additive in a wide range of consumer products. In addition, the FDA approved Epidiolex, the first CBD-derived drug, in 2018.

All of this has culminated in CBD being a priority of the FDA, so much so, that just a week after the Farm Bill was signed into law, the FDA issued a press release clarifying and asserting their regulatory control over all cannabis-derived compounds.

“We treat products containing cannabis or cannabis-derived compounds as we do any other FDA-regulated products — meaning they’re subject to the same authorities and requirements as FDA-regulated products containing any other substance. This is true regardless of the source of the substance, including whether the substance is derived from a plant that is classified as hemp under the Agriculture Improvement Act.”

Concurrent with the Farm Bill and the press release regarding CBD, the FDA also issued three Generally Regarded as Safe (GRAS) notices for hemp by-products: hulled hemp seeds, hemp protein powder, and hemp seed oil. Clearly demonstrating that (some) hemp products have been descheduled and cleared for use by the FDA.

The FDA’s policy is different toward CBD for two key reasons. Firstly, CBD products are largely marketed with a wide variety of therapeutic claims. In their press release the FDA notes:

“The FDA requires a cannabis product (hemp-derived or otherwise) that is marketed with a claim of therapeutic benefit, or with any other disease claim, to be approved by the FDA for its intended use before it may be introduced into interstate commerce.”

Secondly, the FDA’s approval of CBD-based drug Epidiolex, put CBD and THC into the category of “active ingredients in FDA-approved drugs.” Under the Federal Food, Drug, and Cosmetic Act (FD&C Act) it is “illegal to introduce drug ingredients like these into the food supply, or to market them as dietary supplements.”

In short, the FDA does not distinguish between CBD derived from hemp or “marijuana,” and until the agency approves CBD and establishes a regulatory framework, adding CBD to food and beverages is illegal.

Has the regulation of CBD slowed businesses?

While early CBD research has shown promise as a treatment for conditions like epilepsy and anxiety, as a consumer product it is unproven and has been largely unregulated until recently. In the absence of labeling standards and regulated dosage guidelines, consumers often have little understanding of what they are buying and its potential effects.

All of this uncertainty has earned greater regulatory attention for CBD. There have been reports of crackdowns on bakeries, restaurants and retailers selling CBD in California, New York, Maine and Ohio, just to name a few. This regulatory response has shocked and angered a number of hemp producers and CBD retailers who have invested millions into business ventures that they feel only supply the public with products that help manage health concerns.

Despite the confusing legality, the CBD industry appears to be moving full-steam ahead. In recent months, national retailers as diverse as Walgreens, DSW and Barney’s New York have announced plans (or have already begun) selling CBD products. Indicating the burgeoning CBD industry is well on the way to mainstream acceptance.

What is next for CBD?

In February, former FDA Commissioner Scott Pruitt testified before the House Appropriations Committee and said that the FDA is initiating a rule making procedure with the goal of creating “an appropriately efficient and predictable regulatory framework for regulating CBD products.” The FDA will launch the process with a public hearing on CBD scheduled for May 31, 2019.

Further complexity struck when Pruitt unexpectedly announced his resignation, which took effect in early April. Pruitt has been replaced by Dr. Ned Sharpless, the former director of the National Cancer Institute. To date, it is unknown whether Sharpless intends to take a progressive stance toward CBD.

While delays occur at the federal level, states are shifting into action. Maine recently passed an emergency law governing CBD. The bill aligns the definition of hemp in Maine’s laws with the definition used in the Farm Bill. Meaning, as long as CBD is derived from hemp sources it is to be considered a food product, rather than medicine, and is cleared for use in Maine.

Ultimately, until the FDA creates a regulatory framework for CBD, it will remain illegal to add it to any food or drink products.

Learn more about the FDA Public Hearing on CBD here

Provide a public comment for the FDA on CBD here

]]>Currently, cannabis is one of the fastest-growing industries in the world, on the way to generating an estimated $146.4 billion by 2025 (according to Grand View Research). The industry is currently in its early-stages, which can mean that even modest investments now could greatly increase in value 5, 10 or 20 years down the road. As the industry finds its footing on a global scale new investment opportunities emerge every day.

