- A growing organization is a positive, but along with it usually comes increasingly complex financial accounting.

- Outsourcing provides businesses of all sizes with an opportunity to manage an array of issues — from staffing shortages or a lack of specific expertise to disorganized or unsecure financial records.

- Benefits of outsourcing include significant cost savings, direct access to specific accounting knowledge, the minimization of turnover, the ability to scale, access to tools and processes, and flexibility.

Many CEOs and business leaders are experiencing challenges in the aftermath of the COVID-19 pandemic, including changing customer trends, aggressive competition, emerging digital technologies, and the new normal of employee expectations for workplace flexibility.

These uncertain economic forces and cultural shifts are putting increased pressure on staffing for organizations of all sizes – especially fast-growing ones. While these difficulties are difficult to overcome, they are also an opportunity to change the “status quo” and level-up back-office performance.

For leaders navigating the uncertain tailwinds of the pandemic and planning to enter a new era of growth, outsourcing represents a powerful opportunity to address any staffing issues or business challenges. It empowers you to access specialized insight on a temporary basis, create value ahead of a major transaction, manage overhead costs, and modernize and revitalize business processes.

A recent study showed that 59% of all businesses utilize outsourced resources and that accounting is the most commonly outsourced function. So, how do you know if outsourcing your accounting function is right for your organization?

In this article we’ll look at five indicators that this strategy might be right for you and detail the key benefits to outsourcing or augmenting your accounting function.

Five signs your business may benefit from outsourced accounting

Here are some questions you should ask yourself to determine if your organization would benefit from outsourced accounting services:

- Is your business growing rapidly?

If you’re experiencing a significant influx of revenue, first off, great work! Your business model is proving out and you’re on the fast-track to success. But what is happening to your expenses, profitability and working capital? Depending on your answer it could mean that your accounting needs are evolving, the risks of a breakdown are higher, and overall, there is simply more at stake. It may be time to confirm that your current in-house team is qualified and staffed appropriately to handle these new responsibilities.

- Are you struggling to keep up with your accounts receivable or payroll?

One way to get a firm answer to whether your team is understaffed is if you’re missing key deadlines or struggling to get timely collection of cash from your accounts receivable. The inability to collect and follow-up on AR is essential to funding current and future growth and is directly connected to meeting your payroll commitments – one of the largest expenses of any business. If anything falls behind, you can find yourself in a difficult position if you do not have the ability to access cash or financing.

- Are your financial records organized and producing usable data?

Your accounting function does more than compliance, it should help guide your organization’s financial hygiene. Organized financials tell a clear story of earnings, spending, and investment, so you can make informed decisions. An over-worked or inexperienced accounting team will be working furiously to keep up with compliance and may not have the capacity, or necessary experience, to provide guidance on your financial scorecard to accrete value to the organization.

- Do your accounting needs fluctuate significantly throughout the year?

If your business experiences big shifts in labor productivity based on the calendar year and your taxes filings are late with significant overages from the tax preparers, or your audits have a significant number of adjustments, that may mean your accounting team lacks capability. Striking the right balance between hiring quality talent and the speed of bringing new hires up to date with company procedures can be a challenge. Outsourcing your team can deliver the resources you need, when you need them, and limit costs during the slower periods.

- Are you concerned about financial security and checks and balances?

If your internal accounting team is one or two individuals, you may be open to hidden risks. An independent team can provide the checks-and-balances that help mitigate the risk of fraud and asset misappropriation.

If you answered yes to any of these questions, you should consider outsourcing part or all of your accounting function. With an outsourced accounting team, you gain immediate access to trained, knowledgeable staff with the knowledge you need in technical accounting. The right outsourced resources can help your business grow faster and run more smoothly — often at a lower price than building an internal accounting department.