Cannabis does carry lingering social stigmas that may keep investors away. Yet the plant itself is only one facet of a diverse industry that includes everything from “plant-touching” companies to “ancillary” businesses that support the cannabis industry. The following are some of the opportunities tribes and other private investor groups are exploring.

Creating Native-owned cultivation, manufacturing and/or retail operations

As the wave of legalization has slowly but steadily swept across the U.S., the unique sovereignty of Tribal nations has created potential for cannabis business opportunities in communities located in states where recreational-use and/or medicinal cannabis has been legalized.

Investments of this type can take many forms, whether focusing on cultivation, manufacturing, or retail, or the development of a vertically-integrated cannabis operation. This path gives the Tribe complete control over the business.

Leasing Tribal land to cannabis cultivators

In many areas of the country, there are far more aspiring cultivators than there are locations where they can grow. As a result, an emerging trend is the rise of cultivation facilities established by real estate groups or private businesses, which are then leased to cannabis cultivators.

A Tribe looking to invest in cannabis could identify open land or create a greenhouse/indoor cultivation facility that can then be leased to cultivators looking for space. This is an ideal option for Tribal leadership that may not want to take on the operational and legal complexities of cultivating cannabis, but can still benefit from an investment supporting the industry.

Private investment opportunities in cannabis

In recent years a number of leading cannabis companies have gone public, primarily on stock exchanges in Canada, and with a select handful of listed on the NYSE and NASDAQ. The best-in-class producers and retailers represent an intriguing option for private investors. Standard due diligence for purchasing shares of a public company apply equally to the cannabis industry.

Additionally, a number of ancillary companies, those serving the cannabis industry through technology, real estate, or other services, have also gone public and represent a potential investment option. A diverse portfolio that includes a balanced mix of “plant-touching” and “ancillary” businesses could be a low-risk entry into the cannabis industry.

Institutional investment opportunities

As a fast-growing global industry, many cannabis companies are actively searching for capital infusions to expand operations, fund research, launch new products, or enter new markets. There is heated competition for both private venture capital investments, and for institutional investments in newly public cannabis and cannabis-related companies.

Tribal leadership can consider establishing, or investing in, a private equity or venture capital firm and act as an incubator for emerging cannabis businesses. Establishing a fund in conjunction with the other options listed previously could produce a robust cannabis portfolio.

Considering hemp and CBD

While cannabis legalization gets headlines, related products like hemp and CBD are quietly establishing themselves as intriguing industries on their own. The path for growing industrial hemp has recently been opened by federal legislation and the uses of the product are endless. Similarly, CBD has launched a holistic medicine craze, is in great demand for a wide variety of products, and can be derived from non-cannabis sources.

If a Tribe chose to explore hemp and CBD as investment opportunity, they could follow any of the paths illustrated previously and swap out cannabis for hemp or CBD.

Finding the investment mix for your Tribe

The options provided above are just a sample of the opportunities available to investors. There are risks involved with any investment, and cannabis’ complex legal status creates further complications. As result, many traditional investors have been slow to move into the space. But for proactive investor groups, now is the time to get an early foothold in what will soon be a multi-billion dollar global industry.

]]>To help cannabis entrepreneurs and investors keep up with the fast pace of change in the cannabis industry we will be providing monthly summaries of the latest regulatory and legislative news to provide a snapshot of latest happenings while also highlighting matters of interest looking forward.

This month the focus is on prominent federal legislative activity (e.g. the SAFE Act and the STATES Act), state legalization measures (e.g. NJ, NY, IL, and others), and two bills in Colorado that have the potential to attract out-of-state investment to that market.

Changes in federal cannabis legislation

With control of the House of Representatives being transferred to the Democratic party, several bills that have the potential to profoundly impact the cannabis landscape have advanced in Congress. For example, the last week of March saw the House Financial Services Committee move forward the Secure And Fair Enforcement (SAFE) Banking Act to a full House vote, reportedly “within weeks.” Following the momentum of the House bill, U.S. Sens. Jeff Merkley (D-OR) and Cory Gardner (R-CO) have introduced the companion bill in the Senate.