Benefits of outsourced accounting services

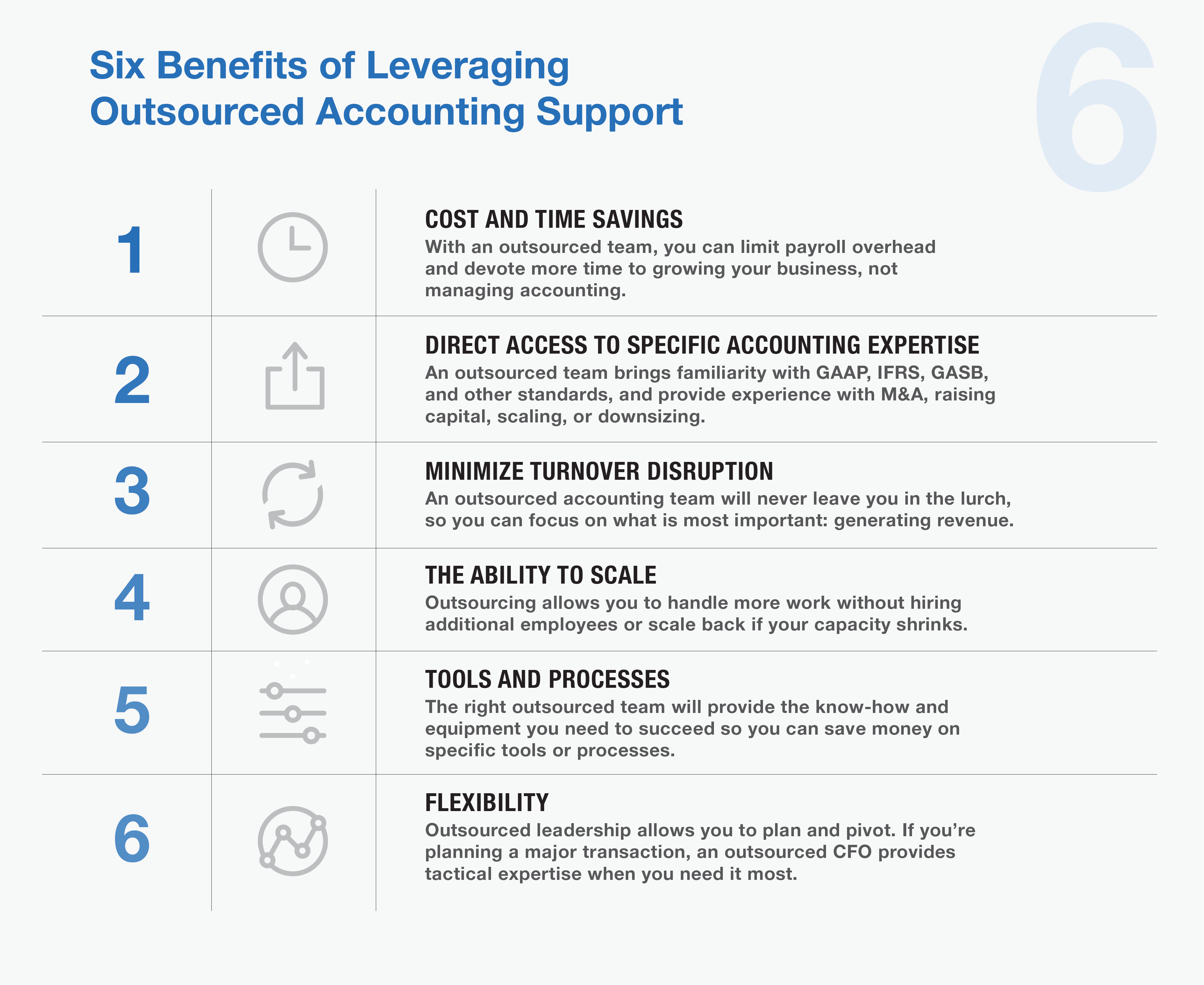

1.Cost and time savings

Maintaining full-time employees can be costly — and for most organizations, labor costs are some of the highest expenses. By relying on an outsourced team, you can devote your time to growing your business and spend less time managing accounting.

- Direct access to specific accounting expertise

Every company is different, which means every company’s needs are different. By outsourcing, you have access to the service you need when you need it. An outsourced team will bring familiarity with an array of accounting and reporting standards, including GAAP, IFRS, GASB, etc. Plus, they can provide specific experience with M&A transactions, raising capital, scaling, or downsizing operations.

- Minimize turnover disruption

In a smaller organization, each employee is vital to the business’s success. When you lose one, the disruption left in their wake can provide additional challenges. An outsourced accounting team will never leave you in the lurch, so you can focus on what is most important: generating revenue.

- The ability to scale

If your organization has grown quickly, you may experience growing pains when your fortunes suddenly shift. In boom times, you may need to hire more staff to meet demand. But that also means you may find yourself laying off employees in a downturn. Outsourcing allows you to handle more work without hiring additional employees or scale back if your capacity shrinks.

- Tools and processes

No matter what your organization’s size, you should always try to keep your overhead costs minimal. By outsourcing, you can save money on specific tools or processes you might otherwise need to function. The right outsourced team will provide the know-how and equipment you need to succeed.

- Flexibility

By outsourcing certain jobs, you can plan — and pivot, as needed — depending on your organization’s needs. This is especially relevant in the case of needing specialized guidance. If you’re planning a major transaction or other market move, an outsourced CFO can provide tactical expertise when and where you need it.

MGO can help

As your organization grows, your financial accounting needs become increasingly complex. Because your in-house accountants may be limited to handle the basics, outsourcing to professional teams with specialized knowledge and experience can provide precisely the kind of service you require — and give you the time you need to focus on the organization’s other needs.

MGO has a robust outsourced accounting team staffed by CPAs with diverse industry background and technical specialties. We’ll provide the right-size solution to your organization’s needs. Areas we support include day-to-day accounting tasks, complex financial systems projects, regulatory compliance demands, and support for M&A deals, raising capital, and other major transactions.

Whether you’re interested in simply augmenting your team with additional financial knowledge, or undertaking a complete accounting transformation, we can help you with the people, processes, and technology you need to move your business forward.

To explore your options and start along the path to organizational change, contact us.

]]>The credit was permanently extended with the passing of the Protecting Americans from Tax Hikes Act of 2015, a welcome reprieve from the credit’s history, where it often expired only to later be temporarily extended, sometimes retroactively. Now that the credit is permanent and has been expanded to benefit certain small businesses and startups, government contractors can incorporate the credit into their tax planning discussions.

Federal tax changes boost R&D

Recently, the value of the credit was enhanced by the Tax Cuts and Jobs Act of 2017 (TCJA), as reflected in BDO’s Tax Outlook Survey.

By reducing the maximum corporate tax rate from 35 to 21 percent, the TCJA effectively increased the credit’s value by 22 percent, from 65 percent when the maximum corporate rate was 35 percent, to 79 percent today.

In addition, by eliminating the corporate Alternative Minimum Tax (AMT), the TCJA affords AMT taxpayers, who generally couldn’t use the credit against their AMT, the opportunity to use their credits down to 25 percent of the amount their net regular tax liability exceeds $25,000. Changes to the AMT regime for individual taxpayers could also increase the amount of benefit allowed to owners of pass-through entities.

Not all contracts limit eligibility

A common misconception in the government contracting industry is that activities don’t qualify for the credit if the government or a third-party finances a contractor’s R&D activities. This isn’t always true: if the contract with the government or other third-party provides that the contractor bears the economic risk if the work fails and that the contractor retains substantial rights in the work’s results, the contractor’s activities can still qualify even if reimbursed by the government or another unrelated third-party.

Don’t overlook software

More good news for government contractors arrived with the Treasury’s final regulations in late 2016. These regulations narrowed the definition of “internal use software” (IUS) activities, which generally must meet a higher standard to qualify. Now, the development of more software, including software to provide services, can qualify more easily, without meeting the higher IUS standards.

MGO’s take

If government contractors pay employees or contractors who are software developers, process engineers, energy consultants, mechanical designers, or other technical personnel, they’re likely to be eligible for the credit. The same is true for government contractors who are trying to develop or improve cybersecurity solutions, aerospace equipment, defense components, cloud computing solutions, and the like.