The latest SAFE iteration addresses the cannabis banking crisis and includes amendments that offer protection to insurance companies and other financial services companies.

The banking issue is long-standing and predates even the implementation of recreational cannabis in the US. The lack of straight forward access to fundamental banking services for the cannabis industry creates a multitude of challenges, most notably the operational and financial difficulties of a multi-billion-dollar industry operating almost entirely in cash. This has obvious implications for public safety and potential diversion to the black market, among other concerns.

The inability to access banking services is often identified as a major hindrance to market entry for large and well-resourced corporations and removal of this barrier could herald a seismic shift in investment into the cannabis industry. At time of writing the House Bill had 152 cosponsors, including 12 Republicans, whereas the Senate bill has 20 co-sponsors.

Adding further momentum to the SAFE bill, last week Last week, Secretary Steve Mnuchin offered his support for a legislative fix for the banking issues facing the cannabis industry. “There is not a Treasury solution to this. There is not a regulator solution to this,” he said. “If this is something that Congress wants to look at on a bipartisan basis, I’d encourage you to do this.”

Another potentially substantial piece of legislation is the Strengthening the Tenth Amendment Through Entrusting States Act (STATES Act), which aims to reduce conflict between federal and state laws as they relate to cannabis. The STATES Act is a potential gamechanger for the cannabis industry, allowing legal certainty for companies seeking to operate in dozens of jurisdictions across the US.

Although this legislation stalled in December, it was reintroduced on April 4th, alongside other measures, which include:

- the Ending Federal Marijuana Prohibition Act that would effectively legalize marijuana at the federal level by removing it from the Controlled Substances Act.

- The Marijuana Justice Act of 2019

The extent to which these bills have bipartisan support may be crucial if they are move beyond the House.

Four steps forward and two steps back in state legalization efforts

It has been a mixed month in terms of advancing cannabis legalization measures at the state level. On the one hand, there has been progress in multiple states, such as Connecticut, Illinois, and New Hampshire. While on the other hand there was a couple of snags holding up the implementation of recreational markets in New Jersey and New York.

Recent adult-use cannabis legalization headlines include:

- The New Jersey cannabis legalization bill was pulled due to lack of support although Gov. Murphey (D) reportedly stated he remained committed to getting the bill passed.

- New York dropped cannabis legalization from its budget bill where it was viewed as more likely to pass, however, regulators remain optimistic of progress later in the year. The New York City Council also voted to ban cannabis testing for job applicants.

- A General Law Committee in the Connecticut Legislature approved a bill that would legalize an adult-use cannabis market in the state.

- In New Hampshire, the House Ways and Means Committee approved a vote on the floor on legislation that would legalize an adult-use cannabis market.

- A bill to legalize retail cannabis in Illinois was introduced and passed to a subcommittee for further consideration.

- Governor of Guam signed a bill legalizing cannabis, becoming the first US territory to do so.

Despite the hiccups outlined above, there is a clear trend towards legal cannabis across the US. Moreover, several states took steps towards expansion or liberalization of their medical cannabis markets. Certainly in the long term, the outlook is optimistic for the cannabis industry on a number of fronts.

Back to the future as Colorado looks to position itself as an investment hub for cannabis

When Colorado became the first state to implement an adult-us cannabis framework in 2014, out of state investment was restricted. This allowed the state to build upon its existing medical cannabis market.

The understandable caution has since been questioned, however, and a Bill offering more flexibility in investment passed both the Colorado House and Senate in 2018, only for then Gov. Hickenlooper to veto it. In 2019, a replacement Bill was introduced and has recently passed its third reading in the House unamended.

As an established market with mature regulations and market stability, Colorado has low-risk potential when compared to emerging markets in other states – although competition is likely to be strong, with ever-thinning margins as prices continue to drop in the state.

Out-of-state investors exploring options in Colorado may be interested in acquiring social consumption licenses in Denver, or seek opportunities for market expansion in the delivery segment of the market. If passed, HB19-1234 would allow licensed dispensaries to offer these services for the first time.

]]>