With the recent taxpayer-friendly developments around the credit and U.S. taxes in general, government contractors should consider how they are impacted and whether they’re missing out on a significant tax-savings opportunity.

This article originally appeared in BDO USA, LLP’s “Government Contracting” newsletter (Summer 2018). Copyright © 2018 BDO USA, LLP. All rights reserved. www.bdo.com

]]>1. The corporate tax rate was permanently reduced from 35 percent to 21 percent.

The top corporate tax rate has been permanently reduced from 35 percent to a flat rate of 21 percent, beginning in 2018. Unlike all other provisions in the new law, including tax breaks for individuals, the new corporate tax rate provision does not expire.

2. There’s a tax break for owners of pass-through entities.

The new law provides owners of pass-through businesses — which include individuals, estates, and trusts — with a deduction of up to 20 percent of their domestic qualified business income, whether it is attributable to income earned through an S corporation, partnership, sole proprietorship, or disregarded entity. Without the new deduction, taxpayers would pay 2018 taxes on their share of qualified earnings at rates up to 37 percent. With the new 20 percent deduction, the tax rate on such income could be as low as 29.6 percent. It should again be noted that certain service industries are excluded from the preferential rate, unless taxable income is below $207,500 (for single filers) and $415,000 (for joint filers), under which the benefit of the deduction is phased out.

3. There might be huge tax benefits to changing your company’s current choice of entity.

Taxpayers should consider evaluating the choice of entity used to operate their businesses. The 21 percent reduced corporate tax rate may increase the popularity of corporations. However, factors such as the new 20 percent deduction for pass-through income, expected use of after-tax cash earnings, and potential exit values will significantly complicate these analyses. The potential after-tax cash benefits ultimately realized by owners could make choice-of-entity determinations one of the most important decisions taxpayers will now make.

4. There have been significant changes to the international tax system.

In connection with these changes, some U.S. shareholders who own stock in certain foreign corporations will have to pay a one-time “transition tax” on their share of accumulated overseas earnings. Other changes include a “participation exemption,” which is a 100 percent dividend-received deduction that permits certain domestic C corporations to receive dividends from their foreign subsidiaries without being taxed on such dividends when certain conditions are satisfied. There is also a new requirement that certain U.S. shareholders of controlled foreign corporations (CFCs) include in income their share of the “global intangible low-taxed income” of such CFCs. Finally, there are new measures to deter base erosion and promote U.S. production.

5. The corporate AMT and DPAD are dead, but Research Tax Credits live on.

The law repeals the Section 199 Domestic Production Activities Deduction (DPAD) and the corporate Alternative Minimum Tax (AMT) for tax years beginning after 2017. The Research Tax Credit was retained and is now more valuable given the reduction of the corporate tax rate from 35 percent to 21 percent.

6. They’ve scrapped NOL carrybacks and limited the use of carryforwards.

Previously, businesses were able to offset current taxable income by claiming net operating losses (NOLs), generally eligible for a two-year carryback and 20-year carryforward. Now NOLs for tax years ending after 2017 cannot be carried back, but can be indefinitely carried forward. In addition, NOLs for tax years beginning in 2018 will be subject to an 80 percent limitation. Companies will have to track their NOLs in different buckets and consider cost-recovery strategy on depreciable assets in applying the 80 percent limitation.

7. Tax reform’s impact on accounting methods may change when revenue is recognized, but new provisions could also lead to temporary and permanent tax benefits.

Under the new law, accrual basis taxpayers must now recognize income no later than the taxable year in which such income is taken into account as revenue in an applicable financial statement.

However, new provisions also provide favorable methods of accounting that were not previously available. That, coupled with the reduction in tax rates, creates a favorable and unique environment for filing accounting method changes.

There are many method changes still available for the 2017 tax year. Taxpayers should evaluate current accounting methods to identify any actionable opportunities to accelerate deductions and defer income for the 2017 tax year, which could result in significant tax savings.

8. There are new rules for bonus depreciation and full expensing on new and used property.

The new tax law allows a 100 percent first-year deduction — up from 50 percent — for the adjusted basis of qualifying assets placed in service after Sept. 27, 2017, and before Jan. 1, 2023, with a gradual phase down in subsequent years before sunsetting after 2026. The definition of qualifying property was also expanded to include used property purchased in an arm’s-length transaction. Businesses should pay close attention to any qualifying asset acquisitions made during the fourth quarter of 2017, as the full expensing can be taken on the 2017 return if the property was acquired and placed in service after Sept. 27, 2017.

Additionally, under new tax law, taxpayers may now deduct up to $1 million under Section 179 for properties placed in service beginning in 2018 — double the previous allowable amount. The phase-out threshold is increased to $2.5 million and will be indexed for inflation in future years and the types of qualifying property has been expanded.

9. The availability of the cash method of accounting expanded for small businesses.

Beginning in 2018, the average annual gross receipts threshold for businesses to use the cash method increases from $5 million to $25 million. Additionally, small businesses who meet the $25 million gross receipts threshold are not required to account for inventories and are exempt from the uniform capitalization rules. The $25 million is indexed for inflation for tax years beginning after 2018.

10. Now is the time to assess total rewards strategies.

Tax reform significantly impacts various components of an employer’s total compensation program — namely the expansion of the $1 million deduction cap on pay to covered employees; disallowed deductions for transportation fringe benefits provided to employees; income inclusion for employer-paid moving expenses; further deduction limitations on certain meal and entertainment expenses; and a two-year tax credit for employer-paid family and medical leave programs. As the IRS releases guidance, employers must immediately modify their payroll systems to reflect tax reform changes impacting individual taxpayers.

For more information about the impact of tax reform on the Government Contracting industry, please reach out to us.

]]>- Insufficient outreach to vendors

- Lowering of bonding requirements

- Burdensome administrative requirements

- Insufficient segregation of procurement approval and receiving duties

- Lack of cross-department evaluation of vendor proposals

- Inconsistent management and designated authority levels

- Organizations are unaware of procurement process times – from start of requisition until vendors are paid

- Procurement activities are not aligned with overall organizational activities

- Too many sign offs/approvals

If any of these issues sound familiar, or your organization has not reviewed its procurement function in a while, you run the risk that your procurement strategies are inconsistent with organizational needs, which can result in paying higher prices for the goods and services required to run your agency, insufficient number of competitive bids, or worse, violating your grant or service agreements.

IntelliBridge Partners has the expertise to improve the procure to pay cycle through business process reviews, risk assessments, and performance audits. If you would like help with your procurement department, please contact Greg Matayoshi at gmatayoshi@intellibridgepartners.com.

]]>Many cheered the passage of the 2018 Farm Bill, which descheduled industrial hemp and its derivatives (including CBD). But that was just the start of a much more complicated regulatory story that continues to have a major impact on entrepreneurs, investors, and advocates and patients who rely on CBD.

CBD and the 2018 Farm Bill

When President Trump signed the 2018 Farm Bill into law one of the key changes affecting the cannabis industry was the separation of “hemp” and “marijuana.” Before the Farm Bill, any incarnation of the cannabis plant and its byproducts were lumped into a single category and considered a Schedule 1 drug. Key language in Section 1103 of the Farm Bill defines hemp as:

“the plant Cannabis sativa L. and any part of that plant, including the seeds thereof and all derivatives, extracts, cannabinoids, isomers, acids, salts, and salts of isomers, whether growing or not with a delta-9 tetrahydrocannabinol concentration of not more than 0.3 percent on a dry weight basis.”

In short, the Farm Bill descheduled industrial hemp and its byproducts as long as it stayed under the threshold of less than 0.3 percent THC. CBD is derived from the cannabis plant, whether there are significant levels of THC or not. CBD industry advocates have interpreted the language “all derivatives, extracts, cannabinoids, isomers, acids, salts, and salts of isomers” as descheduling CBD when industrial hemp is the source. And they are “mostly” correct in this interpretation. Unfortunately, there are other federal agencies in play.

CBD and the FDA

United States Department of Agriculture (USDA) enacted the 2018 Farm Bill in their position overseeing laws related to the cultivation of industrial hemp. The United States Food and Drug Administration (FDA) oversees medicine and food additives. CBD has emerged as a “wonder drug” with a growing list of potential benefits and now appears as an additive in a wide range of consumer products. In addition, the FDA approved Epidiolex, the first CBD-derived drug, in 2018.

All of this has culminated in CBD being a priority of the FDA, so much so, that just a week after the Farm Bill was signed into law, the FDA issued a press release clarifying and asserting their regulatory control over all cannabis-derived compounds.

“We treat products containing cannabis or cannabis-derived compounds as we do any other FDA-regulated products — meaning they’re subject to the same authorities and requirements as FDA-regulated products containing any other substance. This is true regardless of the source of the substance, including whether the substance is derived from a plant that is classified as hemp under the Agriculture Improvement Act.”

Concurrent with the Farm Bill and the press release regarding CBD, the FDA also issued three Generally Regarded as Safe (GRAS) notices for hemp by-products: hulled hemp seeds, hemp protein powder, and hemp seed oil. Clearly demonstrating that (some) hemp products have been descheduled and cleared for use by the FDA.

The FDA’s policy is different toward CBD for two key reasons. Firstly, CBD products are largely marketed with a wide variety of therapeutic claims. In their press release the FDA notes:

“The FDA requires a cannabis product (hemp-derived or otherwise) that is marketed with a claim of therapeutic benefit, or with any other disease claim, to be approved by the FDA for its intended use before it may be introduced into interstate commerce.”

Secondly, the FDA’s approval of CBD-based drug Epidiolex, put CBD and THC into the category of “active ingredients in FDA-approved drugs.” Under the Federal Food, Drug, and Cosmetic Act (FD&C Act) it is “illegal to introduce drug ingredients like these into the food supply, or to market them as dietary supplements.”

In short, the FDA does not distinguish between CBD derived from hemp or “marijuana,” and until the agency approves CBD and establishes a regulatory framework, adding CBD to food and beverages is illegal.

Has the regulation of CBD slowed businesses?

While early CBD research has shown promise as a treatment for conditions like epilepsy and anxiety, as a consumer product it is unproven and has been largely unregulated until recently. In the absence of labeling standards and regulated dosage guidelines, consumers often have little understanding of what they are buying and its potential effects.

All of this uncertainty has earned greater regulatory attention for CBD. There have been reports of crackdowns on bakeries, restaurants and retailers selling CBD in California, New York, Maine and Ohio, just to name a few. This regulatory response has shocked and angered a number of hemp producers and CBD retailers who have invested millions into business ventures that they feel only supply the public with products that help manage health concerns.

Despite the confusing legality, the CBD industry appears to be moving full-steam ahead. In recent months, national retailers as diverse as Walgreens, DSW and Barney’s New York have announced plans (or have already begun) selling CBD products. Indicating the burgeoning CBD industry is well on the way to mainstream acceptance.

What is next for CBD?

In February, former FDA Commissioner Scott Pruitt testified before the House Appropriations Committee and said that the FDA is initiating a rule making procedure with the goal of creating “an appropriately efficient and predictable regulatory framework for regulating CBD products.” The FDA will launch the process with a public hearing on CBD scheduled for May 31, 2019.

Further complexity struck when Pruitt unexpectedly announced his resignation, which took effect in early April. Pruitt has been replaced by Dr. Ned Sharpless, the former director of the National Cancer Institute. To date, it is unknown whether Sharpless intends to take a progressive stance toward CBD.

While delays occur at the federal level, states are shifting into action. Maine recently passed an emergency law governing CBD. The bill aligns the definition of hemp in Maine’s laws with the definition used in the Farm Bill. Meaning, as long as CBD is derived from hemp sources it is to be considered a food product, rather than medicine, and is cleared for use in Maine.

Ultimately, until the FDA creates a regulatory framework for CBD, it will remain illegal to add it to any food or drink products.

Learn more about the FDA Public Hearing on CBD here

Provide a public comment for the FDA on CBD here

]]>